Renewables after COP-21 A global perspective. Cédric Philibert Renewable Energy Division International Energy Agency

|

|

|

- Gwenda Chandler

- 5 years ago

- Views:

Transcription

1 Renewables after COP-21 A global perspective Cédric Philibert Renewable Energy Division International Energy Agency Energy Change Institute, Canberra, 5 May 2016

2 COP21 a historic milestone Universal agreement on: GHG emissions peak asap Stay below 2 C temperature increase, get close to 1.5 Reach carbon-neutrality in second half of this century Renewables around COP21 Renewables explicitly referred to in around 100 pledges Record renewable capacity additions in 2014 and 2015 Lowest-ever announced wind and solar prices Downturn in prices for all fossil fuels Oil & gas set to face a second year of falling upstream investment in 2016 Coal prices remain at rock-bottom as demand slows in China

3 GW Renewables set to dominate additions in power systems World net additions to power capacity Fossil fuels Nuclear Hydropower Non-hydro renewables Analysis from the IEA Medium-Term Renewable Energy Market Report 2015 and the New Policies Scenario of the World Energy Outlook The share of renewables in net additions to power capacity continues to rise with non-hydro sources reaching nearly half of the total

4 Deployment shifting to emerging markets and developing countries Shares of net additional renewable capacity, India 9% Brazil 5% Africa 4% Rest of non-oecd 9% EU-28 13% United States 9% Japan 5% Rest of OECD 8% China 38% As the OECD slows, non-oecd countries account for two-thirds of renewable growth, driven by fast-growing power demand, diversification needs and local pollution concerns

5 2010 = 100 Innovation and scale-up are driving costs down 120 Indexed generation costs Onshore wind Solar PV - residential Solar PV - utility scale High levels of incentives are no longer necessary for solar PV and onshore wind, but their economic attractiveness still depends on regulatory framework and market design

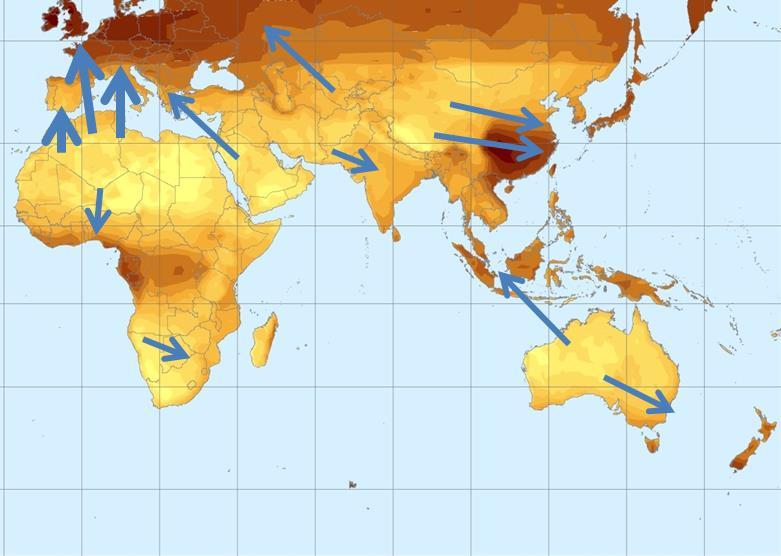

6 Wind and Solar PV prices declining sharply Recent announced long-term contract prices for new renewable power to be commissioned over Onshore wind Utility-scale solar PV Morocco USD 30-35/MWh Germany USD /MWh Germany USD 87 /MWh United States USD 47/MWh Canada USD 66/MWh Turkey USD 73/MWh United States USD 65-70/MWh China USD 80 91/MWh Brazil USD 81/MWh India USD 67-94/MWh Peru USD 38/MWh Mexico USD 35+5/MWh Jordan USD 61-77/MWh Peru USD 49/MWh United Arab Emirates USD 58/MWh Brazil USD 49/MWh Chile USD 65-68/MWh Uruguay USD 90/MWh South Africa USD 51/MWh South Africa USD 65/MWh Egypt USD 41-50/MWh Australia USD 69/MWh This map is without prejudice to the status or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area Note: Values reported in nominal USD includes preferred bidders, PPAs or FITs. US values are calculated excluding tax credits. Delivery date and costs may be different than those reported at the time of the auction. Best results occur where price competition, long-term contracts and good resource availability are combined

7 High capex: WACC matters Impact of cost of capital on the levelised cost of solar PV (assuming same system costs and same resource ) 2X X Dubai Central Africa Market and regulatory risks can increase weighted average cost of capital and undermine competitiveness of PV and Wind power

8 Gt Greater efforts are still needed to reach a 2 C pathway Trend post-cop Gt Energy efficiency Fuel & technology switching in end-uses Renewables Nuclear C Scenario CCS Other Source: World Energy Outlook 2015 In a 2 C Scenario, energy efficiency and renewables, notably solar and wind, deliver the bulk of GHG emission reductions OECD/IEA 2015

9 Global power mix needs a shift reversal Source: Energy Technology Perspectives DS 2DS hi-ren Generation today: Generation 2DS 2050: Fossil fuels: 68% Renewables: 65-79% Renewables: 20% Fossil fuels: 20-12%

10 Where CST fits in the picture 1. Generate dispatchable electricity 2. Provide high-temperature industrial process heat 3. Manufacture energy vectors as «solar fuels»

11 Solar Electricity PV takes all light PV almost everywhere Scalable from kw to GW Variable and mid-day Peak & mid-peak Smart grids STE takes direct light STE only in semi-arid countries Mostly for utilities Firm, dispatchable Peak to base-load }{ backup storage HVDC lines for transport Firm & flexible CSP capacities can help integrate more PV

12 Integrating large shares of PV is challenging California: - expected evolution of the net load of a typical spring day Flexibility of other power system components Grids Generation Source: California ISO, expected evolution of the value of PV and CST Storage Demand Side Source: Jorgenson, Denholm & Mehos, 2014

13 Complementary roles of PV and STE Thanks to thermal storage, STE is generated on demand when the sun sets while demand often peaks and value of electricity increases OECD/IEA 2014

14 Global generation in TWh Share of total electricity generation New roadmap vision for solar electricity % % % % % % Solar PV Solar CSP Share of PV Share of PV+STE 0% Together, PV and STE could become the largest source of electricity worldwide before 2050 OECD/IEA 2014

15 Future possible interconnections Source: Adapted from STE Roadmap 2010

Utility-scale PV")

PV + wind (e.g. South Africa)")

16 Power from CST compares with Distributed PV + battery (e.g. Germany) Utility-scale PV + pumped-hydro storage (e.g. Chile) PV + wind (e.g. South Africa)

Lesedi,")

(e.")

17 or PV + CST! Tomorrow? (e.g. ARPA-E s Focus programme, USA) Lesedi, Jasper and Redstone Power Projects. Source: SolarReserve Today (almost) (e.g. South Africa)

18 Cost matters, but value too! Ten years ago, LCOE of CST power was half that of PV Now, the reverse holds true CST power will not beat PV on costs, but compares with PV + storage Time-of-delivery payments reflect the true value of storage CST Power was born in the 1980s in California thanks to time-of-delivery energy and capacity payments CST is being developed in South Africa thanks to a x2.7 multiplier of Base Price during 5 hours a day

19 Renewable electricity generation is more than a hydropower story Generation (TWh) % 10% Renewable generation by technology ( ) Share of renewables in overall electricity generation Share of non-hydro renewables in overall RE generation 22% 25% 26% 37% Hydropower Bioenergy Onshore wind Offshore wind Solar PV Geothermal STE Ocean Natural gas 2013 Nuclear 2013 Share of non-hydropower in renewable electricity generation is expected to increase significantly OECD/IEA 2015

20 Share of renewables in sector demand Persistent challenges slow growth in heat and transport Historical and forecast share of renewables in electricity, heat and transport sectors % 25% 20% Forecast Renewable electricity 15% Renewable heat 10% 5% 0% Biofuels in road transport Growth of renewable electricity generation is increasing, while renewable heat and transport are falling behind. OECD/IEA 2015

21 2050 Low-Carbon Economy Roadmap 80% GHG decarbonisation in 2050 (cf global 2 C objective) 100% 100% 80% Power Sector Current policy 80% 60% Residential & Tertiary 60% 40% Industry 40% Transport 20% 20% Non CO 2 Agriculture 0% Non CO 2 Other Sectors 0% Source: European Commission 2050 Roadmap,

22 Industry next to power, mostly heat Global CO2 emissions Germany (final energy consumption)

Could play a transitory role")

23 Electric heat technologies Least efficient: resistances (Joule) Could play a transitory role in parallel with existing fossil fuel boilers Industrial heat pumps Commercially available to 100 C output Reaching 140 C output would double potential Induction heating and smelting Microwaves (food, rubber, plastics) Foucaut currents, electric ovens, electric arcs, plasma torches, etc Photo Credit : SAIREM

")

24 Solar heat for industries Solar air drying of coffee beans (Columbia) Solar water heaters in a service area (Austria) Source: AEE INTEC. Experimental mid-size industrial solar oven (France) Source: SolarWall. Deepak Gadhia Cooking with Scheffler dishes (India)

25 Oil men turn to solar to save gas Mirrah, Oman, 2017: 1 GWth for EOR Glasspoint technology

26 Solar fuels From hydrocarbon or water Source: PSI/ETH-Zürich. H 2 can first be blended with natural gas Can be converted into various energy carriers: methane, methanol, DME, ammonia Other options based on redox cycles, flow batteries OECD/IEA, 2011

, biomass plants or")

27 Various CST paths to carbon-free ammonia, steel, cement Solar thermal electro pr Source: Licht et al. Including process CO2 emissions Also to support CO2 capture from coal plants (ARENA), biomass plants or perhaps from air

28 Interconnections reconsidered

29 Subsidies to fossil fuels dominate over carbon pricing Energy-related CO 2 emissions, 2014, shares of coverage by CO 2 prices or subsidies

30 A decisive moment for the future of renewables Paris Agreement accelerates virtuous circle already started before COP Increasingly affordable renewables are set to dominate the growing power systems of the world Sharp cost reductions of RE change policy and market design needs From providing financial support to creating a framework for investment Long-term remuneration crucial to attract financing Innovation must extend from renewable technology to system integration While variability of renewables is a challenge energy systems can learn to adapt to, variability of policies poses a far greater risk Low fossil fuel prices are a good time window to introduce robust longterm carbon pricing and make progress in phasing out fossil fuel subsidies

31

32 Net load (GW) Integrating larger shares of VRE: the balancing challenge Higher uncertainty Larger and more pronounced changes Illustration of Residual power demand at different VRE shares Larger ramps at high shares 0.0% 2.5% 5.0% 10.0% 20.0% Lower minimum Hours Note: Load data and wind data from Germany 10 to 16 November 2010, wind generation scaled, actual share 7.3%. Scaling may overestimate the impact of variability; combined effect of wind and solar may be lower, illustration only.

33 Net load (GW) Integrating larger shares of VRE: the utilisation challenge Netload implies different utilisation for non-vre system Maximum remains high: Scarcity % 2.5% 5.0% 10.0% 20.0% Changed utilisation pattern Lower minimum: Abundance Hours Note: Load data and wind data from Germany 10 to 16 November 2010, wind generation scaled, actual share 7.3%. Scaling may overestimate the impact of variability; combined effect of wind and solar may be lower, illustration only. Peak Baseload Midmerit Midmerit Baseload Peak

34 System-friendly VRE deployment Complementarity of wind and solar generation in Germany System-friendly design of wind turbines reduces variability Source: adapted from Agora, 2013

35 Importance of grids EUROPE Continental Dimension BRAZIL km km Interconnected continental-scale balancing areas smoothen out variability and allow to exploit complementarities

36 120 kw Commercial 3 kw Residential.13 kw Residential Self-use and self-sufficiency Comparison of self-use and self-sufficiency shares by system size and customer (A temperate country example) Generation 100% self-use Consumption 4% self-sufficiency Generation Consumption 37% self-use 35% self-sufficiency Generation 94% self-use Consumption 29% self-sufficiency Annual kwh Consumption from the grid Generation surplus Prosumed

37 Self-consumption with DSI and small storage Self-consumption: 40% With DSI: 50% with DSI and small storage: 60% In most places, the hard limit to solar penetration in power system is the seasonal imbalance, as interseasonal storage is usually expensive

38 Grid cost issues with selfconsumption and net-metering Depending on the time match demand vs. sunshine, grid costs may be reduced or increased T&D costs 30-50% of retail costs, but only 0-15% recovered through fixed payments for efficiency/equity reasons Self-consumers pay less but still benefit from the grid Net-energy metering only increases the size of the issue Recovering grid costs over lesser sales may require tariff increase, but this leads to cross-subsidies, and further incentivizes selfconsumption Load-defection will not (likely) lead to grid defection, but financing of grid development is a real issue. Grids have high value to integrate large shares of variable renewables

39 Regional power mixes differ by 2050 in 2DS hi-ren Source: Energy Technology Perspectives 2014 Differences in resources but also in load shapes lead to quite different technology mixes

CST after COP-21 A global perspective. Cédric Philibert Renewable Energy Division International Energy Agency

CST after COP-21 A global perspective Cédric Philibert Renewable Energy Division International Energy Agency ASTRI Workshop, Melbourne, 2 May 2016 COP21 a historic milestone Universal agreement on: GHG

CST after COP-21 A global perspective Cédric Philibert Renewable Energy Division International Energy Agency ASTRI Workshop, Melbourne, 2 May 2016 COP21 a historic milestone Universal agreement on: GHG

Renewables after COP-21 A global perspective. Dr. Fatih Birol Executive Director International Energy Agency

Renewables after COP-21 A global perspective Dr. Fatih Birol Executive Director International Energy Agency 17 th Symposium, Syndicat des Énergies Renouvelables, Unesco, Paris, 4 February 2016 The start

Renewables after COP-21 A global perspective Dr. Fatih Birol Executive Director International Energy Agency 17 th Symposium, Syndicat des Énergies Renouvelables, Unesco, Paris, 4 February 2016 The start

Integration of wind and solar in power systems. Cédric Philibert Renewable Energy Division International Energy Agency

Integration of wind and solar in power systems Cédric Philibert Renewable Energy Division International Energy Agency Electricity Security Workshop, Bangkok, 21 January 2016, Outline 1. Competitive solar

Integration of wind and solar in power systems Cédric Philibert Renewable Energy Division International Energy Agency Electricity Security Workshop, Bangkok, 21 January 2016, Outline 1. Competitive solar

Economics of solar PV

Economics of solar PV after COP21 Paolo Frankl Head, Renewable Energy Division Energy Agency IEA PVPS workshop, EUPVSEC, Munich, 20 June 2016 2015 The start of a new energy era? Universal agreement from

Economics of solar PV after COP21 Paolo Frankl Head, Renewable Energy Division Energy Agency IEA PVPS workshop, EUPVSEC, Munich, 20 June 2016 2015 The start of a new energy era? Universal agreement from

Renewables for Africa and for the World

RENEWABLE ENERGY Renewables for Africa and for the World Paul Simons Deputy Executive Director International Energy Agency SAIREC, Cape Town, 5 October 2015 Profound changes underway in energy markets

RENEWABLE ENERGY Renewables for Africa and for the World Paul Simons Deputy Executive Director International Energy Agency SAIREC, Cape Town, 5 October 2015 Profound changes underway in energy markets

Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions and global economic growth Oil prices have fallen pre

Keisuke Sadamori Director of Energy Markets and Security, IEA The 88th IEEJ Energy Seminar, 5th October 215 Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions

Keisuke Sadamori Director of Energy Markets and Security, IEA The 88th IEEJ Energy Seminar, 5th October 215 Profound changes underway in energy markets Signs of decoupling of energy-related CO 2 emissions

Medium and long-term perspectives for PV. Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency

Medium and long-term perspectives for PV Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency Solar Power Summit, Brussels, 7-8 March 2017 Annual additions (GW) Cumulative

Medium and long-term perspectives for PV Dr. Paolo Frankl Division Head Renewable Energy Division International Energy Agency Solar Power Summit, Brussels, 7-8 March 2017 Annual additions (GW) Cumulative

Advanced Renewable Incentive Schemes. Simon Müller Senior Analyst System Integration of Renewables International Energy Agency

Advanced Renewable Incentive Schemes Simon Müller Senior Analyst System Integration of Renewables International Energy Agency Berlin Energy Transition Dialogue, 17 March 2016 The start of a new energy

Advanced Renewable Incentive Schemes Simon Müller Senior Analyst System Integration of Renewables International Energy Agency Berlin Energy Transition Dialogue, 17 March 2016 The start of a new energy

Delivering on the clean energy agenda: prospects and the role for policy

Delivering on the clean energy agenda: prospects and the role for policy 6th Asian Ministerial Energy Roundtable 9 November 2015 Keisuke Sadamori Director, Energy Markets and Security Climate pledges shift

Delivering on the clean energy agenda: prospects and the role for policy 6th Asian Ministerial Energy Roundtable 9 November 2015 Keisuke Sadamori Director, Energy Markets and Security Climate pledges shift

Roadmap for Solar PV. Michael Waldron Renewable Energy Division International Energy Agency

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

Medium Term Renewable Energy Market Report Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September Keisuke Sadamori Director

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September 2015 Keisuke Sadamori Director OECD/IEA - 2013 Slide 2 Demand/Supply Balance until 4Q16* mb/d

The global energy outlook to 2025 and the megatrends impacting energy markets beyond that Sydney, 16 September 2015 Keisuke Sadamori Director OECD/IEA - 2013 Slide 2 Demand/Supply Balance until 4Q16* mb/d

Medium Term Renewable Energy Market Report 2013

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

Solar process heat: the IEA scenarios Cédric Philibert Renewable Energy Division International Energy Agency

Solar process heat: the IEA scenarios Cédric Philibert Renewable Energy Division International Energy Agency SHIP 2015 Montpellier 15 September 2015 OECD/IEA 2015 TWh Strong momentum for renewable electricity

Solar process heat: the IEA scenarios Cédric Philibert Renewable Energy Division International Energy Agency SHIP 2015 Montpellier 15 September 2015 OECD/IEA 2015 TWh Strong momentum for renewable electricity

Medium Term Renewable Energy Market Report 2016

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency Atoms for the Future, Paris, 22 October 2013 Positive mid-term outlook

Renewables: challenges and opportunities for the power grid Cédric PHILIBERT Renewable Energy Division International Energy Agency Atoms for the Future, Paris, 22 October 2013 Positive mid-term outlook

Energy Technology Perspectives for a Clean Energy Future

Energy Technology Perspectives for a Clean Energy Future Ms. Maria van der Hoeven Executive Director International Energy Agency Madrid, 2 September 212 OECD/IEA 212 Key messages 1. A sustainable energy

Energy Technology Perspectives for a Clean Energy Future Ms. Maria van der Hoeven Executive Director International Energy Agency Madrid, 2 September 212 OECD/IEA 212 Key messages 1. A sustainable energy

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division EUFORES Parliamentary Dinner Debate, Brussels, 9 September, 2014 What Energy Security is about IEA defines energy

Contribution of Renewables to Energy Security Cédric PHILIBERT Renewable Energy Division EUFORES Parliamentary Dinner Debate, Brussels, 9 September, 2014 What Energy Security is about IEA defines energy

The Power of Transformation Wind, Sun and the Economics of Flexible Power Systems

The Power of Transformation Wind, Sun and the Economics of Flexible Power Systems Federal Ministry for Economic Affairs and Energy, 1 July 2014, Berlin Main Results and Strategic Approach Ms Maria van

The Power of Transformation Wind, Sun and the Economics of Flexible Power Systems Federal Ministry for Economic Affairs and Energy, 1 July 2014, Berlin Main Results and Strategic Approach Ms Maria van

Medium- Term Renewable Energy Market Report Heymi Bahar Project Manager Renewable Energy Division International Energy Agency

Medium- Term Renewable Energy Market Report 2016 Heymi Bahar Project Manager Renewable Energy Division International Energy Agency Energy and Mines World Congress, Toronto, 21-22 November 2016 Context

Medium- Term Renewable Energy Market Report 2016 Heymi Bahar Project Manager Renewable Energy Division International Energy Agency Energy and Mines World Congress, Toronto, 21-22 November 2016 Context

Transforming the energy sector transforming the economy The importance of Global Innovation and Collaboration

Transforming the energy sector transforming the economy The importance of Global Innovation and Collaboration Jean François Gagné Energy Technology Policy Division Head International Energy Agency IEA

Transforming the energy sector transforming the economy The importance of Global Innovation and Collaboration Jean François Gagné Energy Technology Policy Division Head International Energy Agency IEA

TABLE OF CONTENTS 6 RENEWABLES 2017

TABLE OF CONTENTS Executive summary... 13 1. Recent renewable energy deployment trends... 17 Highlights... 17 Electricity... 18 Technology deployment summary... 18 Regional deployment summary... 20 Transport...

TABLE OF CONTENTS Executive summary... 13 1. Recent renewable energy deployment trends... 17 Highlights... 17 Electricity... 18 Technology deployment summary... 18 Regional deployment summary... 20 Transport...

Cédric Philibert, Renewable Energy Division World Solar Congress, Kassel, 1 Sept. 2011

Cédric Philibert, Renewable Energy Division World Solar Congress, Kassel, 1 Sept. 2011 Building on Source: Sundrop Fuels Inc. Source: Sundrop Fuels, Inc. also starring Solar heating and cooling Forthcoming

Cédric Philibert, Renewable Energy Division World Solar Congress, Kassel, 1 Sept. 2011 Building on Source: Sundrop Fuels Inc. Source: Sundrop Fuels, Inc. also starring Solar heating and cooling Forthcoming

Medium Term Energy Market Outlook IEEJ Energy Seminar October 213 Keisuke Sadamori, Director, Energy Markets & Security, IEA Primary Energy Supply from Fossil Fuels Mtoe 5 45 4 35 3 25 2 15 1 5 2 21 22

Medium Term Energy Market Outlook IEEJ Energy Seminar October 213 Keisuke Sadamori, Director, Energy Markets & Security, IEA Primary Energy Supply from Fossil Fuels Mtoe 5 45 4 35 3 25 2 15 1 5 2 21 22

Renewable Power: Has it won the cost race?

Renewable Power: Has it won the cost race? Michael Taylor Senior Analyst, IITC Recent cost evolution Latest trends in the cost and performance of renewable power generation technologies Global results

Renewable Power: Has it won the cost race? Michael Taylor Senior Analyst, IITC Recent cost evolution Latest trends in the cost and performance of renewable power generation technologies Global results

Politique et sécurité énergétique dans le contexte des nouvelles énergies

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

Clean energy technologies: tracking progress and the role of digitalization

Clean energy technologies: tracking progress and the role of digitalization Peter Janoska and George Kamiya, Energy Environment Division, IEA COP23 16 November 2017 IEA OECD/IEA 2017 The IEA works around

Clean energy technologies: tracking progress and the role of digitalization Peter Janoska and George Kamiya, Energy Environment Division, IEA COP23 16 November 2017 IEA OECD/IEA 2017 The IEA works around

Role of clean energy in the context of Paris Agreement

Role of clean energy in the context of Paris Agreement Peter Janoska, Energy Analyst, IEA COP 23, Bonn, 15 November 2017 IEA The IEA works around the world to support an accelerated clean energy transitions

Role of clean energy in the context of Paris Agreement Peter Janoska, Energy Analyst, IEA COP 23, Bonn, 15 November 2017 IEA The IEA works around the world to support an accelerated clean energy transitions

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dr. Uwe Remme, IEA wholesem Annual Conference, 3 July 2017, London IEA IEA Energy Technology & Policy Activities Scenarios

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dr. Uwe Remme, IEA wholesem Annual Conference, 3 July 2017, London IEA IEA Energy Technology & Policy Activities Scenarios

Integration of variable renewable energy in power grid and industry Cédric Philibert, Renewable Energy Division, International Energy Agency

Integration of variable renewable energy in power grid and industry Cédric Philibert, Renewable Energy Division, International Energy Agency International workshop on integration & interconnection, Santiago

Integration of variable renewable energy in power grid and industry Cédric Philibert, Renewable Energy Division, International Energy Agency International workshop on integration & interconnection, Santiago

RENEWABLE POWER: CLIMATE-SAFE ENERGY COMPETES ON COST ALONE

RENEWABLE POWER: CLIMATE-SAFE ENERGY COMPETES ON COST ALONE Photograph: Shutterstock As climate talks focus increasingly on practical solutions to cut carbon emissions, countries around the world are more

RENEWABLE POWER: CLIMATE-SAFE ENERGY COMPETES ON COST ALONE Photograph: Shutterstock As climate talks focus increasingly on practical solutions to cut carbon emissions, countries around the world are more

Renewable electricity: Non-OECD Summary OECD Americas OECD Asia Oceania OECD Europe References...

TABLE OF CONTENTS Foreword... 3 Acknowledgements... 4 Executive summary... 13 The role of renewables in the energy mix continued to expand in 2013... 13 Strong market drivers, but increased risks for renewable

TABLE OF CONTENTS Foreword... 3 Acknowledgements... 4 Executive summary... 13 The role of renewables in the energy mix continued to expand in 2013... 13 Strong market drivers, but increased risks for renewable

Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees i

Renewables 217 Heymi Bahar IEEJ, Tokyo 31 October 217 Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees

Renewables 217 Heymi Bahar IEEJ, Tokyo 31 October 217 Context Three numbers and three core global energy challenges: 6.5 million premature deaths each year can be attributed to air pollution 2.7 degrees

Renewable Energy and other Sustainable Energy Sources. Paul Simons Deputy Executive Director International Energy Agency

Renewable Energy and other Sustainable Energy Sources Paul Simons Deputy Executive Director International Energy Agency G20 ESWG meeting Munich, 14 December 2016 Renewables and efficiency lead the transition

Renewable Energy and other Sustainable Energy Sources Paul Simons Deputy Executive Director International Energy Agency G20 ESWG meeting Munich, 14 December 2016 Renewables and efficiency lead the transition

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario. Agneta Rising Director General

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario Agneta Rising Director General Harmony January 2017 THE CURRENT STATUS OF NUCLEAR ENERGY 2 Global consumption of electricity

Harmony The role of nuclear energy meeting electricity needs in the 2 degree scenario Agneta Rising Director General Harmony January 2017 THE CURRENT STATUS OF NUCLEAR ENERGY 2 Global consumption of electricity

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Director (Acting) of Sustainability, Technology and Outlooks 16 November 2017 COP23, IETA Pavilion IEA Introduction

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Director (Acting) of Sustainability, Technology and Outlooks 16 November 2017 COP23, IETA Pavilion IEA Introduction

RENEWABLE POWER GENERATION COSTS IN 2014

RENEWABLE POWER GENERATION COSTS IN Executive Summary The competiveness of renewable power generation technologies continued improving in 2013 and. The cost-competitiveness of renewable power generation

RENEWABLE POWER GENERATION COSTS IN Executive Summary The competiveness of renewable power generation technologies continued improving in 2013 and. The cost-competitiveness of renewable power generation

IEA WORK ON FUTURE ELECTRICITY SYSTEMS

IEA WORK ON FUTURE ELECTRICITY SYSTEMS Power grids, demand response and the low carbon transition Dr. Luis Munuera Smart Grids Technology Lead IEA Symposium on Demand Flexibility and RES Integration SMART

IEA WORK ON FUTURE ELECTRICITY SYSTEMS Power grids, demand response and the low carbon transition Dr. Luis Munuera Smart Grids Technology Lead IEA Symposium on Demand Flexibility and RES Integration SMART

Fostering Long-Term Investment in Energy

Fostering Long-Term Investment in Energy Dr. Paolo Frankl Head of Renewable Energy Division International Energy Agency B20 Energy Forum, 2 October 2015 Billion dollars Oil price drop and short-term Global

Fostering Long-Term Investment in Energy Dr. Paolo Frankl Head of Renewable Energy Division International Energy Agency B20 Energy Forum, 2 October 2015 Billion dollars Oil price drop and short-term Global

CONTENTS TABLE OF PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY OECD/IEA, 2016 ANNEXES

TABLE OF CONTENTS PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY ANNEXES INTRODUCTION AND SCOPE 1 OVERVIEW 2 OIL MARKET OUTLOOK 3 NATURAL GAS MARKET OUTLOOK 4 COAL MARKET OUTLOOK

TABLE OF CONTENTS PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY ANNEXES INTRODUCTION AND SCOPE 1 OVERVIEW 2 OIL MARKET OUTLOOK 3 NATURAL GAS MARKET OUTLOOK 4 COAL MARKET OUTLOOK

Renewables subsidy schemes in Europe. Energy Economics Summer School, University of Auckland 19-Feb-2018

Renewables subsidy schemes in Europe Energy Economics Summer School, University of Auckland 19-Feb-2018 Briony Bennett 2008 - Bachelor of Arts & Science, University of Auckland 2012 - Masters of International

Renewables subsidy schemes in Europe Energy Economics Summer School, University of Auckland 19-Feb-2018 Briony Bennett 2008 - Bachelor of Arts & Science, University of Auckland 2012 - Masters of International

Table of contents. 1 Introduction System impacts of VRE deployment Technical flexibility assessment of case study regions...

Table of contents Foreword................................................................................. 3 Acknowledgements...5 Executive summary...13 1 Introduction...21 Background...21 Context...21

Table of contents Foreword................................................................................. 3 Acknowledgements...5 Executive summary...13 1 Introduction...21 Background...21 Context...21

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks. Tim Gould, IEA

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks Tim Gould, IEA A new fuel in pole position Change in global primary energy demand Mtoe 2 000 1990-2015 2015-2040 Rest of world 1 500 1 000 Renewables

Third IEA IEF OPEC Symposium on Gas and Coal Market Outlooks Tim Gould, IEA A new fuel in pole position Change in global primary energy demand Mtoe 2 000 1990-2015 2015-2040 Rest of world 1 500 1 000 Renewables

World Energy Outlook 2010 Renewables in MENA. Maria Argiri Office of the Chief Economist 15 December 2010

World Energy Outlook 2010 Renewables in MENA Maria Argiri Office of the Chief Economist 15 December 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears

World Energy Outlook 2010 Renewables in MENA Maria Argiri Office of the Chief Economist 15 December 2010 The context: a time of unprecedented uncertainty The worst of the global economic crisis appears

OECD/IEA 2016 OECD/IEA Canberra November 2016

Canberra November 2016 The global energy context today Key points of orientation: Middle East share in global oil production in 2016 at highest level for 40 years Transformation in gas markets deepening

Canberra November 2016 The global energy context today Key points of orientation: Middle East share in global oil production in 2016 at highest level for 40 years Transformation in gas markets deepening

Where do we want to go?

Where do we want to go? Dave Turk, Acting Director, Sustainability, Technology and Outlooks EU Talanoa Conference, 13 June 218, Brussels IEA Where do we want to go? Global energy-related CO 2 emissions

Where do we want to go? Dave Turk, Acting Director, Sustainability, Technology and Outlooks EU Talanoa Conference, 13 June 218, Brussels IEA Where do we want to go? Global energy-related CO 2 emissions

Auctions in power systems with high shares of renewables. Dr. Paolo Frankl, Head, Renewable Energy Division, IEA AURES, Brussels - 20 November 2017

Auctions in power systems with high shares of renewables Dr. Paolo Frankl, Head, Renewable Energy Division, IEA AURES, Brussels - 20 November 2017 Renewables dominate power generation growth Electricity

Auctions in power systems with high shares of renewables Dr. Paolo Frankl, Head, Renewable Energy Division, IEA AURES, Brussels - 20 November 2017 Renewables dominate power generation growth Electricity

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

The impacts of nuclear energy and renewables on network costs. Ron Cameron OECD Nuclear Energy Agency

The impacts of nuclear energy and renewables on network costs Ron Cameron OECD Nuclear Energy Agency Energy Mix A country s energy mix depends on both resources and policies The need for energy depends

The impacts of nuclear energy and renewables on network costs Ron Cameron OECD Nuclear Energy Agency Energy Mix A country s energy mix depends on both resources and policies The need for energy depends

APEC Energy Demand and Supply Outlook, 6 th Edition

APEC Energy Demand and Supply Outlook, 6 th Edition Cecilia Tam Special Advisor, APERC Asia Pacific Energy Research Centre Business as Usual (BAU) Scenario 2 Mtoe Energy intensity index Outlook for APEC

APEC Energy Demand and Supply Outlook, 6 th Edition Cecilia Tam Special Advisor, APERC Asia Pacific Energy Research Centre Business as Usual (BAU) Scenario 2 Mtoe Energy intensity index Outlook for APEC

Integrating variable renewables: Implications for energy resilience

Integrating variable renewables: Implications for energy resilience Peerapat Vithaya, Energy Analyst System Integration of Renewables Enhancing Energy Sector Climate Resilience in Asia Asia Clean Energy

Integrating variable renewables: Implications for energy resilience Peerapat Vithaya, Energy Analyst System Integration of Renewables Enhancing Energy Sector Climate Resilience in Asia Asia Clean Energy

Analyses market and policy trends for electricity, heat and transport Investigates the strategic drivers for RE deployment Benchmarks the impact and c

Paolo Frankl Head Renewable Energy Division International Energy Agency Institute of Energy Economics, Japan (IEEJ) Energy Seminar Tokyo, 7 March 2012 OECD/IEA 2011 Analyses market and policy trends for

Paolo Frankl Head Renewable Energy Division International Energy Agency Institute of Energy Economics, Japan (IEEJ) Energy Seminar Tokyo, 7 March 2012 OECD/IEA 2011 Analyses market and policy trends for

The Global Annual Energy Meeting The Coming Energy Market, IV edition. GAMESA: a vision from the market Ignacio Martín - Executive Chairman

The Coming Energy Market, IV edition GAMESA: a vision from the market Ignacio Martín - Executive Chairman October 30th, 2015 1 Solid start of a new period 2015 Current ENVIRONMENT: In 2012, Market environment:

The Coming Energy Market, IV edition GAMESA: a vision from the market Ignacio Martín - Executive Chairman October 30th, 2015 1 Solid start of a new period 2015 Current ENVIRONMENT: In 2012, Market environment:

Renewable Energy for Industry

Download the report: www.iea.org/publications/insights Renewable Energy for Industry Cédric Philibert, Renewable Energy Division, International Energy Agency Nordic Pavillion, COP23, Fidji - Bonn, 15 November

Download the report: www.iea.org/publications/insights Renewable Energy for Industry Cédric Philibert, Renewable Energy Division, International Energy Agency Nordic Pavillion, COP23, Fidji - Bonn, 15 November

Enel Green Power. Clean Energy Summit. Gu Yoon Chung, Head of Business Development for Asia and Pacific area. Sydney, July 27 th 2016

Enel Green Power Clean Energy Summit Gu Yoon Chung, Head of Business Development for Asia and Pacific area Sydney, July 27 th 2016 Enel today 1 Italy North America Capacity: 2.5 GW Capacity: 30.7 GW Networks:

Enel Green Power Clean Energy Summit Gu Yoon Chung, Head of Business Development for Asia and Pacific area Sydney, July 27 th 2016 Enel today 1 Italy North America Capacity: 2.5 GW Capacity: 30.7 GW Networks:

The recent revision of Renewable Energy Act in Germany

The recent revision of Renewable Energy Act in Germany Overview and results of the PV tendering scheme Christian Redl SOFIA, 17 JANUARY 2016 The Energiewende targets imply fundamental changes to the power

The recent revision of Renewable Energy Act in Germany Overview and results of the PV tendering scheme Christian Redl SOFIA, 17 JANUARY 2016 The Energiewende targets imply fundamental changes to the power

Strong focus on market and policy analysis

OECD/IEA - 2015 Founded in 1974 OECD agency 29 member countries 1 new applicant - Mexico 3 associate countries: China, Indonesia, Thailand 240 staff in Paris secretariat The European Commission also participates

OECD/IEA - 2015 Founded in 1974 OECD agency 29 member countries 1 new applicant - Mexico 3 associate countries: China, Indonesia, Thailand 240 staff in Paris secretariat The European Commission also participates

The importance of energy and activity data for technology policy modeling

The importance of energy and activity data for technology policy modeling 2016 InterEnerStat Workshop: Energy efficiency and end-use data and Meeting of Organisations 14 December 2016, Paris Eric Masanet,

The importance of energy and activity data for technology policy modeling 2016 InterEnerStat Workshop: Energy efficiency and end-use data and Meeting of Organisations 14 December 2016, Paris Eric Masanet,

Figure ES.1: LCOE ranges for baseload technologies (at each discount rate) 3% 7% 10%

3% 7% 10%") Executive summary Projected Costs of Generating Electricity 215 Edition is the eighth report in the series on the levelised costs of generating electricity. This report presents the results of work performed

Executive summary Projected Costs of Generating Electricity 215 Edition is the eighth report in the series on the levelised costs of generating electricity. This report presents the results of work performed

TABLE OF CONTENTS. Highlights

TABLE OF CONTENTS Executive summary... 13 1. Global overview... 17 Highlights... 17 Recent deployment trends... 18 Recent policy trends... 20 Global outlook... 23 Renewable heat... 25 Renewable electricity...

TABLE OF CONTENTS Executive summary... 13 1. Global overview... 17 Highlights... 17 Recent deployment trends... 18 Recent policy trends... 20 Global outlook... 23 Renewable heat... 25 Renewable electricity...

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth Dr. Fatih Birol, Executive Director, International Energy Agency Delft University of Technology, 20 March

The Future of Global Energy Markets: Implications for Security, Sustainability and Economic Growth Dr. Fatih Birol, Executive Director, International Energy Agency Delft University of Technology, 20 March

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios Dr. Uwe Remme, IEA International Energy Workshop, 19 June 2018, Gothenburg IEA How far can technology take us? 40 Reference

Energy Technology Perspectives 2017 The Role of CCS in Deep Decarbonisation Scenarios Dr. Uwe Remme, IEA International Energy Workshop, 19 June 2018, Gothenburg IEA How far can technology take us? 40 Reference

Renewable Energy Perspectives and Roadmaps 2010

Per lo sviluppo di una filiera industriale delle rinnovabili in Italia Renewable Energy Perspectives and Roadmaps 2010 Rome, 13 July 2010 Roberto VIGOTTI Chair REWP IEA Energy scenarios. What for? neither

Per lo sviluppo di una filiera industriale delle rinnovabili in Italia Renewable Energy Perspectives and Roadmaps 2010 Rome, 13 July 2010 Roberto VIGOTTI Chair REWP IEA Energy scenarios. What for? neither

Decarbonization pathways and the new role of DSOs

Decarbonization pathways and the new role of DSOs Kristian Ruby Secretary General Eurelectric 3 April 2019 We have modelled 3 deep decarbonization scenarios based on electrification of key economic sectors

Decarbonization pathways and the new role of DSOs Kristian Ruby Secretary General Eurelectric 3 April 2019 We have modelled 3 deep decarbonization scenarios based on electrification of key economic sectors

The Renewable Revolution: Power Generation Costs. Michael Taylor IRENA Innovation and Technology Centre

The Renewable Revolution: Power Generation Costs Michael Taylor mtaylor@irena.org IRENA Innovation and Technology Centre 26 October, 2012 COSTING. WHY? HOW? WITH WHOM? 2 Rationale and goals Renewable energy

The Renewable Revolution: Power Generation Costs Michael Taylor mtaylor@irena.org IRENA Innovation and Technology Centre 26 October, 2012 COSTING. WHY? HOW? WITH WHOM? 2 Rationale and goals Renewable energy

Strong momentum for renewable electricity Global renewable electricity production, historical and projected TWh

Renewables Medium-Term Forecasts and Long-Term Scenarios Paolo Frankl Head, Renewable Energy Division International Energy Agency Strong momentum for renewable electricity Global renewable electricity

Renewables Medium-Term Forecasts and Long-Term Scenarios Paolo Frankl Head, Renewable Energy Division International Energy Agency Strong momentum for renewable electricity Global renewable electricity

World Energy Outlook Bo Diczfalusy, Näringsdepartementet

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

Instituto Tecnológico Autónomo de México Mexico City, 28 September 2015

Instituto Tecnológico Autónomo de México Mexico City, 28 September 2015 Energy & climate change today A major milestone in efforts to combat climate change is fast approaching COP21 in Paris in December

Instituto Tecnológico Autónomo de México Mexico City, 28 September 2015 Energy & climate change today A major milestone in efforts to combat climate change is fast approaching COP21 in Paris in December

EXECUTIVE SUMMARY RENEWABLE ENERGY PROSPECTS: CHINA

EXECUTIVE SUMMARY RENEWABLE ENERGY PROSPECTS: CHINA November 2014 Copyright IRENA 2014 Unless otherwise indicated, the material in this publication may be used freely, shared or reprinted, so long as IRENA

EXECUTIVE SUMMARY RENEWABLE ENERGY PROSPECTS: CHINA November 2014 Copyright IRENA 2014 Unless otherwise indicated, the material in this publication may be used freely, shared or reprinted, so long as IRENA

The Solar Revolution Its Scale, the Benefit and Challenges

The Future of Energy: Latin America s Path to Sustainability Santiago, Chile The Solar Revolution Its Scale, the Benefit and Challenges Dr. Francis O Sullivan August 18 th, 2015 1 The scale and distribution

The Future of Energy: Latin America s Path to Sustainability Santiago, Chile The Solar Revolution Its Scale, the Benefit and Challenges Dr. Francis O Sullivan August 18 th, 2015 1 The scale and distribution

World Energy Investment 2017

World Energy Investment 2017 Madrid, September 2017 Alessandro Blasi and Alfredo del Canto IEA OECD/IEA 2017 Global energy investment fell 12% in 2016, a second consecutive year of decline Global energy

World Energy Investment 2017 Madrid, September 2017 Alessandro Blasi and Alfredo del Canto IEA OECD/IEA 2017 Global energy investment fell 12% in 2016, a second consecutive year of decline Global energy

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Acting Director, Directorate of Sustainability, Technology and Outlooks, IEA IEA Innovation for Cool Earth Forum

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Dave Turk, Acting Director, Directorate of Sustainability, Technology and Outlooks, IEA IEA Innovation for Cool Earth Forum

Trends in renewable energy and storage

Trends in renewable energy and storage Energy and Mines World Congress, 2017 Rachel Jiang November 27, 2017 Key trends Solar, wind may make up one-third of global electricity generation by 2040 and a growing

Trends in renewable energy and storage Energy and Mines World Congress, 2017 Rachel Jiang November 27, 2017 Key trends Solar, wind may make up one-third of global electricity generation by 2040 and a growing

Renewables 2018 Analysis and Forecasts to 2023

Renewables 218 Analysis and Forecasts to 223 Heymi Bahar Columbia University SIPA, 26 October 218 IEA Context CO2 emissions to rise again in 218 Progress in energy efficiency is slowing Expensive energy

Renewables 218 Analysis and Forecasts to 223 Heymi Bahar Columbia University SIPA, 26 October 218 IEA Context CO2 emissions to rise again in 218 Progress in energy efficiency is slowing Expensive energy

SECTION 1. EXECUTIVE SUMMARY

SECTION 1. EXECUTIVE SUMMARY Cheaper coal and cheaper gas will not derail the transformation and decarbonisation of the world s power systems. By 2040, zero-emission energy sources will make up 60% of

SECTION 1. EXECUTIVE SUMMARY Cheaper coal and cheaper gas will not derail the transformation and decarbonisation of the world s power systems. By 2040, zero-emission energy sources will make up 60% of

Energy Technology Perspectives: Transitions to Sustainable Buildings

Energy Technology Perspectives: Transitions to Sustainable Buildings John Dulac International Energy Agency IEA Global buildings status report Buildings are not on track to meet 2DS objectives Tracking

Energy Technology Perspectives: Transitions to Sustainable Buildings John Dulac International Energy Agency IEA Global buildings status report Buildings are not on track to meet 2DS objectives Tracking

Christine Lins Executive Secretary

Christine Lins Executive Secretary christine.lins@ren21.net Tokyo, 25 October 2017 REN21 Renewables 2017 Global Status Report The report features: Global Overview Market & Industry Trends Distributed Renewable

Christine Lins Executive Secretary christine.lins@ren21.net Tokyo, 25 October 2017 REN21 Renewables 2017 Global Status Report The report features: Global Overview Market & Industry Trends Distributed Renewable

Introduction to medium term reports Based on the most recent data available 5 years outlook is important for policy making Natural gas and renewables

IEA Medium-Term Market Reports IEEJ Seminar Tokyo, 20 September 2012 Didier Houssin Director, Energy Markets and Security International Energy Agency OECD/IEA 2011 Introduction to medium term reports Based

IEA Medium-Term Market Reports IEEJ Seminar Tokyo, 20 September 2012 Didier Houssin Director, Energy Markets and Security International Energy Agency OECD/IEA 2011 Introduction to medium term reports Based

Making the Electricity System Work

Making the Electricity System Work Variable Renewables Electricity Systems Integration get it right Alessandro Clerici July 24/2017 Varenna Variable Renewables Electricity Systems Integration: how to get

Making the Electricity System Work Variable Renewables Electricity Systems Integration get it right Alessandro Clerici July 24/2017 Varenna Variable Renewables Electricity Systems Integration: how to get

Accelerating energy innovation to achieve a sustainable future

Accelerating energy innovation to achieve a sustainable future Tom Kerr OECD Green Technology and Innovation Workshop Paris,25 October 2010 IEA energy technology activities Where are we today? Global Gaps

Accelerating energy innovation to achieve a sustainable future Tom Kerr OECD Green Technology and Innovation Workshop Paris,25 October 2010 IEA energy technology activities Where are we today? Global Gaps

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division OECD/IEA, 2016 The IEA works around the world to support

Are Sustainable Urban Energy Systems Essential for a New Deal on Energy Access for Africa? By Dave Turk, Head of IEA Energy Environment Division OECD/IEA, 2016 The IEA works around the world to support

Energy & Climate Change ENYGF 2015

Energy & Climate Change ENYGF 2015 Ellina Levina Environment & Climate Change Unit Sustainable Energy Policy and Technology, IEA 22 June 2015 29 Member Countries: Australia, Japan, Korea, New Zealand,

Energy & Climate Change ENYGF 2015 Ellina Levina Environment & Climate Change Unit Sustainable Energy Policy and Technology, IEA 22 June 2015 29 Member Countries: Australia, Japan, Korea, New Zealand,

Competitive energy landscape in Europe

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

Dr. Johannes Trüby, IEA Clean Coal Day, Tokyo 5 September 2017

Dr. Johannes Trüby, IEA Clean Coal Day, Tokyo 5 September 2017 Global CO 2 emissions flat for 3 years Global energy-related CO 2 emissions Gt 35 30 25 20 15 10 5 1970 1975 1980 1985 1990 1995 2000 2005

Dr. Johannes Trüby, IEA Clean Coal Day, Tokyo 5 September 2017 Global CO 2 emissions flat for 3 years Global energy-related CO 2 emissions Gt 35 30 25 20 15 10 5 1970 1975 1980 1985 1990 1995 2000 2005

Energy Technology Perspectives 2014 Harnessing Electricity s Potential

The Global Outlook An active transformation of the energy system is essential to meet long-term goals. (ETP 2014) charts a course by which policy and technology together become driving forces in transforming

The Global Outlook An active transformation of the energy system is essential to meet long-term goals. (ETP 2014) charts a course by which policy and technology together become driving forces in transforming

Perspectives on the Energy Transition

Perspectives on the Energy Transition Global Energy Transition Prospects and the Role of Renewables Dolf Gielen, Director Innovation and Technology Centre, IRENA World Scientific and Engineering Congress

Perspectives on the Energy Transition Global Energy Transition Prospects and the Role of Renewables Dolf Gielen, Director Innovation and Technology Centre, IRENA World Scientific and Engineering Congress

CLIMATE ACTION PLAN 2050

CLIMATE ACTION PLAN 2050 PRINCIPLES AND GOALS OF GERMAN GOVERNMENT S CLIMATE POLICY By Dr. Ursula Fuentes Hu2ilter On leave from former posi:on as Head of Unit, Federal Ministry for the Environment, Nature

CLIMATE ACTION PLAN 2050 PRINCIPLES AND GOALS OF GERMAN GOVERNMENT S CLIMATE POLICY By Dr. Ursula Fuentes Hu2ilter On leave from former posi:on as Head of Unit, Federal Ministry for the Environment, Nature

Tipping the energy world off its axis Four large-scale upheavals in global energy : - The United States is turning into the undisputed global leader f

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

Tipping the energy world off its axis Four large-scale upheavals in global energy : - The United States is turning into the undisputed global leader f

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

The rapidly changing global energy landscape Dr. Fatih Birol Executive Director, International Energy Agency IEEJ, Tokyo, 27 February 2018 IEA Tipping the energy world off its axis Four large-scale upheavals

Electro fuels an introduction

Electro fuels an introduction Cédric Philibert, Renewable Energy Division, International Energy Agency EC-IEA Workshop on Electro fuels, Brussels, 10 Sept 2018 IEA Industry and transports: the hard-to-abate

Electro fuels an introduction Cédric Philibert, Renewable Energy Division, International Energy Agency EC-IEA Workshop on Electro fuels, Brussels, 10 Sept 2018 IEA Industry and transports: the hard-to-abate

Energy, Electricity and Nuclear Power Estimates for the Period up to 2050

REFERENCE DATA SERIES No. 1 2018 Edition Energy, Electricity and Nuclear Power Estimates for the Period up to 2050 @ ENERGY, ELECTRICITY AND NUCLEAR POWER ESTIMATES FOR THE PERIOD UP TO 2050 REFERENCE

REFERENCE DATA SERIES No. 1 2018 Edition Energy, Electricity and Nuclear Power Estimates for the Period up to 2050 @ ENERGY, ELECTRICITY AND NUCLEAR POWER ESTIMATES FOR THE PERIOD UP TO 2050 REFERENCE

Global energy markets outlook versus post-paris Agreement Impact on South East Europe

Global energy markets outlook versus post-paris Agreement Impact on South East Europe Sylvia Elisabeth Beyer International Energy Agency Thessaloniki, 29 June 2016 A 2 C pathway requires more technological

Global energy markets outlook versus post-paris Agreement Impact on South East Europe Sylvia Elisabeth Beyer International Energy Agency Thessaloniki, 29 June 2016 A 2 C pathway requires more technological

A call for public - private efforts for accelerating investments in renewables in MENA and Africa Roberto Vigotti

A call for public - private efforts for accelerating investments in renewables in MENA and Africa Roberto Vigotti Secretary General Rabat 3 May 2016 1. Trends for global RE deployment 2 World electricity

A call for public - private efforts for accelerating investments in renewables in MENA and Africa Roberto Vigotti Secretary General Rabat 3 May 2016 1. Trends for global RE deployment 2 World electricity

World Energy Outlook Dr Fatih Birol Chief Economist, IEA Istanbul, 20 December

World Energy Outlook 2013 Dr Fatih Birol Chief Economist, IEA Istanbul, 20 December The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching roles:

World Energy Outlook 2013 Dr Fatih Birol Chief Economist, IEA Istanbul, 20 December The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries are switching roles:

The Post COP 22 Renewable Energy Landscape 45th Cairo Climate Talks. January 23, Mahmoud El-Refai Power Generation Services, Siemens

The Post COP 22 Renewable Energy Landscape 45th Cairo Climate Talks. January 23, 2017 Power Generation Services, Siemens Unrestricted Siemens 2017 siemens.com Our priority in bringing down CO2 emissions

The Post COP 22 Renewable Energy Landscape 45th Cairo Climate Talks. January 23, 2017 Power Generation Services, Siemens Unrestricted Siemens 2017 siemens.com Our priority in bringing down CO2 emissions

How to Meet the EU's Greenhouse Gas Emission Targets PRIMES modelling for the Winter Package

E3MLab www.e3mlab.eu PRIMES Model 1 How to Meet the EU's Greenhouse Gas Emission Targets PRIMES modelling for the Winter Package By Professor Pantelis Capros, E3MLab central@e3mlab.eu CLEAN ENERGY FOR

E3MLab www.e3mlab.eu PRIMES Model 1 How to Meet the EU's Greenhouse Gas Emission Targets PRIMES modelling for the Winter Package By Professor Pantelis Capros, E3MLab central@e3mlab.eu CLEAN ENERGY FOR

OECD/IEA Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015

Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015 The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment

Brent Wanner, Senior Energy Analyst Stockholm, 24 November 2015 The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment

The start of a new energy era?

The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment in 2016 Coal prices remain at rock-bottom as demand slows

The start of a new energy era? 2015 has seen lower prices for all fossil fuels Oil & gas could face second year of falling upstream investment in 2016 Coal prices remain at rock-bottom as demand slows

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels September 2010

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels 15-16 September 2010 Adam Brown Anselm Eisentraut Renewable Energy Division We need a global 50% CO 2 cut by 2050 Gt CO2 60 55

IEA Roadmap Workshop Sustainable Biomass Supply for Bioenergy and Biofuels 15-16 September 2010 Adam Brown Anselm Eisentraut Renewable Energy Division We need a global 50% CO 2 cut by 2050 Gt CO2 60 55