HGAP. Haynesville Global Access Pipeline. Tellurian Midstream Group April 2018

|

|

|

- Lesley Ray

- 5 years ago

- Views:

Transcription

1 HGAP Haynesville Global Access Pipeline Tellurian Midstream Group April 2018

2 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact are forward-looking statements. The words anticipate, assume, believe, budget, estimate, expect, forecast, initial, intend, may, plan, potential, project, should, will, would, and similar expressions are intended to identify forward-looking statements. The forward-looking statements in this presentation relate to, among other things, future contracts, contract terms and margins, our business and prospects, future costs, prices, financial results, liquidity and financing, regulatory and permitting developments, future demand and supply affecting LNG and general energy markets and the closing of, and the achievement of anticipated benefits from, our natural gas property acquisition. Our forward-looking statements are based on assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions, expected future developments, and other factors that we believe are appropriate under the circumstances. These statements are subject to numerous known and unknown risks and uncertainties, which may cause actual results to be materially different from any future results or performance expressed or implied by the forward-looking statements. These risks and uncertainties include those described in the Risk Factors section of Exhibit 99.1 to our Current Report on Form 8-K/A filed with the Securities and Exchange Commission (the SEC ) on March 15, 2017 and other filings with the SEC, which are incorporated by reference in this presentation. Many of the forward-looking statements in this presentation relate to events or developments anticipated to occur numerous years in the future, which increases the likelihood that actual results will differ materially from those indicated in such forward-looking statements. In addition, the acquisition, exploration and development of natural gas properties involve numerous risks and uncertainties, including the risks that we will assume unanticipated liabilities associated with the assets to be acquired and that the performance of the assets will not meet our expectations due to operational, geologic, regulatory, midstream or other issues. It is possible that the acquisition will not be completed on the terms or at the time expected, or at all. The forward-looking statements made in or in connection with this presentation speak only as of the date hereof. Although we may from time to time voluntarily update our prior forward-looking statements, we disclaim any commitment to do so except as required by securities laws. Non-GAAP financial measures This presentation contains information about projected EBITDA of Tellurian. EBITDA is not a financial measure determined in accordance with U.S. generally accepted accounting principles ( GAAP ), should not be viewed as a substitute for any financial measure determined in accordance with GAAP and is not necessarily comparable to similarly titled measures reported by other companies. It would not be possible without unreasonable efforts to reconcile the projected non-gaap information presented herein to net income, the most directly comparable GAAP financial measure. Similarly, projected future cash flows as set forth herein may differ from cash flows determined in accordance with GAAP. Reserves and resources Estimates of non-proved reserves or resources are based on more limited information, and are subject to significantly greater risk of not being produced, than proved reserves. 2

3 Who we are

of pipeline")

HGAP and PGAP")

4 Building a low-cost global gas business Driftwood Holdings partnership integrated, low-cost Upstream 11,620 acres in the Haynesville with 1.4 Tcf resource Pipeline ~$7 billion (1) of pipeline infrastructure projects in development Liquefaction ~$15 billion of liquefaction infrastructure in development Marketing International delivery of LNG cargoes started in 2017 Note: (1) HGAP and PGAP projects are in early stages and remain under review. 4

5 Business model Tellurian will offer equity interest in Driftwood Holdings Driftwood Holdings will consist of a Production Company, a Pipeline Network and an LNG Terminal (~27.6 mtpa) Equity will cost ~$1,500 per tonne Customer/Partner will receive equity LNG at tailgate of Driftwood LNG terminal at cost Nasdaq: TELL Customer/Partner ~60% Equity ownership ~40% Driftwood Holdings 100% Variable and operating costs expected to be ~$3.00/mmBtu FOB (including maintenance) Tellurian will manage and operate the project Production Company Pipeline Network LNG Terminal ~12 mtpa Tellurian Marketing Tellurian will retain ~12 mtpa and ~40% of the assets ~16 mtpa Customers 5

6 Driftwood Holdings operating costs Total cost of ~$3/mmBtu locks in low cost of supply $/mmbtu $0.22 $0.75 $0.79 $3.00 $0.36 $2.25 $0.88 Drilling and completion(1) Operating Gathering, processing and transportation(2) Contingency Delivered cost Liquefaction cost Total Upstream cost Liquefaction cost Sources: Notes: Wood Mackenzie, Tellurian Research. (1) Drilling and completion based on well cost of $10.2 million, 15.5 Bcf EUR, and 75.00% net revenue interest ( NRI ) (8/8ths). (2) Gathering, processing and transportation includes transportation cost to Driftwood pipeline to market. 6

7 Tellurian Pipeline Network Bringing low-cost gas to Southwest Louisiana 2 1 Driftwood Pipeline Capacity, Bcf/d 4.0 Cost, $ billions $2.2 Length, miles 96 Diameter, inches 48 Compression, HP 274,000 Status FERC approval pending Haynesville Global Access Pipeline Capacity, Bcf/d 2.0 Cost, $ billions $1.4 Length, miles 200 Diameter, inches 42 Compression, HP 23,000 Status Preliminary routing 3 Permian Global Access Pipeline Capacity, Bcf/d 2.0 Cost, $ billions $3.7 Length, miles 625 Diameter, inches 42 Compression, HP 258,000 Status Preliminary routing 7

8 Southwest Louisiana The Big Short

9 SW Louisiana: core of US gas demand 2025 Bcf/d SWLA supply & demand T e x a s Haynesville Perryville Bcf/d West Inbound to SWLA 10.8 Bcf/d Eunice/Station Lake Charles, LA Driftwood LNG Southwest LA: 20 Bcf/d of potential demand Prospective demand Outbound to TX Demand Supply - new projects Supply - existing capacity G u l f o f M e x i c o L o u i s i a n a Notes: LNG demand includes ambient capacity; Source: company data, drilling info, Entergy, Tellurian estimates 9

10 Infrastructure not built for new demand You can get to Carthage or Perryville, but where s the demand? 411 Total selected basin shale production, Bcf/d Marcellus pipelines: 7.7 Bcf/d Anadarko Carthage Midship: 1.3 Bcf/d Haynesville Perryville Transco St Marcellus-Utica Incremental production Permian KMI/DCP: 2.0 Bcf/d 10.2 AD HSC HH FGT Z3 Resource size, Tcf Source: EIA 2018 Annual Energy Outlook, RBN Energy; note Haynesville includes Texas production Eagle Ford 10

11 Market opportunity emerging for HGAP Rolloffs from existing pipes, combined with limited capacity from Perryville to SWLA, make HGAP attractive mmbtu/d 9,000,000 Pipeline capacity between Perryville & Eunice/Gillis mmbtu/d 16,000,000 Pipeline capacity between Carthage & Perryville 8,000,000 14,000,000 7,000,000 6,000,000 5,000,000 4,000,000 Pipeline capacity Contracted capacity Pipeline throughput 12,000,000 10,000,000 8,000,000 Capacity decrease results from contract roll offs on Gulf Crossing, MEP, Tiger, Regency, Enable (Line CP) and Gulf South expansion Pipeline capacity Contracted capacity 3,000,000 2,000,000 1,000,000 Capacity increases resulting from ANR, Texas Gas, Transco, Columbia Gulf, and Tennessee Gas system reversals 6,000,000 4,000,000 2,000,000 Pipeline throughput Current Haynseville production (EIA) 0 0 Source: Gas Supply Consulting 11

12 Perryville to suffer as Haynesville grows Production surge compounding problem of Northeast gas; outlet to market only way to relieve pressure Perryville basis vs. Haynesville production 11,000, ,000, Production (scf/d) 9,000,000 8,000,000 7,000,000 6,000, Basis 5,000, ,000,000 1/1/2017 7/1/2017 1/1/2018 7/1/2018 1/1/2019 7/1/2019 1/1/2020 7/1/2020 1/1/2021 7/1/2021 1/1/2022 7/1/2022 1/1/2023 7/1/2023 Haynesville production (historical) Haynesville production (projected) Perryville Basis (historical) Perryville Basis (projected) Source: NYMEX via Marketview, EIA Drilling Productivity Report, RBN Energy LLC for projections; Columbia Gulf Mainline, as proxy for Perryville 12

: Production: 0.0 Demand: 0.2 Net Inflows: 0.2 1.0 6.8 5.5 Pipeline at capacity South Louisiana S&D (bcf/d): Production: 2.6 Demand: 4.1 Net Inflows: 1.")

13 Louisiana gas flows and basis 2023 Haynesville* S&D (bcf/d): Production: 8.0 Demand: 0.2 Net Outflows: 7.8 East Texas Haynesville* Perryville $0.28 TCO -$ Transco St 85 Perryville S&D (bcf/d): Production: 0.0 Demand: 0.2 Net Inflows: Pipeline at capacity South Louisiana S&D (bcf/d): Production: 2.6 Demand: 4.1 Net Inflows: 1.5 Imbalance Katy/Ship South LA -$ $ *Haynesville, Bossier, Cotton Valley (Terryville) Louisiana only 13

14 Hurricane Permian is just gearing up... Permian producers running into takeaway constraints faster than anticipated... Bcf/d (1.0) Active takeaway capacity Production estimates North Mexico East West Production - GS Production - RBN Production - SocGen Production - TPH 1 Growing Mid- Continent volumes encroached, pushed out of Midwest by NE production, but takeaway options remained 2 Mexico seasonal demand increases, but infrastructure constraints on the other side limit demand pull 3 KMI/DCP Gulf Coast Express comes online and Mexico consumption grows, but Permian production outpaces takeaway growth 4 New pipeline needed in 2021 but to where? Source: Goldman Sachs (GS), Wells Fargo Equity Research, RBN Energy LLC (RBN), Societe Generale (SocGen), TudorPickeringHolt (TPH); Note: Mexico active takeaway capacity assumes less than 50% utilization 14

15 ...and will impact Texas Gulf Coast hardest 2023 Waha Hub Haynesville Perryville -$0.28 Transco St 85? Katy/Ship $-.05 South LA -$0.25 Sabine Pass Cameron Driftwood Agua Dulce Corpus Freeport -$

16 HSC basis moving in anticipation of Permian Backwardated market shows impact of Permian gas coming via intrastates, Agua Dulce 0.15 Rolling forward curve of HOUS SHIP CHANNEL APR $/mmbtu /10/2016 7/5/ /28/2016 6/23/ /16/2017 6/10/ /4/2018 5/29/ /22/2019 Actuals Curve as of: 28-Feb-2018 Curve as of: 29-Dec /16/ /8/2020 Curve as of: 30-Jun-2017 Curve as of: 30-Dec M Moving Average as of 28-Feb-2018 Source: Bloomberg as of 3/15/

17 Summary Bloomberg, EIA, RBN see a wall of gas that needs to find a market US dry gas production to hit 100 Bcf/d in next ten years Marcellus/Utica, Permian and Eagle Ford to provide growth of 18 Bcf/d Highly sensitive to increases in oil price Market needs at least Bcf/d of LNG exports to balance; currently only 10 Bcf/d operating or under construction SW Louisiana is the center of US natural gas demand growth for the next decade Driven by LNG, favorable permitting/sites, and petrochemical growth $170 bn of infrastructure needed to bring new production to demand Even with recently built infrastructure, you still have a last mile problem: you can get close, but cannot get to market Rock and a hard place: Northeast, Permian production growth crowding out other production Basis eroding almost everywhere until infrastructure can get in place Getting to demand first will be key to maximizing revenue Source: EIA AEO 2018, Reference Case; RBN Energy, LLC; Bloomberg New Energy Finance 17

18 HGAP Maps & Rates

19 HGAP route Haynesville Global Access Pipeline Capacity, Bcf/d 2.0 Cost, $ billions $1.4 Length, miles 200 Diameter, inches 42 Compression, HP 23,000 Status Preliminary routing 19

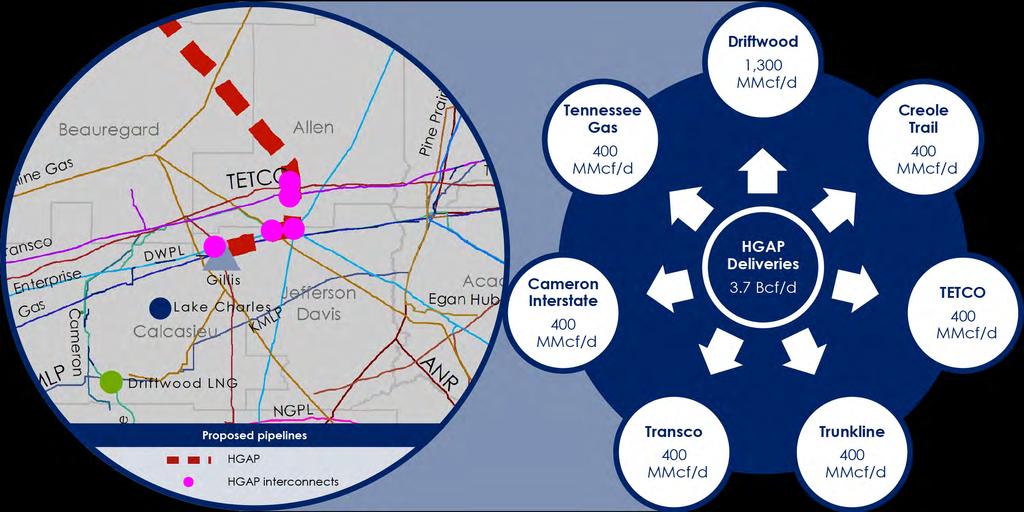

20 20 HGAP receipts

21 21 HGAP deliveries

22 Rates Negotiated rates for higher firm transportation service Shipper classes Standard: 100, ,999 Dth/d Anchor: 250, ,999 Dth/d Foundation: 500,000+ Dth/d Term: 10 years for Anchor, Standard shippers 20 years for Foundation shippers 22

23 Thank you