LNG in the Atlantic Basin plain sailing or choppy waters ahead?

|

|

|

- Earl Hoover

- 5 years ago

- Views:

Transcription

1 LNG in the Atlantic Basin plain sailing or choppy waters ahead? Andrew Jamieson Executive Vice President: Gas and Projects Shell Global Solutions International BV

2 Solutions should meet a combination of the 3E s Efficiency/Economy (Cheap) Oil Shale HVO Coal Oil Sands Hydro Natural Gas ME Oil & Gas Geothermal Energysecurity (Convenient) Wave Solar Bio Environment Wind (Clean) Renewables 2

3 Shell Global Scenarios to 2025 Critical Discontinuities Energy-intensive growth Supply security Carbon dioxide 3

4 LNG Competitors Coal Pipeline Gas Renewables 4

5 More Energy, Less Carbon MM BOE 400 Region MM BOE 400 By Type SE Asia NE Asia S. Asia Africa /ME Latin America FSU and CEE US/Canada Japan/ANZ W. Europe Other Transport Heat Power [Shell Global Energy Scenarios 2005 Data] 5

6 Setting the energy scene The oil industry has to explore new frontiers, develop new hydrocarbon energy sources and integrate CO 2 solutions. The challenge is to develop technology that can fuel growth without environmental degradation. Jeroen van der Veer Chief Executive, Royal Dutch Shell plc World energy demand (IEA World Energy Outlook 2004 reference case) 6

7 At the same time environmental impact must be minimized MANAGING OUR OWN CO 2 EMISSIONS ADDRESSING CO 2 INTENSITY BASELINE EMISSIONS - Increasing gas and LNG supply Improving efficiency Reducing flaring Leading designs CO 2 for enhanced oil recovery CO 2 sequestration Renewables offsets CO 2 credit trading - CO 2 sequestration / Enhanced Oil Recovery - Clean coal technologies - Biofuels - Renewables & Hydrogen REDUCED NET EMISSIONS 7

8 Managing CO 2 multiple approaches Clean coal to Power (IGCC) Buggenum, NL (250 MW) 12 yrs in operation 15% lower CO 2 emissions than conventional coal Stanwell ZeroGen Gas Gathering NLNG Bonny Waste gas from oil wells into LNG and pipeline gas CO2 emissions reductions ~30M tonnes Refinery Efficiency Port Dickson, Malaysia Substantial re-vamp existing facilities and construction of new units to improve efficiency Shell refineries achieved CO2 emissions reductions approaching 1M tonnes 8

9 Shell s Global LNG Business Coral in North America #3 energy marketer 4 LNG import sites Shell in Europe Pan-European marketer #1 LNG importer* Shell in Asia Pacific #1 LNG supplier* India and China access LNG supply In operation Under construction Under development Regas capacity In operation Under construction Under development *Sources: Shell Analysis, Poten & Partners, Platts, Wood Mackenzie, Shell share of sales amongst private companies 9

10 Positioned for Long Term Growth LNG GROWTH PORTFOLIO, (SHELL SHARE*) Mtpa Operation Construction Design Business Dev elop m ent * Incl. indirect interest in Woodside, Sakhalin at 27.5% 10

11 Driving LNG Growth 11

12 N. America: Integrating Gas Supply & Market SUPPLY & MARKET POSITIONS STRONG GROWTH IN SHELL GAS SUPPLY Broadwater Baja #3 gas marketer Cove Point Elba Island Gulf of Mexico Altamira est. REGAS: OPERATION CONSTRUCTION DEVELOPMENT PRODUCTION NORTH AMERICAN PRODUCTION SHELL LNG IMPORTS Source: Shell analysis 12

13 LNG Leadership in Europe DIVERSITY OF MARKET AND SUPPLY Russia Global LNG N. Africa REGAS CAPACITY REGAS OPPORTUNITY PRODUCTION MARKETING PRESENCE CURRENT IMPORT CHANNELS Source: Company reports & Shell estimates 13

14 LNG Fuelling the Future 14

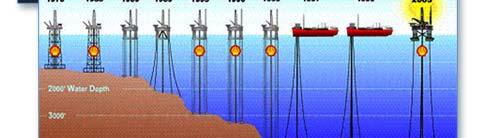

15 Challenges Ahead - Industry cost Rig rates escalation (increases since 2002) North Sea Jack-up GoM Jack-up WW Semi-sub ' WW Floater 5000'+ Alloy L Corrosion resistant alloy pipe (increases since 2002) 0% 100% 200% 300% 400% 500% Source: ODS Petrodata 0% 20% 40% 60% 80% Source: London Metals Exchange, Shell estimates Large specialty fabricated Fabricated pipe General fabricated (eg, exchangers) Mechanical (eg, pumps) Equipment prices (FEED) Construction & labour (increases since 2002) (increases since 2002) 0% 10% 20% 30% 40% 50% 60% Project management rates EPIC/EP contracts Installation vessel rates Construction labour rates 0% 20% 40% 60% 80% 100% Source: IPA Independent Project Analysis Source: IHS, Inc

16 Other Challenges Ahead Sakhalin Construction in Frontier Locations Safeguarding Pacific Grey Whales 16

17 Meeting the Challenges 4D Seismic Brunei Na Kika - Gulf of Mexico 17

18 Dual and Parallel Mixed Refrigerant NG LNG Pre-cooling cycle Main liquefaction cycle Main liquefaction cycle G T M G T M G T M NG LNG Pre-cooling cycle G T M G T M 18

19 Enriching Quality of Life Bonny Community Relations 19

20 Future Skilled Workforce 20

21 21