Investment Insights from Trends in Indonesian Gas Markets

|

|

|

- Doreen Booker

- 5 years ago

- Views:

Transcription

1 Good morning Ladies and gentlemen and thank you for rising early to come and listen to what I have to say today. I trust I will make it worth your while. The title of my presentation today is: Investment Insights from Trends in Indonesian Gas Markets We will see how the Indonesian energy and specifically gas markets are going through some major structural changes and we will look at the investment opportunities and challenges induced by these changes. Before I start however I would like to spend a few minutes introducing Risco Energy, a company that was formed 14 months ago and is growing very rapidly. Risco s investments have been partly driven by some of the insights derived from the gas market trends we will talk about. 1

2 A private Indonesian sponsored Singapore based Energy Investment Company. Bridge between private equity and operating oil and gas company Established July 2010 by experienced upstream oil and gas transaction specialists Strategy to leverage capital, industry and equity market knowledge and relationships to rapidly build a marked driven upstream growth portfolio with a premium valuation. A lot of words here that require some elucidation Invested US$150 million in 14 months and have secured Major stake in Ephindo, Indonesia leading first mover CBM company with 6 PSC s and at first gas from pilot wells in two PSC s 7,500 boepd of production in Indonesia and Philippines Operated oil and gas production and development onshore South Texas Leverage up equity with circa US$40 million in RBL facility On track to IPO Ephindo in 1H 2012 and Risco Energy at end

3 We are a Singapore company but most regional staff are located in a Jakarta Representative Office Differentiated from private Equity or portfolio investors by having significant in-house upstream oil and gas capability Core team responsible for acquiring 500 MM boe reserves over five years at EMP 3

4 In 14 month have established offices in Singapore, Jakarta and Houston with operations in Philippines, Indonesia and Texas 4

5 Risco s first investment, one month after it was founded was a 28% stake in Ephindo, Indonesia s first mover CBM company. We recognized good assets and management that needed additional capital and operating capability. Positioned Ephindo as the local partner of choice that is capable, well capitalized and well positioned at the juncture of CBM resource quality, infrastructure and markets. Grown from 3 to 6 PSc s with more coming 5

6 Significant conventional portfolio build with 19 MMstboe of 2P reserves and 7,000 boepd production Mature assets with significant development potential 6

7 So lets get back to looking at Investment Insights from Trends in Indonesian Gas Markets 7

8 To segment my message, I have the following presentation structure: A brief overview on Indonesian Energy Supply and Demand and the role of gas Some Specific Gas market insights The emergence of Coal Bed Methane as a a potentially material and disruptive supply source A quick look at the implications of commercial success in the emerging Indonesian CBM Industry An overview of the key investment implications of this rapidly changing gas business 8

to deliver one unit of GDP growth.")

9 Like many developing countries, the primary driver of energy consumption is economic growth and this chart clearly shows the impact on energy consumption of Indonesia s dramatic economic growth since emerging from the 1998 Asian financial crisis. The economy shows an energy intensity of around 1.0 meaning it take one unit of energy (a TOE in this case) to deliver one unit of GDP growth. Energy subsidies, as we will see later, are however still pervasive in the Indonesian economy and changes in subsidy levels also periodically impact annual energy consumption growth. Indonesia's 10 year CAGR in energy consumption is 3.6%. At a forecast 6.0% economic growth rate, Indonesia s energy consumption will double in the next 12 years and gas should play a key role in meeting this demand increase. 9

10 Indonesia s economic development of the 1970 s and 1980 s was partly oil export driven. However declining production and rising consumption saw Indonesia transition to become an oil importer in 2003 and loose its OPEC membership shortly thereafter. Indonesia remains a substantial gas exporter however. Indonesia s status as the worlds largest LNG exporter, was lost to Qatar a few years ago, however Indonesia continues today as a net oil and gas exporter on a boe basis. However, on a value basis, with Indonesia importing some half of its petroleum product needs and exporting LNG and piped gas, the hydrocarbon trade account is in balance. Indonesia s coal production and exports have skyrocketed in the last five years as it feeds energy hungry India and China in particular with thermal coal. Production of renewables, largely geothermal and increasing palm oil is growing steadily from a small base however the full potential of geothermal is a long way from being realized. 10

11 The bottom line is that Indonesia s net energy exports remain strongly positive with the industry s historic export status being driven successively by oil, then gas and now coal. The historic migration of exports from Oil to Gas to Coal is apparent Will CBM follow? 11

12 As mentioned earlier, the Indonesian energy sector is still highly distorted by the blunt instrument of subsidies. You cannot talk about energy in Indonesia without talking subsidies so it worth looking at what is really happening In the 2102 draft budget, energy subsidies make up 15% of budget expenditure, and that assumes a 10% 2012 increase in the TDL. These subsidies distort consumption, investment, BOP s and tax revenues. 12

13 Petroleum products consumption has grown at a CAGR of 3.3% p.a. driven by transportation fuels but offset by negative growth in Kerosene and fuel oil. The former has been displaced by LPG and the latter by gas for power generation Growth in consumption was fairly steady until 2005, interrupted however by the 1998 Asian financial crisis and then the doubling of domestic fuel prices in late

14 Post the major price increase in end 2005, the governments main tool to manage subsidies has been limiting the availability of subsidized petroleum products, particularly Kerosene for households and Diesel for industry. This has been quite effective however there is a strong underlying 7.0% p.a. CAGR in gasoline usage driven by the increasing number of cars and motorbikes on the roads. The acceleration of gasoline and diesel consumption in the last few years, is way beyond GDP growth rates, suggests smuggling. This has accelerated as the price differential to do so (differential between subsidized and market price) has risen. Subsidies at the current level are unsustainable and rising domestic fuel prices are inevitable, only the political will is lacking. 14

15 Now lets derive some insights from trends in the natural gas market 15

16 Indonesia's gas production is still rising although the rate of increase has moderated substantially since the growth of LNG export expansion came to an end in the early 1990 s. Pipeline exports boosted export growth in the 1990 s and more recently the Tangguh LNG plant in Papua came on stream as Indonesia third LNG export facility. The most striking long term trend is now the rise of domestic gas consumption. This is driven by the pricing benefits of natural gas and government policy to replace expensive petroleum product imports (which are subsidized) with domestically produced gas. 16

17 So how is the gas production utilized? In 2010 some 83% of Indonesian gas production was sold, with the rest being either consumed in production operation or lost through flaring and shrinkage. Of the gas that was sold some 38% was consumed in the domestic market and the remainder was either exported as LNG, largely to Japan, Korea or Taiwan or through pipelines to Singapore and Malaysia. PLN (State Electricity Company) and PGN (State Gas Company) and Fertilizer Producers (State owned) were the largest domestic consumers responsible for over 70% of consumption between them. All were supply constrained in

18 Unlike oil reserves, proven gas reserves have continued to grow in Indonesia as exploration has more than replaced production. A leveling off in proven reserves is however evident in recent years and a decline in potential reserves is also evident, driven by declining exploration investment and smaller exploration find sizes. The decline of exploration investment is a subject in itself however it clear the upstream business in Indonesia is increasingly mature and gassy. It important to understand that oil drives the industry cost structure and we remain in a US$100 bbl price and cost environment while domestic prices at say US$6.0 mmbtu mean we only have a $36.0 / boe revenue environment. This is a disincentive for exploration investment. 18

19 While Indonesia is gas resource and reserve rich most fields are undeveloped and distant from the major markets in Java with supply constrained by a lack of transportation infrastructure. 19

planned")

20 Beyond upstream gathering pipelines, the major gas transportation infrastructure centers around South & Central Sumatra - West Java and Natuna Sea Singapore and Malaysia Plans for pipelines from Kalimantan to Java have not been realized and are rapidly being overtaken by lower cost, quicker and more flexible LNG import terminals or Floating Storage and Re-gassification units (FSRU s) planned to address critical gas supply shortfalls in Java and North Sumatra. Mini LNG regassification plants are also being planned in Eastern Indonesia as shown on this map (Bali, Halmahera and Polema) Pertamina and PGN are major players in this new infrastructure development with PLN being the major customer, especially where it has CCGT facilities burning expensive imported diesel fuel. 20

21 Indonesia remains undersupplied with gas as pipeline and LNG exports emanate mostly from fields distant to the Java gas demand centers This diagram shows that even with the development of LNG regasification terminals in Java and Sumatra, domestic market supply constraints are expected to remain. This demand forecast is also typical of many developed in Indonesia, where demand growth is fundamentally supply constrained and not reflective of the unconstrained gas demand potential. 21

22 West Java is Indonesia s largest gas market with strong power, fertilizer and industrial markets and here the supply demand imbalance is most apparent. The solution is the 2-4 LNG import terminals being developed over the next five years delivering supply potentially > 1,250 MMSCFD. 22

23 The result is PLN planning for LNG being an increasingly important fuel, that displaces high cost diesel and fills the gap that gas has failed to fill. 23

24 A long history of low domestic gas prices, certainly lowered than export prices as this graphic shows, is one of the reasons behind the current domestic supply constraints. Lack of Infrastructure and customer credit quality were other significant factors impeding supply. Effectively, upstream suppliers were for many years being asked to subsidize largely state owned domestic consumers and support PGN s fat profit margins. This was never sustainable in my view and led to the current shortfalls. This situation, driven by necessity, is now changing. 24

25 Upstream gas prices, as measured by new domestic gas contract signings have been trending strongly upward for a number of years, as oil prices have also trended upward and supply constraints increased. Years of low long flat nominal pricing has been replaced by higher starter prices with some form of indexation now the norm. Oil linked prices paid by some customers deliver prices in excess of US$10.0 / mmbtu at current oil prices. This is a good deal for both producers and customers. In 2010 the average headline price for new gas contracts was US$5.8 / MMbtu. This however compares with an average Minas Indonesian Crude Price (ICP) of US$ 81.44/ bbl or US$14.04 / MMbtu. 25

26 The above is self evident. 26

27 The chart clearly shows the compelling gas value proposition for energy customers whose alternative is market priced or for some, subsidized petroleum products. Also shown is the expected prices of re-gassified LNG delivered from the Bontang LNG plant to customers in West Java from East Kalimantan. While this represents a 250% increase in gas prices, the result is still very cost effective gas and environmentally friendly energy. 27

28 Now lets explore the potential significance of the emerging CBM industry. 28

29 Coal Bed Methane (CBM) known as Coal Seam Methane (CSM) in Australia, like Shale Gas is Unconventional Gas that is not found in traps like conventional gas. CBM is generally found at less than 1,000 m depth, shallower than most conventional gas reservoirs. CBM is gas that is adsorbed onto the surface of coal and held there by the pressure of water in the coals. If the water pressure is reduced by pumping the water out the gas is liberated by desorption. Most exploration, development and production characteristics of CBM make it more expensive than conventional gas on a full cycle basis and its success has been where conventional gas production is in decline and unable to meet demand. Some characteristics of CBM gas are however more attractive than conventional gas. These are: Lower exploration risk Lower drilling costs given shallower depths and lower pressures Higher storage capacity of coal per unit rock volume 29

30 Technology led and market driven CBM production has had a material impact on US, Canadian and Australian gas markets. CBM s impact in the US and Canada has however been totally eclipsed by he success of shale gas. In Australia, a major gas producer and exporter, CBM is currently responsible for 12% of total gas production and this is set to increase dramatically as LNG exports from CBM are developed. 30

31 Indonesia s CBM potential is world class, as would be expected of a major coal producer. The CBM resource potential has been estimated at 450 TCF. If only 30% realized this is equal to the remaining conventional gas reserves we saw earlier. 31

32 Three basins hold 80% of this potential. South Sumatra Kutai Basin Barito Basin However only South Sumatra and Kutai basins also have developed gas markets and infrastructure. 32

33 New regulations that resolved overlapping claims and provided fiscal incentives have resulted in the signing on 39 CBM PSC s since Many more are expected over the near term. 33

34 While local entrepreneurs such as Ephindo, and Medco pioneered CBM in Indonesia, the recent arrival of the super majors is testimony to CBM s gas resource and economic potential. A period of consolidation can now also be expected. 34

35 Pertamina leveraged its large conventional PSC land holding to move into the CBM business largely financed by first mover local and foreign companies Entrepreneurial local companies are the next most significant although their business models are different. 35

36 The 39 PSC have committed to drill 256 core holes and 96 pilot holes over the first three year period. What is needed is the rigs to do this as there are no fit for purpose CBM coring or pilot rigs in the country and the conventional oil and gas rig approach is turning out to be very expensive Solving this is a challenge and a great opportunity for the service sector. Import and local content regulations is certainly not helping 36

37 East Kalimantan is the nexus of CBM Resource Quality, Markets and Infrastructure and has been the initial focus areas for many CBM investors. The presence of a MTPA undersupplied LNG plant is obviously a huge investor draw card and stands in contrast to the billions of dollars of downstream LNG investment that will have to be made to commercialize Queensland LNG. 37

38 Government and Industry have high expectations for Indonesia s CBM production potential and initial drilling results are technically very encouraging all be it generally behind schedule. Material exploration and pilot drilling programs are underway.. 38

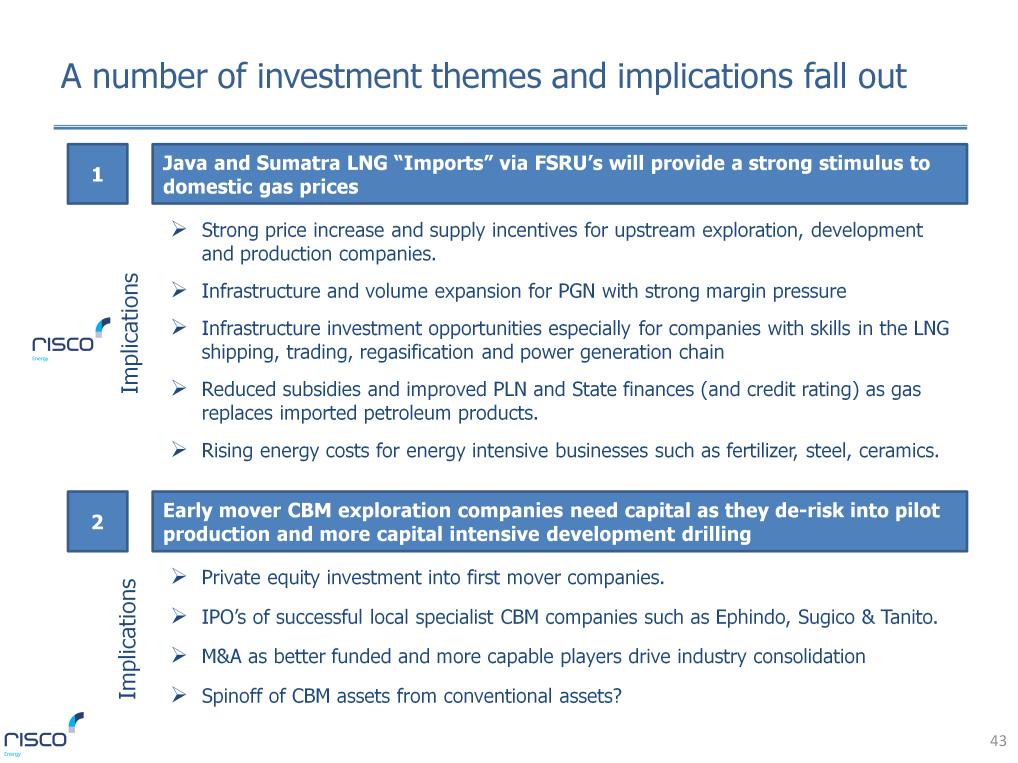

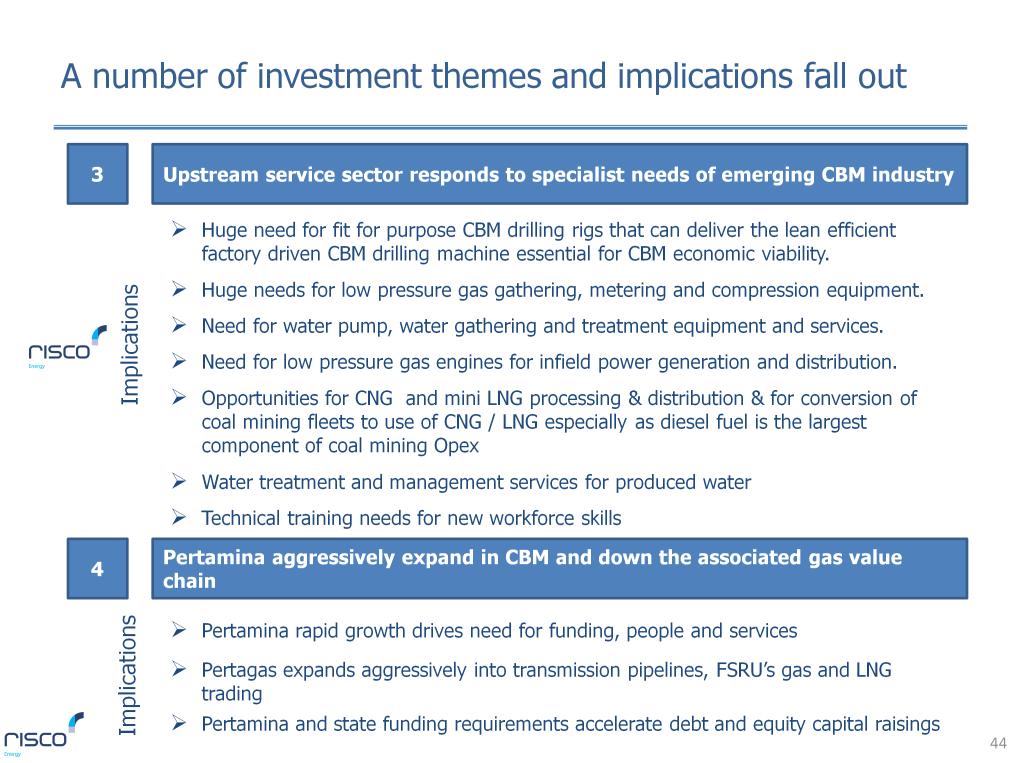

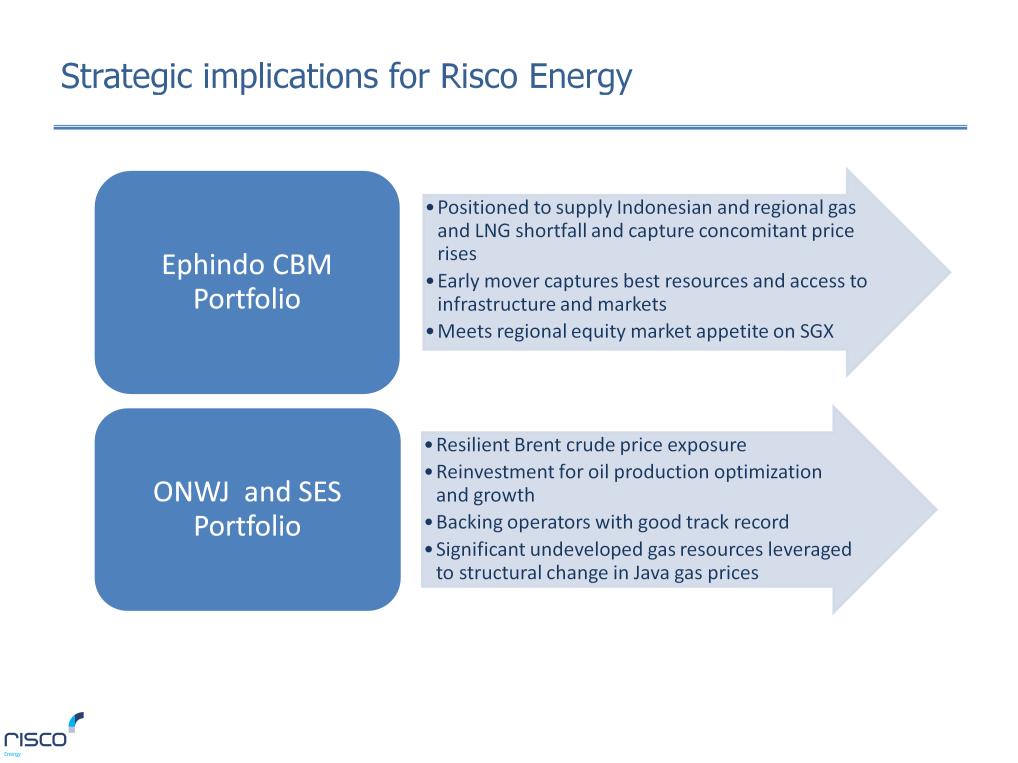

39 39

40 With Indonesian connected to regional markets by LNG and pipeline infrastructure, CBM could emerge as a major new gas supply source, material enough to impact local and regional markets Markets and route to market vary by basin. 40

41 Southeast Asia for example remains a net gas exporter although this is expected to change before 2020 as numerous countries commence gas and LNG imports. As a post 2020 supply demand gap opens up, CBM is well positioned to step into the gap. CBM from East Kalimantan is especially well positioned given the infrastructure is in place meaning the gas should be low on the supply cost curve 41

42 42

43 43

44 44

45 45

46 46