New Momentum for Biofuels

|

|

|

- Conrad Peters

- 5 years ago

- Views:

Transcription

1 New Momentum for Biofuels

2 A Perfect Day for Biofuels Demand Trends Oil consumption outpacing discovery China & India Consumer awareness Energy Security Insufficient domestic supply Oil supply primarily in unstable regions Sources: CERES, Milken Institute. Pressure to create a significant, renewable, domestic source of liquid fuels Supply Trends Nationalization of reserves High oil prices Peak production New technology improving efficiency of production Environmental Carbon emissions Offshore drilling Green legislation

3 Oil and biofuel: Two different business models Cost per unit Oil - High entrance barrier - High initial investment (for lease and facilities) - Low (and stable) marginal cost once scalability is achieved Cost per unit Biofuel - Low entrance barrier - Higher marginal cost even after scalability is achieved - Profitability is subject to uncertainty in raw material price - Possibility to reduce cost with future technology breakthroughs Units produced Units produced Source: Milken Institute.

4 First generation biofuel profile Feedstocks Corn, sugar, soybeans, used vegetable oil Companies VeraSun Process

5 Second generation biofuel profile Feedstocks Cellulose, l lignin, i non food crops Companies Verenium process Source: Verenium Corporation.

6 Third generation biofuel profile Feedstocks Organic wastes, municipal i solid waste, used tires and plastics Companies Coskata process

7 Fourth generation biofuel profile Feedstock: Algae Algae fuel process system design Companies Source: Auburn University, Algae as a Biodiesel Feedstock: A Feasibility Assessment.

8 Overview of the U.S. ethanol industry Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Total Ethanol Plants Ethanol Production Capacity (mgy) Plants Under Construction/ Expanding Capacity Under Construction/ Expanding (mgy) 1,702 1,749 1,922 2,347 2,707 3,101 3,644 4,336 5,493 7,888 10,569 11, ,778 5,636 5,536 2,066 States with Ethanol Plants Source: Renewable Fuels Association.

9 U.S. fuel ethanol production Billions of gallons Source: Renewable Fuels Association.

10 Biofuel mandates are ambitious United States 9 billion gallons blended in 2008 (6% of vehicle fuel consumption) and 36 billion gallons of renewable fuel to be blended with gasoline by 2022 (26% of vehicle fuel if fuel consumption remains consistent) (European Union 10% of vehicle fuel to be derived from renewable sources by 2020) Billions of gallons Total Renewable Fuel Standard Original RFS (2005) production: 10.6 billion gallons 2020 target: 36 billion gallons Source: Renewable Fuels Association.

11 Everybody embraces ethanol Big oil and refinery firms have stepped into ethanol market

")

12 U.S. ethanol biorefinery locations Biorefineries (200) Biorefineries under construction (11) Source: Renewable Fuels Association (As of January 2010).

13 Global venture capital and private equity investment in biofuels US$ billions Sources: New Energy Finance, Milken Institute.

14 Hybrid genetics & biotechnology have driven a five-fold increase in U.S. corn yield since 1940 Yield per harvested acre (Bushels per acre) Double cross Single cross hybrids Biotechnology / / / / / / / / / /04 Sources: USDA and Milken Institute.

15 Move biofuels across the value chain Supply side: Reducing costs and increasing access to finance -Venture capital -Equity financing -Revolving funds - Producer crop credits - Financial instruments to mitigate risks (e.g., insurance for producers, ethanol futures and swaps) Source: Milken Institute. Land Feedstock Process / refine Transportation Distribution Demand side: - Government mandates -RPF - Tax rebates - Infrastructure (e.g., installing pumps) -Consumer awareness

16 Funding challenges for biofuels Public grants and tax incentives Valley of death Valley of death Angel investor Venture capital Project finance Technology incumbent Seed/ Start-up Early stage Expansion Late stage Third generation - R&D - Initial investment in demonstration projects Source: Milken Institute. Second generation - Achieve commercial-scale operation - Bringing down costs - Further investment in facilities Funding challenges First generation - Scaling up - Further R&D - Upgrading pipeline - Increase market share - Mezzanine and bridge finance for IPO or M&A - Collapsing market/falling prices

17 A possible model for securitization Government programs provide loan guarantee for standardized loans Biofuel firms Greenie Mae securitizes standardized loans Possible investors First generation biofuel Second generation biofuel Third generation biofuel Assetbacked securities pool Pooled cash flow Hedge funds Pension funds Sovereign wealth funds Individual investors X generation biofuel Source: Milken Institute.

18 A green bank End investors: Purchase secured bonds Pool of standardized loans Green b ank: A federal agency that provides loan guarantees Small and medium biofuel firms: With the option of buying back debt at below par from the bond market Green lending institutions: originate and service loans, and take first loss Source: Milken Institute.

19 Technology to bring down costs to biofuel consumers Improved yields Improved and more affordable enzymes Improved pipeline and other infrastructure Modified harvesting and process mix Adding pumps to the stations

20

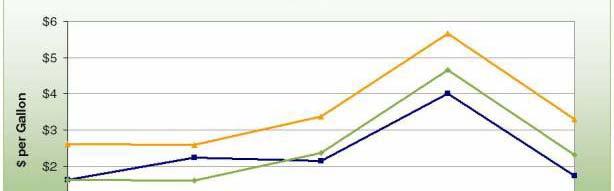

21 U.S. oil price reached historical high in 2008 US$ per barrel Source: Bloomberg.

22 2008 and 2009 world ethanol production estimates Country Millions of Gallons USA 9,000 10,600 Brazil 6,472 6,578 European Union China Canada Other Colombia India Australia Total 17,245 19,530 Source: F.O. Lichts, *Renewable Fuels Association.

23

24 Global private investment in biofuels US$ billions Venture capital/private equity Funds raised via securities offerings on public market Direct investment (est.) Sources: New Energy Finance, Milken Institute. Note: Government grants and subsidies and corporate R&D not included.

25 Clean energy stimulus by country 2009 US$ billions Sources: New Energy Finance, Milken Institute.

26

27 Slides from Desmond King

28 World energy consumption Million tonnes of oil equivalent per year 12,000 10,000 8,000 Non-OECD 6,000 4,000 OECD 2, Source: IEA World Energy Outlook 2008.

29 Where will the supply come from? Biomass and waste 10% Hydro 2% Nuclear 6% ,013 Mtoe* 16,789 Mtoe* Other renewables 1% Coal 27% Biomass and waste 10% Hydro 2% Nuclear 6% Other renewables 2% Coal 29% Gas 21% Source: IEA World Energy Outlook 2009 reference case. Note: Mtoe represents million tons of oil equivalent. Oil 33% Gas 21% Oil 30%

30 Where will the supply come from a 450 ppm carbon scenario? Biomass and waste 10% Hydro 2% Nuclear 6% ,013 Mtoe* Other renewables 1% Coal 27% Biomass and waste 14% Hydro 3% ,390 Mtoe* Other renewables 5% Coal 18% Gas 21% Source: IEA World Energy Outlook ppm case. Note: Mtoe represents million tons of oil equivalent. Oil 33% Nuclear 10% Gas 20% Oil 30%

31 Primary biofuels challenges Scalability Sustainability Cost Policy Source: Chevron. Feedstock: Can we continuously produce the tens of millions of tons of biomass required to produce biofuels at an industrial scale? Fuels: Can we produce enough to make a difference? Can we address environmental and socio-economic issues of biomass use? Can we drive down the costs of cultivating, harvesting, and transporting biomass? Can we economically scale up the conversion technology to an industrial size? Can we reduce costs by producing fuels compatible with existing infrastructure and vehicles? Will policymakers set realistic goals that allow for enough time for technology to advance, consider all of the challenges, and allow the marketplace to choose winners and losers?

32 Fundamentals of the energy system World s largest supply chain Highly integrated infrastructures Very long-lived assets Business is a complex blend of economics, politics, technology, and the Capital- and technology- intensive environment Integration 1 Explore/ Develop 2 Produce 3 Transport 4 Refine 5 Store/Dist 6 Deliver 7 Market Add value at each step Source: Chevron.

33 Scale, time and capital Scale Time Capital Global fuel volume Manufacturing and Today s requirements infrastructure $10+/BBL reserves Takes decades to $40,000+/daily BBL for develop at scale; lasts fuel manufacturing generations $50,000 to Major oil fields 100,000/daily BBL for Can be decades from unconventional fuel World s largest supply chain 40,000 gallons per second ½ gallon for every human, every day 1 trillion gallons/year Source: Chevron. discovery to full production Technology Average >15 years from invention to largescale deployment manufacturing Future estimates call for $20+ trillion in investment over the next 30 years

34 Research to markets 10+ years Laboratory bench Pilot plant Field demonstration at scale Full-scale production infrastructure $ millions $10 s millions $100 s millions $billions Source: Chevron. R&D Validate systems integration Validate scale-up and continuous operations

35 Next-Generation Biofuels Value Chain Feedstock Technology Product Objectives: Develop cost-advantaged access to scalable, sustainable supply Main challenges: Source: Chevron. Scale and economics Sustainability Create technologies to bring biofuels to industrial scale Develop finished fuels and blendstocks that meet consumer expectations Meet consumer performance Laboratory proof of concept expectations Commercially viable scale-up Compatibility with storage and distribution infrastructure Compatibility with vehicles

36 Generation 3: Biohydrocarbons Ligno-Cellulosics Ethanol Incompatible with existing infrastructure Source: Chevron. Lipids Biohydrocarbons Compatible with existing infrastructure

37 Market adoption of transportation fuels Provide equal or improved driving performance, safety, reliability and comfort Be competitively priced Be convenient, readily available Increasingly, have lower carbon footprint Be economical at large scale Source: Chevron.

38 Alan Boyce slides

Economical Low production cost")

39 South America offers the most competitive conditions for food & renewable sustainable production Natural conditions Abundant water Fertile soils Mild temperature Land availability South America Strengths Human & Technology Cutting edge Technology Mechanization Management skills Environmental sensitiveness Brazil and Argentina are Top Food & Renewable Exporters (sugar, ethanol, corn, soybean) Economical Low production cost Cheap land Good infrastructure Vertical integration Geopolitical Private land Food surplus No trade barriers Corporate farming Good quality farmland is globally limited Source: Atlas of Global development, World Bank, 2008

40 Biofuel can be globally produced without decreasing land availability for crops The right crop in the right place: changing from grassland into sugarcane Source: IBGE. Elaboration: UNICA. Millions of hectares (2007) Brazil Total arable land Total Crop Land 76.7 Soybean 20.6 Corn 14.0 Powercane 7.8 Powercane for ethanol Orange Pastures Available area There is room for Cattle to strongly increase its efficiency (operational, crop productivity, feedlots) 1%

Complementary production: ethanol + sugar + bioelectricity Powercane (Brazil) Beet (EU) Powercane (India) Corn (USA) Cassava")

41 Renewable energy and food can complementary be produced without affecting food supply High crop yields means higher biofuel production per unit of land Yields (M 3 /hectare) Complementary production: ethanol + sugar + bioelectricity Powercane (Brazil) Beet (EU) Powercane (India) Corn (USA) Cassava (Thailand) Wheat (EU) Source: IEA ('05), Unica ('08) The higher crop productivity, the higher biofuel production and the better use of land Bioelectricity's Strengths Source: UNICA Synergy with hydro production (dry season) Carbon Credit feasibility Use of straw could increase its potential

42 Powercane is the most efficient and clean feedstock for ethanol production Energy Bala ance GHG Emission ns Reduction Different Feedstocks Comparison % % Powercane Corn Gasoline Source: IEA ('04), Unica ('08), Macedo, I ('04) Energetic Balance (MJ/ha) CORN POWERCANE Agricultural operations 1,083 4,012 Transportation ti , ,107 Inputs: fertilizers, consumables, seedlings, equipment 10,849 9,988 Total agricultural production 14,829 18,107 Processing Energy - - Inputs: chemicals, lubricants, heat & electric 31,055 1,653 Equipment, buildings, facilities 1, Total processing 33,031 2,032 Total energy consumption 47,860 20,139 Ethanol 92, ,863 Co-products (WDG, Bagasse) 36,803 15,1541 Bioelectricity - 7,129 Total energy production 129, ,146 Energy Balance 81, ,007 Energy Ratio Portable Fuel Ratio More important than the Energy Balance (heat) is the Portable Fuel Balance!

43 Best practices as No Till should be applied to achieve sustainable biofuel production 60 No-till Benefits Improves water efficiency Reduces erosion risk Increases organic matter Decreases use of pesticides Improves soil fertility Reduces CO2 emissions Higher and stable yields & lower costs year by year Decreasing fossil fuel usage Improving water storage capacity Water storage ca apacity (in/8 in) NO TILL TILL Decreasing pesticides usage Carmen & Abolengo farms (Humid Pampas) 4,0 8,0 Liters per hectare Convetional Tillage No Till No-till increases land productivity and returns over time Spray per hectare 3,0 2,0 1,0 - Spray/hectare Liters/hectare ,0 6,0 5,0 4,0 3,0 Liters per hectare

44 The convenient Generation 2.5 of biofuels is already on stage performed by efficient operations A NEW MODERN MILL PROJECT REQUIRES 8 YEARS TO ACHIEVE FULL CAPACITY (BIOLOGICAL PROCESSES) K Hectares Sugarcane: Production & Area Evolution Total area (hectares) Total Production (Tons) 4.5 Start Milling hectare of Sugarcane (1) Star Planting Sugarcane = 75 tons Ethanol = 4.3 m3 Sugar = 4.1 tons Power (2) = 4.5 MWh Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 (1) Includes replanting area; average of 7 years cycle; 60% ethanol 40% sugar (2) Does not consider use of straw Need to integrate biofuels industry around the world Infrastructure should be fixed and suited for biofuels - MM Tons

45 Steve McCorkle

46 Corn price, U.S. ethanol production

47 Soybean price, U.S. biodiesel production

48

49

50

51 - Agricultural crop residues could produce 33 billion gallons of cellulosic ethanol - Animal* and process wastes could produce 24 billion gallons of renewable diesel * Animal wastes are the #1 contributor to US waterway pollution (EPA)

52 - Agricultural Wastes: 19% of US fuel demand with negative GHGE, low use of resources, no additional crop land, technology ready, no impact on food supply

53 Joel Velasco slides

54 About UNICA UNICA is the leading sugarcane industry association, representing +120 producers and mills in Brazil Responsible for 60% of all ethanol and sugar production in Brazil Emerging as a leader in the generation of bioelectricity already meeting 5% of Brazil s electricity demand International presence, now in Washington & Brussels, to engage in constructive dialogue Source: UNICA.

; Historical carbon budget of the Brazilian ethanol program in Energy")

55 What we make with sugarcane Sugar 30 million tons Ethanol 7 billion gallons Electricity 16,000 GWh 550 M MT Source: UNICA; Ministry of Mines and Energy BEN (2008); Historical carbon budget of the Brazilian ethanol program in Energy Policy, Volume 37, Issue 11, November 2009, Pages Sugarcane is Brazil s #1 source of renewable energy and the second overall energy source behind petroleum. 600 million tons of CO 2 emissions avoided thanks to the use of ethanol since 1975.

56 Where sugarcane is grown Sources: UNICA, NIPE-Unicamp, IBGE, CTC, CanaSat, see South-Central region represents about 90% of sugarcane harvest

57 A WORLD OF SUGARCANE 100 countries could supply biofuels to 200 nations, while currently 20 oil producers provide fossil fuels today. Source: British Sugar

58 Current and future products Source: UNICA.

59 Clean, affordable, secure yet unavailable Source: UNICA.