Climate Change, Risk Management, & Coming Attractions in Energy Regulation. Miles Keogh, Director. NCSL August Atlanta, Georgia

|

|

|

- Albert Chambers

- 5 years ago

- Views:

Transcription

1 Climate Change, Risk Management, & Coming Attractions in Energy Regulation Miles Keogh, Director NARUC 1101 Vermont Ave. Grants NW & Research Suite 200 Washington DC NCSL August Atlanta, Georgia

2 Disclaimer NARUC is the association of State Commissions. These are opinions, not NARUC policy, nor policy of its members. There are 50 states + DC, with over 200 Commissioners. Everything will apply to some state, but there are exceptions to everything in here in some state too. 2

3 Agenda Shifts: Resource shifts Technology shifts Market and regulatory structure shifts Known unknowns Unknown Unknowns The Game Paths out of the Game What Comes next 3

4 The Theme: We re Probably Wrong About Almost Everything (But Don t Panic!) 4

5 50 states

6 Varied providers and retail electricity prices (2010)

7 Billon kilowatthours How should we meet growth? Recession Impact? Sources: U.S. Department of Energy, Energy Information Administration, Annual Energy Review 2006 and Annual Energy Outlook 2008 Early Release *Electricity demand projections based on expected growth between

8 Wind Solar Source: Coal Foundation. Shale Gas Coal

9 Map of the Fleet

10 MATS-affected plants (ca. 2012)

11

12

13 Estimate Coal Capacity "At Risk" (GW) Adding Rules Increases The Number of At-Risk Plants CSAPR and MATS CSAPR, MATS, CCR, 316(b) MATS Only 60 CSAPR Only Ash Only 316(b) Only CSAPR, MATS, 316(b) CSAPR, MATS, CCR, 316(b), CO 2

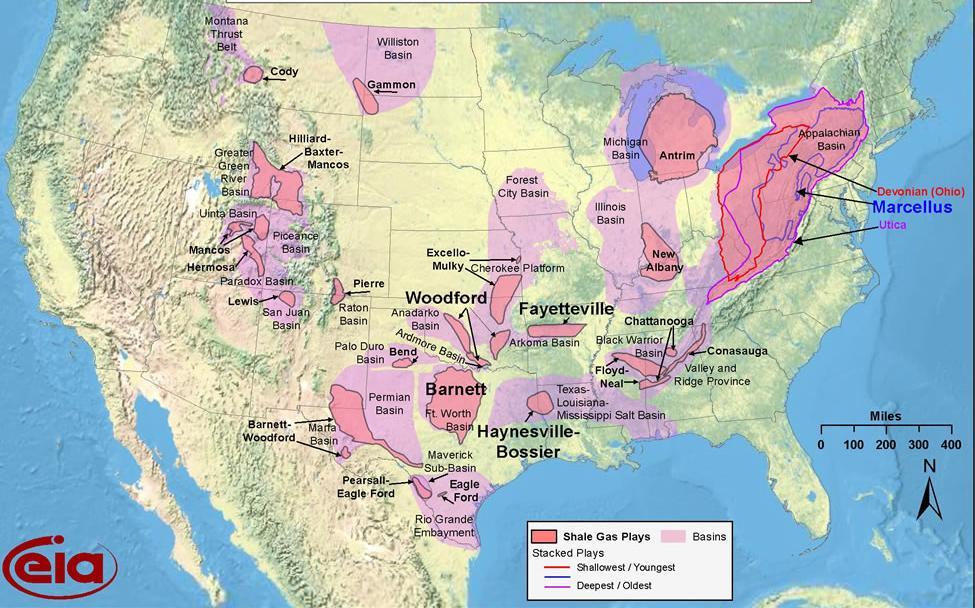

14 Shale Gas: The Game Changer

15 What Will The Price Be?

16 Clean Air Act Sections 111(b) and 111(d) overview Under Sec. 111(b), EPA is required to establish performance standards for new and modified sources of Greenhouse Gases. March 27, 2012 proposed standards for GHG from new electric power plants 111(b), New proposal due in Sept. Under Sec. 111(d), EPA is required to set standards for existing stationary sources. Proposed rules will be issued June 2014, with final rules June 2015.

17 It s Chemistry: Combustion means releasing CO2

18 Advanced Turbines Options for Gas Plants How to reduce GHGs CCS Transmission Work with neighbors Volt/Var System Efficiency Lower GHG (gas, CHP, biomass, other) New Supply Replace Repower Replace Options for Coal Plants Heat Rate Credit Trading Energy Efficiency Negawatts Distributed Generation Zero GHG (nuke, wind, solar, geothermal, other) Demand Response

19 Federal Climate Policy Lags Action by States Source: Pew Center on Global Climate Change 19

20 NARUC Projects, EPA outreach, and the Labs EPA Office of Air and Radiation has provided grant funding to help Regulators understand and proactively address the EPA regulations. National dialogue (the 3N s meeting, the National Council on Electricity policy) State and regional dialogue (such as this one) Labs 20

Coal (non-mats) Gas Nuclear Wind Built")

Retire (market replacement ) $?")

21 The Labs TAKOMA PARK 300 MW 15% 20% 5% Generation Portfolio 30% 30% Coal (MATS) Coal (non-mats) Gas Nuclear Wind Built in 1969 Proximity to gas line: 15 miles Fuel: bituminous coal Pollution control: electrostatic precipitator Coal Rank Switch, Add ACI & Baghouse Add FGD & Baghouse Replace / Repower (Gas) Retire (market replacement ) $? $264 M $330 M $300 M

22 The way out of the game Everything we know now may be wrong in 5 years Minimize your regrets Use planning to anticipate the future Diversity of resources Hedges, where needed Transparent processes that uncover risks Leverage resources that do well in all futures 22

23 Known and Unknown Unknowns Prices, and success of the gas, coal, nuclear, and renewables industries Disruptive technologies and storage Does data change everything? Is there a new business model? Who would use it? Qui Bono? Any of these could make things easier or harder 23

24 Everything We Know Today Could Be Wrong Regulators care about resource adequacy above all, demand is growing & new supply is tough to get. The golden era of declining prices is probably over. Maintenance and planned expansion investments are worth 2x the existing system. Climate is a Known Unknown There is almost certainly a large Unknown Unknown out there. Is the future one of massive stranded investment? We cannot solve the most serious problems using the same thinking that created them. - Albert Einstein 24

25 Conclusions State regulators play a broad role with wideranging responsibilities Regulatory policy is an important driver for what the grid looks like Technology is shifting, but maybe not the technologies we think The hybrid of markets and vertical integration are here to stay Climate caps are out, but we re still decarbonizing With some huge spending coming, we need to make as many no-regrets choices as possible. 25

26 I Will Now Confront Your Most Challenging Questions! Or! Later if you prefer! Miles Keogh,