Dirk Tretter, SINOSTEEL SHANGHAI STEEL SERVICE CO., LTD. Chinese Economic Policy and Its Implications for the Galvanized and Coated Steel Industry

|

|

|

- Angela Briggs

- 5 years ago

- Views:

Transcription

1 Dirk Tretter, SINOSTEEL SHANGHAI STEEL SERVICE CO., LTD. Chinese Economic Policy and Its Implications for the Galvanized and Coated Steel Industry

2 Company Introduction SINOSTEEL SHANGHAI STEEL SERVICE CO., LTD is a Joint Venture of BENGANG STEEL PLATE CO., LTD One of the largest boutique plate production enterprises in China with an annual capacity of 20 million tons. SINOSTEEL IRON STEEL CO., LTD The biggest steel service company in China with a turnover of more than 21 billion EURO. SHANGHAI HUALIAN TIANMAI COATING STEEL CO., LTD The biggest HDG retailer in Eastern China. It is the general agency of TAGAL and BX POSCO in China.

3 Products & Business PCM/VCM Metal-Metal-Sandwich Service Centers Trading House

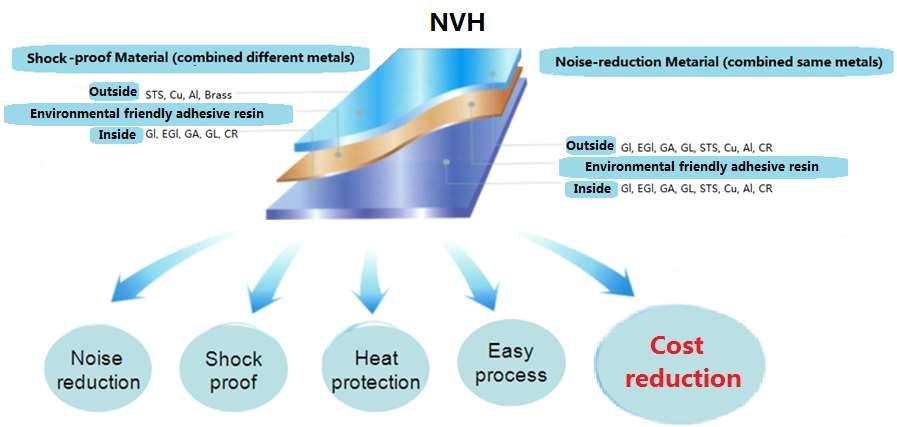

4 New Development: Metal-Metal-Sandwich Example: STS(0.2) + HDG(0.8)

5 - What is the demand like in the Asian galvanized and coated steel market? Main Asian Economies Steel Consumption (Source: The World Steel Association)

6 Apparent Steel Consumption and Forecast of the Main Economies in the World (Source: The World Steel Association)

7 During the last 9 years, China s production of HR, CR, GI and CC increased 265%, 350%, 502% and 435%. China s Flat Steel Production (Source: China National Statistics Bureau)

8 China Galvanized Steel Industry Development (Source: China Iron and Steel Association)

9 China Color Coated Steel Industry Development (Source: China Iron and Steel Association)

10 According to data from Chinese steel institutions, by the end of 2013, there were in total 324 HDG lines in China, with a designed total capacity of around 60 million tons (average 185,000!).

11 China GI s Production, Capacity, Capacity Utilization and Apparent Consumption (Source: China Iron and Steel Association)

12 China CC s Production, Capacity, Capacity Utilization and Apparent Consumption (Source: China Iron and Steel Association)

13 Color coated sheet for home appliance Chinese market has a great development space on CC for home appliance. In developed countries, CC accounts for 88% of the coated products used on home appliance. In China, this ratio is only about 8%~10%. Rest is occupied by powder painting and expensive VCM. Color coated sheet for elevator The demand in elevator industry of color coated sheet is also rising. In the past, the elevator panels were made of stainless steel plate. Now the color coated sheet is widespread used instead of stainless, because of better cost performance. At present, China has already become the world's largest new elevator market and the largest elevator producer. The annual output value will reach 16.3 billion USD. Color coated sheet for construction In recent years, color coated sheet have gradually replaced wood and other materials, are widely used in factories, warehouses, villas, large stadiums, cultural facilities, high-end architectural engineering.

14 The Usage Amount of GI in Each Home-appliance (Source: China Household Electrical Appliance Association)

")

15 China home appliance production in 2014 Q1 (Source: China National Statistics Bureau)

16 Automotive industry is also a main GI consumer. The Chinese car production shows a significant increase in recent years. Chinese Vehicle Industry (Source: China National Statistics Bureau)

17 The Trend of GI s Average Price in China Market (Source: China Iron and Steel Association)

18 - How have changes in governmental policy affected trade in and out of China China s Imports / Exports of Steel Mill Products (Source: China National Statistics Bureau)

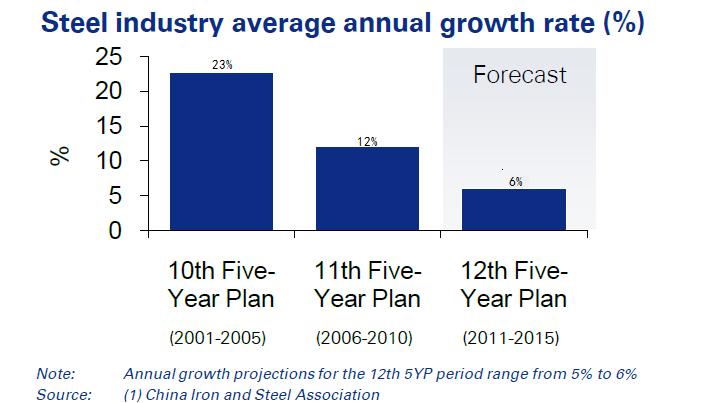

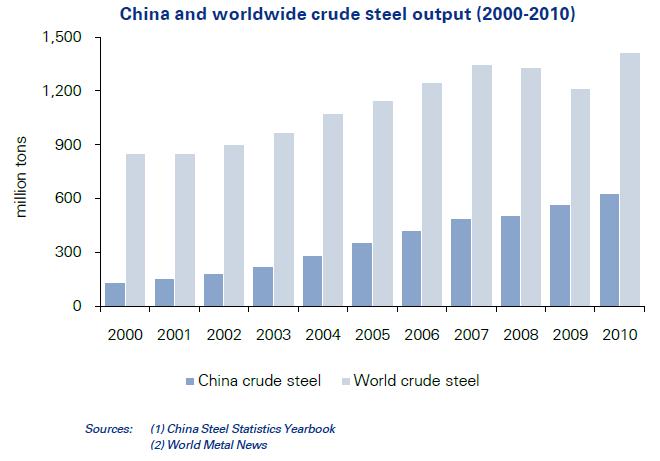

19 China s 12 th Five-Year Plan: Steel

20

21

22

23

24 - A large part of pickling, galvanizing and coating industry is not integrated in the steel makers, but separate processing industry - This processing industry is largely private-owned, highly capital intensive on a high volume - low margin concept - The industry is affected by macro measures, for example financial (QE, interest rates, exchange rates) or environmental (highly restrictive recently) - In view of large over-capacities, new production/processing licensing for sheet steel has been elevated from local government to central government authority

25 - Different from primary carbon steel products, coated/galvanized products are still viewed as valueadded products - The government encourages exports of value-added products - Should this view ever change, there are possible measures like reducing the VAT-refund upon export, which would have an immediate, direct impact on pricing and competitiveness

26 - On the import side, there have been continuous large scale imports of CRC from neighboring countries for coating and subsequent re-export to the respective neighboring countries - Contrary to the straight export of coated/galvanized product, this processing trade is now being actively discouraged by fiscal measures, for being low value added business - We may conclude, that the current view of exports of coated/galvanized products being value-added business is a borderline view, that may be subject to change in future

27 - Is consolidation occurring as a result of huge overcapacity? China's steel industry will continue to see an increasing amount of consolidation in the years to come to get through the tough times. When global steel markets were booming most mergers were pushed forward by government efforts in restructuring the industry. Now that markets are gloomy it is small players that are taking the initiative in realigning.

28 - In general, the definition of what is over-capacity is a thorny issue - While in the EU an average utilization rate in the industry of less than 85% indicates over-capacity, the Chinese may take a different view (65%) - Therefore, we prefer to refer to undisputable overproduction, detaching the issue from whatever the capacity utilization rate may be - In previous years the government induced M&A in the steel industry

29 - This, however, in most cases changed only ownership, but did not resolve fragmentation - The current official view is to let the market resolve the issues - It means the government may allow even larger scale bankruptcies - In the past 2 years (more than?) 30% of companies in the steel distribution & processing industry went out of business

30 - How much of this refers to pickling, galvanizing and coating is unclear, the trend in the private sector to exit the market is continuing - State-owned processing capacity, however, is highly unlikely to be reduced

31 - How can the issue of fragmentation be overcome in such a large country? - As mentioned above, the government wants the market to resolve the issues in the steel industry - Additionally, licensing of new capacity is being handled restrictively - Old capacity is subject to intense scrutiny by environmental authorities, who wield much more power than before - Banks are forced to implement a higher level of risk management

32 - Loans and investments for steel and steel processing industries are currently viewed as highly risky - This restricts access to new loans for related enterprises and makes old loans much more expensive - the result is the current situation, low margin - high volume is no longer possible, while low volume-high margin is not (yet) feasible - Fragmentation may be reduced by this - But, no matter what happens to the industry as a whole, China still is a huge country, and we will always deal with a large number of enterprises

33 - Where will demand be focused in Asia in the coming years? Which countries and which applications?

34 Steel Market in India According to the Institute for Steel Development and Growth, the Indian urban population is expected to reach 600 million by 2030 from the current level of 400 million. Rising middle-class urban population boosts demand for automobiles, white goods and other consumer durables, which leads to higher steel consumption per capita. The country s steel consumption growth has an elasticity of about 1.1 to GDP growth. According to World Bank, the Indian economy is forecasted to grow at 4.7% in 2014, which means steel demand is likely to grow by 5.2% in 2014.

")

35 Steel Market in ASEAN The Southeast Asian is also an unnegligible market, which has a rapid annual growth of steel consumption. Apparent Steel Consumption of ASEAN (Source: World Steel Association)

36 In recent years, because of rapid development of the construction industry, ASEAN countries have a growing demand of building materials. Steel for construction has a great development potential. Comparing with developed economies, like EU, USA and Japan, the construction steel has a large proportion in ASEAN s steel consumption. Construction Steel Consumption of Total (Source: Southeast Asia Iron & Steel Institute)

37 The Chinese economy is likely to result in a policy-driven soft landing. The GDP growth will be around 7.5% this year, it will further decrease to below 7% in the coming years.

38 Soft Landing: Chinese economy peaked at 14.2% in In 2013, the growth of Chinese GDP was 7.7%. The forecast for 2014 is 7.5% with continued downward tendency. China s GDP Growth (2002~2013) (Source: China National Statistics Bureau)

39 Upside chances include fiscal stimulus in form of infrastructure investments, especially in railway transportation, and the export sector. China will be pursuing quality in the ongoing process of urbanization, which will see the urbanization rate of the world's most populated country from slightly above 50 percent to over 70 percent. The disposable income of the population is significantly increasing, especially in the cities.

40 Downside risks with the potential to jeopardize economic stability consist of excess capacity in the entire heavy industrial sector, debt overload among companies and local and provincial authorities (around 240% of the GDP, half of that is corporate debt), the real estate bubble and possible geopolitical conflicts with other Asian countries. Nevertheless, the Chinese economy will not likely face a hard landing. This is because the economy (including the banking sector) remains heavily managed by the central government, which has many tools at its disposal, fiscal as well as monetary.

41 Thank you! If you have any queries, please contact without any hesitation.