Downstream Development Potential for Utica Shale

|

|

|

- Egbert Mark Horn

- 5 years ago

- Views:

Transcription

1 Downstream Development Potential for Utica Shale Paul Boulier Team NEO April 7, 2014 Presented at the Utica Capital Series Sponsors-Canton Regional Chamber & Huntington Bank

2 Today s Objectives Overview the many value chains that come from shale (Power,Fuel, Downstream ) Show the tremendous scale and speed of investment going on in the Downstream Highlight Our Regional strengths and show potential opportunities Stimulate thinking, create readiness, drive dialogue and hopefully spark ideas 2

3 3

4 4

5 5 Opportunity:

6 6

,")

LPG, mix of gases (propane, butane,")

7 Shale Gas Yields Many Products Power Consumer Products Medical Devices Packaging NGLs Ethane Propane Butane Pentane C5+ Injection Molding, Extrusio Blow Molding, etc. Chemicals & Plastics Further Processing Fuel (CNG, LPG, LNG*) Adhesives Paints & Coatings Household Cleaners *CNG, compressed Natural Gas (methane), ~3,000psig LNG, Liquified Natural Gas (methane), (-260F, liquid) LPG, mix of gases (propane, butane, propylene, butylene, etc.) 7

8 Power from Shale Gas * Low-Cost Power E&P Transmission Midstream Storage Derivatives Chemicals & Plastics End Products 8 *Source: Barry Stevens

9 Fuels from Shale Gas* Low-Cost, Plentiful, Local, Efficient, Lower C-emissions E&P Transmission Midstream Storage Derivatives Chemicals & Plastics End Products 9 *Source: Barry Stevens

10 NGLs Ethane Propane Butane Pentane C5+ Chemicals & Plastics 10

11 NGLs Ethane Propane Butane Pentane C5+ Chemicals & Plastics The value which is being unlocked from chemicals and Plastics derived from shale gas has transformed our global competitive position 11

12 Chemicals and Plastics from Shale Gas to Finished Products Plus these other value chains: Methanol Fuel & Chem. Ammonia Fertil. & Chem. Propane Propylene Butane Butenes Pentane Various Chem. C5+ Fuels, diluent Low energy costs, improved transportation & logistics, and lower chemical feedstock improves our ability to compete globally E&P Transmission Midstream Storage Derivatives Chemicals & Plastics End Products 12

13 Examples of Other Derivative & Plastics Value Chains 13

14 1. Energy & Fuel 2. Derivatives & Plastics* *Plus Other Value Chains 3. Infrastructure Opportunities: Pipe, pumps, compressors, fittings, tanks, instruments & controls, consumables Construction, housing, utilities, water & treatment, road & paving, support industries Shale Development provides a solid Portfolio of Opportunity -Plays to our Regions strengths in Advanced Materials -Strong Proximity to Domestic Market and Converters -Springboard on our established Export Capabilities 14

15 15

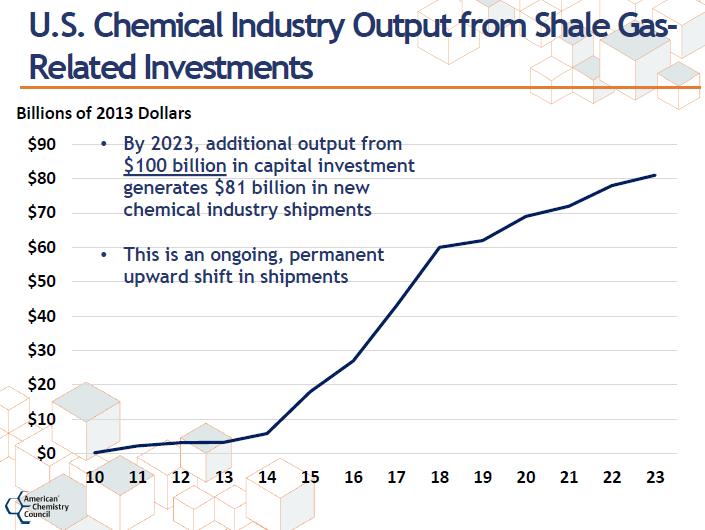

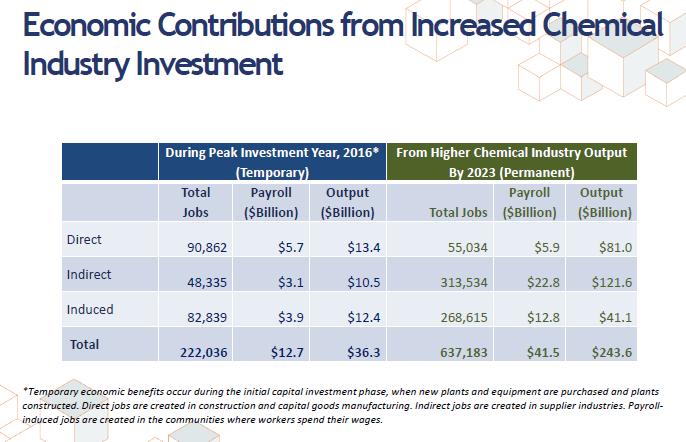

16 ACC Shale Gas Study* Survey of ~100 announced projects through the end of March, 2013 These Incremental Investments from Shale total $72B over the period Most projects geared to expand capacity for ethylene, ethylene derivatives (PE, PVC, etc.), ammonia, methanol, propylene, and chlorine Much of this oriented towards products geared to export market These investments could result in $67B in new chemical industry output! Source: American Chemistry Council, Shale Gas, Competitiveness, And New US Chemical Industry Investment: An Analysis Based on Announced Projects, May 2013.

17 Incremental US CAPEX through 2020 from Shale Gas* Supply-side estimates only (Demand-side effects excluded) $B USD Assumptions Includes: -New Greenfield Crackers -Expanding capacity for efficiencies -New Product Capacity -Replacement existing equipment -Operational Improvements -Energy Savings -Health & Safety -Environmental Production & Other How will Global Market Dynamics influence investment here? (Pharmaceutical not included) Source: American Chemistry Council

18 Incremental US CAPEX through 2020 from Shale Gas* $B USD How will Global Market Dynamics influence investment here? Increase in CAPEX estimates from March 13 to Feb 14: >$28B incremental 0 Source: American Chemistry Council

19 New Chemical Industry Capital Investment from Shale, , by Region* Ohio Valley 13% Gulf Coast 78% Midwest 8% Other 1% *Source: American Chemistry Council Ohio Valley =OH, PA, WV

20 New Chemical Industry Capital Investment from Shale, , by Chemical Segment* Plastic Resins 22% Other 5% Bulk Petrochemicals 55% Fertilizers 14% Inorganic Chemicals 4% *Source: American Chemistry Council

38% Building Construction 10% Engineering Services 9% Electrical 4% *Source: American Chemistry Council Process Instrumentation 8% Piping & Valves 5% Major Process Equipment (pumps,")

21 New Chemical Industry Capital Investment from Shale, , by Asset Type* Other Non- Residential Construction (erection of equipment, piping, etc.) 38% Building Construction 10% Engineering Services 9% Electrical 4% *Source: American Chemistry Council Process Instrumentation 8% Piping & Valves 5% Major Process Equipment (pumps, pressure vessels, heat exchangers, etc.) 26%

22 22

23 23

24 Ohio is all about Manufacturing OH ranks 1,2,3 in almost all categories of manufacturing Leading industries and annual shipments*: Iron & Steel mills & Ferroalloy-$14.6B Petroleum Refineries-$12.5B Aircraft Engines & Parts-$8.8B Plastics Products Manufacturing-$8.0B Soap and Cleaning Compounds-$6.8B Motor Vehicle Metal Stamping-$6.5B OH ships >20% of all US production in the following categories*: Rubber Products Structural Clays Glassware Manufacturing (pressed/blown) Iron & Steel Pipe & Tube Custom Metal Roll Forming & Rolling Mill Equipment Machine Tools Motor Vehicle Metal Stamping Aircraft Engines and Parts *Ohio Manufacturers Association, 2012

25 25 Our Region is well-positioned to leverage resources from Shale Gas

26 26 Our Region is well-positioned to leverage resources from Shale Gas

27 Our Region is well-positioned to leverage resources from Shale Gas 27

28 So what does 2020 look like? Midstream, Storage, Logistics, Barge/Rail/Road--Perpetual Expansion Multiple CNG stations across the Region LNG facility(ies) in evaluation/construction (Lake Erie?) Refineries expanding (much of the NGL output going North, East, South) Fuels (Marathon, others) Numerous Petchem/Plastics facilities in PA, TX (Chevron, $6B; XOM; Dow) Derivative Chemical and Plastics plants running in our Regions NOVA Chemicals (happening now; Utica ethane to Sarnia=polyethylene) Odebrecht/Braskem (announced ethane cracker, 3 PE lines, WV; Antero ethane supplies 50% of need) Shell (still evaluating; in March local govt discussing roads, power, rail/dockage) Aither (?; announced cracker and 2 PE units) Advanced Materials companies expanding-to supply Domestic/Export markets Compounders expanding-production & Innovation capabilities Converters/Assemblers/Major Tier Players expanding 28

29 Our Region s Opportunity in Downstream Logistics & Transport Improved Manufacturing Efficiency OHIO s Advantages From Shale Proximity To Markets Skilled Labor, Higher Ed Strong Export Potential 29

30 Our Region s Opportunity in Downstream Cheap, plentiful electricity Tight, aligned Supply Chain Derivative Chemicals Plastics, Rubbers, Metals Converted Products Improved Manufacturing Efficiency Logistics & Transport OHIO s Advantages From Shale Road Rail Sea Air Proximity To Markets 50% of Consumers Within 500 mi: Auto Aviation Medical Cons. Products Industrial Value Add Innovation IP Creation& Protection Skilled Labor, Higher Ed Strong Export Potential Established Infrastructure 30

31 Our Growth Challenge New Shale Resources = tremendous potential to fuel a Manufacturing Renaissance Manufacturing Efficiency Labor Competitiveness Competition for this resource-regionally & Globally Our Infrastructure foundation is sufficient to be Early Mover (global perspective) Gaps in pipelines and NGL processing being filled--in a big way Derivative Chemicals and Plastics present great potential rewards for our Region already an established major player Substantial Change Management Initiative For America and Our Region 31

Gaps in pipelines and NGL processing being filled--in a big way Derivative Chemicals and Plastics present great")

32 Our Growth Challenge New Shale Resources = tremendous potential to fuel a Manufacturing Renaissance Manufacturing Efficiency Labor Competitiveness Competition for this resource-regionally & Globally Our Infrastructure foundation is sufficient to be Early Mover (global perspective) Gaps in pipelines and NGL processing being filled--in a big way Derivative Chemicals and Plastics present great potential rewards for our Region--an established major player Substantial Change Management Initiative For America and Our Region Use it or Lose it 32

33 Fortune favors the prepared mind. Louis Pasteur 33

34 The secret of success is to be ready when your opportunity comes. Benjamin Disraeli Fortune favors the prepared mind. Louis Pasteur 34

35 The secret of success is to be ready when your opportunity comes. Benjamin Disraeli Improved Manufacturing Efficiency Skilled Labor, Higher Ed Logistics & Transport OHIO s Advantages From Shale Proximity To Markets Strong Export Potential Fortune favors the prepared mind. Louis Pasteur Opportunity is missed by most people because it is dressed in overalls and looks like work. Thomas A. Edison 35

36 Our Region s Shale Opportunity 36

37 Our Region s Shale Opportunity Or 37