|

|

|

- Ruth Victoria Simmons

- 5 years ago

- Views:

Transcription

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37 Setting Executive Compensation Judith E. Stein Quatt Associates, Inc.

38 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 2

39 Developing a Compensation Philosophy A compensation philosophy outlines the values, principles, guidelines and goals of the organization s compensation program. It applies to the entire organization not just its executives It is approved by the Board and ideally developed by a small task force of the Board or Compensation Committee in collaboration with the Chief Executive 3

40 Developing a Compensation Philosophy It should include: The objectives of the compensation plan, for example: To achieve a high level of excellence in fulfilling our mission and reward our people for their hard work, their commitment in support of the organization s values and goals, and their contributions in achieving them or To support the recruitment and retention of outstanding staff members and motivate them so that the organization can achieve its mission and goals 4

41 Developing a Compensation Philosophy It should include: The appropriate marketplace for the organization which typically includes a blend of the following characteristics: Similar missions, stakeholders, and funding sources Same geographic focus and recruitment sources: national, regional, local, etc. Similar scope, e.g., budget and staff size For example, community development organizations in the metropolitan New York region with operating budgets of $10M to $15M that recruit regionally 5

42 Developing a Compensation Philosophy It should include: How the organization wants to pay relative to this market This can be a general statement: Our total compensation will be competitive with the market Or it can be specific: Our salaries are tied to the median of the broad Washington area marketplace If and how compensation is linked to performance and/or other factors, for example: Our salaries are tied to the median of the broad Washington area marketplace, and those staff members with a history of consistently excellent performance are paid at this level 6

43 Developing a Compensation Philosophy It can also include: If and how variable compensation will be incorporated into the compensation program, for example: The compensation plan will include reward programs such as incentive plans where these are consistent with practices in the marketplace. Information about the components of the compensation structure, for example: Salary ranges are tied to an individual s specific marketplace. The salary range for an accountant is directly tied to the salaries of accountants in our marketplace. 7

44 Developing a Compensation Philosophy It can also include: The governance structure and process for setting and adjusting compensation, including the steps necessary for meeting IRS legal standards. For example: The Compensation Committee will: Set compensation for the Chief Executive Annually review compensation of the Chief Executive and other employees considered to be disqualified under IRS intermediate sanctions to ensure compliance. Annually review the budgets for salary increases and other forms of pay, e.g., incentives. Review, every X years, compensation levels and structure for the entire organization to ensure their compliance with the compensation philosophy Ensure that compensation is reasonable with respect to IRS and stakeholder scrutiny 8

45 Developing a Compensation Philosophy It can also include: Other characteristics of the compensation program Managers will regularly communicate the elements of our compensation system to staff Our compensation system is designed to be clear and transparent so that every staff member will understand his or her compensation and opportunities with the organization. Our people are compensated fairly both in relation to each other and to those outside the organization. 9

46 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 10

47 Understanding the Organization and Its Marketplace The goal of a compensation analysis is to find and document data that supports the IRS reasonableness standard: What would ordinarily be paid for like services by like enterprises under like circumstances. The first step in conducting a compensation analysis is to understand the organization, its marketplace, and its current pay practices. The organization s mission: Non-profit markets differ by organization type: Museums, foundations, and advocacy organizations pay differently. An organization s comparator group typically includes organizations that are engaged in the same or similar types of work. 11

48 Understanding the Organization and Its Marketplace Organization size: While budget size is used as a primary factor, other measures can be used and they often differ by sector: Membership organizations such as professional societies and associations may also use number of members Foundations use asset size Academic institutions use endowment 12

49 Understanding the Organization and Its Marketplace Organization scope: The nature of the market is likely to differ depending on the geographical scope of the organization s operations and where it recruits. Organizations that work and/or recruit nationally or internationally are likely to be in different markets than local organizations. While there is usually a correlation between scope of operations and scope of recruitment, some organizations may operate locally, but recruit nationally or even internationally (an opera company, for example). 13

50 Understanding the Organization and Its Marketplace Organization location: A place with an unusually high or low cost of living may be reflected in the market. For example, compensation in New York City is generally above national market levels because of the extremely high cost of living in Manhattan. A regional organization in New York City might therefore pay more than a national organization based in Idaho Falls. 14

51 Understanding the Organization and Its Marketplace Any specific requirements for the position: Some positions may require special technical skills. For example, the chief executive must be an M.D. or a lawyer, or have experience in media or information technology. While the need for these skills may help determine the market place, the market in general for those skills is not generally the right comparison. If special skills are truly needed we will generally look at other non-profit organizations that require those skills. A position may require financial skills, for example, but that won t justify paying a non-profit CEO like an investment banker. 15

52 Understanding the Organization and Its Marketplace Length of service and experience. Longer service and a record of achievement may make an executive more valuable to the organization. Chief executive recruitment sources: Types of organizations from which a chief executive might be recruited, or to which he or she might plausibly go, can be included even if the missions of such organizations are somewhat different. 16

53 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 17

54 Sources of Market Information Having obtained information on the organization s mission, scope and other relevant factors, the next step is to gather market information. There are four main sources of market data: Publicly available IRS Data IRS Form 990s from comparable organizations Publicly available surveys Private or restricted surveys Specially commissioned surveys 18

55 IRS Form 990 Most nonprofit organizations with annual budgets over $25,000 are required to file an IRS Form 990 or 990E-Z every year. Organizations must list the names, addresses, and compensation of their five highest-paid employees. They must include total cash compensation, benefits and deferred compensation, expense accounts, and other allowances. Because 990 data includes all elements of total compensation it can be subject to the caveats below especially valuable in an intermediate sanctions analysis. Organizations also provide data on their revenue and spending. This data is useful in ensuring that comparable organizations are considered as part of the marketplace. 19

56 IRS Form data is available to the public; the 990s from the past three years must be made available to anyone who visits a nonprofit and asks for them. The nonprofit organization Guidestar ( posts 990 data for approximately 390,000 individual organizations on the Web; details of Guidestar s IRS 990-based database are available for a fee. Other organizations, including the Chronicle of Philanthropy, also publish selected 990 data from time to time. 20

57 IRS Form 990 The following pages show sample 990 forms. Especially important are the following: Location Total revenue or expenditures Asset size Compensation columns Elements of compensation Titles of top paid 21

58 IRS Form

59 IRS Form

60 IRS Form

61 IRS Form 990 It is best to try to identify 10 to 15 comparable organizations for a 990 analysis to increase the stability of the group from year to year. (In some cases, however, there may not be 10 organizations; try to get as close to ten as possible). Several aspects of the 990 data should be kept in mind: Organizations report only total cash, deferred compensation, and fringe benefits. The data are useful for understanding the marketplace for total cash compensation, benefits and total compensation, which is the appropriate standard for Intermediate Sanctions. They cannot tell you about base pay practice, which may be relevant in establishing a compensation package. 25

62 IRS Form 990 Deferred compensation data has not always been reliable. In the past, IRS rules required organizations to report deferred compensation the year it was actually paid. This could be a single very large lump sum in the year a chief executive retired. In addition, anecdotal evidence suggests that organizations do not uniformly report deferred compensation amounts. The data are at least a year old, and usually older. The data must also be updated to present-day dollars before they can be used. In addition, any recent changes in compensation levels will not be captured. 26

63 IRS Form 990 It is often hard to identify position matches for other than the CEO. Titles differ from organization to organization, and it can be very hard to tell which are comparable. We therefore often construct a top five paid table from the list of comparable 990s. 27

64 Publicly Available Surveys Compensation survey information is made available to the public by both for-profit and nonprofit organizations. These surveys are traditionally used by organizations to compare their cash compensation to the market. As a result, they include base pay and (often but not always) total cash compensation. Their data on benefits value and total compensation is usually weaker. Some will have benefits prevalence data. 28

65 Publicly Available Surveys National surveys include general compensation surveys, which typically have a nonprofit cut of the data, as well as surveys of the general nonprofit market and surveys of specific nonprofit sectors (for example, foundations, educational institutions, learned professions). Examples of general national surveys include the series of surveys produced by Watson Wyatt, which has a survey on Top Executives with a not-for-profit cut. Examples of specialized surveys are those produced by the Council on Foundations, the College and University Personnel Association, the American Association of Museum Directors, the American Association of Botanical Gardens and Arboreta (AABGA), and the Special Libraries Association. 29

66 Publicly Available Surveys Local surveys will cover a single metropolitan area, a state, or a region; they may cover all organizations, all nonprofits, or a subset of nonprofits. In the Washington, DC area, for example, the National Capital Area Human Resources Association (HRA) publishes a detailed survey of Washington area compensation that includes a nonprofit cut. 30

67 Publicly Available Surveys The data must usually be purchased from the organization publishing the survey costs can range from as little as $50 to over $1,000 for the larger national surveys produced by the major compensation consulting firms. Special cuts of survey data are often available from the sponsoring organization, again for a fee. A special cut allows an organization to obtain data from the relevant subset of a larger group for a particular set of comparable organizations or for a cross cut otherwise not available ( non-profit organizations in DC with a budget size between $5 and $10 million ) Preferably, data from at least eight to ten organizations should be included in any special cut to make the results statistically valid. 31

68 Restricted Access Surveys Not all survey data are publicly available. Surveys are often conducted by a group of nonprofit organizations for their internal use, and the data are, in principle, available only to participants. However, nonparticipants can sometimes obtain the data by promising to participate in the next survey, or by requesting it from a friendly organization taking part in the survey. For example, Quatt Associates conducts participants-only annual surveys for: Major trade associations in the Washington area Major museums (nationally) Large national non-profits Washington-area Educational Organizations 32

69 Special Surveys One of the best ways of gathering data probably the very best if the right set of organizations can be found is to conduct a special survey. With the right participants, a special survey will provide up-to-date data on organizations specifically chosen for their comparability. A special survey can also provide reliable and comprehensive data on total compensation, including benefits and deferred compensation 33

70 Special Surveys However, some practical difficulties are involved in conducting a special survey: Sponsoring a study can be burdensome to the organization. Even if the survey is conducted by an independent firm, the sponsoring organization must secure the participation of other organizations. Filling out the survey by participants can be burdensome, especially for deferred compensation, the value of which may be hard to estimate It is our experience that custom surveys require two to three months to complete For the data to be statistically significant, the survey should include at least eight to 10 participants comparable in as many ways as possible. 34

71 Special Surveys In certain sectors (healthcare, for example,) anti-trust issues may arise when organizations share compensation information. To minimize these, some authorities advise that the data be collected by an independent third party, that it be aggregated, and that at least five organizations participate in the survey. 35

72 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 36

73 Understanding and Using Surveys The survey data will be organized by position, and then by various cuts or subsets of the data. The chief executive position may be listed as CEO, Top Executive, Executive Director, or some other (generally obvious) title. The data may include the following: Base pay or base salary compensation: The annual salary paid Extra cash compensation: Any bonus or incentive paid Total cash compensation: Salary plus any additional cash, generally bonus or incentive Deferred compensation Total compensation 37

74 Understanding and Using Surveys Fringe benefits: Some surveys will report fringe benefits paid, often by type of benefit such as health insurance or free use of automobile. These are not always quantified, and the survey may simply report the existence or prevalence of the benefit. The benefits data is usually reported separately from the compensation data. Organization type: General compensation surveys will have a nonprofit category, which may or may not be further broken down. Organization budget. Time in position. Number of employees The number of organizations reporting the particular data. The date of the information presented: Surveys will show the effective date of the information they present. 38

75 Understanding and Using Surveys Data are generally reported by quartile. Surveys commonly report three quartiles: the 25th percentile the compensation amount above which 75 percent of all reported compensation data fall the median or 50th percentile the compensation amount above which 50 percent of all reported compensation data fall and the third quartile or 75th percentile the compensation amount above which 25 percent of all reported compensation data fall Some surveys will also report the 10th percentile (90 percent of all data is higher), and the 90th percentile (10 percent of all data is higher). 39

76 Understanding and Using Surveys Top Paid Data: In addition to specific position matches, some surveys will include information on top paid executives the top five, eight or ten generally. This is extremely valuable for pricing positions that are unique to an organization, or which are of special value to the organization. As noted earlier, we will often construct a top five paid list from a group of IRS 990 comparators to use in marketpricing positions other than the CEO; direct position matches are difficult with IRS 990 data. See the following pages for survey examples. 40

77 Understanding and Using Surveys 41

78 Understanding and Using Surveys 42

79 Understanding and Using Surveys 43

80 Understanding and Using Surveys 44

81 Understanding and Using Surveys 45

82 Understanding and Using Surveys 46

83 Understanding and Using Surveys 47

84 Understanding and Using Surveys 48

85 Understanding and Using Surveys 49

86 Understanding and Using Surveys In using survey data, the goal is to use the cut that is as close as possible to the organization s market. Data, however, are presented in discrete categories, without necessarily the ideal crosscuts. In some cases, it may be possible to purchase a special cross cut; if this is not possible, a simple approach is to take the single best cut or the two best cuts. If a general survey, start with the non-profit cut. Budget size is the data cut (among non-profits) mostly closely correlated, although by no means perfectly, with chief executive compensation. 50

87 Understanding and Using Surveys Locality adjustments: If the organization is in a high or low paying locality, and it recruits nationally or regionally, it can be appropriate to adjust the overall market data for local pay practices. New York, for example, pays about 15% to 17% above the national average. Sources of locality adjustments include the Federal pay scales, and private survey firms. Be careful, however if the data source being used is already heavily weighted toward organizations in large cities, a further locality adjustment may amount to double counting. 51

88 Understanding and Using Surveys A second important issue is which quartile to use in determining the market. The safest, and most common, approach is to use the median of the marketplace. It can be appropriate to use up to the 75 th percentile if there are special circumstances that distinguish an organization from its peers: for example, if it has ambitious growth plans, currently has an unusually skilled or experienced chief executive, or has a leading position in its specialty area. It may also make sense to use other cuts than the median as a way of adjusting the data. For example, if an organization is substantially larger than the highest budget cut in a survey, the 75th percentile may be closer to the organization s market than the survey median. 52

89 Understanding and Using Surveys Comparing pay above the 75th percentile is unusual. Any organization targeting above the median should be able to explain its decision; a comparison above the 75th percentile should have an especially strong justification. 53

90 Understanding and Using Surveys: Aging the Survey Data All surveys will report when the data were collected; the data must then be updated to the present using an inflation factor. Good sources include the Conference Board ( and WorldatWork (formerly the American Compensation Association; Several of the larger compensation consulting firms, such as Mercer Human Resource Consulting and Hewitt Associates, also produce regular surveys of market pay movement. Over the last year, the average overall increase in market pay has been approximately 2.0% in the Washington, DC area, but this will differ by geographic location and by sector. 54

91 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 55

92 Benefits Analysis Because the IRS standard is total compensation, it is important to consider benefits and deferred compensation as well as cash compensation. There are two approaches to considering benefits: 1. Estimated benefits value IRS 990 data will include reported benefits values. It is, of course, also necessary to get the best possible estimate of benefits value from the organization for which the analysis is being conducted. While IRS 990 data is probably the best available, in our experience the completeness and accuracy of reported benefits as reported on 990s differs considerably from organization to organization. One of the advantages of conducting a special survey is that benefits can be estimate consistently and comprehensively. 56

93 Benefits Analysis It is especially difficult to estimate the value of deferred compensation. While it is possible to conduct an actuarial analysis of deferred compensation value for each participant to arrive at an accurate assessment but it is unlikely that most survey data is equally comprehensive. 2. Benefits prevalence: The second and complementary approach is to examine benefits prevalence. In this approach, each benefit is separately compared to the market, using published or specialized survey data. Data is presented on the percent of the market providing the benefit, and its annual cost, if available. 57

94 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Analysis Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 58

95 Example of A Compensation Analysis: Overview Mission: Environmental advocacy organization Scope: National and International Budget: About $60 million/300 employees Location: New York City Approach: Determine comparable organizations and get 990 data Use data from published and proprietary surveys to estimate total cash and total compensation Conduct benefits prevalence analysis 59

96 Example of A Compensation Analysis: Sources of Data IRS Form 990 Data Quatt Associates determined a list of comparable organizations. Familiarity with client organization Guidestar search Client s own input Similar budgets roughly $25 to $100 million in New York City. Included advocacy AND research organizations organization performs both functions. 60

97 Example of A Compensation Analysis: Sources of Data IRS Form 990 data was used as the principal comparator. We also presented other survey data as a reference. 990s had the only total compensation information. 990s were the closest market match. Other surveys were used as a check of 990 findings. 61

98 Example of A Compensation Analysis: Sources of Data 62 Annual Budgets of Advocacy Organizations in Peer Group Note: IRS Form 990 budget data has been aged to February 1, Total Revenue as reported on IRS Form 990

99 Example of A Compensation Analysis: Sources of Data Annual Budgets of Research Institutions in Peer Group Note: IRS Form 990 budget data has been aged to February 1, Total Revenue as reported on IRS Form

100 Example of A Compensation Analysis: Data Analysis Advocacy organizations were weighted 75% in the market analysis and research institutions 25% to reflect the function of the client organization Targeted median to assess reasonableness 64

101 Example of A Compensation Analysis: Sources of Data 2005 PRM Consulting, Inc. Management Compensation Report of Not-for-Profit Organizations. General nonprofit survey. Used as reference only. Cut used: In this case, as it was determined that budget size and executive compensation were linked; those organizations with a budget size greater or equal to $60 million were the best comparators. Possible issue: survey has large number of trade associations; larger budget organizations may be overweighted with high paying trades Did not adjust for New York; judgment made that highest revenue cut will be located in high-paying metro areas 65

102 Example of A Compensation Analysis: Sources of Data The survey only reports base salary levels. The survey reports a median value for additional compensation as a percentage of base salary (15%). This was added to base pay to determine the total cash compensation value compatible with those reported in the IRS Form 990s. No total compensation data was available Survey has benefits prevalence data Effective date was April 1, 2005; aged to February 1, 2006 using an annual aging factor of 3.7%. 66

103 Example of A Compensation Analysis: Sources of Data 2005 Quatt Database A proprietary survey of not-for-profit organizations including museums, foundations, and other major non-profits. Used as reference only. Cut used: Because our client was an advocacy organization with a budget of $60 million, we compared it to smaller cuts in the Quatt Survey the 10 th percentile as a proxy for the 25 th percentile of the advocacy marketplace and the median to represent the 75 th. Total cash compensation only, no total compensation. Aged according to effective date (same process as above). 67

104 Example of A Compensation Analysis: Sources of Data Quatt Database: 68

105 Example of A Compensation Analysis: Final Report Included the following sections: Methodology and sources. Charts of values from each data source with lists of comparable organizations and survey participants Market analysis tables Calculation of final market price for each position and comparison to current pay practices 69

106 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 70

107 Appendix A: Sample Compensation Philosophy The compensation structures and systems of our organization will support our mission, strategy and values. Organization XYZ will pay for performance; skills and competencies; development and growth; and effective visible commitment to the organization. The compensation system will encourage recruitment, retention, and motivation of outstanding employees so that the organization can achieve its mission and objectives. The compensation system will reward truly outstanding performers and provide appropriate feedback to staff members who need improvement. The compensation structure will be a mixture of base salary; performance-based at risk pay appropriate to the nonprofit marketplace; retirement and other benefits; and special recognition awards where merited by performance. A portion of each employee s pay will be tied to the achievement of organizational and individual objectives. Unusual individual achievement may also merit special financial awards. The compensation system will include annual adjustments to pay ranges based on changes in the marketplace (subject to financial constraints). Adjustments to individual base pay will be based on job performance and growth in mastering job competencies. All adjustments to pay will be consistent with practice in the nonprofit marketplace. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

108 Appendix A: Sample Compensation Philosophy Compensation for the chief executive will be set by the compensation committee of the board with review by the full board, which will comply with all applicable legal standards. The compensation committee will regularly review the compensation of the chief executive and all other employees considered to be disqualified persons under IRS intermediate sanctions regulations, to ensure compliance with the regulations and any other rules and regulations to which the board is subject regarding compensation. The compensation system will have a coherent structure based on pay practices consistent with our nonprofit mission and status, but will recognize that parts of our organization are in different markets and that the compensation for each position must be based on the appropriate marketplace for that professional area. Organization XYZ will pay as close as possible to the median (midpoint) of the appropriate external marketplace, while recognizing that internal equity and financial constraints can justify some deviation from the market. The marketplace adequacy of the structure will be judged in terms of total compensation, including benefits; the total package will be competitive with the marketplace. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

109 Appendix A: Sample Compensation Philosophy The compensation structure will be linked to an effective performance management system with individual growth and development as well as professional achievement goals. The goals will be accompanied by effective benchmarks for measuring success. The board will review chief executive performance on an annual basis. Performance objectives for the coming year will be determined jointly by the chief executive and the board at the annual board meeting, with the explicit understanding that salary adjustments and any incentive opportunity will be based on performance against these objectives. Salary will be adjusted based on inflation/market movement and performance. Any incentive earned will be awarded base on performance. The chief executive will annually prepare and submit to the board a self-assessment of performance as input to the performance review. The board will clearly outline and communicate how performance will be linked to salary adjustments and any incentive opportunity. There will be clear measures for achieving success in each objective, and these will be linked to levels of award. Salary adjustments and any incentive opportunity will be based on market practice. The board will ensure that no salary adjustment or incentive award will cause total compensation to exceed amounts that are reasonable for IRS standards. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

110 Appendix A: Sample Compensation Philosophy The board retains the right to withhold adjustments at its discretion, regardless of performance. Compensation will be fair and transparent. Compensation will be reasonable and defensible relative to IRS regulations and stakeholder expectations. Executives and staff will receive regular and comprehensive training in the compensation system. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

111 Outline Developing a Compensation Philosophy Understanding the Organization and Its Marketplace Sources of Market Information Understanding and Using Surveys Benefits Analysis Example of a Compensation Study Appendix A: Sample Compensation Philosophy Appendix B: Sample Compensation Committee Charter 75

112 Appendix B: Sample Compensation Committee Charter Purpose: The purpose of the Compensation Committee (the Committee ) is to aid the Board of Directors (the board ) in discharging its responsibilities relating to compensation of the staff of Organization XYZ. Responsibilities: The Committee s responsibilities include: Determination of the compensation philosophy for the Organization, updated as necessary to reflect any changes in the law or the organization s operations Negotiation and approval of the chief executive s contract Annual review of the chief executive s performance in light of the Organization s goals and objectives Recommendation to the full board on the chief executive s compensation level, structure and adjustment process Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

113 Appendix B: Sample Compensation Committee Charter Responsibilities (continued): The chief executive will have sole authority for setting the compensation for all employees other than himself or herself. However, the Committee will regularly review compensation for all executives and employees who are considered disqualified persons (including the chief executive): The organization s compensation philosophy The rules governing tax-exempt organizations described in the Internal Revenue Code, including, but not limited to, the intermediate sanctions statute (Section 4958) and regulations. The compensation rules and regulations promulgated by any other regulatory agency or legislative authority The review will include base salary, bonus payments (if any), deferred compensation payments, retirement arrangements, fringe benefits, severance agreements, employment agreements, and any form of compensation promised therein, and any other compensation items. The review will obtain and rely on relevant data on practices at comparable organizations. In the case of the chief executive, the Committee will base its recommendation on compensation upon this review. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

114 Appendix B: Sample Compensation Committee Charter Responsibilities (continued): Regularly review the organization s compensation structure to ensure that it complies with the compensation philosophy Regularly review the organization s bonus/incentive program and determine the size of the bonus/incentive pool, based on performance against strategic milestones or other relevant performance factors determined by the board The Committee will make a formal report to the full board on the results of all reviews, including review of compensation for executives who are disqualified persons (including the chief executive), review of the compensation structure for compliance with the compensation philosophy, and review of the bonus/incentive program. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

115 Appendix B: Sample Compensation Committee Charter Authority: The Committee will make recommendations to the full board regarding all plans designed and intended to provide compensation for the chief executive and for such other senior executives who are deemed to be disqualified persons under Section 4958, as well as recommendations resulting from review of any other issue for which the Committee has been designated as the supervisory body. The full board will have ultimate decision-making authority on any issue for which the Committee has oversight. Final approval of the chief executive s contract and compensation may only be determined by a vote of the board. The Committee will have authority to engage outside independent compensation, accounting, legal, and other advisors and to obtain advice and assistance from such independent advisors. The Committee will review data from studies prepared by an independent third party to assist in the evaluation of senior executive compensation. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

116 Appendix B: Sample Compensation Committee Charter Membership: The Committee will consist of no fewer than [at least 3] board members who are independent and who have not been employed by Organization XYZ in the last five years. There will be a Chair of the Committee, who will be appointed by the board Chair, with approval of the board. No member of the Committee may be an executive, related to an executive, be in a position to benefit from any executive s compensation arrangement, or otherwise have a conflict of interest. No member of the Committee may have any other conflict of interest, as determined by the board s general conflict-of-interest policy. No member of the Committee may be in a position to receive compensation or other economic benefits from any executive or from any transaction arrangement that is subject to the approval of any executive. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

117 Appendix B: Sample Compensation Committee Charter Meetings: The Committee will meet at least times annually. The Committee may meet via teleconference. Special meetings of the Committee may also be called by the Chair of the Committee. The attendance of [at least 3] Committee members, whether in person or by teleconference, will constitute a quorum for these meetings. The Committee will keep written minutes of each of its meetings and will duly file the minutes with the archives of board minutes. Reports of meetings of the Committee will be made to the board at the board s next regularly scheduled meeting following the Committee meeting and will be accompanied by any recommendations to the board approved by the Committee. Vogel, Brian and Quatt, Charles. Nonprofit Executive Compensation: Planning, Performance, and Pay. Washington, DC: BoardSource,

imposes a penalty excise tax directly on certain persons who receive excessive compensation from")

118 TAX-EXEMPT ORGANIZATIONS ALERT NONPROFIT EXECUTIVE COMPENSATION IN SETTING EXECUTIVE COMPENSATION, A TAX-EXEMPT ORGANIZATION SHOULD CONSIDER FOLLOWING THE IRS S REQUIRMENTS TO ESTABLISH A REBUTTABLE PRESUMPTION THAT THE COMPENSATION IS REASONABLE Section 4958 of the Internal Revenue Code (the Code ) imposes a penalty excise tax directly on certain persons who receive excessive compensation from certain taxexempt, nonprofit organizations. If a nonprofit executive violates section 4958 of the Code, the nonprofit executive is personally liable to pay one or more penalty excise taxes. In some cases, managers of a nonprofit who approve excessive compensation arrangements, such as members of the board of directors, may also have to pay an excise tax. A nonprofit organization can limit the potential exposure of its executives to section 4958 taxes by following a safe-harbor procedure contained in applicable IRS regulations. WHOSE COMPENSATION IS POTENTIALLY SUBJECT TO SECTION 4958 PENALTY EXCISE TAXES? Section 4958 of the Code prohibits an applicable tax-exempt organization from participating in an excess benefit transaction with a disqualified person. Applicable tax-exempt organizations are nonprofit organizations (other than private foundations) that are exempt from taxation under section 501(c) (3) or (4) of the Code. An excess benefit transaction occurs when a nonprofit organization provides a benefit to a disqualified person that exceeds the value of the benefit the organization receives from the disqualified person in exchange. For example, if a nonprofit pays its executive director a salary well above what executive directors of similar organizations are paid, the organization would be considered to have engaged in an excess benefit transaction. A disqualified person is generally defined as any person in a position to exercise substantial influence over the affairs of a nonprofit organization anytime during the five-year period preceding the date of the compensation transaction. IRS regulations say that voting members of a nonprofit s board of directors, presidents, chief executive officers, chief operating officers, treasurers, and chief financial officers are in a position to exercise substantial influence over the organization s affairs, and, as such, deem them to be disqualified persons. Disqualified persons also include family members of other disqualified persons 1

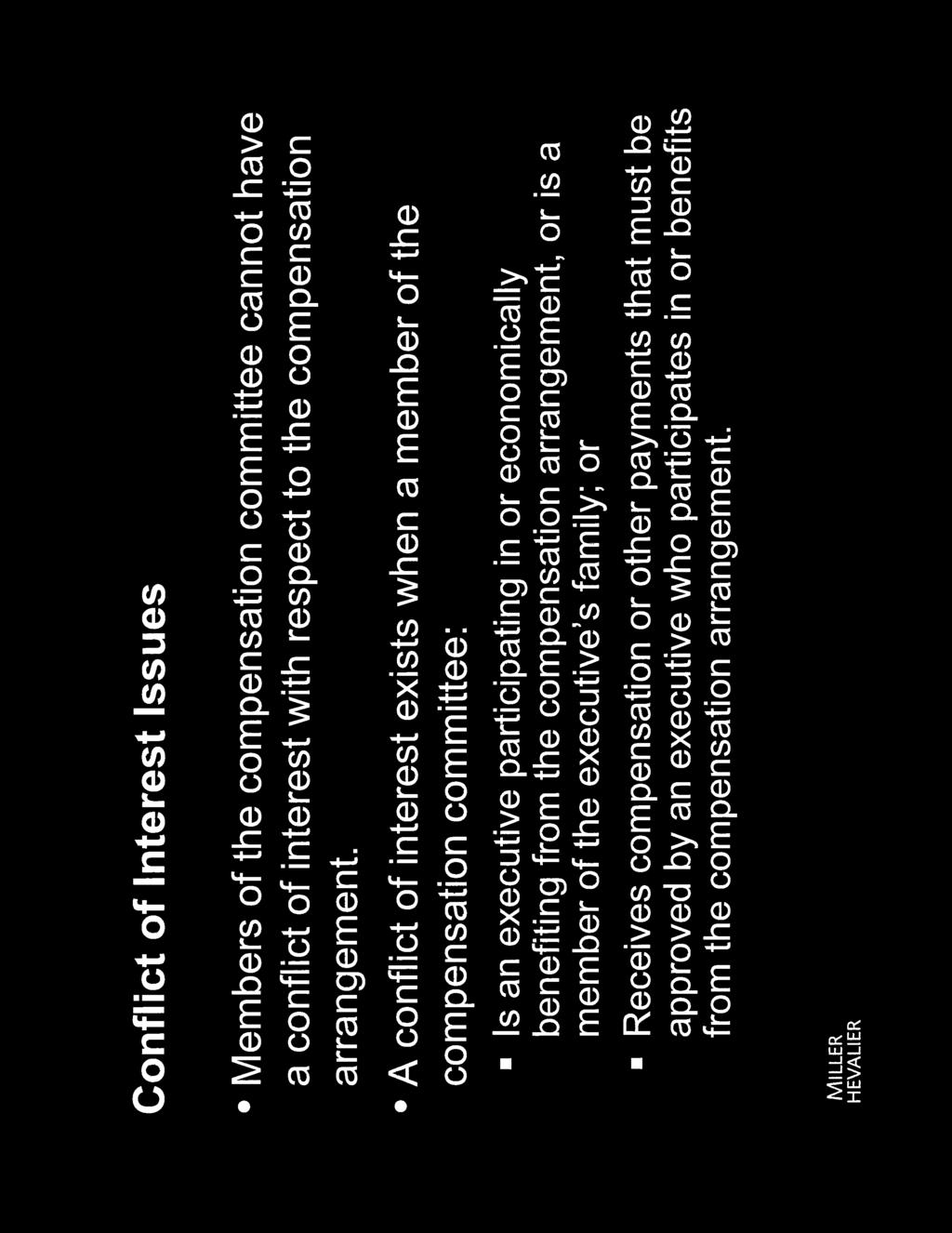

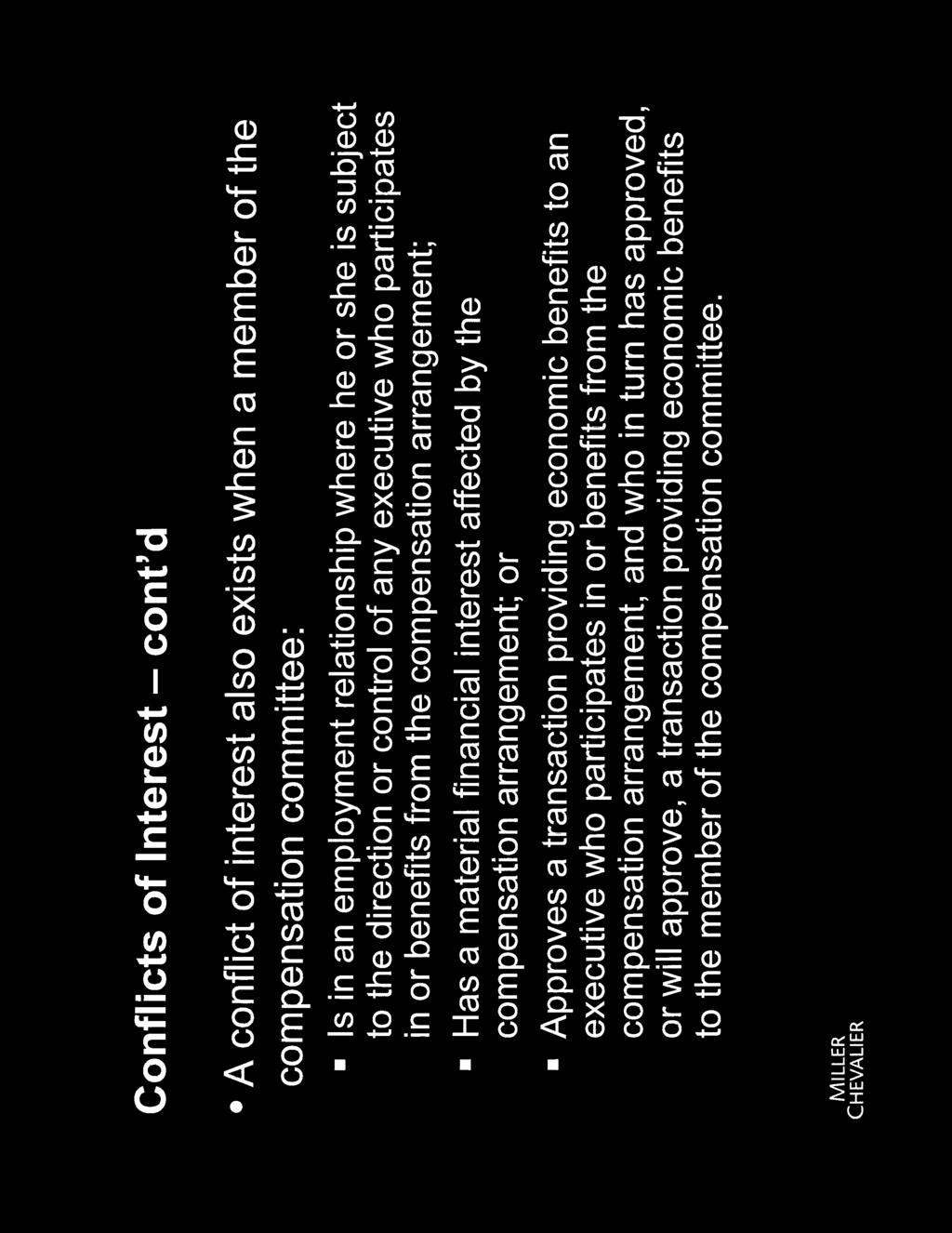

119 (including spouses, siblings, in-laws, ancestors, and children, grandchildren, great grandchildren, and their spouses). For example, the spouse of an executive director would be a disqualified person. Special rules, not discussed here, apply to corporations and partnerships in which disqualified persons have an interest, and to donor advised funds and supporting organizations. You should check with your tax advisor to determine who is a disqualified person with respect to your nonprofit. HOW DO NONPROFIT EXECUTIVES GET THE BENEFIT OF THE REBUTTABLE PRESUMPTION THAT COMPENSATION PAID BY A TAX- EXEMPT ORGANIZATION IS REASONABLE? By following the IRS s three-step safe harbor procedure, a nonprofit organization can significantly minimize the risk that the IRS will later determine that the organization has engaged in an excess benefit transaction. Following this procedure is known as establishing the rebuttable presumption of reasonableness. If the rebuttable presumption of reasonableness is established, payments made under a compensation arrangement will be presumed to be reasonable. Instead of the disqualified person having to show the compensation was reasonable, the burden of proof will shift to the IRS to demonstrate that the compensation paid to the disqualified person was unreasonable. The three steps for establishing the rebuttable presumption of reasonableness involve: approval by an authorized body; use of appropriate comparability data; and documentation. First, an authorized body of the nonprofit organization must approve the compensation arrangement in advance. A nonprofit s authorized body may consist of the organization s governing body (i.e., the board of directors or board of trustees), or if permitted by state law, either a committee of the governing body, or other parties authorized by the governing body to act on its behalf. Members of the authorized body cannot have a conflict of interest with respect to the compensation arrangement. A conflict of interest exists when a member of the authorized body approving the compensation arrangement: is a disqualified person participating in or economically benefiting from the compensation arrangement, or is a member of the family of any such disqualified person; is in an employment relationship where he or she is subject to the direction or control of any disqualified person who participates in or benefits from the compensation arrangement; receives compensation or other payments that must be approved by a disqualified person who participates in or benefits from the compensation arrangement; has a material financial interest affected by the compensation arrangement; or approves a transaction providing economic benefits to a disqualified person who participates in or benefits from the compensation arrangement, and who in turn has approved, or will approve, a transaction providing economic benefits to the member of the authorized body. For example, the son of a nonprofit s executive director cannot serve on the 2

120 authorized body approving the executive director s compensation, because the son has a conflict of interest with respect to the executive director s compensation arrangement. Second, prior to making its decision, the authorized body must retain and rely upon appropriate data as to how the compensation to be paid compares to compensation paid by similar organizations for similar services. Comparability data is appropriate if it provides the authorized body with sufficient information to determine if the compensation arrangement in its entirety is reasonable. Examples of relevant information include: compensation paid by similarly situated for- profit and nonprofit organizations for comparable positions; whether or not there is a ready supply of people to perform similar services in the geographic area where the nonprofit is located; current compensation surveys compiled by independent firms; and actual written offers from similar institutions competing for the services of the disqualified person. For a nonprofit with annual gross receipts of less than $1 million during the three prior taxable years, the IRS will consider the organization to have appropriate comparability data if it obtains data on compensation paid by at least three comparable organizations in the same or similar communities for similar services. Third, when making its determination that compensation to be paid to a nonprofit executive is reasonable, the authorized body must adequately document the basis for its determination. The documentation may be written or electronic, such as written minutes or an summary of the meeting. The documentation must note: the terms of the transaction and the date it was approved; the members of the authorized body who were present when the transaction was debated; the comparability data obtained and relied on by the authorized body and how the data was obtained; and any actions taken by a regular member of the authorized body who had a conflict of interest with respect to the transaction (e.g., recusal). Adequate documentation also means timely documentation. The organization must prepare records before the next meeting of the authorized body or 60 days after the final action or actions of the authorized body are taken, which ever occurs last. Also, the authorized body must, within a reasonable period of time, review and find that the records are reasonable, accurate, and complete. The nonprofit must comply with all three steps to establish the rebuttable presumption of reasonableness. The nonprofit will not enjoy the protections the safe harbor affords if the organization fails to meet any one of its three requirements. Following the threestep procedure for establishing the rebuttable presumption of reasonableness is voluntary. The IRS will not automatically assume a violation by an organization that chooses not to follow the safe harbor. However, establishing the rebuttable presumption of reasonableness is the most reliable way to guard against potential exposure to penalty taxes resulting from a nonprofit executive s receipt of excessive compensation. Establishing the rebuttable presumption of reasonableness is also 3

121 considered to be a best practice in terms of nonprofit governance. WHAT HAPPENS IF A VIOLATION OF SECTION 4958 OF THE CODE OCCURS? Section 4958 of the Code imposes penalty taxes directly on individuals who receive an excess benefit from a nonprofit and on organization managers who knowingly approve a transaction that gives rise to an excess benefit. A disqualified person who receives unreasonable compensation is liable for an initial tax and may be liable for an additional tax. The initial tax on the disqualified person equals 25% of the amount by which the value of the compensation received exceeds the value of the services provided to the organization by the disqualified person in return. If the initial tax is imposed and the disqualified person does not repay the amount of the excessive compensation (with interest) to the nonprofit organization, an additional tax is imposed on the disqualified person equal to 200% of the amount of the excessive compensation received. If a disqualified person makes a payment less than the full amount of excessive compensation (plus interest), the 200% tax is only imposed on the unpaid portion of the correction amount. A tax equal to 10% of the amount of the excessive compensation received by a disqualified person is imposed on any organization manager who knowingly approves excessive compensation. An organization manager includes any officer, director, or trustee of a nonprofit organization, or any individual who has powers and responsibilities similar to officers, directors, or trustees of the organization. A manager knowingly approves excessive compensation if he or she actually knows of facts that indicate that the transaction would result in unreasonable compensation. Furthermore, if more than one organization manager is liable for a section 4958 tax, all such organization managers are jointly and severally liable for this tax. An organizational manager s exposure to the tax may be limited by several factors. If an organization manager relies on the reasoned written opinion of legal counsel, certified public accountants, accounting firms, or independent valuation experts, and the opinion reflects elements of the transaction within the professional s expertise, the organization manager is protected from the tax even if that opinion is ultimately found to be incorrect. The tax is not imposed if the manager s participation was not willful and was due to reasonable cause. An organization manager is not considered to have participated in an excess benefit transaction if he opposed the transaction in a manner consistent with the fulfillment of the organization manager s responsibilities to the organization. Furthermore, the total tax imposed on all organization managers is limited to $20,000 for each excess benefit transaction. Before you develop a compensation package for your executive employees, you should check with your tax advisor to determine whether your nonprofit should take advantage of the IRS safe harbor. This communication is a public service of the D.C. Bar Pro Bono Program. It is provided by the D.C. Bar Pro Bono Program and by the authors of the information solely for informational purposes, without any assurance that it is accurate or complete. It should not be construed as, and does not constitute, legal advice. Receipt of this information does not create an attorney-client relationship between the recipient and any other person, or an offer to create such a relationship. Consult an attorney if you have questions regarding the contents of this communication. 4