Remuneration reporting

|

|

|

- Scott Francis

- 5 years ago

- Views:

Transcription

1 Remuneration reporting November 2015

2 Introduction The current remuneration reporting regulations ( the regulations ) for listed UK companies were introduced for financial years ending on or after 30 September The regulations are highly prescriptive in terms of both the layout and content of companies remuneration reports. We would challenge Remuneration Committees to move beyond compliance towards using the report as a tool for communication with stakeholders. Remuneration reports for the first two financial years under the regulations have generally been highly compliant. However, in securing compliance, something has possibly been lost in the quality of narrative. To address this we would challenge Remuneration Committees to address the following three questions in this year s Directors Remuneration Report: How is the pay of Directors aligned with company strategy? How are the payments authorised by the Committee justified by performance? How does the Committee take into account pay and conditions in the wider workforce when setting the pay of Directors? The requirements of the regulations are now well understood and, with compliance achieved, companies now have the opportunity to consider how to move the remuneration report beyond compliance towards use as a tool for communication and dialogue with stakeholders. While the specificity of the regulations mean that certain aspects of the remuneration report must be presented in a prescribed format, that doesn t mean that they can t be explained in the context of the company s business and circumstances. In this document we consider the opportunity presented by having both a Chairman s Statement (the content of which is only loosely prescribed by the regulations) and At a Glance section to bring out the key information in a transparent way, to better explain the link between pay and strategy, and to reflect on the challenges facing the company and how the Remuneration Committee has responded. 2

3 Differentiating your report As we move into the third year of disclosure under the regulations, companies have the opportunity to improve the transparency and relevance of the remuneration reporting by considering the following questions and recommendations. What are the important messages? Use the Chairman s Statement to: provide an overview of corporate performance in the financial year highlight both the areas in which the company has excelled and those which have been less successful recognise and substantiate any outcomes that may appear inconsistent with performance provide insight on decisions made and explain the background to any exercises of discretion, particularly those that may not accord with best practice; and comment on the achievements of the executive directors. What do shareholders need to know? Include an At a Glance section to: summarise the key information succinctly to increase transparency describe how the remuneration policy was applied in practice in the year under review set out the single figure of remuneration summarise the key performance decisions on bonus and LTI, including targets and outcomes against them show the level of executive director shareholdings at the end of the year; and outline how the policy will be applied in the coming year (including incentive levels, key metrics and targets). How can the report be made more accessible? Prioritise the information that will aid understanding by: covering and, importantly, signposting the most relevant information in the Chairman s Statement and At a Glance section relegating the regulatory requirements (tables required for the Annual Report on Remuneration) to the back of the Annual Report summarising the Directors Remuneration Policy, when not subject to shareholder vote, provide reference to where it is available on the website; and including a section on alignment with strategy to: explain the key components of company strategy and KPIs, crossreferring to the strategic report; and show how the remuneration structure and measures align with that strategy. 3

4 Suggestions for improving remuneration disclosure This report assumes that companies are meeting the regulatory disclosure requirements and focuses on improving the quality of communication and transparency of directors remuneration. On this page, we summarise the areas of disclosure covered in this report. Many of these ideas could readily be incorporated into an At a Glance section, as we set out here. The ideas and mocked-up disclosures that follow draw on a combination of what we have seen in companies remuneration reports and what we consider could improve shareholders understanding of executive pay. The examples have been developed for our fictional company, Generico, and therefore may not be directly referable to every company s reward structures without some adaptation. Covered in this publication (click on titles to go to the relevant page) 4

5 1. Chairman s statement As discussed above, the tenor and content of the Chairman s Statement sets the tone for the report and can be used to provide a much fuller justification for pay outcomes than the formulaic disclosures in the Annual Report on Remuneration. The call-out boxes shown here are intended to demonstrate the impact of candour and the value of up-front discussion of outcomes that may appear to be inconsistent with performance. These features contribute to effectiveness of the Chairman s Statement as a key piece of dialogue between the Remuneration Committee and shareholders. Acknowledgement of the pay environment Candid disclosure in relation to shareholder consultation Transparency in relation to poor or unexpected performance Openness in relation to individual Director performance 5

6 2. Implementing policy this year and next Why is it important? There is a requirement to disclose how the approved policy is to be implemented in the next financial year but it s also important to explain how policy has been implemented in the year under review. Any changes in the implementation in policy from one year to the next must be explained and justified. How could you do it? A number of companies made use of simple graphics in summarising the operation of their policy. This summary table which a number of companies have included instead of the full approved policy when not seeking shareholder approval can be used to summarise how the policy was implemented in the financial year just ended, as well as how the company intends to implement policy over the coming year. This provides the reader with important information up-front and also highlights any changes in the implementation of policy over the coming year compared with the previous. We have found colour-coding the elements of pay consistently throughout the report to be an effective way of aiding the readers navigation of the report. 6

7 3. Cascade of pay Why is it important? When the full Directors Remuneration Policy is included in the remuneration report, it must explain how the remuneration policy for executive directors differs from that for other employees in the company. Very few companies provide more than a high level overview of the relationship between executive and employee pay. The concept of fairness in pay is becoming increasingly important to shareholders. The proposal by the European Commission to require UK companies to disclose the ratio of CEO pay to average employee pay is looking increasingly possible and is unlikely to be opposed by UK investors. If UK companies are to successfully resist the pressure from Europe for greater disclosure of the relationship between executive director and employee pay, they will need to demonstrate that the existing disclosure is at least as transparent as that proposed. How could you do it? Effective diagrams depicting the cascade of pay describe the eligibility of each element of pay and opportunity levels, demonstrating how these change down the organisation. The use of graphics, where possible, limits the use of block text and aids understanding. We have also seen examples of companies summarising the operation of remuneration below Board element by element, consistent with the policy table. Further disclosure in this area could include demonstrating the remuneration committee s oversight of the next tier of management with (for example) the distribution of performance ratings and actual incentive awards by grade. 7

, investors are moving towards zero tolerance of companies reliance on the commercial sensitivity opt-out from disclosure of financial targets.")

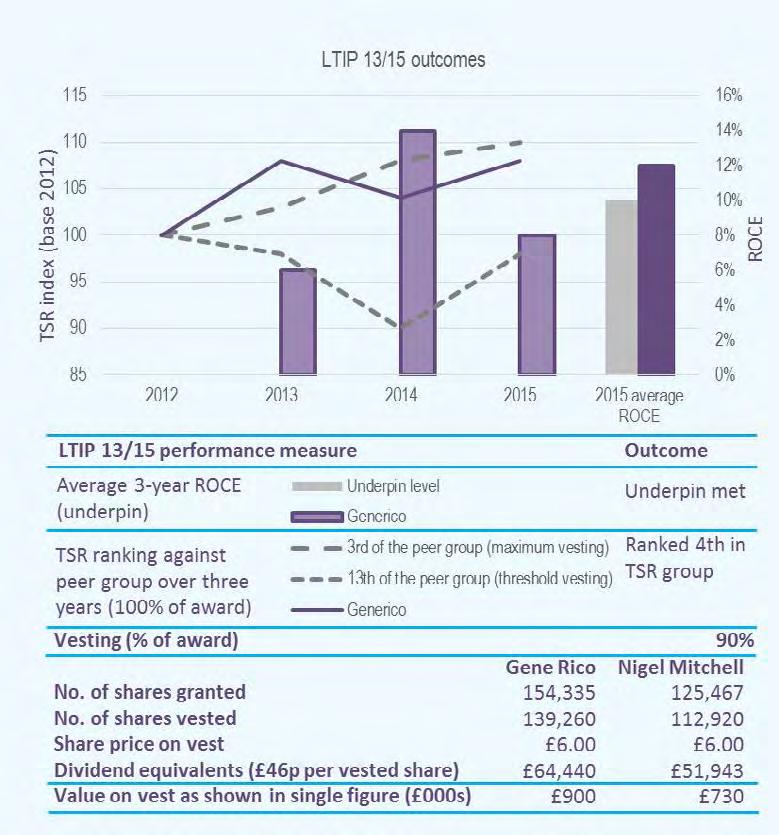

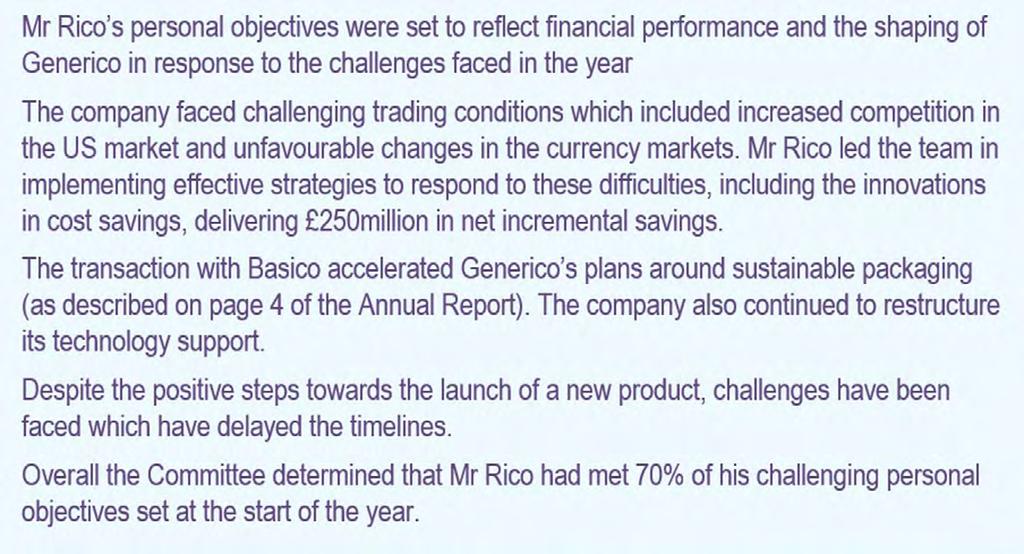

8 4. Outcomes from incentives (1 of 2) Why is it important? As already indicated by the Investment Association (IA), investors are moving towards zero tolerance of companies reliance on the commercial sensitivity opt-out from disclosure of financial targets. Failure to disclose the weighting for each performance metric, targets and vesting structure for financial metrics together with actual performance will weigh as a negative factor in the IA s voting recommendations, and it is likely to be a similar case for ISS. To determine whether there is adequate alignment between remuneration and performance, shareholders may want to get a sense of: where the pay outcomes for the financial year sit on a spectrum of performance scenarios; and how the single figure compares with the potential maximum disclosed when the Directors Remuneration Policy was approved. How could you do it? Setting out actual pay-outs against the scenarios (which form part of the disclosure requirements) provides a neat summary of outcomes versus opportunity, and provides a graphical representation of the single figure. We have seen companies approach the disclosure of outcomes from incentives in a number of ways, and it will frequently be specific to the incentive structure and measures used. Use of diagrams to depict outcomes under each incentive measure, and a candid description of performance, for example under personal measures, also prove effective (shown on the next page). 8

9 4. Outcomes from incentives (2 of 2) 9

or malus")

10 5. Pay at risk: what could be taken away and when Why is it important? The construct of the single figure does not give any insight into the timing of receipt of payments nor the period over which they are at risk of forfeiture (on cessation of employment) or malus and/or clawback. The UK Corporate Governance Code encourages Remuneration Committees to consider adding holding periods for up to two years following vesting, which further fetters executives enjoyment of their earnings. How could you do it? Again, we have found it is most effective to present these disclosures in diagrammatic format. These could include depiction of the proportion of pay that remains at risk, for example a pie chart reflecting the single figure amounts, alongside a timeline of when the pay elements cease to be at risk. This provides additional colour and insight to the single figure, countering the belief that this number reflects the pay pocketed at the end of the year. It can also be helpful to be clear on the timelines of the incentives, given the complexities that factors such as holding periods and clawback periods can add to pay structures,. This includes the period over which performance is measured and the period over which clawback or malus apply. These concepts can be portrayed most clearly using graphics. 10

11 6. Pay alignment with company KPIs (1 of 2) Why is it important? Companies need to be able to demonstrate that incentives are driving the right performance. Very few companies provide evidence of the alignment between performance metrics for annual bonus and LTIP and the company s key strategic priorities. Increasingly investors (and proxy voting agencies) are using their own tools and judgement to assess whether pay outcomes are aligned with performance. Addressing this point in the Annual Report on Remuneration can forestall challenges of this nature. The relative Total Shareholder Return ( TSR ) chart and CEO pay table (over seven years, for years ending between 30 September 2015 and 29 September 2016) do not necessarily illustrate the performance alignment necessary to explain executive pay outcomes. This may be because: Relative TSR is not a significant performance metric for the incentive element of the CEO s remuneration package; and/or The performance period for long-term incentives is three years (rather than seven). Additional tables or charts could present a clearer picture of performance alignment. How could you do it? Demonstrating alignment with corporate strategy is most effective if the key financial metrics and performance against them have been referred to earlier in the annual report. A consistent message is clearest where the presentation of corporate KPIs is consistent throughout the annual report. In order to address these two points in relation to the TSR chart, a company could show payouts against a financial KPI that is more relevant to the company and/or an actual metric used in the incentives and over a more relevant timeframe. This should help demonstrate successful pay for performance. 11

")

12 6. Pay alignment with company KPIs (2 of 2) 12

13 7. Shares and holdings Why is it important? The disclosure regulations require companies to present a snapshot of each director s shareholdings at the financial year end. This is a considerable reduction in the volume of information required under the previous regime and for some investors this may be a step too far. GC100 Guidance suggests that additional information relating to the timing of the award and share price at grant (and option exercise price) should be given. Although detailed information must be given of the share incentives awarded and vesting in the period, it is often difficult to see how the movement is reflected in the overall shareholding. How could you do it? It is far more helpful for company stakeholders to provide more information on this than is required under the regulations. For example, disclosure could include a table showing the reconciliation of share interests and holdings for each Director between the prior year and the year of reporting. This would include where shares have been sold or bought, and where shares were described last year as being subject to performance conditions have vested or lapsed. To make use of graphics, a chart showing actual shareholding against requirement is a quick way to provide this information. Most companies now require or encourage their executives to maintain a multiple of salary in shares. There is a requirement to disclose whether or not the shareholding guideline has been met. Many companies meet this disclosure requirement by simply making a statement (in the affirmative or otherwise) without further detail as to the extent that the guideline has been met, what is taken into account and how it is measured. 13

14 Communicate in the way that s right for your company This paper makes a number of suggestions for improving the quality of remuneration reporting. It is not intended that these should compromise compliance with the regulations but that they should complement the regulatory requirements. The inflexibility of the disclosure regulations means that companies are often forced to provide information in a way that does not reflect the true nature or circumstances of the payment. In this document, we have suggested that some of the detailed tables required by the regulations are relegated to an appendix and that more relevant disclosures that have been tailored to the company s particular scenarios are included in the Chairman s Statement or an upfront summary of remuneration earned in respect of the year. It should be stressed that these are ideas that have been evolved for the fictional company (Generico) that has been at the heart of the Report Leadership project since We don t anticipate that all of these ideas will work for any company or that any of the ideas can be used without adaptation. Our aim, in putting together this report, was to encourage companies to rise to the challenge from investors to differentiate their remuneration reports from those of other companies and to consider what good reporting might look like in the context of their own remuneration framework and particular issues. We would be delighted to discuss with you how the examples in this report could be modified to provide transparent disclosure of directors remuneration in your company. 14

15 Contacts If you would like to discuss the implications for your organisation, please contact your usual adviser or: Tom Gosling T: +44 (0) E: Marcus Peaker T: +44 (0) E: Paul Wolstenholme T: +44 (0) E: Roz Crawford T: +44 (0) E: Fiona Camenzuli T: +44 (0) E: Phillippa O Connor T: +44 (0) E: phillippa.o.connor@uk.pwc.com Daniel Hepburn T: +44 (0) E: daniel.c.hepburn@uk.pwc.com Gemma Carr T: +44 (0) E: gemma.a.carr@uk.pwc.com The contributors to the Report Leadership initiative on which the mock-ups in this report are based are the Chartered Institute of Management Accountants (CIMA), PricewaterhouseCoopers LLP and Radley Yeldar. Other than, these bodies did not contribute to this specific report. 15

16 This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers Legal LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it PricewaterhouseCoopers Legal LLP. All rights reserved. PricewaterhouseCoopers Legal LLP is a member of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity SO-OS