Audits of Group Financial Statements

|

|

|

- Denis Welch

- 6 years ago

- Views:

Transcription

1 Audits of Group Financial Statements

2 Got these? Subsidiaries Divisions Different business activities/locations JVs Equity and cost method investments VIEs Investment in REITs

3 Can the auditor act as a principal? Decision based on the significance of the audit performed Coverage: how much of the revenue or how much of the balance sheet being audited by principal auditor SEC: Generally, the principal auditor is expected to have audited or assumed responsibility for reporting on at least 50% of the assets and revenues of the consolidated entity Many firms adopted this guidance as a threshold issue If other auditors are involved, two decision points: Make reference Do not make reference

4 In all cases: Determine professional reputation of other auditors Obtain representation as to independence Determine through communication with other auditor That they are aware their work on the component will be included in the financial statements That they are familiar with US GAAS and will conduct their audit in accordance with those standards Knowledge of relevant reporting requirement A review will be made with respect to the elimination of intercompany transactions and accounts and other matters

5 Decision to not make reference can be made when: Audit performed by associate firm whose work is deemed to be acceptable; or The other auditor was hired by the principal auditor and performed procedures at the direction of; or Principal auditor takes steps to satisfy himself that the work was adequately performed; or The portion of the financial statements audited by others was not material

6 When not making reference Meet with other auditor to discuss procedures Review programs, and provide additional instructions if necessary Review working papers of the other auditor In some cases, perform additional procedures on the accounts of the entity

7 When making reference Disclose in the report that certain components were audited by others Disclose the magnitude of the components audited by others Do not imply that the division of responsibility somehow is construed as a qualified opinion (i.e. somehow inferior to standard auditors report)

8 Current AICPA (AU 543) Focus: Auditors Basic Approach Principal Auditor Other Auditor Clarified AICPA AU-C 600 Focus: Group Risk Assessment & Effectiveness Group Auditor Component Auditor

9 New Concepts: A group all the components whose financial information are included in the group financial statements A component an entity or business activity, whose financial information should be included in group financial statements Group engagement partner replaces principal auditor and refers specifically to the individual responsible for the group audit performance and report Group engagement team partners and staff that establish audit strategy, communicate with component auditors, perform work on the consolidation and evaluate conclusions drawn from the audit evidence

10 Responsibilities of the group engagement partner: Direction, supervision and performance of the group audit engagement in compliance with audit standards and legal requirements Determining whether the auditors report is appropriate in the circumstances

11 Meeting the responsibilities The group engagement team can assist the group engagement partner in meeting the requirements However, if other auditors do not meet the definition of a member of the group engagement team, then they are considered component auditors Thus, a component auditor can be a network firm or even a different office of the same firm Example: National firm audits a consolidated financial statement which includes a subsidiary in LA. If the firm delegates the auditor of the subsidiary to its LA office, it is likely the LA office would be considered a component auditor and this standard would apply.

12 Change in Focus The group audit itself rather than the interactions with other auditors Moves toward a more unified approach focusing on the group financial statements rather than pieces of it. Moves away from the coverage concept. Changes the terminology from a decision whether to make reference to other auditor to one of responsibility.

13 Facts: Company X has inventory located at a remote location (e.g. warehouse in another state), but does not have prepare separate financial information for that remote location. Question: Does the use of another auditor to observe the inventory count mean the audit is a group audit?

14 Audit Report Holding Company Sub 1 Sub 2 Sub 3

15 Audit Report Company A Division 1 Division 2 Division 3

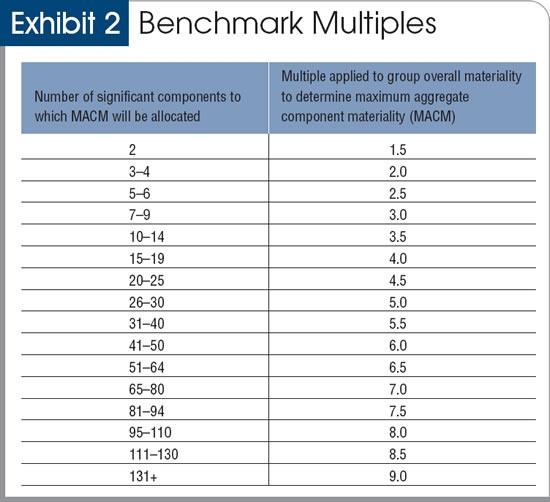

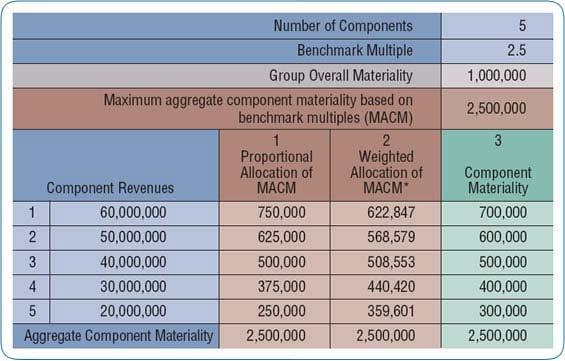

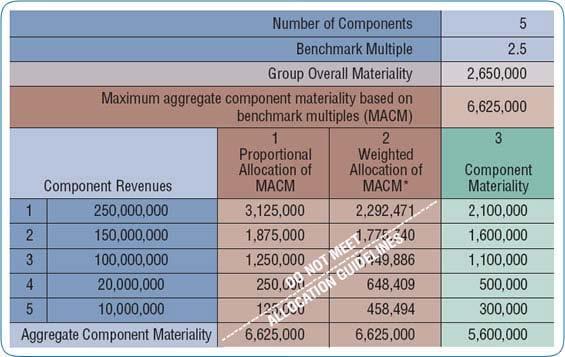

16 All facilities distribute the same product. No individual financial information prepared. Toronto Facility Company A (Roanoke) Roanoke Facility Audit Report Memphis Facility

17 All facilities distribute the same product. No individual financial information prepared. Toronto Facility Company A (Roanoke) Roanoke Facility Audit Report Memphis Facility Other Auditor performs inventory observation

18 All facilities distribute the same product. No individual financial information prepared. Toronto Facility Company A (Roanoke) Roanoke Facility Audit Report Memphis Facility Other Auditor performs limited procedures

19 All facilities distribute the same product. Individual financial information prepared. Toronto Facility Company A (Roanoke) Roanoke Facility Audit Report Memphis Facility

20 All facilities distribute the same product. Individual financial information prepared. Toronto Facility Company A (Roanoke) Roanoke Facility Audit Report Memphis Facility Other Auditor Audits & issues stand-alone statements

21 Pre-Clarified AICPA (AU 543) Focus: Auditors Basic Approach Principal Auditor Other Auditor Clarified AICPA AU-C 600 Focus: Group Risk Assessment & Effectiveness Group Auditor Component Auditor

22 Component materiality should be determined for all components regardless of whether reference is being made to component auditor Component materiality and performance materiality should be lower than group materiality and performance materiality A threshold for trivial misstatements should also be established for each component.

23 Different materiality may be established for different components The aggregate of component materiality may exceed group materiality Component materiality should be allocated to the components where reference is being made; this is likely to differ that what is actually used

24 Allocating component materiality can effectively lead to efficiencies No specific methodology provided in the SAS Helpful article in Journal of Accountancy, December 2008 Component Materiality for Group Audits omponentmaterialityforgroupaudits.htm Uses probability concepts similar to theory for allocating materiality to elements of the financial statements

25

26

27

28

29 41 Technical Questions and Answers Nonauthoritative guidance Where can you find it? TIS Section 8800, Audits of Group Financial Statements and Work of Others On AICPA website chnicalquestionsandanswers.aspx

30 Questions and Answer Topics Applicability of AU-Section 600 Making Reference to Any or All Component Auditors Deciding to Act as Auditor of Group Financial Statements Factors to Consider Regarding Component Auditors Component Financial Statements Prepared in Accordance With International Financial Reporting Standards Governmental Financial Statements that Include a GAAP-Basis Component

31 Questions and Answer Topics Component Auditor Performed in Accordance with International Standards on Auditing Component Audit Performed with Government Auditing Standards Component Auditor Performed by Other Engagement Teams of the Same Firm Terms of the Group Audit Engagement Equity Method Investment Component Criteria for Identifying Components Criteria for Identifying Significant Components No Significant Components are Identified

32 Questions and Answer Topics Restricted Access to Component Auditor Documentation Responsibilities With Respect to Fraud in a Group Audit Inclusion of Component Auditor in Engagement Team Discussions Determining Component Materiality Understanding of Component Auditor Whose Work Will not be Used Involvement in the Work of a Component Auditor

33 Questions and Answer Topics Factors Affecting Involvement in the Work of a Component Auditor Form of Communication with Component Auditors Use of Component Materiality when the Component is Not Reported on Separately Applicability of AU-C Section 600 When Only One Engagement Team is Involved Applicability of AU-C Section 600 When Making Reference to the Audit of an Equity Method Investee Procedures Required When Making Reference to the Audit of an Equity Method Investee Circumstances in Which Making Reference is Inappropriate

34 Questions and Answer Topics Lack of Response from a Component Auditor Equity Investee s Financial Statements Reviewed, and Investment is a Significant Component Making Reference to Review Report Review of Component That is Not Significant Performed by Another Practitioner Issuance of Component Auditor s Report Structure of Component Auditor Engagement

35 Questions and Answer Topics Subsequent Events Procedures Relating to a Component Component and Group have Different Year-Ends Investments Held in a Financial Statement Presented at Cost or Fair Value Employee Benefit Plan Using Investee Results to Calculate Fair Value Using Net Asset Value to Calculate Fair Value Disaggregation of Account Balances or Classes of Transactions

36 Technical Information Service Questions and Answers

37 Inquiry Do the requirements of AU-C section 600, Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) (AICPA, Professional Standards), apply only when the auditor makes reference to the audit of another auditor in his or her report on the group financial statements? Reply No. AU-C section 600 applies to all audits of group financial statements. Certain requirements (detailed in paragraphs of AU-C section 600) are applicable to all components, except those for which the auditor of the group financial statements is making reference to the work of a component auditor. (See paragraph.08 of AU-C section 600.)

38 Inquiry What factors might the group engagement partner consider when deciding to use the work of a component auditor and whether to make reference to the component auditor in the auditor s report on the group financial statements? Reply In all group audits, the group engagement team is required to obtain an understanding of the component auditor, and the group engagement partner uses this and his or her understanding of the component when deciding to use the work of a component auditor and whether to make reference to the component auditor in the auditor s report on the group financial statements. Factors affecting this decision include (a) differences in the financial reporting framework applied in preparing the component and group financial statements, (b) whether the audit of the component financial statements will be completed in time to meet the group reporting schedule, (c) differences in the auditing and other standards applied by the component auditor and those applied in the audit of the group financial statements, and (d) whether it is impracticable for the group engagement team to be involved in the work of the component auditor.

39 Inquiry What matters are required to be included in the terms of the group audit engagement? Reply The auditor of the group financial statements is required to agree upon the terms of the group audit engagement. In addition to the matters identified in AU-C section 210, Terms of Engagement (AICPA, Professional Standards), other matters may be included in the terms of a group audit, including whether reference will be made to the audit of a component auditor in the auditor s report on the group financial statements. The terms of the engagement may also include arrangements to facilitate (a) unrestricted communication between the group engagement team and component auditors to the extent permitted by law or regulation and (b) communication to the group engagement team of important communications between (i) component auditors, those charged with governance of the component, and component management and (ii) regulatory authorities and components related to financial reporting matters. (See paragraphs.17 and.a28 of AU-C section 600.)

40 Inquiry What criteria might the group engagement team use to identify components? Reply A component is defined as "[a]n entity or business activity for which group or component management prepares financial information that is required by the applicable financial reporting framework to be included in the group financial statements." The structure of a group and the nature of the financial information and the manner in which it is reported affect how the group engagement team identifies components. Components can be separate entities or may be identified on the basis of the group financial reporting system that may be (a) a parent, one or more subsidiaries, and so on; (b) a head office and one or more divisions or branches; or (c) both. (See paragraphs.11 and.a1 of AU-C section 600.) In audits of state and local governments, a component may be a separate legal entity reported as a component unit or part of the governmental entity, such as a business activity, department, or program. (See paragraph.a5 of AU-C section 600.)

41 Inquiry If the group engagement partner decides to make reference to a component auditor in the auditor s report on the group financial statements, does the group engagement team establish materiality for the component auditor to use in the separate audit of the component s financial statements? Reply No. Reference in the group auditor s report to the fact that part of the audit was conducted by a component auditor is intended to communicate that the group auditor is not assuming responsibility for the work of the component auditor. In that case, the component auditor is responsible for establishing materiality as part of performing the audit of the component s financial statements. However, if the group engagement partner assumes responsibility for the work of a component auditor, the group engagement team is required to evaluate the appropriateness of materiality at the component level. In addition, the group engagement team is required to communicate the relevant component materiality to that component auditor. The component auditor uses component materiality to evaluate whether uncorrected detected misstatements are material, individually or in the aggregate. (See paragraphs.31,.52.53,.55, and.a73.a74 of AU-C section 600.)

42 Inquiry Is the group engagement team required to obtain an understanding of a component auditor for a component that is not a significant component if the group engagement team does not plan to use the work of the component auditor and plans only to perform analytical procedures at a group level? Reply No. It is not necessary to obtain an understanding of the auditors of those components for which the group auditor will not be using the work of the component auditor to provide audit evidence for the group audit. (See paragraphs.22,.29, and.a41 of AU-C section 600.)

43 Inquiry When the group engagement partner decides to assume responsibility for the work of a component auditor, is the group engagement team required to be involved in the work of the component auditor? Reply Yes. The group engagement team is required to determine the type of work to be performed by the group engagement team (or a component auditor on behalf of the group engagement team) on the financial information of a component. The group engagement team is also required to determine the nature, timing, and extent of its involvement in the work of the component auditor. (See paragraph.51 of AU-C section 600.)

44 Inquiry What factors might affect the group engagement team s involvement in the work of a component auditor? Reply Factors that may affect the group engagement team s involvement in the work of a component auditor include (a) the significance of the component, (b) identified significant risks of material misstatement of the group financial statements, and (c) the group engagement team s understanding of the component auditor. (See paragraph.a84 of AU-C section 600.)

45 Inquiry Is it necessary to use a component materiality lower than group materiality when the component will not be reported on separately, and the audit of the entire group is being performed by the group engagement team as one audit?

46 Reply If the component is a significant component on which the group engagement team will be performing audit procedures, the group engagement team is required to determine component materiality. (See paragraph.31 of AU-C section 600.) To reduce the risk that uncorrected and undetected misstatements in each component s financial statements, when aggregated, exceeds the materiality for the group s financial statements as a whole, component materiality should be less than the materiality for the group financial statements as a whole. In circumstances when appropriate responses to assessed risks of material misstatement for some or all accounts or classes of transactions may be implemented at the group level, for example when accounts receivable for the parent and subsidiaries use the same system and the consolidated accounts receivable are audited as one aggregated amount, there is no risk of aggregation error and, therefore, no need to allocate materiality to components.

47 Inquiry Are there any circumstances in which it would be inappropriate to make reference to the audit of a component auditor of an equity investee in the auditor s report on the group financial statements? Reply AU-C section 600 precludes the auditor of the group financial statements from making reference to the audit of the component auditor in the following circumstances: When the group engagement team has serious concerns about the component auditor s professional competency or independence. (In this circumstance, the group auditor is precluded from using the work of the component auditor at all.) The component auditor s report on the equity investee s financial statements is restricted regarding use. The audit of the component was not performed in accordance with the relevant requirements of GAAS or, if applicable, the standards promulgated by the Public Company Accounting Oversight Board (PCAOB). The financial statements of the component (that is, the equity investee) and group are prepared in accordance with different financial reporting frameworks, unless certain conditions are met.

48 Inquiry Company X has an equity investment in Entity A that is not considered a significant component. A review of the financial statements of Entity A has been performed by another practitioner. Can the group engagement team use the work of the practitioner as part of the audit evidence for the audit of the group financial statements? Reply Paragraphs of AU-C section 600 discuss certain procedures to be performed on a component when the component is not a significant component. In certain circumstances, a review of a component s financial statements may be sufficient audit evidence. Therefore, a group auditor may use the work of another practitioner if the review meets the needs of the group auditor. Although the group auditor may use the review as part of the auditor s evidence for the audit of the group financial statements, the group auditor is not permitted to make reference to the practitioner s review report.

49 FURTHER QUESTIONS/COMMENTS

TIS Section 8800, Audits of Group Financial Statements and Work of Others

TIS Section 8800, Audits of Group Financial Statements and Work of Others.01 Applicability of AU-C Section 600 Inquiry Do the requirements of AU-C section 600, Special Considerations Audits of Group Financial

TIS Section 8800, Audits of Group Financial Statements and Work of Others.01 Applicability of AU-C Section 600 Inquiry Do the requirements of AU-C section 600, Special Considerations Audits of Group Financial

Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors)

") Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) CONTENTS

CONTENTS") SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

International Standard on Auditing (UK) 600 (Revised June 2016)

600 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

Navigating the New AU-C 600 Group Audit Rules Managing Responsibilities and Risk in Engagements Involving Multiple Auditors and Components

Presenting a live 110-minute teleconference with interactive Q&A Navigating the New AU-C 600 Group Audit Rules Managing Responsibilities and Risk in Engagements Involving Multiple Auditors and Components

Presenting a live 110-minute teleconference with interactive Q&A Navigating the New AU-C 600 Group Audit Rules Managing Responsibilities and Risk in Engagements Involving Multiple Auditors and Components

Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over Financial Reporting

Reporting on an Examination of Controls at a Service Organization 1621 AT-C Section 320 Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over

Reporting on an Examination of Controls at a Service Organization 1621 AT-C Section 320 Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

Engagement Quality Review

AUDITING STANDARD NO. 7 Engagement Quality Review Auditing Standard No. 7 Engagement Quality Review [Effective pursuant to SEC Release No. 34-61363, File No. PCAOB-2009-02 (January 15, 2010)] 493 Auditing

AUDITING STANDARD NO. 7 Engagement Quality Review Auditing Standard No. 7 Engagement Quality Review [Effective pursuant to SEC Release No. 34-61363, File No. PCAOB-2009-02 (January 15, 2010)] 493 Auditing

Terms of Engagement 105. Source: SAS No Effective for audits of financial statements for periods ending on or after December 15, 2012.

Terms of Engagement 105 AU-C Section 210 Terms of Engagement Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This

Terms of Engagement 105 AU-C Section 210 Terms of Engagement Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This

FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010)

") SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

Chapter 02. Professional Standards. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Mapping Document AU Section 322 to Clarified Statement on Auditing Standards Using the Work of Internal Auditors

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits AGS 10 Joint Audits was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public Accountants

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits AGS 10 Joint Audits was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public Accountants

Planning an Audit 259

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS. Preface

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

Standing Advisory Group Meeting

1666 K STREET NW, 9 TH FLOOR WASHINGTON, DC 20006 TELEPHONE: (202) 207-9100 FACSIMILE: (202) 862-8430 www.pcaobus.org Agenda Item 9 Standing Advisory Group Meeting Potential Standard Engagement Quality

1666 K STREET NW, 9 TH FLOOR WASHINGTON, DC 20006 TELEPHONE: (202) 207-9100 FACSIMILE: (202) 862-8430 www.pcaobus.org Agenda Item 9 Standing Advisory Group Meeting Potential Standard Engagement Quality

Statement on February 2014 Auditing Standards 128. Using the Work of Internal Auditors

Statement on February 2014 Auditing Standards 128 Issued by the Auditing Standards Board Using the Work of Internal Auditors (Supersedes Statement on Auditing Standards [SAS] No. 65, The Auditor's Consideration

Statement on February 2014 Auditing Standards 128 Issued by the Auditing Standards Board Using the Work of Internal Auditors (Supersedes Statement on Auditing Standards [SAS] No. 65, The Auditor's Consideration

The Auditor s Communication With Those Charged With Governance

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

ASB Meeting October 16-19, Comparison of PCAOB AS 16, Communication with Audit Committees (AS1301), to the Requirements of GAAS

, to the Requirements of GAAS") ASB Meeting October 16-19, 2017 Agenda Item 2B Comparison of with Audit Committees (AS1301), to the Requirements of GAAS Note: for purposes of the comparison, references to those charged with governance

ASB Meeting October 16-19, 2017 Agenda Item 2B Comparison of with Audit Committees (AS1301), to the Requirements of GAAS Note: for purposes of the comparison, references to those charged with governance

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY AUDIT PLANNING

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

Reporting on Pro Forma Financial Information

Reporting on Pro Forma Financial Information 1509 AT Section 401 Reporting on Pro Forma Financial Information Source: SSAE No. 10. Effective when the presentation of pro forma financial information is

Reporting on Pro Forma Financial Information 1509 AT Section 401 Reporting on Pro Forma Financial Information Source: SSAE No. 10. Effective when the presentation of pro forma financial information is

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

May 3, To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS May 3, 2016 To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS May 3, 2016 To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Report on Inspection of K. R. Margetson Ltd. (Headquartered in Vancouver, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Navigating the PCAOB s and SEC s internal control expectations A discussion. June 2015

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS)

") 100-230 THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS) EFFECTIVE DATE AND APPLICABILITY Original Pronouncements

100-230 THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS) EFFECTIVE DATE AND APPLICABILITY Original Pronouncements

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Not much going on here SAS 122 was the Super SAS But has been followed by several additional SASs in recent years, including SASs

1 Not much going on here SAS 122 was the Super SAS But has been followed by several additional SASs in recent years, including SASs 123-132 2 SAS 123, Omnibus Statement on Auditing Standards 2011 SAS 124,

1 Not much going on here SAS 122 was the Super SAS But has been followed by several additional SASs in recent years, including SASs 123-132 2 SAS 123, Omnibus Statement on Auditing Standards 2011 SAS 124,

Companion Policy Acceptable Accounting Principles and Auditing Standards

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEM SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

Reporting on Pro Forma Financial Information

Reporting on Pro Forma Financial Information 1581 AT-C Section 310 Reporting on Pro Forma Financial Information Source: SSAE No. 18. Effective for practitioners' examination and review reports on pro forma

Reporting on Pro Forma Financial Information 1581 AT-C Section 310 Reporting on Pro Forma Financial Information Source: SSAE No. 18. Effective for practitioners' examination and review reports on pro forma

AICPA ACCOUNTING AND AUDIT MANUAL 1

AICPA ACCOUNTING AND AUDIT MANUAL 1 ACCOUNTING AND AUDIT MANUAL AAM Section 1000 Introduction The AICPA Audit and Accounting Manual has not been approved, disapproved, or otherwise acted upon by any senior

AICPA ACCOUNTING AND AUDIT MANUAL 1 ACCOUNTING AND AUDIT MANUAL AAM Section 1000 Introduction The AICPA Audit and Accounting Manual has not been approved, disapproved, or otherwise acted upon by any senior

VERSION #1 PLEASE WRITE ON YOUR SCANTRON

VERSION #1 PLEASE WRITE ON YOUR SCANTRON ECON 132A MIDTERM #1 ANDERSON PLEASE answer multiple choice questions on green scantron and the rest in your blue book. When you are done put your scantron inside

VERSION #1 PLEASE WRITE ON YOUR SCANTRON ECON 132A MIDTERM #1 ANDERSON PLEASE answer multiple choice questions on green scantron and the rest in your blue book. When you are done put your scantron inside

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

Report on Inspection of KPMG Auditores Consultores Ltda. (Headquartered in Santiago, Republic of Chile)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Using the Work of an Auditor s Specialist

Using the Work of an Auditor s Specialist 749 AU-C Section 620 Using the Work of an Auditor s Specialist Source: SAS No. 122. See section 9620 for interpretations of this section. Effective for audits

Using the Work of an Auditor s Specialist 749 AU-C Section 620 Using the Work of an Auditor s Specialist Source: SAS No. 122. See section 9620 for interpretations of this section. Effective for audits

System Reviews Performed at a Location Other Than the Reviewed Firm s Office Surprise Engagements... 4

December 2017 PRP Section 3100 Supplemental Guidance Contents Notice to Readers... 2 Review Requirements for Joint Ventures... 3 System Reviews Performed at a Location Other Than the Reviewed Firm s Office...

December 2017 PRP Section 3100 Supplemental Guidance Contents Notice to Readers... 2 Review Requirements for Joint Ventures... 3 System Reviews Performed at a Location Other Than the Reviewed Firm s Office...

1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002).

.") Chapter 02 The Financial Statement Auditing Environment True / False Questions 1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002). True False 2. The

Chapter 02 The Financial Statement Auditing Environment True / False Questions 1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002). True False 2. The

Agenda Item 1B (marked) Proposed SAS, Communicating Key Audit Matters in the Independent Auditor s Report (AU-C 701)

Proposed SAS, Communicating Key Audit Matters in the Independent Auditor s Report (AU-C 701)") ASB Meeting July 17-20, 2017 Agenda Item 1B (marked) Proposed SAS, Communicating Key Audit Matters in the Independent Auditor s Report (AU-C 701) Requirements Application Material Introduction Scope of

ASB Meeting July 17-20, 2017 Agenda Item 1B (marked) Proposed SAS, Communicating Key Audit Matters in the Independent Auditor s Report (AU-C 701) Requirements Application Material Introduction Scope of

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

New auditing regime: checklist [1]

![New auditing regime: checklist [1]](/thumbs/75/72255631.jpg "New auditing regime: checklist [1]") Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items

501 Audit Evidence Specific Considerations for Selected Items") International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

Standards on Auditing

Standards on Auditing 1. SA 320 (Revised) Materiality in Planning and Performing an Audit 2. SA 530 (Revised) Audit Sampling 1 SA 320 (Revised) Materiality in Planning and Performing an Audit 2 Scope:

Standards on Auditing 1. SA 320 (Revised) Materiality in Planning and Performing an Audit 2. SA 530 (Revised) Audit Sampling 1 SA 320 (Revised) Materiality in Planning and Performing an Audit 2 Scope:

Compliance Attestation

Compliance Attestation 1603 AT-C Section 315 Compliance Attestation Source: SSAE No. 18. Effective for practitioners' examination reports on compliance with specified requirements and for practitioners'

Compliance Attestation 1603 AT-C Section 315 Compliance Attestation Source: SSAE No. 18. Effective for practitioners' examination reports on compliance with specified requirements and for practitioners'

Sample Independent Auditor s Reports

PROPOSED AUDIT GUIDANCE STATEMENT ED AGS 1 Sample Independent Auditor s Reports New Appendix 1J Sample Auditor s Report on Revised Financial Statements Comments are requested by 23 September 2018. 1 PROPOSED

PROPOSED AUDIT GUIDANCE STATEMENT ED AGS 1 Sample Independent Auditor s Reports New Appendix 1J Sample Auditor s Report on Revised Financial Statements Comments are requested by 23 September 2018. 1 PROPOSED

Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures

Auditing Accounting Estimates 511 AU-C Section 540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures Source: SAS No. 122. Effective for audits of financial

Auditing Accounting Estimates 511 AU-C Section 540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures Source: SAS No. 122. Effective for audits of financial

FOCUS ON PRACTICE INSPECTION FINDINGS

June 2006 To: All practising offices Background FOCUS ON PRACTICE INSPECTION FINDINGS 2005-2006 The practice inspection committee reviews the annual inspection results to identify those areas where adherence

June 2006 To: All practising offices Background FOCUS ON PRACTICE INSPECTION FINDINGS 2005-2006 The practice inspection committee reviews the annual inspection results to identify those areas where adherence

Characteristics of Audit Sampling 7

Chapter 1 Characteristics of Audit Sampling 7 Characteristics of Audit Sampling 1.01 This chapter defines audit sampling and illustrates the difference between procedures that involve audit sampling and

Chapter 1 Characteristics of Audit Sampling 7 Characteristics of Audit Sampling 1.01 This chapter defines audit sampling and illustrates the difference between procedures that involve audit sampling and

GAQC Web Event. Group Audits: A Look Back One Year Later and Lessons Learned. Group Audits: A Look Back One Year Later and Lessons Learned

Group Audits: A Look Back One Year Later A Web Event Trouble Shooting Troubleshooting Tips No Audio? Ensure that your computer speakers are turned on that the volume is appropriately set Check to ensure

Group Audits: A Look Back One Year Later A Web Event Trouble Shooting Troubleshooting Tips No Audio? Ensure that your computer speakers are turned on that the volume is appropriately set Check to ensure

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing Standard 16

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services

General Principles for Engagements 2115 AR-C Section 60 General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services Source: SSARS No. 21;

General Principles for Engagements 2115 AR-C Section 60 General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services Source: SSARS No. 21;

Independent Auditor s report

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

2013 PUBLIC ENTITIES OVERVIEW FOR KNOWLEDGE COACH USERS

2013 PUBLIC ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

2013 PUBLIC ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

Accounting and Review Services Committee Meeting Highlights May 9-11, 2017

Accounting and Review Services Committee Meeting Highlights May 9-11, 2017 Committee members present: Mike Fleming, Chair Denny Ard Sheila Balzer (on May 9-10 only) Jimmy Burkes Jeremy Dillard David Johnson

Accounting and Review Services Committee Meeting Highlights May 9-11, 2017 Committee members present: Mike Fleming, Chair Denny Ard Sheila Balzer (on May 9-10 only) Jimmy Burkes Jeremy Dillard David Johnson

1. Auditors may be independent in fact but not independent in appearance. 3. Attestation standards provide guidance for a wide variety of engagements

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)

501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)") Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

(Effective for audits of financial statements for periods ending on or after December 15, 2013) CONTENTS

CONTENTS") INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

Audit Committee of the Board of Directors Charter CNL HEALTHCARE PROPERTIES II, INC.

Audit Committee of the Board of Directors Charter CNL HEALTHCARE PROPERTIES II, INC. [Insert CNL logo] PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors

Audit Committee of the Board of Directors Charter CNL HEALTHCARE PROPERTIES II, INC. [Insert CNL logo] PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors

SA 580- Written Representations

Standard on Auditing SA 580- Written Representations Contents Introduction Objective & Definitions Management Responsibilities and Date of and Period(s) covered Doubt as to the Reliability of Written Representation

Standard on Auditing SA 580- Written Representations Contents Introduction Objective & Definitions Management Responsibilities and Date of and Period(s) covered Doubt as to the Reliability of Written Representation

2013 INSPECTION OF GEORGE STEWART, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

Via

Grant Thornton International Barry Barber Worldwide Director of Audit and Quality Control 399 Thornall Street Edison, New Jersey 08837 732-516-5500 732-516-5550 Direct 732-516-5502 Fax email barry.barber@gt.com

Grant Thornton International Barry Barber Worldwide Director of Audit and Quality Control 399 Thornall Street Edison, New Jersey 08837 732-516-5500 732-516-5550 Direct 732-516-5502 Fax email barry.barber@gt.com

Reporting on Controls at a Service Organization Bridging the Gap Between Canadian and Revised U.S. Standards AUDITING AND ASSURANCE.

AUDITING AND ASSURANCE May 2017 FOR PUBLIC ACCOUNTANTS PERFORMING AUDIT AND REVIEW ENGAGEMENTS This Auditing and Assurance Bulletin was prepared by Auditing and Assurance staff. It is not issued under

AUDITING AND ASSURANCE May 2017 FOR PUBLIC ACCOUNTANTS PERFORMING AUDIT AND REVIEW ENGAGEMENTS This Auditing and Assurance Bulletin was prepared by Auditing and Assurance staff. It is not issued under

31 May Dear Ms. Brown:

e Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: 212 773 3000 www.ey.com Ms. Phoebe W. Brown, Secretary Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, NW Washington,

e Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: 212 773 3000 www.ey.com Ms. Phoebe W. Brown, Secretary Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, NW Washington,

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

2013 INSPECTION OF ENTERPRISE CPAS, LTD.

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA

701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA") Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA... 1 5 Effective Date... 6 Objectives... 7 Definition...

Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA... 1 5 Effective Date... 6 Objectives... 7 Definition...

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15, 2016)

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15, 2016)

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

SRI LANKA AUDITING STANDARD 315 (REVISED)

") SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

International Standard on Auditing (UK) 701

701") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 701 Communicating Key Audit Matters in the Independent Auditor s Report The FRC s mission is to

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 701 Communicating Key Audit Matters in the Independent Auditor s Report The FRC s mission is to

International Standard on Auditing (Ireland) 315

315") International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

Standards on Auditing vis-a-vis Tax Audit

Standards on Auditing vis-a-vis Tax Audit -Anand Banka Rule 6G (1) The report of audit of the accounts of a person required to be furnished under section 44AB shall, (a) in the case of a person who carries

Standards on Auditing vis-a-vis Tax Audit -Anand Banka Rule 6G (1) The report of audit of the accounts of a person required to be furnished under section 44AB shall, (a) in the case of a person who carries

Chapter 02. Professional Standards. Multiple Choice Questions. 1. Control risk is

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

November 21, Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, D.C.

Deloitte & Touche LLP 10 Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: 203-761-3000 Fax: 203-834-2200 November 21, 2003 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street,

Deloitte & Touche LLP 10 Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: 203-761-3000 Fax: 203-834-2200 November 21, 2003 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street,

ASB Meeting July 30-August 1, 2013

ASB Meeting Agenda Item 2B Disposition of s in Extant AT 401, Reporting on Pro Forma Financial, in the Proposed Clarified (Mapping) s in Extant AT 401, Reporting on Pro Forma Financial in Proposed s in

ASB Meeting Agenda Item 2B Disposition of s in Extant AT 401, Reporting on Pro Forma Financial, in the Proposed Clarified (Mapping) s in Extant AT 401, Reporting on Pro Forma Financial in Proposed s in

Audit Evidence This section is effective for audits of financial statements for periods ending on or after December 15, 2012.

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

STAFF QUESTIONS AND ANSWERS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING

AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING") Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

1. Are the objectives of the practitioner in each of the chapters appropriate?

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 761 3013 www.deloitte.com May 27, 2014 Ms. Sharon Macey American Institute of Certified Public

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 761 3013 www.deloitte.com May 27, 2014 Ms. Sharon Macey American Institute of Certified Public

Disposition of Paragraphs in Extant AT 401, Reporting on Pro Forma Financial Information

Disposition of, in Chapter 6, Reporting on Pro Forma Financial of the Proposed Clarified (Mapping) s in Introduction.01 This section provides guidance to a practitioner who is engaged to issue or does

Disposition of, in Chapter 6, Reporting on Pro Forma Financial of the Proposed Clarified (Mapping) s in Introduction.01 This section provides guidance to a practitioner who is engaged to issue or does

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of

Report on Inspection of KPMG Cardenas Dosal, S.C. (Headquartered in Mexico City, United Mexican States)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

Report on Inspection of Ernst & Young Accountants LLP (Headquartered in Rotterdam, Kingdom of the Netherlands)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

1666 K Street, NW K Street, NW Washington, D.C Telephone: (202) Facsimile: (202)

Facsimile: (202)") 1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org SUPPLEMENTAL REQUEST FOR COMMENT: PROPOSED AMENDMENTS RELATING TO THE SUPERVISION OF AUDITS

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org SUPPLEMENTAL REQUEST FOR COMMENT: PROPOSED AMENDMENTS RELATING TO THE SUPERVISION OF AUDITS

13-A. Fraud Phase II Issues Paper

IAASB Main Agenda Page 2002 855 Agenda Item 13-A Convergence with US Fraud Standard 1. In March 2001, the IAPC approved revisions to ISA 240 The Auditor s Responsibility to Consider Fraud and Error in

IAASB Main Agenda Page 2002 855 Agenda Item 13-A Convergence with US Fraud Standard 1. In March 2001, the IAPC approved revisions to ISA 240 The Auditor s Responsibility to Consider Fraud and Error in

2. The auditors' report on a corporation's financial statements usually is addressed to the president of the company.

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

IAASB Agenda Item (September 2008) Page Agenda Item (MARKED FROM EXPOSURE DRAFT)

Page Agenda Item (MARKED FROM EXPOSURE DRAFT)") IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED

IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED