Public Sector Internal Auditors Body of Knowledge (BoK) T&C workshop October 18-19, 2010

|

|

|

- Angela Morrison

- 6 years ago

- Views:

Transcription

1 Public Sector Internal Auditors Body of Knowledge (BoK) T&C workshop October 18-19, 2010

2 14/12/2006

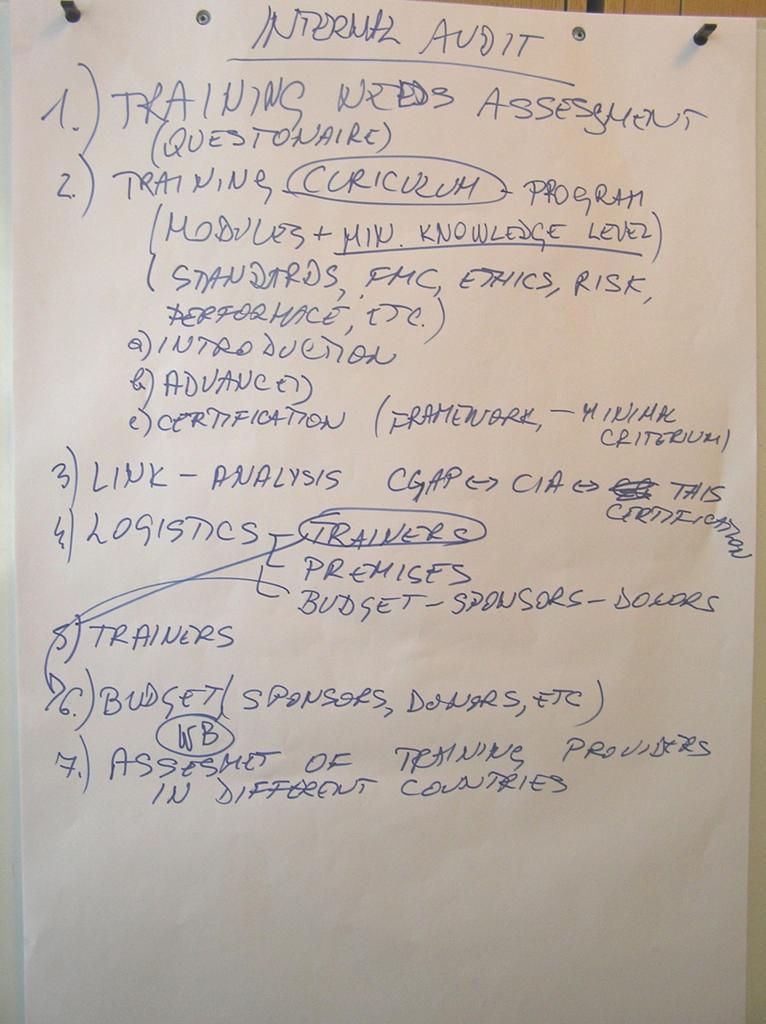

3 Yalta conclusion Members want more information and data about the content of the modules for public sector internal audit training and certification. The objective of the workshop to develop Body of knowledge (or content of internal auditors knowledge) based on work already done (and new tool from IIA), experience and ideas of the members.

4 Contents Concept overview Integration Konrad Knedler report (2008) Frederic Report (2008) IIA BoK Internal Audit Capability Model Next steps discussion, comments, ideas for improving a tool

5 Body of Knowledge? Body of Knowledge (BOK) represent the complete set of concepts, terms and activities make up a professional domain defined by the relevant professional association Examples: Project Management Body of Knowledge Body of Knowledge in Quality

6 Our inputs and process Konrad s report Frederic s report IIA BoK and IA CM CIPFA, CIA, CGAP Your ideas Public Sector IA BoK Area 1 Area 2 Area 3 Area 4 Workshop First draft Of BoK PSIA BoK

7 Konrad report Training content 1. International practice perspective It is highly recommended to place particular emphasis on international dimension. The elementary set of standards for internal audit community has been developed at international level. Development of local regulatory framework without a reference to the international practice could put in danger the idea of IA. 2. Performance management and auditing The origin of auditing is of regularity verification nature. It I still the greatest area of interest for many external audit organization. Internal auditing however due to its specific placement in the organization has a great potential to improve the organization s performance. Therefore a special focus should be places on both performance management and auditing. 3. Information Systems Information technology is becoming part of our day-to-day s life. Internal control systems are in their great parts computerized. This is the basic reason why internal auditors should cover IT issues in their professional training.

8 Konrad report Training content 4. EU perspective The European Union is the most important political organization in the continent. Its policies have substantial impact not only on the member states but also on many other countries. Moreover practices present in the EU have a tendency to spill over on numerous organizations. Many countries have aspirations to join the Union in the near or further future. That is why elements of the European Union s perspective should be included in the TCP. 5. Public sector focus Some internationally recognized certifications were initially designed for the private sector. The elementary difference in public and private sectors is asymmetry of their objectives. The first one s goal is to provide services for the public while in the case of the latter one profit maximizing is above any other goals. Public accountability is another issue which should be recognized. And this focus should be reflected in the TCP content. For individuals holding these kind international certifications and not having enough experience in public sector there should be additional training provided.

9 Konrad report Training content 6. Management techniques Since modern auditing is becoming more and more management oriented profession it is indispensable for the practitioners to get knowledge and skills in management sciences and techniques. 7. Accounting From the very beginning internal auditing have had much in common with accounting. Controls over financial reporting being one of the primary focuses of auditing constitute important part of internal control systems. Modern accounting goes far beyond its traditional bookkeeping role and is basis for decision making process. Therefore it is crucial to include it into the training syllabus.

10 Internal Audit - IIA definition (CBOK) Living reference that represents the collective knowledge of a profession. The key elements described within are referred to as Areas of Knowledge, which reflect generally accepted practices within the profession. associated activities, tasks and skills necessary to be effective in their execution, professional standards and guidance The IIA s International Professional Practices Framework (IPPF),» mandatory and» strongly recommended guidance.

11 IIA's competency framework (our workshop input) Minimum level of knowledge and skills needed to effectively operating and maintain an internal audit function Breakdown of staffing areas found in the standard audit shop, appropriate level of competency for each discipline. When reviewing the framework keep the following in mind: each ranking are being developed to further explain the associated competency. not the final format for the framework competencies and their ranking represent the ideal competencies and rankings were developed by a global task force. Do not assume that every internal auditor will progress up the ranks. There are no "industry-specific" groupings or behaviors. This is intentional at this time. We will be adding industry knowledge as it becomes available. As IT is considered a core area of knowledge for all internal auditors, it is interspersed throughout.

12 IIA CIA Part I - The Internal Audit Activity's Role in Governance, Risk, and Control Part II - Conducting the Internal Audit Engagement Part III - Business Analysis and Information Technology Part IV - Business Management Skills

13 IIA - CGAP Domain I: Standards, Governance, and Risk/Control Frameworks Domain II: Government Auditing Practice Domain III: Government Auditing Skills and Techniques Domain IV: Government Auditing Environment

14 CIPFA - Diploma in Public Audit LEVEL 1 Audit in Context Core Audit Skills Financial Accounting Systems LEVEL 2 Managing the Audit Cycle Innovation and Assurance Financial Reporting

15 Internal Audit - Capability Model Matrix Services and Role of IA People Management Professional Practices Performance Management and Accountability Organizational Relationships and Culture Governance Structures Level 5 Optimizing IA Recognized as Key Agent of Change Leadership Involvement with Professional Bodies Workforce Projection Continuous Improvement in Professional Practices Strategic IA Planning Public Reporting of IA Effectiveness Effective and Ongoing Relationships Independence, Power, and Authority of the IA Activity Level 4 Managed Overall Assurance on Governance, Risk Management, and Control IA Contributes to Management Development IA Activity Supports Professional Bodies Audit Strategy Leverages Organization s Management of Risk Integration of Qualitative and Quantitative Performance Measures CAE Advises and Influences Top-level Management Independent Oversight of the IA Activity CAE Reports to Top-level Authority Workforce Planning Level 3 Integrated Advisory Services Team Building and Competency Quality Management Framework Performance Measures Coordination with Other Review Groups Management Oversight of the IA Activity Performance/Valuefor-Money Audits Professionally Qualified Staff Workforce Coordination Risk-based Audit Plans Cost Information IA Management Reports Integral Component of Management Team Funding Mechanisms Level 2 Infrastructure Compliance Auditing Individual Professional Development Skilled People Identified and Recruited Professional Practices and Processes Framework Audit Plan Based on Management/ Stakeholder Priorities IA Operating Budget IA Business Plan Managing within the IA Activity Full Access to the Organization s Information, Assets, and People Reporting Relationship Established Level 1 Initial Ad hoc and unstructured; isolated single audits or reviews of documents and transactions for accuracy and compliance; outputs dependent upon the skills of specific individuals holding the position; no specific professional practices established other than those provided by professional associations; funding approved by management, as needed; absence of infrastructure; auditors likely part of a larger organizational unit; no established capabilities; therefore, no specific key process areas

16 EU internal control standards Standard 3: Staff competence (recruitment, training and mobility) Each Directorate General shall ensure on a permanent basis the adequacy between staff competence and their tasks by means of: defining the knowledge and skills required by each job; conducting recruitment interviews on the basis of an evaluation sheet defined by the Human Resources Unit; keeping a record of all interviews to identify potential future candidates; identifying during the recruitment process the basic immediate training plan to be followed by the new official; reviewing training needs in the context of the annual staff appraisal; ensuring that identified training needs are met as soon as possible; developing an internal training capacity in order to respond to specific needs not covered by Commission-wide training courses; defining a training and mobility policy aiming at enriching staff background and experience.

17 "Quality in a product or service is not what the supplier puts in. It is what the customer gets out and is willing to pay for." Peter Drucker ( )

18 IA Quality formula INDEPENDENCE -Legal setup -IPPF (atribute) -Ethics -Charter -Organization decree PROFESSIONALISM -IPPF (working standards) -IA Manual -Training and Certification -Continuous Professional Development QUALITY

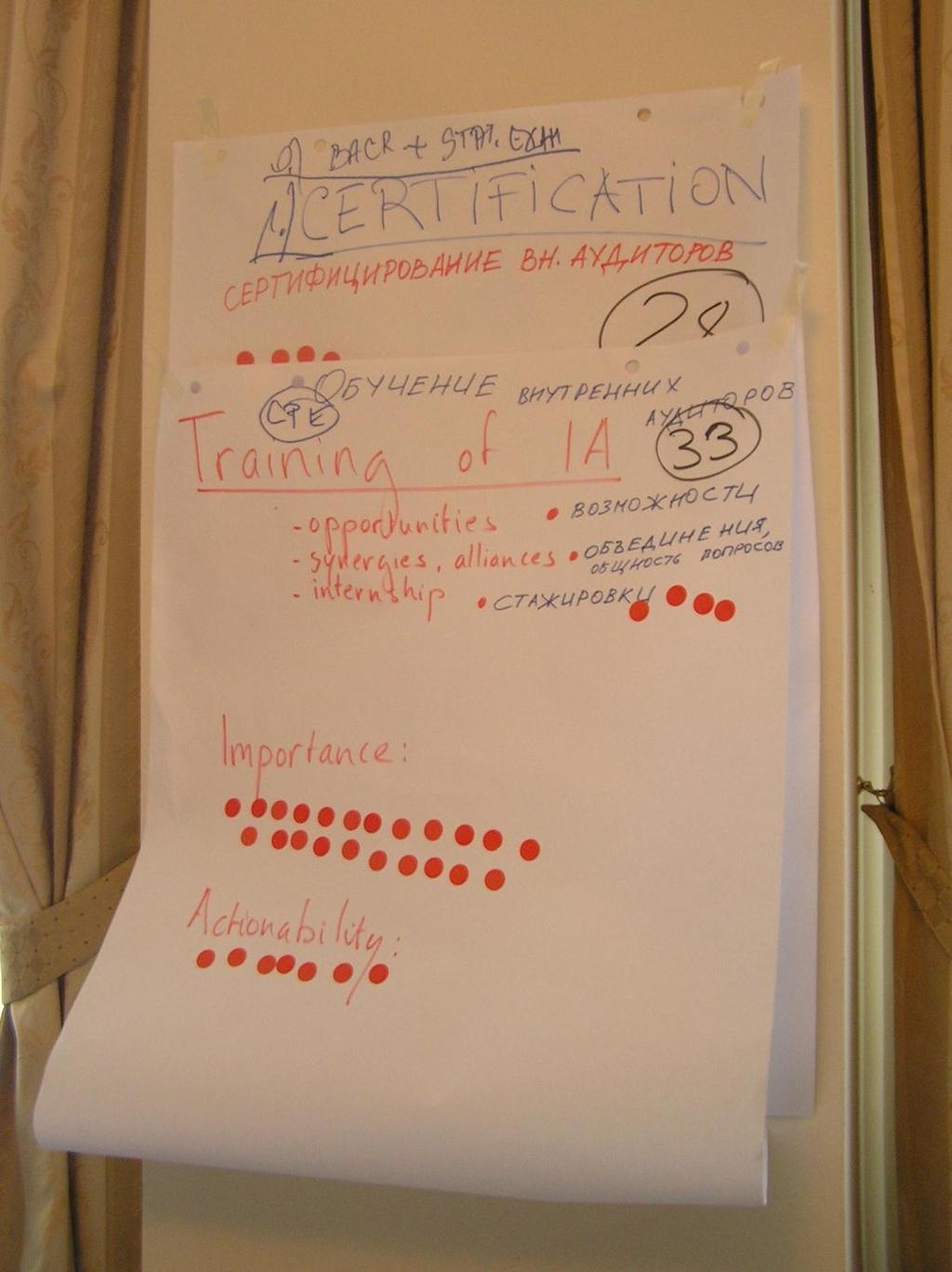

19 C. Knowledge level Public Sector Internal Auditors Body of Knowledge (draft format) Are we missing something? IAPS BoK A. Workplaces in IA This is not inside. B. Knowledge areas? Where to go? (T&C systems, literature, etc)

20 A. Workplaces in IA CAE Director Audit Mana ger Audit Senior Supervi sor Internal Audit Staff New Interna l Audito r (Less than 1 year)

21 IIA's competency framework B. Knowledge areas Attribute Standards I. INTERNAL AUDIT STANDARDS, THEORY, AND METHODOLOGY Performance Standards International Standards for the Professional Practice of Internal Auditing Definition of Internal Auditing Code of Ethics III. TOOLS AND TECHNIQUES Business Process Analysis Operational And Management Research Tools Governance Risk And Control: Tools And Techniques Forecasting Problem Solving Tools And Techniques Data Collection And Analysis Tools And Techniques Project Management Balance Scorecard Computer Assisted Auditing Techniques (Caats) IIA Competency Framework II. KNOWLEDGE AREAS Quality: Understanding Of The Quality Framework In Your Organization Governance, Risk, And Control Regulatory, Legal, And Economics Influence Managerial Accounting Information Technology Financial Accounting And Finance Ethics And Fraud IV. INTERPERSONAL SKILLS Communication Organizational Theory And Behavior IA Management - Policies And Procedures - Staffing Change Catalyst

22 B. Knowledge areas Place for improvement Public sector specifics Previous reports and work Using our knowledge and experience Next sessions

23 C. Level of knowledge 4 = Independently competent in unique and complex situations 5 Expert. I have an expert understanding of the capability. People come to me to seek advice and guidance. 3 = Independently competent in routine situations 4 Strong Capability. I have sufficient mastery of the capability to be able to adapt my approach to the capability based upon the circumstances. 2 = Basic competence and knowledge with support from others 3 Proficiency. I have proficiency in at least one approach to the capability, and am confident in that approach. 1 = Awareness only 2- Familiarity. I have an ability to perform the capability, although I need advice or to consult reference materials and documentation to provide guidance. 1 Novice. I am aware of the capability and have introductory abilities, but require regular guidance or support from reference materials and documentation. 0 0 No ability. I have no skills in the capability. I would not know how to proceed.

24 D. Where to go/what to read? Not developed Place for improvement Each country specific depending on the current T&C system CEF proposal

25 -Management and stakeholder needs -Change in IA standards and practice -Audit reports (internal+external) -Work posts + Training plans -Turnover of staff -Lack of PM knowledge -EC internal control standards+acreditation criteria NEEDS IA Training strategy > PIFC strategy BoK -Traning day in training registers -Training quality assessment -Participation/Exam results -Audit reports -Absorption of EU funds -No. of irregularities - -MoF CHU modules -Traininers+literature -Internet -Budget planining -Projects (existing and new) -Decree/legal framework

26 Next step 1: Strategy for IA Training Albana proposal How to develop a training strategy, then how to implement it? Many of countries in Region don't have yet a or they are in the phase of developing it. Some time even they have assistance from projects, they should be the primary responsible for developing the Strategy, not just wait from the consultants, or they should know what to expect from the consultants. So my idea is to include some discussions how we can develop a training strategy, where we should refer, where we can address our problems with training system ( i.e. to which institutions we can ask for support) and so on.

27 Possible next steps Creation of Training programme or part of the programme (one module) To develop and implement complete training programme

The Red (Book) Rocks The Latest and Greatest Audit Standards

Rocks The Latest and Greatest Audit Standards") The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

Certified Internal Auditor (CIA ) Exam Syllabus

Exam Syllabus") Certified Internal Auditor (CIA ) Exam Syllabus Part 1 Internal Audit Basics 125 questions 2.5 Hours (150 minutes) The CIA exam Part 1 topics tested include aspects of mandatory guidance from the IPPF;

Certified Internal Auditor (CIA ) Exam Syllabus Part 1 Internal Audit Basics 125 questions 2.5 Hours (150 minutes) The CIA exam Part 1 topics tested include aspects of mandatory guidance from the IPPF;

Understanding Changes to the Certified Internal Auditor Program for 2013

Understanding Changes to the Certified Internal Auditor Program for 2013 Certified Internal Auditor (CIA ) 2013 Content Change Overview: This document is provided by IIA Global Headquarters to explain

Understanding Changes to the Certified Internal Auditor Program for 2013 Certified Internal Auditor (CIA ) 2013 Content Change Overview: This document is provided by IIA Global Headquarters to explain

2012 IIA Standards Update

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

10/5/2016. Quality Assessment Review. Agenda. What s the purpose of a QAR? Internal Audit Manager Training October 3-4, 2016

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

What We Will Cover Today

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

August 2017 Proposal to develop a new apprenticeship standard

August 2017 Proposal to develop a new apprenticeship standard Page 1: Proposal to develop a new apprenticeship standard Q1. Please confirm that you have read the "How to" guide for Trailblazers on gov.uk

August 2017 Proposal to develop a new apprenticeship standard Page 1: Proposal to develop a new apprenticeship standard Q1. Please confirm that you have read the "How to" guide for Trailblazers on gov.uk

Implementation Guide 2000

Implementation Guide 2000 Standard 2000 Managing the Internal Audit Activity The chief audit executive must effectively manage the internal audit activity to ensure it adds value to the organization. Interpretation:

Implementation Guide 2000 Standard 2000 Managing the Internal Audit Activity The chief audit executive must effectively manage the internal audit activity to ensure it adds value to the organization. Interpretation:

Implementation Guide 2060

Implementation Guide 2060 Standard 2060 Reporting to Senior Management and the Board The chief audit executive must report periodically to senior management and the board on the internal audit activity

Implementation Guide 2060 Standard 2060 Reporting to Senior Management and the Board The chief audit executive must report periodically to senior management and the board on the internal audit activity

Control Environment Toolkit: Internal Audit Function

III. MODEL DOCUMENT: INTERNAL AUDIT DEPARTMENT CHARTER ADOPTED BY THE AUDIT COMMITTEE OF THE COMPANY MEETING MINUTES NO OF 20 SIGNATURE OF THE CHAIRPERSON OF AUDIT COMMITTEE DATED THIS DAY OF, 20 Approved

III. MODEL DOCUMENT: INTERNAL AUDIT DEPARTMENT CHARTER ADOPTED BY THE AUDIT COMMITTEE OF THE COMPANY MEETING MINUTES NO OF 20 SIGNATURE OF THE CHAIRPERSON OF AUDIT COMMITTEE DATED THIS DAY OF, 20 Approved

External Quality Assessment Are You Ready? Institute of Internal Auditors

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

The IPPF in How changes to The IIA s guidance framework can benefit internal auditors and SAIs

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

Implementation Guide 1200

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Quality Assessment Review. Agenda. The Law Says 11/16/2015. Internal Audit Management November 19-20, 2015

Quality Assessment Review Internal Audit Management November 19-20, 2015 Flerida Rivera-Alsing MBA,CPA, CIA, CFE, CISA, CRMA, CIDA, LIFA Chief Audit Executive State Board of Administration of Florida Agenda

Quality Assessment Review Internal Audit Management November 19-20, 2015 Flerida Rivera-Alsing MBA,CPA, CIA, CFE, CISA, CRMA, CIDA, LIFA Chief Audit Executive State Board of Administration of Florida Agenda

Glossary. Chartered Institute of Internal Auditors. 26 July Add value. Adequate control. Assurance services. Board. Charter

26 July 2017 Glossary Chartered Institute of Internal Auditors This glossary explains the specific meanings of some terms that are used in the The International Standards. Add value The internal audit

26 July 2017 Glossary Chartered Institute of Internal Auditors This glossary explains the specific meanings of some terms that are used in the The International Standards. Add value The internal audit

Audit Standards 6/23/2017. Outline. Let s Refresh. Changes to the IIA Standards

Audit Standards Let s Refresh Outline Changes in the Standards Changes in the Yellowbook Standards Attribute/General Standards Performance/Fieldwork Standards Reporting Standards Key Differences Changes

Audit Standards Let s Refresh Outline Changes in the Standards Changes in the Yellowbook Standards Attribute/General Standards Performance/Fieldwork Standards Reporting Standards Key Differences Changes

Lake County School District. Quality Assurance & Improvement Program. Internal Self-Assessment for. The Internal Audit Department

Lake County School District Quality Assurance & Improvement Program Internal Self-Assessment for The Internal Audit Department Fiscal Year 2017 2018 Completed By: Thomas A. Mock, CIA Date: January 31,

Lake County School District Quality Assurance & Improvement Program Internal Self-Assessment for The Internal Audit Department Fiscal Year 2017 2018 Completed By: Thomas A. Mock, CIA Date: January 31,

Strathclyde Partnership for Transport

Agenda item 5 Strathclyde Partnership for Transport Independent Examination of Internal Audit February 2017 Contents Page Executive summary 1 Section 1 Public sector internal audit standards 2 Section

Agenda item 5 Strathclyde Partnership for Transport Independent Examination of Internal Audit February 2017 Contents Page Executive summary 1 Section 1 Public sector internal audit standards 2 Section

Implementation Guide 2130

Implementation Guide 2130 Standard 2130 Control The internal audit activity must assist the organization in maintaining effective controls by evaluating their effectiveness and efficiency and by promoting

Implementation Guide 2130 Standard 2130 Control The internal audit activity must assist the organization in maintaining effective controls by evaluating their effectiveness and efficiency and by promoting

2014 Global Council. Dubai, UAE 6-9 March 2014 DAY 2. globaliia.org

2014 Global Council Dubai, UAE 6-9 March 2014 DAY 2 Opening Remarks Paul J. Sobel, Chairman of the Board Agenda - Tuesday Opening Remarks P. Sobel Expanding the Umbrella of the IIA D. Beran Tuesday Discussion

2014 Global Council Dubai, UAE 6-9 March 2014 DAY 2 Opening Remarks Paul J. Sobel, Chairman of the Board Agenda - Tuesday Opening Remarks P. Sobel Expanding the Umbrella of the IIA D. Beran Tuesday Discussion

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) ATTRIBUTE STANDARDS 1000 Purpose, Authority and Responsibility The purpose, authority, and responsibility of the internal

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) ATTRIBUTE STANDARDS 1000 Purpose, Authority and Responsibility The purpose, authority, and responsibility of the internal

The Development of Public Internal Financial Control in Albania And His Role in Strengthening the Managerial Accountability

The Development of Public Internal Financial Control in Albania And His Role in Strengthening the Managerial Accountability Doi:10.5901/ajis.2014.v3n4p301 Abstract Dr. Hysen Muceku hysen_muceku@hotmail.com

The Development of Public Internal Financial Control in Albania And His Role in Strengthening the Managerial Accountability Doi:10.5901/ajis.2014.v3n4p301 Abstract Dr. Hysen Muceku hysen_muceku@hotmail.com

Implementation Guide 1300

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

International Standards for the Professional Practice of Internal Auditing (Standards)

") Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

June 2016 Issue 05/2016

CBOK 2015: THE TOP 7 SKILLS CAEs WANT Building the right mix of talent for your organisation This report is part of the 2015 Global Internal Audit Common Body of Knowledge (CBOK) Practitioner Study series.

CBOK 2015: THE TOP 7 SKILLS CAEs WANT Building the right mix of talent for your organisation This report is part of the 2015 Global Internal Audit Common Body of Knowledge (CBOK) Practitioner Study series.

I. Mission. II. Scope of the Work

CHAPTER: I - ORGANIZATION Page: A.1 MANUAL Appendix A CHARTER FOR THE OFFICE OF THE INSPECTOR GENERAL I. Mission 1. The Office of the Inspector General (OIG) provides oversight of the programmes and operations

CHAPTER: I - ORGANIZATION Page: A.1 MANUAL Appendix A CHARTER FOR THE OFFICE OF THE INSPECTOR GENERAL I. Mission 1. The Office of the Inspector General (OIG) provides oversight of the programmes and operations

International Perspectives on Internal Control & Audit Systems in the Public Sector

International Perspectives on Internal Control & Audit Systems in the Public Sector Laurent Sauvage Senior Auditor AFTFM, The World Bank lsauvage@worldbank.org Internal Audit Conference Khartoum, Sudan

International Perspectives on Internal Control & Audit Systems in the Public Sector Laurent Sauvage Senior Auditor AFTFM, The World Bank lsauvage@worldbank.org Internal Audit Conference Khartoum, Sudan

From Dubai to Beijing

From Dubai to Beijing (How we use your GC input) Anton van Wyk, Chairman of the Board What Happens After GC? Global Council plays a key role in the governance process of The IIA. Discussion results are

From Dubai to Beijing (How we use your GC input) Anton van Wyk, Chairman of the Board What Happens After GC? Global Council plays a key role in the governance process of The IIA. Discussion results are

Implementation Guide 1000

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Benchmarking Report Share, Compare, Validate SAMPLE. Year: 2017 Your Organization Date

Benchmarking Report Share, Compare, Validate Year: 2017 Your Organization Date Benchmarking Tier 1: Your Organization Benchmarking Tier 2: Services Benchmarking Tier 3: Services $1B to $5B Benchmarking

Benchmarking Report Share, Compare, Validate Year: 2017 Your Organization Date Benchmarking Tier 1: Your Organization Benchmarking Tier 2: Services Benchmarking Tier 3: Services $1B to $5B Benchmarking

Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function

www.pwc.com/bb Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function Strengthening the Performance and Influence of the Audit Committee

www.pwc.com/bb Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function Strengthening the Performance and Influence of the Audit Committee

CIA EXAM CONTENT. Part 1 :The Internal Audit Activitys Role in Governance Risk and Control

CIA EXAM CONTENT Part 1 :The Internal Audit Activitys Role in Governance Risk and Control A. Comply with The IIA's Attribute Standards (15-25%) (P) 1. Define purpose, authority, and responsibility of the

CIA EXAM CONTENT Part 1 :The Internal Audit Activitys Role in Governance Risk and Control A. Comply with The IIA's Attribute Standards (15-25%) (P) 1. Define purpose, authority, and responsibility of the

PRACTICAL EXPERIENCE CERTIFICATE FOR INTERNATIONALLY TRAINED CANDIDATES

PRACTICAL EXPERIENCE CERTIFICATE FOR INTERNATIONALLY TRAINED CANDIDATES Please read the following information prior to completing the experience certification form as an applicant applying for admission

PRACTICAL EXPERIENCE CERTIFICATE FOR INTERNATIONALLY TRAINED CANDIDATES Please read the following information prior to completing the experience certification form as an applicant applying for admission

Practice Guide. Developing the Internal Audit Strategic Plan

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

Ministry of Finances 2 CHU for Internal Audit Internal Audit Manual Part I: Management of Internal Audit Activities

Ministry of Finances 2 CHU for Internal Audit CONTENTS Foreword...3 Acronyms...5 Chapter 1: Purpose, Structure and Contents...6 Chapter 2: Regulatory Background...8 Chapter 3: Internal Audit Policies...9

Ministry of Finances 2 CHU for Internal Audit CONTENTS Foreword...3 Acronyms...5 Chapter 1: Purpose, Structure and Contents...6 Chapter 2: Regulatory Background...8 Chapter 3: Internal Audit Policies...9

Internal Audit Mandate

1. Constitution 1.1. As a vital component of good Corporate Governance, an in-house and centralised Internal Audit function has been established by the Mr Price Group Board of Directors. 1.2. This function

1. Constitution 1.1. As a vital component of good Corporate Governance, an in-house and centralised Internal Audit function has been established by the Mr Price Group Board of Directors. 1.2. This function

Implementation Guide 1311

Implementation Guide 1311 Standard 1311 Internal Assessments Internal assessments must include: Ongoing monitoring of the performance of the internal audit activity. Periodic self-assessments or assessments

Implementation Guide 1311 Standard 1311 Internal Assessments Internal assessments must include: Ongoing monitoring of the performance of the internal audit activity. Periodic self-assessments or assessments

Policy and Procedures Date: November 5, 2017

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

Implementation Guide 1312

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER. [April 2017]

![ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER. [April 2017]](/thumbs/83/88010492.jpg "ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER. [April 2017]") ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER [April 2017] 1. SCOPE AND PURPOSE ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER s ( Energy Queensland ) Internal Auditing (IA) function provides assurance

ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER [April 2017] 1. SCOPE AND PURPOSE ENERGY QUEENSLAND LIMITED INTERNAL AUDIT CHARTER s ( Energy Queensland ) Internal Auditing (IA) function provides assurance

Certificate in Establishing an Internal Audit Function

Certificate in Establishing an Internal Audit Function Who should attend? Recently appointed Chief Audit Executives (CAE s) or those about to be appointed or wishing to apply for this role CAE s appointed

Certificate in Establishing an Internal Audit Function Who should attend? Recently appointed Chief Audit Executives (CAE s) or those about to be appointed or wishing to apply for this role CAE s appointed

SUPPLEMENT TO PROPOSED IES 2 (REVISED): MAPPING & TRACKED CHANGES DOCUMENT

: MAPPING & TRACKED CHANGES DOCUMENT") SUPPLEMENT TO EXPOSURE DRAFT, PROPOSED IES 2 (REVISED): MAPPING & TRACKED CHANGES DOCUMENT This supplement to the International Accounting Education Standards Board (IAESB) Exposure Draft, Proposed IES

SUPPLEMENT TO EXPOSURE DRAFT, PROPOSED IES 2 (REVISED): MAPPING & TRACKED CHANGES DOCUMENT This supplement to the International Accounting Education Standards Board (IAESB) Exposure Draft, Proposed IES

Natural Resources Canada

against Government of Canada and Institute of Internal Auditors Standards FINAL Report 15 December 2016 Table of Contents 1. Background... 1 2. Objective and Scope... 1 3. Approach and Methodology... 1

against Government of Canada and Institute of Internal Auditors Standards FINAL Report 15 December 2016 Table of Contents 1. Background... 1 2. Objective and Scope... 1 3. Approach and Methodology... 1

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY DRAFT Internal Audit Strategy 2018/19 Presented at the audit committee meeting of: 15 December 2017 This report is solely for the use

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY DRAFT Internal Audit Strategy 2018/19 Presented at the audit committee meeting of: 15 December 2017 This report is solely for the use

Independent Validation of the Internal Auditing Self-Assessment

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT

Canada. Internal Audit Charter 1+1. Canadian Nuclear Safety Commission. Office of Audit and Ethics. April 18, 2011

1+1 Commission canadienne de sorete nucleaire Canadian Nuclear Safety Commission Internal Audit Charter Canadian Nuclear Safety Commission Office of Audit and Ethics April 18, 2011 E-DOCS-#371 0602 v2

1+1 Commission canadienne de sorete nucleaire Canadian Nuclear Safety Commission Internal Audit Charter Canadian Nuclear Safety Commission Office of Audit and Ethics April 18, 2011 E-DOCS-#371 0602 v2

Why Internal Audit Matters

Why Internal Audit Matters Joseph Mauriello, CPA, CIA, CFE, CISA, CMA, CFSA, CRMA Director, Center for Internal Auditing Excellence The University of Texas at Dallas Financial Executives International

Why Internal Audit Matters Joseph Mauriello, CPA, CIA, CFE, CISA, CMA, CFSA, CRMA Director, Center for Internal Auditing Excellence The University of Texas at Dallas Financial Executives International

General Session 1 Operating as

General Session 1 Operating as a Global Profession and Organization Naohiro Mouri, CIA Vice Chair Professional Practices Session Objective How to better collaborate, promote greater engagement, and leverage

General Session 1 Operating as a Global Profession and Organization Naohiro Mouri, CIA Vice Chair Professional Practices Session Objective How to better collaborate, promote greater engagement, and leverage

1. INTERNAL AUDIT CHARTER (PDF)

") 1. INTERNAL AUDIT CHARTER (PDF) The Internal Audit Charter spells out the purpose, authority, and responsibility of the Internal Audit function at the University of Swaziland. The Charter also provides

1. INTERNAL AUDIT CHARTER (PDF) The Internal Audit Charter spells out the purpose, authority, and responsibility of the Internal Audit function at the University of Swaziland. The Charter also provides

Report. Quality Assessment of Internal Audit at <Organisation> Draft Report / Final Report

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Thai Oil Public Company Limited. Internal Audit Charter

Thai Oil Public Company Limited Internal Audit Charter (Translation) 1 Amendment Records Title: INTERNAL AUDIT CHARTER Issue No./ Revision No. Date Amended Sections Reasons for Amendment 01/00 23/09/09

Thai Oil Public Company Limited Internal Audit Charter (Translation) 1 Amendment Records Title: INTERNAL AUDIT CHARTER Issue No./ Revision No. Date Amended Sections Reasons for Amendment 01/00 23/09/09

External Quality Assessment of the Internal Audit Activity at. County of Orange. April County of Orange Final Report: June 13,

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

International Standards for the Professional Practice of Internal Auditing (Standards)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

The IIA s Global Internal Audit Survey. A Component of the CBOK 1 Study

The IIA s Global Internal Audit Survey A Component of the CBOK 1 Study Introduction The Institute of Internal Auditors Research Foundation (IIARF), under the auspices of the William G. Bishop III, CIA,

The IIA s Global Internal Audit Survey A Component of the CBOK 1 Study Introduction The Institute of Internal Auditors Research Foundation (IIARF), under the auspices of the William G. Bishop III, CIA,

EXPOSURE DRAFT SURVEY QUESTIONS

. MISSION OF INTERNAL AUDITING. To what extent do you support the addition of a Mission of Internal Auditing to the IPPF? Very useful in selling IA to the wider community.2 To what extent do you agree

. MISSION OF INTERNAL AUDITING. To what extent do you support the addition of a Mission of Internal Auditing to the IPPF? Very useful in selling IA to the wider community.2 To what extent do you agree

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR. September 11, 2015

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR September 11, 2015 PREPARED BY: MNP LLP 1500 640 5 th Ave SW Calgary, AB, T2P 3G4 MNP CONTACT: Maggie Kiel, CIA, MBA, ABCP,

City of Edmonton EXTERNAL QUALITY ASSESSMENT OF THE OFFICE OF THE CITY AUDITOR September 11, 2015 PREPARED BY: MNP LLP 1500 640 5 th Ave SW Calgary, AB, T2P 3G4 MNP CONTACT: Maggie Kiel, CIA, MBA, ABCP,

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

Quality Assurance and Improvement Program (QAIP)

") Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Bank of Botswana Internal Audit Charter March 18, 2013 INTERNAL AUDIT CHARTER BANK OF BOTSWANA

INTERNAL AUDIT CHARTER BANK OF BOTSWANA 1 CONTENTS PAGE 1. PURPOSE OF THE INTERNAL AUDIT CHARTER 3 2. PURPOSE OF THE INTERNAL AUDIT DIVISION 3 3. POLICY STATEMENTS 3 3.1 Establishment of the Internal Audit

INTERNAL AUDIT CHARTER BANK OF BOTSWANA 1 CONTENTS PAGE 1. PURPOSE OF THE INTERNAL AUDIT CHARTER 3 2. PURPOSE OF THE INTERNAL AUDIT DIVISION 3 3. POLICY STATEMENTS 3 3.1 Establishment of the Internal Audit

THE INSTITUTE OF INTERNAL AUDITORS. 9/18/2012 North American Strategic Planning Document

THE INSTITUTE OF INTERNAL AUDITORS 9/18/2012 North American Strategic Planning Document NORTH AMERICAN STRATEGIC PLANNING DOCUMENT The Institute of Internal Auditors Overview On June 24, 2011, a strategic

THE INSTITUTE OF INTERNAL AUDITORS 9/18/2012 North American Strategic Planning Document NORTH AMERICAN STRATEGIC PLANNING DOCUMENT The Institute of Internal Auditors Overview On June 24, 2011, a strategic

Cutting-Edge Internal Auditing Processes

Cutting-Edge Internal Auditing Processes The purpose of this very unique course is to use workshop discussions to analyze further the challenges that the CAE s are facing in setting up cutting-edge auditing

Cutting-Edge Internal Auditing Processes The purpose of this very unique course is to use workshop discussions to analyze further the challenges that the CAE s are facing in setting up cutting-edge auditing

This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department.

Corporate Audit Department.") CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

IPPF Practice Guide. Interaction with the Board

Interaction with the Board August 2011 Table of Contents Executive Summary... 1 Introduction... 1 1000 Purpose, Authority, and Responsibility... 1 Internal Auditing s Relationship with the Board... 3 A.

Interaction with the Board August 2011 Table of Contents Executive Summary... 1 Introduction... 1 1000 Purpose, Authority, and Responsibility... 1 Internal Auditing s Relationship with the Board... 3 A.

IMPACT AND IMPORTANCE OF INTERNAL AUDIT IN SUCCESSFUL MANAGEMENT OF THE ENTERPRISE

832 IMPACT AND IMPORTANCE OF INTERNAL AUDIT IN SUCCESSFUL MANAGEMENT OF THE ENTERPRISE Fatmir Mehmeti¹ 1 Audit Company ETIKA Kosovo, fatmir_mehmeti@yahoo.com Abstract Internal audit is an independent activity

832 IMPACT AND IMPORTANCE OF INTERNAL AUDIT IN SUCCESSFUL MANAGEMENT OF THE ENTERPRISE Fatmir Mehmeti¹ 1 Audit Company ETIKA Kosovo, fatmir_mehmeti@yahoo.com Abstract Internal audit is an independent activity

PUBLIC FINANCE CONTROL DEVELOPMENT IN UKRAINE

6 th Plenary meeting of PEMPAL Internal Audit Community of Practice PUBLIC FINANCE CONTROL DEVELOPMENT IN UKRAINE Head of CHU PIFC MainCRO Maxim Timokhin Ukraine, Yalta 28.05.2010 Main Public Finance Control

6 th Plenary meeting of PEMPAL Internal Audit Community of Practice PUBLIC FINANCE CONTROL DEVELOPMENT IN UKRAINE Head of CHU PIFC MainCRO Maxim Timokhin Ukraine, Yalta 28.05.2010 Main Public Finance Control

GOVERNMENT OF YUKON POLICY 1.13 GENERAL ADMINISTRATION MANUAL

GOVERNMENT OF YUKON POLICY 1.13 GENERAL ADMINISTRATION MANUAL VOLUME 1: CORPORATE POLICIES - GENERAL TITLE: GOVERNMENT INTERNAL AUDIT SERVICES (GIAS) EFFECTIVE: 16-04-01 1.0 INTRODUCTORY PROVISIONS 1.1

GOVERNMENT OF YUKON POLICY 1.13 GENERAL ADMINISTRATION MANUAL VOLUME 1: CORPORATE POLICIES - GENERAL TITLE: GOVERNMENT INTERNAL AUDIT SERVICES (GIAS) EFFECTIVE: 16-04-01 1.0 INTRODUCTORY PROVISIONS 1.1

Mike Gowell SVP and GM Wolters Kluwer

Mike Gowell SVP and GM Wolters Kluwer Mike Gowell SVP & GM, Wolters Kluwer Founder & General Manager, TeamMate Audit Management System 30 Years of audit and audit technology experience 22 Years with PwC

Mike Gowell SVP and GM Wolters Kluwer Mike Gowell SVP & GM, Wolters Kluwer Founder & General Manager, TeamMate Audit Management System 30 Years of audit and audit technology experience 22 Years with PwC

AUDITING. Auditing PAGE 1

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

INTERNAL AUDIT NEW DEVELOPMENTS & CHALLENGES BEFORE THE PROFESSION

INTERNAL AUDIT NEW DEVELOPMENTS & CHALLENGES BEFORE THE PROFESSION CA Amit Pandit JB Nagar Study Circle Of WIRC January 21, 2018 Agenda History & Evolution of Internal Audit How IA changed over a period

INTERNAL AUDIT NEW DEVELOPMENTS & CHALLENGES BEFORE THE PROFESSION CA Amit Pandit JB Nagar Study Circle Of WIRC January 21, 2018 Agenda History & Evolution of Internal Audit How IA changed over a period

CHARTER INTERNAL OVERSIGHT OFFICE (IOO)

") CHARTER INTERNAL OVERSIGHT OFFICE (IOO) VISION The vision of IOO is - To be a high-performing internal oversight activity that meets the expectations of WMO stakeholders and adheres to the professional

CHARTER INTERNAL OVERSIGHT OFFICE (IOO) VISION The vision of IOO is - To be a high-performing internal oversight activity that meets the expectations of WMO stakeholders and adheres to the professional

The Central Harmonisation function

1 The Central Harmonisation function The role and content of the central harmonisation function (CHF) is not a new topic, but there has been little guidance material available as to the nature of its duties.

1 The Central Harmonisation function The role and content of the central harmonisation function (CHF) is not a new topic, but there has been little guidance material available as to the nature of its duties.

Portfolio Management Specialist GS Career Path Guide

GS-1101 Career Path Guide August 2014 (This page intentionally left blank.) HUD LEARN Career Path Guide TABLE OF CONTENTS PORTFOLIO MANAGEMENT SPECIALIST GS-1101... 1 Career Path Guide... 1 Your Career

GS-1101 Career Path Guide August 2014 (This page intentionally left blank.) HUD LEARN Career Path Guide TABLE OF CONTENTS PORTFOLIO MANAGEMENT SPECIALIST GS-1101... 1 Career Path Guide... 1 Your Career

VACANCIES NSSF KWANZA. Jiunge Nasi. Boresha Maisha Yako

We Build Your Future VACANCIES The National Social Security Fund (NSSF) which is the leading provider of Social Security in Tanzania is hereby inviting applications from suitable, qualified, experienced,

We Build Your Future VACANCIES The National Social Security Fund (NSSF) which is the leading provider of Social Security in Tanzania is hereby inviting applications from suitable, qualified, experienced,

Diploma in Procurement and Supply

CIPS Level 4 Diploma in Procurement and Supply 4 2018 Syllabus For internal use only Introducing... Level 4 Diploma in Procurement and Supply CIPS qualifications are regulated internationally to ensure

CIPS Level 4 Diploma in Procurement and Supply 4 2018 Syllabus For internal use only Introducing... Level 4 Diploma in Procurement and Supply CIPS qualifications are regulated internationally to ensure

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure SIAAB Interpretation Adopted July 9, 2013 Revised In Accordance

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure SIAAB Interpretation Adopted July 9, 2013 Revised In Accordance

IIA Global Update. Director, IIA Global Board Chair, IIA Global Audit Committee

IIA Global Update Cathy Blunt Director, IIA Global Board Chair, IIA Global Audit Committee Steve Coates Member, IIA Professional Issues Committee Director IIA Australia Board Agenda Introduction to the

IIA Global Update Cathy Blunt Director, IIA Global Board Chair, IIA Global Audit Committee Steve Coates Member, IIA Professional Issues Committee Director IIA Australia Board Agenda Introduction to the

BUSINESS RISK MANAGEMENT LTD. Proposal for External Quality Assessment of the Internal Audit function against world class best practice

BUSINESS RISK MANAGEMENT LTD Proposal for External Quality Assessment of the Internal Audit function against world class best practice 1. Summary The following proposal outlines the suggested approach

BUSINESS RISK MANAGEMENT LTD Proposal for External Quality Assessment of the Internal Audit function against world class best practice 1. Summary The following proposal outlines the suggested approach

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment.

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment www.theiia.org/cae Overview Pulse of Internal Auditing: Assessing Emerging and Evolving Risks is a Key Priority Linking Risks

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment www.theiia.org/cae Overview Pulse of Internal Auditing: Assessing Emerging and Evolving Risks is a Key Priority Linking Risks

Quality Assurance in Internal Audit. Standard on Internal Audit (SIA) 7

7") Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

10 Imperatives for Internal Audit

The Auditing Roundtable's International Workshop 2015 The Future For Auditing Brussels, Belgium October 14-15, 2015 Driving Success in a Changing World: 10 Imperatives for Internal Audit Günther Meggeneder,

The Auditing Roundtable's International Workshop 2015 The Future For Auditing Brussels, Belgium October 14-15, 2015 Driving Success in a Changing World: 10 Imperatives for Internal Audit Günther Meggeneder,

Practice Advisory : Quality Assurance and Improvement Program

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Central Bank of Malta Job Description Template

Job Title: Head Internal Audit Department Central Bank of Malta Reports To: Chief Officer Internal Audit Department: Internal Audit Date: July 2018 Job Purpose: To lead the Audit Function at the Central

Job Title: Head Internal Audit Department Central Bank of Malta Reports To: Chief Officer Internal Audit Department: Internal Audit Date: July 2018 Job Purpose: To lead the Audit Function at the Central

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY COMPLIANCE, AUDIT, AND RISK COMMITTEE OF THE BOARD OF VISITORS COMPLIANCE, AUDIT, AND RISK CHARTER

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY COMPLIANCE, AUDIT, AND RISK COMMITTEE OF THE BOARD OF VISITORS I. PURPOSE COMPLIANCE, AUDIT, AND RISK CHARTER The primary purpose of the Compliance,

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY COMPLIANCE, AUDIT, AND RISK COMMITTEE OF THE BOARD OF VISITORS I. PURPOSE COMPLIANCE, AUDIT, AND RISK CHARTER The primary purpose of the Compliance,

Internal Audit & the Audit Committee

HCCA Audit & Compliance Committee Conference February 2008 Internal Audit & the Audit Committee Glen C. Mueller, CPA, CIA, CISA, CISM Scripps Health, San Diego, CA VP-Chief Audit & Compliance Executive

HCCA Audit & Compliance Committee Conference February 2008 Internal Audit & the Audit Committee Glen C. Mueller, CPA, CIA, CISA, CISM Scripps Health, San Diego, CA VP-Chief Audit & Compliance Executive

Project Management Professional (PMP) Certification Exam Preparation Program Course Outline with Outcomes

Certification Exam Preparation Program Course Outline with Outcomes") Module i: Overview of the PMP Certification Gain an understanding of the PMP preparation process. 1. The qualifications required for the PMP 2. How to best study for the PMP 3. General truisms of project

Module i: Overview of the PMP Certification Gain an understanding of the PMP preparation process. 1. The qualifications required for the PMP 2. How to best study for the PMP 3. General truisms of project

Implementation Guide 2431

Implementation Guide 2431 Standard 2431 Engagement Disclosure of Nonconformance When nonconformance with the Code of Ethics or the Standards impacts a specific engagement, communication of the results

Implementation Guide 2431 Standard 2431 Engagement Disclosure of Nonconformance When nonconformance with the Code of Ethics or the Standards impacts a specific engagement, communication of the results

Quality Management in the Internal Audit Activity

German Institute of Internal Auditors (DIIR) DIIR Audit Standard No. 3 Quality Management in the Internal Audit Activity Published in August 2002 and amended in September 2015 (Version 1.1), Frankfurt

German Institute of Internal Auditors (DIIR) DIIR Audit Standard No. 3 Quality Management in the Internal Audit Activity Published in August 2002 and amended in September 2015 (Version 1.1), Frankfurt

Mubarak for Accounting, Auditing & Financial Consultancy

Internal Auditing: The Definition of Internal Auditing 3 Add Value 5 Value-Added Internal Audit Survey - Introduction 7 Value-Added Internal Audit Survey - Responses to our questionnaire 8 IAA in SMEs

Internal Auditing: The Definition of Internal Auditing 3 Add Value 5 Value-Added Internal Audit Survey - Introduction 7 Value-Added Internal Audit Survey - Responses to our questionnaire 8 IAA in SMEs

#PurposeServiceImpact IIA Global Chairman s Theme

#PurposeServiceImpact 2017-18 IIA Global Chairman s Theme J. Michael Peppers, CIA, QIAL, CRMA 2017-18 Chairman of The IIA Global Board Chief Audit Executive, University of Texas System @jmpeppers Retweeted

#PurposeServiceImpact 2017-18 IIA Global Chairman s Theme J. Michael Peppers, CIA, QIAL, CRMA 2017-18 Chairman of The IIA Global Board Chief Audit Executive, University of Texas System @jmpeppers Retweeted

Internal Audit Charter

Internal Audit Charter 1. Introduction 1.1 This document sets out the Internal Audit service vision and clarifies the role and responsibilities of the London Borough of Barnet Internal Audit Service and

Internal Audit Charter 1. Introduction 1.1 This document sets out the Internal Audit service vision and clarifies the role and responsibilities of the London Borough of Barnet Internal Audit Service and

Implementation Guides

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Advanced Audit Techniques

Advanced Audit Techniques Who should attend? Senior Auditors Audit Managers and those about to be appointed to that role Auditors that need to audit technical or complex business areas Assurance professionals

Advanced Audit Techniques Who should attend? Senior Auditors Audit Managers and those about to be appointed to that role Auditors that need to audit technical or complex business areas Assurance professionals

Business Administration Certificate Program

Business and Management Business Administration Certificate Program ce.uci.edu/busadmin Improve Your Career Options with a Professional Certificate University of California, Irvine Extension s professional

Business and Management Business Administration Certificate Program ce.uci.edu/busadmin Improve Your Career Options with a Professional Certificate University of California, Irvine Extension s professional

Main purpose of the job:

Post title Salary and grade: FTE Line manager/s: Chief Finance Officer 40,000-45,000 pro rata 0.8 (4 days) Chief Executive Officer Main purpose of the job: The chief financial officer will be directly

Post title Salary and grade: FTE Line manager/s: Chief Finance Officer 40,000-45,000 pro rata 0.8 (4 days) Chief Executive Officer Main purpose of the job: The chief financial officer will be directly

Tactical Implementation of Enterprise Risk Management

Tactical Implementation of Enterprise Risk Management Presented by: Glen Cooper Copyright Tactical Implementation of ERM CONGRATULATIONS YOU HAVE SUCCESSFULLY MADE YOUR BUSINESS CASE AND ACHIEVED MANAGEMENT

Tactical Implementation of Enterprise Risk Management Presented by: Glen Cooper Copyright Tactical Implementation of ERM CONGRATULATIONS YOU HAVE SUCCESSFULLY MADE YOUR BUSINESS CASE AND ACHIEVED MANAGEMENT

TRENDS

TRENDS WWW.THEIIA.ORG/CAE Internal Audit Budget & Staffing Projections Budget Staffing Remain the Same 55% 71% Increase 35% 25% Decrease 8% 3% Unsure 2% 1% Moving Out of the Comfort Zone 58% 52% 71%

TRENDS WWW.THEIIA.ORG/CAE Internal Audit Budget & Staffing Projections Budget Staffing Remain the Same 55% 71% Increase 35% 25% Decrease 8% 3% Unsure 2% 1% Moving Out of the Comfort Zone 58% 52% 71%

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business