Prince William County Public Schools Annual Audit Plan

|

|

|

- Blaise Scott

- 6 years ago

- Views:

Transcription

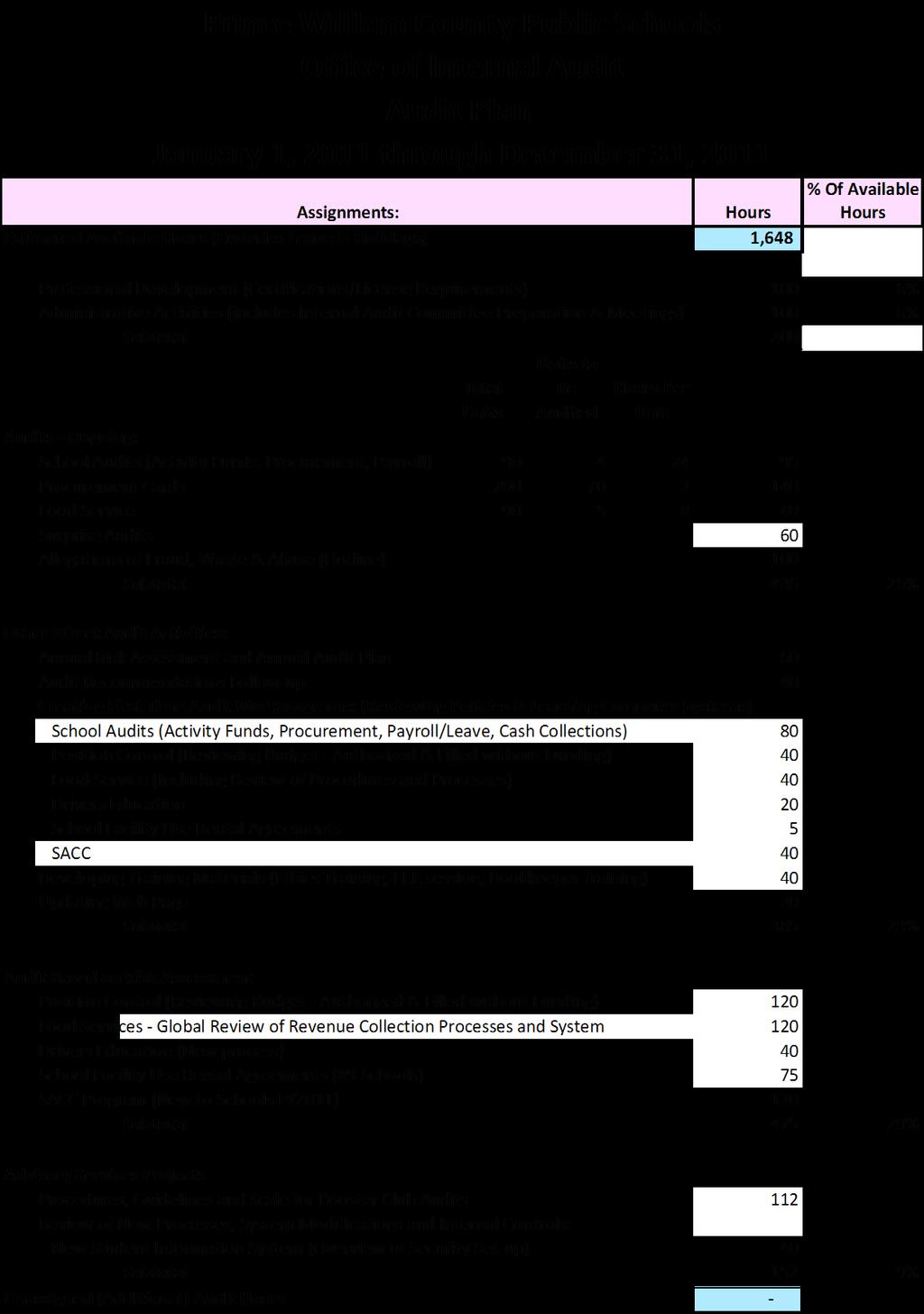

1 Prince William County Public Schools 2011 Annual Audit Plan Office of Internal Audit Vivian Calkins-McGettigan, MBA, CPA, CPFO Chief Internal Auditor

2 Table of Contents Foreword 3 Introduction to the Office of Internal Audit 4 Mission, Vision and Goals 5 Audit Plan (January 1, 2011 December 31, 2011) Annual Audit Projects: On-going Audits: Schools Audits (Four Schools) 7 Procurement Card Audits (70 card holders) 7 Food Service (Five Schools) 8 Surprise Audits (multiple Schools & Offices) 8 Allegations of Fraud, Waste, and Abuse (Hotline) 9 Annual Risk Assessment and Annual Audit Plan 10 Audit Recommendations Follow-up 10 Creating First Time Audit Work Programs for On-Going Audits 11 Developing Training Materials 11 Updating Internal Audit Web Page 12 Audits Based on Risk Assessment: Position Control 12 Food Services Global Review of Revenue Collection Processes 12 and Review of the System Drivers Education 13 School Facility Use Rental Agreements 13 1

3 School Age Child Care (SACC) Program (New) 13 Advisory Services Projects: Procedures, Guidelines, and Scale for Booster Club Audits 14 New Student Information System (Overview of Security Set-up) 14 Risk Assessment Process and Calendar Year 2011 Audit Plan Development 15 2

4 Prince William County Public Schools Office of Internal Audit Calendar Year 2011 Audit Plan FOREWORD The Prince William County Public Schools (PWCS) Office of Internal Audit was established in July 2010 with the hiring of the first Chief Internal Auditor. This report marks the first official Audit Plan for PWCS which is the result of input from numerous management and staff throughout the School Division who have assisted with the identification of the audit risk universe and suggestions for audit work program items based on PWCS unique environment. The Office of Internal Audit herein presents the Calendar Year 2011 Audit Plan for the period of January 1, 2011 through December 31, In accordance with Institute of Internal Auditors Standard 2010 of the International Standards for the Professional Practice of Internal Auditing, the audit plan is a risk-based plan. The audit universe, definitions of risk factors, and risk factor weights were discussed with the School Board, Internal Audit Committee, the Superintendent, and senior management. The scheduled audits address high risk areas, critical issues, and programs that are of interest to the School Board and management. Our audit plan focus corresponds with the School Board and management s objectives and provides assistance in their efforts to provide economical, efficient, and effective programs. The Office of Internal Audit will work cooperatively and in partnership with management to contribute to PWCS mission of providing a World-Class Education to our citizens. In accordance with the Institute of Internal Auditors standards, auditors may participate on committees or task forces in a purely advisory capacity to advise management on issues related to the knowledge and skills of the auditors without impairing their independence. However, auditors should not make management decisions or perform management functions. Auditors can provide routine advice to management to assist in activities such as establishing internal controls or implementing audit recommendations and can answer technical questions and/or provide training. The decision to follow the auditor s advice remains with management. Vivian A. Calkins-McGettigan, MBA, CPA, CPFO Chief Internal Auditor 3

5 Introduction to the Office of Internal Audit Description The Office of Internal Audit provides financial and performance audit services to the School Board and the Superintendent. Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve operations. It provides a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. Objectives and Responsibilities The overall objective of the Office of Internal Audit is to assist all members of the PWCS administration and the School Board in the effective discharge of their responsibilities by providing them with objective analyses, appraisals, recommendations, and pertinent audit comments concerning the following activities: Reviewing and appraising the soundness, adequacy, and application of accounting for financial and other operating controls; Promoting an effective system of internal controls at a reasonable cost; Determining that assets are accounted for and controls are in place to minimize losses; Ascertaining the reliability of financial data; Recommending operating improvements; Determining whether a department or program is achieving its mission, goals, and objectives in an effective manner; Assessing compliance with internal policies and procedures as well as local, state, and federal laws; and Providing sufficient follow-up on audit findings to determine the degree of implementation of audit recommendations. Standards of Practice The Office of Internal Audit follows the Institute of Internal Auditors standards. Reporting Responsibilities The School Board established the Office of Internal Audit, which reports directly to the Internal Audit Committee and through the Internal Audit Committee to the School Board. The Audit Committee consists of three members, including two members of the School Board and the Associate Superintendent for Finance and Support Services. 4

6 Mission, Vision, and Goals Prince William County Public Schools Mission Providing a World-Class Education Vision In Prince William County Public Schools, all students will learn to their fullest potential. The education of each student will be individualized and developmentally appropriate. Student learning will be enhanced by national, global, and multicultural perspectives. Students who graduate from Prince William County Public Schools will possess the basic knowledge and skills that will assure their proficiency in problem solving and the use of technology. Graduates will have a desire to learn and the skills to be life-long learners. They will be responsible citizens. All graduates will be competent to enter the work world and prepared to pursue advanced educational opportunities. Goals Goal 1: All students meet high standards of performance. Goal 2: The teaching, learning, and working environment is caring, safe and healthy, and values human diversity. Goal 3: Family and community engagement create an environment focused on improved student learning and work readiness. Goal 4: Faculty, staff, and leaders are qualified, high performing, diverse, and motivated. Goal 5: The organizational system is aligned, integrated, and equitable. Office of Internal Audit Mission The Office of Internal Audit is committed to assisting the School Board and members of management to effectively discharge their responsibilities while providing a World Class Education. Vision We strive to serve as an independent, objective assurance and consulting activity designed to add value and improve operations of Prince William County Public Schools by providing high quality internal audit services recognized by our customers and our peers for innovation, the integrity of our audit work, and the quality of our reports. The Office of Internal Audit strives to assist Prince William County Public Schools in accomplishing its objectives by bringing a systematic, disciplined approach to evaluating the effectiveness of risk management, control, and governance processes. We are committed to promoting teamwork in a diverse workforce. Goals Goal 1: Develop and implement an audit plan based on annual risk assessment. Goal 2: Ensure that PWCS programs, schools, and departments comply with applicable policies, regulations, and laws. Goal 3: Improve understanding of internal audit functions and services. Maintain a dynamic, team oriented environment which encourages personal and professional growth and challenges and rewards our employees for excelling and reaching their full potential. Goal 4: Encourage self-reviews of systems and procedures. Goal 5: Investigate observed, alleged, or suspected wrongdoing to prevent and detect fraud, waste, and abuse in PWCS schools and activities. 5

7 6

8 School Audits (Four Schools) Staff Hours: 96 These audits will be conducted at a sample of schools and offices. Because the individual schools School Activity Funds are audited by external auditors, the focus of the internal audits will be on overall financial controls and expenditures funded by general fund revenues. This review will provide an overall evaluation of the controls over the business processes performed at the school and office locations. Due to the unique PWCS site-based management approach, each audit work program will be modified based on observations and inquiries of school staff and the unique processes and forms related to the individual schools. These processes will include, but will not be limited to: Activity Funds; Procurement including procurement card activities; Payroll (contracts, supplements, etc); Time and Attendance; Travel and Employee Reimbursement; Cash Collections Process; and Overall Financial Controls Procurement Card Audits (70 card holders) Staff Hours: 140 These audits will be conducted for a sample of card holders and will concentrate on the adequacy of the controls over access, handling, and safekeeping of cards; maintenance of appropriate documentation, approval, oversight, and reconciliation; and compliance with PWCS policies and regulations. 7

9 Associated risks may include: Improper or abusive purchases; Inaccurate or incomplete records; Inadequate monitoring and reconciliation; and Purchase of services or items not received by the County Food Service (Five Schools) Staff Hours: 40 Examination of compliance with operations manual issued by the Office of School Food and Nutrition Services at individual schools selected for audit. Individual audits may include the following: Observe food service employees for compliance with procedures; Observe cash collections, reporting, and reconciliation process; Review management reporting; Review procurement and inventory controls; and Observe and evaluate physical security over cash and deposits Surprise Audits (multiple Schools and Offices) Staff Hours: 60 One element of an effective anti-fraud program aimed at deterring fraud is the potential for surprise audits. This audit will involve dropping in unannounced at individual schools selected based on the Chief Internal Auditor s judgment to observe processes, interview bookkeepers, and review documents. Bookkeepers have been informed of the surprise audits and the possible items to be observed or reviewed so that they can be perpetually prepared with appropriate documentation. The individual audits will vary from audit to audit. A sample of the items audited may include observing: Security of cash; Timeliness of deposits; Collections of cash from teachers and sponsors throughout the day; 8

10 Security of passwords; and Security over check stock The audits may include formal reviewing and testing of: Sponsor forms and reports; Cooperative activities forms and reports; Payroll and leave records; Procurement cards and credit card files; Petty cash and change funds; Check registers and bank reconciliations; and Non-expendable property inventory forms The unexpected nature of the surprise audits and communication of results of the audits have historically been an incentive for those contemplating fraud to reconsider their actions due to the increased risk of detection. Staff Hours: Allegations of Fraud, Waste, and Abuse (Hotline) 100 (Subject to change based on activities) Upon notification or discovery of suspected fraud, the Office of Internal Audit will oversee and coordinate actions taken in following up on the suspected fraud. PWCS has a team approach to responding to suspected fraud with members from Internal Audit, Risk Management, and Financial Services. The Office of Internal Audit s primary role is to be aware of all fraud related allegations and to provide assurance to the Internal Audit Committee that management has addressed the fraud incident and made corrections associated with the knowledge gained from the incidents. Fraud related cases may be the result of calls to the hotline, employee and management reports of suspicious activities, and fraud identified during audits. Incidents reported directly to the Office of Internal Audit through the hotline or employee calls are initially reviewed by the Office of Internal Audit to determine validity. Many reports are routine issues which will be referred to the department responsible for compliance of the policy allegedly violated. Internal Audit will follow-up on the actions taken by the department. If an allegation requires investigation, the Office of Internal Audit will request an investigation from the Office of Risk Management and Security Services through the Associate Superintendent for Finance and Support Services. Investigations consist of performing 9

11 extensive procedures necessary to determine whether fraud, as suspected, has occurred. It includes gathering sufficient evidence about the specific details of a discovered fraud. These investigations are a team effort with Risk Management, Internal Audit, Financial Services, legal counsel and police officers. Financial Services will review the results of the alleged fraud incidents and modify internal control processes to reduce the risk of future incidents as appropriate. Internal Audit will review the investigation files and meet with management as appropriate to provide assurance of management s responses to alleged fraud, waste, and abuse. Internal Audit will follow-up with employees providing tips to ensure that retaliation has not occurred. Annual Risk Assessment and Annual Audit Plan Staff Hours: 60 This report is the result of a comprehensive risk assessment process reflecting the contributions of numerous management, principals, directors, bookkeepers, and staff to identify and prioritize the audit universe. The result of the risk assessment process is the annual audit plan. The audit universe is a dynamic continuously changing environment which requires constant updates. Each year, at a point in time, the audit universe will be updated and the subsequent year s Audit Plan will be developed for the Internal Audit Committee s and School Board s approvals. The process for update may include focus group meetings, contributions from individual department s staff meetings, review of new programs, and significant changes to existing programs. Audit Recommendations Follow-up Staff Hours: 40 The purpose of performing follow-up on audit recommendations is to determine that corrective actions have been put into place to address audit observations. The Office of Internal Audit will perform steps necessary to determine that agreed upon actions have been implemented in a timely manner and whether operations continue to have an adequate control structure in place. These follow-up efforts, as required by Institute of Internal Auditors standards, will assist in ensuring that efficiencies and controls are achieved. When preparing a response to an audit, management indicates what actions they plan to take to address audit observations and the anticipated date of completion. While it is management s responsibility to implement agreed upon actions, Internal Audit will institute a procedure for contacting management to obtain 10

12 feedback regarding progress made and to obtain justification for actions that are not taken within the agreed upon timeframe. Creating First Time Audit Work Programs for On-going Audits Staff Hours: 225 With the Office of Internal Audit having been recently established, no audit work programs currently exist. Over the next few years first time audit work programs will be developed which in subsequent years will require less time for work program modifications. The development of the work programs will require review of relevant policies and regulations, current processes, forms, regulations and systems, as well as development of background and history documents and interviews with staff. This review will provide an overall evaluation of the controls over the business processes performed at schools and office locations related to the specific program. Due to PWCS site-based management approach, standardization of the audit work programs are limited. During 2011 the following work programs will be developed: School Audits Position Control Food Service Drivers Education School Facility Use Rental Agreements School Age Child Care (SACC) Developing Training Materials Staff Hours: 40 One of the components of a strong anti-fraud program is the on-going communication, education, and training processes. At PWCS the primary avenue for communication of financial processes is through the quarterly Bookkeeper Inservice meetings offered by the Office of Financial Services. The general plan is for Internal Audit to present brief segments at each quarterly meeting which will include updates on lessons learned from fraud incidents, which in most cases will be incidents outside of PWCS; information on upcoming audits; and tips to prepare for audits. Regular presentations at these meetings will enhance the familiarity with the 11

13 Internal Audit function, improving communication processes and emphasizing deterrence of fraud from increased possibility for detection. Specific training topics for development in 2011 are an ethics training course and a session at the EEE Conference in the summer. Updating Internal Audit Web Page Staff Hours: 20 To provide transparency to the internal audit activities, a web site will be developed which will provide public access to Internal Audit Committee agendas; minutes to Internal Audit Committee meetings, Annual Audit Plans, Annual Reports, and Fraud, Waste and Abuse Hotline instructions. Position Control Staff Hours: 120 Review the internal controls processes for creation of new positions. Currently, position information is entered into multiple systems which are reconciled manually. This project will consist of: Review of the processes to create new positions in the multiple systems; Review of the reconciliation processes for the multiple systems; Review of the current system reports; and Review segregation of duties controls and the override processes Food Services Global Review of Revenue Collection Processes and Review of the System Staff Hours:

14 Review and provide assessment of Divisionwide revenue collections processes including review of the food services system. Project will include: Review of the Office of School Food and Nutrition Services Operations Manual specifically focused on revenue collections and reconciliation; Meet with Food Services staff to understand their processes; Form focus group to obtain their input on primary risks in Food Service collection area; Observe processes; Review reporting and reconciliation processes focused on cash controls; and Observe and evaluate physical security over cash Drivers Education (New Process) Staff Hours: 40 Review and test the Drivers Education revenue collection process at the high schools. Schools Facility Use Rental Agreements (89 Schools) Staff Hours: 75 Review and test the facility use rental revenue collection processes at the schools and the reconciliation of revenues to be submitted to the Central Office. School Age Child Care (SACC) Program (New) Staff Hours: 120 The SACC program moved from the County to PWCS effective September 1, A PWCS transition team was created to develop procedures which include the implementation of an online registration process. The revenues are collected by a third party administrator, Minnieland Private Day School, Inc., which is subject to external audit. 13

15 The project will include: Review and test the new internal processes; and Review the third party administrator s collection and reporting process including the external audit report addressing the internal control environment Assisting management with the establishment of the SACC program allows internal audit to take a proactive approach to controls. For example, by performing a review of draft procedures and policy guidance, internal audit will make suggestions regarding controls that management may want to put in place. It is more efficient and economical to design a sound control environment from the beginning rather than to try to fit controls in after a function or process has been in place for a length of time. Procedures, Guidelines, and Scale for Booster Club Audits Staff Hours: 112 Participate on an advisory services team with Financial Services and the school attorney to develop procedures and guidelines to enhance accountability of funds collected and disbursed for booster clubs. The project will include developing a scale which will range from dual signatures on annual reports to formal audits based on the magnitude of revenues collected by the booster clubs. The review will include accumulating information on cooperative fund raising activity agreements and annual income statements. Review of New Processes, Systems Modifications, and Internal Controls New Student Information System (Overview of Security Set-up) Staff Hours: 40 Review processes and interview staff to understand the controls developed for the new student information system and specifically review the control environment for the security set-up of the system. Assisting management with the establishment of the new system allows Internal Audit to take a proactive approach to controls. For example, by performing a review of draft procedures and policy guidance Internal Audit will make suggestions regarding controls that management may want to put in place. It is more efficient and economical to design a sound control environment from the beginning rather than to try to fit controls in after a function or process has been in place for a length of time. 14

16 Risk Assessment Process and Calendar Year 2011 Audit Plan Development The Calendar Year 2011 Audit Plan was developed using the following methodology: Purpose of Risk Assessment The level of risk associated with Prince William County Public Schools varies from department to department, program to program, and school to school. Risk assessment is a three-step process including: Risk Identification Risk Measurement Risk Prioritization Determination of the risks Determination of the size of the risks Determination of which risks are the most important In order for the Office of Internal Audit to effectively create its Audit Plan, a structured risk assessment methodology was created that allows Internal Audit to examine the level of risk of each auditable unit. Risk Identification and Risk Management The first step of developing a risk assessment methodology is to determine key risks. Because the Office of Internal Audit was established during the current year, one of the primary focuses has been to identify the global Prince William County Public Schools Audit Universe. This process consisted of reviewing financial documents; and meetings with senior management, principals, directors and bookkeepers to identify division-wide and unique risks. Focus groups were also formed to concentrate on specific high risk areas such as school principals and bookkeeper teams to identify high risk areas at the school level. The second step of developing a risk assessment methodology is to determine the weight factors. Weight factors were chosen based on importance of the risk factors to the determination of the audit selection. Risk Prioritization The third step of developing a risk assessment methodology is to rank the audit universe. Each area is then separately evaluated and assigned a point value. In our first year of developing the audit universe we used a basic model rating the programs using (High, Medium, and Low) which essentially translates to a one-three scale with one representing the lowest level of risk and three the highest. In the future, the Office of Internal Audit will be expanding the model to include multiple weighted factors. The weighted factors will be added together to obtain the representative total impact and probability score for each auditable unit. Once the total scores 15

17 have been calculated the list of auditable units can be sorted from highest to lowest by their respective total risk. Resource Model Due to its size, the Office of Internal Audit first rates all audits from highest to lowest risk then selects those that can be completed by available staff during the calendar year. This approach is the Resource Model of risk assessment based on available resources of the audit function. The auditable unit with the highest risk assessment will be selected for audit on a more frequent basis while the auditable units with the lowest risk assessment will be audited less frequently. 16

Collaboration with Internal Audit

Collaboration with Internal Audit Bookkeepers Meeting February 2013 John Wallingford Director of Finance Vivian McGettigan Chief Internal Auditor Common Misunderstandings and Common Audit Findings What

Collaboration with Internal Audit Bookkeepers Meeting February 2013 John Wallingford Director of Finance Vivian McGettigan Chief Internal Auditor Common Misunderstandings and Common Audit Findings What

Corporate Governance. Information Request List Family- or Founder-Owned Unlisted Companies. Commitment to Corporate Governance

Commitment to Corporate Governance 1. Policies relating to corporate governance. What written policies, codes or manuals have been elaborated that set out the company s approach to governance, the respective

Commitment to Corporate Governance 1. Policies relating to corporate governance. What written policies, codes or manuals have been elaborated that set out the company s approach to governance, the respective

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Guide to Internal Controls

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

FUNCTION: To Protect and Enhance the Nonprofit Organization s Capacity to Serve the Community.

JOB TITLE: BOARD OF DIRECTORS FUNCTION: To Protect and Enhance the Nonprofit Organization s Capacity to Serve the Community. : Assist staff in identifying the organization s mission, developing a strategic

JOB TITLE: BOARD OF DIRECTORS FUNCTION: To Protect and Enhance the Nonprofit Organization s Capacity to Serve the Community. : Assist staff in identifying the organization s mission, developing a strategic

CHAPTER 6 GOVERNMENT ACCOUNTABILITY

Kern County Administrative Policy and Procedures Manual CHAPTER 6 GOVERNMENT ACCOUNTABILITY Section Page 601. General Statement... 1 602. Definitions... 1 603. Fraud, Waste, and Abuse... 1 604. Fraud Protocol...

Kern County Administrative Policy and Procedures Manual CHAPTER 6 GOVERNMENT ACCOUNTABILITY Section Page 601. General Statement... 1 602. Definitions... 1 603. Fraud, Waste, and Abuse... 1 604. Fraud Protocol...

This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department.

Corporate Audit Department.") CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

CORPORATE AUDIT DEPARTMENT CHARTER PURPOSE This charter defines the purpose, authority and responsibility of News Corporation s (the Company ) Corporate Audit Department. The Institute of Internal Auditors

FRIENDSHIP HOUSE JOB DESCRIPTION. Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

COLLEGE OF PHYSICIANS AND SURGEONS OF ONTARIO GOVERNANCE PROCESS MANUAL

COLLEGE OF PHYSICIANS AND SURGEONS OF ONTARIO GOVERNANCE PROCESS MANUAL December 2016 Table of Contents Governance Roles and Responsibilities Table of Contents OVERVIEW OF GOVERNANCE... 3 GOVERNANCE ROLES

COLLEGE OF PHYSICIANS AND SURGEONS OF ONTARIO GOVERNANCE PROCESS MANUAL December 2016 Table of Contents Governance Roles and Responsibilities Table of Contents OVERVIEW OF GOVERNANCE... 3 GOVERNANCE ROLES

IIA ACFE Conference April 17, 2015

IIA ACFE Conference April 17, 2015 Summary of Presentation Forensic Audit / Internal Audit Forensic Audit Role Forensic Audit Methodology Pragmatic examples of how forensic audit can benefit the risk assessment

IIA ACFE Conference April 17, 2015 Summary of Presentation Forensic Audit / Internal Audit Forensic Audit Role Forensic Audit Methodology Pragmatic examples of how forensic audit can benefit the risk assessment

Internal Audit Work Plan

Internal Audit Work Plan Fiscal Year 2018 Department of Management and Finance 1 Internal Audit Services Arlington County s Internal Audit Division is organizationally located in the Department of Management

Internal Audit Work Plan Fiscal Year 2018 Department of Management and Finance 1 Internal Audit Services Arlington County s Internal Audit Division is organizationally located in the Department of Management

4. Organic documents. Please provide an English translation of the company s charter, by-laws and other organic documents.

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

GOVERNANCE GUIDELINES OF THE NATIONAL ASSOCIATION OF CORPORATE DIRECTORS

GOVERNANCE GUIDELINES OF THE NATIONAL ASSOCIATION OF CORPORATE DIRECTORS TABLE OF CONTENTS Title Page 1. History 3 2. Foreword 4 3. Mission and Vision Statement 5 4. Board Membership 5 Size of Board Mix

GOVERNANCE GUIDELINES OF THE NATIONAL ASSOCIATION OF CORPORATE DIRECTORS TABLE OF CONTENTS Title Page 1. History 3 2. Foreword 4 3. Mission and Vision Statement 5 4. Board Membership 5 Size of Board Mix

1. Definition & Mission

1. Definition & Mission 1.1 Internal Auditing is an independent, objective assurance and consulting activity that is guided by a philosophy of adding value to improve the operations of. 1.2 Group Internal

1. Definition & Mission 1.1 Internal Auditing is an independent, objective assurance and consulting activity that is guided by a philosophy of adding value to improve the operations of. 1.2 Group Internal

CSL BEHRING COMPLIANCE PLAN

CSL BEHRING COMPLIANCE PLAN I. POLICY AND PURPOSE Statement of Values CSL Behring adheres to a policy of strict compliance with the laws and regulations governing its business, not only as a legal obligation,

CSL BEHRING COMPLIANCE PLAN I. POLICY AND PURPOSE Statement of Values CSL Behring adheres to a policy of strict compliance with the laws and regulations governing its business, not only as a legal obligation,

What Happens When Internal Controls Fail

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

Chapter 6 Field Work Standards for Performance Audits

Chapter 6 Field Work Standards for Performance Audits Introduction 6.01 This chapter contains field work requirements and guidance for performance audits conducted in accordance with generally accepted

Chapter 6 Field Work Standards for Performance Audits Introduction 6.01 This chapter contains field work requirements and guidance for performance audits conducted in accordance with generally accepted

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

Financial Services Job Summaries

Job Summaries Job 18713 18712 18711 18613 18612 18611 18516 18515 18514 18513 18512 18511 Vice President Finance Senior Associate Vice President Associate Vice President Assistant Vice President Vice Presidents

Job Summaries Job 18713 18712 18711 18613 18612 18611 18516 18515 18514 18513 18512 18511 Vice President Finance Senior Associate Vice President Associate Vice President Assistant Vice President Vice Presidents

SAMPLE BOARD PERFORMANCE EVALUATION: Prepared by DELOITTE & TOUCHE, 2013

SAMPLE BOARD PERFORMANCE EVALUATION: Prepared by DELOITTE & TOUCHE, 2013 The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an individual director

SAMPLE BOARD PERFORMANCE EVALUATION: Prepared by DELOITTE & TOUCHE, 2013 The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an individual director

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

MISSISSIPPI STATE UNIVERSITY INTERNAL AUDIT CHARTER I. The Charter The Office of Internal Audit was established by the President of Mississippi State University to assist the University in meeting its

Delta Dental of Michigan, Ohio, and Indiana. Compliance Plan

Delta Dental of Michigan, Ohio, and Indiana Compliance Plan Procedure #: 420-29 Issue Date: 5/15/2013 Last Revised Date: 5/23/2016 Last Review Date: 5/23/2016 Next Review Date: 5/23/2017 Title: Compliance

Delta Dental of Michigan, Ohio, and Indiana Compliance Plan Procedure #: 420-29 Issue Date: 5/15/2013 Last Revised Date: 5/23/2016 Last Review Date: 5/23/2016 Next Review Date: 5/23/2017 Title: Compliance

AUDITING. Auditing PAGE 1

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

Internal Control in Higher Education

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

BOARD INTERNAL ORGANIZATION. Audit Committee

Audit Committee Board adoption: The Board amended, which serves as the District s Audit Committee charter. Purpose: The purpose of the Audit Committee is to provide structured, systematic oversight of

Audit Committee Board adoption: The Board amended, which serves as the District s Audit Committee charter. Purpose: The purpose of the Audit Committee is to provide structured, systematic oversight of

Metropolitan St. Louis Sewer District. Strategic Business and Operating Plan Fiscal Years

Metropolitan St. Louis Sewer District Strategic Business and Operating Plan Fiscal Years 2013 2017 VISION STATEMENT Quality Service Always MISSION STATEMENT To protect the public s health, safety, and

Metropolitan St. Louis Sewer District Strategic Business and Operating Plan Fiscal Years 2013 2017 VISION STATEMENT Quality Service Always MISSION STATEMENT To protect the public s health, safety, and

INTERNAL AUDIT PLAN AND CHARTER 2018/19

INTERNAL AUDIT PLAN AND CHARTER 208/9 PURPOSE OF REPORT. To present the proposed 208/9 audit plan and charter to the Audit Committee for consideration and approval..2 The Internal Audit Plan for 208/9

INTERNAL AUDIT PLAN AND CHARTER 208/9 PURPOSE OF REPORT. To present the proposed 208/9 audit plan and charter to the Audit Committee for consideration and approval..2 The Internal Audit Plan for 208/9

Innovation and Internal Controls

Innovation and Internal Controls AGA Dallas Chapter January 25, 2018 Renee L. Hayden, CPA, CFE Interim Managing Director Center for Performance Excellence City of Dallas Training Objective: Learn About

Innovation and Internal Controls AGA Dallas Chapter January 25, 2018 Renee L. Hayden, CPA, CFE Interim Managing Director Center for Performance Excellence City of Dallas Training Objective: Learn About

INTERNAL AUDIT OFFICE (IAO) FISCAL YEAR 2019 RISK-BASED AUDIT PLAN

FISCAL YEAR 2019 RISK-BASED AUDIT PLAN") INTERNAL AUDIT OFFICE (IAO) FISCAL YEAR 2019 RISK-BASED AUDIT PLAN Activity Performance Audits, Assurance Services, and Special Requests: Budgeted Hours DC Water Blue Plains WWTP O&M and Capital Indirect

INTERNAL AUDIT OFFICE (IAO) FISCAL YEAR 2019 RISK-BASED AUDIT PLAN Activity Performance Audits, Assurance Services, and Special Requests: Budgeted Hours DC Water Blue Plains WWTP O&M and Capital Indirect

Global Alliance for Improved Nutrition

Job Title: Finance and Administration Manager, Nigeria Classification: Senior Manager, R5 Direct Reports: 1-5 Work Location Nigeria Office Travel Required: Limited GAIN s purpose is to advance nutrition

Job Title: Finance and Administration Manager, Nigeria Classification: Senior Manager, R5 Direct Reports: 1-5 Work Location Nigeria Office Travel Required: Limited GAIN s purpose is to advance nutrition

Maryland School for the Deaf

Audit Report Maryland School for the Deaf December 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Audit Report Maryland School for the Deaf December 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

POSITION DESCRIPTION

POSITION DESCRIPTION Position Title CHIEF FINANCIAL OFFICER Date: April 2016 Group: WA Local Government Superannuation Plan Reports to: Chief Executive Officer Employment Status: Permanent SECTION 1 CORPORATE

POSITION DESCRIPTION Position Title CHIEF FINANCIAL OFFICER Date: April 2016 Group: WA Local Government Superannuation Plan Reports to: Chief Executive Officer Employment Status: Permanent SECTION 1 CORPORATE

2. Agenda and minutes. Is an agenda prepared and distributed in advance of board meetings? Are minutes prepared and approved after board meetings?

Commitment to Good Corporate Governance 1. Ownership and governance structure: Is the everyday, practical governance of the firm and the exercise of ownership rights consistent with the formal documentation

Commitment to Good Corporate Governance 1. Ownership and governance structure: Is the everyday, practical governance of the firm and the exercise of ownership rights consistent with the formal documentation

BRIGHT HORIZONS FAMILY SOLUTIONS, INC. CORPORATE GOVERNANCE GUIDELINES

BRIGHT HORIZONS FAMILY SOLUTIONS, INC. CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Bright Horizons Family Solutions, Inc. (the Company ) has developed the following corporate

BRIGHT HORIZONS FAMILY SOLUTIONS, INC. CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Bright Horizons Family Solutions, Inc. (the Company ) has developed the following corporate

Committee for Senior Business Administrators. Segregation of Duties

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

International Standards for the Professional Practice of Internal Auditing (Standards)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

EY Center for Board Matters. Leading practices for audit committees

EY Center for Board Matters for audit committees As an audit committee member, your role is increasingly complex and demanding. Regulators, standard-setters and investors are pressing for more transparency

EY Center for Board Matters for audit committees As an audit committee member, your role is increasingly complex and demanding. Regulators, standard-setters and investors are pressing for more transparency

Internal Communications: MMU Board of Commissioners, General Manager, department managers, department supervisors, utility staff

Position Title: Finance Manager Department: Finance Immediate Managers Title: General Manager Immediate Supervisor s Title: NA FLSA Status: Exempt Pay Grade: 10 PURPOSE The Finance Manager serves as a

Position Title: Finance Manager Department: Finance Immediate Managers Title: General Manager Immediate Supervisor s Title: NA FLSA Status: Exempt Pay Grade: 10 PURPOSE The Finance Manager serves as a

Audit Committee Member Roles and Responsibilities

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

THE ARCG CHARTER. Issued in March 2008

THE ARCG CHARTER Issued in March 2008 Index Part A Internal Audit Purpose Charter Mission Independence Scope & Responsibilities Authority Accountability Standards Part B Compliance Introduction Guiding

THE ARCG CHARTER Issued in March 2008 Index Part A Internal Audit Purpose Charter Mission Independence Scope & Responsibilities Authority Accountability Standards Part B Compliance Introduction Guiding

ROLES& RESPONSIBILITIES. School Boards & Superintendents

School Boards & Superintendents ROLES& RESPONSIBILITIES A joint publication of Alabama Association of School Boards and School Superintendents of Alabama School Boards & Superintendents ROLES& RESPONSIBILITIES

School Boards & Superintendents ROLES& RESPONSIBILITIES A joint publication of Alabama Association of School Boards and School Superintendents of Alabama School Boards & Superintendents ROLES& RESPONSIBILITIES

Internal Controls: Providing an Effective Control Environment. Why This Session Is Needed. Lesson Overview & Module Objectives

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

KING III COMPLIANCE ANALYSIS

Principle element No Application method or explanation This document has been prepared in terms of the JSE Listings Requirements and sets out the application of the 75 Principles of the King III Report

Principle element No Application method or explanation This document has been prepared in terms of the JSE Listings Requirements and sets out the application of the 75 Principles of the King III Report

Audit-Risk Committee. Board Approval: August 2018

Charter: Audit-Risk Committee Board Approval: August 2018 Authority: 12 CFR 620.30, 621.30 621.32, 620.5(i)(2), & 612.2260; FCA WP 31.3-1 (Audit Committee)(02/16/16); FCA EM-31.3 (Audit & Review Programs)(04/20/16);

Charter: Audit-Risk Committee Board Approval: August 2018 Authority: 12 CFR 620.30, 621.30 621.32, 620.5(i)(2), & 612.2260; FCA WP 31.3-1 (Audit Committee)(02/16/16); FCA EM-31.3 (Audit & Review Programs)(04/20/16);

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

Internal Controls Overview

UMBC Management Advisory Services Internal Controls Overview /mas What Is Internal Control? A process designed to provide reasonable assurance regarding the achievement of the following objectives: Effectiveness

UMBC Management Advisory Services Internal Controls Overview /mas What Is Internal Control? A process designed to provide reasonable assurance regarding the achievement of the following objectives: Effectiveness

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Maryland Department of Health Office of the Chief Medical Examiner

Audit Report Maryland Department of Health Office of the Chief Medical Examiner April 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Audit Report Maryland Department of Health Office of the Chief Medical Examiner April 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Office of Inspector General. Annual Report for Fiscal Year

Annual Report for Fiscal Year 2017-2018 Report Number: S-1819-13 September 28, 2018 Eric M. Larson State CIO/Executive Director Tabitha A. McNulty Inspector General Rick Scott Governor State of Florida

Annual Report for Fiscal Year 2017-2018 Report Number: S-1819-13 September 28, 2018 Eric M. Larson State CIO/Executive Director Tabitha A. McNulty Inspector General Rick Scott Governor State of Florida

Audit and Risk Committee Charter

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

MSD Internal Control Policy 01/16/08. Metropolitan Sewerage District of Buncombe County Internal Control Policy

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Diving into the 2013 COSO Framework. Presented by: Ronald A. Conrad

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

The Red (Book) Rocks The Latest and Greatest Audit Standards

Rocks The Latest and Greatest Audit Standards") The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

The Red (Book) Rocks The Latest and Greatest Audit Standards Presenter Toni Stephens Chief Audit Executive The University of Texas at Dallas Insert Logo Here Course Objectives Explain the development of

OFFICE OF INTERNAL AUDIT AUDIT MANUAL

OFFICE OF INTERNAL AUDIT AUDIT MANUAL Effective Date: October 31, 2006 Revised Date: October 27, 2016 Introduction The purpose of this manual is to outline the authority and scope of the internal audit

OFFICE OF INTERNAL AUDIT AUDIT MANUAL Effective Date: October 31, 2006 Revised Date: October 27, 2016 Introduction The purpose of this manual is to outline the authority and scope of the internal audit

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL June, 2018 AUDIT MANUAL TABLE OF CONTENTS SECTION 100 THE INTERNAL AUDIT ACTIVITY 100.1: Audit Activity Charter 100.2: State Agency General

OFFICE OF INTERNAL AUDITS APPALACHIAN STATE UNIVERSITY AUDIT MANUAL June, 2018 AUDIT MANUAL TABLE OF CONTENTS SECTION 100 THE INTERNAL AUDIT ACTIVITY 100.1: Audit Activity Charter 100.2: State Agency General

INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING

OFFICE OF THE COMMISSIONNER OF LOBBYING OF CANADA INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING AUDIT REPORT Presented by: Samson & Associates February 20, 2015 TABLE OF CONTENT EXECUTIVE SUMMARY... I

OFFICE OF THE COMMISSIONNER OF LOBBYING OF CANADA INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING AUDIT REPORT Presented by: Samson & Associates February 20, 2015 TABLE OF CONTENT EXECUTIVE SUMMARY... I

POSITION PROFILE FOR THE CHIEF OF THE WINNIPEG POLICE SERVICE. Last updated October, 2015

POSITION PROFILE FOR THE CHIEF OF THE WINNIPEG POLICE SERVICE Last updated October, 2015 1 PREFACE The Winnipeg Police Board is required by Section 21 of Manitoba s Police Services Act to appoint a person

POSITION PROFILE FOR THE CHIEF OF THE WINNIPEG POLICE SERVICE Last updated October, 2015 1 PREFACE The Winnipeg Police Board is required by Section 21 of Manitoba s Police Services Act to appoint a person

University System of Maryland University of Maryland, College Park

Audit Report University System of Maryland University of Maryland, College Park May 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Audit Report University System of Maryland University of Maryland, College Park May 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

TERMS OF REFERENCE OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

TERMS OF REFERENCE OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS 1. Purpose An Audit Committee (hereinafter called the Committee ) of the Board of Directors (hereinafter called the Board ) of the Business

TERMS OF REFERENCE OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS 1. Purpose An Audit Committee (hereinafter called the Committee ) of the Board of Directors (hereinafter called the Board ) of the Business

OFFICE OF THE CITY AUDITOR CITY OF GAINESVILLE, FLORIDA

OFFICE OF THE CITY AUDITOR CITY OF GAINESVILLE, FLORIDA POLICIES AND PROCEDURES MANUAL For Audits Initiated After December 15, 2011 Foreword The purpose of this manual is to establish internal policies

OFFICE OF THE CITY AUDITOR CITY OF GAINESVILLE, FLORIDA POLICIES AND PROCEDURES MANUAL For Audits Initiated After December 15, 2011 Foreword The purpose of this manual is to establish internal policies

Session 7: Corporate Governance

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Company LOGO C B T. An Educational Computer Based Training Program

C B T An Educational Computer Based Training Program The University of Texas at Dallas Compliance Training Effectively Controlling Risks Company Effectively Controlling Risks What is the purpose of this

C B T An Educational Computer Based Training Program The University of Texas at Dallas Compliance Training Effectively Controlling Risks Company Effectively Controlling Risks What is the purpose of this

THE SCHOOL BOARD OF BROWARD COUNTY, FLORIDA JOB DESCRIPTION

THE SCHOOL BOARD OF BROWARD COUNTY, FLORIDA JOB DESCRIPTION SBBC: B-002 POSITION TITLE: CONTRACT YEAR: School Principal Twelve Months PAY GRADE: School-based Administrators Salary Schedule Category C,

THE SCHOOL BOARD OF BROWARD COUNTY, FLORIDA JOB DESCRIPTION SBBC: B-002 POSITION TITLE: CONTRACT YEAR: School Principal Twelve Months PAY GRADE: School-based Administrators Salary Schedule Category C,

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Internal Audit Charter

Internal Audit Charter 1. Introduction 1.1 This document sets out the Internal Audit service vision and clarifies the role and responsibilities of the London Borough of Barnet Internal Audit Service and

Internal Audit Charter 1. Introduction 1.1 This document sets out the Internal Audit service vision and clarifies the role and responsibilities of the London Borough of Barnet Internal Audit Service and

Guidelines of Corporate Governance

Guidelines of Corporate Governance December 2017 The Board of Directors (the Board ) of Radian Group Inc. ( Radian or the Company ) has established guidelines for corporate governance based on an assessment

Guidelines of Corporate Governance December 2017 The Board of Directors (the Board ) of Radian Group Inc. ( Radian or the Company ) has established guidelines for corporate governance based on an assessment

Fiscal Oversight Fundamentals

Fiscal Oversight Fundamentals Module 1: School District Finances: Roles and Responsibilities 2012 New York State School Boards Association, Latham NY The Five-Point Plan 1. Requires training for school

Fiscal Oversight Fundamentals Module 1: School District Finances: Roles and Responsibilities 2012 New York State School Boards Association, Latham NY The Five-Point Plan 1. Requires training for school

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016 This table is a useful reference to each of the King III principles and how, in broad terms, they have been applied by the Group. KING III ETHICAL

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016 This table is a useful reference to each of the King III principles and how, in broad terms, they have been applied by the Group. KING III ETHICAL

LI & FUNG LIMITED ANNUAL REPORT 2016

52 Our approach to risk management We maintain a sound and effective system of risk management and internal controls to support us in achieving high standards of corporate governance. Our approach to risk

52 Our approach to risk management We maintain a sound and effective system of risk management and internal controls to support us in achieving high standards of corporate governance. Our approach to risk

Developmental Delay Rehabilitation Services Inc.

Developmental Delay Rehabilitation Services Inc. Corporate Compliance Plan Terence Blackwell, CEO Nathan Cohen, CCC/SLP, President Corporate Compliance Officer Table of Contents Section Name I. Corporate

Developmental Delay Rehabilitation Services Inc. Corporate Compliance Plan Terence Blackwell, CEO Nathan Cohen, CCC/SLP, President Corporate Compliance Officer Table of Contents Section Name I. Corporate

ISM COMMUNICATIONS CORPORATION AUDIT COMMITTEE CHARTER

ISM COMMUNICATIONS CORPORATION AUDIT COMMITTEE CHARTER In accordance with the By-Laws and Revised Manual on Corporate Governance of ISM Communications Corporation (the Company ) dated February 18, 2011

ISM COMMUNICATIONS CORPORATION AUDIT COMMITTEE CHARTER In accordance with the By-Laws and Revised Manual on Corporate Governance of ISM Communications Corporation (the Company ) dated February 18, 2011

ACADEMIC DEPARTMENT FISCAL REVIEW

CSU The California State University Office of Audit and Advisory Services ACADEMIC DEPARTMENT FISCAL REVIEW California State University, Dominguez Hills College of Health, Human Services, and Nursing Audit

CSU The California State University Office of Audit and Advisory Services ACADEMIC DEPARTMENT FISCAL REVIEW California State University, Dominguez Hills College of Health, Human Services, and Nursing Audit

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

ANNUAL STUDENT ACTIVITY WORKSHOP FY JULY 28, 2017

ANNUAL STUDENT ACTIVITY WORKSHOP FY 2017-2018 JULY 28, 2017 STUDENT ACTIVITY WORKSHOP FY 2017-2018 WELCOME & INTRODUCTION Sherri Mathews-Hazel, CPA Chief Financial Officer FINANCIAL SERVICES STUDENT ACTIVITY

ANNUAL STUDENT ACTIVITY WORKSHOP FY 2017-2018 JULY 28, 2017 STUDENT ACTIVITY WORKSHOP FY 2017-2018 WELCOME & INTRODUCTION Sherri Mathews-Hazel, CPA Chief Financial Officer FINANCIAL SERVICES STUDENT ACTIVITY

Career Ladder Editable Template

Career Ladder Editable Template This template is meant to be a guideline only, and can be edited to fit your organizational requirements or limitations. Job Classification: Laboratory Managerial Series

Career Ladder Editable Template This template is meant to be a guideline only, and can be edited to fit your organizational requirements or limitations. Job Classification: Laboratory Managerial Series

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Guidance Note: Corporate Governance - Audit Committee. January Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note

Guidance Note: Corporate Governance - Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note

Internal Audit Charter

Internal Audit Charter Approved by Governing Authority 14 December 2012 Update to previous Internal Audit Charter approved 14 April 2011 1. Introduction 1.1 Internal Audit is responsible for conducting

Internal Audit Charter Approved by Governing Authority 14 December 2012 Update to previous Internal Audit Charter approved 14 April 2011 1. Introduction 1.1 Internal Audit is responsible for conducting

Internal Audit Charter

Internal Audit Charter 1/9 1.0 INTRODUCTION 1.1. Legal Standing a. Bank Indonesia Regulation No.1/6/PBI/1999 dated 20 September 1999 concerning Designation of Compliance Director and Application of the

Internal Audit Charter 1/9 1.0 INTRODUCTION 1.1. Legal Standing a. Bank Indonesia Regulation No.1/6/PBI/1999 dated 20 September 1999 concerning Designation of Compliance Director and Application of the

ROSWELL PARK CANCER INSTITUTE CORPORATION INTERNAL CONTROLS OVER PROCUREMENT AND REVENUES. Report 2005-S-15 OFFICE OF THE NEW YORK STATE COMPTROLLER

Alan G. Hevesi COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE SERVICES Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and Recommendation... 3 Organizational

Alan G. Hevesi COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE SERVICES Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and Recommendation... 3 Organizational

Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources.

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Internal Audit Appendix: IIA Standards

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

TEACHERS RETIREMENT BOARD. AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program

TEACHERS RETIREMENT BOARD AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program CONSENT: ATTACHMENT(S): 3 ACTION: DATE OF MEETING: / 30 mins

TEACHERS RETIREMENT BOARD AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program CONSENT: ATTACHMENT(S): 3 ACTION: DATE OF MEETING: / 30 mins

INTERNAL CONTROLS ON OUR CAMPUS. Kara Kearney-Saylor Director of Internal Audit, UB

INTERNAL CONTROLS ON OUR CAMPUS Kara Kearney-Saylor Director of Internal Audit, UB 1 Select headlines over the past 12 months.. Dennis Black under investigation for UB spending Former UB VP Dennis Black

INTERNAL CONTROLS ON OUR CAMPUS Kara Kearney-Saylor Director of Internal Audit, UB 1 Select headlines over the past 12 months.. Dennis Black under investigation for UB spending Former UB VP Dennis Black

The most commonly applied model for designing and auditing internal

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Internal Audit Charter

Barangaroo Delivery Authority (the Authority) Document Control Approved by: Barangaroo Delivery Authority Board Date of Approval: 9 December 2015 Review Cycle: Annually Reviewed: 29 November 2016 Next

Barangaroo Delivery Authority (the Authority) Document Control Approved by: Barangaroo Delivery Authority Board Date of Approval: 9 December 2015 Review Cycle: Annually Reviewed: 29 November 2016 Next

Quality Assurance and Improvement Program (QAIP)

") Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

OPERATIONAL DIRECTIVE REF. OD.ED INTERNAL AUDIT AND INVESTIGATIONS CHARTER

Headquarters, Copenhagen 15 March 2018 OPERATIONAL DIRECTIVE REF. OD.ED.2018.02 INTERNAL AUDIT AND INVESTIGATIONS CHARTER 1. Authority 1.1. This Operational Directive (OD) is promulgated by the Executive

Headquarters, Copenhagen 15 March 2018 OPERATIONAL DIRECTIVE REF. OD.ED.2018.02 INTERNAL AUDIT AND INVESTIGATIONS CHARTER 1. Authority 1.1. This Operational Directive (OD) is promulgated by the Executive

Chris Horton, Ph.D., CIA, CGAP County Auditor. Arlington County Auditor DRAFT Annual Audit Work Plan FY 2019

Chris Horton, Ph.D., CIA, CGAP County Auditor Arlington County Auditor DRAFT Annual Audit Work Plan FY 2019 June 19, 2018 Introduction The Annual Audit Work Plan for Fiscal Year 2019 (FY 2019 Plan) comprises

Chris Horton, Ph.D., CIA, CGAP County Auditor Arlington County Auditor DRAFT Annual Audit Work Plan FY 2019 June 19, 2018 Introduction The Annual Audit Work Plan for Fiscal Year 2019 (FY 2019 Plan) comprises

SIAAB Guidance #05. Conforming with FCIAA and Standards in Small Audit Functions in the State of Illinois. Adopted December 8, 2015

SIAAB Guidance #05 Conforming with FCIAA and Standards in Small Audit Functions in the State of Illinois Adopted December 8, 2015 Revised In Accordance with 2017 Standards Effective January 1, 2017 ***

SIAAB Guidance #05 Conforming with FCIAA and Standards in Small Audit Functions in the State of Illinois Adopted December 8, 2015 Revised In Accordance with 2017 Standards Effective January 1, 2017 ***

Prince William County, Virginia

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

This document contains a summary of the Group s application of all of the principles contained in King III.

King III Compliance The Board supports the Code of Corporate Practices and Conduct as recommended by the King III Report on Corporate Governance for South Africa 2009 ( King III ). This document contains

King III Compliance The Board supports the Code of Corporate Practices and Conduct as recommended by the King III Report on Corporate Governance for South Africa 2009 ( King III ). This document contains

Fire Department Inventory Management Audit

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

Office of the City Manager

Office of the City Manager TO: FROM: Finance/Audit Committee Ruthe Holden, Internal Audit Manager SUBJECT: Final Fraud Risk Assessment Report-Phase 1 Recommendation This report is for information only.

Office of the City Manager TO: FROM: Finance/Audit Committee Ruthe Holden, Internal Audit Manager SUBJECT: Final Fraud Risk Assessment Report-Phase 1 Recommendation This report is for information only.

S16027 DHS Issued 7/2016

Strategic Plan SFY 2017-2018 DHS STRATEGY MAP SFY 2017-2018 OUR MISSION We improve the quality of life of vulnerable Oklahomans by increasing people s ability to lead safer, healthier, more independent

Strategic Plan SFY 2017-2018 DHS STRATEGY MAP SFY 2017-2018 OUR MISSION We improve the quality of life of vulnerable Oklahomans by increasing people s ability to lead safer, healthier, more independent

Independent Validation of the Internal Auditing Self-Assessment

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT

Minnesota State Colleges & Universities Office of Internal Auditing Independent Validation of the Internal Auditing Self-Assessment Final Report March 7, 2007 Reference Number: 2007-03-004 INDEPENDENT