Production. Microéconomie, chapter 6. Solvay Business School Université Libre de Bruxelles

|

|

|

- Myrtle Franklin

- 6 years ago

- Views:

Transcription

1 Production Microéconomie, chapter 6 1

2 List of subjets Production technology Production with a single input (labor) Isoquants Production with two inputs (labor and capital) Returns to scale 2

3 The production decision of the firm 1. It depends on the available technology How can inputs be transformed into outputs inputs: labor, capital, raw materials outputs: cars, furniture, books Different bundles or inputs deliver different amounts of outputs 3

4 The production decision of the firm 2. It depends also on the production costs The firm takes into account the prices of capital, labor, and other inputs The firm will produce, whatever she chooses, at a minimum cost given technology and the inputs prices If capital is much more expensive than labor, the firm can choose to produce the chosen level of output with more labor and less capital. 4

5 The production decision of the firm 3. The firm maximizes profits Given the minimum cost of producing any given level of output, the firm chooses the level of output that maximizes profits 5

6 The technology of production The production function: Gives the maximum output (q) the can be produced with each bundle of inputs Describes what is technologically feasible using inputs efficiently We will consider two inputs only: labor (L) and capital (K) 6

7 The technology of production The production function with two inputs: q = F(K,L) The level of output (q) depends on the amount of capital (K) and labor (L) used 7

8 The technology of production Short run and long run Adjusting the level of some inputs takes longer the for other inputs The firm must consider both which inputs to adjust and over what time horizon It needs to distinguish between short run and long run 8

9 The technology of production Short run At least one input is a fixed input Long run Horizon beyond which no input is fixed, all inputs are variable inputs 9

10 Production with one input In the short run only one input can be adjusted say capital is fixed and labor is variable Output can be increased increasing labor only 10

11 Production with one input L K q Without labor output is zero The first units of labor are increasingly productive Additional units of labor are less and less productive 11

12 Production with one input The average productivity of labor measures the contribution, on average, of each unit of labor to producing output PM L = output labor = q L 12

13 Production with one input The marginal productivity of labor measures the contribution of an additional unit of labor to the production of output PMg L = Δoutput Δlabor = Δq ΔL 13

14 Production with one input L K q q/l dq/dl

15 Production with one input output 112 D 80 C Total output 60 B 30 A labor 15

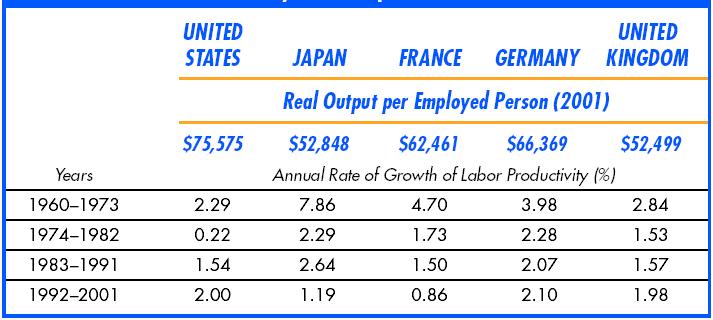

16 Production with one input output 112 D 80 C Total output 60 B Marginal productivity at B 30 A Average productivity at B labor 16

17 Production with one input In the previous example, As labor increases beyond 3 units, output increases less and less At low levels of L additional units allow for a better use of installed capital and thus the marginal productivity of labor is increasing At high levels of L additional units prevent from an efficient use of instaled capital and thus the marginal productivity of labor is decreasing 17

18 Law of decreasing marginal returns As a factor increases, while others remain fixed, the corresponding increases in output become beyond some point smaller and smaller 18

19 Law of decreasing marginal returns It is a consequence of some inputs being fixed in the short run assumes a constant capital stock The productivity of labor increases with the stock of capital assumes constant technology Technical progress increases the output that can be obtained from each combination of inputs The productivity of labor increases with technical progress 19

20 Capital accumulation output 112 D D A higher capital stock increases the level of output at each level of labor C C Increase in the stock of capital B B A A labor 20

21 Technical progress D output 112 C D Technical progress increases the marginal and average productivity of labor at every level C Technical progress 60 B B A A labor 21

22 Productivity of labor Wages (i.e. living standards) and productivity are directly linked When firms maximize profits, inputs are remunerated by their marginal productivity Wages can increase only if labor productivity increases Labor productivity increases if 1. the stock of capital increases 2. there is technological progress 22

23 Productivity of labor 23

24 Productivity of labor 1. The increase in the stock of capital was the main source of the increase in labor productivity 2. The postwar rate of growth of labor productivity in Europe was higher than in the US since the rate of capital accumulation was also higher, due to the reconstruction effort 24

25 Production with two inputs In the long run firms can produce a given level of output with different combinations of labor and capital 25

26 Production with two inputs labor capital

27 Production with two inputs Isoquants link all the inputs combinations that allow to produce a given level of output 27

28 Isoquants capital A Example: 55 units of output can be produced both with 3K and 1L (pt. A) or 1K and 3L (pt. D) 2 q 3 = 90 1 D q 2 = 75 q 1 = labor 28

29 Decreasing returns capital 5 4 For a given level of capital, labor has decreasing returns (A, B, C) 3 A B C 2 1 q 1 = 55 q 2 = 75 q 3 = labor 29

30 Production with two inputs Decreasing returns of labor with a constant capital: If capital stays constant at 3 and labor increases 0 to 1, 2, and 3, then output increases at a decreasing rate (55, 20, 15) 30

31 Decreasing returns capital 5 4 Capital has decreasing returns, for a given level of labor (C, D, E) 3 C 2 1 D E q 1 = 55 q 2 = 75 q 3 = labor 31

32 Production with two inputs Decreasing returns of capital with a constant labor: If labor stays constant at 3 and labor increases 0 to 1, 2, and 3, then output increases at a decreasing rate (55, 20, 15) 32

33 Production with two inputs Inputs substitution Firms can choose the combination of inputs to produce any given level of output A decrease in one input requires and increase in the other input to keep output constant 33

34 Production with two inputs Inputs substitution The slope of each isoquant is the rate at which inputs can be substituted at a given level of output The (absolute value of the) slope is the marginal rate of technical substitution (MRTS) It is the increase in one input needed to compensate a decrease in one unit of the other input in order to keep output constant 34

35 Production with two inputs Marginal rate of technical substitution: TMST = variation of capital variation of labor = ΔK ΔL (q constant) 35

36 Marginal rate of technical substitution capital The MRTS decreases along the isoquant /3 1 Q 1 =55 Q 2 =75 Q 3 = labor 36

37 Production with two inputs As labor substitutes capital Labor becomes relatively less productive Capital becomes relativively more productive Less capital is needed to substitute one unit of labor at constant output The slope of the isoquant becomes smaller (in absolute value) 37

38 MRTS and decreasing marginal returns In the example, increasing labor from 1 to 4 decreases the MRTS from 2 to 1/3 The decrease in the MRTS is a consequence of the decreasing marginal returns of inputs Why? 38

39 MRTS and decreasing marginal returns Assume labor increases and capital decreases so that output remains constant The change in output due to the change in labor is: MgP L ΔL 39

40 MRTS and decreasing marginal returns Assume labor increases and capital decreases so that output remains constant The change in output due to the change in capital is: MgP K ΔK 40

41 MRTS and decreasing marginal returns Since output does not change, both changes must compensate, i.e. MgP L ΔL + MgP K ΔK = 0 MgP L MgP K = ΔL ΔK = MRTS 41

42 Isoquants: special cases Tow special cases of inputs substitution 1. Perfect substitutes The MRTS is constant 42

43 Isoquants: special cases capital A B Perfect substitutes Capital and labor substitute each other always at the same rate C Q 1 Q 2 Q 3 labor 43

44 Isoquants: special cases 2. Perfect complements Inputs must be used in fixed proportions There is no possible substitution between inputs 44

45 Isoquants: special cases capital Perfect complements capital and labor must be used always in the same proportions C Q 3 B Q 2 K 1 Q 1 A labor L 1 45

46 Returns to scale Its the rate at which output increases as inputs increase by a common factor Returns to scale can be Increasing constant decreasing 46

47 Increasing returns to scale Output increases more than proportionally than inputs when mass production is more efficient (e.g. cars) when a single supplier is more efficient (utilities, natural monopolies) 47

48 Increasing returns to scale capital A Output levels of the isoquants increase quickly labor 48

49 Constant returns to scale Output increases in the same proportion than inputs 49

50 Constant returns to scale capital A Output levels of the isoquants increase at a regular pace labor 50

51 Decreasing returns to scale Output increases less than proportionally than inputs Efficiency decreases with the output level 51

52 Decreasing returns to scale capital A 4 20 Output levels of the isoquants increase slowly labor 52

i. The profit maximizing output of firm B is smaller than the profit maximizing output of firm A.

Short Questions 1. A firm is currently producing output using units of labor and units of other materials. The isoquant that corresponds to output level and the firm s optimal input choices are given in

Short Questions 1. A firm is currently producing output using units of labor and units of other materials. The isoquant that corresponds to output level and the firm s optimal input choices are given in

January Examinations 2015

January Examinations 2015 DO NOT OPEN THE QUESTION PAPER UNTIL INS TRUCTED TO DO SO BY THE CHIEF INVIGILATOR Department Module Code Module Title Exam Duration (in words) ECONOMICS EC2000 INTERMEDIATE MICROECONOMICS

January Examinations 2015 DO NOT OPEN THE QUESTION PAPER UNTIL INS TRUCTED TO DO SO BY THE CHIEF INVIGILATOR Department Module Code Module Title Exam Duration (in words) ECONOMICS EC2000 INTERMEDIATE MICROECONOMICS

Chapter 6 Read this chapter together with unit five in the study guide. Firms and Production

Chapter 6 Read this chapter together with unit five in the study guide Firms and Production Topics The Ownership and Management of Firms. Production. Short-Run Production: One Variable and One Fixed Input.

Chapter 6 Read this chapter together with unit five in the study guide Firms and Production Topics The Ownership and Management of Firms. Production. Short-Run Production: One Variable and One Fixed Input.

Review Notes for Chapter Optimal decision making by anyone Engage in an activity up to the point where the marginal benefit= marginal cost

Review Notes for Chapter 5 1. Optimal decision making by anyone Engage in an activity up to the point where the marginal benefit= marginal cost Sunk costs are costs which must be borne regardless of future

Review Notes for Chapter 5 1. Optimal decision making by anyone Engage in an activity up to the point where the marginal benefit= marginal cost Sunk costs are costs which must be borne regardless of future

Last Name First Name ID#

Last Name First Name ID# ---Form A Prof. Harford Price Theory I Section 3, Spring 2003 Second Test, Form A 1. If prices don t all change at the same rate, the consumer price index that calculates what

Last Name First Name ID# ---Form A Prof. Harford Price Theory I Section 3, Spring 2003 Second Test, Form A 1. If prices don t all change at the same rate, the consumer price index that calculates what

Ecn Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman Final Exam You have until 1:50pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman Final Exam You have until 1:50pm to complete this exam. Be certain to put your name,

DEMAND FORECASTING (PART II)

") BEC 30325: MANAGERIAL ECONOMICS Session 06 DEMAND FORECASTING (PART II) Dr. Sumudu Perera Session Outline 2 Smoothing Techniques- Example- Moving Average Limitations of Qualitative Demand Forecasting Limitations

BEC 30325: MANAGERIAL ECONOMICS Session 06 DEMAND FORECASTING (PART II) Dr. Sumudu Perera Session Outline 2 Smoothing Techniques- Example- Moving Average Limitations of Qualitative Demand Forecasting Limitations

Economics 101 Midterm Exam #2. April 9, Instructions

Economics 101 Spring 2009 Professor Wallace Economics 101 Midterm Exam #2 April 9, 2009 Instructions Do not open the exam until you are instructed to begin. You will need a #2 lead pencil. If you do not

Economics 101 Spring 2009 Professor Wallace Economics 101 Midterm Exam #2 April 9, 2009 Instructions Do not open the exam until you are instructed to begin. You will need a #2 lead pencil. If you do not

MICROECONOMICS II - REVIEW QUESTIONS I

MICROECONOMICS II - REVIEW QUESTIONS I. What is a production function? How does a long-run production function differ from a short-run production function? A production function represents how inputs are

MICROECONOMICS II - REVIEW QUESTIONS I. What is a production function? How does a long-run production function differ from a short-run production function? A production function represents how inputs are

Chapter 11. Microeconomics. Technology, Production, and Costs. Modified by: Yun Wang Florida International University Spring 2018

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Classnotes for chapter 13

Classnotes for chapter 13 Chapter 13: Very important Focuses on firms production and costs Examines firm behavior in more detail (previously we simply looked at the supply curve to understand firm behavior)

Classnotes for chapter 13 Chapter 13: Very important Focuses on firms production and costs Examines firm behavior in more detail (previously we simply looked at the supply curve to understand firm behavior)

Choose the one alternative that BEST completes the statement or answers the question.

CHAPTER 3 The Demand for Labor In addition to the multiple choice and quantitative problems listed here, you should answer review questions 1, 3, 5, and 7 and problems 1-4 at the end of chapter 3. Multiple-Choice

CHAPTER 3 The Demand for Labor In addition to the multiple choice and quantitative problems listed here, you should answer review questions 1, 3, 5, and 7 and problems 1-4 at the end of chapter 3. Multiple-Choice

The total final is worth 30 points. Each question is worth 2 points, and each sub question is worth an equal share of the two points.

Final PPA 723, Fall 2002 Professor John McPeak December 9 th, 2002 Name: The total final is worth 30 points. Each question is worth 2 points, and each sub question is worth an equal share of the two points.

Final PPA 723, Fall 2002 Professor John McPeak December 9 th, 2002 Name: The total final is worth 30 points. Each question is worth 2 points, and each sub question is worth an equal share of the two points.

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Managerial Economics & Business Strategy. Final Exam Section 2 May 11 th 7:30 am-10:00 am HH 076

Managerial Economics & Business Strategy Final Exam Section 2 May 11 th 7:30 am-10:00 am HH 076 Grading Scale 5% - Attendance 8% - Homework (Drop the lowest grade) 7% - Quizzes (Drop the lowest grade)

Managerial Economics & Business Strategy Final Exam Section 2 May 11 th 7:30 am-10:00 am HH 076 Grading Scale 5% - Attendance 8% - Homework (Drop the lowest grade) 7% - Quizzes (Drop the lowest grade)

Contents. Concepts of Revenue I-13. About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

Ecn Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman Final Exam You have until 8pm to complete the exam, be certain to use your time wisely.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman Final Exam You have until 8pm to complete the exam, be certain to use your time wisely.

FOR MORE PAPERS LOGON TO

ECO401- Economics Question No: 1 ( Marks: 1 ) - Please choose one Land is best described as: Produced factors of production. "Organizational" resources. Physical and mental abilities of people. "Naturally"

ECO401- Economics Question No: 1 ( Marks: 1 ) - Please choose one Land is best described as: Produced factors of production. "Organizational" resources. Physical and mental abilities of people. "Naturally"

What is Utility: Total utility & Marginal utility:

Economic Theory of Consumer Behavior * What is utility. * Define total utility and marginal utility.*** * State the law of diminishing marginal utility.**** * Define indifference curve and indifference

Economic Theory of Consumer Behavior * What is utility. * Define total utility and marginal utility.*** * State the law of diminishing marginal utility.**** * Define indifference curve and indifference

Midterm 2 - Solutions

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis November 13, 2009 Instructor: John Parman Midterm 2 - Solutions You have until 11:50am to complete this exam. Be certain to

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis November 13, 2009 Instructor: John Parman Midterm 2 - Solutions You have until 11:50am to complete this exam. Be certain to

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Application: the effect of immigration on domestic wages

LABOUR DEMAND Application: the effect of igration on domestic wages Case 1. Immigrants and nonigrants are perfect substitutes in production W S 0 S 1 Law of one price: all workers earn the same wage W

LABOUR DEMAND Application: the effect of igration on domestic wages Case 1. Immigrants and nonigrants are perfect substitutes in production W S 0 S 1 Law of one price: all workers earn the same wage W

ECO401- Economics Spring 2009 Marks: 20 NOTE: READ AND STRICTLY FOLLOW ALL THESE INSTRUCTIONS BEFORE ATTEMPTING THE QUIZ.

www..net - Economics Spring 2009 Marks: 20 NOTE: READ AND STRICTLY FOLLOW ALL THESE INSTRUCTIONS BEFORE ATTEMPTING THE QUIZ. INSTRUCTIONS This quiz covers Lesson # 01-14. Do not use red color in your quiz.

www..net - Economics Spring 2009 Marks: 20 NOTE: READ AND STRICTLY FOLLOW ALL THESE INSTRUCTIONS BEFORE ATTEMPTING THE QUIZ. INSTRUCTIONS This quiz covers Lesson # 01-14. Do not use red color in your quiz.

The Economics of Labor Markets. salary

The Economics of Labor Markets salary Factors of Production Factors of production are the inputs used to produce goods and services. The Market for the Factors of Production The demand for a factor of

The Economics of Labor Markets salary Factors of Production Factors of production are the inputs used to produce goods and services. The Market for the Factors of Production The demand for a factor of

2) A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)

A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)") Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Review Questions. The Own-Wage Elasticity of Labor Demand. Choose the letter that represents the BEST response.

Chapter 4 Labor Demand Elasticities 49 Review Questions Choose the letter that represents the BEST response. The Own-Wage Elasticity of Labor Demand 1. If the wage paid to automobile workers goes up by

Chapter 4 Labor Demand Elasticities 49 Review Questions Choose the letter that represents the BEST response. The Own-Wage Elasticity of Labor Demand 1. If the wage paid to automobile workers goes up by

Preface. Chapter 1 Basic Tools Used in Understanding Microeconomics. 1.1 Economic Models

Preface Chapter 1 Basic Tools Used in Understanding Microeconomics 1.1 Economic Models 1.1.1 Positive and Normative Analysis 1.1.2 The Market Economy Model 1.1.3 Types of Economic Problems 1.2 Mathematics

Preface Chapter 1 Basic Tools Used in Understanding Microeconomics 1.1 Economic Models 1.1.1 Positive and Normative Analysis 1.1.2 The Market Economy Model 1.1.3 Types of Economic Problems 1.2 Mathematics

Economics 323 Microeconomic Theory Fall 2016

pink=a FIRST EXAM Chapter Two Economics 33 Microeconomic Theory Fall 06. The process whereby price directs existing supplies of a product to the users who value it the most is called the function of price.

pink=a FIRST EXAM Chapter Two Economics 33 Microeconomic Theory Fall 06. The process whereby price directs existing supplies of a product to the users who value it the most is called the function of price.

Economics 323 Microeconomic Theory Fall 2016

peach=b FIRST EXAM Chapter Two Economics 33 Microeconomic Theory Fall 06. The process whereby price directs existing supplies of a product to the users who value it the most is called the function of price.

peach=b FIRST EXAM Chapter Two Economics 33 Microeconomic Theory Fall 06. The process whereby price directs existing supplies of a product to the users who value it the most is called the function of price.

Final Exam - Solutions

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 009 Instructor: John Parman Final Exam - Solutions You have until 1:30pm to complete this exam. Be certain to put

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 009 Instructor: John Parman Final Exam - Solutions You have until 1:30pm to complete this exam. Be certain to put

UNIT II THEORY OF PRODUCTION AND COST ANALYSIS

UNIT II THEORY OF PRODUCTION AND COST ANALYSIS Production Function:- The production function expresses a functional relationship between physical inputs and physical outputs of a firm at any particular

UNIT II THEORY OF PRODUCTION AND COST ANALYSIS Production Function:- The production function expresses a functional relationship between physical inputs and physical outputs of a firm at any particular

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 07 No of Questions - 07 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I INTAKE VIII (GROUP A) END SEMESTER

All Rights Reserved No. of Pages - 07 No of Questions - 07 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I INTAKE VIII (GROUP A) END SEMESTER

Chapter 33: Terms of Trade

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Labor Demand. Rongsheng Tang. July, Washington U. in St. Louis. Rongsheng Tang (Washington U. in St. Louis) Labor Demand July, / 53

Labor Demand July, / 53") Labor Demand Rongsheng Tang Washington U. in St. Louis July, 2016 Rongsheng Tang (Washington U. in St. Louis) Labor Demand July, 2016 1 / 53 Overview The production function The employment decision in

Labor Demand Rongsheng Tang Washington U. in St. Louis July, 2016 Rongsheng Tang (Washington U. in St. Louis) Labor Demand July, 2016 1 / 53 Overview The production function The employment decision in

The Production Process: The Behavior of Profit-Maximizing Firms

Chapter 7 The Production Process: The Behavior of Profit-Maximizing Firms Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair The Production

Chapter 7 The Production Process: The Behavior of Profit-Maximizing Firms Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair The Production

Labour Demand Lecturer: Dr. Priscilla T. Baffour

Lecture 3 Labour Demand Lecturer: Dr. Priscilla T. Baffour Determinants of Short Run Demand for Labour The wage rate: The wage rate is a very important determinant of labour demand. Thus the higher the

Lecture 3 Labour Demand Lecturer: Dr. Priscilla T. Baffour Determinants of Short Run Demand for Labour The wage rate: The wage rate is a very important determinant of labour demand. Thus the higher the

Costs: Introduction. Costs 26/09/2017. Managerial Problem. Solution Approach. Take-away

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

Economics 101 Fall 2016 Homework #4 Due November 17, 2016

Economics 101 Fall 2016 Homework #4 Due November 17, 2016 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 101 Fall 2016 Homework #4 Due November 17, 2016 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015

Signature: William M. Boal Printed name: EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015 INSTRUCTIONS: This exam is closed-book, closed-notes. Calculators, mobile phones,

Signature: William M. Boal Printed name: EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015 INSTRUCTIONS: This exam is closed-book, closed-notes. Calculators, mobile phones,

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

Chapter 1- Introduction

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Course Information Introduction to Economics I (ECON 1001)

") Course Information Introduction to Economics I (ECON 1001) Course Code ECON 1001 Course Title Course Discipline Introduction to Economics I Economics Units of Credit Three (3) Pre-requisite None Semester

Course Information Introduction to Economics I (ECON 1001) Course Code ECON 1001 Course Title Course Discipline Introduction to Economics I Economics Units of Credit Three (3) Pre-requisite None Semester

CASE FAIR OSTER PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N. PEARSON 2014 Pearson Education, Inc. Publishing as Prentice Hall

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 50 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 50 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

Marginal Cost. Average Cost 0 20 NA NA NA a) Is this a short run or long run information on cost? Why?

Is this a short run or long run information on cost? Why?") McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

NAME: INTERMEDIATE MICROECONOMIC THEORY FALL 2006 ECONOMICS 300/012 Final Exam December 8, 2006

NAME: INTERMEDIATE MICROECONOMIC THEORY FALL 2006 ECONOMICS 300/012 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1. The slope

NAME: INTERMEDIATE MICROECONOMIC THEORY FALL 2006 ECONOMICS 300/012 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1. The slope

Chapter 4. Labour Demand. McGraw-Hill/Irwin Labor Economics, 4 th edition. Copyright 2008 The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 4 Labour Demand McGraw-Hill/Irwin Labor Economics, 4 th edition Copyright 2008 The McGraw-Hill Companies, Inc. All rights reserved. 4-2 Introduction Firms hire workers because consumers want to

Chapter 4 Labour Demand McGraw-Hill/Irwin Labor Economics, 4 th edition Copyright 2008 The McGraw-Hill Companies, Inc. All rights reserved. 4-2 Introduction Firms hire workers because consumers want to

Final Exam - Solutions

Ecn 00 - Intermediate Microeconomic Theory University of California - Davis September 9, 009 Instructor: John Parman Final Exam - Solutions You have until :50pm to complete this exam. Be certain to put

Ecn 00 - Intermediate Microeconomic Theory University of California - Davis September 9, 009 Instructor: John Parman Final Exam - Solutions You have until :50pm to complete this exam. Be certain to put

AS/ECON AF Answers to Assignment 1 October 2007

AS/ECON 4070 3.0AF Answers to Assignment 1 October 2007 Q1. Find all the efficient allocations in the following 2 person, 2 good, 2 input economy. The 2 goods, food and clothing, are produced using labour

AS/ECON 4070 3.0AF Answers to Assignment 1 October 2007 Q1. Find all the efficient allocations in the following 2 person, 2 good, 2 input economy. The 2 goods, food and clothing, are produced using labour

Historic Growth and Contemporary Development: Lesson & Controversies. The Economics of Growth: Capital, Labor, and Technology:

Historic Growth and Contemporary Development: esson & Controversies The Economics of Growth: Capital, abor, and Technology: 1) Capital accumulation, including all new investments in land, physical equipment,

Historic Growth and Contemporary Development: esson & Controversies The Economics of Growth: Capital, abor, and Technology: 1) Capital accumulation, including all new investments in land, physical equipment,

Average Cost 0 20 NA NA NA a) Is this a short run or long run information on cost? Why?

Is this a short run or long run information on cost? Why?") McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Case: An Increase in the Demand for the Product

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

3 CHAPTER OUTLINE CASE FAIR OSTER PEARSON. Demand, Supply, and Market Equilibrium. Input Markets and Output Markets: The Circular Flow

CASE FAIR OSTER PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N Prepared by: Fernando Quijano w/shelly Tefft 2of 68 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

CASE FAIR OSTER PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N Prepared by: Fernando Quijano w/shelly Tefft 2of 68 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

Chapter 3. Labour Demand. Introduction. purchase a variety of goods and services.

Chapter 3 Labour Demand McGraw-Hill/Irwin Labor Economics, 4 th edition Copyright 2008 The McGraw-Hill Companies, Inc. All rights reserved. 4-2 Introduction Firms hire workers because consumers want to

Chapter 3 Labour Demand McGraw-Hill/Irwin Labor Economics, 4 th edition Copyright 2008 The McGraw-Hill Companies, Inc. All rights reserved. 4-2 Introduction Firms hire workers because consumers want to

Quiz 2 Fall Each question is worth 15 points for a total of 60. 1) Short Answers (2-4 sentences for each part)

Short Answers (2-4 sentences for each part)") EnvEcon 1 / Econ 3 P. Berck Quiz 2 Fall 2004 Directions: Read each question carefully. Write all answers in your blue books. You may use diagrams in your explanations as long as you explain what they show.

EnvEcon 1 / Econ 3 P. Berck Quiz 2 Fall 2004 Directions: Read each question carefully. Write all answers in your blue books. You may use diagrams in your explanations as long as you explain what they show.

ECO232 Chapter 25 Homework. Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books

ECO232 Chapter 25 Homework Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books 1. (Figure: Coffee and Comic Books) Refer to the figure. A consumer has $5 to spend on comic

ECO232 Chapter 25 Homework Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books 1. (Figure: Coffee and Comic Books) Refer to the figure. A consumer has $5 to spend on comic

Course Information Introduction to Economics I (ECON 1001)

") Course Information Introduction to Economics I (ECON 1001) Course Code ECON 1001 Course Title Course Discipline Introduction to Economics I Economics Units of Credit Three (3) Pre-requisites None Semester

Course Information Introduction to Economics I (ECON 1001) Course Code ECON 1001 Course Title Course Discipline Introduction to Economics I Economics Units of Credit Three (3) Pre-requisites None Semester

6. The law of diminishing marginal returns begins to take effect at labor input level: a. 0 b. X c. Y d. Z

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

CHAPTER 11 Consumer Preferences & Consumer Choice. Kazu Matsuda IBEC 202 Microeconomics

CHAPTER 11 Consumer Preferences & Consumer Choice Kazu Matsuda IBEC 22 Microeconomics Mapping the Utility Function A utility function = determines a consumer s total utility given his or her consumption

CHAPTER 11 Consumer Preferences & Consumer Choice Kazu Matsuda IBEC 22 Microeconomics Mapping the Utility Function A utility function = determines a consumer s total utility given his or her consumption

The Cost of Production

C H A P T E R 7 The Cost of Production Prepared by: Fernando & Yvonn Quijano CHAPTER 7 OUTLINE 7.1 Measuring Cost: Which Costs Matter? 7.2 Cost in the Short Run 7.3 Cost in the Long Run 7.4 Long-Run versus

C H A P T E R 7 The Cost of Production Prepared by: Fernando & Yvonn Quijano CHAPTER 7 OUTLINE 7.1 Measuring Cost: Which Costs Matter? 7.2 Cost in the Short Run 7.3 Cost in the Long Run 7.4 Long-Run versus

Name Block Date. Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review

Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review") Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

BUSINESS ECONOMICS (PART 23) FACTOR PRICING UNIT - 6 WAGES II (A)

FACTOR PRICING UNIT - 6 WAGES II (A)") BUSINESS ECONOMICS (PART 23) FACTOR PRICING UNIT - 6 WAGES II (A) 1. INTRODUCTION Welcome viewers, today we shall discuss the theory of factor pricing. But before talking or discussing about the theory

BUSINESS ECONOMICS (PART 23) FACTOR PRICING UNIT - 6 WAGES II (A) 1. INTRODUCTION Welcome viewers, today we shall discuss the theory of factor pricing. But before talking or discussing about the theory

Turgut Ozal University Department of Economics ECO 152 Spring 2014 Assist. Prof. Dr. Umut UNAL PROBLEM SET #5

Turgut Ozal University Department of Economics ECO 152 Spring 2014 Assist. Prof. Dr. Umut UNAL PART A - Definitions 1) Define these terms: Perfect competition Homogeneous products Total revenue Total cost

Turgut Ozal University Department of Economics ECO 152 Spring 2014 Assist. Prof. Dr. Umut UNAL PART A - Definitions 1) Define these terms: Perfect competition Homogeneous products Total revenue Total cost

Quasi-Fixed Labor Costs and Their Effects on Demand

CHAPTER 5 Quasi-Fixed Labor Costs and Their Effects on Demand In addition to the questions below, solve the following end of chapter problems: Review questions 1,3-6, 8; Problems 1-3 1. Suppose that workers

CHAPTER 5 Quasi-Fixed Labor Costs and Their Effects on Demand In addition to the questions below, solve the following end of chapter problems: Review questions 1,3-6, 8; Problems 1-3 1. Suppose that workers

ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

E-BOOK - ELASTICITY OF DEMAND FOR LABOUR

23 May, 2018 E-BOOK - ELASTICITY OF DEMAND FOR LABOUR Document Filetype: PDF 135.09 KB 0 E-BOOK - ELASTICITY OF DEMAND FOR LABOUR Price elasticity of demand (elasticity of demand) is a measure used in

23 May, 2018 E-BOOK - ELASTICITY OF DEMAND FOR LABOUR Document Filetype: PDF 135.09 KB 0 E-BOOK - ELASTICITY OF DEMAND FOR LABOUR Price elasticity of demand (elasticity of demand) is a measure used in

Lesson22: Trade under Monopolistic Competition

International trade in the global economy 60 hours II Semester Luca Salvatici luca.salvatici@uniroma3.it Lesson22: Trade under Monopolistic Competition 1 Trade under Monopolistic Competition Assumptions

International trade in the global economy 60 hours II Semester Luca Salvatici luca.salvatici@uniroma3.it Lesson22: Trade under Monopolistic Competition 1 Trade under Monopolistic Competition Assumptions

Ecn Intermediate Microeconomics University of California - Davis December 7, 2010 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomics University of California - Davis December 7, 2010 Instructor: John Parman Final Exam You have until 12:30 to complete this exam. Be certain to put your name, id number

Ecn 100 - Intermediate Microeconomics University of California - Davis December 7, 2010 Instructor: John Parman Final Exam You have until 12:30 to complete this exam. Be certain to put your name, id number

Microeconomics. Catalog Description

ECON 7005 Microeconomics L T P C Version 1.0 4 0 0 4 Pre-requisites/Exposure - Graduation Co-requisites Course Objectives The objectives of this course are. To understand consumer behavior and its application

ECON 7005 Microeconomics L T P C Version 1.0 4 0 0 4 Pre-requisites/Exposure - Graduation Co-requisites Course Objectives The objectives of this course are. To understand consumer behavior and its application

Econ103_Midterm (Fall 2016)

") Econ103_Midterm (Fall 2016) Total 50 Points. Multiple Choice Identify the choice that best completes the statement or answers the question. 1 point for each question. Total 15 pts. c 1. Which of the following

Econ103_Midterm (Fall 2016) Total 50 Points. Multiple Choice Identify the choice that best completes the statement or answers the question. 1 point for each question. Total 15 pts. c 1. Which of the following

Using Elasticity to Predict Cost Incidence. A Definition & A Question. Who pays when payroll tax added to wage rate?

Using Elasticity to Predict Cost Incidence A Definition & A Question Definition of Incidence: the fact of falling upon; in this case, where costs fall A Question for you what does a statement like this

Using Elasticity to Predict Cost Incidence A Definition & A Question Definition of Incidence: the fact of falling upon; in this case, where costs fall A Question for you what does a statement like this

ECONOMICS 100A: MICROECONOMICS Fall 2006

ECONOMICS 100A: MICROECONOMICS Fall 2006 Section A: Tu, Th 9:30-10:50am York Hall 2622 Section B: Tu, Th 2:00-3:20pm WLH 2005 Prof. Mark Machina Office: Economics Bldg. 217 Office Hours: Wed 8-noon TA

ECONOMICS 100A: MICROECONOMICS Fall 2006 Section A: Tu, Th 9:30-10:50am York Hall 2622 Section B: Tu, Th 2:00-3:20pm WLH 2005 Prof. Mark Machina Office: Economics Bldg. 217 Office Hours: Wed 8-noon TA

EconS Theory of the Firm

EconS 305 - Theory of the Firm Eric Dunaway Washington State University eric.dunaway@wsu.edu October 5, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 16 October 5, 2015 1 / 38 Introduction Theory of the

EconS 305 - Theory of the Firm Eric Dunaway Washington State University eric.dunaway@wsu.edu October 5, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 16 October 5, 2015 1 / 38 Introduction Theory of the

Utility Theory and the Downward Sloping Demand Curve.

Tuesday Notes Utility Theory and the Downward Sloping Demand Curve. Five fundamentals of consumer choice 1. We make decisions purposefully and We are motivated and act based on rational self-interest.

Tuesday Notes Utility Theory and the Downward Sloping Demand Curve. Five fundamentals of consumer choice 1. We make decisions purposefully and We are motivated and act based on rational self-interest.

Microeconomics I PEPM U6101. Summer 2015 Syllabus

Lectures: TR 11:00am-12:50pm, room TBA Instructor: Emanuele Gerratana Office: IAB 1309A Telephone: 212-854 8506 Email: eg198@columbia.edu Office Hours: Thursdays: 1:00pm-2:00pm Microeconomics I PEPM U6101.

Lectures: TR 11:00am-12:50pm, room TBA Instructor: Emanuele Gerratana Office: IAB 1309A Telephone: 212-854 8506 Email: eg198@columbia.edu Office Hours: Thursdays: 1:00pm-2:00pm Microeconomics I PEPM U6101.

Test A. The Market Forces of Supply and Demand. Chapter 4

Chapter 4 The Market Forces of Supply and Demand Test A 1. A market is a a. place where only buyers come together. b. place where only sellers meet. c. group of people with common desires. d. group of

Chapter 4 The Market Forces of Supply and Demand Test A 1. A market is a a. place where only buyers come together. b. place where only sellers meet. c. group of people with common desires. d. group of

Introduction. Consumer Choice 20/09/2017

Consumer Choice Introduction Managerial Problem Paying employees to relocate: when Google wants to transfer an employee from its Seattle office to its London branch, it has to decide how much compensation

Consumer Choice Introduction Managerial Problem Paying employees to relocate: when Google wants to transfer an employee from its Seattle office to its London branch, it has to decide how much compensation

Topic 3. Demand and Supply

Econ 103 Topic 3 page 1 Topic 3 Demand and Supply Text reference: Chapter 3 and 4. Assumptions of the competitive model. Demand: -Determinants of demand -Demand curves -Consumer surplus -Divisibility -

Econ 103 Topic 3 page 1 Topic 3 Demand and Supply Text reference: Chapter 3 and 4. Assumptions of the competitive model. Demand: -Determinants of demand -Demand curves -Consumer surplus -Divisibility -

Langara College Summer archived

Economics 1220 Introductory Microeconomics Section 002 Instructor: Donna Park Office: B147c Phone: 604-323-5841 E-mail: dpark@langara.bc.ca (checked daily during the week) Office Hours 9:45 10:15 and 12:30-1:00

Economics 1220 Introductory Microeconomics Section 002 Instructor: Donna Park Office: B147c Phone: 604-323-5841 E-mail: dpark@langara.bc.ca (checked daily during the week) Office Hours 9:45 10:15 and 12:30-1:00

Please recall how TP, MP and AP are plotted

Please recall how TP, MP and AP are plotted The Marginal Revenue Product (MRP) The increase in total revenue for every additional labor unit employed. Units of Labor TP MP Product Price TR MRP ( TR/ L)

Please recall how TP, MP and AP are plotted The Marginal Revenue Product (MRP) The increase in total revenue for every additional labor unit employed. Units of Labor TP MP Product Price TR MRP ( TR/ L)

Practice Final Exam. Write an expression for each of the following cost concepts. [each 5 points]

![Practice Final Exam. Write an expression for each of the following cost concepts. [each 5 points]](/thumbs/77/75412484.jpg "Practice Final Exam. Write an expression for each of the following cost concepts. [each 5 points]") Practice Final Exam Total : 200 points Exam time: 7:00 9:00. You have 6 questions in 3 pages. Please make your diagrams clear and label it. Good Luck! 1. Amy is currently spending her income to maximize

Practice Final Exam Total : 200 points Exam time: 7:00 9:00. You have 6 questions in 3 pages. Please make your diagrams clear and label it. Good Luck! 1. Amy is currently spending her income to maximize

EXAMINATION 1 VERSION A "Labor Supply and Demand" February 27, 2018

William M. Boal Signature: Printed name: EXAMINATION 1 VERSION A "Labor Supply and Demand" February 27, 2018 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted, but

William M. Boal Signature: Printed name: EXAMINATION 1 VERSION A "Labor Supply and Demand" February 27, 2018 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted, but

b. The marginal opportunity cost of an executive s flight is the price the company could have earned from leasing the jet to someone else.

Chapter 6 Costs SOLUTIONS TO END-OF-CHAPTER QUESTIONS THE NATURE OF COSTS 1.1 The ships that return to Asia are half or completely empty; therefore, the cost of having more merchandise in them is almost

Chapter 6 Costs SOLUTIONS TO END-OF-CHAPTER QUESTIONS THE NATURE OF COSTS 1.1 The ships that return to Asia are half or completely empty; therefore, the cost of having more merchandise in them is almost

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

Final Exam - Solutions

Ecn 100 - Intermediate Microeconomics University of California - Davis December 7, 2010 Instructor: John Parman Final Exam - Solutions You have until 12:30 to complete this exam. Be certain to put your

Ecn 100 - Intermediate Microeconomics University of California - Davis December 7, 2010 Instructor: John Parman Final Exam - Solutions You have until 12:30 to complete this exam. Be certain to put your

Chapter 17: Labor Markets

Chapter 17: Labor Markets Econ 102: Introduction to Microeconomics 1 1.1 Goals of this class Goals of this class Learn how employment and wages are determined in equilibrium. Learn what can shift labor

Chapter 17: Labor Markets Econ 102: Introduction to Microeconomics 1 1.1 Goals of this class Goals of this class Learn how employment and wages are determined in equilibrium. Learn what can shift labor

Chapter 11 Technology, Production, and Costs

Economics 6 th edition 1 Chapter 11 Technology, Production, and Costs Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Technology: An Economic Definition

Economics 6 th edition 1 Chapter 11 Technology, Production, and Costs Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Technology: An Economic Definition

Ecn Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman Final Exam You have until 5:30pm to complete the exam, be certain to use your time wisely.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman Final Exam You have until 5:30pm to complete the exam, be certain to use your time wisely.

ECO401 current paper (May 2010) Today Paper ( )

Today Paper ( )") Solved by afaaq shani bhai adeel Asslam O Alikum ECO 401 MIDTERM PAPERS Solved by Afaaq Shani bhai n Adeel Remember Us In Your Prayers Best regard s Muhammad Afaaq Mba 3 rd Finance Group Afaaq_Tariq@yahoo.com

Solved by afaaq shani bhai adeel Asslam O Alikum ECO 401 MIDTERM PAPERS Solved by Afaaq Shani bhai n Adeel Remember Us In Your Prayers Best regard s Muhammad Afaaq Mba 3 rd Finance Group Afaaq_Tariq@yahoo.com

541: Economics for Public Administration Lecture 8 Short-Run Costs & Supply

I. Introduction 541: Economics for Public Administration Lecture 8 Short-Run s & Supply We have presented how a business finds the least cost way of providing a given level of public good or service. In

I. Introduction 541: Economics for Public Administration Lecture 8 Short-Run s & Supply We have presented how a business finds the least cost way of providing a given level of public good or service. In

Economics 323 Microeconomic Theory Fall 2015

pink=a FIRST EXAM Chapter Two Economics 323 Microeconomic Theory Fall 2015 1. The equilibrium price in a market is the price where a. supply equals demand b. no surpluses or shortages result c. no pressures

pink=a FIRST EXAM Chapter Two Economics 323 Microeconomic Theory Fall 2015 1. The equilibrium price in a market is the price where a. supply equals demand b. no surpluses or shortages result c. no pressures

EXAMINATION 1 VERSION A "Labor Supply and Demand" February 24, 2014

Signature: William M. Boal Printed name: EXAMINATION 1 VERSION A "Labor Supply and Demand" February 24, 2014 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted, but

Signature: William M. Boal Printed name: EXAMINATION 1 VERSION A "Labor Supply and Demand" February 24, 2014 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted, but

ECON Chapter 5 - Labour Economics. Maggie Jones

ECON 370 - Chapter 5 - Labour Economics Maggie Jones Demand for Labour in Competitive Labour Markets Demand for Labour in Competitive Labour Markets The principles that determine the demand for any factor

ECON 370 - Chapter 5 - Labour Economics Maggie Jones Demand for Labour in Competitive Labour Markets Demand for Labour in Competitive Labour Markets The principles that determine the demand for any factor

Commerce 295 Midterm Answers

Commerce 295 Midterm Answers October 27, 2010 PART I MULTIPLE CHOICE QUESTIONS Each question has one correct response. Please circle the letter in front of the correct response for each question. There

Commerce 295 Midterm Answers October 27, 2010 PART I MULTIPLE CHOICE QUESTIONS Each question has one correct response. Please circle the letter in front of the correct response for each question. There

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EXAMINATION JULY 2016

GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EXAMINATION JULY 2016") All Rights Reserved No. of Pages - 08 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EAMINATION JULY 2016 BEC 30325 Managerial

All Rights Reserved No. of Pages - 08 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EAMINATION JULY 2016 BEC 30325 Managerial

Demand & Supply of Resources

Resource Markets 1 Demand & Supply of Resources Resource demand Firms demand resources As long as marginal revenue exceeds marginal cost To maximize profit Resource supply People supply resources To the

Resource Markets 1 Demand & Supply of Resources Resource demand Firms demand resources As long as marginal revenue exceeds marginal cost To maximize profit Resource supply People supply resources To the

1 of 14 5/1/2014 4:56 PM

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

GACE Economics Assessment Test I (038) Curriculum Crosswalk

Curriculum Crosswalk") Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Chapter 4: Individual and Market Demand. Chapter : Implications of optimal choice

Econ 203 Chapter 4 page 1 Overview: Chapter 4: Individual and Market Demand Chapter 4 + 5.1-5.3: Implications of optimal choice What happens if changes? What happens to individual demand if a price changes?

Econ 203 Chapter 4 page 1 Overview: Chapter 4: Individual and Market Demand Chapter 4 + 5.1-5.3: Implications of optimal choice What happens if changes? What happens to individual demand if a price changes?

Final Exam - Solutions

Ecn 100 - Intermediate Microeconomics University of California - Davis June 8, 2010 Instructor: John Parman Final Exam - Solutions You have until 10:00am to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomics University of California - Davis June 8, 2010 Instructor: John Parman Final Exam - Solutions You have until 10:00am to complete this exam. Be certain to put your name,