BALANCED SCORECARD (BSC) Ratapol Wudhikarn, Ph.d. Knowledge management College of Arts, Media and Technology

|

|

|

- Moris Potter

- 6 years ago

- Views:

Transcription

1 BALANCED SCORECARD (BSC) Ratapol Wudhikarn, Ph.d. Knowledge management College of Arts, Media and Technology

2 Contents IC and BSC A concept of BSC The BSC as a management system Why does business need a BSC? The BSC and its perspectives Linking multiple scorecard measures to a single strategy Cause-and-effect relationships Performance driver Design of BSC

3 Objectives The students can Understand a concept of balanced scorecard (BSC). Apply the BSC for planning and executing strategic management.

4 Intellectual capital (IC) and BSC A business competitive has changed. Traditionally, financial assets were solely accepted as a key resource of organizations. Several well-known financial measures have been widely applied for several decades. ROA Return on investment NPV Net present value IRR Internal rate of return

5 IC and BSC (cont.) Measurement of performance using traditional financial methods is currently insufficient (Lerro and Schiuma, 2013). The traditional measures only represent real value of company s assets. Nevertheless, this approach could not reveal hidden values inherent in intangible assets (Fernandez, 2003; Ordóñez de Pablos, 2005).

6 IC and BSC (cont.) Monotonic emphasis >>> Diverse concentrations (Lerro and Schiuma, 2013, Stewart 1997) Financial asset management + Intangible asset management (IC management)

7 IC and BSC (cont.) A traditional management is insufficient anymore (Waterhouse and Svendens, 1998). IC has been broadly identified as a critical management method (Bontis, 1996; Caddy, 2002; Mouritsen, 2004; Kale, 2009). Management of intangible assets with tangible assets was respected as a means of achieving a sustainable competitive advantage (Ordóñez de Pablos, 2005; Solitander and Tidström, 2010).

8 IC and BSC (cont.) Many strategic tools and methods related to IC have been proposed in recent decades. SWOT analysis Five force model BSC EVA TM IC-index Skandia Navigator BSC is a distinguished strategic management technique.

BSC is indicated as major root of IC in a")

9 IC and BSC (cont.) BSC is indicated as major root of IC in a measurement part as depicted in Figure.

10 IC and BSC (cont.) The method comprehensively considers on both financial and non-financial capital. Moreover, it also addresses a critical deficiency of traditional management methods by connecting an organizational long-term strategy with shortterm performances (Kaplan and Norton, 1996).

11 A Concept of BSC The BSC was proposed by Kaplan and Norton (1992). The method provides a systematic framework suggesting conversion processes from the vision, mission and strategy of an organization to coherent strategic objectives and relative key performance indicators (KPIs).

12 A Concept of BSC (cont.) Therefore, this method includes not only management but also measurement consideration (Yüksel and Dağdeviren, 2010). The method considers both lagging and leading measures through four considered perspectives (Janeš, 2013).

13 A Concept of BSC (cont.) Lagging indicators are typically output oriented, easy to measure but hard to improve. Leading indicators are typically input oriented, hard to measure and easy to influence. (

14 A Concept of BSC (cont.) Weight loss activity: What kinds of these indicator? Decreased weight Calories taken in Calories burned (

15 A Concept of BSC (cont.) Most financial indicators such as revenue, profit, costs are lagging indicators. They are results of the activities of the company. Most traditional management approaches focus on the lagging financial indicators.

16 A Concept of BSC (cont.) As previously mentioned, the BSC focuses on both lagging and leading indicators. These indicators are represented in four major perspectives: Financial perspective (F) Customer perspective (C) Internal process perspective (I) Learning and growth perspective (L)

17 A Concept of BSC (cont.) The financial perspective traditionally concentrates on the financial security of the organization. Liquidity Profitability Revenue growth The customer perspective seeks to deliver value to the buyer. Market share Customer retention rate

18 A Concept of BSC (cont.) The internal process perspective encourages the enhancement of process efficiency and effectiveness Defect rate Delivery time New product launching time The learning and growth perspective focuses on the improvement of intangible assets Rate of accomplishment on IT Culture dissemination rate Employee satisfaction

19 The BSC as a Management System Many organizations have performance measurement systems incorporating financial and non-financial measures. Non financial measures >>> local improvements (front-line and customer-facing operations) Financial measures are applied by senior managers as a summary of results of lower and mid-level operations.

20 The BSC as a Management System (cont.) The BSC emphasizes the important of both financial and non-financial measures to be a part of information system for all employees. Front-line employees must to know the financial consequences of their actions. Senior managers also need to realize the relative drivers of long-term financial achievement.

21 The BSC as a Management System (cont.) The objectives and measures of BSC are not derived from adhoc decision. They are systematically derived from a top-down process (vision, mission and strategy). Transforming a business unit s mission and strategy into tangible objectives and measures.

22 The BSC as a Management System (cont.) A Balance of External measures (F and C) and internal measures (I and L) Past efforts (F and C) and future performance (I and L) Objective measures (F and C) and subjective measures (I and L)

23 The BSC as a Management System (cont.) The BSC extends the business s objectives beyond summary financial measures. Executives can measure both current and future values of business delivered to customers. The BSC is more than a tactical or an operational measurement system. A STRATEGIC MANAGEMENT SYSTEM

24 The BSC as a Management System (cont.) Several companies used it to accomplish crucial management processes: Clarify and translate vision and strategy Communicate and link strategic objectives and measures Plan, set targets, and align strategic initiatives Enhance strategic feedback and learning

25 The BSC as a Management System (cont.) (

26 The BSC as a Management System (cont.) Several companies used it to accomplish crucial management processes: Clarify and translate vision and strategy Communicate and link strategic objectives and measures Plan, set targets, and align strategic initiatives Enhance strategic feedback and learning

27 Clarify and translate vision and strategy Senior executives translate business s strategy into strategic objective for all perspectives. One strategy can be transformed to several objectives depending on a business function. For example, one financial institution thought it top 25 senior executives agreed about it strategy. However, each executive had a different definition as to what were the targeted customers.

28 Clarify and translate vision and strategy (cont.) No complete consensus on importance of strategic objectives in group discussion. However the BSC creates a share model of the entire business to which everyone has contributed.

29 The BSC as a Management System (cont.) Several companies used it to accomplish crucial management processes: Clarify and translate vision and strategy Communicate and link strategic objectives and measures Plan, set targets, and align strategic initiatives Enhance strategic feedback and learning

30 Communicate and link strategic objectives and measures The BSC s strategic objectives and measures should be throughly communicated in an organization via Company newsletters Bulletin boards Videos Electronic network The communication serves to signal the critical objectives that must be accomplished.

31 Communicate and link strategic objectives and measures (cont.) Some companies try to break down organizational measures into specific measures at the operational level. For example, on-time delivery (OTD) >>> setup time of machine. In this approach, local improvement efforts become aligned with organizational success factors.

32 Communicate and link strategic objectives and measures (cont.) Once employees understand high-level objectives and measures, they can establish local objectives that support the business s strategy. In conclusion, everyone in firm should realize the business s long-term goals, and strategy for achieving the goals. Individuals can formulate local actions contributing to business s objectives and they will be also aligned to the organizational direction.

33 The BSC as a Management System (cont.) Several companies used it to accomplish crucial management processes: Clarify and translate vision and strategy Communicate and link strategic objectives and measures Plan, set targets, and align strategic initiatives Enhance strategic feedback and learning

34 Plan, set targets, and align strategic initiatives The greatest impact of BSC is generated when it is deployed to drive organizational change. The executive should establish targets that will transform the company. Challenging target!!! Stock price ROI

35 Plan, set targets, and align strategic initiatives (cont.) Therefore, to achieve the financial objectives, executives must identify extended targets to their customer, internal process and learning and growth objectives. The targets can come from several ways: Meeting Customer expectations Benchmarking

36 Plan, set targets, and align strategic initiatives (cont.) The BSC does not only apply to redesign a local process where gains are easily obtained. Improving only the critical activity.

37 Plan, set targets, and align strategic initiatives (cont.) The BSC also enables the consideration of strategic planning with annual budgeting process. The planning and target-setting management process enables the organization to: Quantify the long-term outcomes, Identify mechanism and provide resources for achieving those outcomes, and Establish short-term milestones for the financial and non-financial measures.

38 The BSC as a Management System (cont.) Several companies used it to accomplish crucial management processes: Clarify and translate vision and strategy Communicate and link strategic objectives and measures Plan, set targets, and align strategic initiatives Enhance strategic feedback and learning

39 Enhance strategic feedback and learning The most critical aspect of BSC Nowadays, executives do not have a process to obtain feedback about their strategy and also to test their hypothesis. The BSC enables them to monitor and adjust their strategic management.

40 Enhance strategic feedback and learning (cont.) By having short-term milestones of all measures, management reviews can examine financial outcomes. Moreover, the executives also examine whether the business is achieving its targets for C, I and L. Shifting past performance to learn about future.

The strategic learning")

41 Enhance strategic feedback and learning (cont.) The strategic learning involves with all processes.

42 Enhance strategic feedback and learning (cont.) The first process (clarify and translate vision and strategy) attempts to clarify a shared vision that the entire organization wants to achieve. The second process (communicate and link strategic objectives and measures) drives employees to execute actions related to organizational objectives.

43 Enhance strategic feedback and learning (cont.) The second process (communicate and link strategic objectives and measures) drives employees to execute actions related to organizational objectives. The emphasis on cause and effect in constructing a scorecard introduces dynamic system thinking. It enables individuals in various parts of an organization to understand how their role influences other and entire organization.

44 Enhance strategic feedback and learning (cont.) The third process (plan, set targets, and align strategic initiatives) defines the quantitative expected performance of organization across a balanced set of outcomes and drivers. A comparison of desired goals with current levels represents the performance gap that strategic initiatives can be designed to close.

45 Enhance strategic feedback and learning (cont.) The three processes are crucial for implementing strategy. Only these processes, they are insufficient. The feedback process should be included or integrated with the BSC processes.

46 Enhance strategic feedback and learning (cont.) Sailing Captain (CEO) determines the direction and speed. The sailors (managers and front-line employees) carry out the orders and implement the identified plan.

47 Enhance strategic feedback and learning (cont.) Sailing Operational and management control systems must be established to ensure that the managers and employees act in accordance with the strategic plan indicated by executives.

48 Enhance strategic feedback and learning (cont.) Sailing Operational and management control systems must be established to ensure that the managers and employees act in accordance with the strategic plan indicated by executives.

49 Enhance strategic feedback and learning (cont.) Sailing This approach of establishing a vision and strategy, communicating and linking vision and strategy to all organizational participants, and aligning actions and initiatives to achieving longterm goals is a single-loop feedback process.

50 Enhance strategic feedback and learning (cont.) With the single-loop, the objective remains constant. There is no question about the plan, method and result. XXXXX Are they still appropriate? XXXXX In a real-life situation, the strategies cannot be stable.

51 Enhance strategic feedback and learning (cont.) In currently intensive competition, executives highly require feedback. Thinking about sailing, under changing weather and sea conditions, a chain of command still exists, and captain needs to respond to the turbulent condition.

52 Enhance strategic feedback and learning (cont.) Therefore, in constantly changing environment, new strategies can emerge from opportunities or threats that were not considered before. Traditional management systems do not encourage nor facilitate the formulation, implementation, and testing of strategy in changing environments.

53 Enhance strategic feedback and learning (cont.) Organizations need the double-loop feedback. Checking >>> the operations remain consistent with current situation. Executives strongly need feedback about the planned strategy remains a viable and successful strategy.

54 Enhance strategic feedback and learning (cont.) A properly constructed BSC should represent the cause-and-effect relationships of strategic objectives. If employees and executives have achieved the drivers, but failure to achieve expected results represents that the identified strategy may not be valid.

55 Why does business need a BSC? If you can t measure it, you can t manage it Peter Drucker If companies want to survive, they must use measurement and management systems derived from their strategies and capabilities. Unfortunately, many firms adopts strategies related to CRM, core competencies, organizational capabilities while measuring performance only with financial measures.

56 Why does business need a BSC? (cont.) The BSC still retains financial measurement as a crucial summary of managerial and business performance, but it remains to focusing on a more integrated set of measurement linking customer, internal process and learning and growth to longterm financial success.

57 The BSC and its perspectives The BSC provides a comprehensive framework transforming a organization s vision and strategy into a relative set of measurement system. Several organizations have adopted mission statements to communicate fundamental values and belief to all employees. Nevertheless, the inspirational mission statement and slogans are insufficient.

58 The BSC and its perspectives (cont.) As mentioned, the BSC translates mission and strategy into objectives and measures organized into four perspectives.

59 Financial perspective The BSC retains the financial perspective since financial measures are valuable in summarizing the readily measurable economic consequences of actions already taken. Financial performance measures indicate whether a company s strategy, implementation, and execution are contributing to bottom-line improvement.

60 Financial perspective (cont.) Financial objectives typically relate to profitability measured, for example, by operating income, return-on-capital employed, or, more recently, economic value-added.

61 Customer perspective Managers identify the customer and market segments in which the business unit will compete and the measures of the business unit s performance in these targeted segments. This perspective typically includes several core or generic measures of the successful outcomes from a well-formulated and -implemented strategy.

62 Customer perspective (cont.) The core outcome measures include customer satisfaction, customer retention, new customer acquisition, customer profitability, and market and account share in targeted segments. But the customer perspective should also include specific measures of the value propositions that the company will deliver to customers in targeted market segments.

63 Customer perspective (cont.) The segment-specific drivers of core customer outcomes represent those factors that are critical for customers to switch to or remain loyal to their suppliers. For example, customers could value short lead times and on-time delivery. The customer perspective enables business unit managers to articulate the customer and marketbased strategy that will deliver superior future financial returns.

64 Internal process perspective In the internal-business-process perspective, executives identify the critical internal processes in which the organization must excel. These processes enable the business unit to: deliver the value propositions that will attract and retain customers in targeted market segments, and satisfy shareholder expectations of excellent financial returns.

65 Internal process perspective (cont.) The internal-business-process measures focus on the internal processes that will have the greatest impact on customer satisfaction and achieving an organization s financial objectives. The internal-business-process perspective reveals two fundamental differences between the traditional and the BSC approaches to performance measurement.

66 Internal process perspective (cont.) Traditional approaches attempt to monitor and improve existing business processes. These measurements generally include quality and time-based metrics. They typically concentrate on improvement of existing processes.

67 Internal process perspective (cont.) Nevertheless, the BSC will usually identify entirely new processes at which an organization must excel to meet customer and financial objectives. The objectives directly serve vision, missions, or financial and customer objectives.

68 Internal process perspective (cont.) For instance, from the identification of financial and customer objectives, a company may realize that it should provide a critical process serving customer needs or any process to deliver new services that directly target customers value. The internal process objectives highlight the processes, several of which it may not be identified and focused before the adoption of BSC.

69 Internal process perspective (cont.) The second difference of the BSC approach is to incorporate innovation processes into the internal process perspective. Most traditional performance measurement systems concentrate on the processes of delivering today s products and services to today s customers.

70 Internal process perspective (cont.) They attempt to control and improve existing operations that represent the short wave of value creation. This short wave of value creation begins with the receipt of an order from an existing customer for an existing product (or service) and ends with the delivery of the product to the customer.

71 Internal process perspective (cont.) The organization creates value from producing, delivering, and servicing this product and the customer at a cost below the price it receives. This approach is insufficient since it cannot sustain an organization.

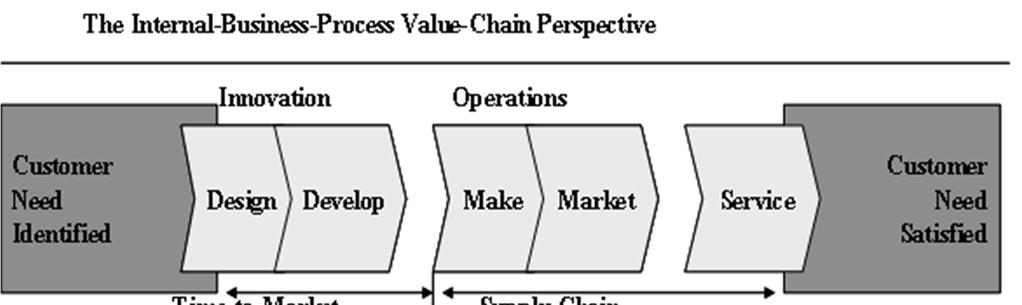

72 Internal process perspective (cont.) Source: 4.gif

73 Internal process perspective (cont.) But the drivers of long-term success may require entirely new products and services responding to the emerging needs of current and future customers. The innovation process is a more powerful driver of future performance than the short-term operating cycle.

74 Internal process perspective (cont.) For several organizations, the ability to manage a product-development process or to reach entirely new categories of customers may be more critical for future economic performance than managing existing operations.

75 Internal process perspective (cont.) Nevertheless, executives do not have to choose between these two vital internal processes. The internal process perspective considers objectives and measures for both the long-term values and the short-wave operations.

76 Learning and growth perspective The fourth perspective identifies the infrastructure of organization that must be built to create longterm growth and improvement. The customer and internal process perspectives identify the factors most critical for current and future success.

77 Learning and growth perspective Organizations cannot achieve their long-term goals using today s technologies and capabilities. Moreover, intensive competition forces companies to continually improve their capabilities for delivering value to customers and shareholders.

78 Learning and growth perspective (cont.) Organizational learning and growth come from three principal sources: people, systems, and organizational procedures The financial, customer, and internal process objectives on the BSC typically will reveal large gaps between the existing capabilities of people, systems, and procedures.

79 Learning and growth perspective (cont.) From the gaps, organizations will realize that what will be required to achieve breakthrough performance. To improve these gaps, companies have to invest in reskilling employees, enhancing information technology and systems, and also aligning organizational procedures and routines.

80 Learning and growth perspective (cont.) These objectives are articulated in the learning and growth perspective of the BSC. Similar to the customer perspective, measures of this perspective include a mixture of generic outcome measures: employee satisfaction, employee retention, training, and skills

81 Learning and growth perspective (cont.) There are also specific drivers of the generic measures, such as detailed, business-specific indexes of the particular skills required for the new competitive environment. Information systems capabilities can be measured by real-time availability of accurate, critical customer and internal process information to employees on the front lines of decision making and actions. Organizational procedures can examine alignment of employee incentives with overall organizational success factors, and measured rates of improvement in critical customer-based and internal processes.

82 Learning and growth perspective (cont.) Along with specific drivers of these generic measures, such as detailed, business-specific indexes of the particular skills required for the new competitive environment. Information systems capabilities can be measured by real-time availability of accurate, customer and process information to employees on the front lines.

83 Learning and growth perspective (cont.) Organizational procedures can examine alignment of employee incentives with overall organizational success factors, and measured rates of improvement in critical customer-based and internal processes.

84 The BSC and its perspectives (cont.) In conclusion, the BSC transforms vision and strategy into objectives and measures across a balanced set of perspectives. The scorecard includes measures of desired outcomes as well as processes that will drive the desired outcomes for the future.

85 Linking multiple scorecard measures to a single strategy In most cases, a company may already establish a mixture of financial and non-financial measures. Especially in recent years, the renewed focus on customers and process quality has forced several companies to track nonfinancial measures such as customer satisfaction and complaints, product and process defect levels, and missed delivery dates.

86 Linking multiple scorecard measures to a single strategy (cont.) Nevertheless, the BSC are more than collections of critical indicators or key success factors. The multiple measures on a properly constructed BSC should consist of a linked series of objectives and measures that are both consistent and mutually reinforcing.

87 Linking multiple scorecard measures to a single strategy (cont.) Like a flight simulator, the scorecard should incorporate the complex set of cause-and-effect relationships among the critical variables, including leads, lags, and feedback loops, that describe the trajectory, the flight plan, of the strategy. The linkages should incorporate both cause-andeffect relationships, and mixtures of outcome measures and performance drivers.

88 Cause-and-effect relationships A strategy is a set of hypotheses about cause and effect. The measurement system should make the relationships (hypotheses) among objectives (and measures) in the various perspectives explicit so that they can be managed and validated. The chain of cause and effect should pervade all four perspectives of a Balanced Scorecard.

89 Cause-and-effect relationships (cont.) For example, return-on-capital-employed may be a scorecard measure in the financial perspective. The driver of this measure could be repeat and expanded sales from existing customers, the result of a high degree of loyalty among those customers. So, customer loyalty is included on the scorecard (in the customer perspective) because it is expected to have a strong influence on ROCE.

90 Cause-and-effect relationships (cont.) But how will the organization achieve customer loyalty? Analysis of customer preferences may reveal that on-time delivery of orders is highly valued by customers.

91 Cause-and-effect relationships (cont.) Thus, improved OTD is expected to lead to higher customer loyalty, which, in turn, is expected to lead to higher financial performance. So both customer loyalty and OTD are incorporated into the customer perspective of the scorecard.

92 Cause-and-effect relationships (cont.) The process continues by asking what internal processes must the company excel at to achieve exceptional on-time delivery. To achieve improved OTD, the business may need to achieve short cycle times in operating processes and high-quality internal processes, both factors that could be scorecard measures in the internal perspective.

93 Cause-and-effect relationships (cont.) And how do organizations improve the quality and reduce the cycle times of their internal processes? By training and improving the skills of their operating employees, an objective that would be a candidate for the learning and growth perspective.

94 Cause-and-effect relationships (cont.) We can now see how an entire chain of causeand-effect relationships can be established as a vertical vector through the four BSC perspectives:

95 Cause-and-effect relationships (cont.) Financial Return on capital employed Customer Customer loyalty On-time delivery Internal process Process quality Process cycle time Learning and growth Employee skills

96 Cause-and-effect relationships (cont.) In a similar vein, recent work in the service profit chain has emphasized the causal relationships among employee satisfaction, customer satisfaction, customer loyalty, market share, and, eventually, financial performance. Thus, a properly constructed Balanced Scorecard should tell the story of the business unit s strategy.

97 Cause-and-effect relationships (cont.) It should identify and make explicit the sequence of hypotheses about the cause-and-effect relationships between outcome measures and the performance drivers of those outcomes. Every measure selected for a Balanced Scorecard should be an element in a chain of cause-and-effect relationships that communicates the meaning of the business unit s strategy to the organization.

98 Performance driver A good BSC should also have a mix of outcome measures and performance drivers. Outcome measures without performance drivers do not communicate how the outcomes are to be achieved. They also do not provide an early indication about whether the strategy is being implemented successfully.

99 Performance driver (cont.) Conversely, performance drivers such as defect rates without outcome measures may enable the business unit to achieve short-term operational improvements, but will fail to reveal whether the operational improvements have been translated into expanded business with existing and new customers, and, eventually, to enhanced financial performance.

100 Performance driver (cont.) A good Balanced Scorecard should have an appropriate mix of outcomes (lagging indicators) and performance drivers (leading indicators) of the business unit s strategy.

101 Performance driver (cont.) The scorecard should be the translation of the business unit s strategy into a linked set of measures that define both the long-term strategic objectives, as well as the mechanisms for achieving those objectives.

102 Design of BSC 1. Collecting all relative data 2. Analyzing internal and external environment 3. Reviewing vision and missions 4. Identifying strategic objectives of each perspective 5. Creating a strategy map 6. Setting KPIs and targets 7. Transforming a strategy to action plans 8. Deploying KPI

103 1. Collecting all relative data Vision, mission and strategy Finance Customer Internal process Learning and growth Vision Mission Strategic plan History Financial report Annual & operational report Financial analysis report Benchmarking report Financial journal Marketing journal Marketing data Consultant Strategic plan Customer annual report Requirements, expectations and opportunities of markets Operational annual report Production report Competitor data Benchmarking data Human capital data Human journal Benchmarking data

104 2. Analyzing internal and external environment Situation analysis Internal (Controllable) External (Uncontrollable) Customer Competitor Organization Industry Country World Strength / Weakness Opportunity / Threat

105 2. Analyzing internal and external environment (cont.) Market Competition Sociocultural Technology Market share Industry competition Trend Agility Growth rate New competitor Structure New technology Profitability Supplier Culture / Belief Production technology Substitute product Economic Politic Revenue per capita Government policy Interest rate Political stability Exchange rate International relationship Infrastructure

106 2. Analyzing internal and external environment (cont.) Strength Weakness Opportunity Threat Finance Customer Internal process Learning and growth

107 3. Reviewing vision and missions Vision Mission Financial objective Customer objective Internal process objective Learning and growth objective

108 3. Reviewing vision and missions (cont.) Vision Where is our destination? Mission & Strategy How can we go to the destination? Where are we now? SWOT

109 4. Identifying strategic objectives of each perspective Financial perspective Customer perspective Internal process perspective Learning and growth perspective

110 4. Identifying strategic objectives of each perspective (cont.) Financial perspective Aim to answer the question: How should the financial performance of organization be? What is the successful financial performance for shareholders? Profitability Liquidity Leverage Revenue growth

111 4. Identifying strategic objectives of each perspective (cont.) Customer perspective Customer intimacy Customer Product leadership Operational excellence

112 4. Identifying strategic objectives of each perspective (cont.) Customer perspective Aim to answer the question: How should a company respond to customer in order to achieve organizational vision? New customers Customer satisfaction Customer retention Market share

113 4. Identifying strategic objectives of each perspective (cont.) Internal process perspective Operations Customer management Innovation Regulatory and society Supply Production Distribution Risk management Selection Acquisition Retention Growth Opportunity R&D Portfolio Design/develop Launch Environment Safety and health Employment Community

114 4. Identifying strategic objectives of each perspective (cont.) Internal process perspective Aim to answer the question: Which process of company should be excellently perform for serving customer and stakeholder? Product improvement Defect rate reduction Delivery time reduction New product launch time

115 4. Identifying strategic objectives of each perspective (cont.) Learning and growth perspective Human capital Skills Knowledge Values Information capital Systems Databases Networks Organizational capital Culture Leadership Alignment Team

116 4. Identifying strategic objectives of each perspective (cont.) Learning and growth perspective Aim to answer the question: How should an organization change & improve process to achieve a vision? Employee satisfaction Safety rate Information system improvement Resignation rate of capable employee

117 5. Creating a strategy map Vision & mission BSC uses cause-and-effect logic Realizing the mission and vision Customer benefits Financial results To deliver customer satisfaction Drive financial responsibility Internal capabilities To build the strategic capabilities Where are we now? Knowledge, kills, systems and tools Equip our people

118 5. Creating a strategy map (cont.) Alignment, cause and effect relationship Finance Outcomes Customer Process Drivers Learning and growth

119 5. Creating a strategy map (cont.) A strategy map creation procedure 1. Verifying an organizational direction and vision 2. Identifying a mission or strategy serving the vision achievement 3. Determining relative strategic objectives following the BSC s perspectives 4. Creating a strategy map by inputting all identified objectives to the related area, and using arrow to identify the relationships among objectives 5. If any objective does not relate to other objectives, there is an error or deficiency with the map

120 5. Creating a strategy map (cont.) Strategy map template VISION Financial Customer Internal process Learning and growth

121 5. Creating a strategy map (cont.) Determining relative strategic objectives following the BSC s perspectives Strategic objective F1 - Increasing revenue F2 - Decreasing a quantity of aircrafts C1 - On-time strategy C2 - Low-cost ticket C3 Customer retention I1 - Increasing departure capability L1 - Employee serving the organizational strategy Perspective F F C C C I L

122 5. Creating a strategy map (cont.) Strategy map Financial F2 F1 Customer C2 C3 C1 Internal process I1 Learning and growth L1

123 5. Creating a strategy map (cont.) Strategic objective KPIs KPI 1 KPI 2 KPI 3 Target XXX YYY ZZZ

124 6. Setting KPIs and targets A key performance indicator (KPI) is a business metric used to evaluate factors that are crucial to the success of an organization ( Quality Quantity Safety Cost Technology Satisfaction Time

125 6. Setting KPIs and targets (cont.) Examples of KPIs Type of KPI Quantity Cost Time Safety Satisfaction Technology KPI Product quantity per day Ratio of cost to revenue Delayed day No. of accident Customer satisfaction score % of technology investment budget

Identifying KPIs and targets Objective KPI Current status Customer")

126 6. Setting KPIs and targets (cont.) Identifying KPIs and targets Objective KPI Current status Customer retention % of repeated purchase 1% 10% Target

127 Reference Kapland R.S., and Nortom, D.P., The balanced scorecard: translating strategy into action, Harvard, 1996.

128 Q&A

Balanced Scorecard. MA. DESIREE D. BELDAD, Ph.D. FEBRUARY 9, 2012

Balanced Scorecard MA. DESIREE D. BELDAD, Ph.D. FEBRUARY 9, 2012 IMAGINE ENTERING THE COCKPIT of a modern jet airplane and seeing only a single instrument there. How do you feel about boarding the plane

Balanced Scorecard MA. DESIREE D. BELDAD, Ph.D. FEBRUARY 9, 2012 IMAGINE ENTERING THE COCKPIT of a modern jet airplane and seeing only a single instrument there. How do you feel about boarding the plane

The Balanced Scorecard- A strategic Management Tool. By Mr. Tarun Mishra. Prologue:

The Balanced Scorecard- A strategic Management Tool Prologue: By Mr. Tarun Mishra It was in 1992, when Robert S Kaplan and David P Norton formed the concept of Balanced Scorecard (BSC) and this revolutionized

The Balanced Scorecard- A strategic Management Tool Prologue: By Mr. Tarun Mishra It was in 1992, when Robert S Kaplan and David P Norton formed the concept of Balanced Scorecard (BSC) and this revolutionized

BALANCE SCORECARD. Introduction. What is Balance Scorecard?

BALANCE SCORECARD Introduction In this completive world where techniques are change in nights, it s very hard for an organization to stay on one technique to grow business. To maintain the business performance

BALANCE SCORECARD Introduction In this completive world where techniques are change in nights, it s very hard for an organization to stay on one technique to grow business. To maintain the business performance

The importance of Balanced Scorecard in business operations

The importance of Balanced Scorecard in business operations Maida Djakovac Novi Pazar, Serbia maidadj86@yahoo.com Abstract The aim of this paper is that to explore the role and importance of applying strategic

The importance of Balanced Scorecard in business operations Maida Djakovac Novi Pazar, Serbia maidadj86@yahoo.com Abstract The aim of this paper is that to explore the role and importance of applying strategic

Quality & Productivity Journal March 2002

Quality & Productivity Journal March 2002 Results that you can count on... The Balanced Score Card -Shree Phadnis, Master Black Belt at KPMG (India) Imagine entering the cockpit of a Jet Plane and observing

Quality & Productivity Journal March 2002 Results that you can count on... The Balanced Score Card -Shree Phadnis, Master Black Belt at KPMG (India) Imagine entering the cockpit of a Jet Plane and observing

Topic. Balanced Scorecard. Performance measurement. William Meaney MBA BSc. ACMA 1

Topic Balanced Scorecard Performance measurement William Meaney MBA BSc. ACMA 1 The Balanced Scorecard Performance measurement William Meaney MBA BSc. ACMA 2 Strategic Implementation People and Systems

Topic Balanced Scorecard Performance measurement William Meaney MBA BSc. ACMA 1 The Balanced Scorecard Performance measurement William Meaney MBA BSc. ACMA 2 Strategic Implementation People and Systems

Quadrant I. Module 25: Balanced Scorecard

Quadrant I Module 25: Balanced Scorecard 1. Learning Outcomes 2. Introduction 3. Balanced Scorecard Framework 4. Balanced Scorecard 5. Organisational Effectiveness 6. Balanced Scorecard & Organisational

Quadrant I Module 25: Balanced Scorecard 1. Learning Outcomes 2. Introduction 3. Balanced Scorecard Framework 4. Balanced Scorecard 5. Organisational Effectiveness 6. Balanced Scorecard & Organisational

Implementation and Practicalities of Balance Scorecard: A Case Study

Page 61 Implementation and Practicalities of Balance Scorecard: A Case Study G.Sreelakshmi # and Prof.D.Suryachandra Rao * # Research Scholar, Krishna University, Andhra Pradesh, India. * Dean, Faculty

Page 61 Implementation and Practicalities of Balance Scorecard: A Case Study G.Sreelakshmi # and Prof.D.Suryachandra Rao * # Research Scholar, Krishna University, Andhra Pradesh, India. * Dean, Faculty

Visionary Leadership. Systems Perspective. Student-Centered Excellence

Core Values and Concepts These beliefs and behaviors are embedded in high-performing organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

Core Values and Concepts These beliefs and behaviors are embedded in high-performing organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

GLOSSARY OF TERMS For Business Performance Management

GLOSSARY OF TERMS For Business Performance Management September 2012 Table of Contents Table of Contents... 1 Introduction... 2 Glossary... 2 Page 1 Introduction Many terms we use when talking about Business

GLOSSARY OF TERMS For Business Performance Management September 2012 Table of Contents Table of Contents... 1 Introduction... 2 Glossary... 2 Page 1 Introduction Many terms we use when talking about Business

The Balanced Scorecard and its Application as a Strategic Decision-making Tool

International Review of Business Research Papers Volume 6. Number 4. September 2010. Pp. 457 466 The Balanced Scorecard and its Application as a Strategic Decision-making Tool Aswini Kumar Dash* and Biswajit

International Review of Business Research Papers Volume 6. Number 4. September 2010. Pp. 457 466 The Balanced Scorecard and its Application as a Strategic Decision-making Tool Aswini Kumar Dash* and Biswajit

Chapter 2: The Balanced Scorecard and Strategy Map Objective 1

Test Bank for Management Accounting Information for Decision Making and Strategy Execution 6th edition by Atkinson Kaplan Matsumura and Young Link download Test Bank for Management Accounting Information

Test Bank for Management Accounting Information for Decision Making and Strategy Execution 6th edition by Atkinson Kaplan Matsumura and Young Link download Test Bank for Management Accounting Information

Balanced Scorecard IT Strategy and Project Management

Balanced Scorecard IT Strategy and Project Management Managing Strategy is is Managing Change Glen B. Alleman Director, Program Management Office Kaiser Hill Company, LLC Rocky Flats Environmental Technology

Balanced Scorecard IT Strategy and Project Management Managing Strategy is is Managing Change Glen B. Alleman Director, Program Management Office Kaiser Hill Company, LLC Rocky Flats Environmental Technology

Cascading the BSC Using the Nine Steps to Success

Cascading the BSC Using the Nine Steps to Success The Balanced Scorecard Institute uses a proven, disciplined framework, Nine Steps to Success, to systematically develop, implement, and sustain a strategic

Cascading the BSC Using the Nine Steps to Success The Balanced Scorecard Institute uses a proven, disciplined framework, Nine Steps to Success, to systematically develop, implement, and sustain a strategic

Core Values and Concepts

Core Values and Concepts These beliefs and behaviors are embedded in high-performing organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

Core Values and Concepts These beliefs and behaviors are embedded in high-performing organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

RESULTS. SAMPLE OF AN ACTUAL REPORT (PART II) Name of site left off. CERTIFIED: No Yes

Name of site left off. CERTIFIED: No Yes") MC WORKFORCE DEVELOPMENT BOARD Technical Assistance Report For XXX Center or Organization From the Certification Subcommittee Of the Quality Assurance Committee DATE SAMPLE OF AN ACTUAL REPORT (PART II)

MC WORKFORCE DEVELOPMENT BOARD Technical Assistance Report For XXX Center or Organization From the Certification Subcommittee Of the Quality Assurance Committee DATE SAMPLE OF AN ACTUAL REPORT (PART II)

Module 9: Balanced Scorecard

file:///f /Courses/2009-10/CGALU/MA2/06course/01mod/m09intro.htm Module 9: Balanced Scorecard Overview Module 9 ties all previous modules together into a method for facilitating decision-making and performance

file:///f /Courses/2009-10/CGALU/MA2/06course/01mod/m09intro.htm Module 9: Balanced Scorecard Overview Module 9 ties all previous modules together into a method for facilitating decision-making and performance

A Guide to the. Incorporating the Essential Elements of Strategy Within Your Organization. Empower

A Guide to the Balanced Scorecard Incorporating the Essential Elements of Strategy Within Your Organization This guide covers Create Keeping strategy creation practical, focused and agile Empower Empowering

A Guide to the Balanced Scorecard Incorporating the Essential Elements of Strategy Within Your Organization This guide covers Create Keeping strategy creation practical, focused and agile Empower Empowering

Balance Sheet. Profit and Loss Account INTELECTUAL ASSETS, BRAND, CUSTOMERS TECNOLOGY

ECONOMIC EVOLUTION COMPANY A TO NEW MANAGEMENT METHODS COMPANY B CLASSIC MANAGEMENT METHODS TO MEASURE ONLY WITH FINANCIAL PARAMETERS ITS NOT ENOUGHT NEW MANAGEMENT TRENDS VALUE CREATION CUSTOMERS Balance

ECONOMIC EVOLUTION COMPANY A TO NEW MANAGEMENT METHODS COMPANY B CLASSIC MANAGEMENT METHODS TO MEASURE ONLY WITH FINANCIAL PARAMETERS ITS NOT ENOUGHT NEW MANAGEMENT TRENDS VALUE CREATION CUSTOMERS Balance

CORE VALUES AND CONCEPTS

CORE VALUES AND CONCEPTS The Criteria are built on the following set of interrelated core values and concepts: visionary leadership customer-driven excellence organizational and personal learning valuing

CORE VALUES AND CONCEPTS The Criteria are built on the following set of interrelated core values and concepts: visionary leadership customer-driven excellence organizational and personal learning valuing

Implementation Of A Computerized Balanced Scorecard (BSC) System In A Manufacturing Organisation In Zimbabwe

System In A Manufacturing Organisation In Zimbabwe") National University of Science and Technolgy NuSpace Institutional Repository Industrial and Manufacturing Engineering http://ir.nust.ac.zw Industrial and Manufacturing Engineering Publications 2013 Implementation

National University of Science and Technolgy NuSpace Institutional Repository Industrial and Manufacturing Engineering http://ir.nust.ac.zw Industrial and Manufacturing Engineering Publications 2013 Implementation

At the end of the programme, the participants should be able to:- Understand the real meaning and importance of KPIs and KRAs to the organisation

PROGRAMME OBJECTIVES At the end of the programme, the participants should be able to:- Understand the real meaning and importance of KPIs and KRAs to the organisation Link PMS to KPIs and KRAs by having

PROGRAMME OBJECTIVES At the end of the programme, the participants should be able to:- Understand the real meaning and importance of KPIs and KRAs to the organisation Link PMS to KPIs and KRAs by having

Core Values and Concepts

Core Values and Concepts These beliefs and behaviors are embedded in highperforming organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

Core Values and Concepts These beliefs and behaviors are embedded in highperforming organizations. They are the foundation for integrating key performance and operational requirements within a results-oriented

Performance Measurement- A Balanced Score Card Approach

Performance Measurement- A Balanced Score Card Approach Dr. P. D. D. Dominic a, Dr.M.Punniyamoorthy b, Savita K. S. c and Noreen I. A. d a Computer Information Sciences Department Universiti Teknologi

Performance Measurement- A Balanced Score Card Approach Dr. P. D. D. Dominic a, Dr.M.Punniyamoorthy b, Savita K. S. c and Noreen I. A. d a Computer Information Sciences Department Universiti Teknologi

Converting Intangible Assets Into Tangible Outcomes. ROBERT S. KAPLAN and DAVID P. NORTON

STRATEGY MAPS Converting Intangible Assets Into Tangible Outcomes ROBERT S. KAPLAN and DAVID P. NORTON ROBERT KAPLAN is the professor of leadership development at Harvard Business School. He is also chairman

STRATEGY MAPS Converting Intangible Assets Into Tangible Outcomes ROBERT S. KAPLAN and DAVID P. NORTON ROBERT KAPLAN is the professor of leadership development at Harvard Business School. He is also chairman

ICMI PROFESSIONAL CERTIFICATION

ICMI PROFESSIONAL CERTIFICATION Contact Center Management Competencies The ICMI Professional Certification Contact Center Management Competencies specify job role-specific knowledge, skills and abilities

ICMI PROFESSIONAL CERTIFICATION Contact Center Management Competencies The ICMI Professional Certification Contact Center Management Competencies specify job role-specific knowledge, skills and abilities

CHAPTER 2. Theoretical Foundation. Scorecard is a new approach to strategic management. They proposed the concept of a

CHAPTER 2 Theoretical Foundation 2.1 Balanced Scorecard Drs.Robert Kaplan (Harvard Business School) and David Norton has developed Balanced Scorecard (BSC) in the beginning of year 1990s, they explained

CHAPTER 2 Theoretical Foundation 2.1 Balanced Scorecard Drs.Robert Kaplan (Harvard Business School) and David Norton has developed Balanced Scorecard (BSC) in the beginning of year 1990s, they explained

ARTICLE BUILDING HOSPITAL BALANCED SCORECARD BY USING DECISION SUPPORT APPROACH Ufuk Cebeci*

ISSN: 0976-3104 ARTICLE BUILDING HOSPITAL BALANCED SCORECARD BY USING DECISION SUPPORT APPROACH Ufuk Cebeci* Department of Industrial Engineering, Istanbul Technical University, TURKEY ABSTRACT Background:

ISSN: 0976-3104 ARTICLE BUILDING HOSPITAL BALANCED SCORECARD BY USING DECISION SUPPORT APPROACH Ufuk Cebeci* Department of Industrial Engineering, Istanbul Technical University, TURKEY ABSTRACT Background:

Pramoul Nurach. Sairung Inlert

1 2 Pramoul Nurach Sairung Inlert Pramoul Nurach is a Professional Development and Resources Manager of Microsoft Consulting Services. He had completed Bachelor Degree in Computer and Communication Engineering

1 2 Pramoul Nurach Sairung Inlert Pramoul Nurach is a Professional Development and Resources Manager of Microsoft Consulting Services. He had completed Bachelor Degree in Computer and Communication Engineering

Decision Support and Business Intelligence Systems (9 th Ed., Prentice Hall) Chapter 9: Business Performance Management

Chapter 9: Business Performance Management") Decision Support and Business Intelligence Systems (9 th Ed., Prentice Hall) Chapter 9: Business Performance Management Learning Objectives Understand the all-encompassing nature of performance management

Decision Support and Business Intelligence Systems (9 th Ed., Prentice Hall) Chapter 9: Business Performance Management Learning Objectives Understand the all-encompassing nature of performance management

Chapter 1: INTRODUCTION TO STRATEGIC MARKETING. Chapter 11: Strategic Leadership

Chapter 1: INTRODUCTION TO STRATEGIC MARKETING Learning outcomes After reading this chapter you should be able to: Distinguish between the different levels of strategy and marketing Describe what strategic

Chapter 1: INTRODUCTION TO STRATEGIC MARKETING Learning outcomes After reading this chapter you should be able to: Distinguish between the different levels of strategy and marketing Describe what strategic

Focus and Success. Presenter: Amanda Dietz

ENTERPRISE ANALYSIS Strategic t Alignment Drives Project Focus and Success Presenter: Amanda Dietz When Do You Get Involved? 2 During the At the end of the After the project strategic planning strategic

ENTERPRISE ANALYSIS Strategic t Alignment Drives Project Focus and Success Presenter: Amanda Dietz When Do You Get Involved? 2 During the At the end of the After the project strategic planning strategic

A Proposed Framework For Integrating The Balanced Scorecard Into The Strategic Management Process.

A Proposed Framework For Integrating The Balanced Scorecard Into The Strategic Management Process. Nikolaos G. Theriou Efstathios Demitriades Prodromos Chatzoglou 1 Τ.Ε.Ι. of Kavala School of Business

A Proposed Framework For Integrating The Balanced Scorecard Into The Strategic Management Process. Nikolaos G. Theriou Efstathios Demitriades Prodromos Chatzoglou 1 Τ.Ε.Ι. of Kavala School of Business

Performance Management Frameworks A Need for Adaptation (focusing on the Balanced Scorecard).

.") Performance Management Frameworks A Need for Adaptation (focusing on the Balanced Scorecard). Joe Molumby B Comm. C Dip AF, M Sc. (ITA), MIAFA, Examiner for P1 Managerial Finance. Traditionally performance

Performance Management Frameworks A Need for Adaptation (focusing on the Balanced Scorecard). Joe Molumby B Comm. C Dip AF, M Sc. (ITA), MIAFA, Examiner for P1 Managerial Finance. Traditionally performance

This course book preview is provided as an opportunity to see the quality of the course material and to help you determine if the course matches your

This course book preview is provided as an opportunity to see the quality of the course material and to help you determine if the course matches your needs. The preview is provided in a PDF form that cannot

This course book preview is provided as an opportunity to see the quality of the course material and to help you determine if the course matches your needs. The preview is provided in a PDF form that cannot

DESIGNING A BALANCED SCORECARD FOR COOPERATIVES

DESIGNING A BALANCED SCORECARD FOR COOPERATIVES Endang Dhamayantie Faculty of Economics and Business Universitas Tanjungpura, Indonesia edhamayantie@yahoo.com Abstract Cooperative conditions in Indonesia

DESIGNING A BALANCED SCORECARD FOR COOPERATIVES Endang Dhamayantie Faculty of Economics and Business Universitas Tanjungpura, Indonesia edhamayantie@yahoo.com Abstract Cooperative conditions in Indonesia

The Balanced Scorecard: Translating Strategy into Results

The Balanced Scorecard: Translating Strategy into Results By Becky Roberts, President, Catoctin Consulting, LLC (540) 882 3593, broberts@catoctin.com Abstract The balanced scorecard provides managers and

The Balanced Scorecard: Translating Strategy into Results By Becky Roberts, President, Catoctin Consulting, LLC (540) 882 3593, broberts@catoctin.com Abstract The balanced scorecard provides managers and

Performance Management, Balanced Scorecards and Business Intelligence: Alignment for Business Results

Performance Management, Balanced Scorecards and Business Intelligence: Alignment for Business Results Introduction The concept of performance management 1 is not a new one, though modern management constructs

Performance Management, Balanced Scorecards and Business Intelligence: Alignment for Business Results Introduction The concept of performance management 1 is not a new one, though modern management constructs

ERROR! BOOKMARK NOT DEFINED.

TABLE OF CONTENTS LEAD AND LAG INDICATORS... ERROR! BOOKMARK NOT DEFINED. Examples of lead and lag indicators... Error! Bookmark not defined. Lead and Lag Indicators 1 GLOSSARY OF TERMS INTRODUCTION Many

TABLE OF CONTENTS LEAD AND LAG INDICATORS... ERROR! BOOKMARK NOT DEFINED. Examples of lead and lag indicators... Error! Bookmark not defined. Lead and Lag Indicators 1 GLOSSARY OF TERMS INTRODUCTION Many

Strategy in brief. Lecture 1

Strategy in brief Lecture 1 Strategic management ranks as one of the most prominent, influential, and costly stories told in organizations. It is how an organisation takes what happens in the external

Strategy in brief Lecture 1 Strategic management ranks as one of the most prominent, influential, and costly stories told in organizations. It is how an organisation takes what happens in the external

Customer loyalty and customer value Setting targets

Publishing Date: July 1998. 1998. All rights reserved. Copyright rests with the author. No part of this article may be reproduced without written permission from the author. Customer loyalty and customer

Publishing Date: July 1998. 1998. All rights reserved. Copyright rests with the author. No part of this article may be reproduced without written permission from the author. Customer loyalty and customer

Balanced Scorecard. The Four Perspectives of the Balanced Scorecard

STRATEGY Strategy specifies how an organization matches its own capabilities with the opportunities in the marketplace to accomplish its objectives. In formulating its strategy, an organization must focus

STRATEGY Strategy specifies how an organization matches its own capabilities with the opportunities in the marketplace to accomplish its objectives. In formulating its strategy, an organization must focus

Designing the Lean Enterprise Performance Measurement System

Designing the Lean Enterprise Performance Measurement System Vikram Mahidhar web.mit.edu/lean 2005 Massachusetts Institute of Technology Vikram Mahidhar 03/22/05-1 Agenda Metrics Team Challenge from LAI

Designing the Lean Enterprise Performance Measurement System Vikram Mahidhar web.mit.edu/lean 2005 Massachusetts Institute of Technology Vikram Mahidhar 03/22/05-1 Agenda Metrics Team Challenge from LAI

Chapter 8: THE MARKETING PLAN. Chapter 11: Strategic Leadership

Chapter 8: THE MARKETING PLAN Learning outcomes After reading this chapter, you will be able to: Plan segmentation, targeting, and positioning Plan direction, objectives and marketing support Develop marketing

Chapter 8: THE MARKETING PLAN Learning outcomes After reading this chapter, you will be able to: Plan segmentation, targeting, and positioning Plan direction, objectives and marketing support Develop marketing

Content Specification Outline

Content Specification Outline Copyright 2017 Institute of Certified Management Accountants Updated 8/25/17 Institute of Certified Management Accountants Content Specification Outline Certified in Strategy

Content Specification Outline Copyright 2017 Institute of Certified Management Accountants Updated 8/25/17 Institute of Certified Management Accountants Content Specification Outline Certified in Strategy

Evaluating the revolutionary process of performance management based on balanced score cards (BSC)

") Evaluating the revolutionary process of performance management based on balanced score cards (BSC) Dr Hassan Soltani 1, Maryam Mohebbi 2 & Fateme Kowsari 3 Abstract: Contemporary organizations face complicated

Evaluating the revolutionary process of performance management based on balanced score cards (BSC) Dr Hassan Soltani 1, Maryam Mohebbi 2 & Fateme Kowsari 3 Abstract: Contemporary organizations face complicated

The Balanced Scorecard Factsheet 35

The Factsheet 35 You would use this approach to introduce a balanced set of measures covering, Customer, Business Processes and People. You will use these measures as part of a strategic planning tool

The Factsheet 35 You would use this approach to introduce a balanced set of measures covering, Customer, Business Processes and People. You will use these measures as part of a strategic planning tool

The Johns Hopkins Bloomberg School of Public Health Managing Long-Term Care Services for Aging Populations NOTES:

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License. Your use of this material constitutes acceptance of that license and the conditions of use of materials on this

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License. Your use of this material constitutes acceptance of that license and the conditions of use of materials on this

CHAPTER III THE BALANCED SCORECARD APPROACH. 3.3 Strategic management system assumption. 3.5 Applications of the Balanced Scorecard approach

CHAPTER III THE BALANCED SCORECARD APPROACH 3.1 Introduction 3.2 The Balanced Scorecard model 3.2.1 Developing a Balanced Scorecard 3.3 Strategic management system assumption 3.4 The cause-and-effect assumption

CHAPTER III THE BALANCED SCORECARD APPROACH 3.1 Introduction 3.2 The Balanced Scorecard model 3.2.1 Developing a Balanced Scorecard 3.3 Strategic management system assumption 3.4 The cause-and-effect assumption

Make FM Count. TITLE (MAIN) Chris Hodges, P.E., CFM, FRICS, IFMA Fellow. Title (sub) Mark Sekula, CFM, FMP, SFP, IFMA Fellow

Chris Hodges, P.E., CFM, FRICS, IFMA Fellow. Title (sub) Mark Sekula, CFM, FMP, SFP, IFMA Fellow") Make FM Count Mark Sekula, CFM, FMP, SFP, IFMA Fellow TITLE (MAIN) Chris Hodges, P.E., CFM, FRICS, IFMA Fellow Title (sub) The environment facility managers serve is fundamentally changing. It s your role

Make FM Count Mark Sekula, CFM, FMP, SFP, IFMA Fellow TITLE (MAIN) Chris Hodges, P.E., CFM, FRICS, IFMA Fellow Title (sub) The environment facility managers serve is fundamentally changing. It s your role

Managing Strategic Initiatives for Effective Strategy Execution

Managing Strategic Initiatives for Effective Strategy Execution Process 1: Initiative Rationalization A Balanced Scorecard Collaborative White Paper September 2005 Introduction The proper management of

Managing Strategic Initiatives for Effective Strategy Execution Process 1: Initiative Rationalization A Balanced Scorecard Collaborative White Paper September 2005 Introduction The proper management of

Chapter 2 Lecture Notes Strategic Marketing Planning. Chapter 2: Strategic Marketing Planning

Chapter 2: I. Introduction A. Beyond the Pages 2.1 discusses several aspects of Ford s strategy to restructure its operating philosophy. B. Although the process of strategic marketing planning can be complex

Chapter 2: I. Introduction A. Beyond the Pages 2.1 discusses several aspects of Ford s strategy to restructure its operating philosophy. B. Although the process of strategic marketing planning can be complex

White paper Balanced Scorecard (BSC) Draft Date: July 02, 2012

Draft Date: July 02, 2012") White paper Balanced Scorecard (BSC) Draft Date: July 02, 2012 Whitepaper ISM Balanced Scorecard (BSC) Ganesh Iyer, JMD Draft Date: July 02, 2012 1. Introduction 2 2. What is BSC? 2 3. Steps to implement

White paper Balanced Scorecard (BSC) Draft Date: July 02, 2012 Whitepaper ISM Balanced Scorecard (BSC) Ganesh Iyer, JMD Draft Date: July 02, 2012 1. Introduction 2 2. What is BSC? 2 3. Steps to implement

4 The balanced scorecard

SUPPLEMENT TO THE APRIL 2009 EDITION Three topics that appeared in the 2007 syllabus have been removed from the revised syllabus examinable from November 2009. If you have the April 2009 edition of the

SUPPLEMENT TO THE APRIL 2009 EDITION Three topics that appeared in the 2007 syllabus have been removed from the revised syllabus examinable from November 2009. If you have the April 2009 edition of the

Introduction to the Balanced Scorecard

Introduction to the Balanced Scorecard This section of Successful Planning provides an introduction to the use of strategic marketing planning, so that you can consider if it is the right approach for

Introduction to the Balanced Scorecard This section of Successful Planning provides an introduction to the use of strategic marketing planning, so that you can consider if it is the right approach for

THE ROLE OF PERFORMANCE MEASUREMENT SYSTEMS ON GLOBALIZED MARKETS

DAAAM INTERNATIONAL SCIENTIFIC BOOK 2010 pp. 313-320 CHAPTER 30 THE ROLE OF PERFORMANCE MEASUREMENT SYSTEMS ON GLOBALIZED MARKETS BILAS, V. & FRANC, S. Abstract: There is a continuous evolution of performance

DAAAM INTERNATIONAL SCIENTIFIC BOOK 2010 pp. 313-320 CHAPTER 30 THE ROLE OF PERFORMANCE MEASUREMENT SYSTEMS ON GLOBALIZED MARKETS BILAS, V. & FRANC, S. Abstract: There is a continuous evolution of performance

Balanced Scorecard and Its Iterations

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 18, Issue 12. Ver. II (December. 2016), PP 78-82 www.iosrjournals.org Balanced Scorecard and Its Iterations

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 18, Issue 12. Ver. II (December. 2016), PP 78-82 www.iosrjournals.org Balanced Scorecard and Its Iterations

CHAPTER 2 STRATEGY AND HUMAN RESOURCES PLANNING

CHAPTER 2 STRATEGY AND HUMAN RESOURCES PLANNING TRUE/FALSE 1. Organizations set major objectives and develop comprehensive plans to achieve those objectives through strategic planning. ANS: T PTS: 1 REF:

CHAPTER 2 STRATEGY AND HUMAN RESOURCES PLANNING TRUE/FALSE 1. Organizations set major objectives and develop comprehensive plans to achieve those objectives through strategic planning. ANS: T PTS: 1 REF:

F.Burstein 1. The KMS Road Map. Evaluation Principle. Knowledge Management

IMS3012 Knowledge Management Lecture The Value Proposition of KM Dr. Henry Linger Lecture 11 IMS3012 - Semester 2, 2005 1 The KMS Road Map The first phase: evaluation of the infrastructure and aligning

IMS3012 Knowledge Management Lecture The Value Proposition of KM Dr. Henry Linger Lecture 11 IMS3012 - Semester 2, 2005 1 The KMS Road Map The first phase: evaluation of the infrastructure and aligning

Continuous Profit Improvement

Continuous Profit Improvement Using Balanced Scorecard Analysis Modern business benchmarking was conceived by IBM, Hewlett Packard, Hershey and other major corporations in the early 1980s as each company

Continuous Profit Improvement Using Balanced Scorecard Analysis Modern business benchmarking was conceived by IBM, Hewlett Packard, Hershey and other major corporations in the early 1980s as each company

Measuring Performance Systems and Structures to drive improvement

Measuring Performance Systems and Structures to drive improvement 2 Workshop Objectives Understand the principles of performance management Learn how to develop performance measures Understand the tools

Measuring Performance Systems and Structures to drive improvement 2 Workshop Objectives Understand the principles of performance management Learn how to develop performance measures Understand the tools

Six Sigma Black Belt Study Guides

Six Sigma Black Belt Study Guides 1 www.pmtutor.org Powered by POeT Solvers Limited. Introduction to Six Sigma Business Performance Measures 2 www.pmtutor.org Powered by POeT Solvers Limited. Index Introduction

Six Sigma Black Belt Study Guides 1 www.pmtutor.org Powered by POeT Solvers Limited. Introduction to Six Sigma Business Performance Measures 2 www.pmtutor.org Powered by POeT Solvers Limited. Index Introduction

Strategy Maps and the Balanced Scorecard. Don Breckenridge Jr. President

Strategy Maps and the Balanced Scorecard Don Breckenridge Jr. President The Typical Owner Owners are typically the Rainmakers Rainmakers tend to work FOR the business instead of ON the business. Most don

Strategy Maps and the Balanced Scorecard Don Breckenridge Jr. President The Typical Owner Owners are typically the Rainmakers Rainmakers tend to work FOR the business instead of ON the business. Most don

Get Better Business Results

Get Better Business Results From the Four Stages of Your Customer Lifecycle Stage 4 Retain How to Retain Your Profitable Customers A white paper from Build in Retention and Profitability at Each Stage

Get Better Business Results From the Four Stages of Your Customer Lifecycle Stage 4 Retain How to Retain Your Profitable Customers A white paper from Build in Retention and Profitability at Each Stage

Get Better Business Results

Get Better Business Results From the Four Stages of Your Customer Lifecycle Stage 4 Retain How to Retain Your Profitable Customers A white paper from Build in Retention and Profitability at Each Stage

Get Better Business Results From the Four Stages of Your Customer Lifecycle Stage 4 Retain How to Retain Your Profitable Customers A white paper from Build in Retention and Profitability at Each Stage

How it works: Questions from the OCAT 2.0

Social Sector Practice How it works: Questions from the OCAT 2.0 OCAT 2.0 is an updated and improved version of our original OCAT survey. It asks nonprofit staff to rate their organization s operational

Social Sector Practice How it works: Questions from the OCAT 2.0 OCAT 2.0 is an updated and improved version of our original OCAT survey. It asks nonprofit staff to rate their organization s operational

An Introduction to Strategic Planning for Service Organizations

A Jolt Consulting Group White Paper An Introduction to Strategic Planning for Service Organizations April 2011 PO BOX 1217, SARATOGA SPRINGS, NY 12866 PAGE 1 of 9 Table of Contents Strategic Planning Challenges...

A Jolt Consulting Group White Paper An Introduction to Strategic Planning for Service Organizations April 2011 PO BOX 1217, SARATOGA SPRINGS, NY 12866 PAGE 1 of 9 Table of Contents Strategic Planning Challenges...

Building a Government Balanced Scorecard. Phase 1 - Planning

Building a Government Balanced Scorecard Phase 1 - Planning Paul Arveson The Balanced Scorecard Institute March 2003 2003 Balanced Scorecard Institute 1 Example of a Government Balanced Scorecard Implementation

Building a Government Balanced Scorecard Phase 1 - Planning Paul Arveson The Balanced Scorecard Institute March 2003 2003 Balanced Scorecard Institute 1 Example of a Government Balanced Scorecard Implementation

Development of Performance Model: A New Measurement Framework for Non-Profit Organization

Available at www.ictom.info www.sbm.itb.ac.id www.cob.uum.edu.my The 3rd International Conference on Technology and Operations Management Sustaining Competitiveness through Green Technology Management

Available at www.ictom.info www.sbm.itb.ac.id www.cob.uum.edu.my The 3rd International Conference on Technology and Operations Management Sustaining Competitiveness through Green Technology Management

The Talent Advantage: How to Develop Your Strategy to Accelerate Business Results By Nancy MacKay, PhD

Adapted from the forthcoming book: The Talent Advantage by coauthors Dr. Alan Weiss and Dr. Nancy MacKay, published by Wiley. A. Definition of Strategy: What will you do to achieve your agreed-upon 3-year

Adapted from the forthcoming book: The Talent Advantage by coauthors Dr. Alan Weiss and Dr. Nancy MacKay, published by Wiley. A. Definition of Strategy: What will you do to achieve your agreed-upon 3-year

Welcome Strategy Leader!

Essentials Guide to Strategic Planning Welcome Strategy Leader! To help close the gap between strategy and execution, we ve created the Essentials Guide to Strategic Planning, which provides an end-to-end

Essentials Guide to Strategic Planning Welcome Strategy Leader! To help close the gap between strategy and execution, we ve created the Essentials Guide to Strategic Planning, which provides an end-to-end

International Balanced Scorecard

BALANCED SCORECARD INSTITUTE EMEA THE STRATEGY EXECUTION COMPANY International Balanced Scorecard Certi cation Master Class How to create and Sustain High Performance using the balanced scorecard institute

BALANCED SCORECARD INSTITUTE EMEA THE STRATEGY EXECUTION COMPANY International Balanced Scorecard Certi cation Master Class How to create and Sustain High Performance using the balanced scorecard institute

Information and Communications Technology (ICT) Strategy Consulting

Strategy Consulting") Information and Communications Technology (ICT) Strategy Consulting Consulting End-to-end ICT consulting services Looking to effectively model your business processes using ICT? You need consulting services

Information and Communications Technology (ICT) Strategy Consulting Consulting End-to-end ICT consulting services Looking to effectively model your business processes using ICT? You need consulting services

International Conference on Information Systems for Business Competitiveness (ICISBC 2013) 332

332") International Conference on Information Systems for Business Competitiveness (ICISBC 2013) 332 Business Performance Management On New Sofware Implementation Of Information Technology Project Using Balance

International Conference on Information Systems for Business Competitiveness (ICISBC 2013) 332 Business Performance Management On New Sofware Implementation Of Information Technology Project Using Balance

The 10th INternational Conference on Software Process Improvement Research into Education and training, INSPIRE 2005, March 2005,

Key Performance Indicators for Quality Assurance in Higher Education the Case of the Department of Informatics at the Technological Educational Institute of Thessaloniki, Greece Kerstin V. Siakas, Aristea-Alexandra

Key Performance Indicators for Quality Assurance in Higher Education the Case of the Department of Informatics at the Technological Educational Institute of Thessaloniki, Greece Kerstin V. Siakas, Aristea-Alexandra

VISION. Vision. e.g. DRB-HICOM Vision: To Be No.1 And Continuously Excel In All That We Do. Manufacturing & Engineering Division

Manufacturing & Engineering Division Vision A concise statement that defines the mid to long-term goals (3-10 years) of the organization. The vision should be external & market oriented and should be expressed

Manufacturing & Engineering Division Vision A concise statement that defines the mid to long-term goals (3-10 years) of the organization. The vision should be external & market oriented and should be expressed

Results & Key Findings. Non-Profit Board of Directors Assessment. Sample fax

Results & Key Findings Sample Non-Profit Assessment 310.652.5678 fax 310.652.5677 www.profitablesolutions.com TABLE OF CONTENTS OVERVIEW..... METHODOLOGY ii iii EXECUTIVE SUMMARY Degree of Impact Results........

Results & Key Findings Sample Non-Profit Assessment 310.652.5678 fax 310.652.5677 www.profitablesolutions.com TABLE OF CONTENTS OVERVIEW..... METHODOLOGY ii iii EXECUTIVE SUMMARY Degree of Impact Results........

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK Dr. Ashok Kumar Gupta 1, Mrs. Sudarshana Sharma 2 1 Lecturer (ABST), Govt. Commerce College, Kota (Raj.) 2 Research Scholar, Govt. Commerce College Kota, University

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK Dr. Ashok Kumar Gupta 1, Mrs. Sudarshana Sharma 2 1 Lecturer (ABST), Govt. Commerce College, Kota (Raj.) 2 Research Scholar, Govt. Commerce College Kota, University

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK Dr. Ashok Kumar Gupta 1, Mrs. Sudarshana Sharma 2 1 Lecturer (ABST), Govt. Commerce College, Kota (Raj.) 2 Research Scholar, Govt. Commerce College Kota, University

BALANCED SCORECARD: A CONCEPTUAL FRAMEWORK Dr. Ashok Kumar Gupta 1, Mrs. Sudarshana Sharma 2 1 Lecturer (ABST), Govt. Commerce College, Kota (Raj.) 2 Research Scholar, Govt. Commerce College Kota, University

Creating a Customer Centric Organization

RESEARCH BRIEF Creating a Customer Centric Organization The Key Drivers of Customer Loyalty Bill Kowalski Integrity Solutions The Sales Management Association +1 312 278-3356 www.salesmanagement.org 2009

RESEARCH BRIEF Creating a Customer Centric Organization The Key Drivers of Customer Loyalty Bill Kowalski Integrity Solutions The Sales Management Association +1 312 278-3356 www.salesmanagement.org 2009

Business Plan

Business Plan 2017-2018 rev. May 2017 MESSAGE FROM THE CEO As the Chief Executive Officer of PEC, I am pleased to present the 2017 2018 Business Plan, a tool that will enable the Cooperative to make informed

Business Plan 2017-2018 rev. May 2017 MESSAGE FROM THE CEO As the Chief Executive Officer of PEC, I am pleased to present the 2017 2018 Business Plan, a tool that will enable the Cooperative to make informed

Performance Measurement Systems

Performance Measurement Systems This package has been created as a practical guide to developing performance measurements in any industry. It has been divided into the following 6 sections: 1. Introduction

Performance Measurement Systems This package has been created as a practical guide to developing performance measurements in any industry. It has been divided into the following 6 sections: 1. Introduction

The Balanced Scorecard

The Balanced Scorecard Translating Strategy Into Action Robert S. Kaplan David P. Norton Learning Objectives After successfully completing this lesson, you will be able to: 1. Explain the concept of balanced

The Balanced Scorecard Translating Strategy Into Action Robert S. Kaplan David P. Norton Learning Objectives After successfully completing this lesson, you will be able to: 1. Explain the concept of balanced

BANGLADESH COST ACCOUNTING STANDARDS BCAS Performance Measurement

BANGLADESH COST ACCOUNTING STANDARDS BCAS - 17 Performance Measurement 17.1 Introduction BACS 17: Performance Measurement Performance measurement is an important tool of strategic analysis. It is the process

BANGLADESH COST ACCOUNTING STANDARDS BCAS - 17 Performance Measurement 17.1 Introduction BACS 17: Performance Measurement Performance measurement is an important tool of strategic analysis. It is the process

Reading F: Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part II by Robert S. Kaplan and David P.

Reading F: Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part II by Robert S. Kaplan and David P. Norton In a previous paper (Kaplan and Norton 2001b), we described

Reading F: Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part II by Robert S. Kaplan and David P. Norton In a previous paper (Kaplan and Norton 2001b), we described

Aligning Strategic and Project Measurement Systems

Essay Often the technical and business sectors of IT organizations work in opposition, toward different goals and objectives. The authors propose a method that integrates strategic and project measurement