The IRS Form 990: A Tool for Understanding Organizational Capacity. Hilda Polanco, CPA, CCSA, CGMA Founder and CEO, FMA

|

|

|

- May Farmer

- 6 years ago

- Views:

Transcription

1 The IRS Form 990: A Tool for Understanding Organizational Capacity Hilda Polanco, CPA, CCSA, CGMA Founder and CEO, FMA March 30, 2016

2 Welcome and Introduction IRS Form 990: Background Summary & Program Service Accomplishments Governance & Leadership Operating Reserves & Other Key Financial Indicators Public Support & Fundraising Other Areas of Note 2

3 What do you think of when you think about organizational capacity? 3

4 Critical Questions What are the organization s programmatic activities? How strong is the organization s governance function. What does it say about leadership? What does the 990 tell us about fundraising activities and the level of public support? 4

5 Three Key Questions About Financial Health 1. How strong are the organization s reserves? How liquid are they? 2. How many months of operations can be covered with available cash? 3. What are the trends in operating results? Surpluses or deficits? How is the organization investing its resources? 5

6

7

8

9 THE IRS FORM 990: BACKGROUND

10 What is it? Information return for organizations exempt from income tax Provides the IRS and state charity agencies with information to assist them in enforcing the laws governing nonprofits The most publicly available document about an organization 10

11 What Are the Filing Requirements? Annual gross revenue of $50K or less: 990-N (E-postcard) Annual gross revenue of $200K or less and total assets of less than $500K: 990-EZ or 990 Gross revenue greater than $200K, or total assets of $500K or more: 990 Extensions on the due date: organizations may request an automatic 3-month extension without showing cause; another 3- month extension may be requested where reasonable cause is explained 11

12 How is Data in the 990 Different from the Audit? Form 990 does not provide detail about donor-imposed restrictions on revenue Does not show board designated net assets In-kind donations of services are not recognized in the 990 Sales of merchandise, special events, and rental activities are shown on the 990 net of expenses Audits conform to Generally Accepted Accounting Principles (GAAP), which is not required of data in the 990 Source GuideStar: Retrieved from: 12

13 SUMMARY & PROGRAM SERVICE ACCOMPLISHMENTS

14 Front Page: Part I, Summary

15 Front Page: Part I, Summary (continued) Key Question: How long after the end of the fiscal year was the organization s 990 filed? 15

16 Schedule O 16

17 Part III: Statement of Program Service Accomplishments

18 Every organization can update its profile on Guidestar.org Different seals awarded based on level of information shared: Bronze, Sliver, or Gold Organizations can answer 5 charting impact questions: What is your organization aiming to accomplish? What are your strategies for making this happen? What are your organization's capabilities for doing this? How will your organization know if you are making progress? What have and haven't you accomplished so far? 18

19 GOVERNANCE & LEADERSHIP

20 Part VI, Section A: Governing Body and Management Use of management company Changes to organizational documents Documentation of board and committee meetings Presentation of 990 to board List of officers, directors, trustee or key employees Did the org become aware of a significant diversion of assets? Key Questions: How many board members? Are they reviewing the 990? Is there an unusual management structure? 20

21 Part VI, Section A: Governing Body and Management

22 Part VI, Section B: Policies Conflict of Interest Monitoring and enforcement of conflict of interest policy Whistle Blower Policy Document retention and destruction Key Questions: Does the organization have appropriate governance policies in place to set the right tone at the top? 22

23 Part VI, Section B: Policies

24 Part VI, Section C: Disclosure States in which 990 is filed How key documents are made public Key Questions: How wide is this organization casting its fundraising net? How committed to transparency are they? 24

25 Part VI, Section C: Disclosure

26 Part VI, Section B: Policies Process for determining compensation. Process should include: A review and approval by independent persons Comparability data Contemporaneous substantiation of the deliberation and decision Key Question: Is there a deliberate, fair, comprehensive process to set compensation for leadership? 26

27 Part VI, Section B: Policies

28 Part VII, Section A Highest compensated employees (paid $100,000 or more) Current and past officers, key employees, directors, and trustees receiving more than in $100,000 in compensation Key Questions: Does compensation seem reasonable? Are there significant pay disparities between employees? Are any board members being paid? 28

29 Part VII: Compensation

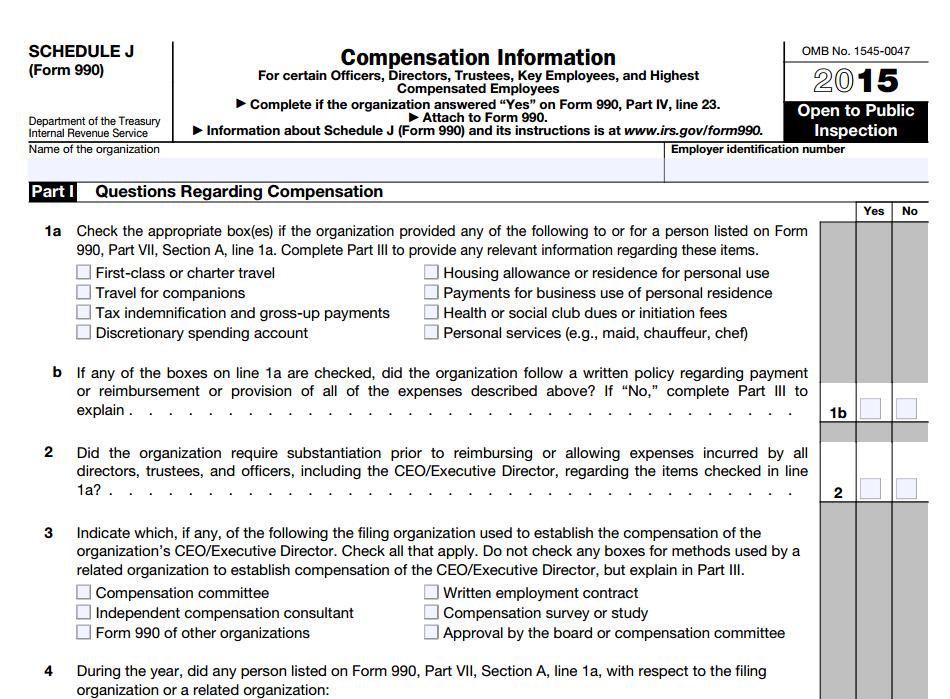

30 Schedule J Provides additional information on compensation practices for officers, directors, trustees and key employees Key Questions: Did the organization pay for first class or charter travel? Was there access to discretionary spending accounts? Did the organization pay for business use of a personal residence? Were personal services (e.g. maid, chauffeur, etc.) provided? 30

31

32 Three Key Questions About Financial Health 1. How strong are the organization s reserves? How liquid are they? 2. How many months of operations can be covered with available cash? 3. What are the trends in operating results? Surpluses or deficits? How is the organization investing its resources? 32

33 OPERATING RESERVES & LIQUIDITY

34 Why do organizations need operating reserves? Unexpected shortfall in revenue Unexpected demands on resources Unanticipated opportunities Inevitable instances of less than perfect judgment and foresight The need for a change in direction Normal day-to-day fluctuations in income and expenses and associated cash flows Source: Operating Reserve Policy Toolkit for Nonprofit Organizations, sponsored by the National Center for Charitable Statistics, Center on Nonprofit and Philanthropy at the Urban Institute, and United Way Worldwide 34

35 What We Own: Cash What We Owe: Bills due Receivables Investments Property, Plant & Equipment, net Assets = Liabilities + Net Assets Line of Credit Deferred Revenue Long-term Debt Our Available Capital Unrestricted Board Designated Fixed Assets Other Temp. Restricted Perm. Restricted

36 Audit: Statement of Financial Position 990: Balance Sheet (Part X)

37 37

38 IRS Form 990: Balance Sheet 38

39 IRS Form 990: Balance Sheet (continued) 39

Temp.")

40 Accessibility LUNA / Working Capital Short-term Liquid Capital Debt Repayment Facility Reserve Growth & Innovation Longer-term Reserves (may be board designated) Temp. Restricted Net Assets* Endowment** Donor restricted capital *To be accessed only if delivering on donor expectations **Only earnings are accessible

41 Liquid Unrestricted Net Assets (LUNA) The portion of unrestricted net assets that could be converted to cash relatively easily (may or may not include board designated funds, based on accessibility) Funds available for purposes such as supplying working capital, guarding against downturns, and pursuing new opportunities LUNA = Unrestricted Net Assets (Fixed Assets Mortgages) Benchmark: LUNA sufficient to cover 3-6 months of operating expenses is generally consideredd healthy, but this depends on an organization s business model, plans, and goals. 41

42 Using the Form 990: Liquid Unrestricted Net Assets (LUNA) Calculation using the 990 Location in 990 Unrestricted Net Assets, End of Year Part X, column (B), line 27 Net Fixed Assets Part X, column (B), line 10c + Mortgages Part X, column (B), line 23 Total LUNA (Total Expenses 12) Part IX, column (A), line 25 Months of LUNA 42

43 43

44 Calculating LUNA: Example

45 Months of Cash on Hand Calculation using the 990 Location in 990 Cash, non-interest bearing Part X, column (B), line 1 + Savings and temp. cash investments Part X, column (B), line 2 Total Cash and Equivalents (Total Expenses 12) Part IX, column (A), line 25 Months of Cash on Hand 45

46 OTHER KEY FINANCIAL INDICATORS

47 Three Key Questions About Financial Health 1. How strong are the organization s reserves? How liquid are they? 2. How many months of operations can be covered with available cash? 3. What are the trends in operating results? Surpluses or deficits? How is the organization investing its resources? 47

48 Audit: Statement of Activities 990: Stmt of Revenues (Part VIII) 990: Stmt of Expenses (Part IX)

49 Two columns

50 Front Page: Part I, Revenue and Expense Only one column 50

51 Calculating Operating Results Calculation using the 990 Location in 990 Unrestricted Net Assets, End of Year Part X, column (B), line 27 Unrestricted Net Assets, Beginning of Year Part X, column (A), line 27 Change in Unrestricted Net Assets* *Represents operating surplus or deficit for the year 51

52 Calculating Operating Results Calculation using the 990 Location in 990 5,159,362 Part X, column (B), line ,081 Part X, column (A), line 27 $4,395,281 52

53 Audit: Statement of Functional Expenses 990: Stmt of Functional Expenses (Part IX)

54 54

55 Part IX: Statement of Functional Expenses Are expenses spread across all three columns? 55

56 Functional Expense Composition Calculation using the 990 Location in 990 Total Program Expense Total Expense Part IX, column (B), line 25 Part IX, column (A), line 25 Total Management & General Expense Total Expense Total Fundraising Expense Part IX, column (C), line 25 Part IX, column (A), line 25 Part IX, column (D), line 25 Total Expense 56 Part IX, column (A), line 25

57 Part IX: Statement of Functional Expenses

58 PUBLIC SUPPORT & FUNDRAISING

59 Public Support Test and Tipping Tipping: Occurs when a donor makes so large a grant that the grantee fails the IRS public support test and is tipped out of public charity status into private foundation status. Public Support Test: charities must prove that they receive at least onethird of their total support in contributions from the general public. Key Questions: Is the organization over-reliant on one funder? If so, what risks may that pose? 59

60 Schedule A: Public Charity Status and Public Support

61 Key Questions on Fundraising Part I: Types of fundraising activities conducted; engagement of outside contractors for fundraising Part II: Financial return on special events Key Questions: Who is doing fundraising for this organization? How are they doing on special events? 61

62 Schedule G: Fundraising Activities

63 Schedule G: Fundraising Activities (continued)

64 OTHER AREAS OF NOTE

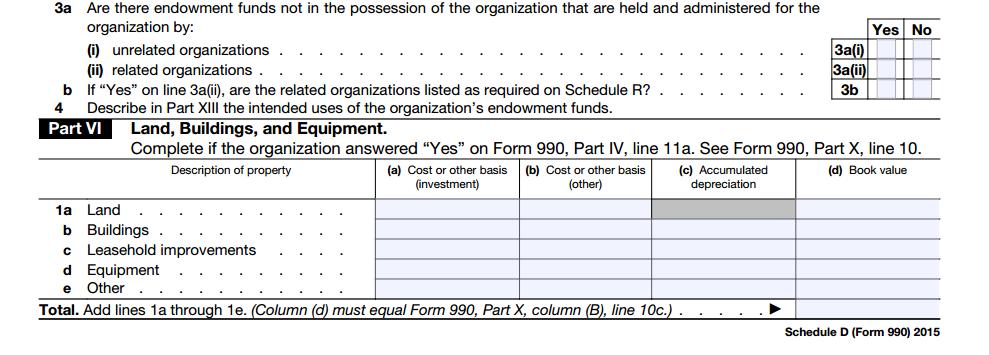

65 Schedule D: Depreciation of Fixed Assets Shows depreciation of fixed assets by category: land, buildings, leasehold improvements, and equipment Key Questions: How depreciated are the organization s buildings and equipment? If highly depreciated (over 80%), are there reserves to fund replacement/repair? 65

66

67 Some Additional Questions to Consider: Part IV, Question 26: Did the organization take out a loan from a board member? (if so, more info will be provided in Schedule L) Part IV, Question 32: Did the organization sell or transfer more than 25% of its net assets (if so, more info will be provided in Schedule N) Part XII, Question 2c: Does the organization have a board committee that oversees the audit process? 67

68 RESOURCES

69 The Key to Long Term Financial Health Liquid Unrestricted Net Assets (LUNA), Hilda Polanco, New York Nonprofit Press, May 2012: term-financial-health-liquid-unrestricted-net-assets-luna- Maintaining Nonprofit Operating Reserves: A Whitepaper, by the Nonprofit Operating Reserves Initiative Workgroup, December Public Support Test: What is Tipping? Rasmuson Foundation: IRS Form 990: Overview and Resources, Independent Sector: Management/Pages/Resource-Center-for-Good-Governance-and-Ethical- Practice.aspx 69

70 Excel Tool (for Audits) Coming in April: Online Tutorial 70

71 StrongNonprofits.org In collaboration with the Wallace Foundation, FMA has created a library of tools and resources to help organizations become fiscally fit Four Topic Areas: Planning Monitoring Operations Governance 71

72 Online Tutorials for StrongNonprofits.org FMA offers complimentary orientation one-hour webinars that feature an overview of the website and drill down on several of its key resources Upcoming webinar dates: April 20th at 3:00pm June 2nd at 2:00pm To register, or see upcoming webinar dates: For a 15-minute, on-demand webinar tour of the site: 72

73 QUESTIONS?

74 Established in 1999 to serve not-for-profit organizations around the country Provides customized financial management, accounting, software, organizational development, human resources, and other consulting services Works directly with organizations or through funder-supported management assistance programs FMA's mission is to empower not-for-profit organizations with the knowledge and skills to successfully serve their constituents and fulfill their missions Hilda Polanco, CPA, CCSA, CGMA New York Chicago Oakland LA /FiscalManagementAssociates linkedin.com/company/fiscal-managementassociates-llc

How to Build a Dashboard for your Nonprofit: A Critical 1 Strategic Tool Reveals Itself

How to Build a Dashboard for your Nonprofit: A Critical 1 Strategic Tool Reveals Itself A conversation with: Hilda Polanco, FMA Christa Gannon, Fresh Lifelines for Youth Jenny Ocon, UpValley Family Centers

How to Build a Dashboard for your Nonprofit: A Critical 1 Strategic Tool Reveals Itself A conversation with: Hilda Polanco, FMA Christa Gannon, Fresh Lifelines for Youth Jenny Ocon, UpValley Family Centers

Session 3: Financial Monitoring

Session 3: Financial Monitoring Financial Management Training Program Hilda Polanco, CPA, CCSA, CGMA, Founder and CEO Gretchen Upholt, MPA, Consultant November 3, 2016 Reflections on Session 2 2 1 As a

Session 3: Financial Monitoring Financial Management Training Program Hilda Polanco, CPA, CCSA, CGMA, Founder and CEO Gretchen Upholt, MPA, Consultant November 3, 2016 Reflections on Session 2 2 1 As a

Session 4: Operational Excellence

Session 4: Operational Excellence Financial Management Training Program Hilda Polanco, CPA, CCSA, CGMA, Founder and CEO Gretchen Upholt, MPA, Consultant December 8, 2016 Reflections on Session 3 2 1 As

Session 4: Operational Excellence Financial Management Training Program Hilda Polanco, CPA, CCSA, CGMA, Founder and CEO Gretchen Upholt, MPA, Consultant December 8, 2016 Reflections on Session 3 2 1 As

Operational Excellence

Operational Excellence City & County of San Francisco Rebecca Coker, Lead Consultant, FMA Roxanne Hanson, Consultant, FMA May 22, 2017 GOVERNANCE PLANNING People People OPERATIONS Technology Process y

Operational Excellence City & County of San Francisco Rebecca Coker, Lead Consultant, FMA Roxanne Hanson, Consultant, FMA May 22, 2017 GOVERNANCE PLANNING People People OPERATIONS Technology Process y

Prepare Now for the New Form 990

Prepare Now for the New Form 990 GUIDING PRINCIPLES Enhancing Transparency Realistic picture of Organization for IRS Stakeholders Promoting Tax Compliance assist IRS in assessing risk of noncompliance

Prepare Now for the New Form 990 GUIDING PRINCIPLES Enhancing Transparency Realistic picture of Organization for IRS Stakeholders Promoting Tax Compliance assist IRS in assessing risk of noncompliance

Above all, a nonprofit board member should understand these four IRS Form 990 concepts:

kit The IRS Form 990 an annual required tax filing highlights a nonprofit s mission and compliance with federal regulations. It is your most public document, available online and viewed by potential donors.

kit The IRS Form 990 an annual required tax filing highlights a nonprofit s mission and compliance with federal regulations. It is your most public document, available online and viewed by potential donors.

Assessing Financial Health: A Donor s Perspective

Assessing Financial Health: A Donor s Perspective Bruce Blasnik, CPA Partner bblasnik@odpkf.com 203 323 2400 323 2400 x5004 860 257 1870 x 5004 Where will they look for info? Information *NEW* Financial

Assessing Financial Health: A Donor s Perspective Bruce Blasnik, CPA Partner bblasnik@odpkf.com 203 323 2400 323 2400 x5004 860 257 1870 x 5004 Where will they look for info? Information *NEW* Financial

Top 5 Must Do s for Reviewing Form 990. Presented By Joe Byrne, Senior Tax Manager October 25, 2017

Top 5 Must Do s for Reviewing Form 990 Presented By Joe Byrne, Senior Tax Manager October 25, 2017 Agenda 1 FORM 990 OVERVIEW What s a 990? What Should We File? Schedules, Schedules, and More Schedules!

Top 5 Must Do s for Reviewing Form 990 Presented By Joe Byrne, Senior Tax Manager October 25, 2017 Agenda 1 FORM 990 OVERVIEW What s a 990? What Should We File? Schedules, Schedules, and More Schedules!

PO Box Washington, DC

www.nonprofithealthcare.org PO Box 41015 Washington, DC 20018 877-299-6497 Alliance Comments and Recommendations on the Independent Sector Nonprofit Panel s Proposed Principles of Effective Practice for

www.nonprofithealthcare.org PO Box 41015 Washington, DC 20018 877-299-6497 Alliance Comments and Recommendations on the Independent Sector Nonprofit Panel s Proposed Principles of Effective Practice for

Prepared: October Presentation prepared by: YOUR PART-TIME CONTROLLER, LLC Washington Philadelphia New York City

Prepared: October 2013 Presentation prepared by: YOUR PART-TIME CONTROLLER, LLC Washington Philadelphia New York City The time has passed when donors invest or make contributions because it s the right

Prepared: October 2013 Presentation prepared by: YOUR PART-TIME CONTROLLER, LLC Washington Philadelphia New York City The time has passed when donors invest or make contributions because it s the right

Standards for Excellence Program Organizational Self-Assessment Checklist

Standards for Excellence Program Organizational Self-Assessment Checklist Instructions for using the checklist: if the organization has met the standard, X if the organization has not met the standard,

Standards for Excellence Program Organizational Self-Assessment Checklist Instructions for using the checklist: if the organization has met the standard, X if the organization has not met the standard,

Nine Questions Every Non-Profit Should Ask Themselves

Nine Questions Every Non-Profit Should Ask Themselves Nine Questions Every Non-Profit Should Ask Themselves Starting a non-profit organization or reviewing a current organization can prove to be an exciting

Nine Questions Every Non-Profit Should Ask Themselves Nine Questions Every Non-Profit Should Ask Themselves Starting a non-profit organization or reviewing a current organization can prove to be an exciting

Standards of Excellence Certification Program Voluntary Health Agency Survey Revised 3/11

Revised 3/11 Name: E-mail Address: Telephone Number: _ Voluntary Health Agency: ABOUT YOUR ORGANIZATION 1. Does the organization have an affiliate structure? (If no, skip to question 9) 2. What type of

Revised 3/11 Name: E-mail Address: Telephone Number: _ Voluntary Health Agency: ABOUT YOUR ORGANIZATION 1. Does the organization have an affiliate structure? (If no, skip to question 9) 2. What type of

Return of Organization Exempt From Income Tax

990 Return of Organization Exempt From Income Tax OMB 1545-0047 Form Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust or private

990 Return of Organization Exempt From Income Tax OMB 1545-0047 Form Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust or private

BOARD SERVICE POLICY AND GUIDELINES

BOARD SERVICE POLICY AND GUIDELINES Table of Contents... 1 Policy... 2 Guidelines... 3 1. Introduction and Purpose... 3 2. Foundation-Sponsorship of Employees to Serve in Governance Roles... 3 2.1 Approved

BOARD SERVICE POLICY AND GUIDELINES Table of Contents... 1 Policy... 2 Guidelines... 3 1. Introduction and Purpose... 3 2. Foundation-Sponsorship of Employees to Serve in Governance Roles... 3 2.1 Approved

7/27/2011. What are the Drivers to Governance? Governance

What are the Drivers to Governance? Susan M. Kirsch Shareholder, Tax Advisors This advice is not intended or written to be used for, and it cannot be used for, the purpose of avoiding any federal tax penalties

What are the Drivers to Governance? Susan M. Kirsch Shareholder, Tax Advisors This advice is not intended or written to be used for, and it cannot be used for, the purpose of avoiding any federal tax penalties

The Guide to Not-for-Profit Governance 2012

The Guide to Not-for-Profit Governance 2012 Sponsored by the Not-for-Profit Practice Group and the Pro Bono Committee of Weil, Gotshal & Manges LLP The Guide to Not-for-Profit Governance 2012 Title Not-for-Profit

The Guide to Not-for-Profit Governance 2012 Sponsored by the Not-for-Profit Practice Group and the Pro Bono Committee of Weil, Gotshal & Manges LLP The Guide to Not-for-Profit Governance 2012 Title Not-for-Profit

West Virginia Nonprofit Association

West Virginia Nonprofit Association 2015 WVNPA P.O. Box 1452 Lewisburg, WV 24901 304-667-2248 www.wvnpa.org West Virginia Principles & Practices for Nonprofit Excellence Introduction West Virginia s nonprofit

West Virginia Nonprofit Association 2015 WVNPA P.O. Box 1452 Lewisburg, WV 24901 304-667-2248 www.wvnpa.org West Virginia Principles & Practices for Nonprofit Excellence Introduction West Virginia s nonprofit

Standards of Excellence Certification Program for Voluntary Health Agencies January 2017

Standards of Excellence Certification Program for Voluntary Health Agencies Page 1 of 7 Standards of Excellence Certification Program for Voluntary Health Agencies January 2017 Standards of Excellence

Standards of Excellence Certification Program for Voluntary Health Agencies Page 1 of 7 Standards of Excellence Certification Program for Voluntary Health Agencies January 2017 Standards of Excellence

Fiduciary Duty of Board of Directors to Oversee Financial Affairs

Fiduciary Duty of Board of Directors to Oversee Financial Affairs 1. Need for Financial Oversight Corporate governance has been an important issue on the national agenda since the Enron scandal, which

Fiduciary Duty of Board of Directors to Oversee Financial Affairs 1. Need for Financial Oversight Corporate governance has been an important issue on the national agenda since the Enron scandal, which

THE LONG ISLAND CENTER FOR NONPROFIT LEADERSHIP ORGANIZATIONAL ASSESSMENT INTRODUCTION

THE LONG ISLAND CENTER FOR NONPROFIT LEADERSHIP ORGANIZATIONAL ASSESSMENT Developed for the Long Island Community Foundation by Patricia Sparks, MSW, 2001 And modified by Ann Marie Thigpen, Director, Long

THE LONG ISLAND CENTER FOR NONPROFIT LEADERSHIP ORGANIZATIONAL ASSESSMENT Developed for the Long Island Community Foundation by Patricia Sparks, MSW, 2001 And modified by Ann Marie Thigpen, Director, Long

THE FIRST OF LONG ISLAND CORPORATION CORPORATE GOVERNANCE GUIDELINES

PURPOSE AND BOARD RESPONSIBILITIES The purpose of these Corporate Governance Guidelines is to continue a long-standing commitment to good corporate governance practices by The First of Long Island Corporation

PURPOSE AND BOARD RESPONSIBILITIES The purpose of these Corporate Governance Guidelines is to continue a long-standing commitment to good corporate governance practices by The First of Long Island Corporation

Financial Management Manual

Financial Management Manual A Resource for Sexual Assault Service Programs Published and disseminated in October 2011 by the National Sexual Assault Coalition Resource Sharing Project, modifications made

Financial Management Manual A Resource for Sexual Assault Service Programs Published and disseminated in October 2011 by the National Sexual Assault Coalition Resource Sharing Project, modifications made

SEATTLE CHILDREN S HOSPITAL. EIN No OMB Uniform Guidance. Supplementary Financial Report. Year ended September 30, 2017

EIN No. 91-0564748 OMB Uniform Guidance Supplementary Financial Report Year ended September 30, 2017 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Balance Sheets

EIN No. 91-0564748 OMB Uniform Guidance Supplementary Financial Report Year ended September 30, 2017 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Balance Sheets

Internal Controls and Financial Accountability for Not-for-Profit Boards. Attorney General ANDREW M. CUOMO

Internal Controls and Financial Accountability for Not-for-Profit Boards Attorney General ANDREW M. CUOMO Charities Bureau 120 Broadway New York, NY 10271 (212) 416-8401 http://www.oag.state.ny.us/bureaus/charities/about.html

Internal Controls and Financial Accountability for Not-for-Profit Boards Attorney General ANDREW M. CUOMO Charities Bureau 120 Broadway New York, NY 10271 (212) 416-8401 http://www.oag.state.ny.us/bureaus/charities/about.html

Contents ADJUSTING THE ACCOUNTS. Analyze Accounts and Prepare Adjusting Entries 43. Learning Goal 4: Explain the Meaning of Accounting Period 7

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

OAK FOUNDATION GOVERNANCE ASSESSMENT TOOL SECTION 1 GUIDELINES FOR USE

OAK FOUNDATION GOVERNANCE ASSESSMENT TOOL SECTION 1 GUIDELINES FOR USE What is the tool? It is a framework that can be applied during the due diligence process to gain an overview and understanding of

OAK FOUNDATION GOVERNANCE ASSESSMENT TOOL SECTION 1 GUIDELINES FOR USE What is the tool? It is a framework that can be applied during the due diligence process to gain an overview and understanding of

Introduction to Nonprofit Finance

Introduction to Nonprofit Finance CompassPoint Nonprofit Services 500 12 th Street Suite 320 Oakland, CA 94607 ph 510-318-3755 fax 415-541-7708 web: www.compasspoint.org e-mail: workshops@compasspoint.org

Introduction to Nonprofit Finance CompassPoint Nonprofit Services 500 12 th Street Suite 320 Oakland, CA 94607 ph 510-318-3755 fax 415-541-7708 web: www.compasspoint.org e-mail: workshops@compasspoint.org

excellence Standards for AN ETHICS AND ACCOUNTABILITY CODE FOR THE NONPROFIT SECTOR The Pennsylvania Association of Nonprofit Organizations

excellence Standards for AN ETHICS AND ACCOUNTABILITY CODE FOR THE NONPROFIT SECTOR 1 Second edition Printed 2017 The Pennsylvania Association of Nonprofit Organizations MAJOR SPONSOR DISCLAIMER AND COPYRIGHT

excellence Standards for AN ETHICS AND ACCOUNTABILITY CODE FOR THE NONPROFIT SECTOR 1 Second edition Printed 2017 The Pennsylvania Association of Nonprofit Organizations MAJOR SPONSOR DISCLAIMER AND COPYRIGHT

Your Organization Address, Telephone,

Your Organization Address, Telephone, Email Board of Directors Candidate Application Name, phone, email address of organizational representative: _ Please return this application to the above address by

Your Organization Address, Telephone, Email Board of Directors Candidate Application Name, phone, email address of organizational representative: _ Please return this application to the above address by

Audit Committee Member Roles and Responsibilities

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

LEGAL OBLIGATIONS OF NON- PROFIT BOARDS

LEGAL OBLIGATIONS OF NON- PROFIT BOARDS ARE WE AT-RISK?? Source: http://www.mncn.org/info/faq_gov.htm#requirementofbddf BOARD PRACTICES Do we have Board meetings at least quarterly. Do our By Laws accurately

LEGAL OBLIGATIONS OF NON- PROFIT BOARDS ARE WE AT-RISK?? Source: http://www.mncn.org/info/faq_gov.htm#requirementofbddf BOARD PRACTICES Do we have Board meetings at least quarterly. Do our By Laws accurately

Board Governance and Best Practice Checklist

Board Governance and Best Practice Checklist Updated April 2015 Developed in consultation with www.creativeoptionc.com This tool was designed to help nonprofit organizations assess their organizational

Board Governance and Best Practice Checklist Updated April 2015 Developed in consultation with www.creativeoptionc.com This tool was designed to help nonprofit organizations assess their organizational

Board Governance Principles. March 15, 2018 TE CONNECTIVITY VISION AND VALUES

March 15, 2018 TE CONNECTIVITY VISION AND VALUES TE Connectivity s Board of Directors (also referred to as the Board ) is responsible for directing, and providing oversight of, the management of TE Connectivity

March 15, 2018 TE CONNECTIVITY VISION AND VALUES TE Connectivity s Board of Directors (also referred to as the Board ) is responsible for directing, and providing oversight of, the management of TE Connectivity

Rayna Shienfield, Canadian Institute of Chartered Accountants. Introduction

Accountable Reporting for Nonprofit Organizations Rayna Shienfield, Canadian Institute of Chartered Accountants Introduction One only needs to look as far as their local newspaper to observe the increasingly

Accountable Reporting for Nonprofit Organizations Rayna Shienfield, Canadian Institute of Chartered Accountants Introduction One only needs to look as far as their local newspaper to observe the increasingly

Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources.

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

Results from Blackbaud s 2006 Accountability Assessment

January 2007 Results from Blackbaud s 2006 Accountability Assessment Oversight Transparency Internal Controls Best Practices Accountability in the nonprofit world means always being open and ready to answer

January 2007 Results from Blackbaud s 2006 Accountability Assessment Oversight Transparency Internal Controls Best Practices Accountability in the nonprofit world means always being open and ready to answer

FOUR SEI NONPROFIT SURVEY SERIES Answers to Key Questions about Managing Nonprofits ONE PART

PART ONE of FOUR Can boards and investment committees support their nonprofits more efficiently? 2016 SEI NONPROFIT SURVEY SERIES Answers to Key Questions about Managing Nonprofits Background The SEI Nonprofit

PART ONE of FOUR Can boards and investment committees support their nonprofits more efficiently? 2016 SEI NONPROFIT SURVEY SERIES Answers to Key Questions about Managing Nonprofits Background The SEI Nonprofit

SEATTLE CHILDREN S HOSPITAL. EIN No OMB Uniform Guidance. Supplementary Financial Report. Year ended September 30, 2016

EIN No. 91-0564748 OMB Uniform Guidance Supplementary Financial Report Year ended September 30, 2016 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Balance Sheets

EIN No. 91-0564748 OMB Uniform Guidance Supplementary Financial Report Year ended September 30, 2016 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Balance Sheets

Volunteers of America Chartering Requirements, Standards, and Minimum Expected Practices

Volunteers of America Chartering Requirements, Standards, and Minimum Expected Practices I Ministry The affiliate is an integral part of the church of Volunteers of America, actively articulating and advancing

Volunteers of America Chartering Requirements, Standards, and Minimum Expected Practices I Ministry The affiliate is an integral part of the church of Volunteers of America, actively articulating and advancing

GOVERNANCE POLICY. This governance policy has been developed to provide the framework from which the

GOVERNANCE POLICY This governance policy has been developed to provide the framework from which the Board of Trustees will be guided in the execution of their fiduciary duties to administer and oversee

GOVERNANCE POLICY This governance policy has been developed to provide the framework from which the Board of Trustees will be guided in the execution of their fiduciary duties to administer and oversee

Energy Trust Board of Directors Corporate Governance Guidelines

2.03.000 Energy Trust Board of Directors Corporate Governance Guidelines History Source Date Action/Notes Next Review Date Board Decision April 5, 2017 Adopted (R801) February 2020 The following corporate

2.03.000 Energy Trust Board of Directors Corporate Governance Guidelines History Source Date Action/Notes Next Review Date Board Decision April 5, 2017 Adopted (R801) February 2020 The following corporate

CHARTER OF THE SONOMA COUNTY INTERNAL AUDIT FUNCTION JANUARY 15, 2013

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

PERFORMANCE EVALUATION POLICY [PTC India Limited (PTC)]

![PERFORMANCE EVALUATION POLICY [PTC India Limited (PTC)]](/thumbs/80/82432276.jpg "PERFORMANCE EVALUATION POLICY [PTC India Limited (PTC)]") PERFORMANCE EVALUATION POLICY [PTC India Limited (PTC)] For internal use only Page 1 of 10 The following Performance Evaluation Policy is for the use to the Board of Directors of PTC ( Company ) and is

PERFORMANCE EVALUATION POLICY [PTC India Limited (PTC)] For internal use only Page 1 of 10 The following Performance Evaluation Policy is for the use to the Board of Directors of PTC ( Company ) and is

The FMA Institute Courses & Resources

The FMA Institute Courses & Resources Institute Overview The Blog Course Descriptions & Prices FUND E-Z FMA articles 1 The FMA Institute is committed to developing nonprofit financial leaders and facilitating

The FMA Institute Courses & Resources Institute Overview The Blog Course Descriptions & Prices FUND E-Z FMA articles 1 The FMA Institute is committed to developing nonprofit financial leaders and facilitating

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Circular A-133 June 30, 2013 Federal Entity

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Circular A-133 June 30, 2013 Federal Entity Identification Number 23-1352685 University of Pennsylvania

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Circular A-133 June 30, 2013 Federal Entity Identification Number 23-1352685 University of Pennsylvania

Management s Accountability to Stakeholders Stakeholders Provide Management is accountable for: Owners Operating activities Government Creditors

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

BANK ONE CORP /OH/ FORM 11-K (Annual Report of Employee Stock Plans) Filed 7/11/1997 For Period Ending 12/31/1996

Filed 7/11/1997 For Period Ending 12/31/1996") BANK ONE CORP /OH/ FORM 11-K (Annual Report of Employee Stock Plans) Filed 7/11/1997 For Period Ending 12/31/1996 Address 100 E BROAD ST COLUMBUS, Ohio 43271 Telephone 614-248-5944 CIK 0000036090 Fiscal

BANK ONE CORP /OH/ FORM 11-K (Annual Report of Employee Stock Plans) Filed 7/11/1997 For Period Ending 12/31/1996 Address 100 E BROAD ST COLUMBUS, Ohio 43271 Telephone 614-248-5944 CIK 0000036090 Fiscal

Board to Death. Cafe TAC

Board to Death Cafe TAC 2012 1 Objectives 1. To better understand and achieve the required and expected levels of involvement by organizational governance bodies; 2. To understand separation of duties

Board to Death Cafe TAC 2012 1 Objectives 1. To better understand and achieve the required and expected levels of involvement by organizational governance bodies; 2. To understand separation of duties

Third Quarter Fiscal 2013 Performance June 29, Financial results and company highlights Fourth quarter and fiscal year 2013 outlook

Third Quarter Fiscal 2013 Performance June 29, 2013 Financial results and company highlights Fourth quarter and fiscal year 2013 outlook Safe Harbor Statement This presentation contains forward looking

Third Quarter Fiscal 2013 Performance June 29, 2013 Financial results and company highlights Fourth quarter and fiscal year 2013 outlook Safe Harbor Statement This presentation contains forward looking

Financial Management in Leisure Organizations Organization of Financial Management

Financial Management in Leisure Organizations Organization of Financial Management Chapters 1-6 1 Financial Management in Multiple Sectors 2 Sectors Public Private Not-for-Profit Commercial 3 Comparison

Financial Management in Leisure Organizations Organization of Financial Management Chapters 1-6 1 Financial Management in Multiple Sectors 2 Sectors Public Private Not-for-Profit Commercial 3 Comparison

1 C. The Chief Executive Officer Affiliate Class of Services are 2 Provided at a Reasonable Cost

1 C. The Chief Executive Officer Affiliate Class of Services are 2 Provided at a Reasonable Cost 3 Q. Are the costs of the Chief Executive Officer affiliate class of services 4 reasonable? 5 A. Yes. The

1 C. The Chief Executive Officer Affiliate Class of Services are 2 Provided at a Reasonable Cost 3 Q. Are the costs of the Chief Executive Officer affiliate class of services 4 reasonable? 5 A. Yes. The

IFRS Seminar. Berlin /24/2015 1

IFRS Seminar Berlin 2015 8/24/2015 1 Accounting Issues for US Parent with European Subsidiaries: Cross Border Consolidation Issues Scott A. Walters, CPA, CGMA Partner, Daszkal Bolton LLP 8/24/2015 2 Purpose

IFRS Seminar Berlin 2015 8/24/2015 1 Accounting Issues for US Parent with European Subsidiaries: Cross Border Consolidation Issues Scott A. Walters, CPA, CGMA Partner, Daszkal Bolton LLP 8/24/2015 2 Purpose

The NonProfit s Guide to Making Data-Driven Decisions. 5 Steps to Increase Outcomes, Raise More Money, and Improve Cash Flow

The NonProfit s Guide to Making Data-Driven Decisions 5 Steps to Increase Outcomes, Raise More Money, and Improve Cash Flow Nonprofits Should Be Run Like For-Profits with Actionable Financial Intelligence.

The NonProfit s Guide to Making Data-Driven Decisions 5 Steps to Increase Outcomes, Raise More Money, and Improve Cash Flow Nonprofits Should Be Run Like For-Profits with Actionable Financial Intelligence.

Wyoming Community Development Authority Job Description

Wyoming Community Development Authority Job Description JOB TITLE: Controller PAY GRADE: 9 DEPARTMENT: Finance FLSA STATUS: Exempt REPORTS TO: Director of Finance & Admin REVISED: April 2017 SUPERVISORY

Wyoming Community Development Authority Job Description JOB TITLE: Controller PAY GRADE: 9 DEPARTMENT: Finance FLSA STATUS: Exempt REPORTS TO: Director of Finance & Admin REVISED: April 2017 SUPERVISORY

Above all, a nonprofit board member should understand these five BALANCE SHEET concepts:

Balance Sheet KIT Healthy organizations know where they are financially at any given time. A Balance Sheet is a report showing where you stand financially at a point in time. It is also known as a Statement

Balance Sheet KIT Healthy organizations know where they are financially at any given time. A Balance Sheet is a report showing where you stand financially at a point in time. It is also known as a Statement

RIGHT FROM THE START: RESPONSIBILITIES of DIRECTORS of NOT-FOR-PROFIT CORPORATIONS

RIGHT FROM THE START: RESPONSIBILITIES of DIRECTORS of NOT-FOR-PROFIT CORPORATIONS Office of the New York State Attorney General Charities Bureau 28 Liberty Street New York, NY 10005 (212) 416-8400 www.charitiesnys.com

RIGHT FROM THE START: RESPONSIBILITIES of DIRECTORS of NOT-FOR-PROFIT CORPORATIONS Office of the New York State Attorney General Charities Bureau 28 Liberty Street New York, NY 10005 (212) 416-8400 www.charitiesnys.com

State Council of Higher Education for Virginia

Rick Legon AGB President October 22, 2014 Best Practices of High-Performing Public-Institution Boards PRESENTED TO State Council of Higher Education for Virginia Board Accountability Boards are accountable:

Rick Legon AGB President October 22, 2014 Best Practices of High-Performing Public-Institution Boards PRESENTED TO State Council of Higher Education for Virginia Board Accountability Boards are accountable:

CATERPILLAR INC. GUIDELINES ON CORPORATE GOVERNANCE ISSUES (amended as of April 1, 2017)

") Preamble CATERPILLAR INC. GUIDELINES ON CORPORATE GOVERNANCE ISSUES (amended as of April 1, 2017) The Board of Directors (the Board ) of Caterpillar Inc. (the Company ) has adopted the following corporate

Preamble CATERPILLAR INC. GUIDELINES ON CORPORATE GOVERNANCE ISSUES (amended as of April 1, 2017) The Board of Directors (the Board ) of Caterpillar Inc. (the Company ) has adopted the following corporate

Right From the Start. Responsibilities of Directors and Officers of. Not-for-Profit Corporations

Right From the Start Responsibilities of Directors and Officers of Not-for-Profit Corporations Attorney General ELIOT SPITZER Charities Bureau 120 Broadway New York, NY 10271 (212) 416-8401 www.oag.state.ny.us/charities/charities.html

Right From the Start Responsibilities of Directors and Officers of Not-for-Profit Corporations Attorney General ELIOT SPITZER Charities Bureau 120 Broadway New York, NY 10271 (212) 416-8401 www.oag.state.ny.us/charities/charities.html

We Build and Transform Lives

CONNECTICUT HOUSING PARTNERS 5-YEAR BUSINESS PLAN FOR GROWTH We Build and Transform Lives Compiled by: RENÉE DOBOS On Behalf of: Connecticut Housing Partners February 2017 CHP Creates Viable Communities

CONNECTICUT HOUSING PARTNERS 5-YEAR BUSINESS PLAN FOR GROWTH We Build and Transform Lives Compiled by: RENÉE DOBOS On Behalf of: Connecticut Housing Partners February 2017 CHP Creates Viable Communities

The Many Roles of the CFO. Tuesday, Oct. 2

The Many Roles of the CFO Tuesday, Oct. 2 Presenters Larry Ladd, Director, National Higher Education Practice, Grant Thornton LLP William G. Laird, Senior Vice President for Finance and CFO, Loyola University

The Many Roles of the CFO Tuesday, Oct. 2 Presenters Larry Ladd, Director, National Higher Education Practice, Grant Thornton LLP William G. Laird, Senior Vice President for Finance and CFO, Loyola University

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012 INTRODUCTION Benchmarking the performance of ICANN s board to principles and practices of other like-minded organizations can lead to overall

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012 INTRODUCTION Benchmarking the performance of ICANN s board to principles and practices of other like-minded organizations can lead to overall

NONPROFIT CONTRACTOR FISCAL & COMPLIANCE REVIEW STANDARD MONITORING FORM

Contractor Name: City Contracts Reviewed: Department / Program NONPROFIT CONTRACTOR FISCAL & COMPLIANCE REVIEW STANDARD MONITORING FORM Contract Name and Description For City Staff Use Only Please indicate

Contractor Name: City Contracts Reviewed: Department / Program NONPROFIT CONTRACTOR FISCAL & COMPLIANCE REVIEW STANDARD MONITORING FORM Contract Name and Description For City Staff Use Only Please indicate

FRIENDSHIP HOUSE JOB DESCRIPTION. Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

Nonprofit Board Evaluation Form

Also adapted from Management Indicators Checklist, with permission from Greater Twin Cities United Way Nonprofit Board Evaluation Form Description This free assessment tool can be used to get a reasonable

Also adapted from Management Indicators Checklist, with permission from Greater Twin Cities United Way Nonprofit Board Evaluation Form Description This free assessment tool can be used to get a reasonable

Cigna Corporation Board Corporate Governance Guidelines (Effective July 25, 2018)

") Cigna Corporation Board Corporate Governance Guidelines (Effective July 25, 2018) Introduction The Cigna Corporation Board of Directors and Committees have adopted these Corporate Governance Guidelines.

Cigna Corporation Board Corporate Governance Guidelines (Effective July 25, 2018) Introduction The Cigna Corporation Board of Directors and Committees have adopted these Corporate Governance Guidelines.

Fundraising Readiness: How does your agency stack up? By Brigette Sarabi

Fundraising Readiness: How does your agency stack up? By Brigette Sarabi Hastily patching together a fundraising scheme to deal with some impending fiscal crisis is an all-too-common approach to an all-too-common

Fundraising Readiness: How does your agency stack up? By Brigette Sarabi Hastily patching together a fundraising scheme to deal with some impending fiscal crisis is an all-too-common approach to an all-too-common

MEAD JOHNSON NUTRITION COMPANY CORPORATE GOVERNANCE GUIDELINES

MEAD JOHNSON NUTRITION COMPANY CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Mead Johnson Nutrition Company (the Company ), which is elected by the stockholders, has responsibility

MEAD JOHNSON NUTRITION COMPANY CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Mead Johnson Nutrition Company (the Company ), which is elected by the stockholders, has responsibility

Board Governance. Role of the Board Chairperson By-Laws Ethic Code Conflict of Interest Disclosure

Board Governance Role of the Board Chairperson By-Laws Ethic Code Conflict of Interest Disclosure Presentation Objectives To provide relevant insights into good governance and its practical impact on HAWS

Board Governance Role of the Board Chairperson By-Laws Ethic Code Conflict of Interest Disclosure Presentation Objectives To provide relevant insights into good governance and its practical impact on HAWS

Stanford University Stanford, California Reports on Federal Awards in Accordance with OMB Uniform Guidance August 31, 2016 EIN:

Stanford University Stanford, California Reports on Federal Awards in Accordance with OMB Uniform Guidance August 31, 2016 EIN: 94-1156365 Stanford University Stanford, California Reports on Federal Awards

Stanford University Stanford, California Reports on Federal Awards in Accordance with OMB Uniform Guidance August 31, 2016 EIN: 94-1156365 Stanford University Stanford, California Reports on Federal Awards

Position Description, Member Board of Directors HISTORY

Position Description, Member Board of Directors HISTORY Make-A-Wish America was founded in 1980. It all began because of a 7- year-old boy named Chris. A small group of people in Phoenix, Arizona helped

Position Description, Member Board of Directors HISTORY Make-A-Wish America was founded in 1980. It all began because of a 7- year-old boy named Chris. A small group of people in Phoenix, Arizona helped

FEDERAL HOME LOAN BANK OF INDIANAPOLIS CHARTER FOR THE AUDIT COMMITTEE

BOARD APPROVAL: JULY 16, 2015 FEDERAL HOME LOAN BANK OF INDIANAPOLIS Mission The mission of the Audit Committee ( Committee ) is to assist the Board of Directors ( Board ) in fulfilling its fiduciary responsibilities

BOARD APPROVAL: JULY 16, 2015 FEDERAL HOME LOAN BANK OF INDIANAPOLIS Mission The mission of the Audit Committee ( Committee ) is to assist the Board of Directors ( Board ) in fulfilling its fiduciary responsibilities

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector Second edition, 2014

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector Second edition, 2014 Disclaimer and Copyright Notice: The Standards for Excellence : An Ethics and Accountability Code

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector Second edition, 2014 Disclaimer and Copyright Notice: The Standards for Excellence : An Ethics and Accountability Code

IRC 509(a)(3) SUPPORTING ORGANIZATIONS GUIDE SHEET TYPE III March 13, 2008

(3) SUPPORTING ORGANIZATIONS GUIDE SHEET TYPE III March 13, 2008") IRC 509(a)(3) SUPPORTING ORGANIZATIONS GUIDE SHEET TYPE III March 13, 2008 PART 1: ORGANIZATIONAL TEST UNDER IRC 509(a)(3)(A) An organization must meet the organizational test to qualify under IRC 509(a)(3).

IRC 509(a)(3) SUPPORTING ORGANIZATIONS GUIDE SHEET TYPE III March 13, 2008 PART 1: ORGANIZATIONAL TEST UNDER IRC 509(a)(3)(A) An organization must meet the organizational test to qualify under IRC 509(a)(3).

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service(77 Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit

Form 990 Department of the Treasury Internal Revenue Service(77 Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit

CANDIDATE CAMPAIGN PERIOD FINANCIAL STATEMENT FORM CD-FS-01 Page 1 of 2

NAME OF REGISTERED CANDIDATE ELECTION FINANCES AND CONTRIBUTIONS DISCLOSURE ACT CANDIDATE CAMPAIGN PERIOD FINANCIAL STATEMENT FORM CD-FS-01 Page 1 of 2 Period From SEE NOTE AT BOTTOM NAME OF REGISTERED

NAME OF REGISTERED CANDIDATE ELECTION FINANCES AND CONTRIBUTIONS DISCLOSURE ACT CANDIDATE CAMPAIGN PERIOD FINANCIAL STATEMENT FORM CD-FS-01 Page 1 of 2 Period From SEE NOTE AT BOTTOM NAME OF REGISTERED

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Uniform Guidance June 30, 2016 Federal Entity

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Uniform Guidance June 30, 2016 Federal Entity Identification Number 23-1352685 University of Pennsylvania

University of Pennsylvania Philadelphia, Pennsylvania Reports on Federal Awards in Accordance with OMB Uniform Guidance June 30, 2016 Federal Entity Identification Number 23-1352685 University of Pennsylvania

BOARD OF DIRECTORS CHARTER

BOARD OF DIRECTORS CHARTER I. Introduction A. The Board is composed of that number of Directors determined by the Board after consultation with the Corporate Governance Committee, and as confirmed by a

BOARD OF DIRECTORS CHARTER I. Introduction A. The Board is composed of that number of Directors determined by the Board after consultation with the Corporate Governance Committee, and as confirmed by a

Financial Responsibilities of Boards of Non-Profits. Presented by Darren Adamson, CPA, CA, Partner

Financial Responsibilities of Boards of Non-Profits Presented by Darren Adamson, CPA, CA, Partner Welcome and Introductions Thank you for coming! Comments and discussion are highly encouraged please share

Financial Responsibilities of Boards of Non-Profits Presented by Darren Adamson, CPA, CA, Partner Welcome and Introductions Thank you for coming! Comments and discussion are highly encouraged please share

FAQs for JOURNEY TO EXCELLENCE PERFORMANCE RECOGNITION PROGRAM (Council)

") 1. Have the calculations been done to determine which level each council falls into based on 2009 data? If so, can we have that information? Yes, those calculations have been done. The results can be requested

1. Have the calculations been done to determine which level each council falls into based on 2009 data? If so, can we have that information? Yes, those calculations have been done. The results can be requested

AUDIT COMMITTEE CHARTER APRIL 30, 2018

AUDIT COMMITTEE CHARTER APRIL 30, 2018 I. Purpose The Audit Committee ( Committee ) is appointed by the Board of Directors ( Board ) to assist the Board in its oversight responsibilities relating to: the

AUDIT COMMITTEE CHARTER APRIL 30, 2018 I. Purpose The Audit Committee ( Committee ) is appointed by the Board of Directors ( Board ) to assist the Board in its oversight responsibilities relating to: the

Nonprofit Organizational Assessment Tool

Nonprofit Organizational Assessment Tool The following checklist was designed to help you review the strategies and practices that your organization might want to put in place to further its effectiveness.

Nonprofit Organizational Assessment Tool The following checklist was designed to help you review the strategies and practices that your organization might want to put in place to further its effectiveness.

Tools and Techniques for Effective CAA Board Leadership. Today s Agenda

Tools and Techniques for Effective CAA Board Leadership 2016 ACAAA Annual Conference Pre-Conference Training for Community Action Boards of Directors May 24, 2016 Veronica Zhang, Esq. Community Action

Tools and Techniques for Effective CAA Board Leadership 2016 ACAAA Annual Conference Pre-Conference Training for Community Action Boards of Directors May 24, 2016 Veronica Zhang, Esq. Community Action

TAX INFORMATION BOOKLET

2011 TAX INFORMATION BOOKLET Enduro Royalty Trust Important Tax Information 919 Congress Avenue 2011 Austin, TX 78701 Telephone (512) 236-6545 EIN: 45-6259461 This booklet provides 2011 tax information

2011 TAX INFORMATION BOOKLET Enduro Royalty Trust Important Tax Information 919 Congress Avenue 2011 Austin, TX 78701 Telephone (512) 236-6545 EIN: 45-6259461 This booklet provides 2011 tax information

FUNCTIONAL EXPENSE ALLOCATION NONPROFITS AFTER FASB ASU YEO & YEO. yeoandyeo.com. CPAs & BUSINESS CONSULTANTS. CPAs & BUSINESS CONSULTANTS

FUNCTIONAL EXPENSE YEO & YEO ALLOCATION FOR NONPROFITS AFTER FASB ASU 2016-14 CPAs & BUSINESS CONSULTANTS yeoandyeo.com BRIEF Y E O TAX & Y O OCTOBER E 2015 CPAs & BUSINESS CONSULTANTS The Importance of

FUNCTIONAL EXPENSE YEO & YEO ALLOCATION FOR NONPROFITS AFTER FASB ASU 2016-14 CPAs & BUSINESS CONSULTANTS yeoandyeo.com BRIEF Y E O TAX & Y O OCTOBER E 2015 CPAs & BUSINESS CONSULTANTS The Importance of

Form 990. Return of Organization Exempt From Income Tax

in C:111 w s J V) i4 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Department of the Treasury

in C:111 w s J V) i4 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Department of the Treasury

University of Rhode Island Office of the Controller. Service Centers. Issuance: December 1, 1998 Effective: July 1, 1999 Revised: December 26, 2014

University of Rhode Island Office of the Controller Service Centers Issuance: December 1, 1998 Effective: July 1, 1999 Revised: December 26, 2014 I. Purpose: This Policy Statement establishes the University

University of Rhode Island Office of the Controller Service Centers Issuance: December 1, 1998 Effective: July 1, 1999 Revised: December 26, 2014 I. Purpose: This Policy Statement establishes the University

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector The Pennsylvania Association of Nonprofit Organizations

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector 1 Version 2.0 The Pennsylvania Association of Nonprofit Organizations Disclaimer and Copyright Notice: 1998-2015 Maryland

excellence Standards for An Ethics and Accountability Code for the Nonprofit Sector 1 Version 2.0 The Pennsylvania Association of Nonprofit Organizations Disclaimer and Copyright Notice: 1998-2015 Maryland

Form 990-EZ. Short Form OMB No Return of Organization Exempt From Income Tax. Open to PubI Inspection

I O N 0 W Form 990-EZ Department of the Treasury Internal Revenue service A For the 2015 calendar year, or tax year be B Check it applicable Short Form OMB No. 1545-1150 Return of Organization Exempt From

I O N 0 W Form 990-EZ Department of the Treasury Internal Revenue service A For the 2015 calendar year, or tax year be B Check it applicable Short Form OMB No. 1545-1150 Return of Organization Exempt From

Records Retention and Destruction

s and Destruction This policy is in effect for all directors, officers, and employees of the National Council of Juvenile and Family Court Judges aand its related entities, which are designated as the

s and Destruction This policy is in effect for all directors, officers, and employees of the National Council of Juvenile and Family Court Judges aand its related entities, which are designated as the

Form 990 Return of Organization Exempt From Income Tax

t A Form 99 Return of Organization Exempt From Income Tax 4 Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Department of the Treasury Do not enter Social

t A Form 99 Return of Organization Exempt From Income Tax 4 Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Department of the Treasury Do not enter Social

400+ scholarship-providing member organizations, awarding over $1 billion in scholarships annually

Executive Director 400+ scholarship-providing member organizations, awarding over $1 billion in scholarships annually Desired Experience and Attributes About the Executive Director Position The Executive

Executive Director 400+ scholarship-providing member organizations, awarding over $1 billion in scholarships annually Desired Experience and Attributes About the Executive Director Position The Executive

Corporate Governance Guidelines

Corporate Governance Guidelines The Board of Directors (the Board ) of (the Corporation ) has adopted these governance guidelines. The guidelines, in conjunction with the Corporation s articles of incorporation,

Corporate Governance Guidelines The Board of Directors (the Board ) of (the Corporation ) has adopted these governance guidelines. The guidelines, in conjunction with the Corporation s articles of incorporation,

JB+A Board Evaluation Tool

Mission/Vision One of the Board's primary roles is to establish the mission of the organization. Once established, the Board is responsible for its regular review and, if necessary, its revision. The mission

Mission/Vision One of the Board's primary roles is to establish the mission of the organization. Once established, the Board is responsible for its regular review and, if necessary, its revision. The mission

Corporate Governance Principles

Corporate Governance Principles I. INTRODUCTION The ISO Board of Governors ( Board ) of the California Independent System Operator Corporation ( ISO ) has adopted these Corporate Governance Principles

Corporate Governance Principles I. INTRODUCTION The ISO Board of Governors ( Board ) of the California Independent System Operator Corporation ( ISO ) has adopted these Corporate Governance Principles

Standards for Excellence Educational Resource Packets

Standards for Excellence Educational Resource Packets The Standards for Excellence Institute has developed and maintains educational resource packets for organizations interested in implementing the Standards

Standards for Excellence Educational Resource Packets The Standards for Excellence Institute has developed and maintains educational resource packets for organizations interested in implementing the Standards

Providing National Leadership and Services for Advancing the Outdoor Recreation Profession

Providing National Leadership and Services for Advancing the Outdoor Recreation Profession SORP Seeking Applications for Executive Director The Society of Outdoor Recreation Professionals (SORP) Board

Providing National Leadership and Services for Advancing the Outdoor Recreation Profession SORP Seeking Applications for Executive Director The Society of Outdoor Recreation Professionals (SORP) Board

Finance Unlocked for Nonprofits

Finance Unlocked for Nonprofits Unlocking Financial Literacy for Nonprofit Board Members to Deliver Mission & Protect Assets An initiative of Washington Nonprofits and Jacobson Jarvis PLLC In partnership

Finance Unlocked for Nonprofits Unlocking Financial Literacy for Nonprofit Board Members to Deliver Mission & Protect Assets An initiative of Washington Nonprofits and Jacobson Jarvis PLLC In partnership

Allergan plc Board of Directors Corporate Governance Guidelines

Allergan plc Board of Directors Corporate Governance Guidelines I. Roles and Responsibilities of the Board of Directors The Board of Directors (the Board ), elected by the shareholders, is the ultimate

Allergan plc Board of Directors Corporate Governance Guidelines I. Roles and Responsibilities of the Board of Directors The Board of Directors (the Board ), elected by the shareholders, is the ultimate