Office of the Utah Legislative Auditor General. Fraud Prevention. Utah Government Finance Officers Association. Spring 2017 Conference

|

|

|

- Winfred Mathews

- 6 years ago

- Views:

Transcription

1 Office of the Utah Legislative Auditor General Fraud Prevention Utah Government Finance Officers Association Spring 2017 Conference

2 Utah Legislative Auditor General Constitutional Charge and Authority The legislative auditor shall have authority to conduct audits of any branch, department, agency, or political subdivision of this state and shall perform such other related duties as may be prescribed by the Legislature. Statutorily The Office of Legislative Auditor General may obtain access to all records, documents, and reports of any entity that receives public funds necessary to the scope of its duties. have authority to conduct audits of any branch, department, Sources: agency, or political subdivision of this state Utah Constitution Section 33 Article VI Utah Code Slide 2

3 Authority and Independence Essential Slide 3

4 Utah Legislative Auditor General Mission Statement The mission of the Office of the Legislative Auditor General is to provide accurate, in-depth information, objective analysis, and useful recommendations that help legislators and other decision makers: Improve Program Effectiveness Reduce Taxpayer Costs Promote Government Accountability Slide 4

5 Types of Audits Conducted by Utah Legislative Auditor General Audit Types Economy or Efficiency Program or Effectiveness Financial Informational Compliance Allegation Audit Focus The degree to which resources have been efficiently used to generate output The extent to which the organization s mission, goals, and objectives are consistent with output Completeness and reliability of financial statements, soundness of financial controls The providing of specifically requested information. Evaluation of that information may or may not occur. Administrative adherence to constitutions, laws, and other requirements The extent to which specific allegations are true Slide 5

6 Our Business Model: Attributes of a Finding Condition What is happening? Criteria What should be happening? Cause What created the condition? Effect What is the impact of the condition? Recommendation What should be done? (corrective or preventative action) Slide 6

7 Criteria & Effect Relationship Weakest Effect Weakest Criteria Laws or Mission Statements Industry or Professional Standards Historical Data or Goals & Objectives Expert Opinion Prudent Business Practices Auditor Opinion Strongest Effect No Significant Impact Implied Savings Small Dollar Impact Improved Services Large Dollar Impact Loss of Life or Public Danger Slide 7

8 ACFE s Occupational Fraud and Abuse 2016 Global Fraud Study Study looked at 2,127 cases worldwide, with 1,038 being from the United States. The total loss caused by the cases exceeded $6.3 Billion, with an average loss per case of $2.7 Million. Typical organizations lose 5% of revenues in a given year as a result of fraud. Slide 8

9 ACFE s Occupational Fraud and Abuse 2016 Global Fraud Study Of the cases involving government, the federal level reported the highest median loss ($194,000), compared to state ($100,000) and local ($80,000). The median loss suffered by small organizations (those with fewer than 100 employees) was the same as that incurred by the largest organizations (those with more than 10,000 employees). Slide 9

10 ACFE s Occupational Fraud and Abuse 2016 Global Fraud Study Organizations of different sizes tend to have different fraud risks. Corruption was more prevalent in larger organizations, while check tampering, skimming, payroll, and cash larceny schemes were twice as common in small organizations as in larger organizations. Slide 10

11 Fraud Exists What Can We Do To Make It More Difficult I think organizations have to tailor their compliance programs and their investigative mechanisms to their organizations. There s no One-Size-Fits-All compliance program. --- Leslie R. Caldwell, Assistant Attorney General, U.S. Department of Justice s Criminal Division--- Slide 11

12 The FIRE Triangle Slide 12

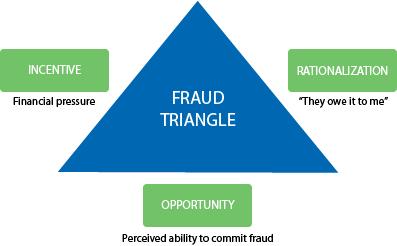

13 The FRAUD Triangle Slide 13

14 Fire to Fraud Comparison Slide 14

15 Fraud Triangle - Incentive Incentive or Pressure: This is often what causes a person to commit fraud. This includes medical bills, expensive tastes, addiction problems, significant financial needs, etc. Often this need/problem is nondiscloseable in the eyes of the fraudster. That is, the person believes, for whatever reason, that their problem must be solved in secret. Incentives to commit fraud can range from dire circumstances, greed, laziness, etc. Utah Medicaid. Slide 15

16 Fraud Triangle - Incentive Slide 16

17 Fraud Triangle Incentive: Utah Medicaid Audit found complete lack of oversight and control with fraud, waste, and abuse likely. Estimate: $20 million MORE could be recovered in Utah Medicaid with proper controls in place. Slide 17

18 Fraud Triangle Incentive: Utah Medicaid Director of Health s Response.. The recommendations we will look at careful and we will implement them whenever we can.... I do not think for a minute that if we recover every inappropriately covered Medicaid service, we would find anything close to $20 million in Utah.... the Utah medical community has a higher ethical standard... I don t think there is as much of it there as has been implied. Slide 18

19 Fraud Triangle Incentive: Utah Medicaid Office of the Utah Inspector General created as a result of the audit.. Slide 19

20 Fraud Triangle - Incentive Slide 20

21 Fraud Triangle - Rationalization Rationalization: It occurs when the individual develops a justification for their fraudulent activities. The rationalization varies by case and individual. Some examples include: I really need this money and I will pay it back Other people are doing it The company owes me People can find a way to rationalize almost anything URS Insider Trading Slide 21

22 Fraud Triangle Rationalization A Few Good Men Slide 22

23 Fraud Triangle - Rationalization Slide 23

24 Fraud Triangle Rationalization: Utah Retirement Systems Asked to conduct an audit of the investment practices of the Utah Retirement Systems (URS). Found asset misclassifications and Chief Investment Officer (CIO) involved in an outside consulting business. Outside activity vaguely disclosed, but nobody questioned it. Slide 24

25 Fraud Triangle Rationalization: Utah Retirement Systems Turns out, CIO s partner was a URS Board Member, who happened to be an investment advisor for the LDS Church. Front-Running/Insider Trading was occurring. URS now has a full-time Compliance Officer. Slide 25

26 Fraud Triangle - Rationalization Slide 26

27 Fraud Triangle - Opportunity Opportunity: Opportunity is the ability to commit fraud. Because fraudsters don t wish to be caught, they must also believe that their activities will not be detected. Opportunity is created by weak internal controls, poor management oversight, and through abuse of power. Fraud cannot be eliminated, but it has to be recognized, and addressed so it can be greatly reduced DABC. Slide 27

28 Fraud Triangle - Opportunity Slide 28

29 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Audit request was for us to look at operations because they had not been audited since the early 1980s, but thought nothing wrong Slide 29

30 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Slide 30

31 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Selected highlights from first 2 DABC audits: DABC did not adequately consider alternatives to budget cuts & used made up numbers DABC Commission had habitually violated open meeting laws, organization had significant conflicts of interests, and lacked any sort of business planning Slide 31

32 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Slide 32

33 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Slide 33

34 Fraud Triangle Opportunity: Department of Alcoholic Beverage Control Selected highlights from remaining DABC audits: Poor management contributed to increased state losses and management tried to conceal the issues DABC had been incompetently managed DABC had been rigging bids and falsifying financial documentation and artificially splitting invoices in violation of state law Business done with DABC Directors son was illegal DABC management failed to ensure oversight of financial affairs Employees and vendors stealing and/or accepting illegal gifts. Other management practices were inappropriate and questionable Slide 34

35 Looking For Risk/Fraud May Be Difficult Sometimes Slide 35

36 Looking For Risk/Fraud May Be Difficult Sometimes Reduce fraud potential Look Around Your Organization Look for vulnerabilities/threats Can you follow the documentation Is there separation of duties Is there checks and balances Remember: I think organizations have to tailor their compliance programs and their investigative mechanisms to their organizations. There s no One-Size-Fits-All compliance program. --- Leslie R. Caldwell, Assistant Attorney General, U.S. Department of Justice s Criminal Division--- Slide 36

37 Tip: Look For Risk Risk: The possibility of an event occurring that will have an impact on the achievement of objectives and it is measured in terms of impact and likelihood FOR MORE INFORMATION Performance Auditing: A Measurement Approach Slide 37

38 Tip: Do Risk Assessments Risk Assessment: The determination of quantitative or qualitative value of risk related to a concrete situation and a recognized threat FOR MORE INFORMATION Performance Auditing: A Measurement Approach Slide 38

39 Tip: Your Risk Assessment Goal Risk Assessment Goal: To prioritize internal audit activities on the basis of the most significant risks. The risk assessment process entails a systematic review of the risks facing an organization. Slide 39

40 Tip: Fraud Detection Association of Certified Fraud Examiners Over 40% of all fraud cases were detected by a tip more than twice the rate of any other detection method *. ACFE, tips have been the most common means of detection in every study since 2002, when we began tracking the data. * Employees know where problems are must work with them to help improve * 2014 Report to the Nations.

41 Tip: Fraud Detection What they willingly contribute Their message Management Policies Criteria What they want you to believe is happening / intend to happen *Mid-level* Cause Documentation What is happening Staff Criteria Allegations What they think is happening

42 Tip: Where to Look - - Four Pitfalls *We examined 134 of our office s recommendations over a three-year period and found that over 80% of the recommendations could be attributed to one or more of the below four pitfalls. 1. Poor Oversight: Lack of governance and/or inadequate organizational structure 2. Policy and Procedure Failures: Lack of strategic planning 3. Inadequate Performance Standards and Measures: Not comparing to proper criteria 4. Weak Data: Lack of data collection or data collection systems and/or use of unreliable data

43 Office of the Utah Legislative Auditor General Brian J. Dean, CIA, CFE Audit Manager Utah State Capitol Complex 315 House Building Salt Lake City, Utah (801) Office Website:

ACUIA October Office of the Utah Legislative Auditor General. Examples of High Impact Auditing. High Impact Auditing

Office of the Utah Legislative Auditor General ACUIA October 2015 High Impact Auditing Examples of High Impact Auditing Slide 2 Auditing for Impact May Be Difficult Sometimes Slide 3 1 Risk Definition:

Office of the Utah Legislative Auditor General ACUIA October 2015 High Impact Auditing Examples of High Impact Auditing Slide 2 Auditing for Impact May Be Difficult Sometimes Slide 3 1 Risk Definition:

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Fraud Awareness Jennifer Murtha Clara Ewing

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

Fraud Risk Management

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

2/20/15. Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention Training

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

Fraud Prevention, Detection and Control. Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Community College Audit and Compliance Workshop. VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014

Community College Audit and Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Community College Audit and Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Can You Spot Fraudsters?

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Presented by Ed Williamson and Erica Bailey

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program Monday June 13, 2011 10:20 11:40 San Diego, California Who owns fraud why is it important? Many companies struggle to determine

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program Monday June 13, 2011 10:20 11:40 San Diego, California Who owns fraud why is it important? Many companies struggle to determine

Karen L. Mosteller, CPA, CHBC

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Module 1: Safeguarding District Resources: Roles & Responsibilities

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Fraud in the Insurance Industry How it Can Impact Your Agency

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

FRD510. Principles of Fraud Examination - 20 hours. Objectives

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

Week 3: Fraud, Procure to Pay Process Controls

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Information and and training provid v ed by Smith Elliott Elliott Kearns & Compan

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Fraud Awareness February 27, 2015

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Fraud Prevention and Detection Michael Schulstad, CPA/CFF/CGMA/FBI (ret)

") WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor Fraud Prevention and

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor Fraud Prevention and

MANAGING FRAUD RISK. Teresa D. Thamer, CPA, CFE Brenau University

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

Fraud incident handling management. Meeting the challenges of fraud

Fraud incident handling management Meeting the challenges of fraud Recently, more companies are becoming more aware of the financial and reputational damage that fraud can cause to a company. Especially

Fraud incident handling management Meeting the challenges of fraud Recently, more companies are becoming more aware of the financial and reputational damage that fraud can cause to a company. Especially

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Moving the Needle: Fighting Fraud from the Inside Through Audit. Mary Breslin, CFE, CIA President Empower Audit Training and Consulting

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

Fraud Prevention and Detection for IT Professionals

Fraud Prevention and Detection for IT Professionals Netsecure 2011 Conference Sandra Rolnicki Senior Vice President, March 2011 Contents (1) Introduction to fraud concepts (2) How control weaknesses are

Fraud Prevention and Detection for IT Professionals Netsecure 2011 Conference Sandra Rolnicki Senior Vice President, March 2011 Contents (1) Introduction to fraud concepts (2) How control weaknesses are

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OUTSMART FRAUD. Strategic Internal Controls to Prevent Business Fraud

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

Changing Your Paradigm on Risks and Controls

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

Internal Audit s Role in Preventing, Deterring and Detecting Fraud Working as Part of a Fraud Management Team The Way Forward

Internal Audit s Role in Preventing, Deterring and Detecting Fraud Working as Part of a Fraud Management Team The Way Forward Ottawa, ON 11/26/2015 Introduction and Objectives The main objectives of today

Internal Audit s Role in Preventing, Deterring and Detecting Fraud Working as Part of a Fraud Management Team The Way Forward Ottawa, ON 11/26/2015 Introduction and Objectives The main objectives of today

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013 I. PURPOSE The purpose of this Charter is to formally define LACERS internal audit function s purpose, authority, and responsibility.

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013 I. PURPOSE The purpose of this Charter is to formally define LACERS internal audit function s purpose, authority, and responsibility.

ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud

![ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud](/thumbs/81/83190759.jpg "ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud") ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

CODE OF BUSINESS CONDUCT AND ETHICS

1 ST FRANKLIN FINANCIAL CORPORATION CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics ( Code ) describes the basic principles of conduct that we share as officers

1 ST FRANKLIN FINANCIAL CORPORATION CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics ( Code ) describes the basic principles of conduct that we share as officers

Internal Controls. They Are Everyone s Business. Valdosta State University Office of Internal Audits June 2016

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

August 2010 Guidelines for Managing the Risk of Fraud in Government.

August 2010 Guidelines for Managing the Risk of Fraud in Government www.bcauditor.com T a b l e o f C o n t e n t s The Five Principles Underpinning a Sound Fraud Risk Strategy 2 Principle 1: Understand

August 2010 Guidelines for Managing the Risk of Fraud in Government www.bcauditor.com T a b l e o f C o n t e n t s The Five Principles Underpinning a Sound Fraud Risk Strategy 2 Principle 1: Understand

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

Laurie Beets. PDG 27 th National College & University Bursars & SFS Conference

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

International Standards for the Professional Practice of Internal Auditing (Standards)

") Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

The State of Fraud in Government

Public and private organizations employ tools and applications for data analysis and predictive analytics to battle both the rising incidence of fraud and improper payments and the increasing cost of detecting

Public and private organizations employ tools and applications for data analysis and predictive analytics to battle both the rising incidence of fraud and improper payments and the increasing cost of detecting

OVERVIEW. Common Personality Traits of Fraudsters. Common Sources of Pressure. Changes in Behavior

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Effective implementation of COSO s new anti-fraud guidance

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,

INTERNAL AUDIT EFFECTIVENESS. Conducting Fraud Investigations Conducting Internal Audit

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

Alyssa G. Martin, CPA Brandon Tanous, CIA, Using the COSO CFE, CGAP, CRMA Framework to Develop a Strong and Preventive Control Environment

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Agenda 11/26/13. Updated COSO Framework

Updated COSO Framework Danny M. Goldberg, Founder Agenda COSO Update Overview History/Background Changes Overview Five Control Objectives 17 Control Principles Case Study: Developing a Checklist for Your

Updated COSO Framework Danny M. Goldberg, Founder Agenda COSO Update Overview History/Background Changes Overview Five Control Objectives 17 Control Principles Case Study: Developing a Checklist for Your

Presentation Overview

International Fraud, Ethics and Culture Seen Through the Lens of a Fraud Examiner Steve C. Morang, CFE CCEP CIA CRMA Copyright Steve C. Morang, All rights reserved. Presentation Overview Introduction Understanding

International Fraud, Ethics and Culture Seen Through the Lens of a Fraud Examiner Steve C. Morang, CFE CCEP CIA CRMA Copyright Steve C. Morang, All rights reserved. Presentation Overview Introduction Understanding

Internal Controls for Deans, Directors and Chairs

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

Internal Control Program

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

Common Frauds Found in Not-for- Profit Organizations

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Format and organization of GAGAS Auditor preparation of financials is a significant threat to independence 3 party arrangements in government State

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

PROFILING THE FRAUDSTER

For so long fraud examination has focused on weaknesses in controls and the investigation of transactions that occurred outside of that control environment. Fraud is perpetrated, however, by human beings

For so long fraud examination has focused on weaknesses in controls and the investigation of transactions that occurred outside of that control environment. Fraud is perpetrated, however, by human beings

Frequently Asked Questions About Government Payment Authorities Provincial Comptroller s Office

Purpose of this document Where are copies of this document available? This publication is intended to act as a summary reference for issues that frequently arise concerning Government payment processes.

Purpose of this document Where are copies of this document available? This publication is intended to act as a summary reference for issues that frequently arise concerning Government payment processes.

International Standards for the Professional Practice of Internal Auditing (Standards)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program. Christopher DiLorenzo, CFE, CPA, CIA, CRMA

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Conducting a Fraud Risk Assessment

Conducting a Fraud Risk Assessment Approach, Pitfalls and Recommendations IAAIA Istanbul October 10-13, 2010 Jean Pierre Garitte, CIA, CCSA, CISA, CFE, RFA May 2010 Introduction and Overview Why Conduct

Conducting a Fraud Risk Assessment Approach, Pitfalls and Recommendations IAAIA Istanbul October 10-13, 2010 Jean Pierre Garitte, CIA, CCSA, CISA, CFE, RFA May 2010 Introduction and Overview Why Conduct

Annual Audit and Other Financial Matters

Getting Ready for Your Annual Audit and Other Financial Matters by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Role of the Auditor The role of the independent auditor

Getting Ready for Your Annual Audit and Other Financial Matters by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Role of the Auditor The role of the independent auditor

Fraud and the Small Business Owner

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

FRAUD IN GOVERNMENT AN OPEN DISCUSSION. Presented By William Blend, CPA, CFE

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

Managing the Business Risk of Financial Fraud for Higher Education Providers

Part II Practical lconsiderations i for Managing the Business Risk of Financial Fraud for Higher Education Providers Mark Albers Deloitte FAS LLP April 23, 2010 Discussion Themes I. Fraud Why it Matters

Part II Practical lconsiderations i for Managing the Business Risk of Financial Fraud for Higher Education Providers Mark Albers Deloitte FAS LLP April 23, 2010 Discussion Themes I. Fraud Why it Matters

Final Report. Project (b)

") Internal Audit Department Final Report Project 2011-301(b) Audit Report Sarasota Board of County Commissioners Mark R. Simmons, CIA CFE - Director, Internal Audit Jody Maxwell, CPA Senior Internal Auditor

Internal Audit Department Final Report Project 2011-301(b) Audit Report Sarasota Board of County Commissioners Mark R. Simmons, CIA CFE - Director, Internal Audit Jody Maxwell, CPA Senior Internal Auditor

HCCA AUDIT & COMPLIANCE COMMITTEE CONFERENCE

HCCA AUDIT & COMPLIANCE COMMITTEE CONFERENCE EXTERNAL AUDIT AND THE AUDIT COMMITTEE CHRIS IDEKER, CPA CHRISIDEKER@ALVAREZANDMARSAL.COM February 25 th, 2013 QUESTIONS TO BE ADDRESSED The involvement and

HCCA AUDIT & COMPLIANCE COMMITTEE CONFERENCE EXTERNAL AUDIT AND THE AUDIT COMMITTEE CHRIS IDEKER, CPA CHRISIDEKER@ALVAREZANDMARSAL.COM February 25 th, 2013 QUESTIONS TO BE ADDRESSED The involvement and

Due Diligence And Oversight of Vendors in the Current Regulatory Environment: What Nonprofits Need to Know November 28, 2017

Due Diligence And Oversight of Vendors in the Current Regulatory Environment: What Nonprofits Need to Know November 28, 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of

Due Diligence And Oversight of Vendors in the Current Regulatory Environment: What Nonprofits Need to Know November 28, 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of

Contract Monitoring. Adam Roberts and Jennifer Berrios

Contract Monitoring Adam Roberts and Jennifer Berrios 1 Harvesting Knowledge 2016 Fall Conference October 25-26 Office of Operations John Traylor, Executive Deputy Comptroller Division of Contracts & Expenditures

Contract Monitoring Adam Roberts and Jennifer Berrios 1 Harvesting Knowledge 2016 Fall Conference October 25-26 Office of Operations John Traylor, Executive Deputy Comptroller Division of Contracts & Expenditures

Internal Control System Components. Workers Compensation Board

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Internal Control System Components Workers Compensation Board Report 2015-S-46 October 2015

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Internal Control System Components Workers Compensation Board Report 2015-S-46 October 2015

Auditors Fraud Primer

Auditors Fraud Primer CAST Presentation Dallas Chapter IIA/Dallas Chapter ACFE Joint Meeting November 1, 2011 Cityplace Conference Center Dallas, Texas Ray Lindsay, CPA/CFF CFE Overview Fraud and Occupational

Auditors Fraud Primer CAST Presentation Dallas Chapter IIA/Dallas Chapter ACFE Joint Meeting November 1, 2011 Cityplace Conference Center Dallas, Texas Ray Lindsay, CPA/CFF CFE Overview Fraud and Occupational

Computer Programs and Systems, Inc. Code of Business Conduct and Ethics

(as of January 28, 2013) Introduction This sets forth the guiding principles by which we operate Computer Programs and Systems, Inc. (the Company ) and conduct our daily business with our stockholders,

(as of January 28, 2013) Introduction This sets forth the guiding principles by which we operate Computer Programs and Systems, Inc. (the Company ) and conduct our daily business with our stockholders,

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

DIVISION OF PROBATION AND CORRECTIONAL ALTERNATIVES QUALITY OF INTERNAL CONTROL CERTIFICATION. Report 2008-S-105

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results Summary... 2 Background... 2 Audit Findings and Recommendations...

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results Summary... 2 Background... 2 Audit Findings and Recommendations...

PLEASE complete #1-25 on your green scantron and the rest of them in your blue book.

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

Fraud Risk Management Review March 18, 2010

Fraud Risk Management Review March 18, 2010 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing Office

Fraud Risk Management Review March 18, 2010 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing Office

Policy and Procedures Date: November 5, 2017

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

I. Mission. II. Scope of the Work

CHAPTER: I - ORGANIZATION Page: A.1 MANUAL Appendix A CHARTER FOR THE OFFICE OF THE INSPECTOR GENERAL I. Mission 1. The Office of the Inspector General (OIG) provides oversight of the programmes and operations

CHAPTER: I - ORGANIZATION Page: A.1 MANUAL Appendix A CHARTER FOR THE OFFICE OF THE INSPECTOR GENERAL I. Mission 1. The Office of the Inspector General (OIG) provides oversight of the programmes and operations

Code of Business Conduct and Ethics

Code of Business Conduct and Ethics Table of Contents Purpose... 1 Scope... 1 Policy... 2 Responsibilities... 8 Enforcement... 8 Review and Revision... 8 PURPOSE Pursuant to the Sarbanes-Oxley Act of 2002

Code of Business Conduct and Ethics Table of Contents Purpose... 1 Scope... 1 Policy... 2 Responsibilities... 8 Enforcement... 8 Review and Revision... 8 PURPOSE Pursuant to the Sarbanes-Oxley Act of 2002

INTERNAL CONTROLS ON OUR CAMPUS. Kara Kearney-Saylor Director of Internal Audit, UB

INTERNAL CONTROLS ON OUR CAMPUS Kara Kearney-Saylor Director of Internal Audit, UB 1 Select headlines over the past 12 months.. Dennis Black under investigation for UB spending Former UB VP Dennis Black

INTERNAL CONTROLS ON OUR CAMPUS Kara Kearney-Saylor Director of Internal Audit, UB 1 Select headlines over the past 12 months.. Dennis Black under investigation for UB spending Former UB VP Dennis Black

ACCELERATE DIAGNOSTICS, INC. CODE OF ETHICS FOR CHIEF FINANCIAL OFFICER AND SENIOR FINANCIAL OFFICERS

ACCELERATE DIAGNOSTICS, INC. CODE OF ETHICS FOR CHIEF FINANCIAL OFFICER AND SENIOR FINANCIAL OFFICERS INTRODUCTION: This Code of Ethics is established pursuant to Section 406 of the Sarbanes-Oxley Act

ACCELERATE DIAGNOSTICS, INC. CODE OF ETHICS FOR CHIEF FINANCIAL OFFICER AND SENIOR FINANCIAL OFFICERS INTRODUCTION: This Code of Ethics is established pursuant to Section 406 of the Sarbanes-Oxley Act

Corporate Governor. Providing vision and advice for management, boards of directors and audit committees Winter 2015

Corporate Governor Providing vision and advice for management, boards of directors and audit committees Winter 2015 COSO 2013 framework boosts fraud risk assessment and prevention Fraud is among the most

Corporate Governor Providing vision and advice for management, boards of directors and audit committees Winter 2015 COSO 2013 framework boosts fraud risk assessment and prevention Fraud is among the most

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) ATTRIBUTE STANDARDS 1000 Purpose, Authority and Responsibility The purpose, authority, and responsibility of the internal

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) ATTRIBUTE STANDARDS 1000 Purpose, Authority and Responsibility The purpose, authority, and responsibility of the internal

Fraud in Construction Companies: Lessons From the Trenches

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

FRAUD DETERRENCE AND DETECTION

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

Effective Internal Control Strategies

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

Community Development Districts Workshop

Community Development Districts Workshop Planning & Zoning Department July 15, 2015 District Map 1 Community Development District (CDD) A Community Development District (CDD) means a governmental unit

Community Development Districts Workshop Planning & Zoning Department July 15, 2015 District Map 1 Community Development District (CDD) A Community Development District (CDD) means a governmental unit

2009 ACBO Annual Conference

Developing an Effective Anti Fraud Program 2009 ACBO Annual Conference October 26, 2009 1 Presenters Linda Saddlemire Carroll King Ernie Cooper VLS Fraud Solutions Team Members 2 Carroll King Tapestry

Developing an Effective Anti Fraud Program 2009 ACBO Annual Conference October 26, 2009 1 Presenters Linda Saddlemire Carroll King Ernie Cooper VLS Fraud Solutions Team Members 2 Carroll King Tapestry

Fraud Detection and Prevention

Fraud Detection and Prevention Washington Association of School Business Officials May 7, 2015 Sherrie Ard, CPA, CFE Local Government Performance Center Financial Management Specialist FRAUD 2 Overview

Fraud Detection and Prevention Washington Association of School Business Officials May 7, 2015 Sherrie Ard, CPA, CFE Local Government Performance Center Financial Management Specialist FRAUD 2 Overview

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

RREGULATION ON INTERNAL CONTROLS AND INTERNAL AUDIT FUNCTION IN MICROFINANCE INSTITUTIONS. Article 1 Scope and Purpose

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010) and Articles 98, 103 and 114

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010) and Articles 98, 103 and 114

PKF Forensic & Risk Services. Integrity Issues in the Australian Workforce Part 2 Integrity Corporate Governance 16 May 2017

PKF Forensic & Risk Services Integrity Issues in the Australian Workforce Part 2 Integrity Corporate Governance 16 May 2017 Agenda Integrity Issues in the Australian Workforce Recap on Part 1: Emerging

PKF Forensic & Risk Services Integrity Issues in the Australian Workforce Part 2 Integrity Corporate Governance 16 May 2017 Agenda Integrity Issues in the Australian Workforce Recap on Part 1: Emerging

CODE OF ETHICS AND CONDUCT

CODE OF ETHICS AND CONDUCT PREFACE Green Mountain Power s Code of Ethics and Conduct is about doing the right thing acting honorably, treating each other with respect, and following the law. It s built

CODE OF ETHICS AND CONDUCT PREFACE Green Mountain Power s Code of Ethics and Conduct is about doing the right thing acting honorably, treating each other with respect, and following the law. It s built

NOGDAWINDAMIN FAMILY AND COMMUNITY SERVICES

This dictionary describes the following six functional competencies and four enabling competencies that support the differentiated territory for professional accountants in strategic management accounting:

This dictionary describes the following six functional competencies and four enabling competencies that support the differentiated territory for professional accountants in strategic management accounting:

Kentucky State University Office of Internal Audit

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

RED FLAGS- CONCEPTS AND TECHNIQUES. P r e s e n t e d b y : B y : J o h n E k a d a h

RED FLAGS- CONCEPTS AND TECHNIQUES P r e s e n t e d b y : B y : J o h n E k a d a h Fraud: Introduction Definition of fraud A false representation of a matter of fact, whether by words or by conduct,

RED FLAGS- CONCEPTS AND TECHNIQUES P r e s e n t e d b y : B y : J o h n E k a d a h Fraud: Introduction Definition of fraud A false representation of a matter of fact, whether by words or by conduct,

Global Expectations for Addressing Fraud Risk and the Investigative Process

Global Expectations for Addressing Fraud Risk and the Investigative Process Waheed Alkahtani CFE, CISA, and CCEP-I Saudi Aramco Internal Auditing Special Audits Division Copyright 2014, Saudi Aramco. All

Global Expectations for Addressing Fraud Risk and the Investigative Process Waheed Alkahtani CFE, CISA, and CCEP-I Saudi Aramco Internal Auditing Special Audits Division Copyright 2014, Saudi Aramco. All

OUR CODE OF BUSINESS CONDUCT AND ETHICS

OUR CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that may arise, but

OUR CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that may arise, but

Kerkering, Barberio & Co. Certified Public Accountants

Kerkering, Barberio & Co. Certified Public Accountants 1990 Main Street, Suite 801, Sarasota, FL 34236 6320 Venture Drive, Suite 203, Lakewood Ranch, FL 34202 941 365 4617 461 www.kbgrp.com ESSENTIAL INTERNAL

Kerkering, Barberio & Co. Certified Public Accountants 1990 Main Street, Suite 801, Sarasota, FL 34236 6320 Venture Drive, Suite 203, Lakewood Ranch, FL 34202 941 365 4617 461 www.kbgrp.com ESSENTIAL INTERNAL