Consistent Allocation of Indirect Cost- Your Competitive Advantage. Presented by CliftonLarsonAllen LLP Veit USA

|

|

|

- Osborne Moore

- 6 years ago

- Views:

Transcription

1 Consistent Allocation of Indirect Cost- Your Competitive Advantage Presented by CliftonLarsonAllen LLP Veit USA

2 Profile Bob Sniegowski is a principal and consultant with the CliftonLarsonAllen Construction and Real Estate Group. After working within the construction industry for 24 years, he joined LarsonAllen in He is the principal in charge of CliftonLarsonAllen s construction group consulting area. Experience in serving clients Bob specializes in operations consulting to construction companies, implementation of technology, dispute resolution support services to attorneys and project management training to various contractors and industry groups. He is a frequent presenter on operations management topics to various contractors and industry groups. Educational/professional involvement Bob graduated from Michigan Technological University in 1976 with a Bachelor of Science degree in civil engineering and is a registered professional engineer in the states of Georgia and Minnesota. Bob began his construction career in 1974 as a student engineer for Bechtel Associates, followed by a twenty-two year career with Al Johnson Construction Co. where he held the positions of estimator, senior estimator, office engineer, project engineer, project manager, vice-president and president of two different subsidiary companies. Bob has worked nationally on heavy civil works projects such as navigation locks, dams, bridges and tunnels; as well as regionally on grading, paving, and utility highway projects and commercial building construction projects. Bob is an active member of the Associated General Contractors and its Annual Meeting Steering Committee. R.J. (Bob) Sniegowski, P.E. 2

3 VEIT USA: Headquartered in Rogers, Minnesota Founded 1928 and in third generation of ownership Specialty Contracting: Demolition, Earthwork, Utilities, Foundations Waste Management: C&D/Industrial landfills, roll-off containers, and waste recycling/transfer facilities 600 Employees completing over 500 projects each year Viewpoint user since 2005, CLA Client since 1991 Brian Volk, Controller Maureen Ghassemlou, Cost Accountant Dwayne Kanzler, Systems Administrator veitusa.com

4 Objectives Articulate the case for accurate indirect cost allocation within your organization Identify areas for improving the management and allocation of indirect cost to job costs within your organization Understand the use of Viewpoint functionality and process improvements to allocate indirect cost within your organization 4

5 Best indicator of inaccurate job costing How does this happen? How do you attack the problem? How do you fix it? 5

6 It may come as shock to you but. With some contractors the cost components of the estimates are different than those included as job costs and In many cases, the job cost reports often cannot be easily compared to the original estimate 6

7 Inability to compare estimate to cost leads to... The masking of variances from bid assumptions Difficulty in proving and quantifying changed work Inaccurate forecasts of cost at completion False indication of profitability while in process Confusion and frustration for third party users of the financial statement (banker, surety, customer) 7

8 Why does this happen? No requirement to convert bid to a budget There is no quantifiable process for determining percentage of completion or production Consistent phase or task coding of labor or equipment use is not required or valued Limited understanding of unassigned costs that are driven by the magnitude of job activity Applied rates are not validated by actual cost Critical cost analysis has never been required in the face of competition or dispute 8

9 Gross profit has a limit to its absorption! Gross Profit Unassigned Labor Unabsorbed Equipment Small tools Consumable supplies General and Administrative Expense 9

10 Indirect cost- how big is your cushion? Indirect Cost Unassigned labor, depreciation, Small tools, general inventory, etc. Estimated Cost Equipment O&M Rented Equipment Subcontracts Material Mechanic time cards & P/R Invoices & A/P Invoices & A/P Labor Time cards & payroll 10

11 Indirect costs can be a monster Indirect costs are determined by each company s job costing practices e.g. if field labor is recorded in the g/l as cost of revenue but not in job cost, it is an indirect cost Expenses benefit several jobs and cannot be identified to one or more specific jobs Indirect cost is more closely related to job activity than the expense of operating the business or home office The magnitude of the annual indirect cost varies based on job activity 11

12 Attack the problem Evaluate the big picture Cost of revenue vs. sum of job cost? What is your variance? Drill down on the nature of the variances Magnitude? Types of jobs? Impact on revenue? Transactional work flow? What is the cost ( in time & money) to change? What are the consequences of inaction? Unintended consequences? e.g. Bidding? 12

13 Making the case, making it happen Pick your cause and establish a cost center Forecast the periodic (quarterly or annual) cost Pick the most likely cost driver Determine your allocation method and rate Know your technology (information system) Monitor accuracy of allocation vs. actual cost Assign management responsibility Adjust the rates periodically 13

14 Common indirect cost allocation strategies Indirect Cost Center Payroll Tax & Insurance Major Equipment ownership, service operation e.g. SHOP Unassigned Labor (e.g. General Superintendent or Shop Time ) Allocation Method % of labor or hourly rate Hourly rate based on hours of equipment use Policy of charging time to active projects or include in shop overhead and equipment rate Consumables/Hand Tools % of labor, monthly charge, invoicing from warehouse Inter job transfers or cost sharing-otr Trucking Consistent application of rule, regardless of bid assumption 14

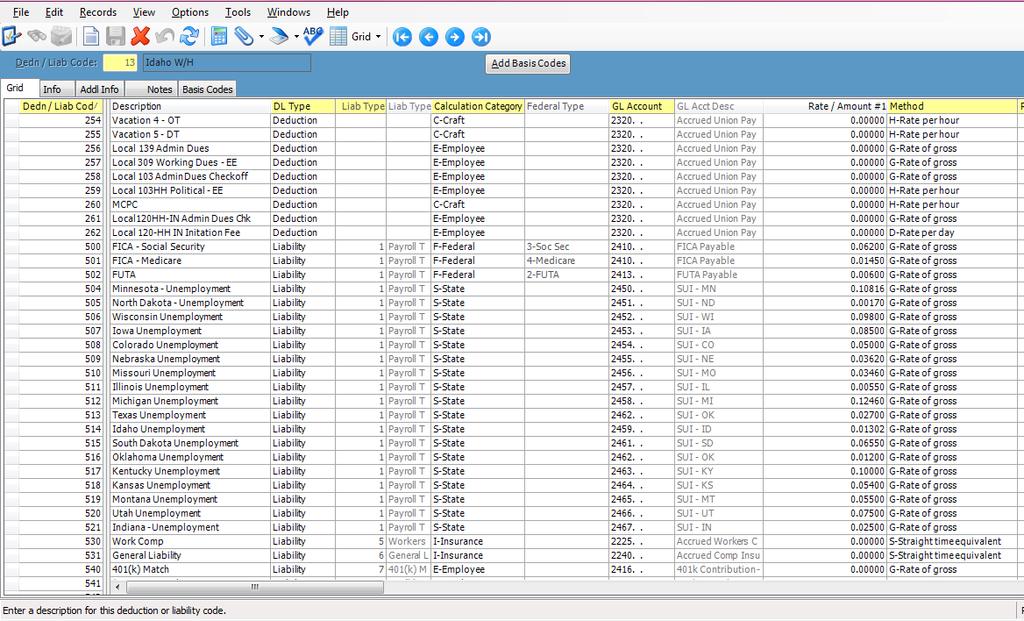

15 Viewpoint functionality can help Job costing labor burdens through PR Setup Union Benefits-Setup PR Craft Classes Payroll Tax-Setup PR Deductions/Liabilities Insurance: worker compensation and commercial liability Equipment cost allocation through EM Revenue Rates applied to equipment hours from payroll entry Use of actual cost by category to establish rates Managing utilization profitability Allocating consumables, supervision and service vehicles to active projects using JC Process Allocations Identifying general ledger cost centers Weekly allocation process 15

16 PR Craft Classes Union Rate Setup

17 PR Craft Classes Union Benefits Setup This is initially setup in PR Craft Master but it will also need to be setup on the employee setup under Craft in order to calculate during payroll.

18 PR Deductions/Liabilities Payroll Tax Setup

19 PR State Insurance Codes - Workers Compensation This is initially setup in PR State Insurance but will also need to be setup on the employee setup under Insurance Code in order to calculate during payroll.

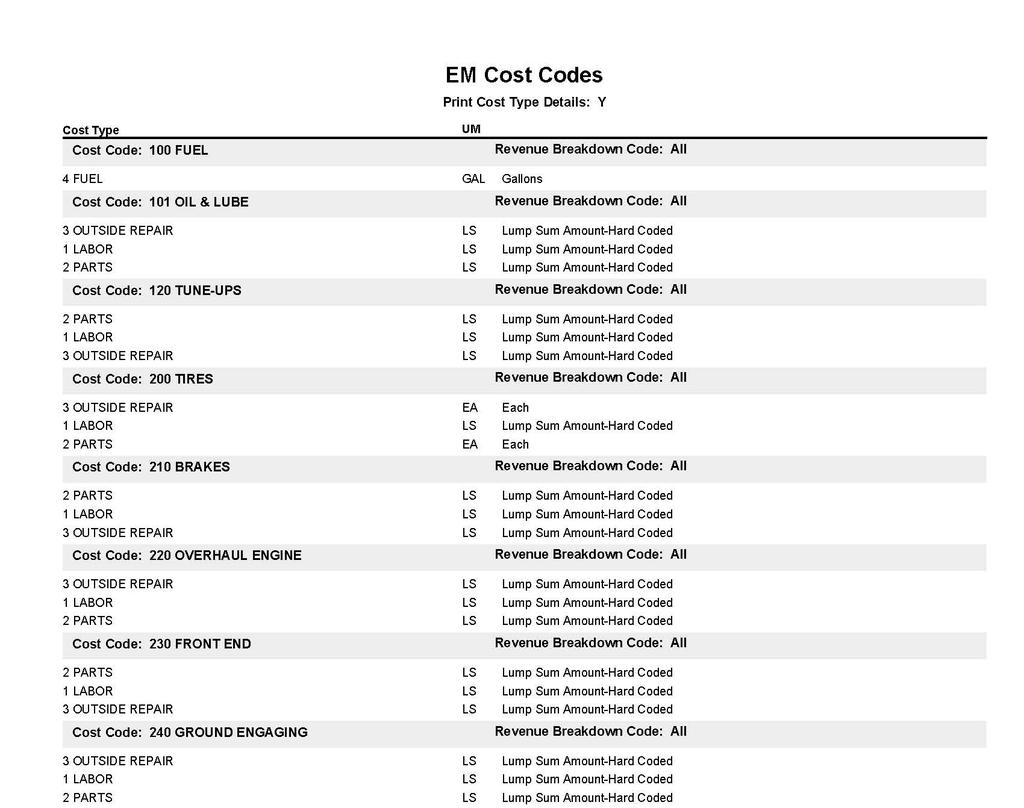

20 Equipment direct cost types Maintenance Repair labor: Mechanic wages, payroll tax, benefits Repair parts (including outsourced repairs) Tires and tracks Operating Cost Fuel Oil, grease, & filters Ground engaging components (cutting edges, bits) Ownership cost (depreciation or operating leases) 20

21 Equipment indirect cost types Shop supervision Shop and repair equipment Interest Transport Insurance Taxes, registration Replacement cost Storage Unassigned labor 21

22

23

24 Forecast annual equipment expense Shop Labor $750,000 17% Depreciation 1,200,000 27% Equipment Repair 900,000 20% Fuel and Lubricants 1,000,000 22% Outside Rentals 250,000 6% Tires 150,000 3% Insurance 100,000 2% Shop Supplies 150,000 3% Total Equipment Expense $4,500, % 24

25 Set rates to fully allocate cost to jobs Units Hours per unit Total Hours Rate Job Cost Allocation Dozer, Small ,000 Dozer, Medium ,000 Dozer, Large ,000 Dump Truck ,000 Excavator, Small ,000 Excavator, Medium ,000 Excavator, Large ,000 Excavator, Jumbo ,000 Grader ,000 Total Allocation to Job Cost 4,597,000 25

26 Setting equipment rates Accurate utilization estimates are essential Use historical costs and utilization as a start Budget to absorb 100% of annual equipment cost within a 10% tolerance +/- Same rate for all equipment in a category Consider reporting inaccuracies in setting rates Use published rental rates as a guide but also use your own good judgment Balance competitive rates and equitable compensation for use by the job/customer 26

27 EM Equipment Setup Individual Piece of Equipment This is to setup a piece of equipment and assign it to a type/category of equipment. You can assign it to a revenue code it should follow (hourly, daily, monthly, etc)

28 EM Revenue Rates by Unit Equipment Rate Setup

29 EM Revenue Rates by Category Equipment Rate Setup

30 Example - Small tools and consumables Determine your allocation method and rate Allocate a percentage of labor $150,000 / $3,500,000 t.l. = 4.2% Allocate a cost per labor hour $150,000 / 120,000 mh = $1.25 per mh Other ideas? 30

31 Example Tools & Supplies Setup These items are setup in Job Cost under JC Cost Allocation Codes. Then they are processed manually through JC Process Cost Allocations. You can run it for a specific date range to allocate the costs. When setting up the allocation codes you can select it to calculate based on costs, hours or revenue. You can also make it specific to a select set of jobs or departments. You can also setup a specific phase code/cost type for the allocation or let it follow where the hours were originally coded.

32 Example Tools & Supplies Cost Allocation So for example you want to allocate costs for tools and supplies for payroll week ending 8/17/13 you can select the date range for the payroll week 8/11/13 8/17/13 and it will calculate the rate you setup with the payroll hours posted and allocate to each job. When you select the allocation code you want to calculate it will show you the date range you last ran that allocation so you don t run it twice for any given time frame.

33 JC Detail Report PR AllocationDetail

34 JC Detail Report JC Allocation Detail

35 In the end-what do we need to know? Are we making money as a company? Credibility Are we as productive as bid? Are all costs in the report? Resource utilization? Are all jobs equally profitable? Better Decisions Are we being fully paid promptly? Cash flow Contracted scope Changed work Timing and cash flow 35

36 Summary The case for accurate indirect cost allocation Knowledge and control of all costs is a competitive advantage Early identification of variances between estimate and cost Credibility with third party users of financial statement Identification of areas for improvement within your organization General and Administrative expense varies annually Under-allocated equipment cost Consumable, small equipment and hand tool expense is uncontrolled Use of Viewpoint functionality and process improvements to allocate indirect costs Establishing a basis for allocation Developing allocation methods and rates Viewpoint functionality to allocate indirect costs

37 Discussion Is indirect cost allocation worth the expense and effort? What is your perspective? Have your project managers resisted indirect cost allocation to their jobs? Why? Is there a complex indirect cost allocation issue that you have solved? How? Benefit? Is there an indirect cost allocation issue that you are reluctant to tackle? Why? Is there an indirect cost allocation issue that you wish had been raised in this session? What is it? 37

38 Questions?

39 Where to go from here Conference Community Vantage Point Self-paced training Knowledge Base Recorded webinar Support Consulting/ Technical Services Contact one or more of us

40 For more information contact: Bob Sniegowski- Job Cost Consultant Direct Brian Volk-Controller Direct Maureen Ghassemlou- Cost Accountant Direct Dwayne Kanzler-Systems Administrator Direct

41 Reminders Complete brief session survey now Complete post event survey to access recordings

42 Consistent Allocation of Indirect Cost- Your Competitive Advantage

Information Systems Tune Up or Major Overhaul?

2015 CliftonLarsonAllen LLP Information Systems Tune Up or Major Overhaul? R.J. (Bob) Sniegowski, PE CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended,

2015 CliftonLarsonAllen LLP Information Systems Tune Up or Major Overhaul? R.J. (Bob) Sniegowski, PE CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended,

HOW TO... Set Up Payroll Allocations

Document Ref: Date: PR-HT014 Oct-02-2014 Document Version: 1.0 Regions: US/CA/AUS Earliest available version of COINS: 10.23 These notes are published as guidelines only. This How to Guide may contain

Document Ref: Date: PR-HT014 Oct-02-2014 Document Version: 1.0 Regions: US/CA/AUS Earliest available version of COINS: 10.23 These notes are published as guidelines only. This How to Guide may contain

Enhancements in Spectrum Last Updated: April 5, 2018

Enhancements in Spectrum 14.24 Last Updated: April 5, 2018 Status: Thunderbirds are GO! AP BI BI BI BI CM JC JC JC MM PO PO PO PR PR PR PS ST ST ST Use Tax Report Supports Work Orders Deep Linking New

Enhancements in Spectrum 14.24 Last Updated: April 5, 2018 Status: Thunderbirds are GO! AP BI BI BI BI CM JC JC JC MM PO PO PO PR PR PR PS ST ST ST Use Tax Report Supports Work Orders Deep Linking New

Enhancements for Last Updated: January 9, 2018

Enhancements for 14.23 Last Updated: January 9, 2018 Status: Released New Branding Changes AP BI BI EK HR IC JC PR PR PR PR PR SDX AP Multi-Cost Center Inter Post Clean Up Rebuild Data Warehouses New Data

Enhancements for 14.23 Last Updated: January 9, 2018 Status: Released New Branding Changes AP BI BI EK HR IC JC PR PR PR PR PR SDX AP Multi-Cost Center Inter Post Clean Up Rebuild Data Warehouses New Data

Financial Transfer Guide DBA Software Inc.

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

PURCHASING AND JOB COSTING FOR CONTRACTORS. Leslie Shiner Owner, Principal of The ShinerGroup

PURCHASING AND JOB COSTING FOR CONTRACTORS Leslie Shiner Owner, Principal of The ShinerGroup Leslie Shiner The ShinerGroup - Owner and Principal Financial & Management Consultant for Contractors MBA in

PURCHASING AND JOB COSTING FOR CONTRACTORS Leslie Shiner Owner, Principal of The ShinerGroup Leslie Shiner The ShinerGroup - Owner and Principal Financial & Management Consultant for Contractors MBA in

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI

, CHENNAI") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION CORPORATE SECRETARYSHIP FOURTH SEMESTER APRIL 2016 BC 4504/BC 5501 COST ACCOUNTING Date: 22-04-2016 Dept. No. Max. : 100 Marks Time:

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION CORPORATE SECRETARYSHIP FOURTH SEMESTER APRIL 2016 BC 4504/BC 5501 COST ACCOUNTING Date: 22-04-2016 Dept. No. Max. : 100 Marks Time:

Job Costing (JC) General Features: Interface with other Systems: System Setup and Maintenance:

General Features: Interface with other Systems: System Setup and Maintenance:") Job Costing (JC) The system serve in setting up and monitoring the progress of projects and individual work orders. The system is based on a work breakdown structure providing the facility to control costs

Job Costing (JC) The system serve in setting up and monitoring the progress of projects and individual work orders. The system is based on a work breakdown structure providing the facility to control costs

Seradex White Paper. Prior to automation the periodic inventory system was commonly used by manufacturing companies.

Seradex White Paper A Discussion of Issues in the Manufacturing OrderStream Lean Accounting Lean Manufacturing and the General Ledger Lean has been applied very successfully to the shop floor with admirable

Seradex White Paper A Discussion of Issues in the Manufacturing OrderStream Lean Accounting Lean Manufacturing and the General Ledger Lean has been applied very successfully to the shop floor with admirable

Managerial Accounting: Making Decisions and Motivating Performance (Datar/Rajan) Chapter 2 An Introduction to Cost Terms and Purposes

Chapter 2 An Introduction to Cost Terms and Purposes") Managerial Accounting: Making Decisions and Motivating Performance (Datar/Rajan) Chapter 2 An Introduction to Cost Terms and Purposes Learning Objective 2-1 1) The cost incurred is: A) actual costs. B)

Managerial Accounting: Making Decisions and Motivating Performance (Datar/Rajan) Chapter 2 An Introduction to Cost Terms and Purposes Learning Objective 2-1 1) The cost incurred is: A) actual costs. B)

CAUSES OF CONSTRUCTION COMPANY COLLAPSE

WEST MICHIGAN CONSTRUCTION FINANCIAL MANAGEMENT ASSOCIATION CAUSES OF CONSTRUCTION COMPANY COLLAPSE February 25, 2016 180 Monroe Ave NW, Suite 2R Grand Rapids, MI 49503 616.233.0020 660 Woodward Ave, Suite

WEST MICHIGAN CONSTRUCTION FINANCIAL MANAGEMENT ASSOCIATION CAUSES OF CONSTRUCTION COMPANY COLLAPSE February 25, 2016 180 Monroe Ave NW, Suite 2R Grand Rapids, MI 49503 616.233.0020 660 Woodward Ave, Suite

What Are Your Sage 100 Contractor Financial Reports Telling You?

What Are Your Sage 100 Contractor Financial Reports Telling You? Presented by: Leslie Shiner Owner, The ShinerGroup L.Shiner@ShinerGroup.com Copyright Notice 2013 Sage Software, Inc. All rights reserved.

What Are Your Sage 100 Contractor Financial Reports Telling You? Presented by: Leslie Shiner Owner, The ShinerGroup L.Shiner@ShinerGroup.com Copyright Notice 2013 Sage Software, Inc. All rights reserved.

Measuring Financial Success at Your Private Duty Agency

Measuring Financial Success at Your Private Duty Agency Mitch Opalski CEO, Synergy HomeCare of Arlington, VA 1 The Data Driven Organization Establish Data Management and Reporting Compare to Financial/Operational

Measuring Financial Success at Your Private Duty Agency Mitch Opalski CEO, Synergy HomeCare of Arlington, VA 1 The Data Driven Organization Establish Data Management and Reporting Compare to Financial/Operational

Full file at

Chapter 2 Job Order Costing ANSWERS TO QUESTIONS 1. The difference between job order costing and process costing relates to the type of product or service the company provides, and whether that product

Chapter 2 Job Order Costing ANSWERS TO QUESTIONS 1. The difference between job order costing and process costing relates to the type of product or service the company provides, and whether that product

No. 8: Avoid Wild Pitches with Overhead Allocation BY MIKE ODE

No. 8: Avoid Wild Pitches with Overhead Allocation BY MIKE ODE No. 8: Avoid Wild Pitches with Overhead Allocation Editor's Note: This is the eighth article in the series, "Software Feature Line-Up," by

No. 8: Avoid Wild Pitches with Overhead Allocation BY MIKE ODE No. 8: Avoid Wild Pitches with Overhead Allocation Editor's Note: This is the eighth article in the series, "Software Feature Line-Up," by

CHAPTER 1 INTRODUCTION

CHAPTER 1 INTRODUCTION Cost is a major factor in most decisions regarding construction, and cost estimates are prepared throughout the planning, design, and construction phases of a construction project,

CHAPTER 1 INTRODUCTION Cost is a major factor in most decisions regarding construction, and cost estimates are prepared throughout the planning, design, and construction phases of a construction project,

The Getting Gross: Make More Gross Margin. Workbook

The Getting Gross: Make More Gross Margin Workbook Getting Gross: How to Make More Gross Margin There are lots of areas of the financials that deserve our attention including revenue, equipment, salaries,

The Getting Gross: Make More Gross Margin Workbook Getting Gross: How to Make More Gross Margin There are lots of areas of the financials that deserve our attention including revenue, equipment, salaries,

Bidding & Estimating Course Syllabus

Bidding & Estimating Course Syllabus 2 Hours (Interactive) Introduction & Overview to Bidding & Estimating Review Sundt/Walsh Abstracting Process Estimating Templates Introduction to Estimating Bid Documents

Bidding & Estimating Course Syllabus 2 Hours (Interactive) Introduction & Overview to Bidding & Estimating Review Sundt/Walsh Abstracting Process Estimating Templates Introduction to Estimating Bid Documents

What is a Successful Company

Welcome 15 Things All Successful Companies Have in Common! We have trained over 14,000 contractors, from coast-to-coast, how to run profitable companies! Bill Kinnard, Vice President What is a Successful

Welcome 15 Things All Successful Companies Have in Common! We have trained over 14,000 contractors, from coast-to-coast, how to run profitable companies! Bill Kinnard, Vice President What is a Successful

INITIAL ASSESSMENT QUESTIONNAIRE

INITIAL ASSESSMENT QUESTIONNAIRE In order to achieve the objectives of the Disadvantaged Business Enterprise Supportive Services Program (DBESS), the New York State Department of Transportation (NYSDOT),

INITIAL ASSESSMENT QUESTIONNAIRE In order to achieve the objectives of the Disadvantaged Business Enterprise Supportive Services Program (DBESS), the New York State Department of Transportation (NYSDOT),

Invoicing Prerequisites and Invoicing

Invoicing Invoicing Prerequisites and Invoicing Table of Contents Invoice Flow... 3 Generating an Invoicing... 4 Prerequisites... 5 The Business... 5 Income Accounts... 7 The Horse... 9 Horse Ownership...

Invoicing Invoicing Prerequisites and Invoicing Table of Contents Invoice Flow... 3 Generating an Invoicing... 4 Prerequisites... 5 The Business... 5 Income Accounts... 7 The Horse... 9 Horse Ownership...

An Accounting Solution You Can Count On

An Accounting Solution You Can Count On To streamline processes and increase profitability, many construction companies are investing in software to manage business more efficiently, cut costs, and improve

An Accounting Solution You Can Count On To streamline processes and increase profitability, many construction companies are investing in software to manage business more efficiently, cut costs, and improve

Microsoft Dynamics SL

Microsoft Dynamics SL 2015 Year-End Close Procedures The information contained herein is the property of MIG & Co. and may not be copied, used or disclosed in whole or In part to any third party except

Microsoft Dynamics SL 2015 Year-End Close Procedures The information contained herein is the property of MIG & Co. and may not be copied, used or disclosed in whole or In part to any third party except

Cost Accounting. Multiple Choice Questions:

Multiple Choice Questions: 1- The Value Chain a- Involves external companies as well as internal activities. b- Is the sequence of business functions in which customer usefulness is added to products or

Multiple Choice Questions: 1- The Value Chain a- Involves external companies as well as internal activities. b- Is the sequence of business functions in which customer usefulness is added to products or

Financial Services Job Summaries

Job Summaries Job 18713 18712 18711 18613 18612 18611 18516 18515 18514 18513 18512 18511 Vice President Finance Senior Associate Vice President Associate Vice President Assistant Vice President Vice Presidents

Job Summaries Job 18713 18712 18711 18613 18612 18611 18516 18515 18514 18513 18512 18511 Vice President Finance Senior Associate Vice President Associate Vice President Assistant Vice President Vice Presidents

B.Com II Year (Hons.) Cost Accounting Model Paper I

Cost Accounting Model Paper I") Max. Marks: 100 B.Com II Year (Hons.) Cost Accounting Model Paper I Durations: 3 Hrs. Attempt all the questions. All Questions are compulsory, each question carry 20 marks. Unit I 1. A Ltd. Is the manufacturer

Max. Marks: 100 B.Com II Year (Hons.) Cost Accounting Model Paper I Durations: 3 Hrs. Attempt all the questions. All Questions are compulsory, each question carry 20 marks. Unit I 1. A Ltd. Is the manufacturer

INTEGRATION GUIDE. Learn about the benefits of integrating your Denali modules

INTEGRATION GUIDE Learn about the benefits of integrating your Denali modules Integration Guide Copyright Notification At Cougar Mountain Software, Inc., we strive to produce high-quality software at reasonable

INTEGRATION GUIDE Learn about the benefits of integrating your Denali modules Integration Guide Copyright Notification At Cougar Mountain Software, Inc., we strive to produce high-quality software at reasonable

Innovations in Business Solutions. Diploma in Accounting and Payroll. Accounting and Payroll I Week 1 to 11

Program Course Duration Diploma in Accounting and Payroll 33 weeks Accounting and Payroll I Week 1 to 11 Introduction to Accounting Fundamentals of Accounting Basic concepts of recording journal entry

Program Course Duration Diploma in Accounting and Payroll 33 weeks Accounting and Payroll I Week 1 to 11 Introduction to Accounting Fundamentals of Accounting Basic concepts of recording journal entry

A GUIDE TO BEST PRACTICES SMALL BUSINESS BASICS:

SMALL BUSINESS BASICS: A GUIDE TO BEST PRACTICES Starting Your Business Controlling Cash Flow Increasing Profitability Growing Your Business Protecting Your Assets Planning for Business Transition Similar

SMALL BUSINESS BASICS: A GUIDE TO BEST PRACTICES Starting Your Business Controlling Cash Flow Increasing Profitability Growing Your Business Protecting Your Assets Planning for Business Transition Similar

Printed Documentation

Printed Documentation Table of Contents GETTING STARTED... 1 Technical Support... 1 Overview... 2 Classifications... 4 Stages... 6 Adding and Deleting Job Folders... 9 Setting Job Defaults... 11 JOBS...

Printed Documentation Table of Contents GETTING STARTED... 1 Technical Support... 1 Overview... 2 Classifications... 4 Stages... 6 Adding and Deleting Job Folders... 9 Setting Job Defaults... 11 JOBS...

W o r k - I n - P r o g r e s s ( W I P ) B a s i c s

B a s i c s") T R A I N I N G P R O G R A M S H e l p i n g C o n t r a c t o r s G r o w P r o f i t a b l y W o r k - I n - P r o g r e s s ( W I P ) B a s i c s PRIVATE WORKSHOP JUST YOUR TEAM Using the WIP Report

T R A I N I N G P R O G R A M S H e l p i n g C o n t r a c t o r s G r o w P r o f i t a b l y W o r k - I n - P r o g r e s s ( W I P ) B a s i c s PRIVATE WORKSHOP JUST YOUR TEAM Using the WIP Report

All of your lines have been muted for the duration of the webinar. Please enter any inquiries in the Question box.

All of your lines have been muted for the duration of the webinar. Please enter any inquiries in the Question box. You can slide the GoToWebinar window closed by clicking the double arrow or orange arrow.

All of your lines have been muted for the duration of the webinar. Please enter any inquiries in the Question box. You can slide the GoToWebinar window closed by clicking the double arrow or orange arrow.

Job Manager for Job Shops

Job Manager for Job Shops What makes Job Shops unique? First, most orders are for a unique item or service. No two Jobs are alike. The Job is a one of a kind job, not a mass production type job. Mass Production

Job Manager for Job Shops What makes Job Shops unique? First, most orders are for a unique item or service. No two Jobs are alike. The Job is a one of a kind job, not a mass production type job. Mass Production

An Introduction to Cost Terms and Purposes

CHAPTER 2 An Introduction to Cost Terms and Purposes Overview This chapter introduces the basic terminology of cost accounting. Communication among managers and management accountants is greatly facilitated

CHAPTER 2 An Introduction to Cost Terms and Purposes Overview This chapter introduces the basic terminology of cost accounting. Communication among managers and management accountants is greatly facilitated

ACCT323, Cost Analysis & Control H Guy Williams, 2005

Costing is a very interesting area because there are many different ways to come up with cost for something. But these principles are generally applicable across the board. Because at any point once you

Costing is a very interesting area because there are many different ways to come up with cost for something. But these principles are generally applicable across the board. Because at any point once you

1. What lists can be imported from Excel spreadsheets, when setting up a QuickBooks Online company?

QuickBooks Online Practice Test (with answers) 1. What lists can be imported from Excel spreadsheets, when setting up a QuickBooks Online company? A) Locations, Classes, Products and Services, and Vendors

QuickBooks Online Practice Test (with answers) 1. What lists can be imported from Excel spreadsheets, when setting up a QuickBooks Online company? A) Locations, Classes, Products and Services, and Vendors

The Tire Industry Economic Impact Study. Methodology and Documentation Prepared for: U.S. Tire Manufacturers Association

The Tire Industry Economic Impact Study Methodology and Documentation Prepared for: U.S. Tire Manufacturers Association By John Dunham & Associates May 12, 2017 Executive Summary: The 2017 U.S. Tire Manufacturers

The Tire Industry Economic Impact Study Methodology and Documentation Prepared for: U.S. Tire Manufacturers Association By John Dunham & Associates May 12, 2017 Executive Summary: The 2017 U.S. Tire Manufacturers

TRAINING OPTIONS. Company-Wide. Accounting

Common Forms & Functionality Webinar (1 hour) For: All users Our growing line of products offers many new and advanced features to assist your entire organization. We ll show you how to navigate the system

Common Forms & Functionality Webinar (1 hour) For: All users Our growing line of products offers many new and advanced features to assist your entire organization. We ll show you how to navigate the system

IM111 INDUSTRIAL RELATIONS

IM111 INDUSTRIAL RELATIONS Cost Analysis What is Cost? Costis the amount of money paid or payable to achieve a specific objective, e.g. the acquirement of materials, property, or services. 2 Is Cost Really

IM111 INDUSTRIAL RELATIONS Cost Analysis What is Cost? Costis the amount of money paid or payable to achieve a specific objective, e.g. the acquirement of materials, property, or services. 2 Is Cost Really

Using the Numbers to Improve Profits. How to use reports and analysis to identify changeable performance, and action steps needed.

Using the Numbers to Improve Profits How to use reports and analysis to identify changeable performance, and action steps needed. Presenter Stephen Gross, CPA, CGMA, CVA, CFE Co-Founder Trusted CFO Solutions

Using the Numbers to Improve Profits How to use reports and analysis to identify changeable performance, and action steps needed. Presenter Stephen Gross, CPA, CGMA, CVA, CFE Co-Founder Trusted CFO Solutions

Sales salaries. Factory repairs. Advertising Office supplies used $ $

E19-4, Determine the total amount of various types of costs. Drew Company reports the following costs and expenses in May. Factory utilities $11.500 $69.100 Depreciation on factory equipment Depreciation

E19-4, Determine the total amount of various types of costs. Drew Company reports the following costs and expenses in May. Factory utilities $11.500 $69.100 Depreciation on factory equipment Depreciation

3712 JACKSON AVENUE, SUITE 331 AUSTIN, TEXAS (512)

") 3712 JACKSON AVENUE, SUITE 331 AUSTIN, TEXAS 78731-6004 (512) 465-7509 WWW.TXDOT.GOV March 3, 2016 Mr. Al Alonzi Division Administrator Federal Highway Administration, Texas Division 300 East 8th Street,

3712 JACKSON AVENUE, SUITE 331 AUSTIN, TEXAS 78731-6004 (512) 465-7509 WWW.TXDOT.GOV March 3, 2016 Mr. Al Alonzi Division Administrator Federal Highway Administration, Texas Division 300 East 8th Street,

SECTION III. ACCOUNTING GUIDELINES AND DOCUMENTS

SECTION III. ACCOUNTING GUIDELINES AND DOCUMENTS A. ACCOUNTING GUIDELINES AND DOCUMENTS APPROVED BY THE MINISTRY OF FINANCE For the purpose of implementing the accounting standards based on IAS, the Ministry

SECTION III. ACCOUNTING GUIDELINES AND DOCUMENTS A. ACCOUNTING GUIDELINES AND DOCUMENTS APPROVED BY THE MINISTRY OF FINANCE For the purpose of implementing the accounting standards based on IAS, the Ministry

Calculation Schema. Setting up the calculation schema in beas. Beas Tutorial. Boyum Solutions IT A/S

Calculation Schema Setting up the calculation schema in beas Boyum Solutions IT A/S Beas Tutorial TABLE OF CONTENTS 1. INTRODUCTION... 3 2. PROCESS... 3 2.1. Master Data Tab... 5 2.2. Overhead Costs Tab...

Calculation Schema Setting up the calculation schema in beas Boyum Solutions IT A/S Beas Tutorial TABLE OF CONTENTS 1. INTRODUCTION... 3 2. PROCESS... 3 2.1. Master Data Tab... 5 2.2. Overhead Costs Tab...

Advanced Accounting (Level 1) Vocabulary/Content

Vocabulary/Content") Unit 1: Introduction to Accounting (Module 1 Chapters 1 & 2) Suggested Duration: about 30 days Advanced Accounting (Level 1) Standards, Big Ideas, and Essential Questions Competencies and Accounting Core

Unit 1: Introduction to Accounting (Module 1 Chapters 1 & 2) Suggested Duration: about 30 days Advanced Accounting (Level 1) Standards, Big Ideas, and Essential Questions Competencies and Accounting Core

Chapter 2 - Basic Managerial Accounting Concepts

1. It is beneficial to assign indirect costs to cost objects. True 2. Price must be greater than cost in order for the firm to generate revenue. False 3. Accumulating costs is the way that costs are measured

1. It is beneficial to assign indirect costs to cost objects. True 2. Price must be greater than cost in order for the firm to generate revenue. False 3. Accumulating costs is the way that costs are measured

Consumer Math Unit Lesson Title Lesson Objectives 1 Basic Math Review Identify the stated goals of the unit and course

Consumer Math Unit Lesson Title Lesson Objectives 1 Basic Math Review Introduction Identify the stated goals of the unit and course Number skills Signed numbers and Measurement scales A consumer application

Consumer Math Unit Lesson Title Lesson Objectives 1 Basic Math Review Introduction Identify the stated goals of the unit and course Number skills Signed numbers and Measurement scales A consumer application

Palmyra Area School District 1125 Park Drive Palmyra, 17078

Palmyra Area School District 1125 Park Drive Palmyra, 17078 Planned Instruction for: Grade Levels: 10, 11, 12 Authors: PALMYRA AREA SCHOOL DISTRICT Overview Course Description gives the student an overall

Palmyra Area School District 1125 Park Drive Palmyra, 17078 Planned Instruction for: Grade Levels: 10, 11, 12 Authors: PALMYRA AREA SCHOOL DISTRICT Overview Course Description gives the student an overall

CHAPTER 20 JOB ORDER COST ACCOUNTING SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements

CHAPTER 20 JOB ORDER COST ACCOUNTING SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 8. 2 K 15. 2 K 22.

CHAPTER 20 JOB ORDER COST ACCOUNTING SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 8. 2 K 15. 2 K 22.

Full file at

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice made to acquire it. True False 2. An expense is an expired cost matched with revenues in a specific

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice made to acquire it. True False 2. An expense is an expired cost matched with revenues in a specific

Sage Master Builder and Your Business

Sage Master Builder and Your Business NOTICE This document and the Sage Master Builder software may be used only in accordance with the accompanying Sage Master Builder End User License Agreement. You

Sage Master Builder and Your Business NOTICE This document and the Sage Master Builder software may be used only in accordance with the accompanying Sage Master Builder End User License Agreement. You

Basic Steps for Starting a Business

1000 Western Avenue PO Box 318 Fergus Falls, MN 56538-0318 DALE UMLAUF, Vice President for Business Development 800 735-2239, 218 739-2239 dale@wcif.org Web site: www.wcif.org Basic Steps for Starting

1000 Western Avenue PO Box 318 Fergus Falls, MN 56538-0318 DALE UMLAUF, Vice President for Business Development 800 735-2239, 218 739-2239 dale@wcif.org Web site: www.wcif.org Basic Steps for Starting

Accounting Master Update for Version 14.2

Accounting Master Update for Version 14.2 Date: October 2014 From: MACC s Product Development Team Re: Version 14.2 Release The following enhancements have been made to the Accounting Master software application.

Accounting Master Update for Version 14.2 Date: October 2014 From: MACC s Product Development Team Re: Version 14.2 Release The following enhancements have been made to the Accounting Master software application.

Full file at

Chapter 02--Job Order Costing Student: 1. Cost accounting systems are used to supply cost data information on costs incurred by a manufacturing process or department. 2. A manufacturer may employ a job

Chapter 02--Job Order Costing Student: 1. Cost accounting systems are used to supply cost data information on costs incurred by a manufacturing process or department. 2. A manufacturer may employ a job

Oregon Regional Pay Survey

2018 Spring Edition Table of Contents Section Page Number Index of Exempt Jobs.......... 1 Exempt Job Detail Reports.. 9 Note: Refer to the Survey Methodology & Demographics report for details regarding

2018 Spring Edition Table of Contents Section Page Number Index of Exempt Jobs.......... 1 Exempt Job Detail Reports.. 9 Note: Refer to the Survey Methodology & Demographics report for details regarding

The Economic Impact of the Auto Care Industry, 2017

The Economic Impact of the Auto Care Industry, 2017 Methodology and Documentation Prepared for The Auto Care Association 7101 Wisconsin Ave. Suite 1300 Bethesda, MD 20814 by John Dunham & Associates, Inc.

The Economic Impact of the Auto Care Industry, 2017 Methodology and Documentation Prepared for The Auto Care Association 7101 Wisconsin Ave. Suite 1300 Bethesda, MD 20814 by John Dunham & Associates, Inc.

Estimating & Bidding. By Charles Vander Kooi

Estimating & Bidding By Charles Vander Kooi 4 Things a Good Estimating System Does For You 1. It enables you to know how every dollar you spend is going to come back to you through the categories on the

Estimating & Bidding By Charles Vander Kooi 4 Things a Good Estimating System Does For You 1. It enables you to know how every dollar you spend is going to come back to you through the categories on the

An accounting perspective: Business insight

An accounting perspective: Business insight Engineers for automobile companies in the United States believe that Japanese manufacturers can build cars for considerably less than their US counterparts.

An accounting perspective: Business insight Engineers for automobile companies in the United States believe that Japanese manufacturers can build cars for considerably less than their US counterparts.

Visual EstiTrack. Understanding Inventory Reconciliation (Supplement) November 2005

November 2005") Visual EstiTrack Understanding Inventory Reconciliation (Supplement) November 2005 OVERVIEW: Methods of Reconciling Inventory Values Most companies that maintain raw material, work in process and finished

Visual EstiTrack Understanding Inventory Reconciliation (Supplement) November 2005 OVERVIEW: Methods of Reconciling Inventory Values Most companies that maintain raw material, work in process and finished

Getting Started: Sage Master Builder and Your Business

Getting Started: Sage Master Builder and Your Business 2006 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein

Getting Started: Sage Master Builder and Your Business 2006 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein

Job Manager for Aerospace and Defense

Job Manager for Aerospace and Defense Aerospace and Defense is very unique. In fact, each Job is unique. You are producing equipment or providing a service and need a way to track the cost of that Job.

Job Manager for Aerospace and Defense Aerospace and Defense is very unique. In fact, each Job is unique. You are producing equipment or providing a service and need a way to track the cost of that Job.

Edw. C. Levy Co. and eam. You spent the bucks on it now get the bang out of it!

Edw. C. Levy Co. and eam You spent the bucks on it now get the bang out of it! Presenter: Cameron R. Frost Steel Service Center business for 9 years Oracle Applications Consultant for 9 years prior to

Edw. C. Levy Co. and eam You spent the bucks on it now get the bang out of it! Presenter: Cameron R. Frost Steel Service Center business for 9 years Oracle Applications Consultant for 9 years prior to

OH WHERE, OH WHERE HAS MY PROFIT GONE? Monte Zwang

OH WHERE, OH WHERE HAS MY PROFIT GONE? Monte Zwang REMEMBER THE BUSINESS PLAN? WHAT WERE YOU EXPECTING? Revenue Growth Profitability What tools were in place to tell you if you were on target or close?

OH WHERE, OH WHERE HAS MY PROFIT GONE? Monte Zwang REMEMBER THE BUSINESS PLAN? WHAT WERE YOU EXPECTING? Revenue Growth Profitability What tools were in place to tell you if you were on target or close?

Who has the Profit and Loss Responsibility in Your Company? Presented by: Fletcher L. Groves, III Vice President SAI Consulting

Who has the Profit and Loss Responsibility in Your Company? Presented by: Fletcher L. Groves, III Vice President SAI Consulting What s behind the Question? The inescapable conclusion that a lot of what

Who has the Profit and Loss Responsibility in Your Company? Presented by: Fletcher L. Groves, III Vice President SAI Consulting What s behind the Question? The inescapable conclusion that a lot of what

Part 1 Study Unit 5. Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Chapter 2--Job Order Costing

Chapter 2--Job Order Costing Student: 1. Cost accounting systems are used to supply cost data information on costs incurred by a manufacturing process or department. 2. A manufacturer may employ a job

Chapter 2--Job Order Costing Student: 1. Cost accounting systems are used to supply cost data information on costs incurred by a manufacturing process or department. 2. A manufacturer may employ a job

Estimating & Bidding. 4 Things a Good Estimating System Does For You. 4 Things a Good Estimating System Does For You. By Charles Vander Kooi

Estimating & Bidding By Charles Vander Kooi 4 Things a Good Estimating System Does For You 1. It enables you to know how every dollar you spend is going to come back to you through the categories on the

Estimating & Bidding By Charles Vander Kooi 4 Things a Good Estimating System Does For You 1. It enables you to know how every dollar you spend is going to come back to you through the categories on the

Tips for Prospective and Experienced Job-Costers BY FRED ODE

Tips for Prospective and Experienced Job-Costers BY FRED ODE Tips for Prospective and Experienced Job-Costers When it comes to accounting for labor costs, most other industries have it easy. If you were

Tips for Prospective and Experienced Job-Costers BY FRED ODE Tips for Prospective and Experienced Job-Costers When it comes to accounting for labor costs, most other industries have it easy. If you were

Cost Engineering and Scope of Work

Cost Engineering and Scope of Work Kul B. Uppal, PE Online Constructor, Inc. Tel. 281-218-9101 Email: kbuppal@onlineconstructor.com Project Scope of Work and Management s Perspective Management has preconceived

Cost Engineering and Scope of Work Kul B. Uppal, PE Online Constructor, Inc. Tel. 281-218-9101 Email: kbuppal@onlineconstructor.com Project Scope of Work and Management s Perspective Management has preconceived

Property Management at Its Best The best customer service starts with great communication.

Property Management at Its Best The best customer service starts with great communication. 30 YEARS OF EXCELLENCE MANAGING RESIDENTIAL PROPERTIES IN NEW YORK CITY Introduction For more than 30 years, The

Property Management at Its Best The best customer service starts with great communication. 30 YEARS OF EXCELLENCE MANAGING RESIDENTIAL PROPERTIES IN NEW YORK CITY Introduction For more than 30 years, The

Operations Advantage Program

The Operations Advantage Program HANDOUT The Operations Advantage Program Delegate and improve the bookkeeping, payroll, and reporting operations of your company with full-service bookkeeping, payroll,

The Operations Advantage Program HANDOUT The Operations Advantage Program Delegate and improve the bookkeeping, payroll, and reporting operations of your company with full-service bookkeeping, payroll,

APPENDIX A - TECHNICAL SPECIFICATIONS. JEA Fleet Services Light Duty Equipment Maintenance and Repair

APPENDIX A - TECHNICAL SPECIFICATIONS JEA Fleet Services Light Duty Equipment Maintenance and Repair 1. GENERAL SCOPE OF WORK This scope of work is looking for a Respondent(s) to provide JEA Fleet Services

APPENDIX A - TECHNICAL SPECIFICATIONS JEA Fleet Services Light Duty Equipment Maintenance and Repair 1. GENERAL SCOPE OF WORK This scope of work is looking for a Respondent(s) to provide JEA Fleet Services

Job Processing 2 Processing Job Expenses

Job Processing 2 Processing Job Expenses Presented By: Carolyn Johnson Table of Contents Job Expenses... 3 Part Expenses... 4 Labor Expenses... 6 Commission Expenses... 8 Miscellaneous Expenses... 9 Job

Job Processing 2 Processing Job Expenses Presented By: Carolyn Johnson Table of Contents Job Expenses... 3 Part Expenses... 4 Labor Expenses... 6 Commission Expenses... 8 Miscellaneous Expenses... 9 Job

ABC Company Recommended Course of Action

ABC Company Recommended Course of Action ABC Company has been utilizing Vantage by Epicor for several months. During the monthly close for November 1999, it was discovered that the G/L accounts for inventory,

ABC Company Recommended Course of Action ABC Company has been utilizing Vantage by Epicor for several months. During the monthly close for November 1999, it was discovered that the G/L accounts for inventory,

Full file at

Chapter 2 Cost Concepts and Behavior rue/false Questions F 1. he cost of an item is the sacrifice made to acquire it. Answer: rue Difficulty: Simple Learning Objective: 1 F 2. A cost can either be an asset

Chapter 2 Cost Concepts and Behavior rue/false Questions F 1. he cost of an item is the sacrifice made to acquire it. Answer: rue Difficulty: Simple Learning Objective: 1 F 2. A cost can either be an asset

OWNER / PRESIDENT / CEO

BY PATRICK SMITH Many people believe, as the saying goes, that you can never please all of the people all of the time. True as that statement might be, successful construction business owners never stop

BY PATRICK SMITH Many people believe, as the saying goes, that you can never please all of the people all of the time. True as that statement might be, successful construction business owners never stop

RG Connect 2016 Microsoft Dynamics GP Tips and Tricks May 13, 2016

RG Connect 2016 Microsoft Dynamics GP Tips and Tricks May 13, 2016 Prepared by Tim Tobias, Carol Livingston, Kayla Schilling, Steve Payne, Elizabeth Bender 600 SW 39 th Street, Suite 250 Renton, WA 98057

RG Connect 2016 Microsoft Dynamics GP Tips and Tricks May 13, 2016 Prepared by Tim Tobias, Carol Livingston, Kayla Schilling, Steve Payne, Elizabeth Bender 600 SW 39 th Street, Suite 250 Renton, WA 98057

Sage MyAssistant - Construction Tasks

Sage MyAssistant - Construction Tasks Accounts Payable Invoice Management Banks with insufficient cash Commitments with unsigned change orders and are selected to be paid Invoices from the same vendor,

Sage MyAssistant - Construction Tasks Accounts Payable Invoice Management Banks with insufficient cash Commitments with unsigned change orders and are selected to be paid Invoices from the same vendor,

B.COM 2 PRIVATE COST ACCOUNTING. B.com-2 PRIVATE Annual Examination COMPILED & SOLVED BY: Jahangeer Khan

B.COM 2 PRIVATE COST ACCOUNTING B.com-2 PRIVATE Annual Examination 20 COMPILED & SOLVED BY: Jahangeer Khan 20 Q.1: MANUFACTURING CONCERN: Consider the following information taken from the books of SAHAB

B.COM 2 PRIVATE COST ACCOUNTING B.com-2 PRIVATE Annual Examination 20 COMPILED & SOLVED BY: Jahangeer Khan 20 Q.1: MANUFACTURING CONCERN: Consider the following information taken from the books of SAHAB

Kianoff & Associates Crystal Clear Reports for Sage 100

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

End of Month Processing

End of Month Processing Ver 040510 Overview: Each of the MAS accounting modules, excluding Bill of Lading, Packaging, Custom Office, Library Master and Report Master require a closing process at or near

End of Month Processing Ver 040510 Overview: Each of the MAS accounting modules, excluding Bill of Lading, Packaging, Custom Office, Library Master and Report Master require a closing process at or near

Understanding Cash Management and Profit Improvement. Washington Small Business Fair September 29, 2018

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 29, 2018 Beth Damis, MBA Director of Finance & Human Resources Penny Arcade, Inc https://www.linkedin.com/in/bethdamis/

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 29, 2018 Beth Damis, MBA Director of Finance & Human Resources Penny Arcade, Inc https://www.linkedin.com/in/bethdamis/

Fleet Maintenance Software

Fleet Maintenance Software Regardless of your industry, PSCS is your best choice in fleet maintenance software. PSCS Fleet Maintenance software is a Windows based client-server application that is easy

Fleet Maintenance Software Regardless of your industry, PSCS is your best choice in fleet maintenance software. PSCS Fleet Maintenance software is a Windows based client-server application that is easy

Please enter the requested information from your 2017 P&L Statement. Water Mitigation $ Fire and Smoke $ Environmental $ Reconstruction $ Other

Part 1 - P&L Please enter the requested information from your 2017 P&L Statement Sales (Residential) Water Mitigation Fire and Smoke Environmental Reconstruction Other Sales (Commercial) Water Mitigation

Part 1 - P&L Please enter the requested information from your 2017 P&L Statement Sales (Residential) Water Mitigation Fire and Smoke Environmental Reconstruction Other Sales (Commercial) Water Mitigation

Gatsby s Accounting System and Policies Designed by Regina Rexrode Copyright - Armond Dalton

Gatsby s Accounting System and Policies a Images used on the front cover and throughout this book were obtained under license from Shutterstock.com 2017, by Armond Dalton Publishers, Inc. All rights reserved.

Gatsby s Accounting System and Policies a Images used on the front cover and throughout this book were obtained under license from Shutterstock.com 2017, by Armond Dalton Publishers, Inc. All rights reserved.

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 9 Lecture - 20 Accounting for Costs Dear students, in our last session we have started

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 9 Lecture - 20 Accounting for Costs Dear students, in our last session we have started

Introduction to Intuit Master Builder

Introduction to Intuit Master Builder Leslie C. Shiner Owner, Principal The ShinerGroup Senior Industry Advisor, Construction Intuit Construction Business Solutions The International Builders Show Orlando,

Introduction to Intuit Master Builder Leslie C. Shiner Owner, Principal The ShinerGroup Senior Industry Advisor, Construction Intuit Construction Business Solutions The International Builders Show Orlando,

This version of the software has been retired. Sage 100. Sage 100 Contractor and Your Business. Contractor (Formerly Sage Master Builder)

") Sage 100 Contractor 2014 (Formerly Sage Master Builder) Sage 100 Contractor and Your Business Version 19.2 This version of the software has been retired NOTICE This is a publication of Sage Software, Inc.

Sage 100 Contractor 2014 (Formerly Sage Master Builder) Sage 100 Contractor and Your Business Version 19.2 This version of the software has been retired NOTICE This is a publication of Sage Software, Inc.

Job Manager for Professional Service Organizations

Job Manager for Professional Service Organizations What makes Professional Service Organizations unique? First, most Professional Service Organizations are tracking their time spent on a Job, and Billing

Job Manager for Professional Service Organizations What makes Professional Service Organizations unique? First, most Professional Service Organizations are tracking their time spent on a Job, and Billing

Economic Impacts Memorandum. December 12, 2017 Revised: January 22, 2018

December 12, 2017 Revised: January 22, 2018 TABLE OF CONTENTS Introduction 2 Background 2 General Methodology 2 Background on IMPLAN Model 3 Description of Economic Impact Output 4 Economic Impacts of

December 12, 2017 Revised: January 22, 2018 TABLE OF CONTENTS Introduction 2 Background 2 General Methodology 2 Background on IMPLAN Model 3 Description of Economic Impact Output 4 Economic Impacts of

1. The cost of an item is the sacrifice of resources made to acquire it. 2. An expense is a cost charged against revenue in an accounting period.

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

Bisan Enterprise. Governmental Edition. A New Dimension in Financial Management Applications

Bisan Enterprise Governmental Edition www.bisan.com A New Dimension in Financial Management Applications Bisan Enterprise Governmental Edition A centralized fully integrated Governmental Solution providing

Bisan Enterprise Governmental Edition www.bisan.com A New Dimension in Financial Management Applications Bisan Enterprise Governmental Edition A centralized fully integrated Governmental Solution providing

Black Hills Utility Holdings, Inc. Cost Allocation Manual

Page 1 of 20 Black Hills Utility Holdings, Inc. Cost Allocation Manual Effective Date: July 14, 2008 Amended: August 1, 2009 Amended: January 1, 2011 Amended: January 1, 2012 Page 2 of 20 Black Hills Utility

Page 1 of 20 Black Hills Utility Holdings, Inc. Cost Allocation Manual Effective Date: July 14, 2008 Amended: August 1, 2009 Amended: January 1, 2011 Amended: January 1, 2012 Page 2 of 20 Black Hills Utility

Inventory Cost Accounting Tips and Tricks. Nick Bergamo, Senior Manager Linda Pei, Senior Manager

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

InterAcct for Job Accounting

InterAcct for Job Accounting Why InterAcct? Job Purchasing Auto Accounting Cost Mark-ups Contract Pricing Budget/Forecast Often the first step once a job has been won is to purchase materials from Suppliers

InterAcct for Job Accounting Why InterAcct? Job Purchasing Auto Accounting Cost Mark-ups Contract Pricing Budget/Forecast Often the first step once a job has been won is to purchase materials from Suppliers

Are Payroll Companies Stealing Your Business?

8 th Annual Independent Insurance Agents of Texas Are Payroll Companies Stealing Your Business? Ed Dittrich Peigo, Owner 105 Pay As You Go Workers Compensation Pay As You Go Workers Compensation 2 What

8 th Annual Independent Insurance Agents of Texas Are Payroll Companies Stealing Your Business? Ed Dittrich Peigo, Owner 105 Pay As You Go Workers Compensation Pay As You Go Workers Compensation 2 What

Arkansas Department of Career Education AgriBusiness Management Rev

Arkansas Department of Education AgriBusiness Management Rev 2017-2018 Arkansas Department of Education AgriBusiness Management Model Framework Course Title Pathway Cluster Course Number 491030 CIP Number

Arkansas Department of Education AgriBusiness Management Rev 2017-2018 Arkansas Department of Education AgriBusiness Management Model Framework Course Title Pathway Cluster Course Number 491030 CIP Number

ACCTG 533, Section 1: Lecture: Profitability Analysis 1. [Slide Content]: Profitability Analysis 1. [Jeanne H. Yamamura]: Profitability Analysis 1.

![ACCTG 533, Section 1: Lecture: Profitability Analysis 1. [Slide Content]: Profitability Analysis 1. [Jeanne H. Yamamura]: Profitability Analysis 1.](/thumbs/83/87114186.jpg "ACCTG 533, Section 1: Lecture: Profitability Analysis 1. [Slide Content]: Profitability Analysis 1. [Jeanne H. Yamamura]: Profitability Analysis 1.") ACCTG 533, Section 1: Lecture: Profitability Analysis 1 Profitability Analysis 1 Profitability Analysis 1. Profitability analysis, also known as differential analysis and relevant cost analysis, builds

ACCTG 533, Section 1: Lecture: Profitability Analysis 1 Profitability Analysis 1 Profitability Analysis 1. Profitability analysis, also known as differential analysis and relevant cost analysis, builds

POCONO MOUNTAIN SCHOOL DISTRICT CURRICULUM

COURSE: Accounting II GRADE(S): 9-12 UNIT: Journalize and posting transactions for a TIMEFRAME: 90 Days Departmentalized Business /Corporation NATIONAL STANDARDS: NATIONAL BUSINESS EDUCATION ASSOCIATION

COURSE: Accounting II GRADE(S): 9-12 UNIT: Journalize and posting transactions for a TIMEFRAME: 90 Days Departmentalized Business /Corporation NATIONAL STANDARDS: NATIONAL BUSINESS EDUCATION ASSOCIATION