Integrating COSO s Fraud Risk Management Guide on an Enterprise Scale

|

|

|

- Robert Anthony

- 6 years ago

- Views:

Transcription

1 Integrating COSO s Fraud Risk Management Guide on an Enterprise Scale September 15, 2017 Vincent Walden Partner EY Atlanta Delores White Director, Internal Audit Southern Company Scott Hulsey Chief Compliance Officer GE Energy

2 Topics for discussion Background on COSO s new anti-fraud guidance Mapping COSO s five anti-fraud principles to your internal controls and analytics program Case examples and company perspectives Resources and reference guides ACFE tools demonstration Dashboard demonstration Page 2

3 COSO s Fraud Risk Management Guide Background & Summary COSO published a Fraud Risk Management Guide at the end of September ACFE is the co-author The Guide builds on Principle 8 of the 2013 internal controls framework Principle 8: The organization considers the potential for fraud in assessing risks to the achievement of objectives. Principle 8 addresses risk assessment, but the new guide addresses fraud risk management 5 Principles of Fraud Risk Management are identified These align to the 17 principles of internal controls from the 2013 Internal Controls Framework Page 3

4 Summary of Fraud Risk Management Components and Principles Control environment Risk assessment Control activities Information and communication Monitoring activities Principle 1 Principle 2 Principle 3 Principle 4 Principle 5 Source: 2016 COSO Fraud Risk Management Guidelines The organization establishes and communicates a fraud risk management program that demonstrates the expectations of the board of directors and senior management and their commitment to high integrity and ethical values regarding managing fraud risk. The organization performs comprehensive fraud risk assessments to identify specific fraud schemes and risks, assess their likelihood and significance, evaluate existing fraud control activities, and implement actions to mitigate residual fraud risks. The organization selects, develops, and deploys preventive and detective fraud control activities to mitigate the risk of fraud events occurring or not being detected in a timely manner. The organization establishes a communication process to obtain information about potential fraud and deploys a coordinated approach to investigation and corrective action to address fraud appropriately and in a timely manner. The organization selects, develops, and performs ongoing evaluations to ascertain whether each of the five principles of fraud risk management is present and functioning and communicates fraud risk management program deficiencies in a timely manner to parties responsible for taking corrective action, including senior management and the board of directors. Page 4

5 2008: First major attempt to increase fraud risk management and fraud risk assessments IIA, ACFE, AICPA Sponsors Fraud risk governance Fraud risk assessment Fraud prevention Fraud detection Fraud investigation and corrective action Page 5

Investigation program 5) Ongoing evaluations and corrective action of the overall program Source: 2016 COSO Fraud Risk Management Guidelines Page")

6 2016 COSO Fraud Risk Management Guidelines 1) Establishment of a fraud risk management program 2) Performs comprehensive fraud risk assessments 3) Selects, develops, and deploys preventive and detective fraud control activities 4) Investigation program 5) Ongoing evaluations and corrective action of the overall program Source: 2016 COSO Fraud Risk Management Guidelines Page 6

7 COSO s Fraud Risk Management Guide Key Points The Guide is not a mandatory standard. But provides a framework that many companies will look to as a resource The Guide s key recommendations: Comprehensive assessment of the risks of fraud, as distinguished from the risks of internal control errors A strategy for proactively using data analysis activities A program leader that reports to the board of directors Page 7

8 Company perspective How did your company utilize the guide? What areas were most helpful? How did the five principles align with current processes? How did management receive the results of your Fraud Risk Assessment? Page 8

9 Page 9 Mapping COSO s five anti-fraud principles to your internal controls and analytics program

10 Control environment Principle 1 Fraud Risk Governance COSO 2013 Framework principles COSO Fraud Risk Management Guide Analytic considerations 1. The organization demonstrates a commitment to integrity and ethical values. 2. The board of directors demonstrates independence from management and exercises oversight of the development and performance of internal control. 3. Management establishes, with board oversight, structures, reporting lines, and appropriate authorities and responsibilities in the pursuit of objectives. 4. The organization demonstrates a commitment to attract, develop, and retain competent individuals in alignment with objectives. 5. The organization holds individuals accountable for their internal control responsibilities in the pursuit of objectives. 1. The organization establishes and communicates a fraud risk management program that demonstrates the expectations of the board of directors and senior management and their commitment to high integrity and ethical values regarding managing fraud risk. Executive reporting Interactive dashboards Targeted analysis around metrics, compliance, and ratios Page 10

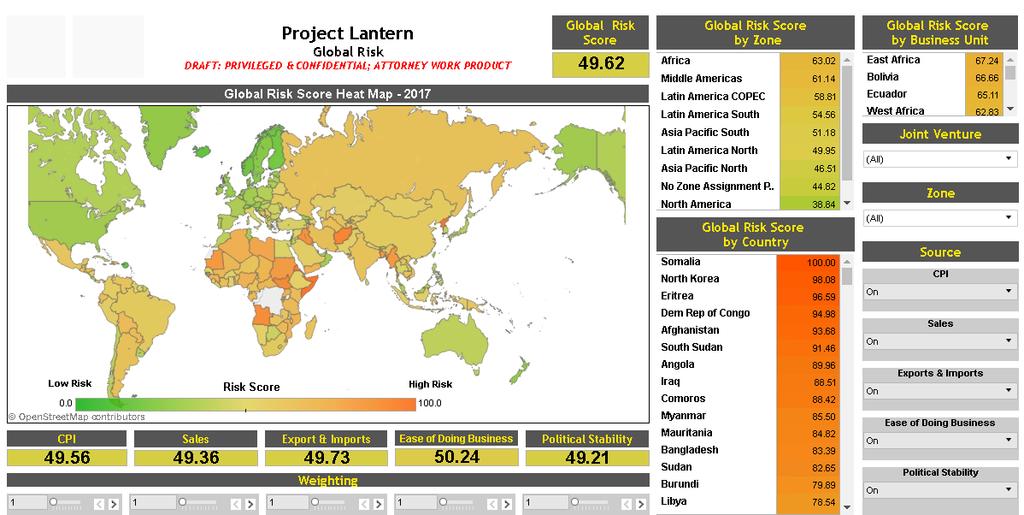

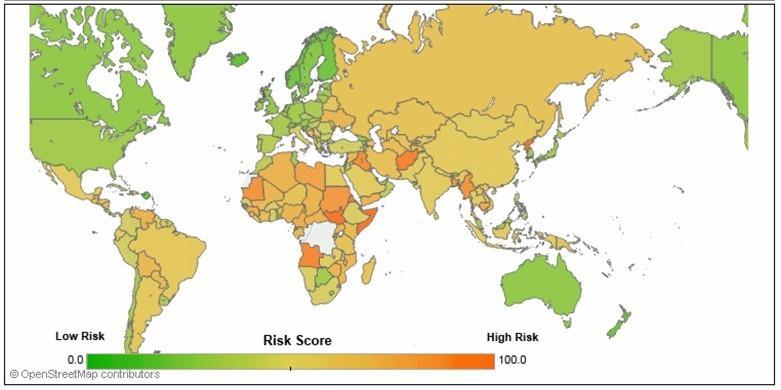

11 Management oversight example: Country risk-ranking dashboard Page 11

12 Risk assessment Principle 2 Fraud Risk Assessment COSO 2013 Framework principles Fraud Risk Management principles Analytic considerations 6. The organization specifies objectives with sufficient clarity to enable the identification and assessment of risks relating to objectives. 7. The organization identifies risks to the achievement of its objectives across the entity and analyzes risks as a basis for determining how the risks should be managed. 8. The organization considers the potential for fraud in assessing risks to the achievement of objectives. 9. The organization identifies and assesses changes that could significantly impact the system of internal control. 2. The organization performs comprehensive fraud risk assessments to identify specific fraud schemes and risks, assess their likelihood and significance, evaluate existing fraud control activities, and implement actions to mitigate residual fraud risks. Surveys and heat maps Media scans and external sources such as industry news Complaints database Page 12

13 Risk assessment example: Combining multiple risk factors to calculate an ambient country score Page 13

14 Control activities Principle 3 Fraud Control Activities COSO 2013 Framework principles Fraud Risk Management principles Analytic considerations 10. The organization selects and develops control activities that contribute to the mitigation of risks to the achievement of objectives to acceptable levels. 11. The organization selects and develops general control activities over technology to support the achievement of objectives. 3. The organization selects, develops, and deploys preventive and detective fraud control activities to mitigate the risk of fraud events occurring or not being detected in a timely manner. ABaC analytics P2P, O2C, T&E, CRM analysis General ledger transaction analysis 12. The organization deploys control activities through policies that establish what is expected and procedures that put policies into action. Page 14

Selected compliance topics Interactive dashboards in")

15 Utilizing data visualization to do more Plan and build tests for: Payment risk scoring Vendor risk scoring High-risk transactions Revenue recognition or sales commissions Conflicts of interests Antitrust/competition Additional tests for enhanced reviews: Inventory management Salaries & payroll Employee travel & entertainment FCPA/UKBA (corruption risks) Selected compliance topics Interactive dashboards in the hands of the business users Page 15

16 Data Visualization: Accounts Payable Monitoring High-risk payment descriptions Page 16

17 Payment systems example: Procure to pay payments focused Analyze payment activity based on a combination of risk factors What were the urgent payments in December? Were there any significant, potentially duplicate payments? What type of charitable contributions were made? Page 17

18 Payment systems example: Risk scoring vendor payments across multiple factors Page 18

19 Information and communication Principle 4 Incident Reporting, Investigation, and Response COSO 2013 Framework principles Fraud Risk Management principles Analytic considerations 13. The organization obtains or generates and uses relevant, quality information to support the functioning of other components of internal control. 14. The organization internally communicates information, including objectives and responsibilities for internal control, necessary to support the functioning of internal control. 15. The organization communicates with external parties regarding matters affecting the functioning of other components of internal control. 4. The organization establishes a communication process to obtain information about potential fraud and deploys a coordinated approach to investigation and corrective action to address fraud appropriately and in a timely manner. Case management Escalation and triage Review workflow management Page 19

20 Investigations tracking example Page 20

21 Monitoring activities Principle 5 Fraud Risk Management Monitoring Activities COSO 2013 Framework principles Fraud Risk Management principles Analytic considerations 16. The organization selects, develops, and performs ongoing and/or separate evaluations to ascertain whether the components of internal control are present and functioning. 17. The organization evaluates and communicates internal control deficiencies in a timely manner to those parties responsible for taking corrective action, including senior management and the board of directors, as appropriate. 5. The organization selects, develops, and performs ongoing evaluations to ascertain whether each of the five principles of fraud risk management is present and functioning and communicates fraud risk management program deficiencies in a timely manner to parties responsible for taking corrective action, including senior management and the board of directors. Investigative procedures Deep dive analysis and communications review Page 21

22 Countries in scope Enterprise monitoring example Data integration strategy Country 1 Country 2 Country 3 Country 4 Country 5 Country 6 Country 7 Data Sources General Ledger Accounts Payable Cash Disbursements Sales / Contra Revenue Vendor / Customer / Employee Master Files Investigations / Case Management Travel & Entertainment Due Diligence Industry Codes Gift Logs Country 8 Country 9 Country 10 Country 11 Country 12 Ambient Risk Urgent Payments Touch Point Vendors Country 13 Compliance Platform Dashboard Modules Global Dashboards Zone and Country Dashboards Investigations & Audit Procure to Pay Payments Duplicate Payments Procure to Pay Vendors High Risk Vendors Country 14 Data Pollution & Integrity Charitable & Political Contributions One Time Vendors Audit External Data AML / Sanctions Travel & Entertainment Order to Cash Page 22

23 Frequent compliance analytics risk areas, particularly in emerging markets Meals & Entertainment Marketing & Events CRM and Sales Information Security/Insider Threat Employee Payroll Sales, Distributor & Margin Analysis Vendor Payments / AP Inventory Capital Projects Third-Party Due Diligence & Watchlist, Shell Companies Accounting Reserves Charity & Donations Emerging monitoring activities may include Social Media Monitoring Advanced Monitoring Mobile Devices Page 23

24 ROI Considerations ACFE s 2016 Report to the Nations Companies without data monitoring/analytics in place suffered a median loss per incident of $200k vs. $92k with data analytics in place. Page 24

25 Monitoring Investigation Performance Metrics (KPIs) Resolution time Investigation costs Repeat incidents Incident location (business unit, operational area, or geography) Value of losses recovered and future losses prevented Corrective actions Internal control remediation, business process remediation, disciplinary action, training, insurance claims, extended investigations, civil actions, criminal referrals **Corrective actions for fraud related incidents is an evaluation component within the Federal Sentencing Guidelines Source: 2016 COSO Fraud Risk Management Guidelines Page 25

26 Page 26 Resources and reference guides

27 ACFE resources demonstration Page 27

28 Company perspective Self Assessment Page 28

29 Thank you Page 29

30 EY Assurance Tax Transactions Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US. Ernst & Young LLP, an equal opportunity employer, values the diversity of our work force and the knowledge of our people Ernst & Young LLP. All Rights Reserved. SCORE no. XX ED none EY is committed to reducing its impact on the environment. This document was printed using recycled paper and vegetable-based ink. This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice. ey.com

Effective implementation of COSO s new anti-fraud guidance

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

Effective implementation of COSO s new anti-fraud guidance In September 2016, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) published a new Fraud Risk Management Guide (Anti-fraud

report that their financial impact of all fraud, corruption and/or money laundering incidents is over per incident

Week of Integrity 2017 1 9 December 2017 Results Integrity Management survey 90% of respondents consider the risk of bribery/corruption and fraud applicable to their business 73% of respondents report

Week of Integrity 2017 1 9 December 2017 Results Integrity Management survey 90% of respondents consider the risk of bribery/corruption and fraud applicable to their business 73% of respondents report

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

Surveillance Program Design and Behavioral Analytics Implementation

Surveillance Program Design and Behavioral Analytics Implementation Scott Jarrell Senior Manager EY #AnalyticsX C o p y r ig ht 201 6, SAS In sti tute In c. Al l r ig hts r ese rve d. EY Fraud Investigation

Surveillance Program Design and Behavioral Analytics Implementation Scott Jarrell Senior Manager EY #AnalyticsX C o p y r ig ht 201 6, SAS In sti tute In c. Al l r ig hts r ese rve d. EY Fraud Investigation

Fraud Risk Management

Fraud Risk Management Fraud Risk Management Overview 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization follow a specific risk management model? If so, which

Fraud Risk Management Fraud Risk Management Overview 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization follow a specific risk management model? If so, which

Fraud Risk Management

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

NYSARC/CP Compliance Seminar: Risk Assessments. May 2, 2016 Robert Hussar and Melissa Zambri

NYSARC/CP Compliance Seminar: Risk Assessments May 2, 2016 Robert Hussar and Melissa Zambri rhussar@barclaydamon.com mzambri@barclaydamon.com Agenda Introductions Compliance Risk Assessment Process OMIG

NYSARC/CP Compliance Seminar: Risk Assessments May 2, 2016 Robert Hussar and Melissa Zambri rhussar@barclaydamon.com mzambri@barclaydamon.com Agenda Introductions Compliance Risk Assessment Process OMIG

Building and operating the UK s infrastructure. Establishing your roadmap to success

Building and operating the UK s infrastructure Establishing your roadmap to success Building for the future The UK government has issued a challenge to the sector to remedy a 50 year backlog in investment

Building and operating the UK s infrastructure Establishing your roadmap to success Building for the future The UK government has issued a challenge to the sector to remedy a 50 year backlog in investment

Managing Fraud Risk: New Professional Guidance

Managing Fraud Risk: New Professional Guidance Mohammed Ahmed & Toby J.F. Bishop Deloitte Financial Advisory Services LLP September 10, 2007 Objectives Make you aware of the new guidance Show how you can

Managing Fraud Risk: New Professional Guidance Mohammed Ahmed & Toby J.F. Bishop Deloitte Financial Advisory Services LLP September 10, 2007 Objectives Make you aware of the new guidance Show how you can

Third Party Risk Management ( TPRM ) Transformation

Transformation") Third Party Risk Management ( TPRM ) Transformation September 20, 2017 Internal use only An introduction to TPRM What is a Third Party relationship? A Third Party relationship is any business arrangement

Third Party Risk Management ( TPRM ) Transformation September 20, 2017 Internal use only An introduction to TPRM What is a Third Party relationship? A Third Party relationship is any business arrangement

Risk Advisory Services Developing your organisation s governance for competitive advantage

Advisory Services Developing your organisation s governance for competitive advantage The Deloitte Advisory Platform of Services can help you to govern your strategic plan to guide your operations measure

Advisory Services Developing your organisation s governance for competitive advantage The Deloitte Advisory Platform of Services can help you to govern your strategic plan to guide your operations measure

A Discussion About Internal Controls February 2016

A Discussion About Internal Controls February 2016 What we will cover today 001 Introductions 002 Defining Internal Controls 003 COSO Internal Controls Integrated Framework 004 Approach to Designing Internal

A Discussion About Internal Controls February 2016 What we will cover today 001 Introductions 002 Defining Internal Controls 003 COSO Internal Controls Integrated Framework 004 Approach to Designing Internal

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Business resilience in the provider care sector. Actively adapting to a changing environment

Business in the provider care sector Actively adapting to a changing environment There has never been a greater need for a company to assess its own business and nowhere is this more true than in the provider

Business in the provider care sector Actively adapting to a changing environment There has never been a greater need for a company to assess its own business and nowhere is this more true than in the provider

Growing opportunity, growing business. EY s financial services practice in ASEAN

Growing opportunity, growing business EY s financial services practice in ASEAN Our team of almost 3,900 financial services professionals across Asia-Pacific and close to 1,700 in ASEAN connects to bring

Growing opportunity, growing business EY s financial services practice in ASEAN Our team of almost 3,900 financial services professionals across Asia-Pacific and close to 1,700 in ASEAN connects to bring

Fisher & Paykel Healthcare Limited Review of Directors Fees Summary of EY report dated 19th June 2017

Fisher & Paykel Healthcare Limited Review of Directors Fees Summary of EY report dated 19th June 2017 1. Introduction Fisher & Paykel Healthcare Corporation Limited (F&P Healthcare) has engaged Ernst &

Fisher & Paykel Healthcare Limited Review of Directors Fees Summary of EY report dated 19th June 2017 1. Introduction Fisher & Paykel Healthcare Corporation Limited (F&P Healthcare) has engaged Ernst &

ESTERLINE ANTI-CORRUPTION PROGRAM CHARTER

ESTERLINE ANTI-CORRUPTION PROGRAM CHARTER Anti-Corruption Program Overview Introduction At Esterline, we win business based on the superiority of our products and services, and never as a result of bribery

ESTERLINE ANTI-CORRUPTION PROGRAM CHARTER Anti-Corruption Program Overview Introduction At Esterline, we win business based on the superiority of our products and services, and never as a result of bribery

Measuring digital advertising revenue to infringing sites

Measuring digital advertising revenue to infringing sites TAG US benchmarking study September 2017 Executive summary Digital advertising has grown at a significant pace over the past several years. Although

Measuring digital advertising revenue to infringing sites TAG US benchmarking study September 2017 Executive summary Digital advertising has grown at a significant pace over the past several years. Although

Leading Practices to Leverage Forensic Data Analytics in Compliance Monitoring and Investigation

Leading Practices to Leverage Forensic Data Analytics in Compliance Monitoring and Investigation Table of contents 1 Proactive Compliance Monitoring 2 EY s First Annual Global Forensic Data Analytics Survey

Leading Practices to Leverage Forensic Data Analytics in Compliance Monitoring and Investigation Table of contents 1 Proactive Compliance Monitoring 2 EY s First Annual Global Forensic Data Analytics Survey

Bearing the Bad News Reporting to the Board on Internal Corruption. Peter Dent, National Leader Deloitte Forensics September 11, 2013

Bearing the Bad News Reporting to the Board on Internal Corruption Peter Dent, National Leader Deloitte Forensics September 11, 2013 Agenda Assessment of Risk in Canada Recent trends in enforcement activity

Bearing the Bad News Reporting to the Board on Internal Corruption Peter Dent, National Leader Deloitte Forensics September 11, 2013 Agenda Assessment of Risk in Canada Recent trends in enforcement activity

Continuous Monitoring: Getting Results Today!

Continuous Monitoring: Getting Results Today! Gerard (Rod) Brennan, PhD, CFE Risk & Internal Control Officer NA, Siemens Corporation Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management,

Continuous Monitoring: Getting Results Today! Gerard (Rod) Brennan, PhD, CFE Risk & Internal Control Officer NA, Siemens Corporation Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management,

COSO Updates and Expectations. IIA San Diego Chapter January 8, 2014

COSO Updates and Expectations IIA San Diego Chapter January 8, 2014 Agenda Overview of 2013 Internal Control-Integrated Framework and Companion Guidance 2013 Framework General Enhancements by Component

COSO Updates and Expectations IIA San Diego Chapter January 8, 2014 Agenda Overview of 2013 Internal Control-Integrated Framework and Companion Guidance 2013 Framework General Enhancements by Component

Present and functioning: Fine-tuning your ICFR using the COSO update

Present and functioning: Fine-tuning your ICFR using the COSO update November 2014 With the COSO s 1992 Control Framework being superseded by the 2013 updated edition on December 15, 2014, now is the time

Present and functioning: Fine-tuning your ICFR using the COSO update November 2014 With the COSO s 1992 Control Framework being superseded by the 2013 updated edition on December 15, 2014, now is the time

Audit Training-of-Trainers Workshop, November 2014, Vienna Components of internal control within organization

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

Session 4C: Model Governance: What Could Possibly Go Wrong? (Part I) Moderator: Dwayne Allen Husbands, FSA, MAAA

Moderator: Dwayne Allen Husbands, FSA, MAAA") Session 4C: Model Governance: What Could Possibly Go Wrong? (Part I) Moderator: Dwayne Allen Husbands, FSA, MAAA Presenters: James Russell Collingwood, ASA, MAAA David Paul, FCAS, MAAA Chad R. Runchey,

Session 4C: Model Governance: What Could Possibly Go Wrong? (Part I) Moderator: Dwayne Allen Husbands, FSA, MAAA Presenters: James Russell Collingwood, ASA, MAAA David Paul, FCAS, MAAA Chad R. Runchey,

Governing the cloud. insights for 5executives. Drive innovation and empower your workforce through responsible adoption of the cloud

insights for 5executives Governing the cloud Drive innovation and empower your workforce through responsible adoption of the cloud Of special interest to Chief information officers Chief information security

insights for 5executives Governing the cloud Drive innovation and empower your workforce through responsible adoption of the cloud Of special interest to Chief information officers Chief information security

COMPLIANCE AT LARGER INSTITUTIONS. November 11 13, Robert F. Roach Chief Compliance Officer New York University

COMPLIANCE AT LARGER INSTITUTIONS November 11 13, 2009 Robert F. Roach Chief Compliance Officer New York University I. Introduction - What is Compliance? We re Watching You! In a University setting, the

COMPLIANCE AT LARGER INSTITUTIONS November 11 13, 2009 Robert F. Roach Chief Compliance Officer New York University I. Introduction - What is Compliance? We re Watching You! In a University setting, the

Internal Audit How the Internal Audit Function Facilitates Internal Controls. Office of the City Auditor City of Tallahassee

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it?

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Risk reduction? Value creation?

The power of culture: Risk reduction? Value creation? Find out what applying a cultural lens to your organisation could reveal Measuring the effectiveness and value of culture and potential risks is one

The power of culture: Risk reduction? Value creation? Find out what applying a cultural lens to your organisation could reveal Measuring the effectiveness and value of culture and potential risks is one

Minimizing fraud exposure with effective ERP segregation of duties controls

Minimizing fraud exposure with effective ERP segregation of duties controls Prepared by: Luke Leaon, Manager, RSM US LLP luke.leaon@rsmus.com, +1 612 629 9072 Adam Harpool, Manager, RSM US LLP adam.harpool@rsmus.com,

Minimizing fraud exposure with effective ERP segregation of duties controls Prepared by: Luke Leaon, Manager, RSM US LLP luke.leaon@rsmus.com, +1 612 629 9072 Adam Harpool, Manager, RSM US LLP adam.harpool@rsmus.com,

Best practice workshop. Training course outline

Best practice workshop Training course outline Overview This course aims to provide participants with a thorough understanding of how to construct a financial model using leading approaches towards model

Best practice workshop Training course outline Overview This course aims to provide participants with a thorough understanding of how to construct a financial model using leading approaches towards model

Synergies between Risk Modeling and Customer Analytics

Synergies between Risk Modeling and Customer Analytics EY SAS Forum, Stockholm 18 September 2014 Lena Mörk and Ramona Klein Agenda 1 2 Introduction Modeling in the financial sector 3 4 5 Consequences from

Synergies between Risk Modeling and Customer Analytics EY SAS Forum, Stockholm 18 September 2014 Lena Mörk and Ramona Klein Agenda 1 2 Introduction Modeling in the financial sector 3 4 5 Consequences from

2013 COSO Internal Control Framework Update. September 5, 2013

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to

Using Transactional Analysis for

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

Global Benchmark. Role of data analytics for internal fraud detection

Global Benchmark Role of data analytics for internal fraud detection 2 overview According to the latest findings in the Ernst & Young Global Forensic Data Analytics Survey 2016 and 2016 ACFE Report to

Global Benchmark Role of data analytics for internal fraud detection 2 overview According to the latest findings in the Ernst & Young Global Forensic Data Analytics Survey 2016 and 2016 ACFE Report to

The winning tax transformation trinity. Data, technology and operations

The winning tax transformation trinity Data, technology and operations Panel Moderators Daryl Blakeway Director South Africa Tax Performance Advisory Anthony Davis Executive Director EMEIA Tax Performance

The winning tax transformation trinity Data, technology and operations Panel Moderators Daryl Blakeway Director South Africa Tax Performance Advisory Anthony Davis Executive Director EMEIA Tax Performance

FINAL ASSESSMENT M.C. DEAN, INC.

FIL ASSESSMENT M.C. DEAN, INC. The following pages contain the detailed scoring for your company based on public information. The following table represents a summary of your scores: Topic Number of questions

FIL ASSESSMENT M.C. DEAN, INC. The following pages contain the detailed scoring for your company based on public information. The following table represents a summary of your scores: Topic Number of questions

Compliance Auditing Done Right

Compliance Auditing Done Right SCCE 10 th Annual Compliance & Ethics Institute September 12, 2011 Scott Avelino Win Swenson Discussion Topics Rationale for Conducting Compliance Audits Identifying Risk

Compliance Auditing Done Right SCCE 10 th Annual Compliance & Ethics Institute September 12, 2011 Scott Avelino Win Swenson Discussion Topics Rationale for Conducting Compliance Audits Identifying Risk

Session 7: Corporate Governance

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Session 7: Corporate Governance New York Bankers Association-Community Bank Auditors Group 2016 Internal Audit Training-June 6-8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

The Road to Continuous Assurance. Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc.

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Agenda Key Drivers for Successful Implementation Technology

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Agenda Key Drivers for Successful Implementation Technology

The trouble with culture:

Top of Mind Issues facing technology companies The trouble with culture: unlocking merger value is really about business behavior Top of Mind 2 Introduction In our experience assisting technology companies

Top of Mind Issues facing technology companies The trouble with culture: unlocking merger value is really about business behavior Top of Mind 2 Introduction In our experience assisting technology companies

CGMA Competency Framework

CGMA Competency Framework Technical skills CGMA Competency Framework 1 Technical skills : This requires a basic understanding of the business structures, operations and financial performance, and includes

CGMA Competency Framework Technical skills CGMA Competency Framework 1 Technical skills : This requires a basic understanding of the business structures, operations and financial performance, and includes

Siemens Compliance System

Siemens Compliance System Due Diligence Procedures hva innebærer det i praksis? ICJ-Norge Oslo, 18. January, 2012 Siemens 2012. All rights reserved Introduction Seite 2 Stakeholder engagement and risk

Siemens Compliance System Due Diligence Procedures hva innebærer det i praksis? ICJ-Norge Oslo, 18. January, 2012 Siemens 2012. All rights reserved Introduction Seite 2 Stakeholder engagement and risk

Quality Assessments what you need to know

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

26th Annual Health Sciences Tax Conference

26th Annual Health Sciences Tax Conference Driving greater tax function effectiveness and December 5, 2016 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

26th Annual Health Sciences Tax Conference Driving greater tax function effectiveness and December 5, 2016 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Developing high performance teams. 2 3 October 2017

Developing high performance teams 2 3 October 2017 Contents Introduction 04 Registration form 06 Introduction Program overview Every individual wants to form part of a winning team, however when dealing

Developing high performance teams 2 3 October 2017 Contents Introduction 04 Registration form 06 Introduction Program overview Every individual wants to form part of a winning team, however when dealing

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

AUDITING. Auditing PAGE 1

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

Effective Risk Management With AML Risk Assessment. January 25, 2017

Effective Risk Management With AML Risk Assessment January 25, 2017 2017 2017 Crowe Crowe Horwath Horwath LLP LLP Agenda Regulatory Trends in Risk Assessment Crowe Approach to Anti-Money Laundering (AML)

Effective Risk Management With AML Risk Assessment January 25, 2017 2017 2017 Crowe Crowe Horwath Horwath LLP LLP Agenda Regulatory Trends in Risk Assessment Crowe Approach to Anti-Money Laundering (AML)

SETTING POLICIES and GUIDELINES for CONDUCTING INTERNAL INVESTIGATIONS

SETTING POLICIES and GUIDELINES for CONDUCTING INTERNAL INVESTIGATIONS Al Gagne, CCEP Director, Ethics & Compliance Textron Systems Corporation SCCE Internal Investigations Workshop November 11-12, 2010

SETTING POLICIES and GUIDELINES for CONDUCTING INTERNAL INVESTIGATIONS Al Gagne, CCEP Director, Ethics & Compliance Textron Systems Corporation SCCE Internal Investigations Workshop November 11-12, 2010

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

Enterprise Risk Management: Developing a Model for Organizational Success. White Paper

Enterprise Risk Management: Developing a Model for Organizational Success White Paper January 2009 Overview Less than a decade ago, Enterprise Risk Management (ERM) was an unfamiliar concept. Today, the

Enterprise Risk Management: Developing a Model for Organizational Success White Paper January 2009 Overview Less than a decade ago, Enterprise Risk Management (ERM) was an unfamiliar concept. Today, the

Are you Fit for Funding

SERVICE OVERVIEW Are you Fit for Funding Helping companies be better prepared to borrow from banks. Delivering Transformation. Together. Contents What makes a company more attractive to a bank? 3 1. Accurate,

SERVICE OVERVIEW Are you Fit for Funding Helping companies be better prepared to borrow from banks. Delivering Transformation. Together. Contents What makes a company more attractive to a bank? 3 1. Accurate,

Peter Fuss Senior Advisory Partner Automotive Ernst & Young

Peter Fuss Senior Advisory Partner Automotive Ernst & Young Shifting from transactional to customercentric Automotive retail in the future Evolving from bricks-and-mortar to an omni-channel strategy Shifting

Peter Fuss Senior Advisory Partner Automotive Ernst & Young Shifting from transactional to customercentric Automotive retail in the future Evolving from bricks-and-mortar to an omni-channel strategy Shifting

Infrastructure and Capital Projects

Infrastructure and Capital Projects Contents Deloitte s Capabilities in Infrastructure and Capital Projects 1 Strategy and Planning 3 Financing and Procurement 4 Project Organisation, Execution and Construction

Infrastructure and Capital Projects Contents Deloitte s Capabilities in Infrastructure and Capital Projects 1 Strategy and Planning 3 Financing and Procurement 4 Project Organisation, Execution and Construction

EY Advisory: Driving business performance

EY Advisory: Driving business performance Advisory EY s consulting practice Helping clients grow, protect and optimize their businesses Page 1 EY Advisory by the numbers 15,000+ Americas 20,000+ EMEIA

EY Advisory: Driving business performance Advisory EY s consulting practice Helping clients grow, protect and optimize their businesses Page 1 EY Advisory by the numbers 15,000+ Americas 20,000+ EMEIA

Crowe Activity Review System

Crowe Activity Review System Quality at the Source Audit Tax Advisory Risk Performance With ever-increasing expectations of review processes from various stakeholders, organizations are under pressure

Crowe Activity Review System Quality at the Source Audit Tax Advisory Risk Performance With ever-increasing expectations of review processes from various stakeholders, organizations are under pressure

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

Catching Fraud During a Recession Through Superior Internal Controls. FICPA s 25 th Annual Accounting Show. J. Stephen Nouss September 29, 2010

Catching Fraud During a Recession Through Superior Internal Controls FICPA s 25 th Annual Accounting Show J. Stephen Nouss September 29, 2010 1 Session Objectives Fraud Facts (2008 Association of Certified

Catching Fraud During a Recession Through Superior Internal Controls FICPA s 25 th Annual Accounting Show J. Stephen Nouss September 29, 2010 1 Session Objectives Fraud Facts (2008 Association of Certified

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Global Expectations for Addressing Fraud Risk and the Investigative Process

Global Expectations for Addressing Fraud Risk and the Investigative Process Waheed Alkahtani CFE, CISA, and CCEP-I Saudi Aramco Internal Auditing Special Audits Division Copyright 2014, Saudi Aramco. All

Global Expectations for Addressing Fraud Risk and the Investigative Process Waheed Alkahtani CFE, CISA, and CCEP-I Saudi Aramco Internal Auditing Special Audits Division Copyright 2014, Saudi Aramco. All

Developing Effective Anti-Corruption Ethics and Compliance Programmes. Sven Biermann

Developing Effective Anti-Corruption Ethics and Compliance Programmes Sven Biermann UNODC Multi-Stakeholder Anti-Corruption Workshop, Sarajevo, 29 September 2017 A multitude of definitions Philanthropy

Developing Effective Anti-Corruption Ethics and Compliance Programmes Sven Biermann UNODC Multi-Stakeholder Anti-Corruption Workshop, Sarajevo, 29 September 2017 A multitude of definitions Philanthropy

The Road to Continuous Assurance. Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc.

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Challenge Statement: Implement a CCM program for the Organization

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Challenge Statement: Implement a CCM program for the Organization

Mitigating Corruption Risk When Acquiring Companies in High-Risk Jurisdictions

Mitigating Corruption Risk When Acquiring Companies in High-Risk Jurisdictions By Bill Olsen, Scott Nemeroff, Dan Reynolds and Alex Koltsov Grant Thornton The hallmark of merger and acquisition activity

Mitigating Corruption Risk When Acquiring Companies in High-Risk Jurisdictions By Bill Olsen, Scott Nemeroff, Dan Reynolds and Alex Koltsov Grant Thornton The hallmark of merger and acquisition activity

IPO Readiness. Sarbanes-Oxley Compliance & Other Considerations. Presented by:

IPO Readiness Sarbanes-Oxley Compliance & Other Considerations Presented by: IPO Readiness Enhanced Financial / Legal compliance SEC / Stock Exchange Compliance Entity Structure / Registration Filing Requirements

IPO Readiness Sarbanes-Oxley Compliance & Other Considerations Presented by: IPO Readiness Enhanced Financial / Legal compliance SEC / Stock Exchange Compliance Entity Structure / Registration Filing Requirements

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

AMETEK, Inc. Code of Ethics and Business Conduct

AMETEK, Inc. Code of Ethics and Business Conduct Code of Ethics and Business Conduct A Message from the Chairman of the Board and Chief Executive Officer Dear AMETEK Colleague: AMETEK has been in business

AMETEK, Inc. Code of Ethics and Business Conduct Code of Ethics and Business Conduct A Message from the Chairman of the Board and Chief Executive Officer Dear AMETEK Colleague: AMETEK has been in business

Audit of Entity Level Controls

Unclassified Internal Audit Services Branch Audit of Entity Level Controls February 2014 SP-606-03-14E You can download this publication by going online: http://www12.hrsdc.gc.ca This document is available

Unclassified Internal Audit Services Branch Audit of Entity Level Controls February 2014 SP-606-03-14E You can download this publication by going online: http://www12.hrsdc.gc.ca This document is available

Triple C Housing, Inc. Compliance Plan

Triple C Housing, Inc. Compliance Plan Adopted by Board of Directors on draft November 13, 2014 Overview Triple C Housing, Inc. is committed to its consumers, employees, contractual providers, vendors,

Triple C Housing, Inc. Compliance Plan Adopted by Board of Directors on draft November 13, 2014 Overview Triple C Housing, Inc. is committed to its consumers, employees, contractual providers, vendors,

It s time to revisit your anti-corruption compliance program How to design an effective and defensible compliance program in response to global trends

It s time to revisit your anti-corruption compliance program How to design an effective and defensible compliance program in response to global trends Many legal and compliance officers are revisiting

It s time to revisit your anti-corruption compliance program How to design an effective and defensible compliance program in response to global trends Many legal and compliance officers are revisiting

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

Introduction. Key points of the recent ODPC guidance, and the Article 29 working group guidance

The Role of the Data Protection Officer Key points of the recent ODPC guidance and the Article 29 Working Group Guidance September 2017 00 Introduction Key points of the recent ODPC guidance, and the Article

The Role of the Data Protection Officer Key points of the recent ODPC guidance and the Article 29 Working Group Guidance September 2017 00 Introduction Key points of the recent ODPC guidance, and the Article

Internal Control Integrated Framework. May 2013

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

MiFID II Extraterritorial Impacts. Product Manufacturing and Distribution

MiFID II Extraterritorial Impacts Product Manufacturing and Distribution Speakers Marie Gervacio, Executive Director, EY Advisory Services Limited Marie has over 17 years of advisory and assurance experience

MiFID II Extraterritorial Impacts Product Manufacturing and Distribution Speakers Marie Gervacio, Executive Director, EY Advisory Services Limited Marie has over 17 years of advisory and assurance experience

Using Data Analytics as a Management Tool to Identify Organizational Risks

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

Success peak performance and personal branding December 2017

Success peak performance and personal branding 10 11 December 2017 Day 1 The psychology of success and peak performance The definition of success The barriers to success Harnessing your inner most power

Success peak performance and personal branding 10 11 December 2017 Day 1 The psychology of success and peak performance The definition of success The barriers to success Harnessing your inner most power

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Executive Steering Committee Meeting. Department of Revenue Building 2, Room 1250 July 27, 2016

Executive Steering Committee Meeting Department of Revenue Building 2, Room 1250 Roll Call and Opening Remarks Facilitator: Robert (Budd) Kneip, Chair Review of June 2016 Meeting Minutes Facilitator: Robert

Executive Steering Committee Meeting Department of Revenue Building 2, Room 1250 Roll Call and Opening Remarks Facilitator: Robert (Budd) Kneip, Chair Review of June 2016 Meeting Minutes Facilitator: Robert

Next Generation Controls(NGC) Moving towards a Robust Control Framework. August Risk

Moving towards a Robust Control Framework. August Risk") (NGC) Moving towards a Robust Control August 2016 Risk Brochure / report title goes here Section title goes here Background Today, in an environment generally distrustful of businesses, regulatory and

(NGC) Moving towards a Robust Control August 2016 Risk Brochure / report title goes here Section title goes here Background Today, in an environment generally distrustful of businesses, regulatory and

The Future of Accounts Payable

May 7-9, 2017 Disney s Yacht & Beach Club Resorts, Florida The Future of Accounts Payable Presented by: Mark Brousseau May 7-9, 2017 Disney s Yacht & Beach Club Resorts, Florida Accounts Payable Automation

May 7-9, 2017 Disney s Yacht & Beach Club Resorts, Florida The Future of Accounts Payable Presented by: Mark Brousseau May 7-9, 2017 Disney s Yacht & Beach Club Resorts, Florida Accounts Payable Automation

Enterprise intelligence in modern shipping

Enterprise intelligence in modern shipping Leveraging commercial and cost performance with data analytics 7th Capital Link Greek Shipping Forum 16 February 2016 Agenda I. What is Enterprise Intelligence?

Enterprise intelligence in modern shipping Leveraging commercial and cost performance with data analytics 7th Capital Link Greek Shipping Forum 16 February 2016 Agenda I. What is Enterprise Intelligence?

Protecting Fixed Assets: Internal Controls for Non Profits

Protecting Fixed Assets: Internal Controls for Non Profits 25 September 2012 Community Sector Council Newfoundland and Labrador (CSC) Darlene Scott, Senior Program Associate darlenescott@cscnl.ca www.communitysector.nl.ca

Protecting Fixed Assets: Internal Controls for Non Profits 25 September 2012 Community Sector Council Newfoundland and Labrador (CSC) Darlene Scott, Senior Program Associate darlenescott@cscnl.ca www.communitysector.nl.ca

Measuring Compliance Program Effectiveness

Measuring Compliance Program Effectiveness Measuring Compliance Program Effectiveness: A Resource Guide HCCA Hawaii Regional Debbie Troklus, CHC-F, CCEP-F, CCEP-I, CHRC, CHPC Aegis Compliance and Ethics

Measuring Compliance Program Effectiveness Measuring Compliance Program Effectiveness: A Resource Guide HCCA Hawaii Regional Debbie Troklus, CHC-F, CCEP-F, CCEP-I, CHRC, CHPC Aegis Compliance and Ethics

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

FCPA COMPLIANCE PROGRAMS

FCPA COMPLIANCE PROGRAMS JIMMY S. PAPPAS INTERNATIONAL INTERNAL INVESTIGATIONS CONFERENCE FRANKFURT, GERMANY DECEMBER 7, 2012 FCPA COMPLIANCE PROGRAMS - OVERVIEW! An effective compliance program is: A

FCPA COMPLIANCE PROGRAMS JIMMY S. PAPPAS INTERNATIONAL INTERNAL INVESTIGATIONS CONFERENCE FRANKFURT, GERMANY DECEMBER 7, 2012 FCPA COMPLIANCE PROGRAMS - OVERVIEW! An effective compliance program is: A

Comprehensive Enterprise Solution for Compliance and Risk Monitoring

Comprehensive Enterprise Solution for Compliance and Risk Monitoring 30 Wall Street, 8th Floor New York, NY 10005 E inquiries@surveil-lens.com T (212) 804-5734 F (212) 943-2300 UNIQUE FEATURES OF SURVEILLENS

Comprehensive Enterprise Solution for Compliance and Risk Monitoring 30 Wall Street, 8th Floor New York, NY 10005 E inquiries@surveil-lens.com T (212) 804-5734 F (212) 943-2300 UNIQUE FEATURES OF SURVEILLENS

Brexit: considerations for your Internal Audit operating model

Brexit: considerations for your Internal Audit operating model Next steps Brexit: considerations for your Internal Audit operating model 1 Brexit: considerations for your Internal Audit operating model

Brexit: considerations for your Internal Audit operating model Next steps Brexit: considerations for your Internal Audit operating model 1 Brexit: considerations for your Internal Audit operating model

Internal Audit Procurement Policies and Controls

Internal Audit Procurement Policies and Controls Melissa Aw Yong 10 October 2012 SAA Global Education Centre Pte Ltd Seminar 6/7 111 Somerset Road, #06-01/02 TripleOne Somerset Singapore 238164 Agenda

Internal Audit Procurement Policies and Controls Melissa Aw Yong 10 October 2012 SAA Global Education Centre Pte Ltd Seminar 6/7 111 Somerset Road, #06-01/02 TripleOne Somerset Singapore 238164 Agenda

ATTACHMENT C CORPORATE COMPLIANCE PROGRAM

ATTACHMENT C CORPORATE COMPLIANCE PROGRAM In order to address deficiencies in its internal controls, policies, and procedures regarding compliance with the Foreign Corrupt Practices Act ( FCPA ), 15 U.S.C.

ATTACHMENT C CORPORATE COMPLIANCE PROGRAM In order to address deficiencies in its internal controls, policies, and procedures regarding compliance with the Foreign Corrupt Practices Act ( FCPA ), 15 U.S.C.

Compliance Plans. Kelly S. McIntosh July 20, 2017

Compliance Plans Kelly S. McIntosh July 20, 2017 Roadmap The importance of compliance and compliance programs Common compliance issues know your risk areas! Guidance for drafting or updating your compliance

Compliance Plans Kelly S. McIntosh July 20, 2017 Roadmap The importance of compliance and compliance programs Common compliance issues know your risk areas! Guidance for drafting or updating your compliance

KPMG Intelligent Diligence An automated approach to KYC. kpmg.com/uk

KPMGIntelligence Diligence 0 KPMG Intelligent Diligence An automated approach to KYC kpmg.com/uk KPMGIntelligence Diligence 1 Key Features KPMG Intelligent Diligence( KPMG ID ) replicatesthe cognitive

KPMGIntelligence Diligence 0 KPMG Intelligent Diligence An automated approach to KYC kpmg.com/uk KPMGIntelligence Diligence 1 Key Features KPMG Intelligent Diligence( KPMG ID ) replicatesthe cognitive

Compliance Program Effectiveness Guide

Compliance Program Effectiveness Guide June 2017 This Guide is a comparison of: Compliance Program Elements New York State, Social Services Law 363-D Office of Inspector General (OIG) Compliance Program

Compliance Program Effectiveness Guide June 2017 This Guide is a comparison of: Compliance Program Elements New York State, Social Services Law 363-D Office of Inspector General (OIG) Compliance Program

Internal Controls In Higher Education

Internal Controls In Higher Education A Queen s University Experience June 2016 Caroline Davis, Vice-Principal (Finance and Administration) Queen s University Carol Devenny Partner - PricewaterhouseCoopers

Internal Controls In Higher Education A Queen s University Experience June 2016 Caroline Davis, Vice-Principal (Finance and Administration) Queen s University Carol Devenny Partner - PricewaterhouseCoopers

A Data Driven Company How Deloitte transformed itself. QlikView Business Discovery World Tour Eindhoven, 9 October 2013

A Data Driven Company How Deloitte transformed itself QlikView Business Discovery World Tour Eindhoven, 9 October 2013 Eponential growth of data will create demand for Data Analytics, which Deloitte has

A Data Driven Company How Deloitte transformed itself QlikView Business Discovery World Tour Eindhoven, 9 October 2013 Eponential growth of data will create demand for Data Analytics, which Deloitte has

Article from: CompAct. April 2013 Issue No. 47

Article from: CompAct April 2013 Issue No. 47 Overview of Programmatic Framework and Key Considerations Key elements Description Items to consider Definition and identification of EUCs The statement that

Article from: CompAct April 2013 Issue No. 47 Overview of Programmatic Framework and Key Considerations Key elements Description Items to consider Definition and identification of EUCs The statement that

Accenture Profit Recovery and Analytics

Business Process Outsourcing Accenture Profit Recovery and Analytics Delivering High Performance through Profit Recovery Accenture: Delivering high performance through profit recovery Are you leaving money

Business Process Outsourcing Accenture Profit Recovery and Analytics Delivering High Performance through Profit Recovery Accenture: Delivering high performance through profit recovery Are you leaving money

Global Enterprise Model (GEM) for Utilities

for Utilities") Business Process Outsourcing the way we do it Global Enterprise Model (GEM) for Utilities Transforming business processes to drive greater efficiencies, reduce operational costs and improve the customer

Business Process Outsourcing the way we do it Global Enterprise Model (GEM) for Utilities Transforming business processes to drive greater efficiencies, reduce operational costs and improve the customer