COSO Internal Control Integrated Framework Public Exposure Feedback Questions, December 2011

|

|

|

- Lucinda Harper

- 6 years ago

- Views:

Transcription

1 March 31, 2012 Response ed to RE: COSO Internal Control Integrated Framework Public Exposure Feedback Questions, December 2011 Dear Sir/Madam: The Institute of Internal Auditors (IIA), as the standards setting body for the international profession of internal auditing, has a passion for guiding organizations to achieve the highest standards of governance, risk management, and control all designed for the sole purpose of fulfilling an organization s strategic objectives in the most efficient, effective, and sustainable manner possible. For those reasons, The IIA became an original member of the Committee of Sponsoring Organizations (COSO) and continues to this day to champion the governance principles that our COSO partners espouse. The IIA s President and Chief Executive Officer serves on the COSO board and we have volunteer leaders serving on the Advisory Council and in other supporting capacities. Given the impact that the Internal Control Integrated Framework (Framework) has had on governance, risk management, and control efforts coupled with the U.S. based Sarbanes-Oxley regulations which require U.S. public companies to align their controls to a generally accepted control framework, our Institutes leaders have been resolute in offering our broad membership an opportunity to respond to the exposure draft in a more direct manner. As The IIA s Chairman of the Board, I am pleased to offer our membership s perspectives on the exposure draft. We applaud the COSO team s efforts and transparency in sharing the basis for revisions, rationale behind the writing team s approach, and opportunity for submission of comments. Given the foundational nature of the Framework, as well as widely differing opinions on the style and nature of principles based documents, we want to acknowledge the difficulty that the writing team and Advisory Council have in balancing theoretical and practical objectives. Our comments are based on discussions conducted by a core team of internal audit professionals who serve on The IIA s Professional Issues Committee (PIC). These professionals consist of Chartered Accountants, Certified Public Accountants, and Certified Internal Auditors who have worked in the public and private sectors, internal and external auditing, and small, medium, and large domestic and international companies. PIC is responsible for all exposure draft responses on governance, risk management, control, compliance, and auditing topics from regulatory and standard setting bodies around the world. In addition, PIC drafts the practice advisories and practice guides which are the basis for the implementation of the International Standards for the Professional Practice of Internal Auditing (Standards). To ensure a broad representation from The IIA s membership, PIC members participated in forums in several cities across the U.S., 1

2 solicited input from our membership and chief audit executives worldwide, as well as solicited and received input from The IIA s Institutes in other countries. The following are our principal comments and observations. Detailed responses to the questions posed in the exposure document, and other matters related to the document, can be found in Attachment A. 1. The first concern is the decision not to further integrate strategic objectives and risk management into the Framework. Our team was concerned by the separation of broader enterprise risk concepts from internal control given that risk assessment is a fundamental necessity for control development. Controls mitigate risks, risk mitigation optimizes execution of operations objectives, and operations objectives achieve strategic objectives (strategic goals). We reference the following section in paragraph 69: Setting the overall level of acceptable risk and associated risk appetite is part of strategic planning and enterprise risk management, not part of internal control. Similarly, setting risk tolerance levels in relation to specific objectives is not part of internal control. A lack of risk tolerance setting can limit an assessment of whether a control is appropriately designed to mitigate a risk. While the setting of risk tolerance is a management decision, the process and action of setting a risk tolerance is essential to the overall integrated Framework. The following principles speak to this alignment: #6 - The organization specifies objectives with sufficient clarity to enable the identification and assessment of risks relating to objectives. #7 - The organization identifies risks to the achievement of its objectives across the entity and analyzes risks as a basis for determining how the risks should be managed. #10 - The organization selects and develops control activities that contribute to the mitigation of risks to the achievement of objectives to acceptable levels. While some of our members would like the writing team to completely merge the COSO ERM concepts into this document, there are also members who believe that strategy setting and enterprise risk management should be kept as separate concepts given the maturity of ERM in many organizations. Our final consensus is that there is an opportunity for COSO to further integrate best practices for governance, risk management and control disciplines while remaining risk-framework agnostic and without mandating additional requirements on organizations which may wish to focus solely on the objective of internal control over financial reporting. Such an approach balances the current need to refresh the Framework and allows organizations to utilize the Framework in the future in ways that the COSO board cannot anticipate today. 2

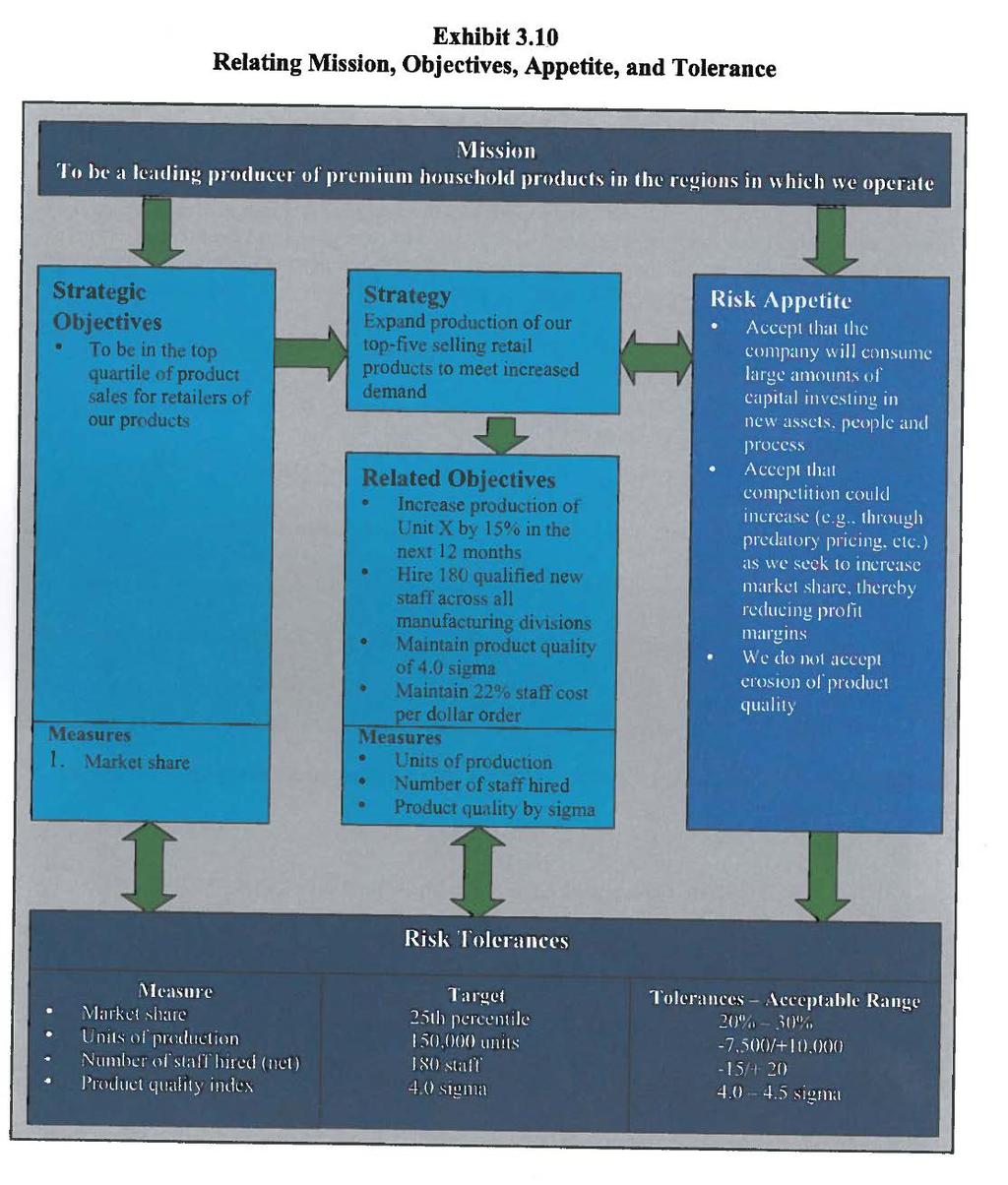

3 This approach is integral to establishing efficient and effective risk based controls tailored to the entity s needs. Such efforts increase the value of the refreshed Framework and facilitate integration with other existing risk and control practices, particularly for users outside the U.S. who are considering frameworks like ISO or Solvency II. The refreshed Framework should: Speak fully to strategic objective setting and enterprise risk management, laying out how they are part of the overall organization governance framework. Clarify the degree to which strategic objective setting and enterprise risk management are inputs to the internal control Framework. Clarify the degree to which a lack of strategic objective setting and ERM efforts impacts the assessment of internal control. Clarify the degree to which an assessment of principle 6 which states, The organization specifies objectives with sufficient clarity to enable the identification and assessment of risks relating to objectives is dependent upon validation that such operational objectives as described are in alignment with strategic objectives. This may be addressed outside the Framework. Consider incorporating an updated graph (see Exhibit 3.10 in Attachment A) from the COSO ERM-Integrated Framework Application Techniques Manual as a reference to explain how the various components of strategy setting, risk management, and control apply. The COSO writing team should ensure that the recent paper on Risk Appetite and any changes to the Framework are appropriately reflected. 2. The second concern involves the principles and attributes in the document. IIA members clearly believe that principles based frameworks are a far better approach for tailoring the development and evaluation of internal controls to the specific objectives and circumstances of each organization. The principles and attributes in the draft were generally considered comprehensive and of value in the understanding of the components of internal control. The new draft emphasizes judgment in the evaluation of internal control effectiveness overall, as components are interrelated, yet it requires not only an overall evaluation of each component but additionally of each principle and attribute. This encourages management and auditors to think in silos within each element of the Framework versus taking a holistic approach to the evaluation of internal control over a given objective. This may encourage a checklist approach to assessing internal control rather than the use of judgment based on the significance of the objective, activity, or risk compared to the more relevant principles and controls that are working effectively versus a simple validation of existence of the principles and attributes outlined in the Framework. Paragraph 78 of the Framework states, When a principle is deemed not to be present or functioning, an internal control deficiency exists. Internal auditing practitioners are concerned about the potential prescriptive nature of a process that results in a deficiency if any of the 17 principles are partially implemented or if any one principle is not in place in an entity s system of internal controls. Evaluating every principle for all key processes may not be necessary. 3

4 We believe that the Framework should guide the evaluator to ask whether the controls that are in place reduce the residual risk to an acceptable level and thereby provide reasonable assurance that the objectives under consideration will be achieved. Paragraph 81 covers this concept: The term deficiency refers to a shortcoming in some aspect of the system of internal control and has the potential to adversely affect the ability of the entity to achieve its objectives. The Framework should focus an evaluator s attention on understanding how an unmitigated risk can adversely affect an objective versus simply assessing whether a principle is in place. We recommend the 81 attributes be clearly published in a manner that ensures they are not considered part of the Framework. We would further suggest that the term attributes be changed to considerations or another term which better reflects that the items are not an additional level of granular checklists which could be used solely to evaluate internal controls. 3. We support and applaud the expanded reporting objectives along with the operational and compliance objectives. However, the writing team should consider enhancing the Framework to more fully discuss operational and compliance objectives. Practitioners believe there should be a more balanced view of these objectives, as the draft focuses predominately on external financial reporting. Operational and compliance objectives should be addressed with similar depth, specificity and flexibility as the Framework allows on external financial reporting. At the same time, the Framework should clearly outline how it is the organization s decision to determine which objectives the entity wishes to address as part of its conformity with the Framework. 4. As discussed in item 2, the principles were considered favorably by members, although many do not believe the principles are evenly focused. We appreciate the writing team s need to blend theory and practical necessity. Fraud and IT general controls are among a number of considerations which bring risk to an objective. Reconsidering the level and definition of principles may be prudent so that they are consistent and applied across similar groups of objectives, risks, processes, systems, information, communication activities, environmental attributes and people factors. Fraud and IT may be more appropriately discussed as extensive attributes to other core principles. 5. We applaud the style, look and tone of the document which is clearly an appropriate refresh of the 1992 document. As the document nears final publication, we would suggest that a review for unnecessary wording and complexity be conducted. The revision has grown in length from the original 80 page document in order to enhance the direction to management and evaluators. Therefore, the writing team should ensure that the length is appropriate and writing succinct to support full adoption of the entire body of work. We believe it is imperative to clarify the difference between the Framework (pages 1-24) and other chapters (pages ). Issuing the other chapters as a separate document could ensure a differentiation between the principles based document and additional optional guidance. 4

5 Thank you again for the opportunity to provide comments. We believe our members comments and insights, once addressed, will ensure the Framework keeps pace with the substantial advances in governance, risk management and control processes inside and outside the U.S. ensuring that the fundamental COSO model stays relevant and embraced for the next 20 years. The IIA welcomes the opportunity to discuss any and all of these recommendations with you. We offer our assistance to COSO in the continued development of this Framework and supporting guidance. Best Regards, Dennis K. Beran, CIA, CCSA, CRMA, CPA, CFE Chairman of the Board About The Institute of Internal Auditors The IIA is the global voice, acknowledged leader, principal educator, and recognized authority of the internal audit profession and maintains the International Standards for the Professional Practice of Internal Auditing (Standards). These principles-based standards are recognized globally and are available in 29 languages. The IIA represents more than 170,000 members across the globe and has 105 Institutes in 165 countries that serve members at the local level. 5

6 ATTACHMENT A (Responses to COSO s Public Exposure Feedback Questions #1 through #18) In answering these questions, there was uncertainty on whether the answers should be limited to the first 24 pages of the draft (the actual Framework per paragraph 68) or to the entire exposure draft. In general, our responses and ratings below are based upon review of the entire draft. We intend to limit specific verbiage suggestions to the Framework (the first 24 pages of the draft). Additionally, we will refer to pages 1 24 as the Framework and pages as guidance. General Questions 1. Are you a member of one or more of the COSO organizations? Yes, the Institute of Internal Auditors is one of the original sponsoring organizations. The IIA is the global voice, acknowledged leader, principal educator, and recognized authority of the internal audit profession and maintains the International Standards for the Professional Practice of Internal Auditing (Standards). 2. Are you responding on behalf of yourself or an organization or company? We are responding on behalf of our global organization. The IIA represents more than 170,000 members across the globe and has 105 Institutes in 165 countries that serve members at the local level. 3. Where do you reside? The IIA is based in Altamonte Springs, Florida, USA. 4. Where within your organization do you apply the COSO Framework? Not answered. Overall Impressions on the Framework (answered on a scale of 1 to 5 with five being the highest or most in agreement) 5. The updated Framework will help strengthen an entity s systems of internal control. Summary Rating 3 The principles based framework is potentially a great improvement. The original conceptual framework clarified what internal control is, but did not give practical guidance on how to achieve it. Our members expressed concern, however, that it would not be applied as intended resulting in a checklist approach. The new draft emphasizes judgment in the evaluation of internal control effectiveness overall, as components are interrelated, yet it requires not only an overall evaluation of each component but additionally of each principle and attribute. This encourages management and auditors to think in silos within each element of the framework versus taking an holistic approach to the evaluation of internal control over a given objective. This will encourage a checklist approach to assessing internal control rather than the use of judgment based on the significance of the objective, activity, or risk compared to the more relevant principles and controls that are working effectively versus a simple validation of existence of the principles and attributes outlined in the framework. Of particular concern is the absolute nature of the statement in paragraph 78 which states, When a principle is deemed not to be present or functioning, an internal control deficiency exists. Paragraph 81 states, The term deficiency refers to a shortcoming in some aspect of the system of internal control and has the potential to adversely affect the ability of the entity to achieve its objectives. The writing team should clarify how these statements should be applied when: principles are partially working, and some principles are working at a high state of maturity while others are non-existent. An example of these dynamics would be a fairly small, informally run organization with a strong commitment to integrity and ethics, a well-understood risk appetite, and unusually close oversight by the board, cascading down through the organization through management at all levels. Such 6

7 an organization may have little in the way of specified policies and procedures, but the wellunderstood culture and close supervision provides reasonable assurance that risks are managed and objectives achieved. The current Framework asks, Are all 17 principles in place and functioning? We believe the correct principle based question to ask is Is the combination of governance, risk management, and internal controls in place to reduce the residual risk to a level acceptable by management (within legal, regulatory, and contractual expectations) and thereby providing reasonable assurance that management s stated objectives will be achieved? 6. The updated Framework is internally consistent and logical. There is logic in seeing strategy formulation and objective setting as pre-conditions of internal control. We feel, however, that it is inconsistent to exclude them because they should be wellcontrolled processes. If the right controls are not present within these processes, the resulting strategies and objectives are likely to be misaligned. The purpose of internal control is to support the achievement of the organization s strategic objectives in an ethical and compliant manner. COCO and Cadbury models include these activities as part of internal control and risk management systems. 7. The updated Framework is written in a manner that is understandable and provides ease of use Most users of the original Framework felt it was hard to read and was written for accountants and auditors, not managers. Unfortunately, the new draft is likely to have the same effect. We present some of the issues and illustrative examples: There are various tools that can be used to assess complexity of writing. One of these tools is the Gunning Fog Factor. We noted that the draft is written at a very high fog factor. This will create barriers to comprehension, for both English and non-native English speaking readers. For example, paragraph 17 presents the very important concept of embedding controls in the process. Its Gunning Fog Factor is According to the tool, this means that a reader would have to have 5.68 years of education after college graduation to comfortably read and comprehend the paragraph. A standard principle of business writing is that no piece of writing should have a fog factor above 12. Sometimes, the use of words is grammatically incorrect. For example, paragraph 118 states, Establishing a strong culture considers, for example, how clearly and consistently ethical and behavioral standards are communicated and reinforced in practice. To consider is a thought process. The gerund Establishing cannot consider. English speakers used to reading audit reports may not have a problem understanding this, but it is not correct. For business managers and non-native English speakers, this word choice is a barrier to comprehension. Examples of this type of auditorese abound in the draft. Rigorous editing is needed to make the entire document clear, concise, understandable and reader-friendly, especially for non-accountants, non-auditors, and non-native English speaking readers. 8. The updated Framework is applicable to organizations of varying legal structures and sizes and operating in various geographies and industries. 3 At the principles level, #2 and #3 regarding board of directors and board oversight may not be applicable to all the organizations referenced in the question. At the guidance level, it is very U.S.-centric; organizations at lower internal control maturity levels will likely not meet the attributes. It will be burdensome for small companies if they have to try to prove compliance with every principle and attribute. 9. The updated Framework will impose additional burdens on entities reporting on 3.2 7

8 internal control e.g., reporting on internal control over external financial reporting based on Sarbanes Oxley Act of 2002 (SOX) requirements. The amount of additional compliance burden is dependent upon the expectation of the SEC, the PCAOB, and external auditors. At the principle level, they are similar to the 1992 Framework. At the guidance level, there are now 81 attributes. Now that companies have stabilized their SOX programs, there is a concern that demonstrating compliance with the updated Framework will require changing the SOX processes and create non value-added work. At a minimum, companies will be compelled to map their components, principles, and attributes to their SOX Programs and then, identify and remediate any gaps. Companies with a centralized SOX program will require fewer resources to complete this update. Considerable resources are required in a decentralized environment if each process owner (a company may have hundreds) has to conclude for each component, all 17 principles and each attribute. There is a concern that the absence of, or partial implementation of, a principle will result in a deficiency or significant deficiency that would prevent the company from concluding their system of internal controls is effective. We believe this is not indicative of a principle based approach. 9a) If you believe that there is an additional burden, is the change appropriate? If not, why not? 2.7 The principles and attributes approach, if used as intended, could lead to a more meaningful evaluation and definitively provide management and evaluators with more guidance on the potential design and considerations for internal control. At the same time, it is very likely that the evaluation will turn into a checklist exercise. Supporting attributes, as noted previously, are good but must be viewed only as considerations that may or may not be needed to conclude that internal controls are sufficient. There is concern that many companies will have to re-map their controls to processes and risks. This concern is expressed most often by U.S. companies that believe they have an established, effective set of documentation to support their SOX reporting. There is a perception that the burden of moving to the updated Framework is not value-added as their existing controls for financial reporting have been deemed adequate by management and external auditors. The COSO board needs to consider whether we are refreshing the framework to assist the current process and expectations or are we raising expectations regarding what we mean by the adequacy of internal control. Specific Areas of Interest (answered on a scale of 1 to 5 with five being the highest or most in agreement) 10. Compared to the 1992 framework, the updated Framework creates a higher threshold for attaining effectiveness of internal control. Summary Rating 3.5 The Framework does not create a higher threshold, but more precise and specific requirements due to the 17 principles and related attributes. For instance, the component on risk assessment has additional guidance related to that component, but the overall threshold of what was expected under the 1992 Framework has not changed. As we noted earlier, care should be taken to ensure that the principles and attributes are not considered overly prescriptive and thus leaving less room for applying professional/management judgment. The specificity of the principles and attributes make it more difficult to say internal control is sound if critical aspects are missing or ineffective. Paragraphs 70 to 90 could be interpreted to require that existing systems be fully remapped and that management would need to conclude across numerous processes on all principles and attributes. If all principles are expected to be addressed substantially, this could create a higher threshold to support an effective assessment. 11. The 17 principles set out in the updated Framework are a complete set of principles. 3 8

9 Although considered fairly comprehensive in general, there are different ways to approach the principles (not necessarily by component). Both completeness and optimal mix are considerations. Below are some specific suggestions: The principles do not sufficiently assess how the external environment may impact the risk profile and resulting internal control needs of the organization. Principles speaking to accountability establishment, segregation of duties, adequacy of assurance process, priority setting, data governance, etc., are possible principles that cross components. Accordingly, assessment may be constrained by assignment of principles to specific components. The writing team may wish to consider how the principles are used to develop an overall evaluation of internal control versus black and white conclusions at the principle/component level. Many have challenged the rationale to establish fraud and IT general controls as principles versus attributes. Listing them as principles runs contrary to the theory of the framework concept which requires the document to not identify the specific risks but ensure appropriate risk assessment. At the same time, we realize the practical focus that all organizations must have on fraud risk and IT risk in some area of their organization. As we have stated previously, being prescriptive on principles may drive assessments that are required by the objectives and risk profile of the organization. 12. The 17 principles with related attributes are helpful in describing important considerations of an effective system of internal control. See responses to #5, 6 and There are necessary changes to the principles Specific comments for change include: Principle 5 Recommend changing to: The organization establishes and holds individuals accountable for effective management of risk in the pursuit of objectives. Internal control is one of the risk management strategies. Risk can be mitigated, transferred, insured or accepted. Effective risk management includes the upside of taking advantage of opportunities and the downside of not preventing undesirable outcomes. Implicit in effective risk management is to be alert to new risks and changes in risk factors and levels as well as being held accountable for responding appropriately. Principle 6 Recommend adding: the assessment of risks relating to achievement of objectives. (We believe this is the intent.) Principle 9 Recommend changing to: The organization identifies and assesses changes that could significantly impact the achievement of objectives. A change increases risk to objectives, good and bad, and requires reassessment of control applicability and design. Principle 11 Recommend eliminating this principle. IT general control activities do not need to be separated from control activities. They are control activities and should be assessed in combination with all controls relied upon for the achievement of objectives just like other process risks. Principle 14 Recommend changing to: The organization internally communicates information, including objectives and responsibilities for effective risk management and internal control 9

10 Recognize internal control as a response to effective risk management. Consider describing how communication processes disclose changes in risk appetite. Principle 16 We recommend changing to: The organization selects, develops and performs ongoing and/or separate evaluations to ascertain whether the components of internal control are present and functioning in an efficient and effective manner. Incorporate continuous improvement as one of the objectives of the evaluation. Principle 17 Recommend changing to: The organization evaluates and communicates internal control deficiencies and improvement opportunities in a timely manner This supports the objective of continuous improvement, not just correcting problems and errors. 14. An entity can conclude that it has effective internal control if one or more of the 17 principles are not present and functioning. 3.5 All practitioners involved in our discussion believe there should be room for judgment in determining whether a control system is adequate for a given objective even if one or more principles are absent or only partially effective. The updated Framework could be read as suggesting that an effective system of internal control is achieved if the principles and related guidance attributes for each of the components of the model are present and functioning. Judgment is necessary to reach that conclusion, not the completion of a checklist assessment of each principle. Reasonable assurance requires, in most cases, a combination of controls across a range of COSO components. Controls are not necessarily needed for every principle. Effective controls for one component of the Framework may compensate for a lack of controls in another component. There should be room for judgment in determining whether a control system remains adequate if any given principles are only partially present by assessing compensating controls. The Framework should be very specific and use examples to show that you can have errors due to internal control issues and still have an effective system of internal control. Considerations in making that assessment will include the frequency and number of errors, the significance of the errors, whether controls mitigated the effect of the errors within tolerances, the period of time during which errors occurred, and whether the risk of nonachievement of objectives remained acceptable. Judgment and relative compensating components or control environment elements could offset principle deficiencies. 15. The updated Framework appropriately expands the reporting objective category (i.e., internal and external reporting, financial and non-financial reporting). This change is welcomed by many and recognized as important by most people familiar with the COSO IC framework updates. 16. The expanded reporting objective, and the manner in which this objective category is presented in the Framework, does not diminish our ability to apply the Framework when reporting on internal control over external financial reporting. We concur. 17. The updated Framework provides an appropriate balance of reporting, operations, and compliance related approaches and examples The IIA supports the expanded reporting objective to ensure it goes beyond financial reporting; however, COSO should enhance the Framework by expanding upon the discussion of operational and compliance objectives. Practitioners believe there should be a more balanced view of these objectives, as the draft focuses on external financial reporting. Operational and compliance objectives should be allowed similar depth, specificity and flexibility as the guidance allows for external financial reporting. This could be emphasized through the attribute guidance. 10

11 In assessing overall effectiveness and related deficiency definitions for Compliance and Operations objectives, the example material appears to be too black and white. Assessing the adequacy of controls over operations and compliance may require more understanding of an organization s risk tolerance and expectations as well as significantly more judgment than an assessment over external financial reporting. Most companies have many of the issues illustrated and may not conclude that their system of internal controls is ineffective. 18. Summary - Are there any other general comments that you would like to provide? 1. COSO should consider the addition of a reporting chapter or additional guidance in order to illustrate flexible alternatives for evaluating internal control systems for various stakeholders. Many stakeholders may not need a point in time conclusion on effectiveness of internal control. The COSO refresh needs to incorporate alternatives such as a maturity scale for reporting on internal control systems. Such an approach would be useful for organizations of different size and complexity. 2. On page 51 on the title page of the risk assessment section, the writers note that Risk is defined as the possibility that an event will occur and adversely affect the achievement of objectives. The use of adversely in this sentence could imply that risk is only referring to negative events versus positive outcomes. The writers should ensure that the broader understanding of risk threats, opportunities, and uncertainties is understood. Such a broader definition is contained in nearly all contemporary risk management literature. 3. Consideration should be given to including a comment related to the effective date of the updated Framework to ensure that it replaces the existing Framework and there is no potential confusion about having two Frameworks existing at the same time. 11

12 12

REVISED CORPORATE GOVERNANCE PRINCIPLES FOR BANKS (CONSULTATION PAPER) ISSUED BY THE BASEL COMMITTEE ON BANKING SUPERVISION

ISSUED BY THE BASEL COMMITTEE ON BANKING SUPERVISION") January 9, 2015 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel, Switzerland Submitted via http://www.bis.org/bcbs/commentupload.htm REVISED CORPORATE

January 9, 2015 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel, Switzerland Submitted via http://www.bis.org/bcbs/commentupload.htm REVISED CORPORATE

Mr. Paul Druckman Chief Executive Officer, International Integrated Reporting Council

Philip D. Tarling, CIA, CRMA, CMIIA Global Chairman of the Board The Institute of Internal Auditors 247 Maitland Avenue Altamonte Springs, FL 32701 July 12, 2013 Professor Mervyn King Chairman, International

Philip D. Tarling, CIA, CRMA, CMIIA Global Chairman of the Board The Institute of Internal Auditors 247 Maitland Avenue Altamonte Springs, FL 32701 July 12, 2013 Professor Mervyn King Chairman, International

Response ed to

February 29, 2012 Office of the Secretary PCAOB 1666 K Street, N.W. Washington, D.C. 20006-2803 Response e-mailed to comments@pcaobus.org RE: PCAOB Rulemaking Docket Matter No. 030 Proposed Auditing Standard

February 29, 2012 Office of the Secretary PCAOB 1666 K Street, N.W. Washington, D.C. 20006-2803 Response e-mailed to comments@pcaobus.org RE: PCAOB Rulemaking Docket Matter No. 030 Proposed Auditing Standard

Internal Control Integrated Framework. An IAASB Overview September 2016

Internal Control Integrated Framework An IAASB Overview September 2016 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing

Internal Control Integrated Framework An IAASB Overview September 2016 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing

FSB Consultative Document - Guidance on Supervisory Interaction with Financial Institutions on Risk Culture

Richard F. Chambers Certified Internal Auditor Certified Government Auditing Professional Certification in Control Self-Assessment Certification in Risk Management Assurance President and Chief Executive

Richard F. Chambers Certified Internal Auditor Certified Government Auditing Professional Certification in Control Self-Assessment Certification in Risk Management Assurance President and Chief Executive

2013 COSO Internal Control Framework Update. September 5, 2013

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to

2013 COSO Internal Control Framework Update September 5, 2013 Agenda 2013 COSO IC Framework Topic Minutes The update process 5 What is not changing / What is changing 5 The 17 principles and changes to

Internal Control Integrated Framework. May 2013

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it?

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

In Control: Getting Familiar with the New COSO Guidelines. CSMFO Monterey, California February 18, 2015

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING PRESENTATION AUDITING IMPLICATIONS OF COSO PROJECT TO UPDATE

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING PRESENTATION AUDITING IMPLICATIONS OF COSO PROJECT TO UPDATE

Practice Guide. Developing the Internal Audit Strategic Plan

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

Practice Guide Developing the Internal Audit Strategic Plan JUly 2012 Table of Contents Executive Summary... 1 Introduction... 2 Strategic Plan Definition and Development... 2 Review of Strategic Plan...

An Update of COSO s Internal Control Integrated Framework. December 2011

An Update of COSO s Internal Control Integrated Framework December 2011 1 Internal Control-Integrated Framework First published in 1992 Gained wide acceptance following financial control failures of early

An Update of COSO s Internal Control Integrated Framework December 2011 1 Internal Control-Integrated Framework First published in 1992 Gained wide acceptance following financial control failures of early

Proposed application material relating to professional scepticism and professional judgement

Proposed application material relating to professional scepticism and professional judgement An exposure draft issued for public consultation by the International Ethics Standards Board for Accountants

Proposed application material relating to professional scepticism and professional judgement An exposure draft issued for public consultation by the International Ethics Standards Board for Accountants

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN Department of Accountancy College of Business 360 Wohlers Hall 1206 S. Sixth Street Champaign, IL 61820 Office of the Secretary PCAOB 1666 K Street Washington,

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN Department of Accountancy College of Business 360 Wohlers Hall 1206 S. Sixth Street Champaign, IL 61820 Office of the Secretary PCAOB 1666 K Street Washington,

The Updated COSO Internal Control Framework

The Updated COSO Internal Control Framework Frequently Asked Questions Second Edition Introduction The Committee of Sponsoring Organizations of the Treadway Commission (COSO) an organization providing

The Updated COSO Internal Control Framework Frequently Asked Questions Second Edition Introduction The Committee of Sponsoring Organizations of the Treadway Commission (COSO) an organization providing

Fraud Risk Management

Fraud Risk Management Fraud Risk Management Overview 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization follow a specific risk management model? If so, which

Fraud Risk Management Fraud Risk Management Overview 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization follow a specific risk management model? If so, which

AUDITING. Auditing PAGE 1

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

AUDITING Auditing 1. Professionalism The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal

LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE

Committee of Sponsoring Organizations of the Treadway Commission Governance and Internal Control LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE By The Institute of Internal Auditors Douglas J. Anderson

Committee of Sponsoring Organizations of the Treadway Commission Governance and Internal Control LEVERAGING COSO ACROSS THE THREE LINES OF DEFENSE By The Institute of Internal Auditors Douglas J. Anderson

An Overview of the 2013 COSO Framework. August 2013

An Overview of the 2013 COSO Framework August 2013 Introduction Dean Geesler, KPMG Senior Manager Course Objectives Summarize the key changes from the 1992 Framework to the 2013 Framework including the

An Overview of the 2013 COSO Framework August 2013 Introduction Dean Geesler, KPMG Senior Manager Course Objectives Summarize the key changes from the 1992 Framework to the 2013 Framework including the

COSO What s New, What s Changed, Why Does it Matter and Other Frequently Asked Questions

COSO 2013 What s New, What s Changed, Why Does it Matter and Other Frequently Asked Questions Today s Presenter Jonathan Reiss is a Director in Protiviti s New York office in the Internal Audit Practice.

COSO 2013 What s New, What s Changed, Why Does it Matter and Other Frequently Asked Questions Today s Presenter Jonathan Reiss is a Director in Protiviti s New York office in the Internal Audit Practice.

COSO Framework Update Webcast. May 23, 2013

COSO Framework Update Webcast May 23, 2013 Today s presenters Rob Kastenschmidt National Leader - Risk Advisory Services Sara Lord Partner - National Professional Standards Group Agenda Topic Minutes The

COSO Framework Update Webcast May 23, 2013 Today s presenters Rob Kastenschmidt National Leader - Risk Advisory Services Sara Lord Partner - National Professional Standards Group Agenda Topic Minutes The

Response ed to Re: PCAOB Rulemaking Docket Matter No. 028

September 7, 2010 Office of the Secretary, PCAOB 1666 K Street, N.W. Washington, D.C. 20006-2803 Response e-mailed to comments@pcaobus.org Re: PCAOB Rulemaking Docket Matter No. 028 Dear PCAOB Board: The

September 7, 2010 Office of the Secretary, PCAOB 1666 K Street, N.W. Washington, D.C. 20006-2803 Response e-mailed to comments@pcaobus.org Re: PCAOB Rulemaking Docket Matter No. 028 Dear PCAOB Board: The

Audit Risk. Exposure Draft. IFAC International Auditing and Assurance Standards Board. October Response Due Date March 31, 2003

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

Organizational Governance: Guidance for Internal Auditors. - July

Position Paper Organizational Governance: Guidance for Internal Auditors - July 2006 - The Institute of Internal Auditors, 247 Maitland Avenue, Altamonte Springs, Florida 32701-4102, USA http://www.theiia.org

Position Paper Organizational Governance: Guidance for Internal Auditors - July 2006 - The Institute of Internal Auditors, 247 Maitland Avenue, Altamonte Springs, Florida 32701-4102, USA http://www.theiia.org

Auditing Standard 16

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

February 23, Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, D.C.

McGladrey & Pullen LLP Third Floor 3600 American Blvd West Bloomington, MN 55431 O 952.835.9930 February 23, 2007 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington,

McGladrey & Pullen LLP Third Floor 3600 American Blvd West Bloomington, MN 55431 O 952.835.9930 February 23, 2007 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington,

GoldSRD Audit 101 Table of Contents & Resource Listing

Au GoldSRD Audit 101 Table of Contents & Resource Listing I. IIA Standards II. GTAG I (Example Copy of the Contents of the GTAG Series) III. Example Audit Workprogram IV. Audit Test Workpaper Example V.

Au GoldSRD Audit 101 Table of Contents & Resource Listing I. IIA Standards II. GTAG I (Example Copy of the Contents of the GTAG Series) III. Example Audit Workprogram IV. Audit Test Workpaper Example V.

Policy and Procedures Date: November 5, 2017

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

Virginia Polytechnic Institute and State University No. 3350 Rev.: 8 Policy and Procedures Date: November 5, 2017 Subject: Charter for the Office of Audit, Risk, and Compliance 1. Purpose... 1 2. Policy...

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants [28 July 2017] TO: Professor Arnold Schilder The Chairman International Auditing

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants [28 July 2017] TO: Professor Arnold Schilder The Chairman International Auditing

Quality Assessments what you need to know

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Introductions. An Overview of the COSO 2013 Framework. Christian Peo Sharon Todd. An Overview of the 2013 COSO Framework.

An Overview of the 2013 COSO Framework An Overview of the COSO 2013 Framework August 8, 2013 Introductions Christian Peo Sharon Todd Marc Wittenberg Module Name/SL/1 firms Course Objectives By the end

An Overview of the 2013 COSO Framework An Overview of the COSO 2013 Framework August 8, 2013 Introductions Christian Peo Sharon Todd Marc Wittenberg Module Name/SL/1 firms Course Objectives By the end

From Dictionary.com. Risk: Exposure to the chance of injury or loss; a hazard or dangerous chance

Sharon Hale and John Argodale May 28, 2015 2 From Dictionary.com Enterprise: A project undertaken or to be undertaken, especially one that is important or difficult or that requires boldness or energy

Sharon Hale and John Argodale May 28, 2015 2 From Dictionary.com Enterprise: A project undertaken or to be undertaken, especially one that is important or difficult or that requires boldness or energy

REPORT 2016/033 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/033 Advisory engagement on the Statement on Internal Control project at the United Nations Joint Staff Pension Fund 25 April 2016 Assignment No. VS2015/800/01 CONTENTS

INTERNAL AUDIT DIVISION REPORT 2016/033 Advisory engagement on the Statement on Internal Control project at the United Nations Joint Staff Pension Fund 25 April 2016 Assignment No. VS2015/800/01 CONTENTS

Proposed Attestation Requirements for FR Y-14A/Q/M reports. Overview and Implications for Banking Institutions

Proposed Attestation Requirements for FR Y-14A/Q/M reports Overview and Implications for Banking Institutions O Background n September 16, 2015, the Board of Governors of the Federal Reserve System ( Federal

Proposed Attestation Requirements for FR Y-14A/Q/M reports Overview and Implications for Banking Institutions O Background n September 16, 2015, the Board of Governors of the Federal Reserve System ( Federal

Strengthening Control and integrity: A Checklist for government Managers

Forum: Analytics and Risk Management Tools for Making Better Decisions Strengthening Control and integrity: A Checklist for government Managers By James A. Bailey The next contribution is based on a Center

Forum: Analytics and Risk Management Tools for Making Better Decisions Strengthening Control and integrity: A Checklist for government Managers By James A. Bailey The next contribution is based on a Center

Australian Government Auditing and Assurance Standards Board

Australian Government Auditing and Assurance Standards Board Podium Level 14, 530 Collins Street Melbourne VIC 3000 Australia PO Box 204, Collins Street West Melbourne VIC 8007 1 August 2017 Mr Matt Waldron

Australian Government Auditing and Assurance Standards Board Podium Level 14, 530 Collins Street Melbourne VIC 3000 Australia PO Box 204, Collins Street West Melbourne VIC 8007 1 August 2017 Mr Matt Waldron

IAASB Main Agenda (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

IPPF Practice Guide. Internal Audit Opinions

Formulating and Expressing Internal Audit Opinions March 2009 Table of Contents 1. Executive Summary...1 2. Introduction...1 3. Planning the Expression of an Opinion...2 3.1 Expressing an Opinion...2 3.2

Formulating and Expressing Internal Audit Opinions March 2009 Table of Contents 1. Executive Summary...1 2. Introduction...1 3. Planning the Expression of an Opinion...2 3.1 Expressing an Opinion...2 3.2

PRACTICE GUIDE. Formulating and Expressing Internal Audit Opinions

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

See your auditor clearly. Transparency report: How we perform quality audit engagements

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

[RELEASE NOS ; ; FR-77; File No. S ]

![[RELEASE NOS ; ; FR-77; File No. S ]](/thumbs/75/72094692.jpg "[RELEASE NOS ; ; FR-77; File No. S ]") SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

IPPF Practice Guide. Assessing the Adequacy of

Assessing the Adequacy of Risk Management Using ISO 31000 December 2010 Table of Contents Executive Summary... 1 Introduction... 1 Risk Management in the Organization... 2 Internal Auditing and Risk Management...

Assessing the Adequacy of Risk Management Using ISO 31000 December 2010 Table of Contents Executive Summary... 1 Introduction... 1 Risk Management in the Organization... 2 Internal Auditing and Risk Management...

COSO Internal Control Integrated Framework Proposed Update

COSO Internal Control Integrated Framework Proposed Update Presented by: Dustin Birashk September 20, 2012 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational purposes

COSO Internal Control Integrated Framework Proposed Update Presented by: Dustin Birashk September 20, 2012 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational purposes

IAASB CAG Public Session (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background

Report. Quality Assessment of Internal Audit at <Organisation> Draft Report / Final Report

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

Case Report from Audit Firm Inspection Results

Case Report from Audit Firm Inspection Results July 2014 Certified Public Accountants and Auditing Oversight Board Table of Contents Expectations for Audit Firms... 1 Important Points for Users of this

Case Report from Audit Firm Inspection Results July 2014 Certified Public Accountants and Auditing Oversight Board Table of Contents Expectations for Audit Firms... 1 Important Points for Users of this

For the first time in the history of corporate financial reporting and. Management Reporting on Internal Control. Use of COSO 1992 in.

Cover Story Use of COSO 1992 in Management Reporting on Internal Control THE COSO FRAMEWORK provides an integrated framework that identifies components and objectives of internal control. But does it set

Cover Story Use of COSO 1992 in Management Reporting on Internal Control THE COSO FRAMEWORK provides an integrated framework that identifies components and objectives of internal control. But does it set

Guidance Note: Corporate Governance - Audit Committee. March Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Ms. Maridel Piloto de Noronha, PAS Secretariat Via

October 7, 2015 Ms. Maridel Piloto de Noronha, PAS Secretariat Via email: semec@tcu.gov.br RE: Exposure Drafts ISSAI 3000 Performance Audit Standard; ISSAI 3100 Guidelines on central concepts for Performance

October 7, 2015 Ms. Maridel Piloto de Noronha, PAS Secretariat Via email: semec@tcu.gov.br RE: Exposure Drafts ISSAI 3000 Performance Audit Standard; ISSAI 3100 Guidelines on central concepts for Performance

Audit of Entity Level Controls

Unclassified Internal Audit Services Branch Audit of Entity Level Controls February 2014 SP-606-03-14E You can download this publication by going online: http://www12.hrsdc.gc.ca This document is available

Unclassified Internal Audit Services Branch Audit of Entity Level Controls February 2014 SP-606-03-14E You can download this publication by going online: http://www12.hrsdc.gc.ca This document is available

Practice Advisory : Quality Assurance and Improvement Program

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

up Texas Society of ~ Certified Public Accountants

up Texas Society of ~ Certified Public Accountants Office of the Secretary 1666 K Street, N.W. Washington, D.C. 20006-2803 RE: Proposed Auditing Standard An Audit of Internal Control Over Financial Reporting

up Texas Society of ~ Certified Public Accountants Office of the Secretary 1666 K Street, N.W. Washington, D.C. 20006-2803 RE: Proposed Auditing Standard An Audit of Internal Control Over Financial Reporting

ISACA. The recognized global leader in IT governance, control, security and assurance

ISACA The recognized global leader in IT governance, control, security and assurance High-level session overview 1. CRISC background information 2. Part I The Big Picture CRISC Background information About

ISACA The recognized global leader in IT governance, control, security and assurance High-level session overview 1. CRISC background information 2. Part I The Big Picture CRISC Background information About

Continuous Auditing - A Delicate Chemistry

Continuous Auditing - A Delicate Chemistry Continuous Auditing - A Delicate Chemistry - WeiserMazars LLP s Governance, Risk and Compliance (GRC) Group WeiserMazars LLP is an independent member firm of

Continuous Auditing - A Delicate Chemistry Continuous Auditing - A Delicate Chemistry - WeiserMazars LLP s Governance, Risk and Compliance (GRC) Group WeiserMazars LLP is an independent member firm of

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

Charter for Enterprise Risk Management

for Enterprise Risk Management Prepared by: Shannon Sinclair Version: 1.2 Document Id: Date: Release Date TABLE OF CONTENTS TABLE OF CONTENTS... i 1. Background... 1 2. Objectives... 1 3. Scope... 2 3.1

for Enterprise Risk Management Prepared by: Shannon Sinclair Version: 1.2 Document Id: Date: Release Date TABLE OF CONTENTS TABLE OF CONTENTS... i 1. Background... 1 2. Objectives... 1 3. Scope... 2 3.1

Arnold H. Schanfield, CPA, CIA Principal, Schanfield Risk Management Advisors, LLC

Arnold H. Schanfield, CPA, CIA Principal, Schanfield Risk Management Advisors, LLC 201-207-7935 aschanfield@verizon.net January 23, 2014 Ms. Catherine Woods Financial Reporting Council Fifth Floor Aldwych

Arnold H. Schanfield, CPA, CIA Principal, Schanfield Risk Management Advisors, LLC 201-207-7935 aschanfield@verizon.net January 23, 2014 Ms. Catherine Woods Financial Reporting Council Fifth Floor Aldwych

COSO 2013: Updated internal control framework

COSO 2013: Updated internal control framework Athens, 10 October 2013 Background COSO's structure and mission COSO 1 is a joint initiative of five sponsoring organizations - American Accounting Association

COSO 2013: Updated internal control framework Athens, 10 October 2013 Background COSO's structure and mission COSO 1 is a joint initiative of five sponsoring organizations - American Accounting Association

Internal Financial Controls New perspectives as per Companies Act 2013 and CARO 2016

New perspectives as per Companies Act 2013 and CARO 2016 1 Contents: Background Meaning of IFC IFC on Financial Reporting Why IFC? Regulatory mandate Role of various authorities Components of IFC IFC under

New perspectives as per Companies Act 2013 and CARO 2016 1 Contents: Background Meaning of IFC IFC on Financial Reporting Why IFC? Regulatory mandate Role of various authorities Components of IFC IFC under

INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

The Future of Internal Auditing:

Internal Audit The Future of Internal Auditing: Changing Internal Audit s Value Proposition October 12, 2010 Istanbul, Turkey Presented by: Naman Parekh Partner, Agenda Background of the 2012 Study Key

Internal Audit The Future of Internal Auditing: Changing Internal Audit s Value Proposition October 12, 2010 Istanbul, Turkey Presented by: Naman Parekh Partner, Agenda Background of the 2012 Study Key

Audit Training-of-Trainers Workshop, November 2014, Vienna Components of internal control within organization

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

) ) ) ) ) ) ) ) ) ) ) ) REPORTING ON WHETHER A PREVIOUSLY REPORTED MATERIAL WEAKNESS CONTINUES TO EXIST. PCAOB Release No July 26, 2005

) ) ) ) ) ) ) ) ) ) ) REPORTING ON WHETHER A PREVIOUSLY REPORTED MATERIAL WEAKNESS CONTINUES TO EXIST. PCAOB Release No July 26, 2005") 1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org REPORTING ON WHETHER A PREVIOUSLY REPORTED MATERIAL WEAKNESS CONTINUES TO EXIST ) ) ) ) ) ) )

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org REPORTING ON WHETHER A PREVIOUSLY REPORTED MATERIAL WEAKNESS CONTINUES TO EXIST ) ) ) ) ) ) )

Enterprise Risk Management Aligning Risk with Strategy and Performance COSO ERM Framework Update

Enterprise Risk Management Aligning Risk with Strategy and Performance COSO ERM Framework Update April 4, 2017 Agenda 1. Setting the Stage for Enterprise Risk Management 2. Project Overview 3. Key Changes

Enterprise Risk Management Aligning Risk with Strategy and Performance COSO ERM Framework Update April 4, 2017 Agenda 1. Setting the Stage for Enterprise Risk Management 2. Project Overview 3. Key Changes

August 14, Dear Ms. Gula:

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

Department of Internal Audit North End Center, Suite 3200, Virginia Tech 300 Turner Street NW Blacksburg, Virginia 24061 Campus Mail Code: 0328 540-231-5883 Fax: 540-231-4681 www.ia.vt.edu August 14, 2013

AUSTRALIAN ENGINEERING COMPETENCY STANDARDS STAGE 2 - EXPERIENCED PROFESSIONAL ENGINEER IN LEADERSHIP AND MANAGEMENT

AUSTRALIAN ENGINEERING COMPETENCY STANDARDS STAGE 2 - EXPERIENCED IN LEADERSHIP AND MANAGEMENT The Stage 2 Competency Standards are the profession's expression of the knowledge and skill base, engineering

AUSTRALIAN ENGINEERING COMPETENCY STANDARDS STAGE 2 - EXPERIENCED IN LEADERSHIP AND MANAGEMENT The Stage 2 Competency Standards are the profession's expression of the knowledge and skill base, engineering

Proposed Changes to Certain Provisions of the Code Addressing the Long Association of Personnel with an Audit or Assurance Client

IFAC Board Exposure Draft August 2014 Comments due: November 12, 2014 Exposure Draft October 2011 Comments due: February 29, 2012 International Ethics Standards Board for Accountants Proposed Changes to

IFAC Board Exposure Draft August 2014 Comments due: November 12, 2014 Exposure Draft October 2011 Comments due: February 29, 2012 International Ethics Standards Board for Accountants Proposed Changes to

Guidance for Smaller Public Companies Reporting on Internal Control Over Financial Reporting Exposure Draft

3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 13 January 2006 COSO Board In care of Dr.

3701 Algonquin Road, Suite 1010 Telephone: 847.253.1545 Rolling Meadows, Illinois 60008, USA Facsimile: 847.253.1443 Web Sites: www.isaca.org and www.itgi.org 13 January 2006 COSO Board In care of Dr.

CONTENTS. Acknowledgments... iv. 1: Introduction : Why have organizations chosen to seek compliance with the Standards?...2

IIA STANDARD 1312 - EXTERNAL QUALITY ASSESSMENTS: RESULTS, TOOLS, TECHNIQUES AND LESSONS LEARNED THE IIA RESEARCH FOUNDATION JULY 2007 Disclosure Copyright 2007 by The Institute of Internal Auditors Research

IIA STANDARD 1312 - EXTERNAL QUALITY ASSESSMENTS: RESULTS, TOOLS, TECHNIQUES AND LESSONS LEARNED THE IIA RESEARCH FOUNDATION JULY 2007 Disclosure Copyright 2007 by The Institute of Internal Auditors Research

Diving into the 2013 COSO Framework. Presented by: Ronald A. Conrad

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Several matters are pertinent to a discussion of audit quality with respect to external audits of banks.

June 21, 2013 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel Switzerland By email: baselcommittee@bis.org CONSULTATIVE DOCUMENT: EXTERNAL AUDITS

June 21, 2013 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel Switzerland By email: baselcommittee@bis.org CONSULTATIVE DOCUMENT: EXTERNAL AUDITS

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS Introduction As part of the corporate governance policies, processes and procedures of ImmunoGen, Inc. ( ImmunoGen or the Company

IMMUNOGEN, INC. CORPORATE GOVERNANCE GUIDELINES OF THE BOARD OF DIRECTORS Introduction As part of the corporate governance policies, processes and procedures of ImmunoGen, Inc. ( ImmunoGen or the Company

Corporate Governance Principles of Auditing: An Introduction to International Standards on Auditing - Ch 14

Slide 14.1 Corporate Governance Principles of Auditing: An Introduction to International Standards on Auditing - Ch 14 Rick Stephan Hayes, Roger Dassen, Arnold Schilder, Philip Wallage Slide 14.2 Corporate

Slide 14.1 Corporate Governance Principles of Auditing: An Introduction to International Standards on Auditing - Ch 14 Rick Stephan Hayes, Roger Dassen, Arnold Schilder, Philip Wallage Slide 14.2 Corporate

Advisory Services Governance, Risk & Compliance

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Business Context of ISO conform Internal Financial Control Assessment

Business Context of ISO 15504 conform Internal Financial Control Assessment By János Ivanyos, Memolux Ltd. (H), IIA Hungary Introduction In this paper the business context of the ISO/IEC 15504 [1] conformant

Business Context of ISO 15504 conform Internal Financial Control Assessment By János Ivanyos, Memolux Ltd. (H), IIA Hungary Introduction In this paper the business context of the ISO/IEC 15504 [1] conformant

Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, DC September 2011

Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, DC 20006-2803 30 September 2011 RE: PCAOB Rulemaking Docket Matter No. 34, Concept Release on Possible

Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, DC 20006-2803 30 September 2011 RE: PCAOB Rulemaking Docket Matter No. 34, Concept Release on Possible

KING IV IMPLEMENTATION

KING IV IMPLEMENTATION The board of directors implements the highest standards of corporate governance at all operations. The board understands and values long-term and ethical client relationships, and

KING IV IMPLEMENTATION The board of directors implements the highest standards of corporate governance at all operations. The board understands and values long-term and ethical client relationships, and

Group Internal Audit Charter

Group Internal Audit Charter March 2018 1. Introduction 1.1. This internal audit charter defines the purpose, authority, responsibilities and framework within which the Group Internal Audit (GIA) function

Group Internal Audit Charter March 2018 1. Introduction 1.1. This internal audit charter defines the purpose, authority, responsibilities and framework within which the Group Internal Audit (GIA) function

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

METROPOLITAN TRANSPORTATION AUTHORITY

ENTERPRISE RISK MANAGEMENT AND INTERNAL CONTROL GUIDELINES Pursuant to Public Authorities Law Section 2931 Adopted by the Board on November 16, 2016 These guidelines apply to the Metropolitan Transportation

ENTERPRISE RISK MANAGEMENT AND INTERNAL CONTROL GUIDELINES Pursuant to Public Authorities Law Section 2931 Adopted by the Board on November 16, 2016 These guidelines apply to the Metropolitan Transportation

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015 DIRECTOR TRAINING AND QUALIFICATIONS SAMPLE SELF-ASSESSMENT TOOL INTRODUCTION The purpose of this tool is to help determine

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015 DIRECTOR TRAINING AND QUALIFICATIONS SAMPLE SELF-ASSESSMENT TOOL INTRODUCTION The purpose of this tool is to help determine

CGIAR System Management Board Audit and Risk Committee Terms of Reference

Approved (Decision SMB/M4/DP4): 17 December 2016 CGIAR System Management Board Audit and Risk Committee Terms of Reference A. Purpose 1. The purpose of the Audit and Risk Committee ( ARC ) of the System

Approved (Decision SMB/M4/DP4): 17 December 2016 CGIAR System Management Board Audit and Risk Committee Terms of Reference A. Purpose 1. The purpose of the Audit and Risk Committee ( ARC ) of the System

White Paper. Effective and Practical Deployment of COSO: Entity Level Control and Lessons Learned. July 10, 2008 THE ROBERTS COMPANY, LLC

THE ROBERTS COMPANY, LLC Compliance Services: IT and Business Processes 3394 Holly Oak Lane, Escondido, CA 92027 TEL: 760.550.2160 * FAX 760.839.2160 E-mail: robertputrus@therobertsglobal.com http://www.therobertsglobal.com/

THE ROBERTS COMPANY, LLC Compliance Services: IT and Business Processes 3394 Holly Oak Lane, Escondido, CA 92027 TEL: 760.550.2160 * FAX 760.839.2160 E-mail: robertputrus@therobertsglobal.com http://www.therobertsglobal.com/

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

CREATING A FRAUD RISK ASSESSMENT AND IMPLEMENTING A CONTINUOUS MONITORING PROGRAM Compliance professionals around the world are struggling with how to do more with less. In order to provide effective assurance

A FRAMEWORK FOR AUDIT QUALITY. KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

The Auditor s Response to the Risks of Material Misstatement Posed by Estimates of Expected Credit Losses under IFRS 9

The Auditor s Response to the Risks of Material Misstatement Posed by Estimates of Expected Credit Losses under IFRS 9 Considerations for the Audit Committees of Systemically Important Banks Global Public

The Auditor s Response to the Risks of Material Misstatement Posed by Estimates of Expected Credit Losses under IFRS 9 Considerations for the Audit Committees of Systemically Important Banks Global Public

Approaches to auditing standards and their possible impact on auditor behavior

Original Article Approaches to auditing standards and their possible impact on auditor behavior Received (in revised form): 28 th July 2010 Jennifer Burns is a partner at Deloitte LLP and former Professional

Original Article Approaches to auditing standards and their possible impact on auditor behavior Received (in revised form): 28 th July 2010 Jennifer Burns is a partner at Deloitte LLP and former Professional

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

What We Will Cover Today

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

Standards for the Professional Practice of Internal Auditing The IIA Red Book The Basics of Internal Auditing September 8, 2014 Sam McCall, PhD, CPA, CGFM, CIA, CGAP, CIG Chief Audit Officer Florida State

The New COSO Framework: Avoiding Deficiencies and Driving Change