King III Apply or Explain

|

|

|

- Tabitha Butler

- 5 years ago

- Views:

Transcription

")

1 23 & 24 September 2011 (Frank Muller ) Apply or Explain

2 The philosophy of the Report revolves around leadership, sustainability and corporate citizenship -Mervyn King 2011 Inc. All rights reserved. refers to the network of member firms of International Limited, each of which is a separate and independent legal entity. Inc is an authorised financial services provider.

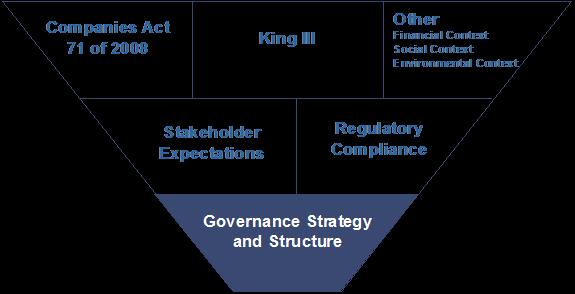

3 Code Code launched on 1 Replaces/ updated King II Implementation date is on 1 March 2010 Practice notes have/ to be issued by the IoD Written from a Board perspective Must vs Should language Setting a standard for governance in South Africa VERY APPLICABLE TO ALL SECTORS Slide 1

4 Applicability of the Code Applicability Positive statement of compliance Applies to all entities, regardless of their nature, size or form of incorporation Similar requirements to King II King II Listed companies Financial institutions Public sector enterprises The directors should report in the annual report that the Code has been adhered to. Reasons should be given for non-compliance Governance framework Apply or explain as opposed to comply or else Comply or explain as opposed to comply or else Slide 2

5 Implications for companies, boards of directors and audit committees Scope of corporate governance framework in South Africa widened Entities encouraged to tailor the Code principles as appropriate to the size, nature and complexity of their businesses The board or those charged with governance should explain to stakeholders where a specific principle or recommendation has not been applied Slide

6 Slide 4

7 Slide 5

8 Slide 6

9 chapters Chapter 1 Chapter 2 Chapter 3 Chapter 4 Chapter 5 Chapter 6 Ethical Leadership and Corporate Citizenship Boards and Directors Audit Committees The Governance of Risk The Governance of Information, Communication and Technology (ICT) Compliance with Laws, Rules and Standards Chapter 7 Chapter 8 Chapter 9 Internal Audit Governing Stakeholder Relationships Integrated Reporting and Disclosure Slide 7

10 chapters Chapter 1 Chapter 2 Ethical Leadership and Corporate Citizenship Board composition Ethics programme/ framework Stakeholder inclusive strategies Boards and Directors Majority independent (non-executive) Directors CEO and CFO executive Directors Board charter and terms of reference for each sub-committee Disclosure of conflicts/ interests Chairperson independent, role defined, succession plan Delegation of authority framework CEO role formalised, performance evaluated Director nomination process and induction Company Secretary Board evaluations annually (disclose in integrated report) Remuneration policy Slide 8

11 chapters Chapter 3 Chapter 4 Audit Committees Members = at least 3; independent non-executive Directors Chairperson of the AC to be present at the AGM Oversight over integrated reporting Combined assurance model Review finance function (expertise, resources, experience) AC vs Risk Committee Report to Board on IFC and Systems of Risk and Control The Governance of Risk Separate Risk Committee? CRO? Formal risk assessment (at least annually) Adopt a risk management framework (e.g. COSO) Internal audit to provide a written assessment on the effectiveness of the system of internal controls and risk management to the Board (via the AC) Slide 9

12 chapters Chapter 5 Chapter 6 The Governance of Information, Communication and Technology (ICT) IT to be on the Board agenda (IT is strategic) IT governance and oversight CIO or similar IT internal control framework (e.g. Cobit) Board assurance on effectiveness of IT (including outsourced) Information Security Management System Compliance with Laws, Rules and Standards Board awareness and understanding on compliance Compliance programme/ framework and assurance Slide 10

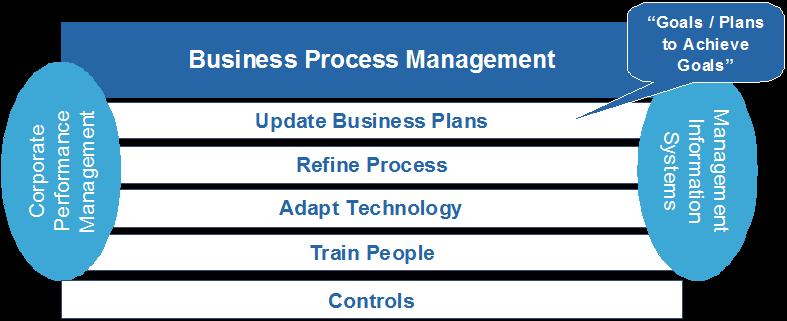

13 IT Risk Management Performance Responsimngt & value delivery Roles & bilities IT Governance Reporting Slide 11 IT Project Management IT Sustainability Alignment and Business IT Strategy IT Cost Management Security Information Management Information SUMMARY KING III IT GOVERNANCE Third Parties & Disposal Acquisition Planning Disaster Recovery

14 chapters Chapter 7 Chapter 8 Chapter 9 Internal Audit Written assessment on IFC and Risk Management/ Controls Independent Quality Assurance Review CAE to attend executive committee meetings Governing Stakeholder Relationships Identify important stakeholder groupings Stakeholder policy/ framework Communication guidelines Integrated Reporting and Disclosure Integrated report Audit Committee oversight Assurance over elements of non-financial/ sustainability information Slide 12

15 Disclosure requirements Integrated Report: Integrated financial and sustainability information of interest and concern to stakeholders. Forward-looking information that contextualizes financial results. Statement of application of, going concern. Disclosure regarding Directors. Statement by the board on Internal Controls. Statement by the board on Risk management as well as Internal Audit. Assurance on sustainability data. Managing stakeholder relations. Compliance statement as well as ethical performance. IT Reporting Commentary on financial results. Slide 13

Slide")

16 Integrated reporting Integrated Reporting Committee (IRC) of South Africa: Framework for Integrated Reporting and the Integrated Report Discussion Paper (25 January 2011) Slide 14

17 Integrated reporting refer: Slide 15

18 Chapter 1 Ethical leadership and corporate citizenship Board to provide effective leadership based on an ethical foundation Board to ensure that the company is and is seen to be a responsible corporate citizen Board to ensure that the company s ethics are managed effectively Key Implications/ Questions Does the Board s composition support the principles of corporate citizenship, sustainability and stakeholder inclusivity? Time to relook the Ethics Programme of the organisation? Slide 18

19 Chapter 2 Board and Directors The focal point for and custodian of corporate governance Strategy, risk, performance and sustainability are inseparable Effective ethical leadership and a responsible corporate citizen Ethics are managed effectively The company has an effective and independent audit committee Responsible for the governance of risk Responsible for information, communication and technology (ICT) governance Compliance with laws, adherence to rules/ codes/ standards (even non-binding ones) An effective risk-based internal audit Ensure the integrity of the company s integrated report (incl. effectiveness of system of internal control) Commence business rescue proceedings as soon as the company is financially distressed Chairman of the board who is an independent non executive director. The CEO of the company should not be chairman of the board (CEO delegation framework) always act in the company s best interest The board should comprise a balance of executives and non-executive directors, with a majority of nonexecutive directors Directors should be appointed through a formal process The evaluation of the board, its committees and the individual directors should be performed annually A governance framework should be agreed between the group and its subsidiary boards Companies should remunerate directors and executives fairly and responsibly Slide 19

20 Chapter 2 Boards and Directors Key Implications/ Questions Do we have the right people to lead the organisation? Is the board sufficiently independent of management? Is the Board/ sub-committee structures effective? Do the Board and sub-committee Charters require revision? Are the Board/ sub-committees performance properly evaluated? How do we incorporate strategy, risk, performance and sustainability into our decision-making philosophy? Slide 20

21 Chapter 3 Audit committees Chaired by an independent non-executive director The audit committee should oversee integrated reporting Audit committee should be satisfied on the expertise, resources and experience of the finance function Responsible for the oversight of internal audit An integral part of the risk management process Responsible for recommending the external auditor and overseeing the external audit process Report to the board and shareholders on how it has discharged its duties (including the effectiveness of internal financial controls) Key Implications/ Questions Is the Audit Committee capacitated to discharge its responsibilities? Is the Audit Committee ensuring that a combined assurance model is in place? Slide 21

22 Skills required of audit committee Audit committees collectively need to have understanding of: Integrated reporting Risk management Internal financial controls Internal and external audit process Sustainability reporting IT Governance relating to integrated reporting Corporate law Governance processes Assess effectiveness of Combined Assurance Slide 22

23 Combined Assurance Overview Management Internal assurance providers External assurance providers Combined assurance Slide 23

24 Membership and resources King II Membership Minimum number of members Majority of members to be independent non-executive directors Not addressed All members independent non-executive directors At least 3 members Chairman of board Not the chairman of the audit committee Preference for chairman of board not to be a member, may attend by invitation Not a member or chairman of audit committee May attend by invitation Slide 24

25 Integrated reporting Holistic and integrated presentation of company s finances and sustainability Financial results contextualised Reporting should be integrated across all areas of performance Audit Committee to recommend assurance on material sustainability/ non-financial issues Slide 25

26 Sustainability reporting King II did not address: - Oversight; or - Assurance of sustainability reporting requirements for audit committee: - Review sustainability reporting for reliability and consistency with financial information - Recommend the need to engage an external assurance provider Slide 26

27 Reporting on internal controls : Board responsibilities Integrated report to include a statement from board of directors on the effectiveness of the company s system of internal controls Who will give this assurance? Slide 27

28 Chapter 4 The governance of risk Board responsible for governance of risk Determine the levels of risk tolerance The risk committee or audit committee should assist the board in carrying out its risk responsibilities Management has the responsibility to design, implement and monitor the risk management plan Risk assessments are performed on a continuous basis (at least annually) Framework and methodologies are implemented to increase the profitability of anticipating unpredictable risks Management considered and implements appropriate risk responses Continuous risk monitoring by management The Board should receive combined assurance regarding the effectiveness of the risk management process Key Implications/ Questions How effective is the risk management plan? Are all types of risks considered, incl. fraud risk? Slide 28

29 Strategic, operational, and business risks underlie 80 % of the rapid declines in shareholder value Strategic & business 60 % Operational 20 % Financial 15 % Compliance 5 % Slide 29

30 The heart of the matter More CEOs intend to change their risk management process than any other element of their strategy or organisation Slide 30

31 Chapter 5 The governance of information, communication and technology (ICT) New chapter (not in King II) Board responsible for ICT governance IT to be aligned with business/ sustainability objectives Management has the responsibility for the implementation of ICT (per IT governance framework e.g. Cobit) Monitor and evaluate all ICT investments and expenditure Information assets should be effectively managed (integral part of risk management) Risk and audit committees to assist the Board with IT risks Slide 31

32 IT governance - highlights Dealt with in detail for the first time in IT governance should focus on four key areas: - Strategic alignment with the business and collaborative solutions, including the focus on sustainability and the implementation of green IT principles; - Value delivery: concentrating on optimising expenditure and proving the value of IT; - Risk management: addressing the safeguarding of IT assets, disaster recovery and continuity of operations; and - Resource management: optimising knowledge and IT infrastructure IT security should focus on three key areas: - Confidentiality - Integrity - Availability - COBIT may be used to check adequacy of the company s information security no one size fits all solution Slide 32

33 IT governance Implications/ questions for companies, boards of directors and audit committees The board should operate with IT governance in mind A thorough analysis on adherence of current IT operations IT should be on the board agenda (programme for implementation and what to explain to be signed of by the board) IT performance should be measured and reported to the board The board should set a management framework for IT governance based on a common approach (for example COBIT) Audit committees should oversee IT risks and controls Slide 33

34 Chapter 6 Compliance with laws, rules and standards The company complies with applicable laws and should consider adherence to non-binding rules and standards Board and Directors to have a working understanding of applicable legislative framework Compliance should form an integral part of the risk management process Implement and effective compliance framework and processes Key Implications/ Questions Where does compliance responsibility lie? Is the Board informed of compliance/ compliance exposure? Can our compliance efforts withstand scrutiny? Slide 34

35 Chapter 7 Internal Audit There is an effective risk based internal audit - Evaluating the company s governance processes - Objective assessment of the effectiveness of risk management and the internal control framework - Analysing and evaluating business process and associated controls - Adhere to the IIA Standards and Code of ethics Should follow a risk based approach to its plan - Informed by the strategy and risks of the company - Assess the company s risks and opportunities The audit committee should be responsible for the oversight of internal audit - Subjected to an independent quality review Slide 35

36 Internal Audit - continues Provide a written assessment of the effectiveness of the company s system of internal controls and risk management - An integral part of the combined assurance model as internal assurance provider - Internal controls should be established not only over financial matters, but also operational, compliance and sustainability issues - Internal audit should provide a written assessment of internal controls and risk management to the board - Written assessment of internal financial controls to the audit committee Should be strategically positioned to achieve its objectives - The CAE should have standing invitation to attend executive committee meetings - Internal audit function should be appropriately resourced and have sufficient budget allocated to the function - Skilled and resourced as is appropriate for the complexity and volume of risk and assurance needs - The CAE should develop and maintain a quality assurance and improvement programme - Written assessment of internal financial controls made available to the audit committee Slide 36

37 Risk-based internal audit Implications/ questions for companies, boards of directors and audit committees Internal audit planning and approach should be risk-based rather than compliance-based A CAE of appropriate stature, who has the respect and cooperation of the board and management, should be appointed Internal audit reporting lines to be evaluated internal audit should report at a level in the company that allows it to remain independent and objective to ensure it fully achieves its responsibilities Internal audit metrics must change to drive value adding CAE invited to attend company s executive committee Slide 37

38 Chapter 8 Governing stakeholder relationships Appreciate how stakeholder s perceptions affect a company s reputation Management to proactively deal with stakeholder relationships Strive to achieve the appropriate balance between its various stakeholders groupings in the best interests of the company Equitable treatment of shareholders Transparent and effective communication with stakeholders Disputes are resolved as effectively and expeditiously as possible Slide 38

39 Chapter 8 Governing stakeholder relationships Key Implications/ Questions Do we have a stakeholder strategy and policies in place? Have we identified our material stakeholders (incl. the associated issues, risks and concerns)? How do we actually engage with all our stakeholders in practice? Slide 39

40 Chapter 9 Integrated reporting and disclosure Integrity of the company s integrated report Sustainability and disclosure should be integrated with the company s financial reporting Sustainability reporting and disclosure should independently assured Why? The market capitalisation of any company equals its economic value, not its book value Integrated report consists of - Annual financial statements; and - Integrated sustainability (economic, social and environmental) information Slide 40

41 Integrated reporting - highlights Integrated report should be prepared annually Integrated reporting should be balanced between positive aspects and challenges facing the business Integrated report should also provide forward-looking information Integrated report should contain a board statement on the effectiveness of the company s internal financial controls Board may delegate responsibility for, and review of the sustainability information to either the risk committee, sustainability committee or audit committee Slide 41

42 Integrated reporting Implications/ questions for companies, boards of directors and audit committees Companies to dedicate time and resource to the preparation of integrated report Integrated reporting entails more than a mere add-on of economic, social and environmental information in the annual report sustainability reporting to be embedded in the organisation Responsibility of the audit committee may be extended beyond financial reporting to include sustainability reporting Audit committees may need additional expertise in discharging their responsibilities Slide 42

43 Thank you For more information contact Frank Muller Associate Director: Internal Audit, Risk and Governance Services Slide 43

44 The practical application of Appendices Detailed questions per Chapter

45 Ch 1. Key questions for management Ethics and Leadership Corporate citizenship, sustainability and stakeholder inclusivity requires judgement, balance and compromise. Does the board have the right composition, skills and reliable data to make these types of judgement calls? Have we assessed the moral and economic imperatives of corporate citizenship? Have we taken this into account when reviewing our corporate strategy? Citizenship and sustainability risks may be obscure or indirect. How do we identify and manage these risks as well as opportunities? Do we have policies in place that will guide every level of the business in terms of expected behaviours and practices and with reference to our interaction with all material stakeholders? Do we measure the impact or lack thereof, of our corporate citizenship initiatives? Slide 45

46 Ch 2. Key questions for management Boards and Directors Do we have the right people in place to lead and manage all aspects of our business? Is the board sufficiently independent of management? Do we need to get external expert advice? Will we get greater value from board and committee evaluations if we employ an independent service provider? Are we comfortable that we have satisfied our overarching responsibilities adequately where we have delegated functions to sub committees? Are we spending our time efficiently in meetings and dealing only with material issues? Is there a need to revise our board and committee charters? In which committee should we deal with sustainability issues? Are the current roles and structures of our subsidiary boards adding value? How do we incorporate strategy, risk, performance and sustainability into our decision making philosophy? Slide 46

47 Ch 3. Key questions for management Audit Committees Does the audit committee have the appropriate blend of skills to discharge its responsibilities? What level of reliance may the audit committee place on the company s finance team? Will the committee need to recruit additional members in order to meet the new requirements for minimum numbers of non executive and independent directors? Does the committee have the necessary skills to oversee integrated reporting? How will the committee determine the most appropriate mix of internal auditors, external auditors and management to assess the application of the combined assurance model? Slide 47

48 Ch 4. Key questions for management Risk Do we understand how risk appetite and tolerance is applied in our organisation? How do we know that the biggest risk exposures to our organisation are being adequately managed? When last did we participate in a risk assessment activity? How often have we considered the same risk-related issue in the various management and governance meetings? Is ICT risk actively considered in our risk management process? Do we specifically consider compliance risk and, if so, how satisfied are we that it is effectively covered? Are risks prioritised and ranked to focus the responses and interventions on those risks outside the board s risk tolerance limits? Do we have an approved annual risk management plan? Who assures non financial risks, such as plant availability, staff capacity and competency, the impact of legislative changes on the business/organisation etc? And to which management or board committee is the assurance provided? Are we satisfied that this assurance is reliable? Do we have a fraud risk plan to consider our fraud exposure and prevention? Does our disclosure on the effectiveness of risk management reflect the actual position of our business/organisation? Slide 48

49 Ch 5. Key questions for management Information, Communication and Technology (ICT) Do we understand how IT decisions are taken and who is accountable? Do we have an IT Governance framework in place which defines and supports decision models, governance structures, accountability and governance processes? Is IT involved in strategic business decisions and planning? Is the investment in IT understood? Is our Intellectual Property, company and client information properly protected? How do we ensure compliance of IT against laws, rules, codes, standards and regulations? How is the value delivered by IT measured? Is the approach towards IT risks facing the organisation clear? I.e. risk-avoidance vs. risktaking? Is the board regularly briefed on IT risks to which the enterprise is exposed? Is IT a regular item on the agenda of the board and is it addressed in a structured manner? Does the board have a clear view on the major IT investments from a risk and return perspective? Does the board obtain regular progress reports on major IT projects? Is the board getting independent assurance on the achievement of IT objectives and the containment of IT risks? Slide 49

50 Ch 6. Key questions for management Compliance What are the key statutory and regulatory obligations to which our organisation needs to comply? Are we in compliance with these requirements? If so, how have we received this assurance and are we satisfied that the assurance is credible? When last did we consider compliance at the board? Are we aware that many Acts, such as the National Credit Act, can impact our organisation even though we are not a financial institution? How are we apprised of changes in the legal and regulatory landscape? Do we have sufficient evidence to defend your organisation in court or to prove to a regulator that we have complied with a specific act? Does our disclosure on the effectiveness of compliance reflect the actual position in our business/organisation? Slide 50

51 Ch 7. Key questions for management Internal Audit Is internal audit aligned to strategy and does its plan focus on areas that are most likely to impact stakeholder value? Is internal audit effective and frequent enough in its communications with the audit committee and us? When last was an objective assessment as to whether internal audit has the appropriate level of technical and analytical skills required to address the industry risk and risk requirements of your business? Is our internal audit function poised to lead a combined assurance initiative? Is there sufficient assurance of our ethics and risk management programmes? Does internal audit utilise technology in its processes and use existing systems and data effectively in the performance of its work? What were our most recent loss events and what comfort did internal audit provide us with on these? How does our internal audit function compare against its peers in benchmark studies? Is our Chief Audit Executive subjected to a robust annual assessment based on key attributes relevant to our business? What is our true absorbed cost of internal audit? Is our internal audit agile enough to address emerging business issues? Slide 51

52 Ch 8. Key questions for management Stakeholder Relationships Do we have a stakeholder strategy and policies in place? If so, are they adequate or do they need revamping? If not, do we have the in-house knowledge to draft documents that will deliver value? Have we identified our material stakeholders? Do we know and understand the issues, risks and opportunities associated with our various stakeholders? Are our current forms of stakeholder communication effective? Do we have the necessary reliable information to make informed judgement calls when balancing the legitimate interests of various stakeholder groupings? How do we actually engage with all our stakeholders in practice? Slide 52

53 Ch 9. Key questions for management Integrated Reporting Does the company have a sustainability strategy and policy? Is sustainability considered part of ongoing business activities? Are sustainable development issues integrated into business management systems and departments such as risk, environmental, legal and financial? Have sustainability criteria been built into individual performance agreements? Do you have a suitably qualified director/s and executive/s with the responsibility for sustainable development? Does an integrated report mean one document? Who in the company is the custodian of the content and assurance of the integrated report? Do we have to follow the GRI G3 guidelines? Slide 53

54 The practical application of Exotics Boards and directors, acting in the best interests of the company, form the focal point of corporate governance

55 The practical application of Sustainability Sustainability is listed second, only to effective leadership, as a key aspect of. A key challenge for leadership is to mainstream sustainability issues : i.e. integrate strategy, sustainability and governance. Slide 55

to")

56 Statement on effectiveness of internal financial controls by the board of directors Board responsible for the integrity of financial reporting systems Board to make a statement in the integrated report on the effectiveness of internal financial controls Audit committee should report to the board on effectiveness of internal financial controls annually Management (or internal audit) to conduct a formal documented review of design, implementation and effectiveness of internal financial controls on an annual basis Slide 56

57 Statement on effectiveness of internal financial controls by the board of directors How does this compare to the SOX requirement? Section 404 of Sarbanes-Oxley Act: Annual report should include an internal control report that - States management s responsibility for establishing and maintaining an adequate internal control structure and procedures for financial reporting and - Contains an assessment of the effectiveness of the internal control structure and procedures of the issuer for financial reporting Attestation from the external auditors required on management s assertion regarding internal financial control highlights that SOX s statutory requirements for rigorous internal controls has not prevented collapse of many leading names in US banking and finance - and SOX similar in requiring directors to make a statement on the effectiveness of internal financial controls - does not require attestation from external auditors on internal financial controls Slide 57

58 Setting the Scene Observation on the Impact of Internal Financial Control It is worth noting that Sarbanes-Oxley legislation established a new paradigm for corporate accountability. Responsibilities of the audit committee, CEO and CFO were clearly established at higher levels than in the past. It created a new standard for companies regarding the reporting of internal control effectiveness and has raised the bar for the design, documentation, and operation of internal financial control. Good internal control will ensure sustained business development! Slide 58

59 Typical Internal Financial Control Project Approach Continuous Improvement Management Internal Auditor Initiate Project And Assess Risk Document and Evaluate Control Design Remediate Test Operating Effectiveness Prepare Report on Internal Control and embed through Training & accountability Monitor and Report Project Management Support Slide 59

60 Approach DESIGN IMPLEMENTATION TESTING MAINTENANCE Significant Account identification Top down approach Identify controls at a Corporate Reporting Level first to mitigate risks identified during the design phase Risk Assessment Consolidate risks identified during design phase Project Set-up Expected Controls Document Actual Controls - Corporate Reporting (First layer) - Regional Offices (Second layer) - Business Unit (Third layer) Evaluate Design Effectiveness Walkthrough Remediate Test Operating Effectiveness Ongoing Maintenance, Training & Awareness Project Management, Communication, Issue Management, Change Management, Training, Internal audit testing Slide 60

61 Cost Benefit Analysis Benefits Increased executive management and audit committee confidence Enhanced control environment, awareness and discipline Improved Audit Committee oversight Increased knowledge of internal business processes Identification of improvement opportunities in both controls and processes Fewer control failure embarrassments Increased comfort for senior management Better quality audits (internal and external) Formalisation of processes and controls Increased awareness of internal controls at various levels within the business End to end process ownership and accountability Slide 61

62 Thinking Ahead Creating a Sustainable Process This should not be seen as a one-time event Efficient and effective processes must be developed to sustain board reporting Management needs to design and sustain a process that Provides a solid base for management s quarterly and annual reporting Is seamlessly embedded with other business processes Achieve efficiency and effectiveness in documenting, updating and assessing company control documentation, as well as company policies Reduce administrative burden in assuring a sound internal control environment Enables management/internal audit to identify, report and remediate control deficiencies in a timely manner Proactively deals with change in people, processes and technology Eliminating redundant or inefficient processes that add little value to the company and its control environment King 11III Slide 62

63 Key questions for management Internal Financial Control Is there a control framework (e.g. COSO) governing financial reporting in the organisation? Have we identified and documented all probable risks to fair presentation in the financial statements and disclosures? (Fair presentation implies that the numbers and disclosures are not materially misstated). Are there controls in place to address these risks and are they adequately designed to prevent or detect material misstatements in the financial statements and disclosures? Do the controls identified operate as they are supposed to and are they appropriately evidenced? Have we examined or tested the controls identified above to ensure that our report to the audit committee is accurate and complete? Have we appropriately evidenced our assessment? Is a process in place to ensure that the framework remains relevant over time? Slide 63

64 Combined assurance What is combined assurance? A coordinated approach to all assurance activities to ensure that assurance provided by - management; - internal assurance providers (such as internal audit); and - external assurance providers (such as external audit or sustainability assurance providers) adequately addresses significant risks facing the company and that suitable controls exist to mitigate and reduce these risks Integrating and aligning assurance processes in an organisation to maximise risk and governance oversight and control efficiencies, and optimise overall assurance to the Audit and Risk Committee, considering the organisation s risk appetite Slide 64

65 Combined assurance (continued) What is combined assurance? Management Internal assurance providers External assurance providers Combined assurance Slide 65

66 Risk and Audit committees ask Where do we get our assurance from? Who is the custodian of assurance in the organisation? Who is ultimately confirming all is in order in the governance/risk space? Are we sure that our controls financial and operational - are robust and our risk management mechanisms would highlight concerns? Slide 66

67 Combined assurance Implications for audit committees Audit committees are able to assess significant risks facing the company with information to hand Assessment to be made of in-house skills and qualifications and track record of external service providers Audit committees to coordinate the utilisation of appropriate assurance providers in the assurance model (management, internal or external assurance providers) to provide assurance on the identified risks May result in the increased utilisation of external assurance providers Slide 67

68 Key questions for management Alternate Dispute Resolution Is our organisation involved in significant disputes? What do these disputes teach us about our customers/suppliers and our own approach to business? Has negotiation failed in these disputes? Can we consider ADR processes? E.g. mediation, conciliation Is there potentially value to be added in changing the dispute mechanism form an enforcement of rights process to a partnership approach? Has the organisation considered adopting a dispute response plan? Slide 68

69 Key questions for management Business Rescue Are there signs of a future potential need for business rescue and can they act sooner to avert this and seek assistance to turnaround the company? Is the company financially distressed? Are there reasonable prospects of rescuing the company? Is the company or its directors trading recklessly? Should we commence business rescue proceedings? Who should we appoint as the business rescue practitioner? Is this person independent and sufficiently experienced to rescue the business? What are the board s obligations to stakeholders, the courts and appointed representatives? Are we aware of and fulfilling our obligations as a board and individual directors in line with the requirements of the business rescue proceedings? Slide 69

70 Corporate Governance Framework Internal Audit s journey COMBINED ASSURANCE RISK MANAGEMENT FINANCIAL SOCIAL & ETHICAL ENVIRON- MENTAL INTERNAL CONTROLS INTEGRATED REPORT ACCOUNTABILITY CORPORATE CULTURE ETHICS CONDUCT OPERATIONS PEOPLE SYSTEMS PROCESS LEGAL REGULATORY COMPLIANCE REQUIREMENTS POLICY AUTHORITIES STRUCTURE PURPOSE STRATEGY VALUES GOALS PERFORMANCE MEASUREMENT Slide 70

71 The Integrated Business Model Slide 71

CORPORATE GOVERNANCE King III - Compliance with Principles Assessment Year ending 31 December 2016

No N/A 1 Chapter 1 - Ethical leadership and corporate citizenship 1.1 The board s should provide effective leadership based on an ethical foundation 1.2 The board should ensure that the Company is and

No N/A 1 Chapter 1 - Ethical leadership and corporate citizenship 1.1 The board s should provide effective leadership based on an ethical foundation 1.2 The board should ensure that the Company is and

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017 This document has been prepared in terms of the JSE Listing Requirements and sets out the application of the 75 corporate governance principles by

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017 This document has been prepared in terms of the JSE Listing Requirements and sets out the application of the 75 corporate governance principles by

Explanation where the company has partially applied or not applied King III principles

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,

Chapter 1 : Ethical leadership and corporate citizenship. Principle 1.1: The board should provide effective leadership based on an ethical foundation.

Chapter 1 : Ethical leadership and corporate citizenship Principle 1.1: The board should provide effective leadership based on an ethical foundation. The board is responsible for corporate governance and

Chapter 1 : Ethical leadership and corporate citizenship Principle 1.1: The board should provide effective leadership based on an ethical foundation. The board is responsible for corporate governance and

Strate Compliance with King III. Prepared by: Company Secretary

Strate Compliance with King III Prepared by: Company Secretary 1 ETHICAL LEADERSHIP AND CORPORATE RESPONSIBILITY Responsible leadership 1.1 The board should provide effective leadership based on an ethical

Strate Compliance with King III Prepared by: Company Secretary 1 ETHICAL LEADERSHIP AND CORPORATE RESPONSIBILITY Responsible leadership 1.1 The board should provide effective leadership based on an ethical

Corporate Governance Principles 2015

Corporate s 2015 corporate principles 1 corporate principles 1. Ethical leadership and corporate citizenship Responsible leadership 1.1 The board should provide effective leadership based on an ethical

Corporate s 2015 corporate principles 1 corporate principles 1. Ethical leadership and corporate citizenship Responsible leadership 1.1 The board should provide effective leadership based on an ethical

CORPORATE GOVERNANCE

CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report No. Area Requirement Status Comments 1. Ethical Leadership and Corporate

CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report No. Area Requirement Status Comments 1. Ethical Leadership and Corporate

King lll Principle Comments on application in 2013 Reference in 2013 Integrated Report

Application of King III Principles 2013 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles by the Clicks Group. The following

Application of King III Principles 2013 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles by the Clicks Group. The following

MICROMEGA CORPORATE GOVERNANCE

MICROMEGA CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report No. Area Requirement Status Comments 1. Ethical leadership and

MICROMEGA CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report No. Area Requirement Status Comments 1. Ethical leadership and

King lll Principle Comments on application in 2016 Reference Chapter 1: Ethical leadership and corporate citizenship Principle 1.

Clicks Group Application of King III Principles 2016 APPLICATION OF King III PrincipleS 2016 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King

Clicks Group Application of King III Principles 2016 APPLICATION OF King III PrincipleS 2016 This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King

CORPORATE GOVERNANCE King III - Compliance with Principles Assessment Year ending 31 December 2015

No N/A 1 Chapter 1 - Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation 1.2 The Board should ensure that the Company is and is

No N/A 1 Chapter 1 - Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation 1.2 The Board should ensure that the Company is and is

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016 This table is a useful reference to each of the King III principles and how, in broad terms, they have been applied by the Group. KING III ETHICAL

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2016 This table is a useful reference to each of the King III principles and how, in broad terms, they have been applied by the Group. KING III ETHICAL

This document contains a summary of the Group s application of all of the principles contained in King III.

King III Compliance The Board supports the Code of Corporate Practices and Conduct as recommended by the King III Report on Corporate Governance for South Africa 2009 ( King III ). This document contains

King III Compliance The Board supports the Code of Corporate Practices and Conduct as recommended by the King III Report on Corporate Governance for South Africa 2009 ( King III ). This document contains

Phumelela Gaming and Leisure Limited

King III assessment register 2015 CHAPTER 1: ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP 1.1 The Board should provide effective leadership based on an ethical foundation. 1.2 The Board should ensure that

King III assessment register 2015 CHAPTER 1: ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP 1.1 The Board should provide effective leadership based on an ethical foundation. 1.2 The Board should ensure that

1. Ethical leadership and corporate citizenship. 2. Boards and directors. Role and function of the board

CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report Area Requirement Status Comments 1. Ethical leadership and corporate citizenship

CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report Area Requirement Status Comments 1. Ethical leadership and corporate citizenship

KING III CHECKLIST. We do it better

KING III CHECKLIST 2016 We do it better 1 KING III CHECKLIST African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance for South

KING III CHECKLIST 2016 We do it better 1 KING III CHECKLIST African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance for South

Lewis Group Limited Application of King III Corporate Governance Principles March 2017

Lewis Group Limited Application of King III Corporate Governance Principles March This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles

Lewis Group Limited Application of King III Corporate Governance Principles March This document has been prepared in terms of the JSE Listings Requirements and sets out the application of King III principles

Ethical leadership and corporate citizenship. Applied. Applied. Applied. Company s ethics are managed effectively.

CORPORATE GOVERNANCE- KING III COMPLIANCE Analysis of the application as at 24 June 2015 by Master Drilling Group Limited (the Company) of the 75 corporate governance principles as recommended by the King

CORPORATE GOVERNANCE- KING III COMPLIANCE Analysis of the application as at 24 June 2015 by Master Drilling Group Limited (the Company) of the 75 corporate governance principles as recommended by the King

OVERVIEW OF KING III PRINCIPLES

OVERVIEW OF KING III PRINCIPLES This checklist has been prepared in terms of the JSE Listings Requirements and sets out Brimstone s approach to corporate governance in relation to the King Report on Governance

OVERVIEW OF KING III PRINCIPLES This checklist has been prepared in terms of the JSE Listings Requirements and sets out Brimstone s approach to corporate governance in relation to the King Report on Governance

KING III CHECKLIST. In accordance with the Board Charter the board is the guardian of the values and ethics of the group.

KING III CHECKLIST Principle number Description Compliance Chapter 1: Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2

KING III CHECKLIST Principle number Description Compliance Chapter 1: Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2

King iii checklist 2013

King III checklist 2013 King III checklist 2013 1 King III checklist African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance

King III checklist 2013 King III checklist 2013 1 King III checklist African Rainbow Minerals Limited (ARM or the Company) supports the principles and practices set out in the King Report on Governance

KING IV GOVERNANCE PRINCIPLES APPLICATION BY MURRAY & ROBERTS FY The governing body should lead ethically and effectively (Leadership)

") KING IV GOVERNANCE PRINCIPLES APPLICATION BY MURRAY & ROBERTS FY2018 LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP 1. The governing body should lead ethically and effectively (Leadership) The Board is the

KING IV GOVERNANCE PRINCIPLES APPLICATION BY MURRAY & ROBERTS FY2018 LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP 1. The governing body should lead ethically and effectively (Leadership) The Board is the

The Institute of Directors of South Africa ( IoDSA ) is the convener of the King Committee and the custodian of the King reports and practice notes.

is the convener of the King Committee and the custodian of the King reports and practice notes.") ANDULELA INVESTMENT HOLDINGS LIMITED CORPORATE GOVERNANCE Corporate Governance Overview December 2016 The Board of Directors is committed to the implementation of good corporate governance within the group

ANDULELA INVESTMENT HOLDINGS LIMITED CORPORATE GOVERNANCE Corporate Governance Overview December 2016 The Board of Directors is committed to the implementation of good corporate governance within the group

KING REPORT ON GOVERNANCE FOR SOUTH AFRICA 2009 (KING III)

") UPDATED: 18 FEBRUARY 2015 KING REPORT ON GOVERNANCE PRINCIPLE PER KING III ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP 1.1 The board should provide effective leadership based on an ethical foundation.

UPDATED: 18 FEBRUARY 2015 KING REPORT ON GOVERNANCE PRINCIPLE PER KING III ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP 1.1 The board should provide effective leadership based on an ethical foundation.

WG WEARNE LIMITED (Registration number: 1994/005983/07) ( the Company / Wearne )

( the Company / Wearne )") WG WEARNE LIMITED (Registration number: 1994/005983/07) ( the Company / Wearne ) ANALYSIS OF THE APPLICATION OF THE 75 CORPORATE GOVERNANCE PRINCIPLES AS RECOMMENDED IN THE KING III REPORT CHAPTER 1: ETHICAL

WG WEARNE LIMITED (Registration number: 1994/005983/07) ( the Company / Wearne ) ANALYSIS OF THE APPLICATION OF THE 75 CORPORATE GOVERNANCE PRINCIPLES AS RECOMMENDED IN THE KING III REPORT CHAPTER 1: ETHICAL

Applied / Partially. Explanation / Compensating Practices. Not Applied. Chapter Principle Principle Description

/ Partially Chapter Principle Principle Description / Not IoDSA GAI Score Chapter 1 Principle 1.1 The Board provides effective leadership based on ethical foundation Chapter 1 Principle 1.2 The Board ensures

/ Partially Chapter Principle Principle Description / Not IoDSA GAI Score Chapter 1 Principle 1.1 The Board provides effective leadership based on ethical foundation Chapter 1 Principle 1.2 The Board ensures

MAZOR GROUP LIMITED CORPORATE GOVERNANCE COMPLIANCE KING III REGISTER

MAZOR GROUP LIMITED CORPORATE GOVERNANCE COMPLIANCE KING III REGISTER Mazor Group Limited has in its Integrated Report for 2015 disclosed its level of compliance with the King Code of Corporate Governance

MAZOR GROUP LIMITED CORPORATE GOVERNANCE COMPLIANCE KING III REGISTER Mazor Group Limited has in its Integrated Report for 2015 disclosed its level of compliance with the King Code of Corporate Governance

CORPORATE GOVERNANCE KING III COMPLIANCE

CORPORATE GOVERNANCE KING III COMPLIANCE Analysis of the application as at March 2013 by AngloGold Ashanti Limited (AngloGold Ashanti) of the 75 corporate governance principles as recommended by the King

CORPORATE GOVERNANCE KING III COMPLIANCE Analysis of the application as at March 2013 by AngloGold Ashanti Limited (AngloGold Ashanti) of the 75 corporate governance principles as recommended by the King

Analysis of the application of the 75 corporate governance principles as recommended in the King III report

King III report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2 The board should ensure that the company is and is

King III report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2 The board should ensure that the company is and is

CORPORATE GOVERNANCE

M ICROM EGA HOLDINGS LTD KING-III75 PRINCIPLES 31 M ARCH 2017 No. 1. CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report Area

M ICROM EGA HOLDINGS LTD KING-III75 PRINCIPLES 31 M ARCH 2017 No. 1. CORPORATE GOVERNANCE Analysis of the application of the 75 corporate governance principles as recommended in the King III Report Area

GOLD BRANDS INVESTMENTS LIMITED

Applied/ Chapter 1 - Ethical leadership and corporate citizenship 1,1 The Board should provide effective leadership based on an ethical foundation. The Board and the Company subscribe to a Code of Ethics

Applied/ Chapter 1 - Ethical leadership and corporate citizenship 1,1 The Board should provide effective leadership based on an ethical foundation. The Board and the Company subscribe to a Code of Ethics

PRINCIPLES OF CORPORATE GOVERNANCE Novus Holdings Limited

PRINCIPLES OF CORPORATE GOVERNANCE Novus Holdings Limited KING III APPLICATION The Directors have pro-actively taken steps to ensure that the Company is fully compliant with the King Code recommendations

PRINCIPLES OF CORPORATE GOVERNANCE Novus Holdings Limited KING III APPLICATION The Directors have pro-actively taken steps to ensure that the Company is fully compliant with the King Code recommendations

KING III COMPLIANCE ANALYSIS

Principle element No Application method or explanation This document has been prepared in terms of the JSE Listings Requirements and sets out the application of the 75 Principles of the King III Report

Principle element No Application method or explanation This document has been prepared in terms of the JSE Listings Requirements and sets out the application of the 75 Principles of the King III Report

KING III ON CORPORATE GOVERNANCE. The AEEI level of compliance continually increases since the introduction of the Code.

KING III ON CORPORATE GOVERNANCE The Board of African Equity Empowerment Investments Limited (AEEI) remains committed to and endorses the principles of the Code of Corporate Practices and Conduct as set

KING III ON CORPORATE GOVERNANCE The Board of African Equity Empowerment Investments Limited (AEEI) remains committed to and endorses the principles of the Code of Corporate Practices and Conduct as set

Application of King III Principles

Application of King III Principles Principle Status Application 1. Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation. The ethical

Application of King III Principles Principle Status Application 1. Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation. The ethical

Application of King III Corporate Governance Principles

Application of Corporate Governance Principles / 1 This table is a useful reference to each of the principles and how, in broad terms, they have been applied by the Group. The information should be read

Application of Corporate Governance Principles / 1 This table is a useful reference to each of the principles and how, in broad terms, they have been applied by the Group. The information should be read

Analysis of the application of the

King III Report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation 1.2 The board should ensure that the company is and is seen

King III Report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation 1.2 The board should ensure that the company is and is seen

CORPORATE GOVERNANCE REPORT

CORPORATE GOVERNANCE REPORT The board is of the opinion that the group has complied throughout the accounting period with all the objectives incorporated in the Code of Governance Principles for South

CORPORATE GOVERNANCE REPORT The board is of the opinion that the group has complied throughout the accounting period with all the objectives incorporated in the Code of Governance Principles for South

BSI Steel Limited. King III Compliance

BSI Steel Limited King III Compliance Area Requirement Status Comments 1. Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation 1.2

BSI Steel Limited King III Compliance Area Requirement Status Comments 1. Ethical leadership and corporate citizenship 1.1 The Board should provide effective leadership based on an ethical foundation 1.2

SHOPRITE HOLDINGS LTD. King III Reporting in terms of the JSE Listings Requirements

1 SHOPRITE HOLDINGS LTD King III Reporting in terms of the JSE Listings Requirements The JSE Listings Requirements require all JSE-listed companies to provide a narrative on how it has applied the new

1 SHOPRITE HOLDINGS LTD King III Reporting in terms of the JSE Listings Requirements The JSE Listings Requirements require all JSE-listed companies to provide a narrative on how it has applied the new

KING IV APPLICATION REGISTER. We do it better

KING IV APPLICATION REGISTER 2017 We do it better 1 KING IV APPLICATION REGISTER APPLICATION OF KING IV African Rainbow Minerals Limited (ARM or the Company) supports the governance outcomes, principles

KING IV APPLICATION REGISTER 2017 We do it better 1 KING IV APPLICATION REGISTER APPLICATION OF KING IV African Rainbow Minerals Limited (ARM or the Company) supports the governance outcomes, principles

CORPORATE GOVERNANCE KING CODE

CORPORATE GOVERNANCE KING CODE The Board of Directors of RECM and Calibre Limited ( RAC ) ( The Board ) supports the King III Report ( King Code ) on Corporate Governance, with corporate governance being

CORPORATE GOVERNANCE KING CODE The Board of Directors of RECM and Calibre Limited ( RAC ) ( The Board ) supports the King III Report ( King Code ) on Corporate Governance, with corporate governance being

Analysis of the application of the 75 corporate governance principles as recommended in the King III Report

the King III Report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2 The board should ensure that the company is and

the King III Report 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation. 1.2 The board should ensure that the company is and

APPLICATION OF PRINCIPLES IN KING III

APPLICATION OF PRINCIPLES IN KING III Zeder Investments Ltd ( Zeder ) is committed to the principles of transparency, integrity, fairness and accountability as also advocated in the King Code of Governance

APPLICATION OF PRINCIPLES IN KING III Zeder Investments Ltd ( Zeder ) is committed to the principles of transparency, integrity, fairness and accountability as also advocated in the King Code of Governance

Corporate Governance. This King III Reporting is prepared in terms of the JSE Listings Requirements for the period 01 July 2015 to 30 June 2016

Corporate Governance This King III Reporting is prepared in terms of the JSE Listings Requirements for the period 01 July 2015 to 30 June 2016 [King III apply or explain approach is set out below] Compliant

Corporate Governance This King III Reporting is prepared in terms of the JSE Listings Requirements for the period 01 July 2015 to 30 June 2016 [King III apply or explain approach is set out below] Compliant

KING CODE APPLICATION GAP ANALYSIS

KING CODE APPLICATION GAP ANALYSIS Principle Status Narrative Action plan 1.1 The Board should provide effective leadership based on an ethical foundation 1.2 The Board should ensure that the company is

KING CODE APPLICATION GAP ANALYSIS Principle Status Narrative Action plan 1.1 The Board should provide effective leadership based on an ethical foundation 1.2 The Board should ensure that the company is

PICK N PAY STORES LIMITED KING III REPORT. Introduction. Summary of the application of King III principles

PICK N PAY STORES LIMITED KING III REPORT Introduction The Board takes guidance from: The King Report on Governance for South Africa 2009 (King III) JSE Listings Requirements Companies Act, no. 71 of 2008,

PICK N PAY STORES LIMITED KING III REPORT Introduction The Board takes guidance from: The King Report on Governance for South Africa 2009 (King III) JSE Listings Requirements Companies Act, no. 71 of 2008,

CORPORATE GOVERNANCE PRINCIPLES

CORPORATE GOVERNANCE or 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation Pg 6, 13 1.2 The board should ensure that the company

CORPORATE GOVERNANCE or 1. Ethical leadership and corporate citizenship 1.1 The board should provide effective leadership based on an ethical foundation Pg 6, 13 1.2 The board should ensure that the company

CORPORATE GOVERNANCE

Full Partial None CORPORATE GOVERNANCE This document has been prepared in terms of the JSE Listings Requirements and sets out Distell Group Limited s application of the principles contained in King III.

Full Partial None CORPORATE GOVERNANCE This document has been prepared in terms of the JSE Listings Requirements and sets out Distell Group Limited s application of the principles contained in King III.

TOYOTA FINANCIAL SERVICES (SOUTH AFRICA) LIMITED

LIMITED") FOR THE YEAR ENDED 31 MARCH 2016 KING III - PRINCIPLES TOYOTA FINANCIAL SERVICES (SOUTH AFRICA) LIMITED (TFSSA) To be read in conjunction with the 2016 Integrated Report Toyota Financial Services (South

FOR THE YEAR ENDED 31 MARCH 2016 KING III - PRINCIPLES TOYOTA FINANCIAL SERVICES (SOUTH AFRICA) LIMITED (TFSSA) To be read in conjunction with the 2016 Integrated Report Toyota Financial Services (South

Toyota Financial Services (South Africa) Limited: King III Principles

Limited: King III Principles") FOR THE YEAR ENDED 31 MARCH 2017 KING III - PRINCIPLES TOYOTA FINANCIAL SERVICES (SOUTH AFRICA) LIMITED (TFSSA) To be read in conjunction with the 2017 Annual Financial Statements Toyota Financial Services

FOR THE YEAR ENDED 31 MARCH 2017 KING III - PRINCIPLES TOYOTA FINANCIAL SERVICES (SOUTH AFRICA) LIMITED (TFSSA) To be read in conjunction with the 2017 Annual Financial Statements Toyota Financial Services

King IV Application Register

King IV Register 1. The governing body should lead ethically and effectively. The directors hold one another accountable for decision-making based on integrity, competence, responsibility, fairness and

King IV Register 1. The governing body should lead ethically and effectively. The directors hold one another accountable for decision-making based on integrity, competence, responsibility, fairness and

Application of the King IV Report on Corporate Governance for South Africa 2016 SASOL INZALO PUBLIC (RF) LIMITED

LIMITED") Application of the King IV Report on Corporate Governance for South Africa 2016 1 July 2017 Ethical culture Good performance Effective control Legitimacy SASOL INZALO PUBLIC (RF) LIMITED Although the King

Application of the King IV Report on Corporate Governance for South Africa 2016 1 July 2017 Ethical culture Good performance Effective control Legitimacy SASOL INZALO PUBLIC (RF) LIMITED Although the King

Corporate governance report

Corporate governance report Deneb is committed to a high standard of corporate governance and endorses the recommendations contained in the King Code of Governance Principles for South Africa 2009 (King

Corporate governance report Deneb is committed to a high standard of corporate governance and endorses the recommendations contained in the King Code of Governance Principles for South Africa 2009 (King

TRANS HEX GROUP LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES

TRANS HEX GROUP LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES Trans Hex Group Limited (Transhex or the Company ) is a listed company on the Johannesburg Stock Exchange operated by the JSE Limited

TRANS HEX GROUP LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES Trans Hex Group Limited (Transhex or the Company ) is a listed company on the Johannesburg Stock Exchange operated by the JSE Limited

Corporate Governance/King III and Companies Act 71 of 2008 ( Companies Act ) reviews. [King III s apply or explain approach will be addressed below]

![Corporate Governance/King III and Companies Act 71 of 2008 ( Companies Act ) reviews. [King III s apply or explain approach will be addressed below]](/thumbs/87/95550502.jpg "Corporate Governance/King III and Companies Act 71 of 2008 ( Companies Act ) reviews. [King III s apply or explain approach will be addressed below]") Corporate Governance/King III and Companies Act 71 of 2008 ( Companies Act ) reviews [King III s apply or explain approach will be addressed below] Compliant Under review X Non-compliant # Partially compliant

Corporate Governance/King III and Companies Act 71 of 2008 ( Companies Act ) reviews [King III s apply or explain approach will be addressed below] Compliant Under review X Non-compliant # Partially compliant

NAMPAK LIMITED Application of the King IV Report on Corporate Governance for South Africa 2016 ( King IV TM )

") NAMPAK LIMITED Application of the King IV Report on Corporate Governance for South Africa 2016 ( King IV TM ) Nampak Limited ( Nampak or the Company ) is a listed company on the Johannesburg Stock Exchange

NAMPAK LIMITED Application of the King IV Report on Corporate Governance for South Africa 2016 ( King IV TM ) Nampak Limited ( Nampak or the Company ) is a listed company on the Johannesburg Stock Exchange

KING III CORPORATE GOVERNANCE CHECKLIST

KING III CORPORATE GOVERNANCE CHECKLIST Governance Element Principle Recommended Practice 1. ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP Responsible Leadership Board responsibilities 1.1 The Board should

KING III CORPORATE GOVERNANCE CHECKLIST Governance Element Principle Recommended Practice 1. ETHICAL LEADERSHIP AND CORPORATE CITIZENSHIP Responsible Leadership Board responsibilities 1.1 The Board should

APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 TM (King IV TM )

") (Incorporated in the Republic of South Africa) (Registration number 2006/019240/06) APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 TM (King IV TM ) DATE OF ISSUE: MAY 2018

(Incorporated in the Republic of South Africa) (Registration number 2006/019240/06) APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 TM (King IV TM ) DATE OF ISSUE: MAY 2018

BOARD OF DIRECTORS CHARTER

BOARD OF DIRECTORS CHARTER Title: Board of directors charter Document No.001 Effective Date: 7 November 2017 Next Review Date: November 2020 Approved by the Chairman and board of directors TABLE OF CONTENTS

BOARD OF DIRECTORS CHARTER Title: Board of directors charter Document No.001 Effective Date: 7 November 2017 Next Review Date: November 2020 Approved by the Chairman and board of directors TABLE OF CONTENTS

ANGLOGOLD ASHANTI LIMITED Reg No: 1944/017354/06 BOARD CHARTER

ANGLOGOLD ASHANTI LIMITED Reg No: 1944/017354/06 BOARD CHARTER APPROVED BY THE BOARD OF DIRECTORS ON 16 FEBRUARY 2018 1. INTRODUCTION The board of directors of AngloGold Ashanti Limited ( the Company )

ANGLOGOLD ASHANTI LIMITED Reg No: 1944/017354/06 BOARD CHARTER APPROVED BY THE BOARD OF DIRECTORS ON 16 FEBRUARY 2018 1. INTRODUCTION The board of directors of AngloGold Ashanti Limited ( the Company )

APPLICATION OF THE KING IV TM PRINCIPLES

APPLICATION OF THE KING IV TM PRINCIPLES Ethical culture Good performance Effective control Legitimacy LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP Leadership 1 The Board should lead ethically and effectively

APPLICATION OF THE KING IV TM PRINCIPLES Ethical culture Good performance Effective control Legitimacy LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP Leadership 1 The Board should lead ethically and effectively

Application of the King IV Report on Corporate Governance for South Africa 2016 (King IV)

") Application of the King IV Report on Corporate Governance for South Africa 2016 (King IV) THE GROUP ENDORSES THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA, 2016 (KING IV) AND HAS STRIVED

Application of the King IV Report on Corporate Governance for South Africa 2016 (King IV) THE GROUP ENDORSES THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA, 2016 (KING IV) AND HAS STRIVED

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP Leadership Principle 1. The

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 LEADERSHIP, ETHICS AND CORPORATE CITIZENSHIP Leadership Principle 1. The

SUMMARY OF KING IV PRINCIPAL DISCLOSURES. Leadership, ethics and corporate citizenship

Capitec Bank Holdings Limited (Capitec or the group) is a bank controlling company and is listed on the Johannesburg Stock Exchange (JSE) equity market. Capitec Bank Limited (Capitec Bank), a wholly owned

Capitec Bank Holdings Limited (Capitec or the group) is a bank controlling company and is listed on the Johannesburg Stock Exchange (JSE) equity market. Capitec Bank Limited (Capitec Bank), a wholly owned

Group Five Limited. ( Group Five or the Company or the Group )

") Group Five Limited (1969/000032/06) ( Group Five or the Company or the Group ) 1. INTRODUCTION 1.1 The board of directors of Group Five ( the board ) acknowledges the need for a board charter as recommended

Group Five Limited (1969/000032/06) ( Group Five or the Company or the Group ) 1. INTRODUCTION 1.1 The board of directors of Group Five ( the board ) acknowledges the need for a board charter as recommended

GENERAL GUIDANCE NOTE The Board Charter aligned to King IV August 2018

1 GENERAL GUIDANCE NOTE The Board Charter aligned to King IV August 2018 PURPOSE In accordance with the King IV Report on Corporate Governance for South Africa 2016 1 the governing body ensures that its

1 GENERAL GUIDANCE NOTE The Board Charter aligned to King IV August 2018 PURPOSE In accordance with the King IV Report on Corporate Governance for South Africa 2016 1 the governing body ensures that its

Tiso Blackstar Group SE. (Registration No: SE ) King IV Report on Corporate Governance

King IV Report on Corporate Governance") Tiso Blackstar Group SE (Registration No: SE 000110) King IV Report on Corporate Governance Policy 2017 Application of King IV Report on Corporate Governance for South Africa 2017 Tiso Blackstar Group

Tiso Blackstar Group SE (Registration No: SE 000110) King IV Report on Corporate Governance Policy 2017 Application of King IV Report on Corporate Governance for South Africa 2017 Tiso Blackstar Group

AYO TECHNOLOGY SOLUTIONS LIMITED (AYO)

") Application of the King IV Report on Corporate Governance for South Africa 2016 Ø Ø Ø Ø Ethical culture Good performance Effective control Legitimacy 1 November 2017 AYO TECHNOLOGY SOLUTIONS LIMITED (AYO)

Application of the King IV Report on Corporate Governance for South Africa 2016 Ø Ø Ø Ø Ethical culture Good performance Effective control Legitimacy 1 November 2017 AYO TECHNOLOGY SOLUTIONS LIMITED (AYO)

APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2018 (KING IV)

") APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2018 (KING IV) MICROmega Holdings Limited ( MICROmega or the Company or the Group ) is publicly listed on the Johannesburg Stock

APPLICATION OF THE KING IV REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2018 (KING IV) MICROmega Holdings Limited ( MICROmega or the Company or the Group ) is publicly listed on the Johannesburg Stock

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 Tiger Brands Limited ( Tiger Brands or the Company ) is a listed company

TIGER BRANDS LIMITED REGISTER OF APPLICATION OF THE KING IV PRINCIPLES IN THE REPORT ON CORPORATE GOVERNANCE FOR SOUTH AFRICA 2016 Tiger Brands Limited ( Tiger Brands or the Company ) is a listed company

KING IV IMPLEMENTATION

KING IV IMPLEMENTATION The board of directors implements the highest standards of corporate governance at all operations. The board understands and values long-term and ethical client relationships, and

KING IV IMPLEMENTATION The board of directors implements the highest standards of corporate governance at all operations. The board understands and values long-term and ethical client relationships, and

Corporate Governance Statement

Corporate Governance Statement The Board of Directors of Frontier Digital Venture Limited (FDV or the Company) is responsible for the corporate governance of the Company and its subsidiaries. The Board

Corporate Governance Statement The Board of Directors of Frontier Digital Venture Limited (FDV or the Company) is responsible for the corporate governance of the Company and its subsidiaries. The Board

Effective control. Ethical culture. Good performance. Legitimacy

KING IV REPORT ON CORPORATE GOVERNANCE Following the launch of the King IV Report on Corporate Governance (King IV ) in November 2016, the board has familiarised itself with the requirements of the report.

KING IV REPORT ON CORPORATE GOVERNANCE Following the launch of the King IV Report on Corporate Governance (King IV ) in November 2016, the board has familiarised itself with the requirements of the report.

PRINCIPLES OF KING IV AND DISCLOSURE REQUIREMENTS

Principles of King IV and disclosure requirements This report is to be read in conjunction with the remaining provisions of Gemgrow s 2017 integrated annual report in particular the corporate governance

Principles of King IV and disclosure requirements This report is to be read in conjunction with the remaining provisions of Gemgrow s 2017 integrated annual report in particular the corporate governance

CORPORATE GOVERNANCE FRAMEWORK

CORPORATE GOVERNANCE FRAMEWORK 1 P a g e TABLE OF CONTENTS Page 1. Introduction 3 2. Purpose 3 3. Scope 4 4. Governance Principles 4 4.1 Role Players 4 4.2 Combined Assurance 4 5. Governance Structure

CORPORATE GOVERNANCE FRAMEWORK 1 P a g e TABLE OF CONTENTS Page 1. Introduction 3 2. Purpose 3 3. Scope 4 4. Governance Principles 4 4.1 Role Players 4 4.2 Combined Assurance 4 5. Governance Structure

INTEGRATED REPORT 2017 APPLICATION OF KING IV. Think Efficient. Realise potential.

INTEGRATED REPORT 2017 APPLICATION OF KING IV Think Efficient. Realise potential. King IV Application Register The purpose of this register is to provide an overview of the application by EFG of the principles

INTEGRATED REPORT 2017 APPLICATION OF KING IV Think Efficient. Realise potential. King IV Application Register The purpose of this register is to provide an overview of the application by EFG of the principles

For personal use only

CORPORATE GOVERNANCE STATEMENT 31 MARCH 2017 Horseshoe Metals Limited s (the Company) Board of Directors (Board) is responsible for establishing the corporate governance framework of the Company and its

CORPORATE GOVERNANCE STATEMENT 31 MARCH 2017 Horseshoe Metals Limited s (the Company) Board of Directors (Board) is responsible for establishing the corporate governance framework of the Company and its

The Corporate Governance Statement is accurate and up to date as at 30 June 2018 and has been approved by the board.

Rules 4.7.3 and 4.10.3 1 Appendix 4G Key to Disclosures Corporate Governance Council Principles and Recommendations Name of entity: Catalyst Metals Limited ABN / ARBN: Financial year ended: 54 118 912

Rules 4.7.3 and 4.10.3 1 Appendix 4G Key to Disclosures Corporate Governance Council Principles and Recommendations Name of entity: Catalyst Metals Limited ABN / ARBN: Financial year ended: 54 118 912

CORPORATE GOVERNANCE REPORT

CORPORATE GOVERNANCE REPORT Framework AVI Limited ( the Company ) is a public company incorporated in South Africa under the provisions of the Companies Act 71 of 2008, as amended and the Regulations thereto

CORPORATE GOVERNANCE REPORT Framework AVI Limited ( the Company ) is a public company incorporated in South Africa under the provisions of the Companies Act 71 of 2008, as amended and the Regulations thereto

King III Chapter 2 Board Charter. September 2009

Chapter 2 Board Charter September 2009 The information contained in this Practice Note is of a general nature and is not intended to address the circumstances of any particular individual or entity. The

Chapter 2 Board Charter September 2009 The information contained in this Practice Note is of a general nature and is not intended to address the circumstances of any particular individual or entity. The

SANTAM GROUP RISK COMMITTEE CHARTER

1 SANTAM GROUP RISK COMMITTEE CHARTER 1. Constitution 1.1 The Risk Committee (the Committee) is constituted as a Committee of the Board of Directors (the Board) of Santam Limited (the Company). 1.2 The

1 SANTAM GROUP RISK COMMITTEE CHARTER 1. Constitution 1.1 The Risk Committee (the Committee) is constituted as a Committee of the Board of Directors (the Board) of Santam Limited (the Company). 1.2 The

CORPORATE GOVERNANCE. Composition of the board

CORPORATE GOVERNANCE Ethical conduct, good corporate governance, risk governance and fair remuneration are fundamental to the way that Montauk manages its business. Stakeholders interests are balanced

CORPORATE GOVERNANCE Ethical conduct, good corporate governance, risk governance and fair remuneration are fundamental to the way that Montauk manages its business. Stakeholders interests are balanced

KUMBA IRON ORE LIMITED (Registration number: 2005/015852/06) ( Kumba or the Company )

( Kumba or the Company )") INTERNAL KUMBA IRON ORE LIMITED (Registration number: 2005/015852/06) ( Kumba or the Company ) HUMAN RESOURCES AND REMUNERATION COMMITTEE ( Remco or the ) TERMS OF REFERENCE Kumba Iron Ore Limited Human

INTERNAL KUMBA IRON ORE LIMITED (Registration number: 2005/015852/06) ( Kumba or the Company ) HUMAN RESOURCES AND REMUNERATION COMMITTEE ( Remco or the ) TERMS OF REFERENCE Kumba Iron Ore Limited Human

BOARD CHARTER. Standard Chartered Bank Kenya Limited. Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya

BOARD CHARTER Standard Chartered Bank Kenya Limited. Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya BOARD CHARTER 1. PURPOSE This charter sets out the key values and principles

BOARD CHARTER Standard Chartered Bank Kenya Limited. Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya BOARD CHARTER 1. PURPOSE This charter sets out the key values and principles

ECS ICT Berhad (Company No H) Board Charter

Board Charter") 1. Introduction In achieving the objectives of transparency, accountability and effective performance for ECS ICT Berhad ( ECS or the Company ) and its subsidiaries ( the Group ), the enhancement of corporate