Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

|

|

|

- Daisy Neal

- 5 years ago

- Views:

Transcription

1 Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each question by placing a mark in the appropriate space on the answer sheet. 1. Which of the following characteristics most likely will heighten an auditor s concern about the risk of material misstatements due to fraud in an entity s financial statements? a. Employees who handle cash receipts are not bonded. b. Internal auditors have direct access to the board of directors and the entity s management. c. The audit committee is active in overseeing the entity s financial reporting policies. d. The entity s industry is experiencing declining customer demand. 2. Which procedure must be performed during the planning stage of the audit concerning potential fraud? a. Document the results of procedures used to address the risk of fraud. b. Consider the characteristics of journal entries, particularly those made near year end. c. Consider whether estimates prepared and recorded by management could indicate a bias in reporting. d. Conduct discussions among the engagement personnel regarding the risks of material misstatement due to error or fraud. 3. Based on the video shown in class, the White Electric Supply Company fraud a. involved an employee that hid stolen money in the walls of his house. b. involved a bookkeeper for a small business located in Lincoln, Nebraska. c. resulted in a long jail sentence for an employee in an insurance agency. d. was perpetrated by an individual that started a carpet cleaning business as a teenager. 4. Three conditions are generally present in the client s organization when fraud occurs. Those conditions include each of the following except a(n) a. incentive or pressure to commit fraud. b. professional skepticism about the likelihood of fraud. c. opportunity to commit fraud. d. attitude or rationalization about the act of fraud. 5. Moor, CPA, discovers a likely fraud during an audit but concludes that its effects, if any, could not be so material as to affect the opinion. Moor should a. notify the proper external authorities. b. perform additional audit procedures to establish that fraud has occurred. c. confer with the client about the additional audit procedures necessary to establish that fraud has occurred. d. report the finding to the appropriate representatives of the client with the recommendation that it be pursued to a conclusion. 6. Which of the following certifications shows expertise in fraud auditing? a. CFE b. CIA c. CMA d. CPA

2 7. The scope and nature of an auditor s contractual obligation to a client is ordinarily set forth in the a. management representation letter. b. scope paragraph of the auditor s report. c. engagement letter. d. introductory paragraph of the auditor s report. 8. Which of the following conditions most likely would pose the greatest risk in accepting a new audit engagement? a. Staff will need to be rescheduled to cover this new client. b. There will be a client-imposed scope limitation. c. The firm will have to hire a specialist in one audit area. d. The client s financial reporting system has been in place for 10 years. 9. Early appointment of the auditor enables preliminary work to be performed by the auditor that benefits the client because it permits the audit to be performed in a. a more efficient manner. b. a more thorough manner. c. accordance with quality control standards. d. accordance with generally accepted auditing standards. 10. Before accepting an engagement to audit a new client, an auditor is required to a. make inquiries of the predecessor auditor after obtaining the consent of the prospective client. b. obtain a copy of the client s financial statements. c. prepare a memorandum setting forth the staffing requirements and documenting the preliminary audit plan. d. discuss the management representation letter with the prospective client s audit committee. 11. Which of the following statements is true concerning analytical procedures used as risk assessment procedures? a. Analytical procedures usually involve comparisons of ratios developed from recorded amounts with expectations developed by management. b. Analytical procedures used in planning an audit ordinarily use data aggregated at a high level. c. Analytical procedures can replace tests of controls in gathering evidence to support the assessed level of control risk. d. Analytical procedures are more efficient, but not more effective, than tests of details and transactions. 12. The objective of performing analytical procedures in planning an audit is to identify the existence of a. unusual transactions and events. b. illegal acts that went undetected because of internal control weaknesses. c. related party transactions. d. recorded transactions that were not properly authorized. 13. If the independent auditors decide that it is efficient to consider how the work performed by the internal auditors may affect the nature, timing, and extent of audit procedures, they should assess the internal auditors a. efficiency and experience. b. independence and review skills. c. training and supervisory skills. d. competence and objectivity.

3 14. The section of the auditor s audit documentation called the permanent file usually contains the a. confirmation received from the bank. b. engagement letter. c. organization chart. d. audit plan. 15. Which of the following would an auditor most likely use in determining the auditor s preliminary judgment about materiality? a. The anticipated sample size of the planned substantive tests. b. The entity s annualized interim financial statements. c. The results of the internal control questionnaire. d. The contents of the representation letter. 16. Vouching sales invoices to shipping documents provides evidence that a. shipments to customers were recorded in the sales journal. b. invoiced sales were recorded in the sales journal. c. shipments to customers were invoiced. d. recorded sales were shipped. 17. The acceptable level of detection risk is inversely related to the a. assurance provided by substantive tests. b. risk of misapplying auditing procedures. c. preliminary judgment about materiality levels. d. risk of failing to discover material misstatements. 18. Which of the following audit risk components may be assessed in nonquantitative terms? Control Detection Inherent Risk Risk Risk a. Yes Yes Yes b. No Yes Yes c. Yes Yes No d. Yes No Yes 19. Audit risk at the account balance, transaction class, or disclosure level consists of inherent risk, control risk, and detection risk. Which of the following statements is true? a. Cash is more susceptible to theft than an inventory of coal because it has a greater inherent risk. b. The risk that material misstatement will not be prevented or detected on a timely basis by internal control can be reduced to zero by effective controls. c. Detection risk is a function of the efficiency of an auditing procedure. d. The existing levels of inherent risk, control risk, and detection risk can be changed at the discretion of the auditor.

4 20. Which of the following is a step in an auditor s decision to rely on the internal controls? a. Apply analytical procedures to both financial data and nonfinancial information to detect conditions that may indicate weak controls. b. Perform tests of details of transactions and account balances to identify potential errors and fraud. c. Identify specific controls that are likely to detect or prevent material misstatements and perform tests of controls. d. Document that the additional audit effort to perform tests of controls exceeds the potential reduction in substantive testing. 21. Regardless of the assessed risk of material misstatement, an auditor of a nonissuer would perform some a. tests of controls to determine their effectiveness. b. analytical procedures to verify the design of controls. c. substantive procedures to restrict detection risk for significant transaction classes. d. dual-purpose tests to evaluate both the risk of monetary misstatement and preliminary control risk. 22. Which of the following statements about the auditor s response to assessed risks in a financial statement audit is true? a. Risk assessment procedures performed to obtain an understanding of an entity s internal control also may serve as tests of controls. b. When the risk of material misstatement is high, an auditor should reduce the amount of substantive testing. c. Reliance on internal control may be sufficient to allow the auditor to eliminate substantive testing for significant transaction classes. d. When assessing the risk of material misstatement, an auditor should not consider evidence obtained in prior audits about the operation of controls. 23. According to auditing standards about audit risk and materiality in conducting an audit, the concepts of audit risk and materiality are interrelated and must be considered together by the auditor. Which of the following is true? a. Material fraud but not material errors cause financial statements to be materially misstated. b. If misstatements are not important individually but are important in the aggregate, the concept of materiality does not apply. c. Audit risk is the risk that the auditor may unknowingly express a modified opinion when in fact the financial statements are fairly stated. d. The phrase in the auditor s standard report present fairly, in all material respects, in conformity with generally accepted accounting principles indicates the auditor s belief that the financial statements taken as a whole are not materially misstated. 24. The auditing standards gives a formula for risk relationships. Overall allowable audit risk (AR) is the risk that monetary misstatements equal to tolerable misstatement may remain undetected. The risk of material misstatement (RMM) is the combined assessments of inherent and control risk. In the audit risk formula, AP is the auditor s assessment of the risk that substantive analytical procedures and other relevant substantive tests related to the same assertion will fail to detect material misstatements not detected by the relevant controls. TD is the allowable risk of incorrect acceptance for a test of details given that material misstatements occur in an assertion and are not detected by internal control or by analytical procedures and other substantive tests. Which model represents the allowable risk of incorrect acceptance (TD)? a. TD = AR (RMM AP). b. TD = RMM (AR AP). c. TD = AP (RMM AR). d. TD = RMM AP AR.

5 Use this information for questions Two auditors, Mark and Molly, independently assessed the risks associated with their client's accounts receivable. They both decide to hold audit risk at.04. Both agree that inherent risk should be set at.5 and no analytical procedures will be performed. However, Molly evaluates the control risk as moderate (.40) while Mark assesses it a little higher (.50). Using the audit risk model, answer the following questions. 25. What is detection risk for Mark? a..50 b..25 c..20 d What is detection risk for Molly? a..50 b..25 c..20 d If audit risk was changed to.06 (instead of.04) and all other factors remain unchanged except detection risk, then detection risk for each auditor would a. decrease. b. increase. c. remain unchanged. d. cannot be determined with the information given. 28. Which auditor, Mark or Molly, will have to collect the most substantive testing evidence? a. Mark. b. Molly. c. Evidence is never collected in an audit. d. An audit would not be conducted because audits are illegal. 29. The auditor should perform tests of controls when the auditor s risk assessment includes an expectation of the operating effectiveness of internal control or when a. substantive procedures alone do not provide sufficient appropriate audit evidence at the relevant assertion level. b. tests of details and substantive analytical procedures provide sufficient appropriate audit evidence to support the assertion being evaluated. c. the auditor is not able to obtain an understanding of internal controls. d. the owner-manager performs virtually all the functions of internal control. 30. The ultimate purpose of understanding the entity and its environment and assessing inherent risk and control risk is to contribute to the auditor s assessment of the risk that a. tests of controls may fail to identify procedures relevant to assertions. b. material misstatements may exist in the financial statements. c. specified controls requiring separation of duties may be circumvented by collusion. d. entity policies may be inappropriately overridden by senior management.

6 31. When assessing the risk of material misstatement at a low level, an auditor is required to document the auditor s Understanding of Overall the Entity's Control Responses to Environment Assessed Risks a. Yes No b. No Yes c. Yes Yes d. No No 32. The Sarbanes-Oxley Act of 2002 (SOX) requires management of issuers to do all of the following except a. establish and document internal control procedures and to include in their annual reports a report on the company s internal control over financial reporting. b. provide a report to include a statement of management s responsibility for and assessment of internal control. c. provide an identification of the framework used to evaluate the effectiveness of internal control. d. provide a statement that the board approves changes in internal control procedures. 33. During the audit of internal controls for an issuer, the auditor discovered a material weakness in internal control. The auditor would most likely express a(n) a. adverse opinion on internal control. b. qualified opinion on internal control. c. unqualified opinion on internal control. d. disclaimer of opinion on internal control. 34. As the acceptable level of detection risk decreases, an auditor may change the a. timing of substantive tests by performing them at an interim date rather than at year end. b. nature of substantive tests from a less effective to a more effective procedure. c. timing of tests of controls by performing them at several dates rather than at one time. d. assessed level of inherent risk to a higher amount. 35. When an auditor obtains an understanding of the entity and its environment, which of the following is the most likely order of performing the steps A through C below? A = Tests of controls B. = Preparation of a flowchart documenting the understanding of the client s internal control C. = Substantive tests a. ABC. b. ACB. c. BAC. d. BCA. 36. The auditor should perform tests of control when the auditor s risk assessment includes an expectation a. of a low level of inherent risk. b. that the controls are not being applied. c. that the controls are not suitably designed. d. of the operating effectiveness of internal control.

7 37. An auditor wishes to evaluate the design and perform tests of controls over a client s cash disbursements procedures. If the controls leave no audit trail of documentary evidence, the auditor most likely will test the procedures by a. confirmation and observation. b. observation and inquiry. c. analytical procedures and confirmation. d. inquiry and analytical procedures. 38. Which of the following audit procedures most likely would provide an auditor with the most assurance about the effectiveness of the operation of a client's internal control? a. Substantive tests of control procedures. b. Reperformance of client s control procedures. c. Inquiry of client personnel about control procedures. d. Confirmation with outside parties about the control procedures. 39. After auditors assess RMM at a high level, they will tend to a. perform a great deal of risk assessment procedures. b. perform a great deal of walkthroughs. c. perform a great deal of tests of controls. d. perform a great deal of substantive tests. 40. The most important component of an entity s internal control is the a. risk assessment function. b. monitoring element. c. information and communication system. d. control environment. 41. In a sampling application, the group of items about which the auditor wants to estimate some characteristic is called the a. population. b. attribute of interest. c. sample. d. sampling unit. 42. The probability that an auditor s conclusion based on a sample might be different from the conclusion based on an audit of the entire population is the concept of a. sampling risk. b. the confidence level. c. statistical sampling. d. the tolerable rate. 43. An auditor plans to examine a sample of 20 purchase orders for proper approvals as prescribed by the client s internal control. One of the purchase orders in the chosen sample of 20 cannot be found, and the auditor is unable to use alternative procedures to test whether that purchase order was properly approved. The auditor should a. choose another purchase order to replace the missing purchase order in the sample. b. consider this test of controls invalid and proceed with substantive tests because internal control is ineffective. c. treat the missing purchase order as a deviation for the purpose of evaluating the sample. d. select a completely new set of 20 purchase orders.

8 44. Statistical sampling usually may be applied in tests of controls when the client s controls a. permit detection of material misstatements in the accounting records. b. leave an audit trail. c. are described in accounting manuals. d. depend primarily on separation of duties. 45. For which of the following audit tests will an auditor most likely use attribute sampling? a. Making an independent estimate of the amount of a LIFO inventory. b. Examining invoices in support of the valuation of fixed asset additions. c. Selecting accounts receivable for confirmation of account balances. d. Inspecting employee time cards for proper approval by supervisors. 46. As a result of sampling procedures applied as tests of controls, an auditor incorrectly assesses control risk too low. The most likely explanation for this situation is that the a. deviation rates of both the auditor s sample and the population exceed the tolerable rate. b. deviation rates of both the auditor s sample and the population are less than the tolerable rate. c. deviation rate in the auditor s sample is less than the tolerable rate, but the deviation rate in the population exceeds the tolerable rate. d. deviation rate in the auditor s sample exceeds the tolerable rate, but the deviation rate in the population is less than the tolerable rate. 47. If systematic selection is used with a starting point of 10, a population size of 100, and a necessary sample size of 20, the first three items selected for examination would be a. 10, 110, 210. b. 110, 210, 310. c. 10, 15, 20. d. 15, 20, 25.

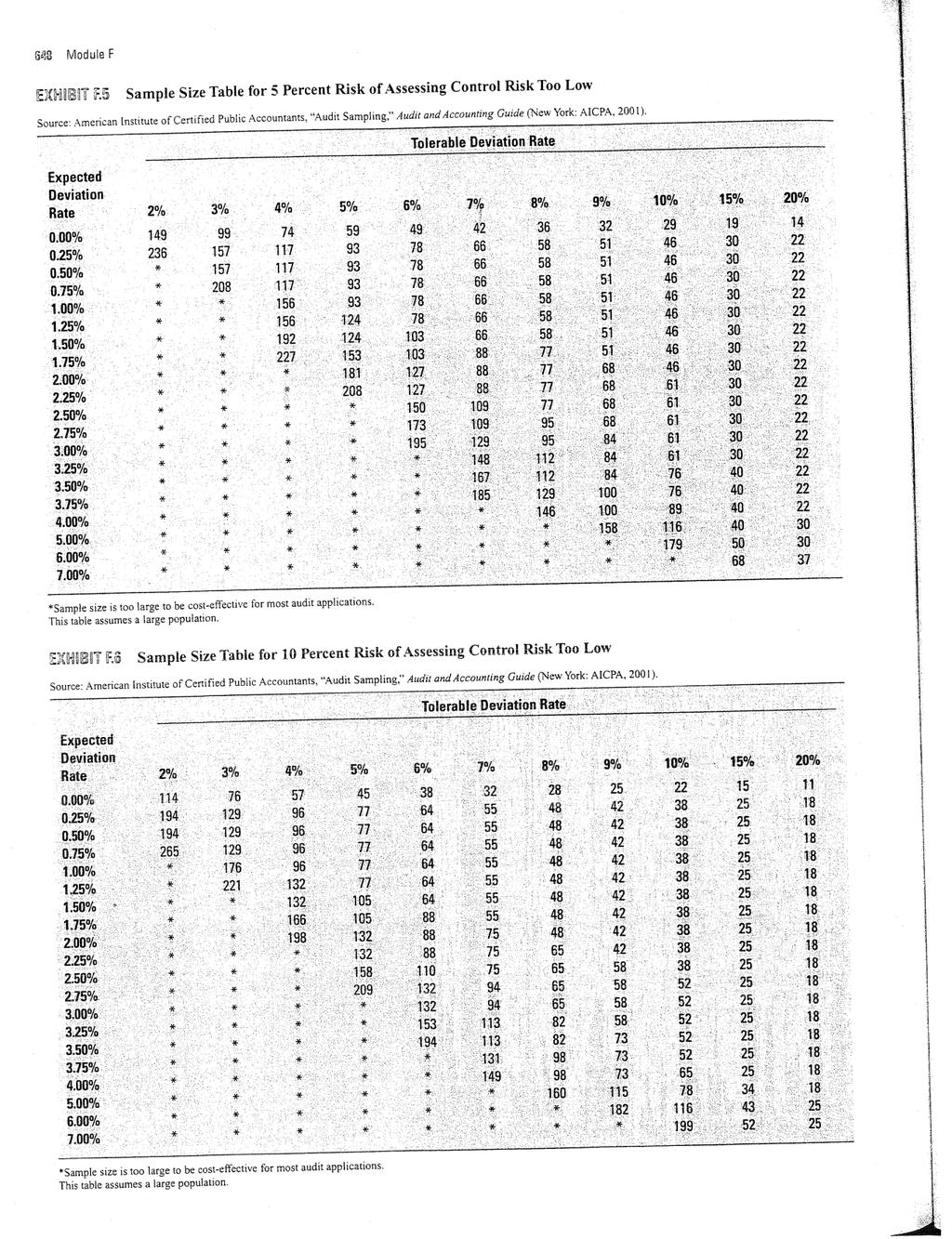

9 Use the following information for questions Answer the following questions assuming an independent attribute sampling application is followed. Use the sample size shown in the table and round (if necessary) the sample size when you determine the upper limit. Round in the most appropriate way. Case: A B C Risk of Overreliance (Risk of Assessing Control Risk Too Low) 5% 5% 10% Tolerable Deviation Rate 7% 15% 5% Expected Deviation Rate 1% 4% 0% Actual Number of Deviations Found The sample size for Case A is a. 22 b. 42 c. 66 d The computed upper limit (UEL) for Case A is (assume the number of items examined was equal to the actual computed sample) a. 3.8 b. 4.2 c. 4.6 d The computed upper limit (UEL) for Case C is (assume the number of items examined was equal to the actual computed sample) a b. 8.4 c. 6.5 d. 5.0

10

11

12 Que. No. Answer Que. No. Answer 1 d 26 c 2 d 27 b 3 b 28 a 4 b 29 a 5 d 30 b 6 a 31 c 7 c 32 d 8 b 33 a 9 a 34 b 10 b 35 c 11 b 36 d 12 a 37 b 13 d 38 b 14 c 39 d 15 b 40 d 16 d 41 a 17 a 42 a 18 a 43 c 19 a 44 b 20 c 45 d 21 c 46 c 22 a 47 c 23 d 48 c 24 a 49 c 25 d 50 d

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY AUDIT PLANNING

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

VERSION #1 WRITE ON YOUR SCANTRON!!!

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING CONTENTS

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

IAASB Main Agenda (February 2007) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (February 2007) Page 2007 441 Agenda Item 6-B PROPOSED INTERNATIONAL STANDARD ON AUDITING 530 (REDRAFTED) AUDIT SAMPLING AND OTHER MEANS OF TESTING Paragraph of extant ISA 530 Redrafted

IAASB Main Agenda (February 2007) Page 2007 441 Agenda Item 6-B PROPOSED INTERNATIONAL STANDARD ON AUDITING 530 (REDRAFTED) AUDIT SAMPLING AND OTHER MEANS OF TESTING Paragraph of extant ISA 530 Redrafted

Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Audit Sampling and Other Means of Testing

Issued December 2007 International Standard on Auditing Audit Sampling and Other Means of Testing The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL

Issued December 2007 International Standard on Auditing Audit Sampling and Other Means of Testing The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

1. Auditors may be independent in fact but not independent in appearance. 3. Attestation standards provide guidance for a wide variety of engagements

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

PLEASE complete #1-25 on your green scantron and the rest of them in your blue book.

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

Name: Date: You can keep this exam. PLEASE complete #1-25 on your green scantron and the rest of them in your blue book. 1. To qualify as "principal auditor" and render an opinion on the financial statements

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF SELECTIVE TESTING PROCEDURES CONTENTS

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF SELECTIVE TESTING PROCEDURES (Effective for audits of financial statements for periods ending on or after July 1, 1999, but contains

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF SELECTIVE TESTING PROCEDURES (Effective for audits of financial statements for periods ending on or after July 1, 1999, but contains

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

NEPAL STANDARDS ON AUDITING AUDIT SAMPLING AND OTHER SELECTIVE TESTING PROCEDURES

NSA 09 NEPAL STANDARDS ON AUDITING AUDIT SAMPLING AND OTHER SELECTIVE TESTING PROCEDURES CONTENTS Paragraphs Introduction 1-5 Definitions 6-15 Audit Evidence 16-20 Risk Considerations in Obtaining Evidence

NSA 09 NEPAL STANDARDS ON AUDITING AUDIT SAMPLING AND OTHER SELECTIVE TESTING PROCEDURES CONTENTS Paragraphs Introduction 1-5 Definitions 6-15 Audit Evidence 16-20 Risk Considerations in Obtaining Evidence

Audit Workshop Part 2 12 December 2009

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 8. Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting. Prepared by Richard J.

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

WATCH WORDS FROM THE PEER REVIEW PROCESS

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

INSTRUCTION ON METHODOLOGY ON PERFORMING FINANCIAL AUDIT AND REGULARITY AUDIT ( Official Gazette of MN, no. 07/15 from 17 th February 2015)

") On the basis of Article 38 item 1 point 4 of the Law on the State Audit Institution ( Official Gazette of Republic of Montenegro, no. 28/04, 27/06, 78/06, Official Gazette of Montenegro, no. 17/07, 73/10,

On the basis of Article 38 item 1 point 4 of the Law on the State Audit Institution ( Official Gazette of Republic of Montenegro, no. 28/04, 27/06, 78/06, Official Gazette of Montenegro, no. 17/07, 73/10,

Statements. This Standard is effective for reviews of financial statements for periods ending on or after 31 December 2013.

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Characteristics of Audit Sampling 7

Chapter 1 Characteristics of Audit Sampling 7 Characteristics of Audit Sampling 1.01 This chapter defines audit sampling and illustrates the difference between procedures that involve audit sampling and

Chapter 1 Characteristics of Audit Sampling 7 Characteristics of Audit Sampling 1.01 This chapter defines audit sampling and illustrates the difference between procedures that involve audit sampling and

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

THE AUDITOR S RESPONSES TO ASSESSED RISKS SRI LANKA AUDITING STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

Chapter 02. Professional Standards. Multiple Choice Questions. 1. Control risk is

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008

1 February 2008") Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

The Auditor s Responses to Assessed Risks

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

Presentation by: CPA Zachary Muthui

Audit Planning and Risk Assessment Presentation by: CPA Zachary Muthui Uphold public interest Audit planning Objectives of audit planning To ensure that the audit is performed in a smooth and effective

Audit Planning and Risk Assessment Presentation by: CPA Zachary Muthui Uphold public interest Audit planning Objectives of audit planning To ensure that the audit is performed in a smooth and effective

Community Bankers Conference

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

SCA Standard on Cost Auditing Audit Sampling

SCA - 106 Standard on Cost Auditing Audit Sampling Contents Cost Auditing and Assurance Standards Board Name of Clause Paragraph Number Introduction 1 Objective 2 Scope 3 Definitions 4.1-4.6 Requirements

SCA - 106 Standard on Cost Auditing Audit Sampling Contents Cost Auditing and Assurance Standards Board Name of Clause Paragraph Number Introduction 1 Objective 2 Scope 3 Definitions 4.1-4.6 Requirements

ECON 132A SPRING 2008 MT#2

ECON 132A SPRING 2008 MT#2 Name: Perm #: ANSWER QUESTIONS#1-25 ON GREEN SCANTRON ANSWER #26 & 27 IN THE SPACE PROVIDED. SIMULATION: WRITE YOUR NAME ON THE SIMULATION ASSIGNMENT ITSELF, ANSWER IN YOUR BLUE

ECON 132A SPRING 2008 MT#2 Name: Perm #: ANSWER QUESTIONS#1-25 ON GREEN SCANTRON ANSWER #26 & 27 IN THE SPACE PROVIDED. SIMULATION: WRITE YOUR NAME ON THE SIMULATION ASSIGNMENT ITSELF, ANSWER IN YOUR BLUE

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

Chapter The audit evidence gathering technique known as computation or recalculation refers to. A. sending letters to independent third parties

Chapter 08 1. The audit evidence gathering technique known as computation or recalculation refers to. A. sending letters to independent third parties B. counting inventory C. recalculating depreciation

Chapter 08 1. The audit evidence gathering technique known as computation or recalculation refers to. A. sending letters to independent third parties B. counting inventory C. recalculating depreciation

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

IAASB Main Agenda (December 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

AT Assertions, Audit Procedures and Audit Evidence Red Sirug Page 1

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

Audit Evidence. SSA 500, Audit Evidence superseded the SSA of the same title in September 2009.

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

ISA 240 (Redrafted), The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements

, The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements") CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

Special Audit Techniques. CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

SA 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL

Part I : Engagement and Quality Control Standards I.169 SA 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING

Part I : Engagement and Quality Control Standards I.169 SA 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING

Chapter 4. Risk Assessment. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Report on Inspection of KPMG Auditores Consultores Ltda. (Headquartered in Santiago, Republic of Chile)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 330 (Redrafted) THE AUDITOR S RESPONSES TO ASSESSED RISKS Introduction PHILIPPINE STANDARD ON AUDITING 330 (REDRAFTED) THE AUDITOR

Auditing and Assurance Standards Council Philippine Standard on Auditing 330 (Redrafted) THE AUDITOR S RESPONSES TO ASSESSED RISKS Introduction PHILIPPINE STANDARD ON AUDITING 330 (REDRAFTED) THE AUDITOR

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) CONTENTS

CONTENTS") SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

2. The auditors' report on a corporation's financial statements usually is addressed to the president of the company.

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

CPA REVIEW SCHOOL OF THE PHILIPPINES Manila. AUDITING THEORY OTHER PSAs and PAPSs

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

Report on Inspection of PricewaterhouseCoopers Audit (Headquartered in Neuilly-Sur-Seine, French Republic)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

International Standard on Auditing (Ireland) 300. Planning an Audit of Financial Statements

300. Planning an Audit of Financial Statements") International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

After completing this Session, you should be able to answer the following questions:

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008

10 July 2008") Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS. Preface

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

Audit Evidence. HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

Report on. Issued by the. Public Company Accounting Oversight Board. June 16, 2016 THIS IS A PUBLIC VERSION OF A PCAOB INSPECTION REPORT

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

Analytical Procedures

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

Detailed competency map

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

International Standard on Auditing (UK) 600 (Revised June 2016)

600 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

Audit Risk. Exposure Draft. IFAC International Auditing and Assurance Standards Board. October Response Due Date March 31, 2003

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

ASB Meeting January 12-15, 2015

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

of Financial Statements

Issued November 2004 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 300 Planning an Audit of Financial Statements HONG KONG

Issued November 2004 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 300 Planning an Audit of Financial Statements HONG KONG

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

IAASB CAG Public Session (March 2018) CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1

CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1") Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Planning and Supervision

Statement on Auditing Standards No. 108 1591 Statement on Auditing Standards No. 108 Planning and Supervision (Supersedes Appointment of the Independent Auditor, as amended, of Statement on Auditing Standards

Statement on Auditing Standards No. 108 1591 Statement on Auditing Standards No. 108 Planning and Supervision (Supersedes Appointment of the Independent Auditor, as amended, of Statement on Auditing Standards

MODULE 2: Engagement Planning (11% 17%)

") AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

AU2 Advanced External Auditing MODULE 2: Engagement Planning (11% 17%) Lecturer: Glen B. Carlson, B. Comm.(Honours), C.G.A. Module 2 engagement planning Module 2 covers the planning of an audit engagement,

International Standard on Auditing (UK and Ireland) 500

500") Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

ISA 500. Issued March 2009; updated June International Standard on Auditing. Audit Evidence

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

Cost Auditing Standard Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

GLOSSARY OF TERMS 1. Unauthorized access to on-line terminal devices, programs and data; The use of computer programs by unauthorized personnel; and

1 Access controls Procedures designed to restrict access to on-line terminal devices, programs and data. Access controls consist of user authentication and user authorization. User authentication typically

1 Access controls Procedures designed to restrict access to on-line terminal devices, programs and data. Access controls consist of user authentication and user authorization. User authentication typically

AUDIT RESPONSIBILITIES AND OBJECTIVES

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

WATCH WORDS FROM THE PEER REVIEW PROCESS

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

Question No: 1 FINALTERM EXAMINATION Fall 2008 ACC311- Fundamentals of Auditing (Session - 1) When the cash sales should be recorded by the companies in order to achieve control objectives? Record the

Question No: 1 FINALTERM EXAMINATION Fall 2008 ACC311- Fundamentals of Auditing (Session - 1) When the cash sales should be recorded by the companies in order to achieve control objectives? Record the

AUDIT TECHNIQUES---SA 500

AUDIT TECHNIQUES---SA 500 Audit techniques stand for the methods that are adopted by an auditor to obtain evidence. Audit evidence Information used by the auditor in arriving at the conclusions on which

AUDIT TECHNIQUES---SA 500 Audit techniques stand for the methods that are adopted by an auditor to obtain evidence. Audit evidence Information used by the auditor in arriving at the conclusions on which

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 333 AU-C Section 330 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained Source: SAS No. 122.

Performing Audit Procedures in Response to Assessed Risks 333 AU-C Section 330 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained Source: SAS No. 122.

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR)

& Internal Financial Controls over Financial Reporting (IFCoFR)") Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Chapter 7. Auditing Internal Control over Financial Reporting. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Assurance Hand Note Professional Stage-Knowledge Level By: Shafique Ahmed-Sr. Officer (Internal Audit-BSRM) Assurance

Assurance") Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

Chapter 02. Professional Standards. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,