Econ Department Final. Unit One Fundamentals of Economics Prepping for Success!

|

|

|

- Kory Gordon

- 5 years ago

- Views:

Transcription

1 Econ Department Final Unit One Fundamentals of Economics Prepping for Success!

2 Econ Department Final Exam Your Economics Departmental Final Exam is cumulative and will count as 5% of your class grade. Following is our Review Schedule: Tuesday we ll review Unit One and Unit Two Wednesday we ll review Unit Three and Unit Four Thursday we ll review Unit Five and finish with a wrap-up game!

3 Econ Department Final Exam Econ Study Cards To help you, you ll create one Study Card per unit. You can write as much as you want on each index card front and back They will help you study and prepare! Each Study Card will count for a classwork grade 25 points/study Card Your Name on each card Unit 1, 2, 3, 4 or 5

4 Complete Your Study Card As You Review! As you review each unit, capture key information on your Study Card. At the end of each unit review, there will be questions you have to answer. These will receive a grade, so take them seriously! Hint everyone should make a 100% because you can go back and find the answer if you don t know it!

5 Here s Your Timing First half of class (45 min.) minutes review the unit and capture important info on your index card minutes answer the review questions When you re done, come show me your index card and I ll give you the access code for the next unit to review. Second half of class (45 min) minutes review the unit and capture important info on your index card minutes answer the review questions

6 Unit One Review Each Unit Review will unpack our unit learning standards to help you understand what you need to know. We ll take each learning standard and break it down. Please pay particular attention to the bold/colored words and make sure you include this information on your Unit Summary Index Card.

7 Unit One Learning Standard #1 of 6 SSEF1 Explain why limited productive resources and unlimited wants result in scarcity, opportunity costs, and tradeoffs for individuals, businesses, and governments. a. Define scarcity as a basic condition that exists when unlimited wants exceed limited productive resources. b. Define and give examples of productive resources (i.e. factors of production): natural resources (i.e. land), human resources (i.e. labor and human capital), physical capital and entrepreneurship. c. Explain the motivations that influence entrepreneurs to take risks (e.g., profit, job creation, innovation, and improving society). d. Define opportunity cost as the next best alternative given up when individuals, businesses, and governments confront scarcity by making choices.

to you may not mean anything to someone else Timing Needs")

8 Big Economic Idea Scarcity Because we have unlimited wants and very limited resources we will ALWAYS have scarcity. No matter how wealthy someone is they always want more Scarcity is relative: what is precious/valuable (i.e. scarce) to you may not mean anything to someone else Timing Needs

9 Wants vs. Needs To understand scarcity we need to remember the difference between wants and needs: Need Things we need for survival air, food, water, shelter, cloths Wants (not cell phones!) Things we desire but are NOT essential for survival. (yes that s a cell phone!)

10 Scarcity and Choice Because our limited resources won t allow us to have everything we want/need, we have to make choices.

and through governments economists study each")

11 Economics Economics is the study of how we try to needs and wants by choices. Because people act: individually, in groups (such as businesses) and through governments economists study each of these groups. satisfy our making

12 Who makes the decisions? Consumers- make decisions on what to buy Producers- make decisions on what to produce Possible products fall into two categories: Goods- physical objects to purchase Services- actions/activities performed for a fee

13 Resources Anything that people use to make or obtain what they need or want is called a resource. In economics, resources are sometimes called inputs. Resources that can be used to produce goods and services are called FACTORS OF PRODUCTION.

14 4 Factors of Production 1. Natural Resources anything provided by Mother Nature This includes not just land, but anything that comes from the land. Some common land or natural resources are water, oil, copper, natural gas, coal, and forests. Land resources are the raw materials in the production process. These resources can be renewable, such as forests, or nonrenewable such as oil or natural gas. The income that resource owners earn in return for land resources is called rent.

15 4 Factors of Production 1. Human Resources /Labor - people s physical and intellectual value Labor is the effort that people contribute to the production of goods and services. Labor resources include the work done by the waiter who brings your food at a local restaurant as well as the engineer who designed the bus that transports you to school. It includes an artist's creation of a painting as well as the work of the pilot flying the airplane overhead. If you have ever been paid for a job, you have contributed labor resources to the production of goods or services. The income earned by labor resources is called wages and is the largest source of income for most people.

16 4 Factors of Production 1. Capital resources - are goods produced and used to make other goods and services. Think of capital as the machinery, tools and buildings humans use to produce goods and services. Some common examples of capital include hammers, forklifts, conveyer belts, computers, and delivery vans. Capital differs based on the worker and the type of work being done. The income earned by owners of capital resources is interest.

17 4 Factors of Production 1. Entrepreneurship An entrepreneur is a person who combines the other factors of production - land, labor, and capital - to earn a profit. The most successful entrepreneurs are innovators who find new ways produce goods and services or who develop new goods and services to bring to market. Entrepreneurs thrive in economies where they have the freedom to start businesses and buy resources freely. The payment to entrepreneurship is profit.

18 Opportunity Cost Basic economic problem is scarcity Scarcity causes us to make choices We prioritize our options and choose the one that serves our best interest best The next best option is called Opportunity Cost (we measure it s value as what we give up when we make our #1 choice) All other options (other than #1 and #2) are called Trade-offs.

19 Unit Learning Standard #2 of 6 SSEF2 Give examples of how rational decision making entails comparing the marginal benefits and the marginal costs of an action. a. Define marginal cost and marginal benefit. b. Explain that rational decisions occur when the marginal benefits of an action equal or exceed the marginal costs. c. Explain that people, businesses, and governments respond to positive and negative incentives in predictable ways.

20 How do you know if you are wisely using resources? By studying productivity Productivity is the level of output that results from a given level of input (aka resources). Economic Goal >>> Use resources/inputs as efficiently as possible to create the largest amount of output or productivity.

21 Efficiency A company that is not wisely using its resources should improve efficiency. Efficiency is the (often measurable) ability to avoid wasting materials, energy, efforts, money, and time in doing something or in producing a desired result. 'Economic Efficiency' is a broad term that implies an economic state in which every resource is optimally allocated to serve each person in the best way while minimizing waste and inefficiency. When an economy is economically efficient, any changes made to assist one person would harm another.

22 Efficiency When There s Room for Improvement When companies strive to improve efficiencies they might introduce division of labor Division of Labor involves assigning one or more task/s to each individual worker. Each worker specializes in that particular task/s and becomes proficient (or very efficient) at that task. The production of most goods can be broken down into a number of specific tasks (division of labor), with each of these tasks assigned to specific workers (specialization)

23 Three Types of Exchange 1. Barter- A direct trade of goods and services without money. 2. Money- Any item commonly accepted in exchange of goods, services, or the payment of debts. 3. Credit- A form of exchange with a promise to repay over a specified time.

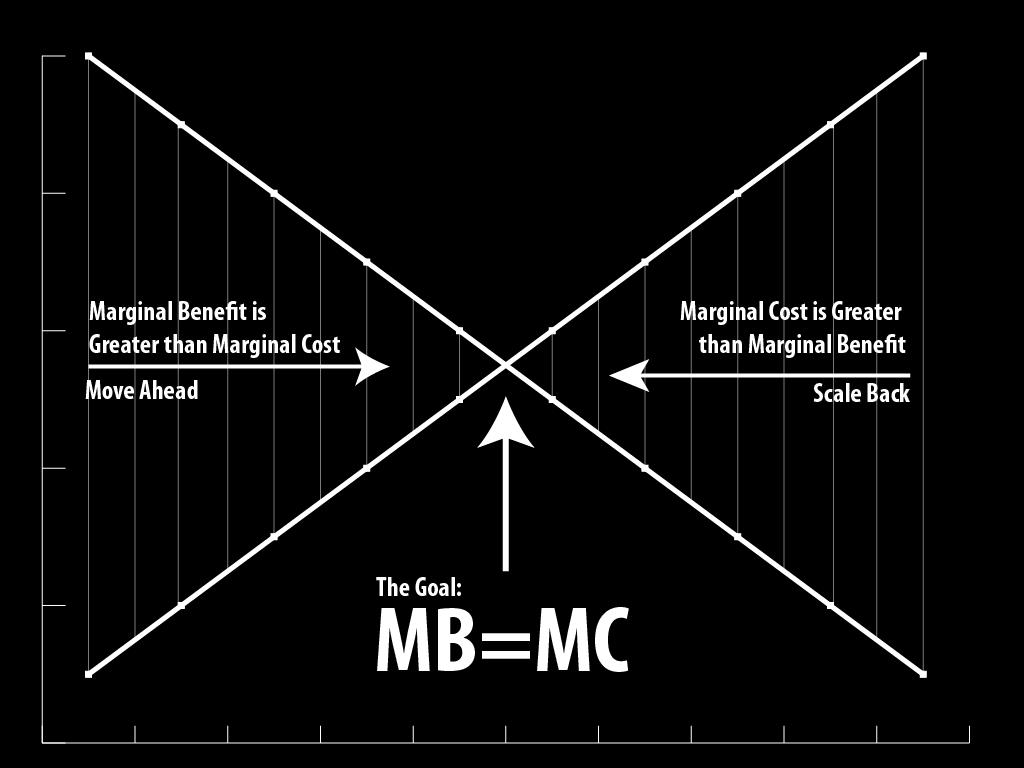

24 Marginal Cost vs. Marginal Benefit Because the opportunity cost of producing extra units of goods increases after a certain point, then there is a point for which the cost of producing the good is less than the benefit to society.

25 Marginal Producing one more unit >>> the cost of producing it = marginal cost the benefit derived from it = marginal benefit

26 Marginal Cost & Allocation Efficiency Soooo an efficient allocation of resources is maximized when the marginal benefit equals the marginal cost of producing one extra unit. Marginal Benefit = Marginal Cost

27 The Goal: MB = MC

28 Unit One Learning Standard #3 of 6 SSEF3 Explain how specialization and voluntary exchange influence buyers and sellers. a. Explain how and why individuals and businesses specialize, including division of labor. b. Explain that both parties gain as a result of voluntary, non-fraudulent exchange.

29 Division of Labor The division of labor refers to the practice that the tasks of producing a good or service are divided up into separate tasks. When workers focus on performing separate tasks, specialization occurs.

30 Examples of Specialization Within the economy as a whole, the division of labor explains why even if you bake your own bread, you typically don't grow your own wheat, grind it into flour, build your own oven, make your own bread-pans and so on. Instead, people specialize in a few skills and then take the wages that they earn from those skills to purchase the other goods and services that they desire from other specialists. In this way, the division of labor and specialization is the basis for an economy to exist.

31 Adam Smith The Wealth of Nations Adam Smith started his classic book The Wealth of Nations with a discussion of the division of labor as the basis for understanding how an economy works. He identified three reasons why the division of labor increases output: 1. workers who specialize on one job become much better at doing it; 2. with specialization, the time that it would take to switch between jobs is eliminated; and 3. workers who specialize on one job often invent more effective ways or new machines for doing the job. But as Adam Smith makes clear, specialization is possible only when people are able to coordinate their production and consumption decisions with each other. The study of economics is largely concerned with explaining how this coordination takes place.

32 Voluntary Exchange People do not make everything that they and their family use: that is, They do not grow all their own food, Sew their own clothes, Build their own house and Provide themselves personally with health care and education. Instead, people focus on a particular job and then use the wages that they earn from that job to purchase the goods and services they desire. In this way, an economy forms an interlinked network of trade, exchange and interdependence.

33 Voluntary Exchange Specialization is the basis of trade and interdependence among individuals, cities, regions and countries. Most countries do not produce all of what they consume. Instead, they focus more heavily on producing certain products and trading with other countries. Thus, the global economy is a network of trade and interdependence. When trade is voluntary and non-fraudulent, both parties in the trade gain.

34 Unit One Learning Standard #4 of 6 SSEF4 Compare and contrast different economic systems and explain how they answer the three basic economic questions of what to produce, how to produce, and for whom to produce. a. Compare traditional, command, market, and mixed economic systems with regard to private ownership, profit motive, consumer sovereignty, competition, and government regulation. b. Analyze how each type of system answers the three economic questions and meets the broad social and economic goals of freedom, security, equity, growth, efficiency, price stability, full employment, and sustainability.

35 Economic Systems An economic system is a system of production and exchange of goods and services as well as allocation of resources in a society. The system is determined by who answers the 3 basic economic questions 1. What goods & services to produce? 2. How should these goods & services be produced? 3. Who gets to consume these goods & services?

36 Traditional Economy Traditional Economy an economic system that is based on customs and beliefs. People will make what they ve always made. They do things the same way as their parents and grandparents. People are not free to make their own decisions on what they want. Exchange of goods is done through bartering exchanges with no money involved Examples of these societies do not really exist any more. Native American societies and India in the past were like this.

37 Command Economies Command Economy One in which a central authority makes all economic decisions about how best to allocate resources. Examples of these economies include Cuba, North Korea, and China.

38 Market Economy Market Economy One in which people or businesses use their own best interest to make a profit. These economies are based on supply and demand. Buyers and sellers answer the economic questions as they come together to exchange goods and services. Examples include the USA, Great Britain and Japan

39 Mixed Economy Market + Command = Mixed Economy There are no pure market or command economies. To some extent, all existing economic systems demonstrate characteristics of both systems and can be called mixed economies. Economies are usually closer to one type of economic system than the other. People/businesses own most resources and determine what & how to produce, but the government may regulate certain industries.

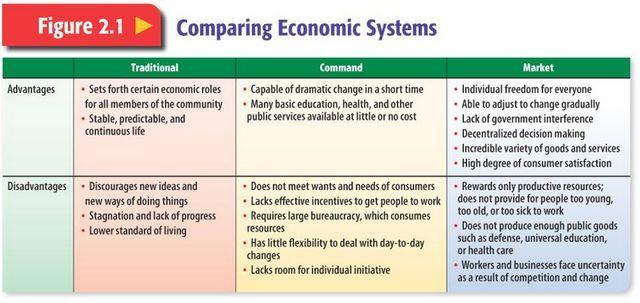

40 Strengths of These Economies Traditional Sets certain economic roles for all members of the community. It is stable, predictable, and continuous for life. Command Capable of dramatic changes in a short time. Market Very resilient and self-sustaining. Is able to self-adjust to change gradually. Individual freedom for everyone. Notable lack of government interference. Decentralized decision making. Variety of goods and services. High degree of consumer satisfaction.

41 Weaknesses of These Economies Traditional Discourages new ideas and new ways of doing things. Usually has a lack of progress. Command Does not meet the needs of consumers. Lacks incentives to get people to work. Has little flexibility to deal with small changes. New ideas are discouraged. Market Rewards only productive resources. Many people are too young, old, or sick to work. Must guard against market fluctuations.

42

43 Continuum of Economic Systems

44 Unit One Learning Standard #5 of 6 SSEF5 Describe the roles of government in the United States economy. a. Explain why government provides public goods and services, redistributes income, protects property rights, and resolves market failures. b. Explain the effects on consumers and producers caused by government regulation and deregulation.

Redistribute Income 5) Correct Market Failures 6) Stabilize the")

45 Government s Role 1) Provide a Legal System 2) Maintain Competition 3) Public Goods and Services 4) Redistribute Income 5) Correct Market Failures 6) Stabilize the Economy

46 Provide a Legal System Make and enforce laws to protect private property rights Examples: courts, monetary system

47 Maintain Competition Regulates monopolies Examples Anti-trust laws

48 Public Goods and Services Uses tax dollars to provide goods and services that private individuals wouldn t provide Benefits everyone Examples: Parks, national defense, schools

49 Redistribute Income Taxing large income groups to provide for those in need Examples: social security, Medicare, Medicaid

50 Resolve Market Failures Corrects externalities(unintended side effects or reactions to an action) Positive externality- unintended benefit Negative externality- unintended cost Examples: Environmental pollution, subsidies, education

51 Stabilize the Economy Reduces unemployment and inflation and promotes economic growth Examples Government budgets, monetary supply

52 Unit One Learning Standard #6 of 6 SSEF6 Explain how productivity, economic growth, and future standards of living are influenced by investment in factories, machinery, new technology, and the health, education, and training of people. a. Define productivity as the relationship of inputs to outputs. b. Explain how investment in equipment and technology can lead to economic growth. c. Explain how investments in human capital (e.g., education, job training, and healthcare) can lead to a higher standard of living. d. Analyze, by means of a production possibilities curve: trade-offs, opportunity cost, growth, and efficiency.

53 Production Possibilities Frontier Production Possibilities Frontier The Production Possibilities Frontier/Curve Featuring the following simplifying assumptions a society that produces only two goods the efficient use and full employment of resources fixed technology a single snapshot in time

54 PRODUCTION POSSIBILITIES Production Possibilities Frontier/Curve The production possibility curve is a hypothetical representation of the amount of two different goods that can be obtained by shifting resources from the production of one, to the production of the other. The curve is used to describe a society's choice between two different goods Sometimes called the Production Possibilities Frontier

55 Production Possibilities Frontier Production Possibilities Frontier Production Possibilities Frontier units of potatoes units of apples A B C D E F G

56 Production Possibilities Frontier Production Possibilities Frontier Production Possibilities Frontier

57 Production Possibilities Frontier Production Possibilities Frontier units of potatoes A B C 3 D 2 E units of potatoes units of apples 1 G units of apples A B C D E F G F

58 PPC Rules 1. Any point on the PPC uses existing resources efficiently 2. Any point outside the PPC is not realistic, attainable or sustainable given existing resources 3. Any point inside the PPC is inefficient

59 PPC Example

60 SO CAN A PRODUCTION POSSIBILITIES CURVE SHIFT OUT? Yes! Events that can expand production possibilities outward A technological advance (remember a technology is anything that makes life easier) rail cars refrigeration computers An increase in human or natural resources population increase new discoveries Capital investment new factories new infrastructure

61 SO CAN A PRODUCTION POSSIBILITIES CURVE SHIFT IN? Yes! Events that can reduce production possibilities and cause a shift: Natural disasters hurricanes earthquakes tornadoes Wars Reduction in resources layoffs rising resource prices Inefficiency human resources employees sick, need training, etc. capitol resources equipment breaks, new technologies not used, etc.

62

63