Responsibility Accounting

|

|

|

- Jason Bryan

- 5 years ago

- Views:

Transcription

1 Responsibility Accounting

2 Objectives To understand the concept of Responsibility Accounting

3 Responsibility Accounting Responsibility accounting is used to measure the performance of people and departments to foster goal congruence. Responsibility Accounting is a management system that aims to develop performance measures by which segment managers are evaluated. 12-3

4 Contd. It helps managers to trace cost, revenue and profits in order to enable them to arrive at right decisions. It also provides costing information about controllable costs to the manager of the responsibility center It focuses on people who participate actively in planning process and thereby helps the management in cost control through budgeting process. It means business activities are identified with persons rather than product and responsibility is assigned to the manager best placed to effect control

5 According to CIMA Responsibility accounting is a system of accounting that segregates revenues and cost into areas of personal responsibility in order to assess the performance attained by persons to whom authority has been assigned

6 R.A. In big businesses, there are various functional departments such as purchasing, production, marketing etc. All these departments are under charge of their respective department heads who are accountable for their performance These dept heads have the decision making authority and with it comes responsibility It has no scope in a small organization Reason All decision making is centralized at one place and one individual

7 Contd Responsibility accounting can be used at every level of management that fulfils the following conditions: Costs and revenues can be directly associated with the specific level of management responsibility. The costs and revenues are controllable at the level of responsibility with which they are associated. Budget data can be developed for evaluating the manager's effectiveness in controlling the costs and revenues.

8 Assumptions of Responsibility Accounting System A sound responsibility accounting system is based on number of assumptions. The same are explained in brief as under: a) Managers are held responsible only for those activities over which they exercise control. b) Managers strive to achieve the goals and objectives that have been established for them. This is mainly because of their involvement in the planning process. c) Managers participate in establishing the goals against which their performance will be measured. d) Goals are attainable with efficient and effective performance. e) Performance reports and feedback are made available timely. f) The role of responsibility accounting in the company's reward structure is clearly stated and followed.

9 Responsibility Centers Responsibility centers denote any organization unit that is headed by a responsible manager. Responsibility centers exist to accomplish one or more purpose (objectives). The individual objectives help in achieving the overall goal It can be assigned very narrowly in terms of the activities the senior management decides to assign a particular manager. A responsibility center may be Department (HR, Finance) Product line (steel wires, steel casting) Territory (east zone, south zone) Any identifiable area 9

10 Advantages of responsibility accounting: Performance Evaluation Delegating Authority Corrective Action Growth and Prosperity of the Business High Morale and Efficiency Motivation 10

11 Cost centres Managers are held responsible for cost incurred in the centres. Manager is accountable for the costs that are under his control but not for its revenues. Only those cost are charged to cost center which are controllable by manager of cost center. 11

12

13 Revenue Centres Generally a revenue centre acquires finished goods and is responsible for selling and distributing them. Eg. Marketing org. is a sales revenue center. Such a center is devoted to increase the revenue and assumes no responsibility for production. In this center, the manager is responsible for the level of revenue or output of a center, measured in monetary terms, but are not responsible for the cost of goods that center offers 13

14

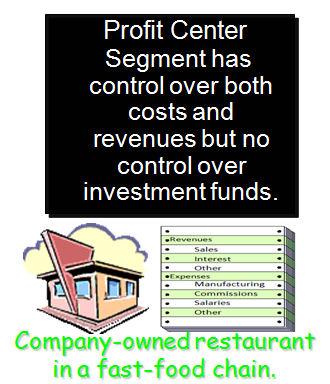

15 Profit Centres In this case, managers have almost complete operational decision-making. They are evaluated on the basis of profit generated. It sells majority of its output to the outside world It is a center where manager is accountable for sales revenue as well as costs Eg a department of a company is responsible for sales as well as production in that department.

16

17 Investment Centres Centers whose managers control revenue, costs, and the level of investments. They can be evaluated on the basis of ROI 17

18

19 Illustration 7-20