Fundamental Prospecting - time for another gold rush?

|

|

|

- August Moore

- 5 years ago

- Views:

Transcription

30th Annual Marine Money")

1 Fundamental Prospecting - time for another gold rush? Dr Adam Kent - Maritime Strategies International (MSI) 30th Annual Marine Money Money Week New York City June 19 th to 21 st 2017

2 Agenda Fundamental Prospecting - time for another gold rush? 1. Mining the Demand Data 2. Supply Overburden 3. Earning Seekers 4. Price Formation 6. Panning for Prospects Gold Bullion or Fools Gold? Maritime Strategies International 2

3 Fundamental Prospecting Mining the Demand Data Maritime Strategies International

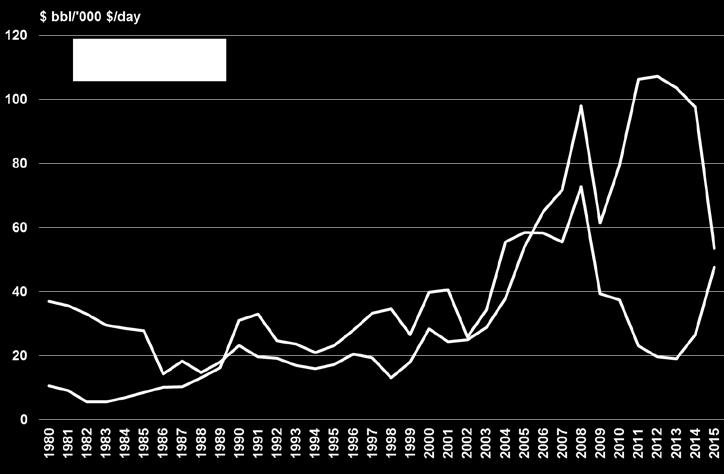

4 Strengthening Product Tanker Market in H MR Tanker TC2 NW Europe to United States Index 1.2 Jan Forecast Feb Forecast Mar Forecast 1.0 Apr Forecast May Forecast Actual Model based on trade, refining and pricing signals Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Based on MSI and WoodMac Forecasting Model Maritime Strategies International 4

5 Incremental Product Imports Improving macro position High stocks IMO bunker regulation Maritime Strategies International 5

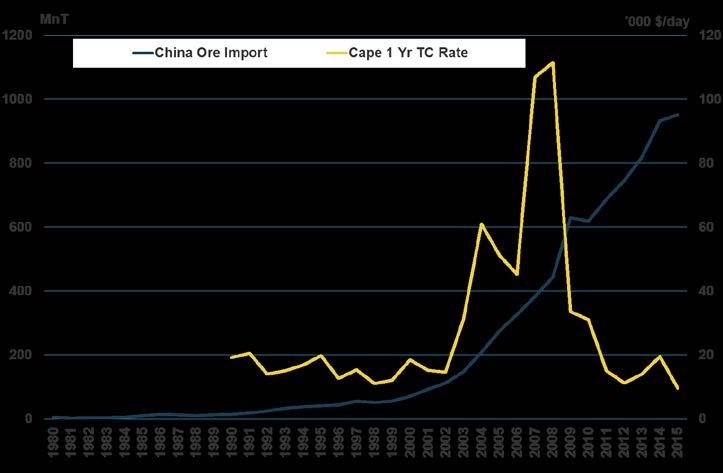

6 Bulker Incremental Cargo Growth Limited new iron ore capacity, coal squeezed Steel production increases Maritime Strategies International 6

7 Coal - Major Demand Risks & Rewards China Coal Imports Risks dependent on: Price Domestic production Policy Environmental regulation Energy efficiency India Coal Imports Maritime Strategies International 7

8 k TEU Jun-16 Jun Container Panamax Plight Cascade coming back into play Eur-Afr Eur-LAM Eur-ME/ISC FE-Afr FE-Eur FE-LAM FE-ME/ISC FE-Oceania intra-asia intra-europe intra-lam intra-me/isc intra-nam NAM-LAM NAM-Oceania Pendulum South-South Transatlantic Transpacific Maritime Strategies International 8

9 Intra Asia Deployment 40% Share of total intra-asia 35% 30% Trade Deployment 25% 20% 15% 10% 5% 0% intra-se Asia SE Asia- China China Domestic SE Asia Cabotage NE Asia- China NE Asia-SE Asia Other NE Asia Cabotage intra-ne Asia Maritime Strategies International 9

10 Vessel Demand on Intra Asia Mn TEU Deployed SE Asia-China SE Asia Cabotage Other NE Asia Cabotage NE Asia-SE Asia NE Asia-China intra-se Asia intra-ne Asia Maritime Strategies International 10

11 Organic Chemical Growth Imbalance will drive trade Maritime Strategies International 11

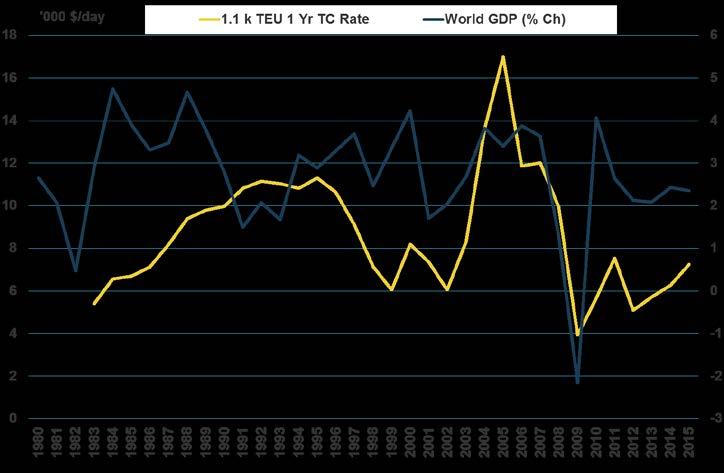

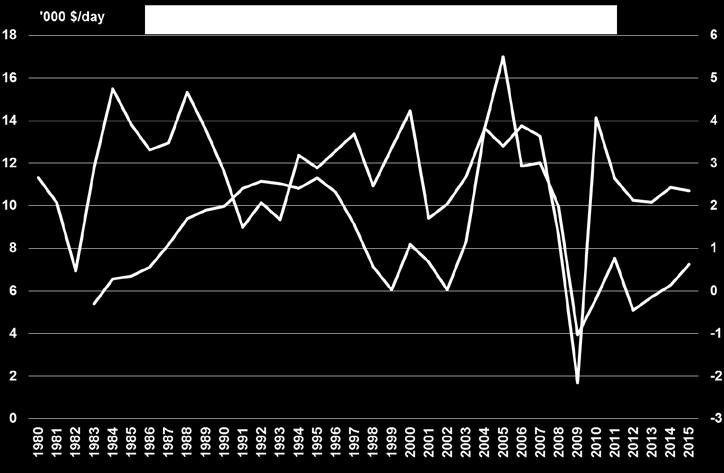

12 Seaborne Cargo Growth - Positive Cargo growth positive across the board Maritime Strategies International

13 Fundamental Prospecting Supply Overburden Maritime Strategies International

14 Supply has been the Party Pooper Supply Supply Supply Supply Maritime Strategies International 14

15 Orderbook Improving Picture for most % of Fleet 45% 40% 35% 30% 25% 20% 15% 10% 5% Orderbook dwindling across main sectors mid-2015 mid % Oil Tanker Bulker Chemical LPG LNG FCC General Cargo RoRo/RoPax Cruise ship PCTC Maritime Strategies International 15

16 Orderbook Replacement Tonnage 40 Mn GT 20+ Year Old Orderbook Old as % of Orderbook % of Old Fleet 300% % % % 20 Replacement requirement 100% 15 50% 10 0% 5-50% 0-100% Oil Tanker Bulker Chemical LPG LNG FCC General Cargo RoRo/RoPax Cruise ship PCTC Maritime Strategies International 16

17 Success is in their Hands? Old Tonnage by CoD Oil Tankers Bulkers Containerships Gas Carriers Maritime Strategies International 17

18 Contracting Depression Mn GT 25 Cruise PCTC RoRo MPP Container Gas Bulkers Tankers Q Q Q Q Q Q Q Q Q Q2 Maritime Strategies International 18

19 Supply Side Developments Annual Average Fleet Growth : +2.4% +0.6% +2.6% Tanker Bulker Container Includes MSI s current assumptions on scrapping, contracting, slippage and cancellations Maritime Strategies International

20 Fundamental Prospecting Earnings Expectations Maritime Strategies International

21 Where on the Earnings Cycle Are We? Crude and Product Tanker OSVs LPG Carrier Rigs LNG MPP Chemical Tanker Container PCTC Bulker RoRo Maritime Strategies International

22 At Todays Prices it makes Sense for Some Based on 60% financing of a 5 Year Old Maritime Strategies International

23 Earnings Outlook - Generally Positive Maritime Strategies International 23

24 Fundamental Prospecting Price Formation Maritime Strategies International

25 The Complete Pricing Jigsaw Maritime Strategies International 25

26 Shipyard Cover is Still Weak +1 Year Out South Korea China Japan Other Maritime Strategies International 26

27 Chinese Shipyard White List No Guarantee Privately Owned State Backed Only 30 white list Chinese yards have taken orders in the last year Maritime Strategies International 27

28 Elapsed Days Between Contract & Delivery Maritime Strategies International 28

29 Newbuilding Prices are Close to Bedrock % of Fleet 20% 15% Costs YoY Change Price YoY Change Yard Forward Cover (RHA) Years % 2.0 5% 1.5 0% -5% % % Maritime Strategies International 29

30 Secondhand Prices Development 10 Year old Prices Maritime Strategies International 30

31 Fundamental Prospecting Panning for Prospects Maritime Strategies International

32 MSI - FMV MSI Forecast Marine evaluator (FMV) is the first web-based tool to provide forecast and historical price data covering virtually all of the deepsea shipping fleet. Data includes forecasts of newbuilding, second-hand prices, 1 year timecharter rates and operating costs for specific vessels. MSI FMV draws on MSI s proven, proprietary models and a consistent cross-sectional view across all principal shipping sectors. It puts asset values in the context of the near term market to enable reliable benchmarking with outputs based on annual averages. Coverage: Crude Oil Tanker Chemical Tanker Multi Purpose Product Oil Tanker LPG Carrier Containership Dry Bulk Carrier LNG Carrier PCC/PCTC AHTS /fmv PSV Maritime Strategies International 32

33 Where are the Biggest Nuggets? Maritime Strategies International 33

34 IRR Returns 5 Year Old Year of divestment Maritime Strategies International 34

volatility Yes No Opex and scrap value forecasts (model derived) Yes Yes No Yes Ability to stress the forecasts with endogenous and exogenous scenarios Yes Only Proxy Based")

35 MSI s ABS Shadow Rating Model Descriptive Statistics MSI Approach Traditional Shipping Expected softening of the markets increases likelihood of default Earnings forecasts (Cycles accommodated) Conditional (time varying) volatility Yes No Opex and scrap value forecasts (model derived) Yes Yes No Yes Ability to stress the forecasts with endogenous and exogenous scenarios Yes Only Proxy Based Stable calibration procedures Yes No Copula based dependency Yes No Model based Enforcement delays Yes No Increased likelihood of default Costs estimates for enforcements Model based (time varying) recovery estimates Yes Only anecdotal experience Risk based pricing tool for asset values Yes No Yes No Accommodate credit enhancements (cash cushions, dividend playouts etc.) Yes Subjective or experience based Sensitivity to input parameters Yes No Levered IRR's should be treated with caution due to a concentration of risk (PD) in a cyclical trough Maritime Strategies International Ltd. 35 The model is similar to those applied by rating agencies, but with enhanced data, econometrics and inputs. The model incorporates volatility wrapped around cyclical trends, enforcement and recovery scenarios and targeted optimisation of loan structure. The model provides a detailed view on the point-in-time, PD, LGD and EL and is used by banks towards IFRS9 compliance. Primary and secondary debt portfolios are also typically shadow rated using our models

36 Maritime Strategies International 36

37 MSI Background For over 30 years, MSI has developed integrated relationships with a diverse client base of financial institutions, ship owners, shipyards, brokers, investors, insurers and equipment and service providers. MSI s expertise covers a broad range of shipping sectors, providing clients with a combination of sector reports, forecasting models, vessel valuations and bespoke consultancy services. MSI is staffed by economists and scientists offering a structured quantitative perspective to shipping analysis combined with a wide range of industry experience. MSI balances analytical power with service flexibility, offering a comprehensive support structure and a sound foundation on which to build investment strategies and monitor/assess exposure to market risks. Maritime Strategies International 37

38 Disclaimer While this document has been prepared, and is presented, in good faith, Maritime Strategies International assumes no responsibility for errors of fact, opinion or market changes, and cannot be held responsible for any losses incurred or action arising as a result of information contained in this document. The copyright and other intellectual property rights in data, information or advice contained in this document are and will at all times remain the property of Maritime Strategies International. Maritime Strategies International 38

39 Maritime Strategies International Ltd 6 Baden Place Crosby Row London SE1 1YW United Kingdom Tel: +44 (0) Fax: +44 (0) info@msiltd.com