MTO and Terminal Operator: organization and challenges in the last four an a half decades

|

|

|

- Victoria McLaughlin

- 5 years ago

- Views:

Transcription

1 TrainMoS II Project Module 2.1.1: Maritime sustainability and MoS MTO and Terminal Operator: organization and challenges in the last four an a half decades 14 September 2015 Daniele Testi Marketing Director Contship Italia Group

2 DANIELE TESTI 45 years old Marketing Director Industrial engineering degree Married 2 children, age 3 an 7 Born in Genoa Grew up in La Spezia living in Milan since 1989 Hobby: Music and home recording Sports: Running and skiing Fan of Ferrari F1 and Juventus

since September 2014 Part of Contship Italia holding company since May 2002 as Marketing and Planning Manager Previous professional experiences: KPMG consulting")

3 Marketing & Corporate Communication director of Contship Italia Group since January President of SOS Log (association) since September 2014 Part of Contship Italia holding company since May 2002 as Marketing and Planning Manager Previous professional experiences: KPMG consulting (senior consultant) Tarros Group (Container Control Manager). About Contship Italia Contship is the larger operator in Italy for maritime container terminals and intermodal services. It employs 3,000 people with over 300 million turnover. Contship is the South European subsidiary of Eurokai (Hamburg), a private company listed on the stock exchange and the largest independent Container Terminal operator in Europe with 14.8 million TEU handled end 2014.

4 it.linkedin.com/pub/daniele-testi/0/63b/92 On line:

5 containerisation revolution modern terminal operations Transhipment & intermodal transport big ships and future challenges

6 6 SINCE 1969 PIONEER IN CONTAINERIZATION

.")

in Gioia Tauro.")

7 45 YEARS OF EXPERIENCE Sogemar is merged with Intermodale Italia. North Africa start up of operations at Tangier 1969 Angelo Ravano establishes Contship. The first liner service is operated from Fos Sur Mer to Casablanca for FIAT. Contship establishes the first ever container line service from Europe to India Contship Containerlines is acquired by CP Ships. Eurokai becomes the main shareholders of Contship Contship establishes Oceanogate Italia, as a Group rail traction company In Melzo, Contship establishes RAIL HUB MILANO In Australia with Eagle Containerlines Contship operates the first private container terminal in Italy (La Spezia). Operations commence at Medcenter Container Terminal (MCT) in Gioia Tauro. Terminal Container Ravenna and Cagliari International Container Terminal join the terminals network. La Spezia is the first gateway in Italy to operate ULCC 14,000 TEUs class. La Spezia is the first Italian gateway to deploy 23 rows cranes. Gioia Tauro and La Spezia, welcome the 16,600 TEUs containership. 7

8 CONTSHIP TODAY We bring the ship to your factory 8

9 ONE FLAG! ONE TEAM! ONE SOUL! INTERMODAL&LOGISTICS 50% 33.4% 66.6% MARITIME TERMINALS 9

10 CONTSHIP AT A GLANCE MARITIME TERMINALS 6 state of the art MARITIME TERMINALS 6.4 million TEU HANDLED in % MARKET SHARE in ITALY INTERMODAL&LOGISTICS LOGISTIC SERVICE PROVIDER 240,000 TRANSPORTED TEU/YEAR 1.1 MILLION TRAIN-KM OPERATED TOTAL INVESTMENTS to date: EURO 800 MILLION 3,000 EMPLOYEES, 3% female. 8% managers 10

11 CONTSHIP UNIQUE SELLING PROPOSITION Intermodal SUPPLY CHAIN VERTICAL INTEGRATION Gateway DIRECT ACCESS TO MULTIPLE MARKETS Transhipment MINIMAL DEVIATION FROM MAIN EAST-WEST ROUTE INTERMODAL SOLUTIONS TRANSHIPMENT & GATEWAY 11

12 VERTICAL INTEGRATION FASTER SEAMLESS TRANSFER TO YOUR FACTORY 12

13 13 LOGISTIC SERVICE PROVIDER

14 14 INTEGRATED SOLUTIONS

15 SOUTHERN GATEWAY, A NEW BEGINNING RAILability FULL CONTROL FROM PORT TO DOOR PRECLEARING FOR FASTER UNLOADING AND FINAL DELIVERY OF YOUR CARGO REDUCING TRANSIT TIME AND CO2 EMISSIONS ITALIAN CARGO via ITALIAN PORTS EXTENDED TO REACH TO SOUTHERN EUROPE 15

16 16 THE RIGHT PRODUCTS IN THE RIGHT PLACE

17 Containerization revolution modern terminal operations Transhipment & intermodal transport big ship and future challenges

18 The Birth of "Intermodalism Intermodalism is a system that is based on the theory that efficiency will be vastly improved when the same container, with the same cargo, can be transported with minimum interruption via different transport modes from an initial place of receipt to a final delivery point many kilometers or miles away. That means the containers would move seamlessly between ships, trucks and trains. CONTAINERISATION

19 CONTAINERISATION Assumptions: changes in the socio-economic factors Decrease of the manorial work model Increase of the per capita income Reduction of protectionist barriers EXPONENTIAL INCREASE OF TRADES

20 BETWEEN 30s and 50s 1929: Seatrain load a few rail wagons on deck of one of its ships deployed in the New Orleans Havana route 1937: Malcom Mc Lean has to wait a full day in the port of Jersey City to unload his truck. He is convinced that if he could leave there only the trailer he might do another trip with its tractor. 1950: Malcom Mc Lean order to General Motors 600 tractors separated from trailers 27 April 1956: 58 trailers, 35 feet long of Mc Lean, separated from the wheels and platforms are loaded on board of M/v Ideal X, a ship deployed on the Newark Houston route

21

22 On 23 April 1966, ten years after the first converted container ship sailed, Sea- Land s Fairland sailed from Port Elizabeth in the USA to Rotterdam in the Netherlands with 236 containers. This was the first international voyage of a container ship. Meanwhile, during the rapid build-up to the Vietnam War, the US military was faced with the logistical problem of getting supplies to troops. It had somehow to transport mass supplies to a war zone in south-east Asia through a single under-developed port on the Saigon River and a partially-functioning railway. The government turned to container shipping as the most efficient option. Container shipping began to prove its worth at an international level. From this point on the industry began to grow to the point where it would quickly become the backbone of global trade, even though few at the time would have made such bold predictions and 1969 were the Baby Boomer years for container shipping. In 1968 alone, 18 container vessels were built, ten of them with a capacity of 1,000 TEUs which was large for the time. In 1969, 25 ships were built and the size of the largest ships increased to approaching 2,000 TEU. In 1972, the first container ships with a capacity of more than 3,000 TEU were completed by the Howaldtwerke Shipyard in Germany. Now an entire industry had emerged, demanding unprecedented investment in vessels, containers, terminals, offices and information technology to manage the complex logistics.

23 FOS SUR MER (MARSEILLE), TEU, of ship capacity 23

24 LA SPEZIA, 1971 The first PRIVATE Container terminal in ITALY 24

25 MIDDLE EAST, 1974 The closing of SUEZ did not stop the TRADES 25

26 TARTOUS (SIRIA), 1975 Difficult situations are swiftly met with good practical SOLUTIONS 26

27 INDIA 1977 First ever container service between EUROPE and INDIA 27

28 BEIRUT, 1978 Supporting MIDDLE EAST recover and development 28

29 29

30 Containerization revolution modern terminal operations Transhipment & intermodal transport big ship and future challenges

31 IPSWICH, 1979 A new LIFE in the UK 31

32 AUSTRALIA, 1982 The first ever INDIPENDENT liner service operator in AUSTRALIA 32

33 BAGHDAD (IRAQ), 1983 CONTINAER BOOM the word within reach 33

34 LA SPEZIA, 1987 A new STEP FORWARD The modern container terminal era 34

35

36

37 BASIC MARITIME CONTAINER TERMINAL LAYOUT The container terminal can be roughly distinguished into four areas: The quayside of the terminal The stacking area The landside of the terminal Areas for supporting activities

38 Quayside At the quayside, a quay wall with water depths well over 14,5 meters at all tides should provide for berthing of the container vessels. The largest deepsea container vessels require a berth of up to meters. Where simultaneous handling of more than one deepsea vessel and also feeder and barge vessels is required, the total quay wall length of a container terminal unit will be between one and three and a half kilometres. Stacking area In the stacking area the containers are stored, received from the landside or from feeders, and waiting for loading on the deepsea vessel or discharging from the deepsea vessel for delivering. Non-standard containers and refrigerated containers, so-called reefers, are stacked in special areas. Reefers or temperature-controlled containers have to be powered at special stacking areas. Special segregation provisions are taken for containers with dangerous goods. Landside At the landside of the terminal the direct import and export containers are handled, originating from or destined for the terminal s hinterland. Areas for supporting activities At a designated breakbulk area the special cargo is handled. This cargo is too large or heavy for a container, such as yachts, agricultural machines, industrial machinery or parts of an entire factory.

39

40 EVOLUZIONE DEI TERMINAL PORTUALI

41 APM Terminals' Maasvlakte2 in Rotterdam The world's first fully automated container

42

43 TERMINAL OF THE FUTURE?

44

45 + 5.6% 2014/ 2013

46

47 53%

48

49

50

51

52

53

54

55 Marketing of container terminals The decision-making units (DMUs), especially at shipping lines, are complex, with various organisational levels, functions and locations involved and various roles performed. There are local, regional and global DMU members, all taking part in the influencing and decision-making processes,with varying interests. There are also functional interests to be identified. Whether a shipping line decides to call at a port or not is dependent on strategic, political, operational, commercial, nautical and financial parameters, to be evaluated in their interrelationship. People can play various roles in a decision-making process, which can vary, dependent on the decision at hand. They can be: - a decision-maker, - a decision influencer, - an information-provider, - an advisor and so on. Marketing of container terminals therefore requires building and maintaining a network of relations within the customer organisation.

56 In Italy Transhipment Gioia Tauro, Cagliari, Taranto 2014 total Italy 10.1 mio TEUs North Tyrrhenian Genoa, La Spezia, Savona, Livorno North Adriatic Trieste, Venice, Ravenna Gioia Tauro Genoa La Spezia Cagliari 7.1 mio TEUs 70% of total

57 Total AREA of Italian and Foreign PORTS (mio sqm) Source: Iniziativa di studio sulla portualità Italiana (DIPE)

58 Max WATER DEPTH in the main European and Med ports * Taranto holds also facilities with 25 m water depth but they are not used for cargo Source: Iniziativa di studio sulla portualità Italiana (DIPE)

59 Port Authorities (PA) Projects estimated total investment by Port Authorities 5.7 billion 20% Tyrrhenian - 66% Adriatic - 14 Others 80% 70% Percentage of Investment 60% 50% 40% 30% 20% 10% 0 New infrastructure Refurbishment Maintenance Recovery Restoration Demolition Total

60 Overview of the main Container Terminal Projects in Italy GENOA New, Calata Bettolo ( 400 k TEUs), December 2015 Upgrade, Messina (400 k TEUs), 2016 New, Molo Canepa, 2019 TRIESTE Upgrade. Molo VII, (1.2 mio TEUs), 2017 SAVONA VADO New, APMT (800 k TEUs), 2017 LA SPEZIA Upgrade, LSCT (1.8 mio TEUs), 2018 Upgrade, Tarros/Arkas, tbd VENICE New, OFF Shore Terminal, (3 mio TEUs) New, former Montefibre area (1.4 mio TEUs) RAVENNA Upgrade, channel Candiano /14.5 m water depth), 2015 New, TCR, (500 k TEUs), 2020 LEGHORN Upgrade, Port Entrance, 2015 New, Europa Platform, 5 KM of new Quay, tbd CIVITAVECCHIA New, CTR, (700 k TEUs), 2016 SALERNO Upgrade, Port Entrance, tbd NAPLES Upgrade, water depth, 2015 Upgrade, Conateco, suspended TARANTO Upgrade, TCT, ( m Quays), tbd CAGLIARI Upgrade, CICT, (3.6 MIO TEUs), tbd GIOIA TAURO Upgrade, Water Depth, 2015 Upgrade, Energy Plant, Cold Ironing

61 LA SPEZIA READY FOR THE FUTURE, NOW 61

62 LA SPEZIA SYSTEM YOUR DOOR TO ITALY AND SOUTH EUROPE 62

63 LSCT, TODAY 1.4 million TEUs CAPACITY 63

64 LSCT, TOMORROW ULCC ULCC ULCC 10 x 23 rows across 6 x 20 rows across 2 million TEUs CAPACITY 64

65 LSCT, TOMORROW 200 million EUROS of planned investments 2 million TEUs CAPACITY 65

66 RAIL TRANSPORT IN LA SPEZIA = 30% of total throughput OVERALL SUPPLY CHAIN COSTS TO IMPROVE SPEED AND AVERAGE QUANTITY OF CONTAINERS FROM PORT TO DOOR 66

67 Containerization revolution modern terminal operations Transhipment & intermodal transport big ship and future challenges

68

69 LA SPEZIA, 1989 The largest INTERMODAL network in ITALY takes shape 69

70 MELZO (MILAN), 1990 INVESTING in MILAN 70

71 HAMBURG, 1990 Think PINK 71

72 HONG KONG, 1990 Globalization EFFECTS 72

73 SINGAPORE, 1991 New PARTNERSHIP 73

,")

74 74 NOUMEA, (NEW CALEDONIA), 1991

75 75 LA SPEZIA, 1991

76 76 NHAVA SHEVA (INDIA), 1991

77 SIDNEY, 1992 EXPO 92 Australian pavilion official logistic provider 77

78 CONTSHIP SINGAPORE, 1994 The FLEET CAPACITY continues to increase 78

79 CONTSHIP MANAGEMENT TEAM, 1995 CONTSHIP international TEAM WORK 79

80 80 CONTSHIP OFFICES, 1996

81 GIOIA TAURO, 1995 Contship MEGA HUB 81

82 Contents

17,7 10,8 9,9 12,6")

83 TRANSHIPMENT HUBs future MED market (TEUs/000,000) 17,7 10,8 9,9 12,6 13,4 12,2 Morocco/Gibraltar West Med 8,2 4 7,7 8,4 5,1 6,3 Central Med East Med Black Sea Source: Contship on Ocean Shipping Consultants data

84 MARKET factors Shipping development model TRANSHIPMENT IN ITALY: because of (larger tonnage, concentration, economy of scale, geopolitics) Global supply chain (global markets, global hubs) ECONOMIC factors 50% of Italian port handling Investments (1 billion public, 1 billion private) Local (south) economic impact (9,000 employees) STRATEGIC factors Italy as logistic platform in the Med (hubs=largest container terminals, water depth, quay length, yard extension, equipment, linked with growing emerging market GDPs) European maritime cargo flows (marginalization to North Africa hubs)

85 TEN T / CORE Ports Network 1 mio TEUs exchanged by Switzerland, Austria and South Germany with MED/east of SUEZ countries Congestion of North European PORTS Transit time from Far East

86 CONTSHIP INTERMODAL OFFER 24 TRAINS WEEK dominating the MILAN RAIL CORRIDOR MARKET PLUS 29 INTERNATIONAL ROUND TRIP CONNECTIONS every WEEK INTERMODAL & LOGISTICS 86

87 SOUTHERN GATEWAY, A NEW BEGINNING RAILability FULL CONTROL FROM PORT TO DOOR PRECLEARING FOR FASTER UNLOADING AND FINAL DELIVERY OF YOUR CARGO REDUCING TRANSIT TIME AND CO2 EMISSIONS ITALIAN CARGO via ITALIAN PORTS EXTENDED TO REACH TO SOUTHERN EUROPE 87

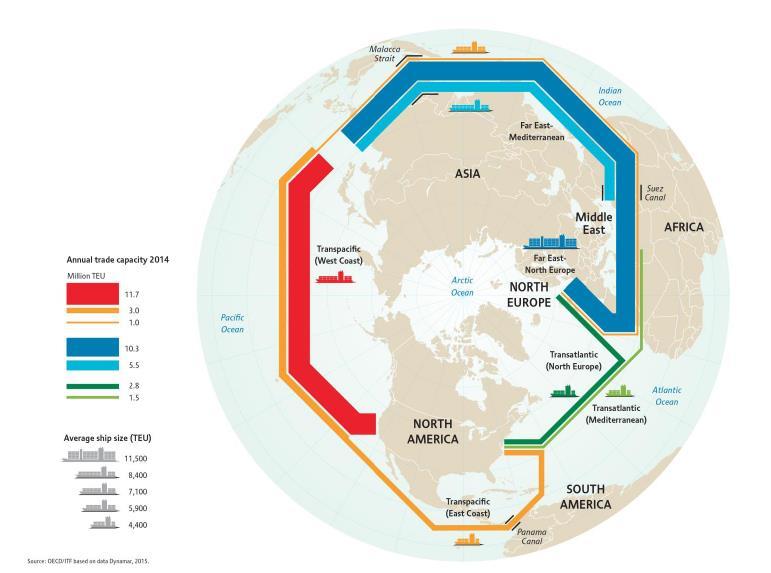

88 RAIL HUB MILANO 260,000 m2 SURFACE 4x 750 3x up to 600m RAIL TRACKS YOUR LINK TO EU 4,400 m2 BONDED & NATIONALWAREHOUSES 1,540 m2 for EQUIPMENT M&R 300,000 TEUs HANDLING CAPACITY 6,000 TRAINS/YEAR IN/OUT 88

HIGHWAY GATE 13 KM FROM A4 (TURIN-VENICE) HIGHWAY GATE")

89 STRATEGIC CROSSROAD 22% of ITALIAN GDP 5 KM FROM A35 (BRESCIA-MILAN) HIGHWAY GATE 19 KM FROM A1 (MILAN-ROME) HIGHWAY GATE 13 KM FROM A4 (TURIN-VENICE) HIGHWAY GATE 89

90 90 HANNIBAL

91 NETWORK (including third party company trains*) INTERNATIONAL RAIL LINKS MELZO ROTTERDAM 17 MELZO VENLO* 10 MELZO LUDWIGSHAFEN 3 MELZO FRENKENDORF (Basel) 3 MELZO DUISBURG 3 MELZO ZEEBRUGGE* 1 Round Trips/week 80 trains/week connecting south, central and north Europe MELZO COLOGNE 3 DOMESTIC RAIL LINKS Trains/week LA SPEZIA MELZO 28 GENOA MELZO 12 BARI MELZO 6 PADUA MELZO 18 FROSINONE MELZO 6 RAVENNA MELZO 6 LA SPEZIA REGGIO EMILA 13 LA SPEZIA PARMA 4 LA SPEZIA PADUA trains/week from/to Italian ports 91

92 OCEANOGATE 1.5 million TONS CO2 saved every year THE SMARTER TRANSPORT FOR A BETTER FUTURE 92

93 Train Kms in ITALY % 6% % 33% 3% 64% Trenitalia Others Fercargo

94 94

95

; 30 containers 40 each train Average cost could increase/decrease up to 15-30% if scheduled time for the train load/unload do not guarantee the optimal round trip based on")

96 Intermodal cost of production Assumptions Intermodal transport(one way); km (es. Genova or Spezia Padua); 30 containers 40 each train Average cost could increase/decrease up to 15-30% if scheduled time for the train load/unload do not guarantee the optimal round trip based on train composition costs and optimal use of the locomotors and rail wagons. Shunting operations at sea port Rail traction Shunting operations at inland terminal Terminal handling charge Total cost

97 Container terminal EFFICIENCY, where to find it DRY PORT INTERMODAL TRANSPORT PORT OPERATIONS H24 7/7 PRECLEARING CUSTOMS FORMALITIES

98 PRECLEARING CUSTOM CLEARANCE (PRECLEARING) DISCHARGE LIST + PROSECUTION LIST by RAIL RELOAD ORDER FROM MTO CONTAINER AVAILABLE FOR DELIVERY/INSPECTION UPON DISCHARGE GATE-OUT TO WITH PRECLEARING LA SPEZIA GENOA TIME SAVINGS DUE TO PRECLEARING: UP TO 48/60h (UP TO 72/90 IN CASE OF WEEK END OR HOLIDAY) -24h +24h +60h +90h -48h -00h +48h +72h SHIP ARRIVAL SHIP OPERATIONS SHIP DEPARTURE WITHOUT PRECLEARING CUSTOM CLEARANCE RELOAD ORDER FROM MTO CONTAINER AVAILABLE FOR DELIVERY/ INSPECTION GATE-OUT TO 98

99

100 11,000 km 16 / 20 days vs 30 days (ship)

101

102

103 Containerization revolution modern terminal operations Trnashipment & intermodal transport big ship and future challenges

104 LEGHORN, 2001 Improving the TERMINALS OFFER 104

105 RAVENNA, 2002 Adding new PRODUCT 105

106 CAGLIARI, 2003 The era of TRANSHIPMENT 106

107 TANGIER, 2008 North Africa DEVELOPMENTS 107

108 LA SPEZIA, 2011 The first ULCC call in ITALY 108

109 MILAN, 2012 A new PRIVATE RAIL operator 109

110 LA SPEZIA, ,600 TEU, the largest ship ever calling an Italian port 110

111 MELZO (MILAN), 2015 Improving the SOUTH CORRIDOR 111

112 LA SPEZIA, brand new 23 ROWS quay cranes 112

113 Source: A. Penfold

114 Source: A. Penfold

115 Source: Drwery 2 Container Forecast 2015

116 Source: A. Penfold

117 Source: A. Penfold

118 Source: A. Penfold

119 Source: A. Penfold

120 IMPACT ON FREIGHT RATES 120

121 Alphaliner - TOP 20 Operated fleets as per 13 September 2015 Today, there are 6,070 ships active on liner trades, for 20,010,806 TEU

122

123

124 THE LARGEST SHIPS TODAY 124

125

126

127

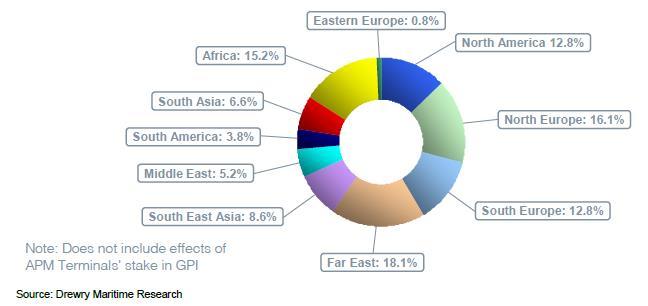

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142 Infographic: Drewry, Global Container Terminal Operators Annual Report 2014

143 IMPACT OF MEGA SHIPS ON PORTS 143

144

145 + = SUPPLY/DEMAN FREIGHT RATES PRESSURE ON INFRASTRUCTURE 145

146 146

147 IMPACT OF MEGASHIPS ++ INSURANCE COSTS 147

148

149 IMPACT ON PORT PRODUCTIVITY 149

150

151

152