Update of the 2010 City of Toronto Blue Bin Lifestyle and Packaging

|

|

|

- Philip Singleton

- 5 years ago

- Views:

Transcription

1 Update of the 2010 City of Toronto Blue Bin Lifestyle and Packaging Vincent Sferrazza, Director of Policy, Planning & Support Canadian Waste to Resource Conference October 24, 2018

2 Agenda Item Study Background Changing Lifestyles Packaging Trends Industry Interview Findings Consolidating Findings Conclusion

3 Study Background

4 Toronto Blue Bin Trends Studies Study completed by Kelleher Environmental. Blue Bin Trends Study 2010 Identified lifestyle trends that would impact Blue Bin material composition for the next 15 years. Projections informed Toronto s business planning process. Evolving Tonne has been studied by other jurisdictions (e.g. City of Calgary, 2014). Blue Bin Trends Study 2018 Composition changes continuing but there are new packaging formats: Multi-layer packaging Small, single-serve packages Take-out containers, etc. Related to consumer demands by different demographics. Updated research with projections to 2025.

5 Changing Lifestyles

6 Demographics and Purchasing Patterns

7 Sales in billion U.S. dollars Internet Sales * 2018* 2019* 2020* 2021* Statista: E-commerce as percentage of total retail sales in Canada from 2013 to 2020.

8 Meal Kits

9 Prepared Foods

10 Packaging Trends

11 Package Light-Weighting FoodBev Media. 27 October % less material used in water bottles than in 2007, IBWA says.

12 Packaging Material Changes Fairley, A. 17 August Evolving Recycling Systems and Strategies: The Effect on State Recycling Goals.

13 Shrink-flation UK Example Poulter, S. 20 June Your shrinking shop: Big-name brands cutting size of their products but the cost says the same.

14 Shrink-flation

15 Concentrated Products and Refillable Formats

16 Flexible Packaging Increasing Packaging Europe. 19 May Flexible Packaging Market Growing at 5% CAGR to Exceed $250BN By 2024.

17 Bioplastic Packaging Increasing

18 kg/cap generated Other Plastics Generation Increasing PET Bottles HDPE Bottles Plastic Film Plastic Laminates Polystyrene Other Plastics

19 Decline in Newspaper

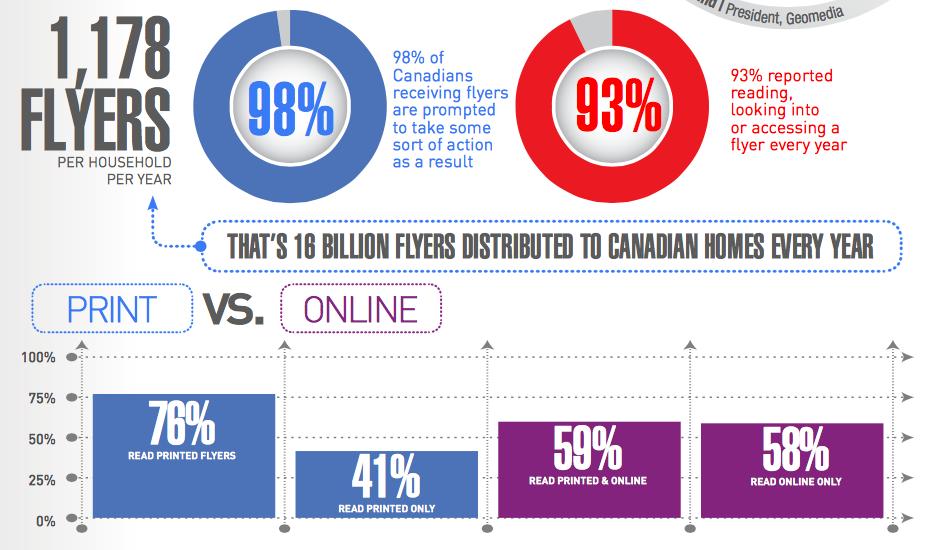

20 Flyers

21 Interview Findings

22 Material Recovery Facility Interview Findings Fibres Paper still makes up 50% of incoming materials and 50% of revenue. Single stream and two-stream responses varied: Optical sorting of old newsprint residue varied 0.5% to 10%. Sharp decline in newsprint, decline in old boxboard, and increase in old corrugated cardboard, creating fibre marketing challenges. International standards of 0.5% residue in bales. Shredded fine paper from in-home shredders cannot be recovered in most Material Recovery Facilities.

23 Material Recovery Facility Interview Findings - Packaging Old corrugated cardboard pieces becoming smaller (Internet or Amazon effect). Loose plastic bags and recyclables placed in bags continue to be largest disrupter of Material Recovery Facility productivity. Downtime to clean disc screens. Its hard to see a future where plastic film has any real value.

24 Association Interview Findings E-commerce increasing Food sector trends: Flexible packaging significantly increasing Reasons why everything is now in a package : Freshness Portion size Food lasts longer Example Fresh Cucumber Lasts 3 days if not wrapped in film plastic Lasts 10 days if wrapped in film plastic

25 Tonnes Mixed Plastics Recovered Increasing 7,000 6,000 5,000 4,000 3,000 2,000 PET HDPE Plastic Film Tubs and Lids Polystyrene Mixed Plastic 1,

26 Consolidating Findings

27 Putting it Together Traditional Packaging Materials Packaging Material Steel Status in 2018 compared to 2010, and likely changes by Declined as more food products move to more flexible formats. Expect continued decline. Aluminum Polyethylene Terephthalate (PET) High-density Polyethylene (HDPE) Polystyrene (PS) Has remained steady. Expect to remain steady. Increased for fresh produce and prepared foods; PET thermoform replacing Polyvinyl Chloride thermoform for household items. Increase expected to continue. Potential for some products (e.g. water) to switch to polycoat cartons. Has remained steady with moderate increase. Expected to remain steady with moderate increase. Has remained flat; no separate data on rigid PS. Likely to continue flat with increased pressure on single-use packaging growth.

28 Putting it Together New Format Packaging Packaging Material Stand-up Pouches Multilayered and Flexible Food Packaging Plastic Film Status in 2018 compared to 2010, and likely changes by Increased substantially used for liquid products. Other mixed plastics have also grown. Significant growth expected up to 50%. Significantly more. Substantial shift into multi-layer from old boxboard and steel packaging (for cereals, tuna, soup, etc.). Increase for prepared meats and produce expected up to 50% if current lifestyle trends continue. Has remained steady. May decline as single-use plastics policies implemented.

29 Putting it Together New Format Packaging (continued) Packaging Material Smart Packaging Status in 2018 compared to 2010, and likely changes by Began to emerge in early to mid 2000 s. Expected to slowly gain some market share for very specific items. Sustainable Packaging Biodegradable and Compostable Packaging Began to emerge in early to mid 2000 s. Expected to increase as more companies announce sustainability targets, particularly since more attention on plastics. Expected to continue to grow as more companies announce sustainability targets, and biodegradable and compostable are messages which consumers view favourably.

30 Putting it Together Paper Packaging Packaging Material Old Corrugated Cardboard (OCC) Old Boxboard (OBB) Polycoat and Aseptic Containers Status in 2018 compared to 2010, and likely changes by Increased due to on-line shopping but not observed in Toronto recovery data (perhaps due to light-weighting of OCC). Increased generation likely but offset by switch to lighter materials (e.g. old boxboard and heavy film plastic or bubble wrap formats), and also to optimizing package size. Has remained steady. Increased generation expected due to online sales. Has been reasonably stable. Expect increase with continuing switch from heavier packaging materials (e.g. soup packaging moving from steel to polycoat containers).

31 Putting it Together Newspaper Packaging Material Daily Newspapers Community Newspapers and Ethnic Press Status in 2018 compared to 2010, and likely changes by Significant decline, with smaller newspapers, and some newspapers likely to stop publishing a paper version. Future is more digital, with less print advertising, as advertising revenues are going to Internet Companies such as Facebook and Google. Slight decline. As advertising moves to digital formats, sustainability of community papers and ethnic press will decline, but more slowly than major dailies.

32 Putting it Together Other Printed Paper Packaging Material Telephone Directories Flyers Magazines and Catalogues Other Printer Paper (home office printing, junk mail, paper bills, flyers, etc.) Packaging Status in 2018 and likely changes by Minimal amounts. Not expected to change by Same pace as community newspapers. Slight decline but will remain for some market niches. Steady decline due to shift to digital formats. Has declined. Expected to continue to decline due to on-line banking; decline in junk mail, increase on-line advertising. Shredded paper problem in Material Recovery Facilities likely to continue.

33 Conclusion

34 2018 Toronto Blue Bin Trends Study Conclusions Combined with focus on healthy food, packaging and portions have completely changed: Everything is now in a package. One tonne of recyclables contains thousands of small packages. E-commerce exploding, trend will continue: Amazon using machine learning/ai to right size box. Where small item, moving to envelope with bubble wrap.

35 Thank you! Contact Information: Vincent Sferrazza Director of Policy, Planning & Support City of Toronto City Hall 100 Queen Street West 25 th Floor, East Tower Toronto, ON M5H 2N2