The Shipping Industry

|

|

|

- Ashlyn Malone

- 5 years ago

- Views:

Transcription

1 The Shipping Industry G.Skrimizeas Athens University of Economics and Business Page 1

2 The Shipping Industry Represents 90% of world trade Reflects world economy In 2016, about millιon tonnes of cargo were transported Page 2

4% 30% 18% Container Trade ( 1.794 million tonnes) Oil Trade( 3.035 million tonnes) Gas Trade ( 377 million tonnes) Major Bulk Trade( iron etc.) (3.")

3 World Seaborne Trade Total World Seaborne Trade Million Tonnes 12000, , , , , ,00 0, (f) World Seaborne Trade Breakdown 30% 18% Minor Bulk Trade( Scrap etc) (1.886 million tonnes) 4% 30% 18% Container Trade ( million tonnes) Oil Trade( million tonnes) Gas Trade ( 377 million tonnes) Major Bulk Trade( iron etc.) (3.094 million tonnes) Page 3

4 Main Dry bulk Routes Grains Grains Coal Coal Grains Iron Ore Coal Iron Ore Coal Major Coal Trades Australia Far East Australia W. Europe S. Africa W. Europe Colombia W. Europe Major Iron Ore Trades Australia Japan Australia China Brazil - China Brazil W. Europe Major Grain Trades U.S. Gulf Latin America U.S. Gulf - Japan U.S. Gulf - China Argentina Middle / Far East Asia Page 4

5 Main Tanker & Product Routes Crude Oil Products Products Crude Oil Crude Oil Products Products Crude Oil Products Crude Oil Major Crude Oil Routes Arabian Gulf USA Black Sea Europe Arabian Gulf Far East North Sea Europe West Africa USA North Africa Europe West Africa Far East South America USA Major Oil Products Routes Arabian Gulf USA North Sea Europe Arabian Gulf Far East North Africa Europe Arabian Gulf Europe South America USA Europe USA South Korea USA Europe West Africa Inter Far East Black Sea Europe Page 5

Europe Asia (Eastbound) Intra Asia Page")

6 Main Container Routes Container Asia-Europe Westbound Container Trans-Pacific Trans-Atlantic Europe-Asia Eastbound Container Intra-Asia Major Container Routes Trans Pacific Trans Atlantic Asia Europe (Westbound) Europe Asia (Eastbound) Intra Asia Page 6

Ultramax 60,000 67,999 Handymax / Supramax 40,000 59,999 Handysize < 39,999")

7 Vessel Sizes Dry bulk Carriers Vessel Size DWT Range VLOC > 200,000 Capesize 110, ,999 Post-Panamax 90, ,999 Panamax / Kamsarmax 68,000 89,999 35% of World Fleet (By % of GT) Ultramax 60,000 67,999 Handymax / Supramax 40,000 59,999 Handysize < 39,999 Page 7

MRs 30,000 59,999 Handy < 30,000 Page")

8 Vessel Sizes Tankers Vessel Size DWT Range VL/ULCC > 200,000 Suezmax 120, ,999 Aframax 80, ,999 Panamax 60,000 79,999 25% of World Fleet (By % of GT) MRs 30,000 59,999 Handy < 30,000 Page 8

Sub-Panamax 2,000 2,999 Handy 1,000 1,999 Feeder < 999 Page")

9 Vessel Sizes Containerships Vessel Size TEU Range Very Large > 10,000 Large 8,000 9,999 Post-Panamax 5,000 7,999 Panamax 3,000 4,999 18% of World Fleet (By % of GT) Sub-Panamax 2,000 2,999 Handy 1,000 1,999 Feeder < 999 Page 9

10 Greek Shipping Cluster About vessels Bss GT, 16% of Global & 44% of EU fleet About 650 ship-owning companies Greek Seafarers shore personnel ( directly or indirectly) 58%ofUSlistedshippingcompaniesareofGreekinterest World Champion Page 10

11 Ship Type Analysis of The Greek owned Fleet in Dwt Page 11

12 Fleet Percentage held by Each Size Group DWT Terms Page 12

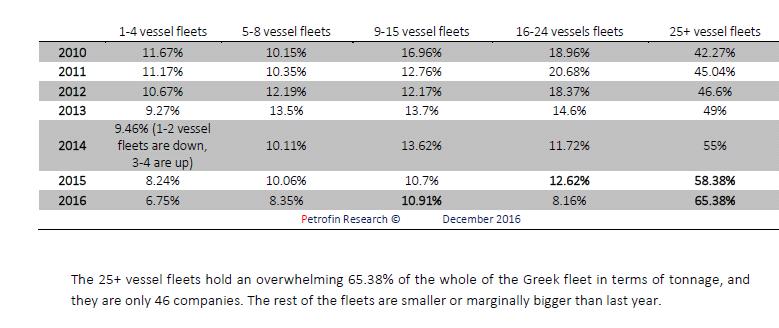

13 Number of Greek Shipping Companies in operation Page 13

14 Number of Greek Shipping Companies in terms of fleet size Page 14

15 Greek Shipping Powers Page 15

16 Benefits for Greece 13.4billionannually 6%ofGreekGDP Employs approximately people 3.5% of total Greek employment 136 billion receipts in Services Balance for the past decade Invests shipping funds in basic sectors of Greek economy Example for other sectors Reverses negative stereotypes for Greece Page 16

17 Strategic Decisions Sector Selection Revenue - Cash Management Leverage Equity Timing Page 17

- Chartering - Leverage, strategy - Private Sector how (spot much?")

18 Balancing Fleet Investment ASSETS LIABILITIES & EQUITY CURRENT ASSETS - Chartering strategy (spot or period) - Counterparty risk FIXED ASSETS (Fleet) - Sector - Type - Age - Timing FIXED CURRENT FINANCE ASSETS EQUITY ASSETS (Fleet) - Chartering - Leverage, strategy - Private Sector how (spot much? or period) Corporate - Type - Counterparty of borrowing Strategy --Public Type (bilateral, risk syndicate, bonds etc.) - Age - Timing FINANCE - Leverage, how much? - Type of borrowing (bilateral, syndicate, bonds etc.) EQUITY -Private -Public Slide 18

19 Main Drivers Changes in Demand Changes in Supply Page 19

20 Changes in Demand Political Decisions Bans, Boycotts, War, Trade Agreements Global Economy Environmental Regulations Natural Phenomena Unexpected Crises NO Control over Demand Page 20

21 Changes in Supply Scrapping Lay-Up Slow Steaming New Deliveries (Ordering) Future Prospects New building Prices Access to Finance Interest Rates Technological Improvements of New Designs Owners CAN Control Page 21

22 The Shipping Cycle HIGH: Shortage of Global Fleet Shrinks Demand: Unknown Ordering: Scrapping: Ships Strong Market Average Weak Market Scrapping: Ordering: Demand: Unknown Deliveries: Depending on Yard Capacity LOW: Surplus of Ships Page 22

23 TIMING!! Investment Environment Funding Demand Supply Asset Values & Charter Levels Page 23

24 Asset Values & Charter Levels Panamax Drybulk Carrier Aframax Tankers USD Per Day USD Million USD Per Day USD Million Yr TC Rate Average 5 Yr Old Value Average 1 Yr TC Rate Average 5 Yr Old Value Average USD Per Day 3,500 TEU Containerships Yr TC Rate Average 5 Yr Old Value Average USD Million Asset Values TC Rates Bulk Carriers -53% -57% Tankers -32% -21% Containers -76% -54% Source: Clarkson s Research Page 24

25 Challenges Ahead Crewing Compliance Capital Markets Demand Page 25

26 Key Takeaways Shipping is a very dynamic, yet demanding industry. Greek Shipping : The Global Leader. Greek Shipping is mainly International Shipping. Shipping should be one of the driving forces for the Greek Economy. Page 26

27 Thank you 15, Karamanli Avenue, Voula, GR , Athens, Greece Telephone: Fax : info@allseas.gr Web Site: Page 27