Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Alicia Singleton

- 6 years ago

- Views:

Transcription

1 Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Chapter 05 Reporting and Analyzing Inventories

3 Conceptual Chapter Objectives C1: Identify the items making up merchandise inventory. C2: Identify the costs of merchandise inventory.

4 Analytical Chapter Objectives A1: Analyze the effects of inventory methods for both financial and tax reporting. A2: Analyze the effects of inventory errors on current and future financial statements. A3: Assess inventory management using both inventory turnover and days sales in inventory.

5 Procedural Chapter Objectives : Compute inventory in a perpetual system using the methods of specific identification, FIFO, LIFO, and weighted average. P2: Compute the lower of cost or market amount of inventory. P3: Appendix 5A Compute inventory in a periodic system using the methods of specific identification, FIFO, LIFO, and weighted average (see text for details). P4: Appendix 5B Apply both the retail inventory and gross profit methods to estimate inventory (see text for details).

6 C1 Determining Inventory Items Merchandise inventory includes all goods that a company owns and holds for sale, regardless of where the goods are located when inventory is counted. Items requiring special attention include: Goods in Transit Goods on Consignment Goods Damaged or Obsolete

7 C1 Goods in Transit FOB Shipping Point Public Carrier Seller Buyer Ownership passes to the buyer here. Public Carrier Seller FOB Destination Point Buyer

8 C2 Determining Inventory Costs Include all expenditures necessary to bring an item to a salable condition and location. Minus Discounts and Allowances Plus Import Duties Invoice Cost Plus Freight Plus Insurance Plus Storage

9 C2 Internal Controls and Taking a Physical Count Most companies take a physical count of inventory at least once each year. When the physical count does not match the Merchandise Inventory account, an adjustment must be made. Inv e Cou ntory n Qua t Tag nt Cou ity nte d_ Cou n t e by d

10 Inventory Costing Under a Perpetual System Accounting for inventory requires several decisions... Costing Method Specific Identification, FIFO, LIFO, or Weighted Average Inventory System Perpetual or Periodic

11 Frequency in Use of Inventory Methods

12 Inventory Cost Flow Assumptions First-In, First-Out (FIFO) Assumes costs flow in the order incurred. Last-In, First-Out (LIFO) Assumes costs flow in the reverse order incurred. Weighted Average Assumes costs flow at an average of the costs available.

13 Inventory Costing Illustration

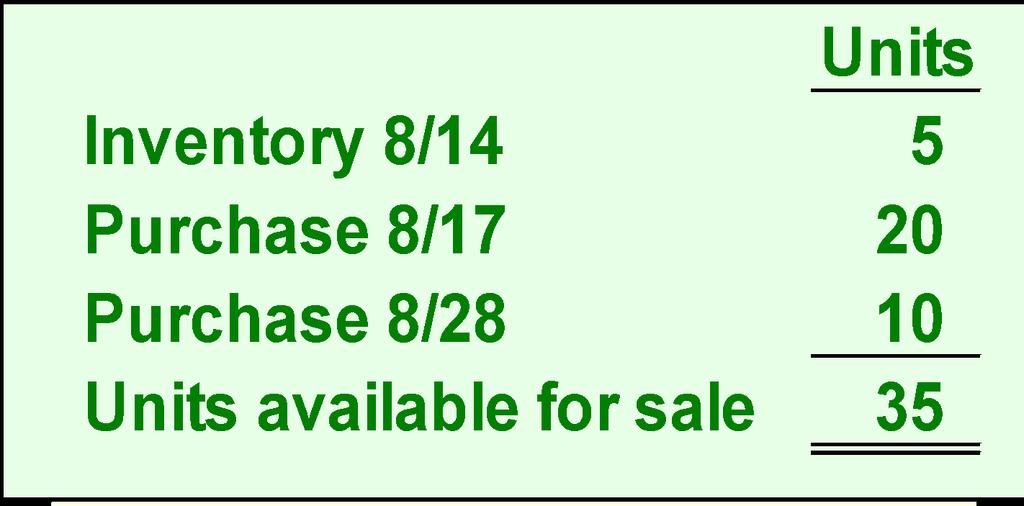

14 Specific Identification The above purchases were made in August. On August 14, a company sold 8 bikes originally costing $91 and 12 bikes originally costing $106.

15 Specific Identification The cost of goods sold for the 20 bikes sold on the August 14 sale is $2, = $ = $1,272 After this sale, there are five units in inventory at $500: 2 $91 = $ $106 = $ 318

16 Specific Identification Additional purchases were made on August 17 and 28. The cost of the 23 items sold on August 31 were as follows: $91 $106 $115 $119

17 Specific Identification Cost of goods sold for August 31 = $2,582

18 Specific Identification Here are the entries to record the purchases and sales. The numbers in red are determined by the cost flow assumption used. All purchases and sales are made on credit. The selling price of inventory was as follows: 8/14 $130 8/31 150

19 First-In, First-Out (FIFO) The above purchases were made in August. On August 14, the company sold 20 bikes.

20 First-In, First-Out (FIFO) The Cost of goods sold for the August 14 sale is $1,970. After this sale, there are five units in inventory at $530: $106

21 First-In, First-Out (FIFO) Cost of goods sold for August 31 = $2,600

22 First-In, First-Out (FIFO) Income Statement COGS = $4,570 Balance Sheet Inventory = $1,420

23 First-In, First-Out (FIFO) Here are the entries to record the purchases and sales entries. The numbers in red are determined by the cost flow assumption used. All purchases and sales are made on credit. The selling price of inventory was as follows: 8/14 $130 8/31 150

24 Last-In, First-Out (LIFO) The above purchases were made in August. On August 14, the company sold 20 bikes.

25 Last-In, First-Out (LIFO) The Cost of goods sold for the August 14 sale is $2,045. After this sale, there are five units in inventory at $455: $91

26 Last-In, First-Out (LIFO) Cost of goods sold for August 31 = $2,685

27 Last-In, First-Out (LIFO) Income Statement COGS = $4,730 Balance Sheet Inventory = $1,260

28 Last-In, First-Out (LIFO) Here are the entries to record the purchases and sales entries. The numbers in red are determined by the cost flow assumption used. All purchases and sales are made on credit. The selling price of inventory was as follows: 8/14 $130 8/31 150

29 Weighted Average When a unit is sold, the average cost of each unit in inventory is assigned to cost of goods sold. Cost of goods Units on hand available for on the date of sale sale

30 Weighted Average First, we need to compute the weighted average cost per unit of items in inventory. The cost of goods sold for the August 14 sale is $2,000. After this sale, there are five units in inventory at $500:

31 Weighted Average Additional purchases were made on August 17 and 28. Twenty-three bikes were sold on August 31. What is the weighted average cost per unit of items in inventory?

32 Weighted Average

33 Weighted Average Cost of goods sold for August 31 = $2,622 Ending inventory is comprised of 12 an average cost of $114 each or $1,368.

34 Weighted Average Income Statement COGS = $4,622 Balance Sheet Inventory = $1,368

35 Weighted Average Here are the entries to record the purchases and sales entries for Trekking. The numbers in red are determined by the cost flow assumption used. All purchases and sales are made on credit. The selling price of inventory was as follows: 8/14 $130 8/31 150

36 A1 Financial Statement Effects of Costing Methods Because prices change, inventory methods nearly always assign different cost amounts.

37 A1 Financial Statement Effects of Costing Methods Advantages of Methods Weighted Average First-In, First-Out Last-In, FirstOut Smoothes out price changes. Ending inventory approximates current replacement cost. Better matches current costs in cost of goods sold with revenues.

identifies several acceptable methods for")

38 A1 Tax Effects of Costing Methods The Internal Revenue Service (IRS) identifies several acceptable methods for inventory costing for reporting taxable income. If LIFO is used for tax purposes, the IRS requires it be used in financial statements.

39 A1 Consistency in Using Costing Methods The consistency concept requires a company to use the same accounting methods period after period so that financial statements are comparable across periods.

40 P2 Lower of Cost or Market Inventory must be reported at market value when market is lower than cost. Defined as current replacement cost (not sales price). Consistent with the conservatism principle. Can be applied three ways: (1) separately to each individual item. (2) to major categories of assets. (3) to the whole inventory.

41 P2 Lower of Cost or Market A motorsports retailer has the following items in inventory:

42 P2 Lower of Cost or Market Here is how to compute lower of cost or market for individual inventory items.

43 A2 Financial Statement Effects of Inventory Errors Income Statement Effects

44 A2 Financial Statement Effects of Inventory Errors Balance Sheet Effects

45 A3 Inventory Turnover Shows how many times a company turns over its inventory during a period. Indicator of how well management is controlling the amount of inventory available. Cost of goods sold Inventory turnover = Average inventory

46 A3 Days Sales in Inventory Reveals how much inventory is available in terms of the number of days sales. Days' sales in inventor y Ending inventory = Cost of goods sold 36 5

47 End of Chapter 05

INVENTORIES AND COST OF SALES

Chapter 06 INVENTORIES AND COST OF SALES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 06 INVENTORIES AND COST OF SALES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

Financial Accounting Chapter 6 Notes Inventories

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

CHAPTER 5: MERCHANDISING OPERATIONS

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

Chapter 7 Condensed (Day 1)

") Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

INTERMEDIATE ACCOUNTING 321 FEB 28, 2018 TAD MILLER INVENTORY TEST

INTERMEDIATE ACCOUNTING 321 FEB 28, 2018 TAD MILLER INVENTORY TEST 03. 2182 1. WHAT S INCLUDED IN INVENTORY? The Tucson Corporation's fiscal year ends on December 31. Tucson determines inventory quantity

INTERMEDIATE ACCOUNTING 321 FEB 28, 2018 TAD MILLER INVENTORY TEST 03. 2182 1. WHAT S INCLUDED IN INVENTORY? The Tucson Corporation's fiscal year ends on December 31. Tucson determines inventory quantity

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Inventories. 2. Explain the accounting for inventories and apply the inventory cost flow methods.

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

Valuation of inventories

Valuation of inventories The sale of inventory at a price greater than total cost is the primary source of income for manufacturing and retail businesses. Inventories are asset items held for sale in the

Valuation of inventories The sale of inventory at a price greater than total cost is the primary source of income for manufacturing and retail businesses. Inventories are asset items held for sale in the

Ch6 Practice Test Part 1: Multiple Choice Choose the most correct answer from the choices provided.

Part 1: Multiple Choice Choose the most correct answer from the choices provided. 1. The factor which determines whether or not goods should be included in a physical count of inventory is a. physical

Part 1: Multiple Choice Choose the most correct answer from the choices provided. 1. The factor which determines whether or not goods should be included in a physical count of inventory is a. physical

PURCHASES - GROSS METHOD

INTERMEDIATE ACCOUNTING 321 MAY 21, 2016 TAD MILLER INVENTORY TEST 03. 2184 Round your answers to the nearest cent $xxx.xx PURCHASES - GROSS METHOD - PERIODIC INVENTORY SYSTEM On May 10 th Our Co. ordered

INTERMEDIATE ACCOUNTING 321 MAY 21, 2016 TAD MILLER INVENTORY TEST 03. 2184 Round your answers to the nearest cent $xxx.xx PURCHASES - GROSS METHOD - PERIODIC INVENTORY SYSTEM On May 10 th Our Co. ordered

INVENTORY VALUATION THE SIGNIFICANCE OF INVENTORY

THE SIGNIFICANCE OF INVENTORY INVENTORY VALUATION Accounting Unit 3 In the balance sheet inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining

THE SIGNIFICANCE OF INVENTORY INVENTORY VALUATION Accounting Unit 3 In the balance sheet inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining

PREVIEW OF CHAPTER. Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

Chapter Outline. Study Objective 1 - Describe the Steps in Determining Inventory Quantities

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

ACCOUNTING FOR MERCHANDISING OPERATIONS

Chapter 05 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 05 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 9: Inventories. Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules

Chapter 9: Inventories Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules 1 Characteristics of Inventories belong to current assets

Chapter 9: Inventories Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules 1 Characteristics of Inventories belong to current assets

ACCOUNTING - CLUTCH CH. 5 - INVENTORY.

!! www.clutchprep.com CONCEPT: MERCHANDISING COMPANY VS MANUFACTURING COMPANY A merchandising company has Inventory account. Merchandisers goods manufactured by others. The Inventory account might also

!! www.clutchprep.com CONCEPT: MERCHANDISING COMPANY VS MANUFACTURING COMPANY A merchandising company has Inventory account. Merchandisers goods manufactured by others. The Inventory account might also

Chapter 7: Merchandise Inventory

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K a 22. 7 C sg 29. 3

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K a 22. 7 C sg 29. 3

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS Key Terms and Concepts to Know Merchandise Inventory: Merchandise Inventory (Inventory or MI) refers to the goods the company has purchased and intends

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS Key Terms and Concepts to Know Merchandise Inventory: Merchandise Inventory (Inventory or MI) refers to the goods the company has purchased and intends

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

C H A P T E R. Inventories. Corporate Financial Accounting 13e. human/istock/360/getty Images. Warren Reeve Duchac

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

Prepared by Johnny Howard 2015 South-Western, a part of Cengage Learning

Prepared by Johnny Howard 17 2 T E R M S Accounting for Inventory Physical inventory an actual counting of the merchandise on hand Perpetual inventory a running count of all inventory items, based on tracking

Prepared by Johnny Howard 17 2 T E R M S Accounting for Inventory Physical inventory an actual counting of the merchandise on hand Perpetual inventory a running count of all inventory items, based on tracking

CHAPTER 6. Inventory Costing. Brief Questions Exercises Exercises 4, 5, 6, 7 3, 4, *14 3, 4, 5, 6, *12, *13 7, 8, 9, 10, 11, 12, 13

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

CHAPTER 6. Inventories 12, 13, , , 11 16, , 13

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

Accounting 1 Instructor Notes

Accounting 1 Instructor Notes CHAPTER 6 ACCOUNTING FOR MERCHANDISING BUSINESS Accounting for a merchandising business is much more complex than a service business. This is because a service business sells

Accounting 1 Instructor Notes CHAPTER 6 ACCOUNTING FOR MERCHANDISING BUSINESS Accounting for a merchandising business is much more complex than a service business. This is because a service business sells

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT

Learning Objectives CHAPTER 6 MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT 1. Record journal entries for sales transactions involving merchandise. 2. Describe

Learning Objectives CHAPTER 6 MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT 1. Record journal entries for sales transactions involving merchandise. 2. Describe

Inventories DETERMINING INVENTORY ON HAND DETERMINING COST OF INVENTORY. Chapter 19. Perpetual system. Periodic system. Transfer of ownership

Chapter 19 Inventories PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd DETERMINING INVENTORY ON HAND Perpetual system Detailed records required Periodic

Chapter 19 Inventories PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd DETERMINING INVENTORY ON HAND Perpetual system Detailed records required Periodic

CHAPTER 6. Inventories ASSIGNMENT CLASSIFICATION TABLE For Instructor Use Only 6-1. Brief. B Problems. A Problems 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

Week 5. ACT102 Introduction to Accounting. Objectives 21/02/2018. What are retailing operations?

ACT102 Introduction to Accounting Week 5 Objectives Describe retailing operations, perpetual and periodic inventory systems and understand how to account for GST Account for the purchase of inventory using

ACT102 Introduction to Accounting Week 5 Objectives Describe retailing operations, perpetual and periodic inventory systems and understand how to account for GST Account for the purchase of inventory using

CHAPTER 8: INVENTORY

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

MGACO1 INTERMEDIATE ACCOUNTING I

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations I. Management Issues in Merchandising Business Merchandising business earns income by buying and selling goods. Such

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations I. Management Issues in Merchandising Business Merchandising business earns income by buying and selling goods. Such

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 8, Perpetual vs. periodic. 2 9, 13, 14, 17, 20

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

Chapter 6 Accounting for Merchandising Businesses Study Guide Do You Know?

Chapter 6 Accounting for Merchandising Businesses Study Guide Do You Know? Learning Objective 1: Distinguish between the activities and financial statements of service and merchandising businesses. Some

Chapter 6 Accounting for Merchandising Businesses Study Guide Do You Know? Learning Objective 1: Distinguish between the activities and financial statements of service and merchandising businesses. Some

Accounting 101 Class Notes Chapter 4 Accounting for Merchandising Operations

I. WHAT IS A MERCHANDISER? Merchandiser vs. Service Business Wholesaler vs. retailer This chapter changes the focus from a service-oriented business to a merchandising form of business. Merchandisers buy

I. WHAT IS A MERCHANDISER? Merchandiser vs. Service Business Wholesaler vs. retailer This chapter changes the focus from a service-oriented business to a merchandising form of business. Merchandisers buy

Chapter 6 Question Review 1

Chapter 6 Question Review 1 Chapter 6 Questions Multiple Choice 1. In a perpetual inventory system, a. LIFO cost of goods sold will be the same as in a periodic inventory system. b. average costs are based

Chapter 6 Question Review 1 Chapter 6 Questions Multiple Choice 1. In a perpetual inventory system, a. LIFO cost of goods sold will be the same as in a periodic inventory system. b. average costs are based

These Review Notes for the CHAE Examination. Stephen M. LeBruto, Ed.D, CPA, CHAE. i Management and Technology. Rosen College of Hospitality Management

CHAE Review Basics, Inventory and Internal Controls These Review Notes for the CHAE Examination Were Prepared By: Stephen M. LeBruto, Ed.D, CPA, CHAE HFTP Professor of Hospitality Financial i Management

CHAE Review Basics, Inventory and Internal Controls These Review Notes for the CHAE Examination Were Prepared By: Stephen M. LeBruto, Ed.D, CPA, CHAE HFTP Professor of Hospitality Financial i Management

1 INTRODUCTION DEFINITIONS VALUATION INVENTORY ALLOWANCE (NET REALIZABLE VALUE) REPORTING INTERNAL INVENTORY...

REPORTING INTERNAL INVENTORY...") RAPALA INVENTORY VALUATION PRINCIPLES AND INTERNAL INVENTORY 1 INTRODUCTION... 2 2 DEFINITIONS... 2 2.1 INVENTORIES... 2 2.2 STOCK COVERAGE... 3 2.3 OBSOLETE INVENTORY... 3 2.4 NET REALIZABLE VALUE...

RAPALA INVENTORY VALUATION PRINCIPLES AND INTERNAL INVENTORY 1 INTRODUCTION... 2 2 DEFINITIONS... 2 2.1 INVENTORIES... 2 2.2 STOCK COVERAGE... 3 2.3 OBSOLETE INVENTORY... 3 2.4 NET REALIZABLE VALUE...

CHAPTER 6 Inventory Costing ANSWERS TO QUESTIONS

CHAPTER 6 Inventory Costing ANSWERS TO QUESTIONS 1. Taking a physical inventory involves counting, weighing or measuring each kind of inventory on hand. This is normally done when the store is closed.

CHAPTER 6 Inventory Costing ANSWERS TO QUESTIONS 1. Taking a physical inventory involves counting, weighing or measuring each kind of inventory on hand. This is normally done when the store is closed.

Inventory and Cost of Goods Sold C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Inventory and Cost of Goods Sold E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition

Inventory and Cost of Goods Sold E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2

9-1 C H A P T E R 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2 Learning Objectives 1. Describe and apply the lower-of-cost-or-net realizable

9-1 C H A P T E R 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2 Learning Objectives 1. Describe and apply the lower-of-cost-or-net realizable

Chapter 6. Inventory Costing - Periodic

Chapter 6 Inventory Costing - Periodic Periodic Inventory Valuation a physical count of inventory is taken at the end of the fiscal year to determine how many units make up ending inventory. Throughout

Chapter 6 Inventory Costing - Periodic Periodic Inventory Valuation a physical count of inventory is taken at the end of the fiscal year to determine how many units make up ending inventory. Throughout

Chapter 13. Auditing the Inventory Management Process

Chapter 13 Auditing the Inventory Management Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Chapter 13 Auditing the Inventory Management Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Exercises. Use of purchase orders and vendors invoices, locking all high-priced items in a cabinet

Chapter 6 Inventories Study Guide Solutions Fill-in-the-Blank Equations 1. Units available for sale 2. Estimated selling price 3. Inventory turnover 4. Average daily cost of merchandise sold Exercises

Chapter 6 Inventories Study Guide Solutions Fill-in-the-Blank Equations 1. Units available for sale 2. Estimated selling price 3. Inventory turnover 4. Average daily cost of merchandise sold Exercises

The Purchasing Function:

ACCT 100 - Intro to Acct. Chapter 8 - Accounting for Purchases, A/P, and Cash Payments Prof. Johnson Where we have been: Last time we started our discussion for merchandising entities and focused on the

ACCT 100 - Intro to Acct. Chapter 8 - Accounting for Purchases, A/P, and Cash Payments Prof. Johnson Where we have been: Last time we started our discussion for merchandising entities and focused on the

SOLUTIONS. Learning Goal 18

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

PREVIEW OF CHAPTER 9-2

9-1 PREVIEW OF CHAPTER 9 9-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 9 Inventories: Additional Valuation Issues LEARNING OBJECTIVES After studying this chapter, you should

9-1 PREVIEW OF CHAPTER 9 9-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 9 Inventories: Additional Valuation Issues LEARNING OBJECTIVES After studying this chapter, you should

6) Items purchased for resale with a right of return must be presented separately from other inventories.

Items purchased for resale with a right of return must be presented separately from other inventories.") Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

CHAPTER 5. Accounting for Merchandising Operations 2, 3, , 12, 13, 14

CHAPTER 5 Accounting for Merchandising Operations ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Identify the differences between

CHAPTER 5 Accounting for Merchandising Operations ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Identify the differences between

Worksheet 2: Inventory Valuation and Control Study Questions

UNIVERSITY OF THE WEST INDIES Open Campus ACCT 1003 - Intro. to Cost & Management Accounting Worksheet 2: Inventory Valuation and Control Study Questions Question 1 Hyatt Magic carries an inventory of

UNIVERSITY OF THE WEST INDIES Open Campus ACCT 1003 - Intro. to Cost & Management Accounting Worksheet 2: Inventory Valuation and Control Study Questions Question 1 Hyatt Magic carries an inventory of

Accounting 101 Chapter 5 Inventories and Cost of Sales

I. Internal Controls of Inventory Accounting 101 Inventory consists of the items a business has for resale to customers in the normal course of business. A. s included in inventory 1. of the merchandise

I. Internal Controls of Inventory Accounting 101 Inventory consists of the items a business has for resale to customers in the normal course of business. A. s included in inventory 1. of the merchandise

ACCOUNTING FOR MERCHANDISING ACTIVITIES

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

Type of Inventory. OVERVIEW In case of manufacturing concerns. Stores and Spares. Formulae for Determining Cost of Inventory

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

Contents ADJUSTING THE ACCOUNTS. Analyze Accounts and Prepare Adjusting Entries 43. Learning Goal 4: Explain the Meaning of Accounting Period 7

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

INVENTORIES, DISCUSSION QUESTIONS

INVENTORIES, DISCUSSION QUESTIONS Cristina Maslach Zampetakis Laschinger 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for

INVENTORIES, DISCUSSION QUESTIONS Cristina Maslach Zampetakis Laschinger 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for

CHAPTER 7 INVENTORIES

INVENTORIES DISCUSSION QUESTIONS 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before inventory purchases are recorded and paid. This procedure will

INVENTORIES DISCUSSION QUESTIONS 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before inventory purchases are recorded and paid. This procedure will

Chapter 9 Inventories: Additional Issues

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

CHAPTER 6 INVENTORIES

1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for inventory purchases. This procedure will verify that the inventory received

1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for inventory purchases. This procedure will verify that the inventory received

Basic Inventory & CGS

Professor Authored Problem Solutions Intermediate Accounting 2 Basic Inventory & CGS Solution to Problem 55 Costs to add to inventory account 1. Cost to acquire or purchase 2. Cost to transport or ship

Professor Authored Problem Solutions Intermediate Accounting 2 Basic Inventory & CGS Solution to Problem 55 Costs to add to inventory account 1. Cost to acquire or purchase 2. Cost to transport or ship

Inventories. IAS Standard 2 IAS 2. IFRS Foundation

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

Accounting for Merchandising Businesses

CHAPTER 3 Accounting for Merchandising Businesses LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Identify and explain the primary features of the perpetual

CHAPTER 3 Accounting for Merchandising Businesses LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Identify and explain the primary features of the perpetual

Provided by Academy of Professional Accounting (APA)

") Professional Accounting Education Provided by Academy of Professional Accounting (APA) CMA Part I Section A External Financial Reporting Decisions CMA Lecturer: Eric HU ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright

Professional Accounting Education Provided by Academy of Professional Accounting (APA) CMA Part I Section A External Financial Reporting Decisions CMA Lecturer: Eric HU ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright

Palmyra Area School District 1125 Park Drive Palmyra, 17078

Palmyra Area School District 1125 Park Drive Palmyra, 17078 Planned Instruction for: Grade Levels: 11, 12 Authors: PALMYRA AREA SCHOOL DISTRICT Overview Grade Levels: 11, 12 Course Description This course

Palmyra Area School District 1125 Park Drive Palmyra, 17078 Planned Instruction for: Grade Levels: 11, 12 Authors: PALMYRA AREA SCHOOL DISTRICT Overview Grade Levels: 11, 12 Course Description This course

COURSE DESCRIPTION. Rev 2.0 March 2017

COURSE DESCRIPTION This CE course provides information on inventory management. Information discussed includes inventory methods and accounting systems, cost of goods sold, and inventory turnovers and

COURSE DESCRIPTION This CE course provides information on inventory management. Information discussed includes inventory methods and accounting systems, cost of goods sold, and inventory turnovers and

Chapter 16. using math in sales. Section 16.1 Sales Transactions. Section 16.2 Cash Registers. Section 16.3 Purchasing, Invoicing, and Shipping

Chapter 16 using math in sales Section 16.1 Sales Transactions Section 16.2 Cash Registers Section 16.3 Purchasing, Invoicing, and Shipping Section 16.1 Sales Transactions PREDICT What kinds of math does

Chapter 16 using math in sales Section 16.1 Sales Transactions Section 16.2 Cash Registers Section 16.3 Purchasing, Invoicing, and Shipping Section 16.1 Sales Transactions PREDICT What kinds of math does

COURSE TITLE. Honors Accounting LENGTH. Full Year Grades DEPARTMENT. Business Education Barbara O Donnell, Supervisor SCHOOL

COURSE TITLE Honors Accounting LENGTH Full Year Grades 11-12 DEPARTMENT Business Education Barbara O Donnell, Supervisor SCHOOL Rutherford High School DATE Fall 2016 Honors Accounting Page 1 I. Introduction/Overview/Philosophy

COURSE TITLE Honors Accounting LENGTH Full Year Grades 11-12 DEPARTMENT Business Education Barbara O Donnell, Supervisor SCHOOL Rutherford High School DATE Fall 2016 Honors Accounting Page 1 I. Introduction/Overview/Philosophy

Work4Me. Algorithmic Version. Problem Eight. Accounting for Accounts Payable and Merchandise Inventory with Perpetual Inventory System

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Eight Accounting for Accounts Payable and Merchandise Inventory with Perpetual Inventory System Page 1 UPTIGHT TOOLS, INCORPORATED CHART OF ACCOUNTS

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Eight Accounting for Accounts Payable and Merchandise Inventory with Perpetual Inventory System Page 1 UPTIGHT TOOLS, INCORPORATED CHART OF ACCOUNTS

IAS - 02 INVENTORIES

IAS - 02 INVENTORIES Objective To prescribe the accounting treatment for inventories. Scope All inventories except: (a) (b) Financial instruments (see IAS 32 Financial Instruments: Presentation and IFRS

IAS - 02 INVENTORIES Objective To prescribe the accounting treatment for inventories. Scope All inventories except: (a) (b) Financial instruments (see IAS 32 Financial Instruments: Presentation and IFRS

Topic 4. Session Objectives. Inventory Adjustments. Session Objectives. Inventory

Session Objectives Topic 4 Inventory Understand the need for adjustment for inventory in preparing financial statements Describe how opening and closing inventory appears in the profit and loss accounts

Session Objectives Topic 4 Inventory Understand the need for adjustment for inventory in preparing financial statements Describe how opening and closing inventory appears in the profit and loss accounts

Inventories IAS 2 IAS 2. IFRS Foundation

IAS 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

IAS 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

PROBLEMS INVENTORY VALUATION (1-6)

") Problems Accounting 21 PROBLEMS INVENTORY VALUATION (1-6) Problem # 21.1: Use the following information of Fatima Malik and Co. A company just starting business made the following four inventory purchases

Problems Accounting 21 PROBLEMS INVENTORY VALUATION (1-6) Problem # 21.1: Use the following information of Fatima Malik and Co. A company just starting business made the following four inventory purchases

ACCOUNTING. Contest Basics SAC 2016

ACCOUNTING Contest Basics SAC 2016 P a g e 2 UIL Accounting Basics Agenda 1. Constitution & Contest Rules and NEW Handbook 2. 2017 Condensed Contest Schedule & Solution 3. State-adopted textbooks (high

ACCOUNTING Contest Basics SAC 2016 P a g e 2 UIL Accounting Basics Agenda 1. Constitution & Contest Rules and NEW Handbook 2. 2017 Condensed Contest Schedule & Solution 3. State-adopted textbooks (high

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Study Guide 20. Part One Identifying Accounting Terms. Column II. Answers. Column I

Study Guide 20 Name Identifying Accounting Terms Analyzing Inventory Systems Analyzing LIFO, FIFO, and Weighted-Average Methods Total Perfect Score 9 Pts. 10 Pts. 12 Pts. 31 Pts. Your Score Part One Identifying

Study Guide 20 Name Identifying Accounting Terms Analyzing Inventory Systems Analyzing LIFO, FIFO, and Weighted-Average Methods Total Perfect Score 9 Pts. 10 Pts. 12 Pts. 31 Pts. Your Score Part One Identifying

COPYRIGHTED MATERIAL. FEATURE STORY: Financial Reporting: A Matter of. FEATURE STORY: No Such Thing as a Perfect

D E T A I L E D C O N T E N T S CHAPTER 1 HOSPITALITY ACCOUNTING IN ACTION 1 FEATURE STORY: Financial Reporting: A Matter of Trust 1 What Is Accounting? 2 Who Uses Accounting Data? 4 Brief History of Accounting

D E T A I L E D C O N T E N T S CHAPTER 1 HOSPITALITY ACCOUNTING IN ACTION 1 FEATURE STORY: Financial Reporting: A Matter of Trust 1 What Is Accounting? 2 Who Uses Accounting Data? 4 Brief History of Accounting

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA. Course Title ACCOUNTING II

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING II COURSE OF STUDY: ACCOUNITNG II COURSE LENGTH: Full Year ENDURING UNDERSTANDING: Accounting represents formal record keeping

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING II COURSE OF STUDY: ACCOUNITNG II COURSE LENGTH: Full Year ENDURING UNDERSTANDING: Accounting represents formal record keeping

Chapter 2 An Introduction to Cost Terms and Purposes

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

White Paper. Best Practice mbas Valuation Methodology

White Paper Best Practice mbas Valuation Methodology Table of Contents 1. Introduction... 3 2. Overview... 3 3. Benefits... 8 4. Conclusion... 8 Page 2 of 8 1. Introduction Objective of this document is

White Paper Best Practice mbas Valuation Methodology Table of Contents 1. Introduction... 3 2. Overview... 3 3. Benefits... 8 4. Conclusion... 8 Page 2 of 8 1. Introduction Objective of this document is

Sri Lanka Accounting Standard LKAS 2. Inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

August Copyright 2016 Open Systems Holdings Corp. All rights reserved.

This document describes the intended features and technology for TRAVERSE 11 as of August, 2016. Features and technology are subject to change and there is no guarantee that any particular feature or technology

This document describes the intended features and technology for TRAVERSE 11 as of August, 2016. Features and technology are subject to change and there is no guarantee that any particular feature or technology

New Zealand Equivalent to International Accounting Standard 2 Inventories (NZ IAS 2)

") New Zealand Equivalent to International Accounting Standard 2 Inventories (NZ IAS 2) Issued November 2004 and incorporates amendments up to and including 30 November 2012 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 2 Inventories (NZ IAS 2) Issued November 2004 and incorporates amendments up to and including 30 November 2012 other than consequential amendments

Entrepreneurship 2013 Chapter 15: Purchases and Inventory Management

Chapter 15: Purchases and Inventory Management Tools: Printer 8.5 x 11 paper Scissors Directions: 1. Print 2. Fold paper in half vertically 3. Cut along dashed lines Copyright Goodheart-Willcox Co., Inc.

Chapter 15: Purchases and Inventory Management Tools: Printer 8.5 x 11 paper Scissors Directions: 1. Print 2. Fold paper in half vertically 3. Cut along dashed lines Copyright Goodheart-Willcox Co., Inc.

Akuntansi Biaya. Angela Dirman, SE., M.Ak. Modul ke: Fakultas FEB. Program Studi Manajemen.

Akuntansi Biaya Modul ke: Material: Controlling, Costing, and Planning. Materials Procurement and Use. Quantitative Models. Material Control. Inventory Costing Method. Fakultas FEB Angela Dirman, SE.,

Akuntansi Biaya Modul ke: Material: Controlling, Costing, and Planning. Materials Procurement and Use. Quantitative Models. Material Control. Inventory Costing Method. Fakultas FEB Angela Dirman, SE.,

OPERATIONAL AND CONSUMABLE INVENTORY POLICY

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

Understanding Inventory Fundamentals

CHAPTER SEVEN Understanding Inventory Fundamentals McGraw-Hill/Irwin Copyright 2011 by the McGraw-Hill Companies, Inc. All rights reserved. Where We Are Now Relationships Sustainability Globalization Organizational

CHAPTER SEVEN Understanding Inventory Fundamentals McGraw-Hill/Irwin Copyright 2011 by the McGraw-Hill Companies, Inc. All rights reserved. Where We Are Now Relationships Sustainability Globalization Organizational

Geneva CUSD 304 Content-Area Curriculum Frameworks Grades 6-12 Business

Geneva CUSD 304 Content-Area Curriculum Frameworks Grades 6-12 Business Mission Statement In the Business Department, our mission is to: Provide a variety of subject areas. Introduce students to current

Geneva CUSD 304 Content-Area Curriculum Frameworks Grades 6-12 Business Mission Statement In the Business Department, our mission is to: Provide a variety of subject areas. Introduce students to current

7 Estimate the value of inventory using the. 8 Measure a company's management of. 9 Determine the value of inventory using the

1 Determine the value of inventory using the specific identification method under the perpetual inventory system 2 Determine the value of inventory using the first-in, first-out (FIFO) method under the

1 Determine the value of inventory using the specific identification method under the perpetual inventory system 2 Determine the value of inventory using the first-in, first-out (FIFO) method under the

FM038: Inventory Accounting and Costing

FM038: Inventory Accounting and Costing FM038 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Whether you are a trader, manufacturer, contractor or a service provider, inventory has a major

FM038: Inventory Accounting and Costing FM038 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Whether you are a trader, manufacturer, contractor or a service provider, inventory has a major

Chapter 8: Cost-Based Inventories and Cost of Sales

Chapter 8: Cost-Based Inventories and Cost of Sales Case 8-1 Love Your Pet, Inc. 8-2 Alliance Appliance Ltd. 8-3 Terrific Titles Inc. Suggested Time Technical Review TR-1 Right to Recovery Asset... 5 TR-2

Chapter 8: Cost-Based Inventories and Cost of Sales Case 8-1 Love Your Pet, Inc. 8-2 Alliance Appliance Ltd. 8-3 Terrific Titles Inc. Suggested Time Technical Review TR-1 Right to Recovery Asset... 5 TR-2

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

Supply Chain Finance

CTL.SC2x -Supply Chain Design Supply Chain Finance MIT Center for Transportation & Logistics Inventory Valua.on Methods: LIFO and FIFO 2 1 Inventory Valua.on In order to keep track of inventory, we need

CTL.SC2x -Supply Chain Design Supply Chain Finance MIT Center for Transportation & Logistics Inventory Valua.on Methods: LIFO and FIFO 2 1 Inventory Valua.on In order to keep track of inventory, we need

6 The following terms are used in this Standard with the meanings specified: Inventories are assets:

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

CONCEPTS FOR REVIEW INVENTORIES AND COST OF GOODS CALCULATION

9 INVENTORIES AND COST OF GOODS CALCULATION THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 265 p. 272 p. 280

9 INVENTORIES AND COST OF GOODS CALCULATION THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 265 p. 272 p. 280