IFIAR: International Forum of Independent Audit Regulators

|

|

|

- Loren White

- 6 years ago

- Views:

Transcription

1 IFIAR: International Forum of Independent Audit Regulators Marjolein Doblado, IFIAR SCWG Chair International Auditing and Assurance Standards Board Consultative Advisory Group Meeting Paris, 8 March

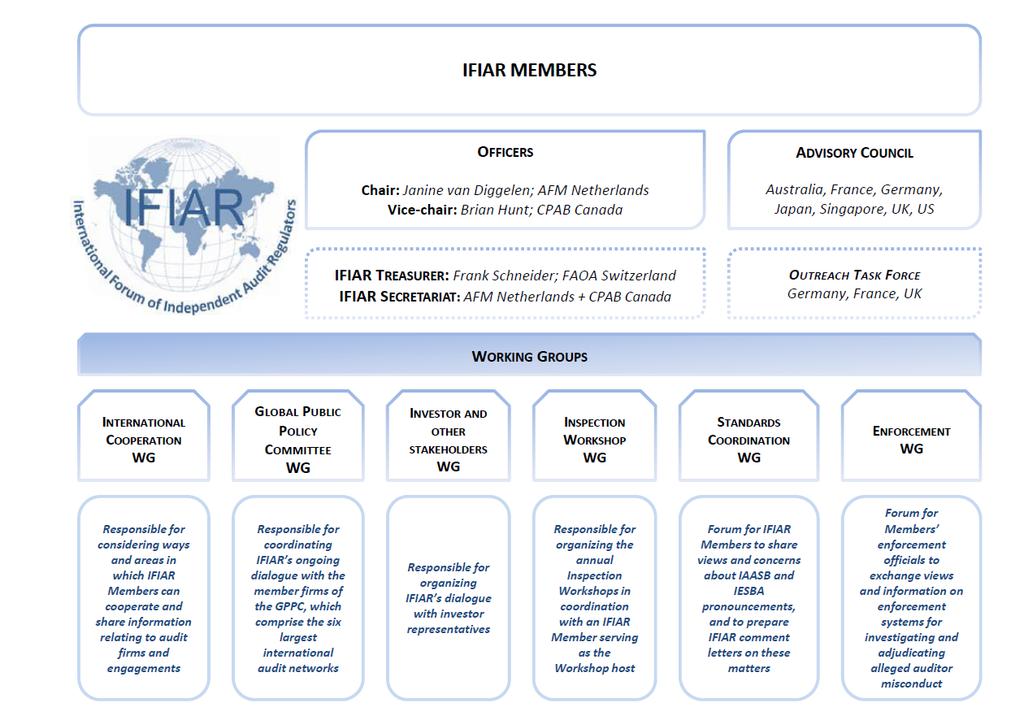

2 International Forum of Independent Audit Regulators Established in 2006 by independent audit regulators from 18 jurisdictions Has grown to 50 Members by 2016 Members must be independent of the profession, and engaged in audit regulatory functions, at least including inspections, in the public interest IFIAR s Members are from jurisdictions in Africa, Asia, Australia, Europe, the Middle East, North America and South America 2

3 IFIAR s Mission To share knowledge of the audit market environment and practical experience of independent audit regulatory activity; To promote collaboration in regulatory activity; and To provide a focus for contacts with other international organizations which have an interest in audit quality. 3

4 IFIAR Today Most IFIAR activities occur through working groups: Enforcement Working Group Global Audit Quality (GAQ) Working Group Inspection Workshop Working Group International Cooperation Working Group Investor and Other Stakeholders Working Group Standards Coordination Working Group 4

5

6 IFIAR Today Main events: Annual plenary meeting (open to all Members) Annual interim meeting (Advisory Council and Working Group Chairs) Annual Inspection Workshop (open to all Members) Keynote presentation; discussion of current financial reporting and audit trends; smaller group discussions on key aspects of audit inspections 6

7 IFIAR Today Officer Led Initiatives: Officers regularly meet with the CEOs of the six largest global audit firm networks Officers regularly meet with key stakeholders to advance audit quality initiatives Officers represent IFIAR at conferences where audit quality is being discussed 7

8 IFIAR Today Working Group Initiatives: Global Audit Quality Working Group meets with the six largest global audit firm networks (two/three times per year) Standards Coordination Working Group meets regularly with IAASB and IESBA Annual Enforcement Workshop 8

9 IFIAR Today Main external IFIAR products: Comment letters to international audit and ethics standard setters Papers, presentations and summaries related to annual panels with investors and audit committee members Annual report on a survey of IFIAR Members inspection findings Annual report including IFIAR activities as well as national and regional developments in Members jurisdictions 9

10 Investor and Other Stakeholders WG Publicly available material from annual panels with investors and audit committee members Summary of panel discussions with investor representatives from Background papers and presentations from 2013 and 2014 panels 2013: how the auditor might best improve audit quality and protect investors; summary of policy developments 2014: Auditor s communications with audit committees See -Other-Stakeholders-Working-Group.aspx 10

11 Standards Coordination WG Forum for IFIAR Members to share views and concerns about pronouncements from the International Auditing and Assurance Standards Board (IAASB) and the International Ethics Standards Board for Accountants (IESBA); Primary focus: sharing views on standards and preparing IFIAR comments on relevant consultations issued by IAASB and IESBA organizing the dialogue between IFIAR and the standard setters providing input for the Monitoring Group's discussion 11

12 IFIAR Comment Letters to Standard Setters To the IAASB December 2013 May 2014 August 2014 October 2014 November 2015 Audit Reporting Exposure Draft The IAASB s Proposed Strategy for and The IAASB s Proposed Work Program for Proposed International Standard on Auditing (ISA) 720 (Revised) - the Auditor s Responsibilities Relating to Other Information Addressing Disclosures in the Audit of Financial Statements Exposure Draft on Reponding to Non-Compliance with Laws and Regulations To the IESBA March 2015 Improving the Structure of the Code of Ethics September 2015 Responding to Non-Compliance with Laws and Regulations 12

13 Some Messages - from Comment Letters Focus on auditing and quality control standards and ethics relevant to audit Specific focus to clarity and enforceability of standards Attention to requirements versus application material in standards Consideration given to the public interest in any standardsetting action undertaken Consideration of audit inspections findings Flexibility for dealing with urgent emerging issues 13

14 Survey of Inspection Findings: Overview In 2015, IFIAR conducted its fourth global survey of inspection findings related to the audits of public companies. The results of that survey were published 3 March IFIAR Members contributed to the 2015 survey (30 in 2014). The survey results generally revealed similarities in the nature and extent of inspection findings compared to 2014 The most frequent areas of findings in each of the survey s categories of inspections findings were generally consistent with the 2014 results. 14

15 Survey: Summary of findings 872 inspected audit engagements of which 376 had deficiencies (43%); 96 inspected major financial institutions of which 49 had deficiencies (51%) For Issuers Internal control testing (23%); Fair value measurements (18%); For Financial Institutions Internal control testing (40%); Audit of allowance for loan losses and loan impairment (51%); Risk assessment (14%) Revenue Recognition (15%) Valuation of investments and securities (27%); Use of Experts and Specialists (26%) 15

16 2015 Survey: Findings from Listed PIE Audit Inspections Inspection Theme Number of Findings (a single PIE may have multiple findings for the same theme) # of Listed PIE Audits Inspected # of Listed PIE Audits with at Least One Finding % of Listed PIE Audits Inspected with at Least One Finding Internal Control Testing % Fair Value Measurement % Risk Assessment % Revenue Recognition % Inventory % Adequacy of Financial Statement Presentation and Disclosure % Group Audits % Substantive Analytical Procedures % Adequacy of Review and Supervision % 16

17 2015 Survey: Findings from Listed PIE Audit Inspections (cont d) Inspection Theme Number of Findings (a single PIE may have multiple findings for the same theme) # of Listed PIE Audits Inspected # of Listed PIE Audits with at Least One Finding % of Listed PIE Audits Inspected with at Least One Finding Fraud Procedures % Audit of Allowance for Loan Losses and Loan Impairments % Engagement Quality Control Review % Use of Experts and Specialists % Related Party Transactions % Audit Report % Audit Committee Communication % Going Concern % TOTAL # of FINDINGS

18 2015 Survey: SIFI Findings Inspection Theme Number of Findings # of SIFI Audits Inspected # of SIFI Audits with at Least One Finding % of SIFI Audits Inspected with at Least One Finding Internal Control Testing % Audit of Allowance for Loan Losses and Impairments % Valuation of Investments and Securities % Use of Experts and Specialists % Risk Assessment % Insufficient Challenge and Testing of Management's Judgments and Assessments % Testing of Customer Deposits and Loans % Audit Methodology including Programs and Tools % Group Audits % Adequacy of Financial Statement Presentation and Disclosures % Substantive Analytical Procedures % Fraud Procedures % Audit Committee Communication % Audit Report % TOTAL # of FINDINGS

19 2015 Survey: Quality Control Findings Audit Firms with at Least One Total Number of Quality Control Finding Findings Inspection Theme # % Engagement Performance % Independence and Ethical Requirements % Human Resources % Monitoring % Client Risk Assessment, Acceptance, and Continuance % Leadership Responsibilities for Quality within the Firm % TOTAL # of FINDINGS

20 The Survey s Connection to IFIAR Work Global Audit Quality Working Group Annual discussion with firms on findings from their internal quality reviews (inspections) Discussions on root cause analysis and remediation Progress will be measured over 4 years againsttargeted reduction Annual Inspection Workshop Survey results discussed Selection of workshop topics informed, in part, by survey results Evaluation of standard-setting projects / focus Standards Coordination Working Group considers the survey results when evaluating a standard-setting project or the standard setters agenda / strategy 20

21 Relevance to Standard setting The circumstances that give rise to inspections findings require careful analysis: the cause underlying an inspection finding may suggest considerations related to standards Consideration whether knowledge from inspection findings have implications relevant to the international auditing standards In particular, attention paid to whether standards are providing sufficient clarity regarding the requirements that the auditor shall comply with and whether standards are driving the auditor to consistent application and the exercise of sufficient professional skepticism 21

22 Relevance to Standard setting Preliminary review performed to identify the international standards that address the topics and audit procedures related to the areas with the greatest level and frequency of observed inspection findings. A summary of related standards is provided in appendix to the survey and does not necessarily imply an IFIAR view about any individual standard Topics on the current IAASB work plan quality control, group audits and professional skepticism audit of accounting estimates and risk assessment and internal control testing, and use of high volumes of data and of dedicated tools (data analytics) Topics not currently on the IAASB work plan materiality, use of experts, responses to assessed risks, and analytical procedures 22

23 IFIAR Outreach IFIAR regularly engages with other regulatory bodies: Monitoring Group (MG) Financial Stability Board (FSB) International Organization of Securities Commissions (IOSCO) Basel Committee on Banking Supervision (BCBS) Public Interest Oversight Board (PIOB) World Bank (WB) European Commission (EC) 23

24 Other Ongoing IFIAR Initiatives Multilateral Memorandum of Understanding for Information Sharing Global Joint Audit Inspection Current Trends in the Audit Industry Thematic Review of Regulators Core Principles Audit regulators should ensure that a risk-based inspections program is in place; and Audit regulators should have a mechanism for reporting inspections findings to the audit firm and ensuring remediation of findings with the audit firm Consideration of a permanent secretariat function for IFIAR 24

25 IFIAR: International Forum of Independent Audit Regulators Marjolein Doblado, IFIAR SCWG Chair International Auditing and Assurance Standards Board Consultative Advisory Group Meeting Paris, 8 March

IFIAR: International Forum of Independent Audit Regulators

IFIAR: International Forum of Independent Audit Regulators Janine van Diggelen, IFIAR Vice Chair Marjolein Doblado, IFIAR SCWG Chair International Auditing and Assurance Standards Board meeting Brussels,

IFIAR: International Forum of Independent Audit Regulators Janine van Diggelen, IFIAR Vice Chair Marjolein Doblado, IFIAR SCWG Chair International Auditing and Assurance Standards Board meeting Brussels,

Engagement Performance 49% Independence and Ethical Requirements 40% Human Resources 31% Monitoring 28%

International Forum of Independent Audit Regulators Report on 2016 Survey of Inspection Findings March 2017 1 Highlights In 2016, IFIAR conducted the fifth annual survey ( Survey ) of its Members findings

International Forum of Independent Audit Regulators Report on 2016 Survey of Inspection Findings March 2017 1 Highlights In 2016, IFIAR conducted the fifth annual survey ( Survey ) of its Members findings

International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014

Executive Summary International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014 This report summarizes the results of the second survey conducted by the

Executive Summary International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014 This report summarizes the results of the second survey conducted by the

IAASB Main Agenda (December 2016) Agenda Item

Agenda Item") Agenda Item 9-A ENHANCING AUDIT QUALITY: PROJECT PROPOSAL FOR THE REVISION OF THE IAASB S INTERNATIONAL STANDARDS RELATING TO QUALITY CONTROL AND GROUP AUDITS This document was developed and approved by

Agenda Item 9-A ENHANCING AUDIT QUALITY: PROJECT PROPOSAL FOR THE REVISION OF THE IAASB S INTERNATIONAL STANDARDS RELATING TO QUALITY CONTROL AND GROUP AUDITS This document was developed and approved by

STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR DECEMBER 31, 2017

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR DECEMBER 31, 2017 The ("PCAOB" or "Board") seeks to

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR DECEMBER 31, 2017 The ("PCAOB" or "Board") seeks to

STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR MARCH 31, 2018

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR MARCH 31, 2018 The ("PCAOB" or "Board") seeks to establish

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR MARCH 31, 2018 The ("PCAOB" or "Board") seeks to establish

STANDARD-SETTING AGENDA OFFICE OF THE CHIEF AUDITOR JUNE 30, 2016

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 http://www.pcaobus.org STANDARD-SETTING AGENDA OFFICE OF THE CHIEF AUDITOR JUNE 30, 2016 The Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 http://www.pcaobus.org STANDARD-SETTING AGENDA OFFICE OF THE CHIEF AUDITOR JUNE 30, 2016 The Public Company Accounting

Key Elements that Create an Environment for Audit Quality. Jon Grant

Framework for Audit Quality Key Elements that Create an Environment for Audit Quality Jon Grant Page 1 Background to the Audit Quality Project For an external audit to fulfill its objective the users of

Framework for Audit Quality Key Elements that Create an Environment for Audit Quality Jon Grant Page 1 Background to the Audit Quality Project For an external audit to fulfill its objective the users of

STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR SEPTEMBER 30, 2017

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR SEPTEMBER 30, 2017 The ("PCAOB" or "Board") seeks to

1666 K Street NW Washington, DC 20006 Office: (202) 207-9100 Fax: (202) 862-8430 www.pcaobus.org STANDARD-SETTING UPDATE OFFICE OF THE CHIEF AUDITOR SEPTEMBER 30, 2017 The ("PCAOB" or "Board") seeks to

We suggest the Consultative Document consider a two prong approach which:

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London, SE1 7EU Tel: +44 (0)207 980 0004 Fax: +44 (0)207 980 0275 www.ey.com 21 June 2013 Secretariat of the Basel Committee on Banking Supervision

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London, SE1 7EU Tel: +44 (0)207 980 0004 Fax: +44 (0)207 980 0275 www.ey.com 21 June 2013 Secretariat of the Basel Committee on Banking Supervision

Basel Committee on Banking Supervision. Consultative Document. External audits of banks. Issued for comment by 21 June 2013

Basel Committee on Banking Supervision Consultative Document External audits of banks Issued for comment by 21 June 2013 March 2013 This publication is available on the BIS website (www.bis.org). Bank

Basel Committee on Banking Supervision Consultative Document External audits of banks Issued for comment by 21 June 2013 March 2013 This publication is available on the BIS website (www.bis.org). Bank

IAASB Main Agenda (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

Ralf Bose Cief Executive Director, Auditor Oversight Body Germany Chair Committee of European Auditing Oversight Bodies (CEAOB)

") Key International Developments Panel Consistent views and inspection methodologies in the EU with a focus on the financial services area and risks seen by european prudential regulators Ralf Bose Cief

Key International Developments Panel Consistent views and inspection methodologies in the EU with a focus on the financial services area and risks seen by european prudential regulators Ralf Bose Cief

Draft Proposed Strategy for and Work Plan for

Agenda Item 7-A International Auditing and Assurance Standards Board Draft Proposed Strategy for 2020 2023 and Work Plan for 2020 2021 Prepared by: Beverley Bahlmann and Jasper van den Hout (November 2018)

Agenda Item 7-A International Auditing and Assurance Standards Board Draft Proposed Strategy for 2020 2023 and Work Plan for 2020 2021 Prepared by: Beverley Bahlmann and Jasper van den Hout (November 2018)

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate governance

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate governance

IAASB CAG Public Session (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background

A FRAMEWORK FOR AUDIT QUALITY. KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

IAASB Main Agenda (December 2018) Joint Matters Relating to the Quality Management (QM) Projects

Joint Matters Relating to the Quality Management (QM) Projects") Agenda Item 5 Joint Matters Relating to the Quality Management (QM) Projects Objective of Agenda Item The objective of this Agenda Item is to discuss matters related to the projects on proposed ISQM 1

Agenda Item 5 Joint Matters Relating to the Quality Management (QM) Projects Objective of Agenda Item The objective of this Agenda Item is to discuss matters related to the projects on proposed ISQM 1

International Forum of Independent Audit Regulators

Meeting of the International Forum of Independent Audit Regulators, Berlin, April 2011 International Forum of Independent Audit Regulators PRESS RELEASE Meeting highlights IFIAR Members agreed upon a set

Meeting of the International Forum of Independent Audit Regulators, Berlin, April 2011 International Forum of Independent Audit Regulators PRESS RELEASE Meeting highlights IFIAR Members agreed upon a set

December 19, Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB)

") December 19, 2018 Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB) This document is issued by the Interim Nominating Committee. The Interim Nominating Committee

December 19, 2018 Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB) This document is issued by the Interim Nominating Committee. The Interim Nominating Committee

Feedback Statement and Impact Assessment ISA (UK) 540 (Revised December 2018) Auditing Accounting Estimates and Related Disclosures

540 (Revised December 2018) Auditing Accounting Estimates and Related Disclosures") Feedback Statement and Impact Assessment Professional discipline Financial Reporting Council December 2018 Feedback Statement and Impact Assessment ISA (UK) 540 (Revised December 2018) Auditing Accounting

Feedback Statement and Impact Assessment Professional discipline Financial Reporting Council December 2018 Feedback Statement and Impact Assessment ISA (UK) 540 (Revised December 2018) Auditing Accounting

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

The Changing Audit Environment

The Changing Audit Environment Key Note Speech by Prof. Arnold Schilder, Chairman, International Auditing and Assurance Standards Board (IAASB) Presented at the 8th Annual Auditing Conference: Ensuring

The Changing Audit Environment Key Note Speech by Prof. Arnold Schilder, Chairman, International Auditing and Assurance Standards Board (IAASB) Presented at the 8th Annual Auditing Conference: Ensuring

Re: Exploring the Growing Use of Technology in the Audit, with a Focus on Data Analytics

National Association of State Boards of Accountancy 150 Fourth Avenue, North Suite 700 Nashville, TN 37219-2417 Tel 615.880-4201 Fax 615.880.4291 www.nasba.org Data Analytics Working Group International

National Association of State Boards of Accountancy 150 Fourth Avenue, North Suite 700 Nashville, TN 37219-2417 Tel 615.880-4201 Fax 615.880.4291 www.nasba.org Data Analytics Working Group International

Comments to be received by 14 March 2011

January 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL AUDITING AND ASSURANCE STANDARDS BOARD (IAASB) CONSULTATION PAPER

January 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL AUDITING AND ASSURANCE STANDARDS BOARD (IAASB) CONSULTATION PAPER

IAASB Main Agenda (December 2018) Quality Management (QM) Projects International Ethics Standards Board for Accountants (IESBA) Coordination

Quality Management (QM) Projects International Ethics Standards Board for Accountants (IESBA) Coordination") Agenda Item 5 B Quality Management (QM) Projects International Ethics Standards Board for Accountants (IESBA) Coordination Objective of Agenda Item The objective of this Agenda Item is to provide an overview

Agenda Item 5 B Quality Management (QM) Projects International Ethics Standards Board for Accountants (IESBA) Coordination Objective of Agenda Item The objective of this Agenda Item is to provide an overview

June Auditor regulation and oversight plan This report is for:

June 2018 Auditor regulation and oversight plan 2018-2021 This report is for: Auditors People who prepare financial statements Directors of FMC reporting entities. This copyright work is licensed under

June 2018 Auditor regulation and oversight plan 2018-2021 This report is for: Auditors People who prepare financial statements Directors of FMC reporting entities. This copyright work is licensed under

Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB)

") Exposure Draft April October 5, 2011 2018 Comments due: February 29, 2012 Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB) This document is issued by the

Exposure Draft April October 5, 2011 2018 Comments due: February 29, 2012 Call for Applications: Chair of the International Auditing and Assurance Standards Board (IAASB) This document is issued by the

Standard Setting Highlights

Standard Setting Highlights INTOSAI PSC-SC June 2017 James Gunn, Managing Director Professional Standards Common Themes Across the SSBs Strategies: Impactful, Public Interest-Focused, and Future-Oriented

Standard Setting Highlights INTOSAI PSC-SC June 2017 James Gunn, Managing Director Professional Standards Common Themes Across the SSBs Strategies: Impactful, Public Interest-Focused, and Future-Oriented

Audit Oversight Board

Audit Board Conversation with Audit Committees Presentation by Lim Fen Nee Head, Audit Board 16 May 2016 Agenda 1. About the Audit Board 2. Global Developments Independence Technology Impact New Auditors

Audit Board Conversation with Audit Committees Presentation by Lim Fen Nee Head, Audit Board 16 May 2016 Agenda 1. About the Audit Board 2. Global Developments Independence Technology Impact New Auditors

ISA 540 (Revised): Overview of Responses

: Overview of Responses") ISA 540 (Revised): Overview of Responses Rich Sharko, IAASB Member and Chair of the ISA 540 Task Force Marc Pickeur, IAASB Member and Co-Chair of the ISA 540 Task Force IAASB Meeting, New York Agenda Item

ISA 540 (Revised): Overview of Responses Rich Sharko, IAASB Member and Chair of the ISA 540 Task Force Marc Pickeur, IAASB Member and Co-Chair of the ISA 540 Task Force IAASB Meeting, New York Agenda Item

Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits. We have responsibility f

Financial Reporting Council DELOITTE LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits.

Financial Reporting Council DELOITTE LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits.

IESBA Meeting (December 2012) Agenda Item. Matters for Consideration Survey for Strategy and Work Plan

Agenda Item. Matters for Consideration Survey for Strategy and Work Plan") Agenda Item 6-A Matters for Consideration Survey for 2014-2016 Strategy and Work Plan Background 1. In accordance with IFAC s due process and working procedures for its Public Interest Activity Committees

Agenda Item 6-A Matters for Consideration Survey for 2014-2016 Strategy and Work Plan Background 1. In accordance with IFAC s due process and working procedures for its Public Interest Activity Committees

Navigating your auditor reporting journey. Forging your own path in a world of change

Navigating your auditor reporting journey Forging your own path in a world of change In this publication, we outline how the changes to auditor reporting can improve the information provided to you as

Navigating your auditor reporting journey Forging your own path in a world of change In this publication, we outline how the changes to auditor reporting can improve the information provided to you as

Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised)

") IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

DFSA S AUDIT MONITORING PROGRAMME. Public Report 2014

DFSA S AUDIT MONITORING PROGRAMME Public Report 0 Issued March 05 Contents. Foreword. About this Report 7. Dubai Financial Services Authority 8. Key focus areas 9. Audit evidence and professional scepticism

DFSA S AUDIT MONITORING PROGRAMME Public Report 0 Issued March 05 Contents. Foreword. About this Report 7. Dubai Financial Services Authority 8. Key focus areas 9. Audit evidence and professional scepticism

International Standards on Auditing: Taking ISAs into the National Context

International Standards on Auditing: Taking ISAs into the National Context Prof. Arnold Schilder, IAASB Chairman World Bank REPARIS Conference Amsterdam April 5, 2011 IAASB s Role, Objectives and Structure

International Standards on Auditing: Taking ISAs into the National Context Prof. Arnold Schilder, IAASB Chairman World Bank REPARIS Conference Amsterdam April 5, 2011 IAASB s Role, Objectives and Structure

AN UPDATE ON THE PROJECT AND INITIAL THINKING ON THE AUDITING CHALLENGES ARISING FROM THE ADOPTION OF EXPECTED CREDIT LOSS MODELS

THE IAASB S PROJECT TO REVISE ISA 540 March 2016 AN UPDATE ON THE PROJECT AND INITIAL THINKING ON THE AUDITING CHALLENGES ARISING FROM THE ADOPTION OF EXPECTED CREDIT LOSS MODELS This publication has been

THE IAASB S PROJECT TO REVISE ISA 540 March 2016 AN UPDATE ON THE PROJECT AND INITIAL THINKING ON THE AUDITING CHALLENGES ARISING FROM THE ADOPTION OF EXPECTED CREDIT LOSS MODELS This publication has been

IOSCO Comments on SWP Consultation Paper (CP) and Planning Committee (PC) Responses and Recommendations

and Planning Committee (PC) Responses and Recommendations") Agenda Item 3-C IOSCO Comments on SWP Consultation Paper (CP) and Planning Committee (PC) Responses and Recommendations Focus of the Board Accountants have a duty to act with integrity, objectivity, and

Agenda Item 3-C IOSCO Comments on SWP Consultation Paper (CP) and Planning Committee (PC) Responses and Recommendations Focus of the Board Accountants have a duty to act with integrity, objectivity, and

Auditor regulation and oversight plan June For the three years ending 30 June 2018

Auditor regulation and oversight plan June 2015 For the three years ending 30 June 2018 This copyright work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. You are free to copy,

Auditor regulation and oversight plan June 2015 For the three years ending 30 June 2018 This copyright work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. You are free to copy,

The IAASB s Proposed Strategy for

IFAC Board Consultation Paper December 2013 Comments due: April 4, 2014 The IAASB s Proposed Strategy for 2015 2019 The IAASB s Proposed Work Program for 2015 2016 REQUEST FOR COMMENTS This Consultation

IFAC Board Consultation Paper December 2013 Comments due: April 4, 2014 The IAASB s Proposed Strategy for 2015 2019 The IAASB s Proposed Work Program for 2015 2016 REQUEST FOR COMMENTS This Consultation

IAASB Main Agenda (September 2017)

") Agenda Item 3 A Quality Management (Firm Level): Proposed Exposure Draft of International Standard on Quality Control (ISQC) 2 Engagement Quality Control (EQC) Reviews Objective of the IAASB Discussion

Agenda Item 3 A Quality Management (Firm Level): Proposed Exposure Draft of International Standard on Quality Control (ISQC) 2 Engagement Quality Control (EQC) Reviews Objective of the IAASB Discussion

Monitoring Group Proposals to Strengthen the Governance and Oversight of Audit-related Standard Setting in the Public Interest

February 8, 2018 The Monitoring Group c/o International Organization of Securities Commissions Calle Oquendo 12 28006 Madrid Spain By e-mail: MG2017consultation@iosco.org Dear Sirs Monitoring Group Proposals

February 8, 2018 The Monitoring Group c/o International Organization of Securities Commissions Calle Oquendo 12 28006 Madrid Spain By e-mail: MG2017consultation@iosco.org Dear Sirs Monitoring Group Proposals

Agreed-Upon Procedures. Ron Salole, IAASB Member and Working Group Chair IAASB Consultative Advisory Group Meeting September 11, 2017 Agenda Item F

Agreed-Upon Procedures Ron Salole, IAASB Member and Working Group Chair IAASB Consultative Advisory Group Meeting September 11, 2017 Agenda Item F Presentation outline Introduction Public interest Discussion

Agreed-Upon Procedures Ron Salole, IAASB Member and Working Group Chair IAASB Consultative Advisory Group Meeting September 11, 2017 Agenda Item F Presentation outline Introduction Public interest Discussion

ISRS 4410 (Revised), Compilation Engagements

, Compilation Engagements") International Auditing and Assurance Standards Board Exposure Draft October 2010 Comments requested by March 31, 2011 Proposed International Standard on Related Services ISRS 4410 (Revised), Compilation

International Auditing and Assurance Standards Board Exposure Draft October 2010 Comments requested by March 31, 2011 Proposed International Standard on Related Services ISRS 4410 (Revised), Compilation

QUALITY CONTROL: ENGAGEMENT QUALITY CONTROL REVIEW ISSUES AND WORKING GROUP VIEWS

Agenda Item 5 B QUALITY CONTROL: ENGAGEMENT QUALITY CONTROL REVIEW ISSUES AND WORKING GROUP VIEWS Objective of the IAASB discussion The objective of this Agenda Item is to obtain the IAASB s input on certain

Agenda Item 5 B QUALITY CONTROL: ENGAGEMENT QUALITY CONTROL REVIEW ISSUES AND WORKING GROUP VIEWS Objective of the IAASB discussion The objective of this Agenda Item is to obtain the IAASB s input on certain

Chapter 2. The CPA Profession

Chapter 2 The CPA Profession Review Questions 2-1 The four major services that CPAs provide are: 1. Audit and assurance services Assurance services are independent professional services that improve the

Chapter 2 The CPA Profession Review Questions 2-1 The four major services that CPAs provide are: 1. Audit and assurance services Assurance services are independent professional services that improve the

2. The auditors' report on a corporation's financial statements usually is addressed to the president of the company.

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Quality Control Issues and Working Group Recommendations

Agenda Item 12-A Quality Control Issues and Working Group Recommendations Objectives of the Discussion The objective of the discussion is to: Inform the Board on alternative internal control and risk management

Agenda Item 12-A Quality Control Issues and Working Group Recommendations Objectives of the Discussion The objective of the discussion is to: Inform the Board on alternative internal control and risk management

Work Plan for : Enhancing Audit Quality

The IAASB s Work Plan for 2017 2018 February 2017 International Auditing and Assurance Standards Board Work Plan for 2017 2018: Enhancing Audit Quality About the IAASB This document was developed and approved

The IAASB s Work Plan for 2017 2018 February 2017 International Auditing and Assurance Standards Board Work Plan for 2017 2018: Enhancing Audit Quality About the IAASB This document was developed and approved

Proposed Strategy for

International Auditing and Assurance Standards Board Consultation Paper October 2007 Proposed Strategy for 2009-2011 REQUEST FOR COMMENTS The International Auditing and Assurance Standards Board (IAASB),

International Auditing and Assurance Standards Board Consultation Paper October 2007 Proposed Strategy for 2009-2011 REQUEST FOR COMMENTS The International Auditing and Assurance Standards Board (IAASB),

Audit Quality Monitoring Report. 1 July June 2018

Audit Quality Monitoring Report 1 July 2017 30 June 2018 Financial Markets Authority 2017/18 Audit Quality Monitoring Report Purpose Contents Under the Auditor Regulation Act 2011 (the Act) we must carry

Audit Quality Monitoring Report 1 July 2017 30 June 2018 Financial Markets Authority 2017/18 Audit Quality Monitoring Report Purpose Contents Under the Auditor Regulation Act 2011 (the Act) we must carry

) ) ) ) ) ) ) ) ) ) ) ) PROPOSED AUDITING STANDARDS RELATED TO THE AUDITOR'S ASSESSMENT OF AND RESPONSE TO RISK

) ) ) ) ) ) ) ) ) ) ) PROPOSED AUDITING STANDARDS RELATED TO THE AUDITOR'S ASSESSMENT OF AND RESPONSE TO RISK") 1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARDS RELATED TO THE AUDITOR'S ASSESSMENT OF AND RESPONSE TO RISK AND

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARDS RELATED TO THE AUDITOR'S ASSESSMENT OF AND RESPONSE TO RISK AND

Overview of Auditing Standards Recap and Update 6 July 2011

Overview of Auditing Standards Recap and Update 6 July 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1

Overview of Auditing Standards Recap and Update 6 July 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1

2-2 The major characteristics of CPA firms that permit them to fulfill their social function competently and independently are:

Link full download Solution Manual : http://testbankair.com/download/solution-manual-forauditing-and-assurance-services-16th-edition-by-arens-elder-beasley-and-hogan Link full download test bank: http://testbankair.com/download/test-bank-for-auditing-andassurance-services-16th-edition-by-arens-elder-beasley-and-hogan/

Link full download Solution Manual : http://testbankair.com/download/solution-manual-forauditing-and-assurance-services-16th-edition-by-arens-elder-beasley-and-hogan Link full download test bank: http://testbankair.com/download/test-bank-for-auditing-andassurance-services-16th-edition-by-arens-elder-beasley-and-hogan/

Inform Representatives about the activities of the Quality Control Task Force (QCTF) since the March 2018 IAASB CAG meeting.

since the March 2018 IAASB CAG meeting.") Meeting: IAASB Consultative Advisory Group (CAG) Meeting Location: New York, United States of America Meeting Date: September 11 12, 2018 Objectives of Agenda Item Proposed ISQC 1 (Revised) 1 Report Back

Meeting: IAASB Consultative Advisory Group (CAG) Meeting Location: New York, United States of America Meeting Date: September 11 12, 2018 Objectives of Agenda Item Proposed ISQC 1 (Revised) 1 Report Back

Auditing Accounting Estimates and Fair Value Measurements: Project Update and Discussion. Barbara Vanich Associate Chief Auditor

Auditing Accounting Estimates and Fair Value Measurements: Project Update and Discussion Barbara Vanich Associate Chief Auditor Disclaimer The views expressed by each of the presenters are their own personal

Auditing Accounting Estimates and Fair Value Measurements: Project Update and Discussion Barbara Vanich Associate Chief Auditor Disclaimer The views expressed by each of the presenters are their own personal

Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits. We have responsibility f

Financial Reporting Council ERNST & YOUNG LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits.

Financial Reporting Council ERNST & YOUNG LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits.

Prototype to Demonstrate the Functionality of the Maintenance Framework.

Prototype to Demonstrate the Functionality of the Maintenance Framework. The purpose of the following table is to provide an illustrative example to show how the proposed framework can be used to maintain

Prototype to Demonstrate the Functionality of the Maintenance Framework. The purpose of the following table is to provide an illustrative example to show how the proposed framework can be used to maintain

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

IAASB Main Agenda (June 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (June 2004) Page 2004 1009 Agenda Item 7-B INTERNATIONAL STANDARD ON AUDITING 300 (MARK-UP) PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-5 Preliminary

IAASB Main Agenda (June 2004) Page 2004 1009 Agenda Item 7-B INTERNATIONAL STANDARD ON AUDITING 300 (MARK-UP) PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-5 Preliminary

Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits. We have responsibility f

Financial Reporting Council PwC LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits. We have

Financial Reporting Council PwC LLP AUDIT QUALITY INSPECTION JUNE 2018 Our mission is to promote transparency and integrity in business. We monitor the quality of UK Public Interest Entity audits. We have

Prototype to Demonstrate the Functionality of the Maintenance Framework.

Prototype to Demonstrate the Functionality of the Maintenance Framework. The purpose of the following table is to provide an illustrative example to show how the proposed framework can be used to maintain

Prototype to Demonstrate the Functionality of the Maintenance Framework. The purpose of the following table is to provide an illustrative example to show how the proposed framework can be used to maintain

Compilation Engagements

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

Financial Reporting Council GRANT THORNTON UK LLP AUDIT QUALITY INSPECTION

Financial Reporting Council GRANT THORNTON UK LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate

Financial Reporting Council GRANT THORNTON UK LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate

and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

Key areas of concern in the current standard-setting model

Section 1 Key areas of concern in the current standard-setting model 1. Do you agree with the key areas of concern identified with the current standard setting model? We do not agree that there is no evidence

Section 1 Key areas of concern in the current standard-setting model 1. Do you agree with the key areas of concern identified with the current standard setting model? We do not agree that there is no evidence

Agenda Item 6-2. Committee: International Accounting Education Standards Board Meeting

Agenda Item 6-2 Committee: International Accounting Education Standards Board Meeting IFAC Headquarters, New York, USA Location: Meeting Date: June 17-19, 2013 SUBJECT: Revision of IES 8 -Task Force s

Agenda Item 6-2 Committee: International Accounting Education Standards Board Meeting IFAC Headquarters, New York, USA Location: Meeting Date: June 17-19, 2013 SUBJECT: Revision of IES 8 -Task Force s

International Standard on Auditing (UK) 220 (Revised June 2016)

220 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Audit monitoring visits cycle 1 / cycle 2 BUSINESS WITH CONFIDENCE

Audit monitoring visits cycle 1 / cycle 2 Outline Recap on Cycle 1 monitoring activities and findings 2016 support between formal cycles Cycle 2 visit programme Cycle 2 what to expect Recap on cycle 1

Audit monitoring visits cycle 1 / cycle 2 Outline Recap on Cycle 1 monitoring activities and findings 2016 support between formal cycles Cycle 2 visit programme Cycle 2 what to expect Recap on cycle 1

IAASB Main Agenda (December 2018) Agenda Item EXPOSURE DRAFT OF PROPOSED INTERNATIONAL STANDARD ON QUALITY MANAGEMENT 2 ENGAGEMENT QUALITY REVIEWS

Agenda Item EXPOSURE DRAFT OF PROPOSED INTERNATIONAL STANDARD ON QUALITY MANAGEMENT 2 ENGAGEMENT QUALITY REVIEWS") IAASB Main Agenda (December 2018) Agenda Item 4-A EXPOSURE DRAFT OF PROPOSED INTERNATIONAL STANDARD ON QUALITY MANAGEMENT 2 ENGAGEMENT QUALITY REVIEWS [CONTENTS PAGE TO BE INSERTED] (CLEAN) Proposed International

IAASB Main Agenda (December 2018) Agenda Item 4-A EXPOSURE DRAFT OF PROPOSED INTERNATIONAL STANDARD ON QUALITY MANAGEMENT 2 ENGAGEMENT QUALITY REVIEWS [CONTENTS PAGE TO BE INSERTED] (CLEAN) Proposed International

Overview of Comments Received on Recent Standard Setting Proposals

Overview of Comments Received on Recent Standard Setting Proposals Keith Wilson Deputy Chief Auditor Barbara Vanich Associate Chief Auditor Lisa Calandriello Associate Chief Auditor Dima Andriyenko Associate

Overview of Comments Received on Recent Standard Setting Proposals Keith Wilson Deputy Chief Auditor Barbara Vanich Associate Chief Auditor Lisa Calandriello Associate Chief Auditor Dima Andriyenko Associate

Basis for Conclusions: ISA 501 (Redrafted), Audit Evidence Specific Considerations for Selected Items

, Audit Evidence Specific Considerations for Selected Items") Basis for Conclusions: ISA 501 (Redrafted), Audit Evidence Specific Considerations for Selected Items Prepared by the Staff of the International Auditing and Assurance Standards Board December 2008 , AUDIT

Basis for Conclusions: ISA 501 (Redrafted), Audit Evidence Specific Considerations for Selected Items Prepared by the Staff of the International Auditing and Assurance Standards Board December 2008 , AUDIT

CGIAR System Management Board Audit and Risk Committee Terms of Reference

Approved (Decision SMB/M4/DP4): 17 December 2016 CGIAR System Management Board Audit and Risk Committee Terms of Reference A. Purpose 1. The purpose of the Audit and Risk Committee ( ARC ) of the System

Approved (Decision SMB/M4/DP4): 17 December 2016 CGIAR System Management Board Audit and Risk Committee Terms of Reference A. Purpose 1. The purpose of the Audit and Risk Committee ( ARC ) of the System

Basis for Conclusions: International Auditing and Assurance Standards Board Strategy and Work Program,

Basis for Conclusions: International Auditing and Assurance Standards Board Strategy and Work Program, 2009-2011 Prepared by the Staff of the International Auditing and Assurance Standards Board July 2008

Basis for Conclusions: International Auditing and Assurance Standards Board Strategy and Work Program, 2009-2011 Prepared by the Staff of the International Auditing and Assurance Standards Board July 2008

International Standard on Auditing (Ireland) 300. Planning an Audit of Financial Statements

300. Planning an Audit of Financial Statements") International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD INTERIM TERMS OF REFERENCE

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD INTERIM TERMS OF REFERENCE (Approved November 2004) CONTENTS Paragraph Purpose of the International Public Sector Accounting Standards Board... 1

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS BOARD INTERIM TERMS OF REFERENCE (Approved November 2004) CONTENTS Paragraph Purpose of the International Public Sector Accounting Standards Board... 1

Audrey A. Gramling Kennesaw State University. Larry E. Rittenberg. University of Wisconsin Madison. Karla M. Johnstone

Auditin Audrey A. Gramling Kennesaw State University Larry E. Rittenberg University of Wisconsin Madison Karla M. Johnstone University of Wisconsin Madison /% SOUTH-WESTERN *% CENGAGE Learning- Australia

Auditin Audrey A. Gramling Kennesaw State University Larry E. Rittenberg University of Wisconsin Madison Karla M. Johnstone University of Wisconsin Madison /% SOUTH-WESTERN *% CENGAGE Learning- Australia

A Framework for Audit Quality

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London SE1 7EU Tel: +44 [0]20 7980 0000 Fax: +44 [0]20 7980 0275 www.ey.com Mr. James Gunn Technical Director International Auditing and

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London SE1 7EU Tel: +44 [0]20 7980 0000 Fax: +44 [0]20 7980 0275 www.ey.com Mr. James Gunn Technical Director International Auditing and

Exposure Draft: Proposed International Standard on Auditing 540 (Revised), Auditing Accounting Estimates and Related Disclosures

, Auditing Accounting Estimates and Related Disclosures") Chairman Restricted Via e-mail Mr Arnold Schilder Chairman International Auditing and Assurance Standards Board 529 Fifth Avenue, 6th Floor New York, New York 100017 United States 1 August 2017 Exposure

Chairman Restricted Via e-mail Mr Arnold Schilder Chairman International Auditing and Assurance Standards Board 529 Fifth Avenue, 6th Floor New York, New York 100017 United States 1 August 2017 Exposure

ISA 315 (Revised) IAASB Meeting Agenda Item 6 A New York, USA December Fiona Campbell, Chair of ISA 315 Task Force

IAASB Meeting Agenda Item 6 A New York, USA December Fiona Campbell, Chair of ISA 315 Task Force") ISA 315 (Revised) IAASB Meeting Agenda Item 6 A New York, USA December 2018 Fiona Campbell, Chair of ISA 315 Task Force ISA 315 (Revised) Exposure Draft Respondents by type Total 68 Member Bodies and Other

ISA 315 (Revised) IAASB Meeting Agenda Item 6 A New York, USA December 2018 Fiona Campbell, Chair of ISA 315 Task Force ISA 315 (Revised) Exposure Draft Respondents by type Total 68 Member Bodies and Other

IOSCO Report on Good Practices for Audit Committees in Supporting Audit Quality

IOSCO Report on Good Practices for Audit Committees in Supporting Audit Quality The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FR01/2019 JANUARY 2019 i The International Organization

IOSCO Report on Good Practices for Audit Committees in Supporting Audit Quality The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FR01/2019 JANUARY 2019 i The International Organization

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

PCAOB Public Company Accounting Oversight Board

PCAOB Public Company Accounting Oversight Board Executive Highlights Annual Report on the Interim Inspection Program This Executive Highlights of the Public Company Accounting Oversight Board's Annual

PCAOB Public Company Accounting Oversight Board Executive Highlights Annual Report on the Interim Inspection Program This Executive Highlights of the Public Company Accounting Oversight Board's Annual

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS") INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

MONITORING GROUP CONSULTATION

MONITORING GROUP CONSULTATION STRENGTHENING THE GOVERNANCE AND OVERSIGHT OF THE INTERNATIONAL AUDIT-RELATED STANDARD-SETTING BOARDS IN THE PUBLIC INTEREST 1 MONITORING GROUP: STRENGTHENING THE GOVERNANCE

MONITORING GROUP CONSULTATION STRENGTHENING THE GOVERNANCE AND OVERSIGHT OF THE INTERNATIONAL AUDIT-RELATED STANDARD-SETTING BOARDS IN THE PUBLIC INTEREST 1 MONITORING GROUP: STRENGTHENING THE GOVERNANCE

Arnold Schilder Chairman International Auditing and Assurance Standards Board 529 Fifth Avenue 6th Floor New York, NY

THE CHAIRPERSON Arnold Schilder Chairman International Auditing and Assurance Standards Board 529 Fifth Avenue 6th Floor New York, NY 100017 EBA/2016/D/695 11 May 2016 Overview of the Invitation to Comment:

THE CHAIRPERSON Arnold Schilder Chairman International Auditing and Assurance Standards Board 529 Fifth Avenue 6th Floor New York, NY 100017 EBA/2016/D/695 11 May 2016 Overview of the Invitation to Comment:

Annual Assessment of the External Auditor

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

IAASB Meeting (December 2018)

") Agenda Item 5 A PROPOSED CONFORMING AMENDMENTS TO THE INTERNATIONAL STANDARDS ON AUDITING (ISAs) ARISING FROM PROPOSED ISQM 1 1 AND ISA 220 (REVISED) 2 Note to IAASB: The extracts below are shown marked

Agenda Item 5 A PROPOSED CONFORMING AMENDMENTS TO THE INTERNATIONAL STANDARDS ON AUDITING (ISAs) ARISING FROM PROPOSED ISQM 1 1 AND ISA 220 (REVISED) 2 Note to IAASB: The extracts below are shown marked

OFFICE OF THE CHIEF AUDITOR STANDARD-SETTING AGENDA MARCH 2012

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org OFFICE OF THE CHIEF AUDITOR STANDARD-SETTING AGENDA MARCH 2012 As part of developing and periodically

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org OFFICE OF THE CHIEF AUDITOR STANDARD-SETTING AGENDA MARCH 2012 As part of developing and periodically

8 February Dear Mr. Everts,

8 February 2018 Mr Gerben J. Everts Chairman Monitoring Group C/O International Organization of Securities Commissions Calle Oquendo 12 28006 Madrid Spain By email: MG2017consultation@iosco.org Dear Mr.

8 February 2018 Mr Gerben J. Everts Chairman Monitoring Group C/O International Organization of Securities Commissions Calle Oquendo 12 28006 Madrid Spain By email: MG2017consultation@iosco.org Dear Mr.

Proposed International Standard on Auditing 315 (Revised)

") Exposure Draft July 2018 Comments due: November 2, 2018 International Standard on Auditing Proposed International Standard on Auditing 315 (Revised) Identifying and Assessing the Risks of Material Misstatement

Exposure Draft July 2018 Comments due: November 2, 2018 International Standard on Auditing Proposed International Standard on Auditing 315 (Revised) Identifying and Assessing the Risks of Material Misstatement

Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

Audit Risk. Exposure Draft. IFAC International Auditing and Assurance Standards Board. October Response Due Date March 31, 2003

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

the truth and fairness of the view given by the financial statements of the Company

1 Purpose The key role of the Altium Limited Audit Committee is to assist The Board of Directors (The Board) to fulfil its corporate governance and overseeing responsibilities in relation to Altium Limited

1 Purpose The key role of the Altium Limited Audit Committee is to assist The Board of Directors (The Board) to fulfil its corporate governance and overseeing responsibilities in relation to Altium Limited

IFAC S SUPPORT FOR A SINGLE SET OF AUDITING STANDARDS: AUDITS OF SMALL- AND MEDIUM-SIZED ENTITIES

IFAC POLICY POSITION 2 March 2012 IFAC S SUPPORT FOR A SINGLE SET OF AUDITING STANDARDS: AUDITS OF SMALL- AND MEDIUM-SIZED ENTITIES It is in the public interest that users of audited financial statements

IFAC POLICY POSITION 2 March 2012 IFAC S SUPPORT FOR A SINGLE SET OF AUDITING STANDARDS: AUDITS OF SMALL- AND MEDIUM-SIZED ENTITIES It is in the public interest that users of audited financial statements

February 9, The Monitoring Group c/o IOSCO Calle Oquendo Madrid Spain. By to:

Auditing and Assurance Standards Board 277 Wellington Street West, Toronto, ON Canada M5V 3H2 T. 416 204.3240 F. 416 204.3412 www.frascanada.ca February 9, 2018 The Monitoring Group c/o IOSCO Calle Oquendo

Auditing and Assurance Standards Board 277 Wellington Street West, Toronto, ON Canada M5V 3H2 T. 416 204.3240 F. 416 204.3412 www.frascanada.ca February 9, 2018 The Monitoring Group c/o IOSCO Calle Oquendo