Port Everglades Master/Vision Plan Update

|

|

|

- Vivien Craig

- 5 years ago

- Views:

Transcription

1 Port Everglades Master/Vision Plan Update Container and Non-Containerized Cargo Charrette Meeting June 18,

2 The purpose of this presentation was to review the progress of the update to the 2006 Master/Vision Plan with the audience. The information contained herein is in draft form and was accompanied by a verbal description during the presentation and has not been approved by Broward County. Since the following slides are in draft form the information thereon is subject to change. 2

3 Progress to Date Working on Phase I Update Updated Element 1: Existing Conditions Assessment - Discussed at Tenant/Stakeholder Meeting Updating Element 2: Market Assessment Updating Element 3: Plan Development 3

4 Updating Element 2: Market Assessment Bermello, Ajamil & Partners - Cruise Martin & Associates - Containerized Cargo Purvin & Gertz - Liquid Bulk Sclar & Associates - Non-Containerized Cargo (For 20-year Design Horizon; 2009 to 2029) 4

5 Containerized Cargo Presented by John Martin/Jeff Sweeney Martin Associates 5

6 Study Progress Overview of containerized trade US Southeast Review of PEV Performance (6-month FY09) Discussion of Current Port Shares to Key Importer/Exporter Locations By Trade Route Competitive Market Assessment Truck Hinterland Intermodal Assessment By Trade Route Preliminary Draft Forecast Low Baseline Scenario Potential High Scenario 6

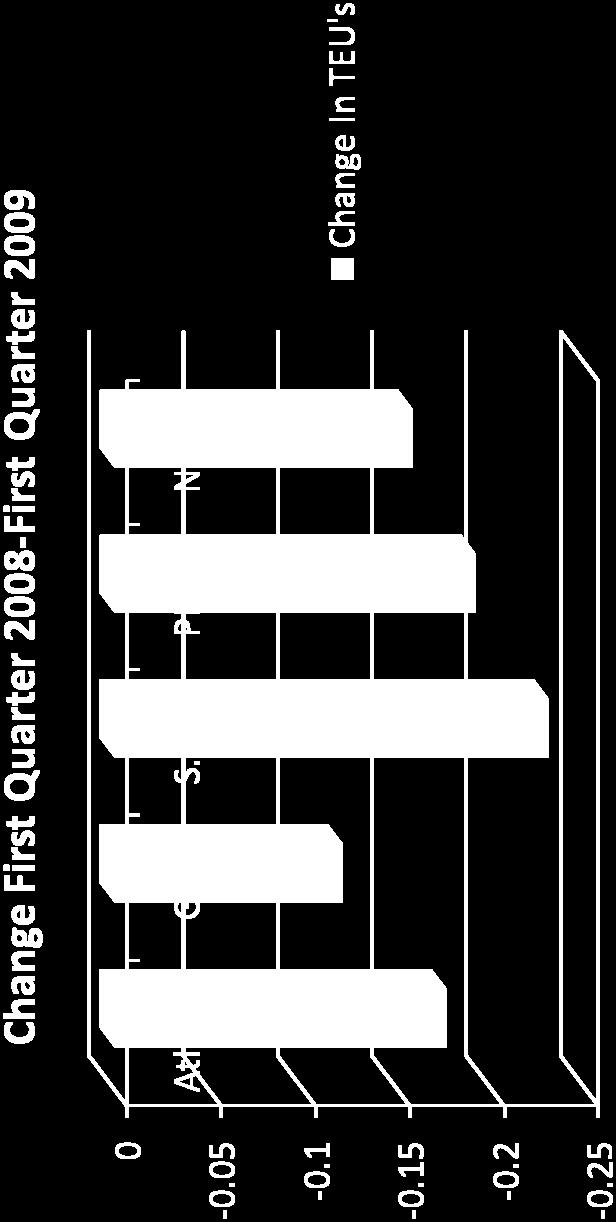

7 Trade Growth has Suffered Due to Economic Conditions Source: AAPA 7 7

8 West Coast Ports are Experiencing a Greater Decline in Containerized Trade Source: AAPA 8

9 China Has Been the Growing Source of Imported Containerized Tonnage Source: US Bureau of Census 9 9

10 However, Asian Supply Sources are Shifting Source: US Bureau of Census 10

11 TEU Growth at South Atlantic Ports has been Driven Primarily by Savannah Source: AAPA 11 11

12 Imported Asian Container Tonnage South Atlantic Port Range Savannah continues to increase market share in the South Atlantic Source: US Bureau of Census 12 12

13 Imported Asian Container Tonnage Florida Port Everglades tonnage has decreased since 2006 Source: US Bureau of Census 13 13

14 Through Six Months of FY09, Port Everglades TEUs are off by 15% Key losses include APM/Universal and APL service to Miami Source: Port Everglades 14

15 Key Changes in PEV Tenant Base and Throughput from 2006 Universal APM - ceased service (Feb 08) In 2006, approximately 100,000 TEU PET - lost APL service to Miami (Jan 09) In 2006, APL approximately 50,000 TEU FIT - new services in place In 2006, FIT handled 76,000 TEU; 2009 estimate 125, ,000 TEU 15

16 Current South Atlantic and Florida Market Assessment 16

17 Asian Imports Port Share by Importer Location Savannah controls the South Atlantic market Charleston offers some competition in South Carolina market 17

18 Asian Exports Port Share by Exporter Location Savannah controls into Northern Florida Miami and Port Everglades presence is in the South Florida market consolidation activity 18

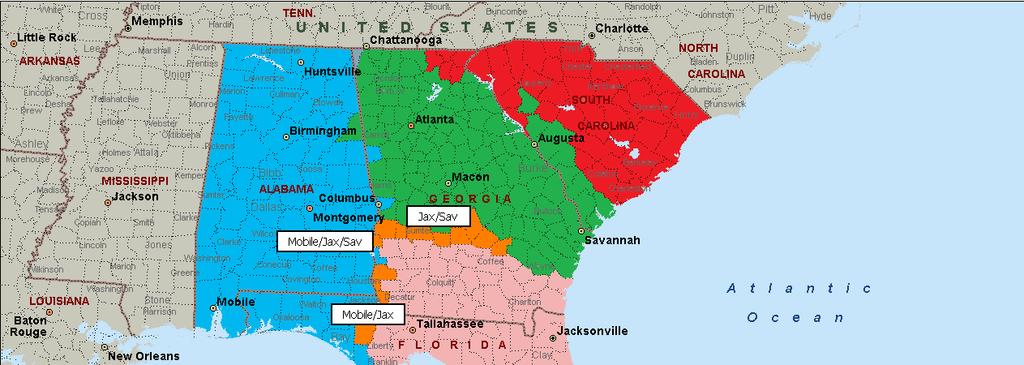

19 Northern European Imports Port Share by Importer Location Charleston controls key markets South Florida imports move via Savannah and Miami 19

20 Northern European Exports Port Share by Exporter Location Charleston and Savannah serve into Northern Florida Miami controls South Florida 20

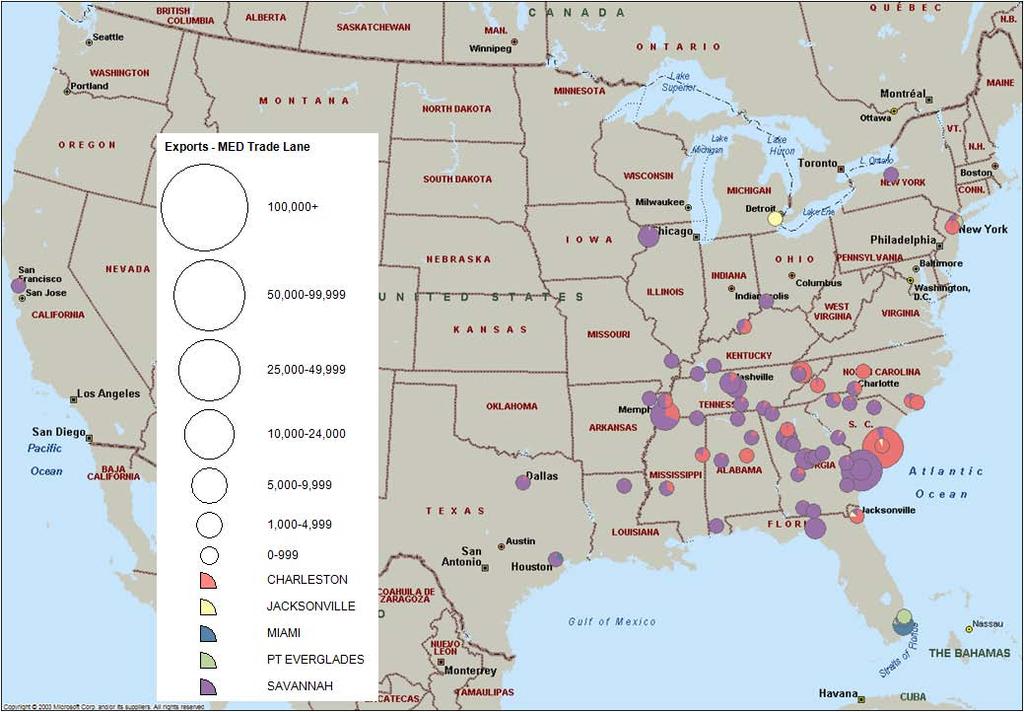

21 Mediterranean Imports Port Share by Importer Location 21

22 Mediterranean Exports Port Share by Exporter Location 22

23 Middle Eastern Imports Port Share by Importer Location 23

24 Middle Eastern Exports Port Share by Exporter Location 24

25 Caribbean Imports Port Share by Importer Location 25

26 Caribbean Exports Port Share by Exporter Location Jacksonville controls into Central Florida Miami and Port Everglades compete for consolidated cargo in South Florida 26

27 Central American Imports Port Share by Importer Location Port Everglades penetrates into the Midwest and Northeast 27

28 Central American Exports Port Share by Exporter Location Miami and Port Everglades compete for market share in South Florida as well as the Midwest and Mid Atlantic regions 28

29 East Coast South American Imports Port Share by Importer Location 29

30 East Coast South American Exports Port Share by Exporter Location 30

31 West Coast South America Imports Port Share by Importer Location 31

32 West Coast South American Exports Port Share by Exporter Location 32

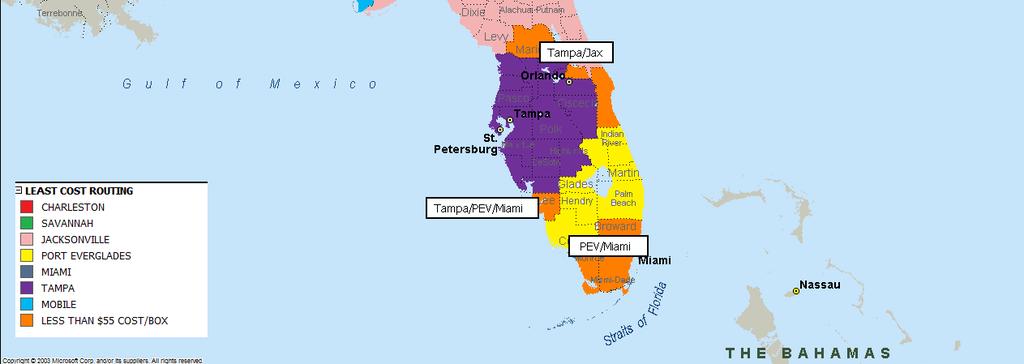

33 Estimate of Potential Port Everglades Market 33

34 Cost Competitive Truck Hinterland FL, GA, SC and AL 34

35 TEU Consumption by County -FL,GA, SC and AL Total consumption for 4 state area inbound outbound and empty containers is about 5.7 million TEUs 35

36 TEU Consumption by County within PEV Truck Hinterland PEV is competitive to serve market of 390,000 loaded inbound TEU; When factoring in export loads and empties, total PEV truck market is 995,000 TEU 36

37 Vessel Costs and Total Logistics Costs to Serve Key Intermodal Hubs Analysis to show potential market beyond South/Central Florida Market penetration into Atlanta intermodal hub is key Also Memphis St. Louis Chicago Martin Associates least cost routing methodology Martin Associates Vessel Cost Model Intermodal rates obtained from 1% Waybill Sample (STB) and Carriers Intermodal Departments Drayage cost applied for ports without on-dock ICTF Assume PEV will build near-dock ICTF 37

38 Vessel Costs and Total Logistics Costs to Serve Key Intermodal Hubs Analysis completed for each trade route Analysis based on fully-laden first port of call Analysis completed for pre and post Panama Canal expansion eras Pre expansion assumes vessel sizes: 4,800 TEU vessel Miami, PEV, Jacksonville, Tampa Savannah, Charleston, Houston, New York, Norfolk, Baltimore 6,000 TEU vessel for LA/LB, Oakland and Seattle Post expansion assumes vessel sizes: 4,800 TEU Jacksonville and Port Everglades 7,000 TEU Savannah, New York, Norfolk, Baltimore 7,000 TEU Miami and Houston 8,500 TEU LA/LB, Oakland and Seattle 38

39 HONG KONG PRE EXPANSION Jacksonville holds advantage into Atlanta 39

40 HONG KONG POST EXPANSION With 7,000 TEU Savannah Captures Atlanta Market West Coast ports continue to dominate the other Midwest intermodal hubs 40

41 Summary of Hong Kong Routings HONG KONG PRE Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $3,161 $3,772 $3,577 $4,556 $3,854 $3, New York $3,648 $3,003 $3,619 $3,178 $3,544 $4, Norfolk $4,056 $3,133 $4,047 $3,326 $4,293 NA 4800 Jacksonville $3,046 $3,363 $3,220 $3,454 $3,460 $3, Miami $3,198 $3,708 $3,501 $3,657 $6,939 $4, Port Everglades $3,115 $3,625 $3,418 $3,574 $6,856 $4, Houston $3,597 $3,374 $3,041 $2,941 $3,105 $2, Los Angeles $3,256 $2,695 $2,589 $2,549 $2,551 $2, Oakland $3,450 $2,723 $2,617 $2,577 $2,579 $2, Seattle/Tacoma $4,866 $2,418 $2,711 $2,497 $2,453 $2,722 PRE Savannah Miami differential $38 ($64) ($77) ($899) $3,086 $633 POST Atlanta Chicago Memphis St. Louis KC DFW 7000 Savannah $2,424 $3,035 $2,840 $3,819 $3,117 $3, New York $2,888 $2,243 $2,859 $2,418 $2,784 $3, Norfolk $3,307 $2,384 $3,298 $2,577 $3,544 NA 4800 Jacksonville $3,046 $3,363 $3,220 $3,454 $3,460 $3, Miami $2,482 $2,992 $2,785 $2,941 $6,223 $3, Port Everglades $3,115 $3,625 $3,418 $3,574 $6,856 $4, Houston $2,878 $2,655 $2,322 $2,222 $2,386 $2, Los Angeles $2,797 $2,236 $2,130 $2,090 $2,092 $2, Oakland $3,015 $2,288 $2,182 $2,142 $2,144 $2, Seattle/Tacoma $4,451 $2,003 $2,296 $2,082 $2,038 $2,307 POST Savannah Miami differential $58 ($43) ($55) ($878) $3,106 $654 41

42 SINGAPORE PRE EXPANSION Jacksonville Holds Advantage into Atlanta 42

43 SINGAPORE POST EXPANSION Savannah Cost Effectively Serves Atlanta Houston captures Dallas; competes for Memphis and St Louis 43

44 Summary of Singapore Routings SINGAPORE PRE Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $2,909 $3,520 $3,325 $4,304 $3,602 $3, New York $3,292 $2,647 $3,263 $2,822 $3,188 $4, Norfolk $3,756 $2,833 $3,747 $3,026 $3,993 NA 4800 Jacksonville $2,857 $3,174 $3,031 $3,265 $3,271 $3, Miami $3,067 $3,577 $3,370 $3,526 $6,808 $4, Port Everglades $2,985 $3,495 $3,288 $3,444 $6,726 $4, Houston $3,616 $3,393 $3,060 $2,960 $3,124 $2, Los Angeles $3,488 $2,927 $2,821 $2,781 $2,783 $2, Oakland $3,655 $2,928 $2,822 $2,782 $2,784 $2, Seattle/Tacoma $5,068 $2,620 $2,913 $2,699 $2,655 $2,924 PRE Savannah Miami differential $159 $57 $44 ($778) $3,207 $754 POST Atlanta Chicago Memphis St. Louis KC DFW 6000 Savannah $2,222 $2,833 $2,638 $3,617 $2,915 $2, New York $2,618 $1,973 $2,589 $2,148 $2,514 $3, Norfolk $3,073 $2,150 $3,064 $2,343 $3,310 NA 4800 Jacksonville $2,857 $3,174 $3,031 $3,265 $3,271 $3, Miami $2,358 $2,868 $2,661 $2,817 $6,099 $3, Port Everglades $2,985 $3,495 $3,288 $3,444 $6,726 $4, Houston $2,851 $2,628 $2,295 $2,195 $2,359 $2, Los Angeles $2,922 $2,361 $2,255 $2,215 $2,217 $2, Oakland $3,125 $2,398 $2,292 $2,252 $2,254 $2, Seattle/Tacoma $4,559 $2,111 $2,404 $2,190 $2,146 $2,415 POST Savannah Miami differential $136 $35 $23 ($800) $3,184 $732 44

45 SRI LANKA PRE EXPANSION Jacksonville Competes in Atlanta and Memphis 45

46 SRI LANKA POST EXPANSION Savannah Serves Atlanta Houston strengthens its position in the Midwest 46

47 Summary of Sri Lanka Routings SRI LANKA PRE Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $2,655 $3,266 $3,071 $4,050 $3,348 $3, New York $3,038 $2,393 $3,009 $2,568 $2,934 $3, Norfolk $3,502 $2,579 $3,493 $2,772 $3,739 NA 4800 Jacksonville $2,602 $2,919 $2,776 $3,010 $3,016 $3, Miami $2,813 $3,323 $3,116 $3,272 $6,554 $4, Port Everglades $2,730 $3,240 $3,033 $3,189 $6,471 $4, Houston $3,354 $3,131 $2,798 $2,698 $2,862 $2, Los Angeles $3,735 $3,174 $3,068 $3,028 $3,030 $3, Oakland $3,901 $3,174 $3,068 $3,028 $3,030 $3, Seattle/Tacoma $5,314 $2,866 $3,159 $2,945 $2,901 $3,170 PRE Savannah Miami differential $159 $57 $44 ($778) $3,207 $754 POST Atlanta Chicago Memphis St. Louis KC DFW 6000 Savannah $2,056 $2,667 $2,472 $3,451 $2,050 $2, New York $2,452 $1,807 $2,423 $1,982 $2,348 $3, Norfolk $2,908 $1,985 $2,899 $2,178 $3,145 NA 4800 Jacksonville $2,602 $2,919 $2,776 $3,010 $3,016 $3, Miami $2,193 $2,703 $2,496 $2,652 $5,934 $3, Port Everglades $2,730 $3,240 $3,033 $3,189 $6,471 $4, Houston $2,681 $2,458 $2,125 $2,025 $2,189 $1, Los Angeles $3,054 $2,493 $2,387 $2,347 $2,349 $2, Oakland $3,257 $2,530 $2,424 $2,384 $2,386 $2, Seattle/Tacoma $4,692 $2,244 $2,537 $2,323 $2,279 $2,548 POST Savannah Miami differential $137 $36 $24 ($799) $3,884 $733 47

48 BREMERHAVEN Jacksonville Is Competitive into Atlanta and Memphis 48

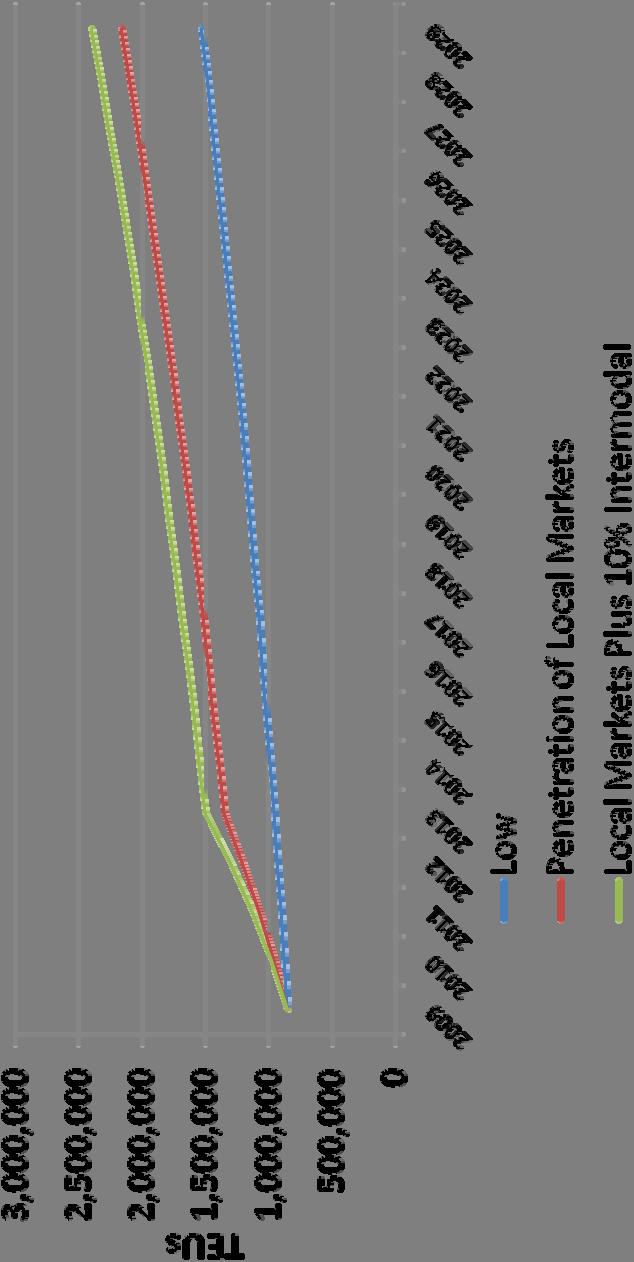

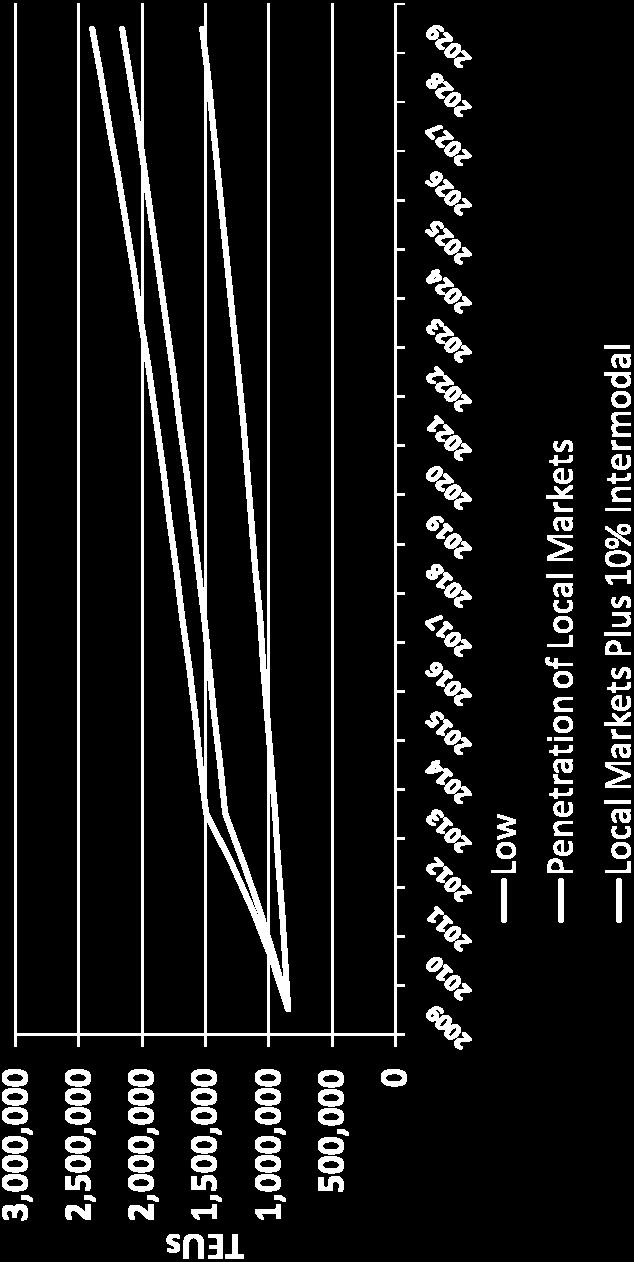

49 Summary of Bremerhaven Routings BREMERHAVEN Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $1,567 $2,178 $1,983 $2,962 $2,260 $2, New York $1,935 $1,290 $1,906 $1,465 $1,831 $2, Norfolk $2,401 $1,478 $2,392 $1,671 $2,638 NA 4800 Jacksonville $1,512 $1,829 $1,686 $1,920 $1,926 $1, Miami $1,729 $2,239 $2,032 $2,188 $5,470 $3, Port Everglades $1,642 $2,152 $1,945 $2,101 $5,383 $2, Houston $2,266 $2,043 $1,710 $1,610 $1,774 $1,555 Savannah Miami differential $163 $61 $48 ($774) $3,211 $758 49

50 ALGECIRAS Jacksonville is Competitive into Atlanta and Memphis 50

51 Summary of Algeciras Routings ALGECIRAS Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $1,488 $2,099 $1,904 $2,883 $2,181 $2, New York $1,871 $1,226 $1,842 $1,401 $1,767 $2, Norfolk $2,336 $1,413 $2,327 $1,606 $2,573 NA 4800 Jacksonville $1,436 $1,753 $1,610 $1,844 $1,850 $1, Miami $1,647 $2,157 $1,950 $2,106 $5,388 $2, Port Everglades $1,764 $2,274 $2,067 $2,223 $5,505 $3, Houston $2,195 $1,972 $1,639 $1,539 $1,703 $1,484 Savannah Miami differential $160 $58 $45 ($777) $3,208 $755 51

52 SANTOS Jacksonville Holds a Strong Position into Atlanta, Memphis and Chicago 52

53 Summary of Santos Routings SANTOS Atlanta Chicago Memphis St. Louis KC DFW 4800 Savannah $1,730 $2,341 $2,146 $3,125 $2,423 $2, New York $2,158 $1,513 $2,129 $1,688 $2,054 $3, Norfolk $2,590 $1,667 $2,581 $1,860 $2,827 NA 4800 Jacksonville $1,629 $1,946 $1,803 $2,037 $2,043 $2, Miami $1,843 $2,353 $2,146 $2,302 $5,584 $3, Port Everglades $1,766 $2,276 $2,069 $2,225 $5,507 $3, Houston $2,320 $2,097 $1,764 $1,664 $1,828 $1,609 Savannah Miami differential $114 $12 ($1) ($823) $3,162 $709 53

54 Logistics Cost Analysis Summary Port Everglades competitive truck hinterland is South Florida Before canal expansion, Jacksonville holds intermodal advantage to Atlanta After canal expansion, Savannah emerges as the key port of entry due to the ability to handle 7,000 and dual on-dock ICTF JAXPORT - Authorization to -45 ft still limits to a fully-laden 4,800 TEU vessel based on design draft Issue at Miami is dray to railhead in Hialeah or Medley ondock rail is questionable Assumption that PEV will have on site ICTF, but needs to be able to accommodate a fully-laden 7,000 TEU vessel to compete with Miami and Savannah for Atlanta market Currently, pilots will only bring in a ship with a draft of -40 ft (-41 ft. on high tide) PEV near-dock ICTF will increase intermodal throughput on baseline operations In post-expansion era, Houston strengthens its position in other Midwest markets such as St. Louis, Memphis, Kansas City 54

55 Potential Market 380,000 estimated inbound consumption market Of this PEV handles about 80,000 boxes based on Piers data -- 21% of local market Assume can get 50% of South Florida Market 150,000 TEU loads Balance outbound loads and exports 150,000 TEU s Total 300,000 TEU loads 400,000 TEU inbound loaded Central Florida market potential Assume 25% market penetration 100,000 TEU inbound loaded Assume 100,00 TEU match outbound load and empty Total potential 200,000 additional TEUs from Central Florida With current 850,000 TEUs - current potential million TEUS If assume 10% intermodal - Total is 1.5 million TEUs in near term 55

56 Projected Container Throughput Projection Assumptions: Low 3% of base cargo, no new market penetration Medium - Capture 50% of local market and 25% of Tampa market by 2014 and grow at 3% thereafter High - Capture local and Tampa market shares and achieve 10% intermodal, and grow 3% thereafter Bt 2029, container throughput projected to range between 1.5 million and 2.4 million TEU s 56

57 Container Projections 57

58 Non-Containerized Cargo (Dry Bulk and Neo Bulk) Presented by Mike Sclar Sclar & Associates 58

59 Housing Starts and Population Growth Dry Bulk and Neo Bulk Commodities Handled in Port Everglades are Primarily Related to Construction Activity in Florida. Near Term Housing Starts are Driven by the Economic Cycle and Long Term Housing Starts are Projected to Increase with Population Growth In 2006 Housing Starts Were Projected to Decline by 35.9% in FY2007 and then Recover in FY2008 and Beyond Housing Starts Fell 39.8% in FY2007 but Subsequently Declined 51.6% in FY2008 and are Projected to Decline by 44.8% in FY2009 and 30.0% in FY Population Projections are 4.0% Below Previous Projections and 2029 Housing Starts are 30.7% Lower than Projected in 2006 The Reduced Housing Start and Population Projections Result in Housing Starts Falling Below the 2006 Peak Throughout the Forecast 59

60 Private Housing Starts (000 s) Private Housing Starts

61 Cement and Aggregates Cement Declined Faster than Housing Starts in 2007 and 2008 Due to Lower Demand Plus New Domestic Cement Capacity Aggregates ( Bauxite, Gypsum and Fero) Fell Moderately in 2007 and Have Recovered and lncreased in 2008 and First Half 2009 As They Are Required for Domestic Cement Production Cement Imports Have Leveled Off in 2009 Despite Continued Declines in Housing Starts Cement Is Not Declining as Much as Housing Starts in 2009 and Will Recover With Housing Start Increases Longer Term, Base Line Cement Imports Will Approach 81.4% of the Peak Levels of 2006 In the Base Line Forecast 61

62 Cement, Gypsum, Bauxite and Fero Base Line Forecast 3,000,000 2,500,000 2,000,000 1,500,000 1,000,000 Cement Gypsum Bauxite Fero 500,

63 Tallow, Steel, Yachts and Xfile Steel declined due to high inventories and falling demand relative to domestic production. Current steel imports are sporadic, but will return to growth with the recovery of the construction market Tallow exports increased in FY2009 and are projected to increase moderately in the future Yachts have shown strong growth but are projected to soften in the near term before returning to moderate long term growth Xfile has included various shipments such as ceramic tiles and more recently bagged cement. Future volumes are projected to show small, sporadic volumes with moderate growth 63

64 Tallow, Steel,Yachts and Xfile 300, , , , ,000 Tallow Steel Yachts Xfile 50,

65 Crushed Rock Crushed Rock Remains an Opportunity For PEV Lake Belt Mining Has Shut Down Under Court Order The Army Corps SEIS Is Under Comment Period New Mining Permits Are Under Consideration New Mining Permits Will Likely Be Granted But Will Be Challenged Lake Belt Mining Will Likely Be Restarted But Will Not Likely Meet Future Demand The ACE SEIS identifies Jacksonville and Tampa as Ports Capable of Increased Crushed Rock Imports. However, PEV is better positioned to serve critical parts of the Florida Market 65

66 Crushed Rock: High Forecast 9,000,000 8,000,000 7,000,000 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000,000 0 High Fcst Rock&Sand

67 Base Line Forecast The Base Line Forecast Results in Total Dry Bulk and Neo Bulk Tons Returning to 92.1% of the Peak 2006 Levels by 2029 The Base Line Forecast Reaches Million Tons in 2029 Compared with Million Tons in 2006 and Million Tons in 2008 The Base Line Forecast Includes a Small Increase in 2009 Holding the Gains in the First Half of FY2009 The Forecast Includes Moderate Recovery Relative to the Recovery in the Housing Market Followed by Longer Term Growth in Line with Population Growth Projections 67

68 Baseline Forecast 3,500,000 3,000,000 2,500,000 2,000,000 1,500,000 1,000, , Total Drybulk Total Neo Bulk Total Tons 68

69 Low Forecast The Low Forecast Reaches Only 61.9% of the 2006 Dry Bulk and Neo Bulk Tons The Low Forecast Includes Lower Volumes in the Second Half of FY2009 followed by more modest growth over the forecast period The Low Forecast reaches Million Tons in 2029 Compared with Million Tons of Dry Bulk and Neo Bulk in 2006 and Million Tons in

70 Low Forecast 3,500,000 3,000,000 2,500,000 2,000,000 1,500,000 1,000, , Total Drybulk Total Neo Bulk Total 70

71 High Forecast The High Forecast Includes Crushed Rock Imports Rising to 4 Million Tons Per Year Over the Forecast Period In Addition, other PEV Dry Bulk and Neo Bulk Commodities are Projected to Increase at Higher Growth Rates Than Projected in the Base Line Case The High Forecast Reaches Million Tons Compared with Million Tons in

72 High Forecast 9,000,000 8,000,000 7,000,000 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000, Total Drybulk Total Neo Bulk Total Tons 72

73 Dry Bulk and Neo Bulk Base, High and Low Forecasts The Base Line Forecast Reaches Million Tons in 2029 or 92.1% of the Million Tons in 2006 The Low Forecast Only Recovers to Million Tons or 61.9% of the 2006 Tons The High Forecast Reaches Million Tons or 229.1% of the 2006 Tons Including 4 Million Tons of Crushed Rock 73

74 Dry Bulk and Neo Bulk Base, High and Low Forecasts 9,000,000 8,000,000 7,000,000 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000, BaseForecast HighForecast LowForecast 74

75 Updating Element 3: Plan Development Updating Project Development: - Southport Berth Expansion - Crushed Rock Import Facility - McIntosh Road Development - ICTF Development - Midport Berth Expansion - Port Wide Traffic and Parking Strategies 75

76 Southport Berth Expansion Location of berth(s) for post-panamax ships to accommodate: Vessel air draft: 180 feet Vessel LOA: 1140 feet Vessel Beam: 140 feet Crane Height, above mean sea level (AMSL): 190 feet Location of berth(s) for panamax ships to accommodate: Existing crane height of 160 feet AMSL Vessel LOA: 900 feet Location of berth(s) for RO/RO and other ships to accommodate: Vessel LOA: 600 feet RORO ramps or ship gear 76

77 TEU Throughput Capacity Based on Yard Acreage 5-YEAR MASTER PLAN 10-YEAR VISION PLAN 20-YEAR VISION PLAN Storage Mode Annual Throughput (TEU/gross ac) Storage Mode Annual Throughput (TEU/gross ac) Storage Mode Annual Throughput (TEU/gross ac) Wheeled (RORO) 5,300 Wheeled (RORO) 5,400 Wheeled (RORO) 5,400 Wheeled (Banana) 10,500 Wheeled (Banana) 10,500 Wheeled (Banana) 10,500 Top-Pick (2-wide) 3,600 Top-Pick (4-wide) 7,600 Top-Pick (4-wide) 7,600 Top-Pick (4-wide) 7,400 RTG 13,900 RTG 15,300 RTG 12,000 77

78 TEU Throughput Capacity Based on Berths 5 YEAR MASTER PLAN 10 YEAR VISION PLAN 20 YEAR VISION PLAN Vessel Loading Mode Annual Berth Throughput (TEU/Berth) Vessel Loading Mode Annual Berth Throughput (TEU/Berth) Vessel Loading Mode Annual Berth Throughput (TEU/Berth) RORO 153,000 RORO 157,000 RORO 163,000 Ship Mounted Crane 95,000 Ship Mounted Crane 133,000 Ship Mounted Crane 169,000 STS Crane (Shared) 113,000 STS Crane (Shared) 144,000 STS Crane (Shared) 174,000 STS Crane 204,000 STS Crane 242,000 STS Crane 315,000 78

79 TEU Throughput Capacity Based on Berths 20 YEAR VISION PLAN Vessel Loading Mode Annual Berth Throughput (TEU/Berth) Number of Berths Available Estimated Annual Throughput RORO 163, ,000 Ship Mounted Crane 169, ,000 STS Crane (Shared) 174, ,000 STS Crane 315, ,260,000 Total 2,266,000 79

80 Lowest Composite Surface/Proposed Conditions Airspace Obstruction Study by Jacobs Consultancy 80

81 81

82 82

83 83

84 84

85 Alternative Enhancement Plan Proposed Removal of 8.68 Acres Proposed Additional /- Acres Existing Manatee Nursery.5 Acre Turning Notch FPL Discharge Canal 4.74 Acres N 85

86 Crushed Rock Import Facility Location and size of ship berth if Turning Notch is expanded Location and size of ship berth if Turning Notch is not expanded 86

87 McIntosh Road Development Incorporation of latest alternative Review of traffic on McIntosh north of the Gate Concept Plan N 87

88 ICTF Development - Definition of throughput capacity and infrastructure requirements 88

89 Midport Berth Expansion Location of berth(s) for panamax ships to accommodate: Existing crane height of 160 feet AMSL Vessel LOA: 900 feet Berth 27 expansion for cruise ships Location of Ferry Vessels? 89

90 90

91 91

92 Port-Wide Projects Incorporation of Locally Preferred Plan for Harbor Dredging and Widening Incorporation of Updates to the Bulkhead Conditions Assessment Location of ID center Traffic and Parking Strategies 92

93 Traffic Projections through the Gates Location: McIntosh Road s/o Eller Drive Start Date 04/01/09 Direction: N Direction: S Combined Total 24-Hour Totals Peak Volume Hour Volume Hour Volume Hour Volume AM AM AM PM PM PM Daily Daily Daily Truck Percentage

94 Parking Projections Parameter Parking Facility Additional Parking Midport Northport T 19 Surface Lot Total Spaces Parking C apacity 1,950 2, ,704 Peak Month Overnight Dec 08 Mar 08 Nov 08 Average peak Month Overnight 1, ,827 High Peak Month Overnight 1,872 1, ,505 CT

95 5-Year Plan to be Updated to Fiscal Years 2010 to Plan to be Updated 95

96 10-Year Vision Plan to be Updated to Fiscal Years 2015 to Plan to be Updated 96

97 20-Year Vision Plan to be Updated to Fiscal Years 2020 to Plan to be Updated 97

98 Next Steps All Business Sectors to meet for Summary of Comments - June 19, 2009; 10:00 am to 12:00 noon; Port Everglades Administration Building; Auditorium 98

Port Everglades Master/Vision Plan Update Stakeholder Meeting. January 28, 2010

Port Everglades Master/Vision Plan Update Stakeholder Meeting January 28, 2010 1 2 Agenda Updated Market Assessments determine. Master Plan Facility/Infrastructure Needs requiring. Berth Expansion into.

Port Everglades Master/Vision Plan Update Stakeholder Meeting January 28, 2010 1 2 Agenda Updated Market Assessments determine. Master Plan Facility/Infrastructure Needs requiring. Berth Expansion into.

Please Do Not Copy or Distribute. Visit: for all the latest updates!

Please Do Not Copy or Distribute Visit: www.nears.org for all the latest updates! The Port of Baltimore The Maryland Port Administration NEARS North East Association of Rail Shippers April 2013 Over 300

Please Do Not Copy or Distribute Visit: www.nears.org for all the latest updates! The Port of Baltimore The Maryland Port Administration NEARS North East Association of Rail Shippers April 2013 Over 300

2018 Port Everglades Master/Vision Plan Update. Environmental Stakeholder Meeting #1 July 19, 2018

2018 Port Everglades Master/Vision Plan Update Environmental Stakeholder Meeting #1 July 19, 2018 1 Overview Introduction Direction and Strategy Work Completed to Date Early Observations Your Input 2 Introduction

2018 Port Everglades Master/Vision Plan Update Environmental Stakeholder Meeting #1 July 19, 2018 1 Overview Introduction Direction and Strategy Work Completed to Date Early Observations Your Input 2 Introduction

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY A PRESENTATION TO: CHANGING TRADE PATTERNS JANUARY 24, 2013 MARTIN ASSOCIATES 941 Wheatland Avenue, Suite 203 Lancaster,

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY A PRESENTATION TO: CHANGING TRADE PATTERNS JANUARY 24, 2013 MARTIN ASSOCIATES 941 Wheatland Avenue, Suite 203 Lancaster,

Port of Los Angeles. America s Port Harbor Transportation Club June 20, 2013 Kathryn McDermott

Port of Los Angeles America s Port 2013 Harbor Transportation Club June 20, 2013 Kathryn McDermott Sea/Tac Battle for Discretionary Cargo Prince Rupert Eastern Canada NY/NJ OAK Norfolk LA/LB Savannah

Port of Los Angeles America s Port 2013 Harbor Transportation Club June 20, 2013 Kathryn McDermott Sea/Tac Battle for Discretionary Cargo Prince Rupert Eastern Canada NY/NJ OAK Norfolk LA/LB Savannah

CONTAINERS AND BEYOND Derrick Smith AAPA Spring Conference - March 18, 2013

CONTAINERS AND BEYOND Derrick Smith AAPA Spring Conference - March 18, 2013 1 What are some of the major trends that are occurring? Increased cargo Significant investments Greater rail usage 2 Many economic

CONTAINERS AND BEYOND Derrick Smith AAPA Spring Conference - March 18, 2013 1 What are some of the major trends that are occurring? Increased cargo Significant investments Greater rail usage 2 Many economic

Terminal Opportunities & Challenges. Peter I. Keller NYK Line April 24, 2006

Terminal Opportunities & Challenges Peter I. Keller NYK Line April 24, 2006 . First, a word about NYK 2 Sea Earth Air Logistics Integrator Hardware / Assets 660 Vessels Sea Software / Services NYK Line

Terminal Opportunities & Challenges Peter I. Keller NYK Line April 24, 2006 . First, a word about NYK 2 Sea Earth Air Logistics Integrator Hardware / Assets 660 Vessels Sea Software / Services NYK Line

PORT OF SAVANNAH. Garden City Terminal: The Southeast Gateway for the U.S.

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. GEORGIA PORTS AUTHORITY MORE DEEPWATER & INLAND TERMINAL OPTIONS Chatsworth Garden City Terminal Ocean Terminal Appalachian Regional

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. GEORGIA PORTS AUTHORITY MORE DEEPWATER & INLAND TERMINAL OPTIONS Chatsworth Garden City Terminal Ocean Terminal Appalachian Regional

AMERICAN ASSOCIATION OF PORT AUTHORITES JUNE 5, 2012 MARTIN ASSOCIATES PREPARED FOR:

THE DYNAMICS OF THE US CONTAINER MARKET AND SHIFTING TRADE PATTERNS IMPLICATIONS FOR FUTURE INVESTMENT TO PROMOTE US EXPORT ACTIVITY AND ECONOMIC GROWTH PREPARED FOR: AMERICAN ASSOCIATION OF PORT AUTHORITES

THE DYNAMICS OF THE US CONTAINER MARKET AND SHIFTING TRADE PATTERNS IMPLICATIONS FOR FUTURE INVESTMENT TO PROMOTE US EXPORT ACTIVITY AND ECONOMIC GROWTH PREPARED FOR: AMERICAN ASSOCIATION OF PORT AUTHORITES

Global Supply Chain Management: Seattle-Tacoma

Boston Strategies International, Inc. February 2008 Global Infrastructure Series Global Supply Chain Management: Seattle-Tacoma www.bostonstrategies.com b t t t i (1) (781) 250 8150 Page 1 This report

Boston Strategies International, Inc. February 2008 Global Infrastructure Series Global Supply Chain Management: Seattle-Tacoma www.bostonstrategies.com b t t t i (1) (781) 250 8150 Page 1 This report

PORT OF HOUSTON AUTHORITY

PORT OF HOUSTON AUTHORITY I-TED 2014 PORT OF HOUSTON AUTHORITY Governmental subdivision chartered by the State Governed by a seven member Commission Appointed by Harris County, City of Houston and other

PORT OF HOUSTON AUTHORITY I-TED 2014 PORT OF HOUSTON AUTHORITY Governmental subdivision chartered by the State Governed by a seven member Commission Appointed by Harris County, City of Houston and other

The Emergence of. Florida s Seaports and Inland Ports. Florida League of Cities - International Relations Committee November 17, 2011

The Emergence of Florida s Seaports and Inland Ports Florida League of Cities - International Relations Committee November 17, 2011 History of the Global Supply Chain 2 Supply Chain, Circa 1950 Regional

The Emergence of Florida s Seaports and Inland Ports Florida League of Cities - International Relations Committee November 17, 2011 History of the Global Supply Chain 2 Supply Chain, Circa 1950 Regional

Port Everglades Master Plan Project Introduction TABLE OF CONTENTS. Table of Contents... iii List of Figures... v List of Tables...

PORT EVERGLADES MASTER PLAN TABLE OF CONTENTS AND PROJECT INTRODUCTION PRESENTED BY TABLE OF CONTENTS Element Title Page Table of Contents... iii List of Figures... v List of Tables... x EXECUTIVE SUMMARY

PORT EVERGLADES MASTER PLAN TABLE OF CONTENTS AND PROJECT INTRODUCTION PRESENTED BY TABLE OF CONTENTS Element Title Page Table of Contents... iii List of Figures... v List of Tables... x EXECUTIVE SUMMARY

Container Flows in World Trade, U.S. Waterborne Commerce and Rail Shipments in North American Markets

Container Flows in World Trade, U.S. Waterborne Commerce and Rail Shipments in North American Markets Dr. William W. Wilson University Distinguished Professor Department of Agribusiness and Applied Economics

Container Flows in World Trade, U.S. Waterborne Commerce and Rail Shipments in North American Markets Dr. William W. Wilson University Distinguished Professor Department of Agribusiness and Applied Economics

Accommodating Mega-Ships at Existing Wharves

Accommodating Mega-Ships at Existing Wharves Presented by: Kevin P. Abt, P.E. The Virginia Port Authority and Bruce Lambert U.S. Army Corps of Engineers February 22, 2006 National Cargo Trends U.S. Cargo

Accommodating Mega-Ships at Existing Wharves Presented by: Kevin P. Abt, P.E. The Virginia Port Authority and Bruce Lambert U.S. Army Corps of Engineers February 22, 2006 National Cargo Trends U.S. Cargo

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm. October 7, 2009

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm October 7, 2009 Today s Objectives Endeavor to provide a broad context for today s session by

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm October 7, 2009 Today s Objectives Endeavor to provide a broad context for today s session by

House Select Committee on Strategic Transportation and Long Term Funding Solutions. November 6, 2017

House Select Committee on Strategic Transportation and Long Term Funding Solutions November 6, 2017 1 Welcome to N.C. Ports Fast Facts Two locations serving the Carolinas Over 350,000 teus Over 4 million

House Select Committee on Strategic Transportation and Long Term Funding Solutions November 6, 2017 1 Welcome to N.C. Ports Fast Facts Two locations serving the Carolinas Over 350,000 teus Over 4 million

FREIGHT AND INTERMODAL SYSTEMS

FREIGHT AND INTERMODAL SYSTEMS FREIGHT AND INTERMODAL SYSTEMS ARE MAJOR DRIVERS OF OUR ECONOMIC GROWTH AND INVESTMENTS ARE NEEDED FOR US TO BE COMPETITIVE IN THE FUTURE. OVERVIEW This section summarizes

FREIGHT AND INTERMODAL SYSTEMS FREIGHT AND INTERMODAL SYSTEMS ARE MAJOR DRIVERS OF OUR ECONOMIC GROWTH AND INVESTMENTS ARE NEEDED FOR US TO BE COMPETITIVE IN THE FUTURE. OVERVIEW This section summarizes

BRIDGING GLOBAL TRADE

BRIDGING GLOBAL TRADE PREPARING FOR FUTURE GROWTH AND CHANGE Presented to AAPA S 2013 Shifting International Trade Routes January 24, 2013 Curtis J. Foltz Executive Director, Georgia Ports Authority Georgia

BRIDGING GLOBAL TRADE PREPARING FOR FUTURE GROWTH AND CHANGE Presented to AAPA S 2013 Shifting International Trade Routes January 24, 2013 Curtis J. Foltz Executive Director, Georgia Ports Authority Georgia

Supply Chain Management Summit August 23, 2012

Supply Chain Management Summit August 23, 2012 Steven J. King, P.E. Managing Director Quonset Business Park 3,207 Total Acres 168 Companies 8,800 Jobs Transportation Facilities Freight Seaport: 2 piers

Supply Chain Management Summit August 23, 2012 Steven J. King, P.E. Managing Director Quonset Business Park 3,207 Total Acres 168 Companies 8,800 Jobs Transportation Facilities Freight Seaport: 2 piers

Port Everglades. is South Florida s Powerhouse Port. Presented to American Association of Port Authorities Environment Committee. September 17, 2015

Port Everglades is South Florida s Powerhouse Port Presented to American Association of Port Authorities Environment Committee Port Everglades Baseline Emissions Inventory EPA Partnership Emission Modeling

Port Everglades is South Florida s Powerhouse Port Presented to American Association of Port Authorities Environment Committee Port Everglades Baseline Emissions Inventory EPA Partnership Emission Modeling

1.7 Berthing Analysis

1.7 Berthing Analysis Port Everglades currently operates its facilities as a landlord port; the Port constructs the facilities and leases them back to tenant operators. The majority of berths at the Port

1.7 Berthing Analysis Port Everglades currently operates its facilities as a landlord port; the Port constructs the facilities and leases them back to tenant operators. The majority of berths at the Port

CLASS I RAIL CSX & Norfolk Southern

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Updated 3/28/18 Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Updated 3/28/18 Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL

WEDA 2012 Presented by: Steven M. Cernak, P.E., PPM Chief Executive & Port Director

WEDA 2012 Presented by: Steven M. Cernak, P.E., PPM Chief Executive & Port Director Port Everglades Overview Second busiest cruise homeport in the world Florida s top seaport for international export trade

WEDA 2012 Presented by: Steven M. Cernak, P.E., PPM Chief Executive & Port Director Port Everglades Overview Second busiest cruise homeport in the world Florida s top seaport for international export trade

Southeast Florida Freight and Goods Movement Update Treasure Coast Regional Planning Council September 16, 2011

Southeast Florida Freight and Goods Movement Update Treasure Coast Regional Planning Council September 16, 2011 For Questions on this Presentation, Please Contact: Jeff Weidner, Mobility Manager Florida

Southeast Florida Freight and Goods Movement Update Treasure Coast Regional Planning Council September 16, 2011 For Questions on this Presentation, Please Contact: Jeff Weidner, Mobility Manager Florida

LOGISTICS Emerging & Alternative Ports. Title Sponsor : February 8-11, 2009 Gaylord Texan Dallas, Texas

LOGISTICS 2009 February 8-11, 2009 Gaylord Texan Dallas, Texas Emerging & Alternative Ports Title Sponsor : Ports Panel: Emerging and Alternative Ports David W. Eaton VP of Corporate Affairs & Right of

LOGISTICS 2009 February 8-11, 2009 Gaylord Texan Dallas, Texas Emerging & Alternative Ports Title Sponsor : Ports Panel: Emerging and Alternative Ports David W. Eaton VP of Corporate Affairs & Right of

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to June 6, 2017 Chatham ICTF served by CSX Transportation Mason ICTF served by Norfolk Southern Railroad GARDEN CITY

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to June 6, 2017 Chatham ICTF served by CSX Transportation Mason ICTF served by Norfolk Southern Railroad GARDEN CITY

Measuring Supply Chain Performance A Government Perspective. APCGI Workshop Toronto June 18, 2010

Measuring Supply Chain Performance A Government Perspective APCGI Workshop Toronto June 18, 2010 1 Agenda Why should governments measure supply chain performance? 1. Policy Context 2. Supply Chain Metrics

Measuring Supply Chain Performance A Government Perspective APCGI Workshop Toronto June 18, 2010 1 Agenda Why should governments measure supply chain performance? 1. Policy Context 2. Supply Chain Metrics

Shifting Trade Routes Kyle Hancock January 25, 2013

Shifting Trade Routes Kyle Hancock January 25, 2013 1 CSX is a Fortune 250 company with 32,000 employees operating East of the Mississippi CSX Rail Network Our Business Midwest Chicago St Louis Northeast

Shifting Trade Routes Kyle Hancock January 25, 2013 1 CSX is a Fortune 250 company with 32,000 employees operating East of the Mississippi CSX Rail Network Our Business Midwest Chicago St Louis Northeast

Business Development Update

Business Development Update Performance By Commodity FY16 FY17 Total Port Berth Dry Bulk Liquid Bulk General Cargo +10% -1% +33% 2017 14,940,326 2017 21,717,106 2017 1,444,192 2016 13,618,586 2016 21,870,838

Business Development Update Performance By Commodity FY16 FY17 Total Port Berth Dry Bulk Liquid Bulk General Cargo +10% -1% +33% 2017 14,940,326 2017 21,717,106 2017 1,444,192 2016 13,618,586 2016 21,870,838

Intermodalism -- Metropolitan Chicago's Built-In Economic Advantage

May 1, 2015 Intermodalism -- Metropolitan Chicago's Built-In Economic Advantage CMAP's regional economic indicators microsite features key measures of metropolitan Chicago's economy and, where applicable,

May 1, 2015 Intermodalism -- Metropolitan Chicago's Built-In Economic Advantage CMAP's regional economic indicators microsite features key measures of metropolitan Chicago's economy and, where applicable,

U.S. Port and Inland Waterway Modernization Strategy: Options for the Future

U.S. Port and Inland Waterway Modernization Strategy: Options for the Future Inland Waterways Users Board Meeting 66, Pittsburgh Jim Walker Navigation Branch HQ, USACE 6 June 2012 US Army Corps of Engineers

U.S. Port and Inland Waterway Modernization Strategy: Options for the Future Inland Waterways Users Board Meeting 66, Pittsburgh Jim Walker Navigation Branch HQ, USACE 6 June 2012 US Army Corps of Engineers

How Tomorrow Moves: Ohio Conference on Freight 2011 Atlantic Connections to the Midwest

How Tomorrow Moves: Ohio Conference on Freight 2011 Atlantic Connections to the Midwest 1 Agenda CSX Review Market Overview National Gateway & NW Ohio Intermodal Hub Bridging Global Commerce 2 2011 first

How Tomorrow Moves: Ohio Conference on Freight 2011 Atlantic Connections to the Midwest 1 Agenda CSX Review Market Overview National Gateway & NW Ohio Intermodal Hub Bridging Global Commerce 2 2011 first

Packer Avenue Marine Terminal operator:

Packer Avenue Marine Terminal operator: Delaware River Main Channel Deepening PhilaPort Channel Deepening: 85% Complete Delaware River Main Channel Deepening Project Details Current Depth vs. Future Depth

Packer Avenue Marine Terminal operator: Delaware River Main Channel Deepening PhilaPort Channel Deepening: 85% Complete Delaware River Main Channel Deepening Project Details Current Depth vs. Future Depth

M. John Vickerman Principal Norfolk, Virginia

Port & Intermodal Development In the Face of The Impending Tsunami M. John Vickerman Principal Norfolk, Virginia Trends Maritime : Current Course & Direction? Cargo Demands, Capacity, Funding, Productivity

Port & Intermodal Development In the Face of The Impending Tsunami M. John Vickerman Principal Norfolk, Virginia Trends Maritime : Current Course & Direction? Cargo Demands, Capacity, Funding, Productivity

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES. Leipzig, May 2, 2012

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES Leipzig, May 2, 2012 1 Canada s Gateways and Trade Corridors: System-wide Approach Need objective fact-based metrics to: Asia-Pacific

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES Leipzig, May 2, 2012 1 Canada s Gateways and Trade Corridors: System-wide Approach Need objective fact-based metrics to: Asia-Pacific

American Association of Port Authorities Port Property Management and Pricing Seminar June 25, 2008 Toronto, Ontario

American Association of Port Authorities Port Property Management and Pricing Seminar June 25, 2008 Toronto, Ontario Frank C. Brogan, PPM Port of Corpus Christi Authority Kevin G. Carney, Executive Director

American Association of Port Authorities Port Property Management and Pricing Seminar June 25, 2008 Toronto, Ontario Frank C. Brogan, PPM Port of Corpus Christi Authority Kevin G. Carney, Executive Director

Technical Memorandum 3 Executive Summary Existing Conditions and Constraints Presentation. March 22, 2006

Technical Memorandum 3 Executive Summary Existing Conditions and Constraints Presentation March 22, 2006 MCGMAP Overview Develop a: Goods Movement Action Plan M A X I M I Z E S Mitigation of communities'

Technical Memorandum 3 Executive Summary Existing Conditions and Constraints Presentation March 22, 2006 MCGMAP Overview Develop a: Goods Movement Action Plan M A X I M I Z E S Mitigation of communities'

CLASS I RAIL CSX & Norfolk Southern

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL HUB Savannah Gateway

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL HUB Savannah Gateway

Now this is how you serve Florida s largest and fastest growing market.

Now this is how you serve Florida s largest and fastest growing market. May 2016 Overview Port Tampa Bay Florida s largest port in cargo tonnage and area 37 million tons cargo/year and encompassing 5000

Now this is how you serve Florida s largest and fastest growing market. May 2016 Overview Port Tampa Bay Florida s largest port in cargo tonnage and area 37 million tons cargo/year and encompassing 5000

Ports and Waterways: Lifeline for U.S. Agriculture

Ports and Waterways: Lifeline for U.S. Agriculture Ag Transportation Summit Steven L. Stockton, PE Director of Civil Works US Army Corps of Engineers 30 July 2013 US Army Corps of Engineers America s Future

Ports and Waterways: Lifeline for U.S. Agriculture Ag Transportation Summit Steven L. Stockton, PE Director of Civil Works US Army Corps of Engineers 30 July 2013 US Army Corps of Engineers America s Future

TRB - Annual Meeting

TRB - Annual Meeting NATIONAL DREDGING NEEDS STUDY PHILLIP J. THORPE Institute for Water Resources 16 January 2002 AGENDA Background Information Historical Perspective Global and US Trade World and US

TRB - Annual Meeting NATIONAL DREDGING NEEDS STUDY PHILLIP J. THORPE Institute for Water Resources 16 January 2002 AGENDA Background Information Historical Perspective Global and US Trade World and US

Select U.S. Ports Prepare For Panama Canal Expansion

Select U.S. Ports Prepare For Panama Canal Expansion Port of Jacksonville Grace Wang Associate Professor, Maritime Administration Texas A&M University at Galveston Galveston, Texas Anthony M. Pagano Director,

Select U.S. Ports Prepare For Panama Canal Expansion Port of Jacksonville Grace Wang Associate Professor, Maritime Administration Texas A&M University at Galveston Galveston, Texas Anthony M. Pagano Director,

Growth In Container Volumes

US GDP and TEU Trade: 1980-2005 600 Recession Total US TEUs 500 US GDP 400 300 200 100 0 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

US GDP and TEU Trade: 1980-2005 600 Recession Total US TEUs 500 US GDP 400 300 200 100 0 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Container Shipping. Outlook and Issues for US East Coast Shippers and Ports. Tina Liu Country Manager, China. October 15, 2015 TPM Shenzhen

Container Shipping Outlook and Issues for US East Coast Shippers and Ports October 15, 2015 TPM Shenzhen Tina Liu Country Manager, China Agenda Container volume growth Mega-alliances Mega-ships Port diversification

Container Shipping Outlook and Issues for US East Coast Shippers and Ports October 15, 2015 TPM Shenzhen Tina Liu Country Manager, China Agenda Container volume growth Mega-alliances Mega-ships Port diversification

437 Telfair Road. Property Highlights. Pricing FOR LEASE > WAREHOUSE SPACE GARDEN CITY, GA 31415

Property Highlights > ±207,676 SF available > 24 ceiling height > Building depth: 190 > High quality masonry & metal construction > Sprinklered > ±4,000 SF office (±2,000 on 2 floors) > Abundant outside

Property Highlights > ±207,676 SF available > 24 ceiling height > Building depth: 190 > High quality masonry & metal construction > Sprinklered > ±4,000 SF office (±2,000 on 2 floors) > Abundant outside

Northwestern University Transportation Center

Northwestern University Transportation Center 1 Overview» Fully integrated: large scale development, redevelopment, investment and property management operations» Founded in 1984, NYSE listed from 1993

Northwestern University Transportation Center 1 Overview» Fully integrated: large scale development, redevelopment, investment and property management operations» Founded in 1984, NYSE listed from 1993

CLASS I RAIL CSX & Norfolk Southern

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL HUB Savannah Gateway

INDUSTRIAL PARK ±2,700 Acres CLASS I RAIL CSX & Norfolk Southern PORT OF SAVANNAH Rail & Highway Access Industrial Park & Logistics Hub Highlights & Services SAVANNAH GATEWAY INDUSTRIAL HUB Savannah Gateway

Intermodal Success Story: BMW, SCPA and Norfolk Southern

Intermodal Success Story: BMW, SCPA and Norfolk Southern 2016 North American Rail Shippers Annual Meeting Randy Bayles, Director International Intermodal Discussion Topics NS Overview Market Drivers Impacting

Intermodal Success Story: BMW, SCPA and Norfolk Southern 2016 North American Rail Shippers Annual Meeting Randy Bayles, Director International Intermodal Discussion Topics NS Overview Market Drivers Impacting

The Potential Impact of Trucker Demand and Supply Issues at U.S. East Coast and Gulf Coast Ports

The Potential Impact of Trucker Demand and Supply Issues at U.S. East Coast and Gulf Coast Ports AAPA Maritime Economic Development/Public Relations Seminar June 8-10, 2005 Martin Associates 2938 Columbia

The Potential Impact of Trucker Demand and Supply Issues at U.S. East Coast and Gulf Coast Ports AAPA Maritime Economic Development/Public Relations Seminar June 8-10, 2005 Martin Associates 2938 Columbia

Preparing for the future today. Formerly known as Treasure Coast Intermodal Campus St. Lucie County, Florida USA

Preparing for the future today Formerly known as Treasure Coast Intermodal Campus St. Lucie County, Florida USA Table of Contents Florida Inland Port at a glance Project vision The business case The St.

Preparing for the future today Formerly known as Treasure Coast Intermodal Campus St. Lucie County, Florida USA Table of Contents Florida Inland Port at a glance Project vision The business case The St.

Savannah Harbor Expansion Project. Critical Infrastructure Expansion for the United States

Savannah Harbor Expansion Project Critical Infrastructure Expansion for the United States May 3, 2017 1 SAVANNAH: #4 AND FASTEST GROWING TOP 10 PORTS: 10-YEAR GROWTH RATE CY2006-2016 FASTEST GROWING U.S.

Savannah Harbor Expansion Project Critical Infrastructure Expansion for the United States May 3, 2017 1 SAVANNAH: #4 AND FASTEST GROWING TOP 10 PORTS: 10-YEAR GROWTH RATE CY2006-2016 FASTEST GROWING U.S.

Challenges with Evaluating Container Port Projects and the Corps of Engineers

Challenges with Evaluating Container Port Projects and the Corps of Engineers Smart Rivers Conference 14 September 2011 Kevin Knight Economist Institute for Water Resources U.S. Corps of Engineers 1 Trends

Challenges with Evaluating Container Port Projects and the Corps of Engineers Smart Rivers Conference 14 September 2011 Kevin Knight Economist Institute for Water Resources U.S. Corps of Engineers 1 Trends

PORT OF SAVANNAH. Garden City Terminal: The Southeast Gateway for the U.S.

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. July 24, 2018 GEORGIA PORTS AUTHORITY DEEPWATER & INLAND TERMINAL OPTIONS 9 Container berths 9,693 ft (2,955 m) of contiguous

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. July 24, 2018 GEORGIA PORTS AUTHORITY DEEPWATER & INLAND TERMINAL OPTIONS 9 Container berths 9,693 ft (2,955 m) of contiguous

Appalachia s Coastal Port Partners, Gateways to Global Commerce

Appalachia s Coastal Port Partners, Gateways to Global Commerce Jim Walker Director of Navigation Policy and Legislation American Association of Port Authorities November 13, 2013 American Association

Appalachia s Coastal Port Partners, Gateways to Global Commerce Jim Walker Director of Navigation Policy and Legislation American Association of Port Authorities November 13, 2013 American Association

Industrial Property Trends

Industrial Property Trends May 7, 2018 Lang Williams, SIOR Senior Vice President CBRE Hampton Roads 1 AGENDA SUPPLY CHAIN DYNAMICS ECONOMIC CYCLE & U.S. LOGISTCS MARKET INDUSTRIAL REAL ESTATE INVESTOR

Industrial Property Trends May 7, 2018 Lang Williams, SIOR Senior Vice President CBRE Hampton Roads 1 AGENDA SUPPLY CHAIN DYNAMICS ECONOMIC CYCLE & U.S. LOGISTCS MARKET INDUSTRIAL REAL ESTATE INVESTOR

BNSF Railway. The West Coast is the Best Coast. Fred Malesa. Vice President International Marketing Oct. 11, 2011

BNSF Railway The West Coast is the Best Coast Fred Malesa Vice President International Marketing Oct. 11, 2011 All slides are copyright 2011. Burlington Northern Santa Fe Corporation and BNSF Railway Company.

BNSF Railway The West Coast is the Best Coast Fred Malesa Vice President International Marketing Oct. 11, 2011 All slides are copyright 2011. Burlington Northern Santa Fe Corporation and BNSF Railway Company.

Infrastructure Investments Enhance Economic Activity

Infrastructure Investments Enhance Economic Activity National Association of Legislative Fiscal Offices 2013 Fiscal Analysts Seminar Jason Powell October 8, 2013 Virginia s Multimodal Transportation System:

Infrastructure Investments Enhance Economic Activity National Association of Legislative Fiscal Offices 2013 Fiscal Analysts Seminar Jason Powell October 8, 2013 Virginia s Multimodal Transportation System:

North Carolina Offshore Energy Exploration Subcommittee. Mr. Jeff Keever Senior Deputy Executive Director Virginia Port Authority February 23, 2010

North Carolina Offshore Energy Exploration Subcommittee Mr. Jeff Keever Senior Deputy Executive Director Virginia Port Authority February 23, 2010 East Coast Logistics Hub for Offshore Energy Exploration

North Carolina Offshore Energy Exploration Subcommittee Mr. Jeff Keever Senior Deputy Executive Director Virginia Port Authority February 23, 2010 East Coast Logistics Hub for Offshore Energy Exploration

The Immediate Aftermath of the Panama Canal Expansion on the Southeastern United States

Expansion on the Southeastern United States Bruce Lambert, Executive Director Institute for Trade and Transportation Studies - 10 Veterans Blvd., New Orleans, LA 70124 T: 540-455-9882 E: bruce@ittsresearch.org

Expansion on the Southeastern United States Bruce Lambert, Executive Director Institute for Trade and Transportation Studies - 10 Veterans Blvd., New Orleans, LA 70124 T: 540-455-9882 E: bruce@ittsresearch.org

Introduction to Industrial Property. By Norm G. Miller University of San Diego

Introduction to Industrial Property By Norm G. Miller University of San Diego nmiller@sandiego.edu Industrial Overview Key topics Drivers of industrial demand Types of industrial property Importance of

Introduction to Industrial Property By Norm G. Miller University of San Diego nmiller@sandiego.edu Industrial Overview Key topics Drivers of industrial demand Types of industrial property Importance of

139 FR AMPTON D r i v e FOR SALE

FRAMPTON D r i v e FOR SALE FRAMPTON D r i v e Point South is strategically located at the intersection of Hwy 17 and Interstate 95, a heavily traveled corridor for both tourism and commerce traffic. I-95

FRAMPTON D r i v e FOR SALE FRAMPTON D r i v e Point South is strategically located at the intersection of Hwy 17 and Interstate 95, a heavily traveled corridor for both tourism and commerce traffic. I-95

Logistics Impact on Industrial Development and Investment. Prepared By: Curtis D. Spencer, President IMS Worldwide, Inc.

Logistics Impact on Industrial Development and Investment Prepared By: Curtis D. Spencer, President IMS Worldwide, Inc. About IMS Worldwide Inc. IMSW has completed over 295 FTZ Projects during 45 years.

Logistics Impact on Industrial Development and Investment Prepared By: Curtis D. Spencer, President IMS Worldwide, Inc. About IMS Worldwide Inc. IMSW has completed over 295 FTZ Projects during 45 years.

Parent Company World Shipping - Cleveland, OH. Family owned business in operation since 1960 s

ContainerPort, Inc. Parent Company World Shipping - Cleveland, OH Family owned business in operation since 1960 s Vessel husbandry, liner agency, ISO Tank and Dry Box NVOCC ContainerPort Group has been

ContainerPort, Inc. Parent Company World Shipping - Cleveland, OH Family owned business in operation since 1960 s Vessel husbandry, liner agency, ISO Tank and Dry Box NVOCC ContainerPort Group has been

Presentation Topics The Alameda Corridor Project Corridor Performance Goods Movement Challenges

1 Presentation Topics The Alameda Corridor Project Corridor Performance Goods Movement Challenges 2 Ports of Los Angeles and Long Beach Largest port complex in the U.S. Fifth largest in the world Highest

1 Presentation Topics The Alameda Corridor Project Corridor Performance Goods Movement Challenges 2 Ports of Los Angeles and Long Beach Largest port complex in the U.S. Fifth largest in the world Highest

Expectations for Port Customers and Clients. Dan Sheehy -NYK Line AAPA Meeting October 23, 2008

Expectations for Port Customers and Clients Dan Sheehy -NYK Line AAPA Meeting October 23, 2008 Areas for Review 1. Overview of NYK Line 2. Liner Trade Business 3. Demand versus Supply Outlook 4. Bunker

Expectations for Port Customers and Clients Dan Sheehy -NYK Line AAPA Meeting October 23, 2008 Areas for Review 1. Overview of NYK Line 2. Liner Trade Business 3. Demand versus Supply Outlook 4. Bunker

Port Cooperation Agreements Propelling Capital Projects

Port Cooperation Agreements Propelling Capital Projects AAPA Capital Projects Seminar Norfolk, VA May 9, 2018 1 Andy Hecker Chief Financial Officer PortMiami Dakota Chamberlain Chief Facilities Development

Port Cooperation Agreements Propelling Capital Projects AAPA Capital Projects Seminar Norfolk, VA May 9, 2018 1 Andy Hecker Chief Financial Officer PortMiami Dakota Chamberlain Chief Facilities Development

Attracting Distribution Center and Related Logistics Investment to Florida to Anchor Traffic through Florida Ports

Attracting Distribution Center and Related Logistics Investment to Florida to Anchor Traffic through Florida Ports Florida Seaport Transportation and Economic Development Council Meeting February, 208

Attracting Distribution Center and Related Logistics Investment to Florida to Anchor Traffic through Florida Ports Florida Seaport Transportation and Economic Development Council Meeting February, 208

Port of Baltimore and Economic Development

Port of Baltimore and Economic Development Presentation to the National Conference of State Legislatures Fiscal Analysts Seminar Department of Legislative Services Office of Policy Analysis Annapolis,

Port of Baltimore and Economic Development Presentation to the National Conference of State Legislatures Fiscal Analysts Seminar Department of Legislative Services Office of Policy Analysis Annapolis,

Port of Philadelphia Port Advisory Board

Port of Philadelphia Port Advisory Board JULY 7, 2016 Meeting Overview: Natural flow of port development arising from the channel being deepened to 45 feet. Channel Deepening Project The Channel Deepening

Port of Philadelphia Port Advisory Board JULY 7, 2016 Meeting Overview: Natural flow of port development arising from the channel being deepened to 45 feet. Channel Deepening Project The Channel Deepening

Southport A Unique Perspective on P3s

Southport A Unique Perspective on P3s 1 Snapshot in Time 2014-2015 Expansion Considerations Background Noise Container capacity peaking 3 rd time to market Time for a change of leadership No Plan Energy

Southport A Unique Perspective on P3s 1 Snapshot in Time 2014-2015 Expansion Considerations Background Noise Container capacity peaking 3 rd time to market Time for a change of leadership No Plan Energy

The ever changing supply chain strategy. Tom Scorsune January 20, 2012

The ever changing supply chain strategy Tom Scorsune January 20, 2012 Domestic production Circa 1950 Domestic Production Regional Distribution Production Distribution 2 Domestic production Circa 1970 New

The ever changing supply chain strategy Tom Scorsune January 20, 2012 Domestic production Circa 1950 Domestic Production Regional Distribution Production Distribution 2 Domestic production Circa 1970 New

Russell McMurry Georgia Dept. Of Transportation. Chris Tomlinson SRTA and GRTA. Griff Lynch Georgia Ports Authority

Griff Lynch Georgia Ports Authority Russell McMurry Georgia Dept. Of Transportation Chris Tomlinson SRTA and GRTA Michael Sullivan Georgia Transportation Alliance Roosevelt Council, Jr. Hartsfield-Jackson

Griff Lynch Georgia Ports Authority Russell McMurry Georgia Dept. Of Transportation Chris Tomlinson SRTA and GRTA Michael Sullivan Georgia Transportation Alliance Roosevelt Council, Jr. Hartsfield-Jackson

Seaport Perspective. I-75 Relief Task Force Meeting #3. Charles Klug, Principal Counsel, Tampa Port Authority. Presented by:

Seaport Perspective I-75 Relief Task Force Meeting #3 Presented by: Charles Klug, Principal Counsel, Tampa Port Authority F e b r u a r y 2 6, 2016 NOTE: Information is preliminary and subject to change

Seaport Perspective I-75 Relief Task Force Meeting #3 Presented by: Charles Klug, Principal Counsel, Tampa Port Authority F e b r u a r y 2 6, 2016 NOTE: Information is preliminary and subject to change

Panama Canal Expansion: Who Wins? Who Loses?

Panama Canal Expansion: Who Wins? Who Loses? Curtis Spencer, IMS Worldwide, Inc. Jim MacLellan, Port of Los Angeles Kevin Burwell, Virginia Port Authority John Moseley, Port of Houston Authority Agenda

Panama Canal Expansion: Who Wins? Who Loses? Curtis Spencer, IMS Worldwide, Inc. Jim MacLellan, Port of Los Angeles Kevin Burwell, Virginia Port Authority John Moseley, Port of Houston Authority Agenda

RTSA Technical Session

RTSA Technical Session US Port & Intermodal Challenges April 21, 2015 5:30 p.m. PB 1885 Company founded by General William Parsons 1899 Mapping China s Hankow to Canton Railway 1906 Henry Brinckerhoff

RTSA Technical Session US Port & Intermodal Challenges April 21, 2015 5:30 p.m. PB 1885 Company founded by General William Parsons 1899 Mapping China s Hankow to Canton Railway 1906 Henry Brinckerhoff

Norfolk Southern: Creating Options for Ohio Shippers. Ohio Conference on Freight 15 September 2010

Norfolk Southern: Creating Options for Ohio Shippers Ohio Conference on Freight 15 September 2010 Norfolk Southern s Intermodal Network Chicago 47th Street 63 rd Street Landers Calumet Ashland Ave Detroit

Norfolk Southern: Creating Options for Ohio Shippers Ohio Conference on Freight 15 September 2010 Norfolk Southern s Intermodal Network Chicago 47th Street 63 rd Street Landers Calumet Ashland Ave Detroit

Gene Seroka APL President, Americas. January 24, 2013 Tampa, Florida

Gene Seroka APL President, Americas January 24, 2013 Tampa, Florida Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand

Gene Seroka APL President, Americas January 24, 2013 Tampa, Florida Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand

Facilities Guide NORTH & SOUTH HARBORS S E AT T L E TAC O M A, U. S. A.

Facilities Guide NORTH & SOUTH HARBORS S E AT T L E TAC O M A, U. S. A. CONTAINER TERMINALS Size Ship Berths Berth Depth Cranes Truck Lanes Scales Reefer Plugs Rail Ramps NORTH HARBOR SEATTLE T-8 SSA T-5/

Facilities Guide NORTH & SOUTH HARBORS S E AT T L E TAC O M A, U. S. A. CONTAINER TERMINALS Size Ship Berths Berth Depth Cranes Truck Lanes Scales Reefer Plugs Rail Ramps NORTH HARBOR SEATTLE T-8 SSA T-5/

Miami River Freight Improvement Plan Financial Management Number:

Miami River Commission January 8, 2018 Miami, FL Carlos A. Castro, District Freight Coordinator Miami River Freight Improvement Plan Financial Management Number: 437946-1-22-01 Agenda Study Background

Miami River Commission January 8, 2018 Miami, FL Carlos A. Castro, District Freight Coordinator Miami River Freight Improvement Plan Financial Management Number: 437946-1-22-01 Agenda Study Background

Intermodal Committee Discussion. January 16, 2008 Charlotte, North Carolina

Intermodal Committee Discussion January 16, 2008 Charlotte, North Carolina Population Context Eastern markets account for two-thirds of U.S. population Chicago New York Markets drive three-fourths of total

Intermodal Committee Discussion January 16, 2008 Charlotte, North Carolina Population Context Eastern markets account for two-thirds of U.S. population Chicago New York Markets drive three-fourths of total

POINT SOUTH 139 Frampton Drive Yemassee, Jasper County, South Carolina

for sale POINT SOUTH 139 Frampton Drive Yemassee, Jasper County, South Carolina For More Information, Contact: Tradd Varner Senior Associate Industrial & Investment Services O 843.725.7200 F 843.725.7201

for sale POINT SOUTH 139 Frampton Drive Yemassee, Jasper County, South Carolina For More Information, Contact: Tradd Varner Senior Associate Industrial & Investment Services O 843.725.7200 F 843.725.7201

Panama Canal Expansion: Impacts on the US Marketplace

NMHC General Session April 22, 2015 NMHC Spring Board Meeting Waldorf Astoria Hotel New York Panama Canal Expansion: Impacts on the US Marketplace M. John Vickerman Williamsburg, Virginia Today s Global

NMHC General Session April 22, 2015 NMHC Spring Board Meeting Waldorf Astoria Hotel New York Panama Canal Expansion: Impacts on the US Marketplace M. John Vickerman Williamsburg, Virginia Today s Global

Alabama State Port Authority

Alabama State Port Authority Port Update IFFCBANO June 6, 2014 www.asdd.com Port of Mobile Excellent Transportation Infrastructure I-10 & I-65 5 Class 1 Railroads (BNSF, CN, CSX, KCS, NS) Rail Ferry Service

Alabama State Port Authority Port Update IFFCBANO June 6, 2014 www.asdd.com Port of Mobile Excellent Transportation Infrastructure I-10 & I-65 5 Class 1 Railroads (BNSF, CN, CSX, KCS, NS) Rail Ferry Service

Process for Port Master Planning

Process for Port Master Planning Presented by Kerry Simpson, P.E. Vice President, Marine Terminals AAPA Port Executive Management Seminar Merida, Mexico December 2014 Moffatt & Nichol Founded in 1945 in

Process for Port Master Planning Presented by Kerry Simpson, P.E. Vice President, Marine Terminals AAPA Port Executive Management Seminar Merida, Mexico December 2014 Moffatt & Nichol Founded in 1945 in

Port of Los Angeles Presentation to the Los Angeles Investors Conference March 19, 2018

Port of Los Angeles Presentation to the Los Angeles Investors Conference March 19, 2018 1 Today s Focus Introduction to the Port of Los Angeles Market Position & Cargo Volumes Capital Improvement Program

Port of Los Angeles Presentation to the Los Angeles Investors Conference March 19, 2018 1 Today s Focus Introduction to the Port of Los Angeles Market Position & Cargo Volumes Capital Improvement Program

AAPA Harbors, Navigation and Environment Seminar Vancouver, B.C.

AAPA Harbors, Navigation and Environment Seminar Vancouver, B.C. Estimating Emissions From Container Cargo Operations Using a Comprehensive Container Terminal Model June 7, 7, 2006 Moffatt & Nichol MN

AAPA Harbors, Navigation and Environment Seminar Vancouver, B.C. Estimating Emissions From Container Cargo Operations Using a Comprehensive Container Terminal Model June 7, 7, 2006 Moffatt & Nichol MN

PANAMA CANAL BUSINESS FORUM

PRESENTATION TO: PANAMA CANAL BUSINESS FORUM IMPACT OF THE PANAMA CANAL AND MARKET OPPORTUNITY FOR TEXAS Presentation By: Dr. Alexander Metcalf JANUARY 18, 2016 Transportation Economics & Management Systems,

PRESENTATION TO: PANAMA CANAL BUSINESS FORUM IMPACT OF THE PANAMA CANAL AND MARKET OPPORTUNITY FOR TEXAS Presentation By: Dr. Alexander Metcalf JANUARY 18, 2016 Transportation Economics & Management Systems,

OHIO STATEWIDE FREIGHT STUDY PROGRESS UPDATE. Ohio Conference on Freight: September 12, 2012

OHIO STATEWIDE FREIGHT STUDY PROGRESS UPDATE Ohio Conference on Freight: September 12, 2012 Progress and Timeline Dec 2011 Aug 2012 Sept 2012 Dec 2012 Stakeholder Involvement Interviews Supply Chain Survey

OHIO STATEWIDE FREIGHT STUDY PROGRESS UPDATE Ohio Conference on Freight: September 12, 2012 Progress and Timeline Dec 2011 Aug 2012 Sept 2012 Dec 2012 Stakeholder Involvement Interviews Supply Chain Survey

LONE STAR HARBOR SAFETY COMMITTEE Roger Guenther Executive Director Port of Houston Authority

LONE STAR HARBOR SAFETY COMMITTEE Roger Guenther Executive Director Port of Houston Authority Terminal/Refinery Symposium Thursday, February16, 2017 HOUSTON THE BUSIEST U.S. CHANNEL ECONOMIC IMPACTS FOR

LONE STAR HARBOR SAFETY COMMITTEE Roger Guenther Executive Director Port of Houston Authority Terminal/Refinery Symposium Thursday, February16, 2017 HOUSTON THE BUSIEST U.S. CHANNEL ECONOMIC IMPACTS FOR

D E C AT U R I N T E R M O D A L R A M P O P P O R T U N I T Y F I N A L R E P O R T A U G U S T 3 1,

D E C AT U R I N T E R M O D A L R A M P O P P O R T U N I T Y F I N A L R E P O R T A U G U S T 3 1, 2 0 1 5 Agenda Executive Summary Terminal Overview Shipper Opportunities and Requirements Conclusions

D E C AT U R I N T E R M O D A L R A M P O P P O R T U N I T Y F I N A L R E P O R T A U G U S T 3 1, 2 0 1 5 Agenda Executive Summary Terminal Overview Shipper Opportunities and Requirements Conclusions

Port Activity and Competitiveness Tracker

Comprehensive Regional Goods Movement Plan and Implementation Strategy Port Activity and Competitiveness Tracker Presented to I-710 Corridor Advisory Committee Gill Hicks Cambridge Systematics, Inc. May

Comprehensive Regional Goods Movement Plan and Implementation Strategy Port Activity and Competitiveness Tracker Presented to I-710 Corridor Advisory Committee Gill Hicks Cambridge Systematics, Inc. May

The Economic Impacts of Virginia s Maritime Industry

The Economic Impacts of Virginia s Maritime Industry PORT COMMERCE Million Tons of Cargo Moved 0,00 Jobs $. Billion In Wages $. Billion In Spending $. Billion In State/Local Taxes.% of Virginia Gross State

The Economic Impacts of Virginia s Maritime Industry PORT COMMERCE Million Tons of Cargo Moved 0,00 Jobs $. Billion In Wages $. Billion In Spending $. Billion In State/Local Taxes.% of Virginia Gross State

Port Partnerships Strategic Opportunities for Gateway & Closer Market Ports to Work Together Presented by Rainer Lilienthal General Manager-Trade

Port Partnerships Strategic Opportunities for Gateway & Closer Market Ports to Work Together Presented by Rainer Lilienthal General Manager-Trade Development Port of Houston Overview The Port of Houston

Port Partnerships Strategic Opportunities for Gateway & Closer Market Ports to Work Together Presented by Rainer Lilienthal General Manager-Trade Development Port of Houston Overview The Port of Houston

Connecting Hinterlands to Ports Through Rail Investment

Connecting Hinterlands to Ports Through Rail Investment The Ideal: Every inland warehouse door is a virtual port From Ideal to Reality Rail Solution is Competitive vs. Truck Direct All In Total Logistics

Connecting Hinterlands to Ports Through Rail Investment The Ideal: Every inland warehouse door is a virtual port From Ideal to Reality Rail Solution is Competitive vs. Truck Direct All In Total Logistics

Southeastern Seaboard Savannah, GA, USA

Southeastern Seaboard Savannah, GA, USA ±365 acre dual rail-served industrial terminal 1 st marine terminal on the Savannah River, 42 depth (future depth 47 ) Full range of industrial services available

Southeastern Seaboard Savannah, GA, USA ±365 acre dual rail-served industrial terminal 1 st marine terminal on the Savannah River, 42 depth (future depth 47 ) Full range of industrial services available

SEARS UP Intermodal. Allison Watson, General Director March 26, 2014

SEARS UP Intermodal Allison Watson, General Director March 26, 2014 0 Union Pacific Intermodal $4.0 Billion Revenue 2013 Volume Mix Seattle Tacoma Portland Sparks Minneapolis / St. Paul Council Bluffs

SEARS UP Intermodal Allison Watson, General Director March 26, 2014 0 Union Pacific Intermodal $4.0 Billion Revenue 2013 Volume Mix Seattle Tacoma Portland Sparks Minneapolis / St. Paul Council Bluffs

Shifting Trade Patterns A VIEW FROM THE WEATHER DECK

Shifting Trade Patterns A VIEW FROM THE WEATHER DECK National Freight Infrastructure Policies The Impact of Shifting Trade Patterns Infrastructure Needs & Investment Plans January 24, 2013 Tampa, Florida

Shifting Trade Patterns A VIEW FROM THE WEATHER DECK National Freight Infrastructure Policies The Impact of Shifting Trade Patterns Infrastructure Needs & Investment Plans January 24, 2013 Tampa, Florida

Latin American Ports: Logistical Challenges for a Post Panama Canal Expansion Era

Foro Iberoamericano de Logística y Puertos, Panama, September 19 2013 Los Puertos Iberoamericanos en las Nuevas Rutas de Transporte Marítimo Latin American Ports: Logistical Challenges for a Post Panama

Foro Iberoamericano de Logística y Puertos, Panama, September 19 2013 Los Puertos Iberoamericanos en las Nuevas Rutas de Transporte Marítimo Latin American Ports: Logistical Challenges for a Post Panama