Chapter 13. Auditing the Inventory Management Process

|

|

|

- Beverly Hart

- 5 years ago

- Views:

Transcription

1 Chapter 13 Auditing the Inventory Management Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

2 Overview of the Inventory Management Process LO# 1 Purchasing process Inventory management process Revenue process Purchase of raw materials Payment of manufacturing overhead Human resource management process Assignment of direct and indirect labor costs Sale of goods 13-2

3 Types of Documents and Records 1. Production Schedule Based on the expected demand for the entity s products. 2. Receiving Report Records the receipt of goods from vendors. 3. Materials Requisition Used to track materials during the production process. 4. Inventory Master File Contains all the important information related to the entity s inventory, including the perpetual inventory records. LO# 2 Production Schedule Inventory Master File 13-3

4 Types of Documents and Records 5. Production Data Information Contains information about the transfer of goods and related cost accumulation at each stage of production. 6. Cost Accumulation and Variance Report Material, labor, and overhead costs are charged to inventory as part of the manufacturing process. The variance report compares actual costs to standard or budgeted costs. 7. Inventory Status Report Shows the type and amount of products on hand. 8. Shipping Order Used to remove goods from the perpetual inventory records. Shipping Order LO#

5 LO# 3 The Major Functions 13-5

6 LO# 4 Key Segregation of Duties 13-6

7 LO# 4 Key Segregation of Duties Segregation of duties is a particularly important control in the inventory management process because of the potential for theft and fraud. 13-7

8 LO# 5 Inherent Risk Assessment The auditor should consider industry-related factors and operating and engagement characteristics when assessing the possibility of a material misstatement. If industry competition is intense, there may be problems with the proper valuation of inventory. Technology changes in certain industries may also promote material misstatement due to obsolescence. Products that are small and of high value are more susceptible to theft. The auditor must be alert to related-party transactions for acquiring raw materials and selling finished products. Prior-year misstatements are good indicators of potential misstatements in the current year. 13-8

9 LO# 6 Control Risk Assessment Major steps in setting the control risk in the inventory management process. Understand and document the inventory management process based on a reliance strategy. Plan and perform tests of controls on inventory transactions. Set and document the control risk for the inventory management process. 13-9

10 Control Activities and Tests of Controls Inventory Transactions LO#

11 Control Activities and Tests of Controls Inventory Transactions Occurrence of Inventory Transactions The auditor s main concern is that all recorded inventory exists. The auditor should also be concerned that goods may be stolen. Review and observation are the main tests of controls used by the auditor to test the control procedures. LO#

12 LO# 7 Control Activities and Tests of Controls Inventory Transactions Completeness of Inventory Transactions The primary control procedure for completeness relates to recording inventory that has been received. Controls are closely related to the purchasing process

13 LO# 7 Control Activities and Tests of Controls Inventory Transactions Authorization of Inventory Transactions The auditor s concern with authorization in the inventory system is with unauthorized purchase or production activity that may lead to excess levels of certain types of finished goods

14 LO# 7 Control Activities and Tests of Controls Inventory Transactions Accuracy of Inventory Transactions Inventory transactions that are not properly recorded result in misstatements that directly affect the amounts reported in the financial statements. Inventory purchases must be recorded at the correct price and actual quantity received. Inventory shipped must be properly recorded in cost of goods sold and the related revenue recognized

15 Control Activities and Tests of Controls Inventory Transactions LO# 7 Cutoff of Inventory Transactions Inventory transactions recorded in the improper period could affect a number of accounts, including inventory, purchases, and cost of goods sold

16 Control Activities and Tests of Controls Inventory Transactions Classification of Inventory Transactions The entity must have control procedures to ensure that inventory is properly classified as raw materials, work in process, or finished goods. By knowing which manufacturing department holds the inventory, the auditor is able to classify it by type. LO#

17 LO# 8 Auditing Inventory 13-17

18 LO# 8 Auditing Inventory 13-18

19 LO# 8 Auditing Inventory 13-19

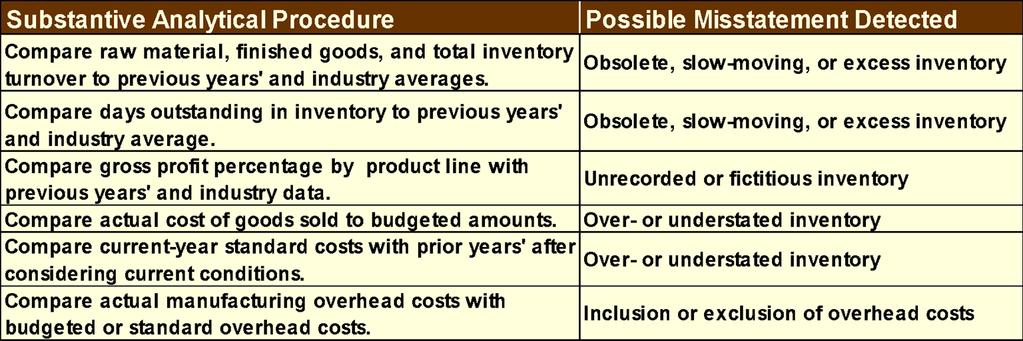

20 LO# 9 Substantive Analytical Procedures 13-20

21 LO# 10 Auditing Standard Costs Materials Test the quantity and type of materials included in the product and the price of the materials. Labor Gather evidence about the type and amount of labor needed for production and the labor rate. Overhead Review the entity s method of overhead allocation for reasonableness, compliance with GAAP, and consistency

22 LO# 11 Observing Physical Inventory During the observation of the physical inventory count, the auditor should do the following: 1. Ensure that no production is scheduled. If production is scheduled proper controls must be established for movement between departments in order to prevent double counting. 2. Ensure that there is no movement of goods during the inventory count. 3. Make sure that the entity s count teams are following the inventory count instructions. 4. Ensure that inventory tags are issued sequentially to individual departments

23 LO# 11 Observing Physical Inventory 5. Perform test counts and record a sample of counts in the working papers. 6. Obtain tag control information for testing the entity s inventory compilation. 7. Obtain cutoff information, including the number of the last shipping and receiving documents issued. 8. Observe the condition of the inventory for items that may be obsolete, slow moving, or carried in excess quantities. 9. Inquire about goods held on consignment for others or held on a billand-hold basis

24 LO# 12 Tests of Details of Transactions 13-24

25 Tests of Details of Account Balances LO#

26 LO# 12 Tests of Details of Disclosures 13-26

27 Tests of Details of Transactions, Account Balances, and Disclosures LO# 12 Possible causes of book-to-physical differences: 1. Inventory cutoff errors. 2. Unreported scrap or spoilage. 3. Pilferage or theft

28 Tests of Details of Transactions, Account Balances, and Disclosures Examples of Disclosure Items: 1. Cost method (FIFO, LIFO, retail method). 2. Components of inventory. 3. Long-term purchase contracts. 4. Consigned inventory. 5. Purchases from related parties. 6. LIFO liquidations. 7. Pledged or assigned inventory. 8. Disclosure of unusual losses from write-downs or losses on long-term purchase commitments. 9. Warranty obligations. LO#

29 Evaluating the Audit Findings - Inventory LO# 13 At the conclusion of testing, the auditor should aggregate all identified misstatements. The likely misstatement is compared to the tolerable misstatement allocated to the inventory account. Likely misstatement < Tolerable misstatement The auditor may accept the inventory account as fairly presented. Likely misstatement > Tolerable misstatement The auditor must conclude the inventory is not fairly presented

30 End of Chapter

New cycles...same story

Instructor Michael Brownlee B.Comm(Hons),CGA Course AU1 Module 9: Inventory and property, plant, and equipment balances, production and payroll cycles, and finance and investment cycle New cycles...same

Instructor Michael Brownlee B.Comm(Hons),CGA Course AU1 Module 9: Inventory and property, plant, and equipment balances, production and payroll cycles, and finance and investment cycle New cycles...same

Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Chapter 5. Evidence and Documentation. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

PREVIEW OF CHAPTER. Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

CA Abhijit Sanzgiri.

CA Abhijit Sanzgiri. Inventory - idle stock of physical goods. Contains economic value. Held in various forms by an organization in its custody awaiting packing, processing, transformation. For use or

CA Abhijit Sanzgiri. Inventory - idle stock of physical goods. Contains economic value. Held in various forms by an organization in its custody awaiting packing, processing, transformation. For use or

Quality Control Review Checklist

Institute of Cost and Management Accountants of Pakistan Quality Control Review Checklist For Cost Audit Engagements Issued By Quality Assurance Board Table of Contents 1. PRE ENGAGEMENT ACTIVITIES...

Institute of Cost and Management Accountants of Pakistan Quality Control Review Checklist For Cost Audit Engagements Issued By Quality Assurance Board Table of Contents 1. PRE ENGAGEMENT ACTIVITIES...

Inventories. 2. Explain the accounting for inventories and apply the inventory cost flow methods.

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

1 INTRODUCTION DEFINITIONS VALUATION INVENTORY ALLOWANCE (NET REALIZABLE VALUE) REPORTING INTERNAL INVENTORY...

REPORTING INTERNAL INVENTORY...") RAPALA INVENTORY VALUATION PRINCIPLES AND INTERNAL INVENTORY 1 INTRODUCTION... 2 2 DEFINITIONS... 2 2.1 INVENTORIES... 2 2.2 STOCK COVERAGE... 3 2.3 OBSOLETE INVENTORY... 3 2.4 NET REALIZABLE VALUE...

RAPALA INVENTORY VALUATION PRINCIPLES AND INTERNAL INVENTORY 1 INTRODUCTION... 2 2 DEFINITIONS... 2 2.1 INVENTORIES... 2 2.2 STOCK COVERAGE... 3 2.3 OBSOLETE INVENTORY... 3 2.4 NET REALIZABLE VALUE...

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Using Data Analytics in Audits

Using Data Analytics in Audits Data Analytics is the process of inspecting, cleansing, transforming and modelling raw data with the purpose of discovering useful information, drawing conclusions and supporting

Using Data Analytics in Audits Data Analytics is the process of inspecting, cleansing, transforming and modelling raw data with the purpose of discovering useful information, drawing conclusions and supporting

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

C H A P T E R. Inventories. Corporate Financial Accounting 13e. human/istock/360/getty Images. Warren Reeve Duchac

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Internal Controls and Sampling Tests

Question 1: What important concepts should management consider in the design and implementation of internal controls? The two concepts that are important for management to consider in the design and implementation

Question 1: What important concepts should management consider in the design and implementation of internal controls? The two concepts that are important for management to consider in the design and implementation

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

AUDIT RESPONSIBILITIES AND OBJECTIVES

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Chapter 21 Audit of the Payroll and Personnel Cycle. Copyright 2014 Pearson Education

Chapter 21 Audit of the Payroll and Personnel Cycle Identify the accounts and transactions in the payroll and personnel cycle. Describe the business functions and the related documents and records in the

Chapter 21 Audit of the Payroll and Personnel Cycle Identify the accounts and transactions in the payroll and personnel cycle. Describe the business functions and the related documents and records in the

CHAPTER 9 TESTS OF CONTROLS

CHAPTER 9 TESTS OF CONTROLS 1 TESTS OF CONTROLS Provide auditor with evidence to support their assessment of control risk. When control risk assessed at less than high, necessary to gather evidence that

CHAPTER 9 TESTS OF CONTROLS 1 TESTS OF CONTROLS Provide auditor with evidence to support their assessment of control risk. When control risk assessed at less than high, necessary to gather evidence that

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEM SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

Chapter 9 Inventories: Additional Issues

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

Analytical Procedures

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

Chapter 7 Condensed (Day 1)

") Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

OPERATIONAL AND CONSUMABLE INVENTORY POLICY

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES. (Refer paragraphs 77 and 100)

") APPENDIX IV ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES (Refer paragraphs 77 and 100) Standards on Auditing ( SA ) 315 Identifying and Assessing the Risk

APPENDIX IV ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES (Refer paragraphs 77 and 100) Standards on Auditing ( SA ) 315 Identifying and Assessing the Risk

Chapter 4. Risk Assessment. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

Chapter 4 Risk Assessment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Audit Risk The risk that an auditor expresses an unqualified opinion on materially

FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010)

") SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)

501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)") Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

Akuntansi Biaya. Modul ke: 09FEB. Direct Material Cost. Fakultas. Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi. Program Studi Akuntansi

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Type of Inventory. OVERVIEW In case of manufacturing concerns. Stores and Spares. Formulae for Determining Cost of Inventory

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

Seminar Internal Control Identification and Filtering

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Detailed competency map

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley

Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable. Chapter 18 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items

501 Audit Evidence Specific Considerations for Selected Items") International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

Audit Evidence Specific Considerations for Selected Items

ISA 501 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence Specific Considerations for Selected Items INTERNATIONAL STANDARD ON AUDITING 501 AUDIT EVIDENCE SPECIFIC

ISA 501 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence Specific Considerations for Selected Items INTERNATIONAL STANDARD ON AUDITING 501 AUDIT EVIDENCE SPECIFIC

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT ACCOUNTING, ECONOMICS & FINANCE 23BACF BACHELOR OF ACCOUNTING COURSE: AUDITING 38 COURSE CODE: AUD312S SECOND OPPORTUNITY EXAMINATION QUESTION

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT ACCOUNTING, ECONOMICS & FINANCE 23BACF BACHELOR OF ACCOUNTING COURSE: AUDITING 38 COURSE CODE: AUD312S SECOND OPPORTUNITY EXAMINATION QUESTION

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

FM038: Inventory Accounting and Costing

FM038: Inventory Accounting and Costing FM038 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Whether you are a trader, manufacturer, contractor or a service provider, inventory has a major

FM038: Inventory Accounting and Costing FM038 Rev.001 CMCT COURSE OUTLINE Page 1 of 5 Training Description: Whether you are a trader, manufacturer, contractor or a service provider, inventory has a major

Cost Auditing Standard Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Chapter 7. Auditing Internal Control over Financial Reporting. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Accounting for Inventory

Accounting for Inventory Steven M. Bragg CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 Accounting for Inventory Steven M. Bragg Copyright 2014 by Steven M. Bragg. Course and

Accounting for Inventory Steven M. Bragg CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 Accounting for Inventory Steven M. Bragg Copyright 2014 by Steven M. Bragg. Course and

SECTION A CASE QUESTIONS (Total: 50 marks)

") SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Control activities that are relevant to an audit are: - Control activities that relate to significant risks or relate to risks for which substantive

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Control activities that are relevant to an audit are: - Control activities that relate to significant risks or relate to risks for which substantive

THE AUDITOR S RESPONSES TO ASSESSED RISKS SRI LANKA AUDITING STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

SRI LANKA STANDARD 330 THE AUDITOR S RESPONSES TO ASSESSED RISKS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction Scope of

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008

10 July 2008") Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Chapter 16. Auditing Operations and Completing the Audit. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

CHAPTER 2: ACCOUNTING FOR MATERIALS

1. An effective cost control system should include: a. An established plan of objectives and goals to be achieved. b. Regular reports showing the difference between goals and actual performance. c. Specific

1. An effective cost control system should include: a. An established plan of objectives and goals to be achieved. b. Regular reports showing the difference between goals and actual performance. c. Specific

RE Revisjon 1 Candidate 7608 KANDIDAT PRØVE. RE Revisjon :00. Sensurfrist 1/8

KANDIDAT 7608 PRØVE RE-400 1 Revisjon 1 Emnekode RE-400 Vurderingsform Skriftlig eksamen Starttid 13.10.2017 09:00 Sluttid 13.10.2017 13:00 Sensurfrist -- PDF opprettet 21.09.2018 10:17 Opprettet av Digital

KANDIDAT 7608 PRØVE RE-400 1 Revisjon 1 Emnekode RE-400 Vurderingsform Skriftlig eksamen Starttid 13.10.2017 09:00 Sluttid 13.10.2017 13:00 Sensurfrist -- PDF opprettet 21.09.2018 10:17 Opprettet av Digital

In addition, Angel is not involved in any regulated industry, accordingly, industry or regulatory factors are also not factors leading to the risk.

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) The risks of material misstatements at the financial statement level refer to risks of material misstatements that relate pervasively to the financial

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) The risks of material misstatements at the financial statement level refer to risks of material misstatements that relate pervasively to the financial

CHAPTER 8: INVENTORY

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

Financial Accounting Chapter 6 Notes Inventories

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Chapter 7: Merchandise Inventory

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

IFRS Training. IAS 2 Inventories. Professional Advisory Services

IFRS Training IAS 2 Inventories Table of Contents Section 1 Overview 2 Scope 3 Definitions 4 Measurement 5 Perpetual Versus Periodic 6 Cost Formulas 7 Net Realizable Value 8 Recognition 9 Disclosure Section

IFRS Training IAS 2 Inventories Table of Contents Section 1 Overview 2 Scope 3 Definitions 4 Measurement 5 Perpetual Versus Periodic 6 Cost Formulas 7 Net Realizable Value 8 Recognition 9 Disclosure Section

CHAPTER 2 THEORETICAL FOUNDATIONS

CHAPTER 2 THEORETICAL FOUNDATIONS This chapter covered the theoretical foundation used in the analysis and implementation process of this thesis. The main terms and concepts that are covered in this section

CHAPTER 2 THEORETICAL FOUNDATIONS This chapter covered the theoretical foundation used in the analysis and implementation process of this thesis. The main terms and concepts that are covered in this section

IAASB Agenda Item (September 2008) Page Agenda Item (MARKED FROM EXPOSURE DRAFT)

Page Agenda Item (MARKED FROM EXPOSURE DRAFT)") IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED

IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED

6) Items purchased for resale with a right of return must be presented separately from other inventories.

Items purchased for resale with a right of return must be presented separately from other inventories.") Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

CHAPTER 2 QUESTIONS (1) (1) (2) (3)

(1) (2) (3)") CHAPTER 2 QUESTIONS 1. The two major objectives of materials control are (1) physical control or safeguarding the materials and (2) control of the investment in materials. 2. The controls established for

CHAPTER 2 QUESTIONS 1. The two major objectives of materials control are (1) physical control or safeguarding the materials and (2) control of the investment in materials. 2. The controls established for

Institute of Chartered Accountants of India. Standards on Auditing

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

Financial Statement Close Process

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

Special Audit Techniques. CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

Special Audit Techniques CA Final Paper 3: Advanced Auditing & Professional Ethics Chapter 5 CA Arijit Chakraborty 2 Agenda for discussion - Special Audit Techniques Audit evidence -Confirmation, inquiry,

ACCA Certified Accounting Technician Examination Paper T8 (INT) Implementing Audit Procedures (International Stream)

Implementing Audit Procedures (International Stream)") Answers ACCA Certified Accounting Technician Examination Paper T8 (INT) Implementing Audit Procedures (International Stream) December 2010 Answers Section A NOTES Part Answer See Note Below 1 C 1 2 D 2

Answers ACCA Certified Accounting Technician Examination Paper T8 (INT) Implementing Audit Procedures (International Stream) December 2010 Answers Section A NOTES Part Answer See Note Below 1 C 1 2 D 2

evidence explained Chapter 6 The search for

Chapter 6 The search for evidence explained Learning objectives Explain why the audit evidence search is a central concept of auditing. Identify the stages of the audit process and show that evidence has

Chapter 6 The search for evidence explained Learning objectives Explain why the audit evidence search is a central concept of auditing. Identify the stages of the audit process and show that evidence has

PERFORMANCE MEASUREMENT TOOLS 5

PERFORMANCE MEASUREMENT TOOLS 5 Inventory Management 1 INVENTORY MANAGEMENT 5 INVENTORY MANAGEMENT CONTENTS About Stitch Diary and Mausmi... 1 Introduction... 2 Monthly Inventory Value... Inventory Turnover...

PERFORMANCE MEASUREMENT TOOLS 5 Inventory Management 1 INVENTORY MANAGEMENT 5 INVENTORY MANAGEMENT CONTENTS About Stitch Diary and Mausmi... 1 Introduction... 2 Monthly Inventory Value... Inventory Turnover...

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES 1 RELATIONSHIP BETWEEN TESTS OF CONTROLS AND SUBSTANTIVE TESTS OF TRANSACTIONS Most controls built around transaction flows. Tests of controls:

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES 1 RELATIONSHIP BETWEEN TESTS OF CONTROLS AND SUBSTANTIVE TESTS OF TRANSACTIONS Most controls built around transaction flows. Tests of controls:

Performance Measurement Tools INVENTORY MANAGEMENT

Performance Measurement Tools 5 INVENTORY MANAGEMENT 5 INVENTORY MANAGEMENT CONTENTS About Stitch Diary and Mausmi... 1 Introduction... 2 Monthly Inventory Value... Inventory Turnover... 3 5 Obsolete Inventory

Performance Measurement Tools 5 INVENTORY MANAGEMENT 5 INVENTORY MANAGEMENT CONTENTS About Stitch Diary and Mausmi... 1 Introduction... 2 Monthly Inventory Value... Inventory Turnover... 3 5 Obsolete Inventory

Materiality and Risk. Chapter Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/Elder

Materiality and Risk Chapter 9 9-1 Learning Objective 1 Apply the concept of materiality to the audit. 9-2 Materiality The auditor s responsibility is to determine whether financial statements are materially

Materiality and Risk Chapter 9 9-1 Learning Objective 1 Apply the concept of materiality to the audit. 9-2 Materiality The auditor s responsibility is to determine whether financial statements are materially

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 520

520") Issued 07/11 Compiled 11/13 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 520 Analytical Procedures (ISA (NZ) 520) This compilation was prepared in October 2013 and incorporates amendments up to and

Issued 07/11 Compiled 11/13 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 520 Analytical Procedures (ISA (NZ) 520) This compilation was prepared in October 2013 and incorporates amendments up to and

Chapter 9: Inventories. Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules

Chapter 9: Inventories Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules 1 Characteristics of Inventories belong to current assets

Chapter 9: Inventories Raw materials and consumables Finished goods Work in Progress Variants of valuation at historical cost other valuation rules 1 Characteristics of Inventories belong to current assets

AUDITING MOBILE MONEY AND ELECTRONIC TRANSACTIONS Presentation by:

AUDITING MOBILE MONEY AND ELECTRONIC TRANSACTIONS Presentation by: Moses Kang ethe Chief Finance Officer, Britam Life Assurance Company (Kenya) Limited Thursday, 1 st February 2018 Uphold public interest

AUDITING MOBILE MONEY AND ELECTRONIC TRANSACTIONS Presentation by: Moses Kang ethe Chief Finance Officer, Britam Life Assurance Company (Kenya) Limited Thursday, 1 st February 2018 Uphold public interest

OFFICE OF FINANCIAL MANAGEMENT & BUDGET (OFMB) June 12, 2018 June 12, 2018

June 12, 2018 June 12, 2018") TO: FROM: PREPARED BY: SUBJECT: PPM #: ALL COUNTY PERSONNEL VERDENIA C. BAKER COUNTY ADMINISTRATOR OFFICE OF FINANCIAL MANAGEMENT & BUDGET (OFMB) INVENTORY OF PARTS & SUPPLIES CW-F-059 ISSUE DATE EFFECTIVE

TO: FROM: PREPARED BY: SUBJECT: PPM #: ALL COUNTY PERSONNEL VERDENIA C. BAKER COUNTY ADMINISTRATOR OFFICE OF FINANCIAL MANAGEMENT & BUDGET (OFMB) INVENTORY OF PARTS & SUPPLIES CW-F-059 ISSUE DATE EFFECTIVE

3/29/15. Module 3: Audit objectives, evidence, procedures, and documentation

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Inventory Cost Accounting Tips and Tricks. Nick Bergamo, Senior Manager Linda Pei, Senior Manager

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

FOCUS ON PRACTICE INSPECTION FINDINGS

June 2006 To: All practising offices Background FOCUS ON PRACTICE INSPECTION FINDINGS 2005-2006 The practice inspection committee reviews the annual inspection results to identify those areas where adherence

June 2006 To: All practising offices Background FOCUS ON PRACTICE INSPECTION FINDINGS 2005-2006 The practice inspection committee reviews the annual inspection results to identify those areas where adherence

Chapter 2 An Introduction to Cost Terms and Purposes

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Study Unit 10. Inventories (IAS 2)

") Study Unit 10 Inventories (IAS 2) IAS 2: Inventories SUMMARY STANDARD ON A PAGE (SOAP) IAS 2 Inventories Held for sale in ordinary course of business In the process of production for such sales To be consumed

Study Unit 10 Inventories (IAS 2) IAS 2: Inventories SUMMARY STANDARD ON A PAGE (SOAP) IAS 2 Inventories Held for sale in ordinary course of business In the process of production for such sales To be consumed

The Auditor s Responses to Assessed Risks

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

SINGAPORE STANDARD SSA 330 ON AUDITING The Auditor s Responses to Assessed Risks SSA 330, The Auditor s Responses to Assessed Risks superseded SSA 330, The Auditor s Procedures in Response to Assessed

AT Assertions, Audit Procedures and Audit Evidence Red Sirug Page 1

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom)

Foundations in Audit (United Kingdom)") Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Audit Risk Assessment

SELF-STUDY CONTINUING PROFESSIONAL EDUCATION Companion to PPC s Guide to Audit Risk Assessment (800) 231-1860 cl.thomsonreuters.com 2017 Thomson Reuters/Tax & Accounting. Thomson Reuters, Checkpoint, PPC,

SELF-STUDY CONTINUING PROFESSIONAL EDUCATION Companion to PPC s Guide to Audit Risk Assessment (800) 231-1860 cl.thomsonreuters.com 2017 Thomson Reuters/Tax & Accounting. Thomson Reuters, Checkpoint, PPC,

International Standard on Auditing (UK) 501

501") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 501 Audit Evidence Specifi c Considerations for Selected Items The FRC s mission is to promote

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 501 Audit Evidence Specifi c Considerations for Selected Items The FRC s mission is to promote

SOLUTIONS. Learning Goal 18

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

Implementation Tool for Auditors

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Endunamoo BCTA Support Course (BCTA2018)

") Endunamoo BCTA Support Course (BCTA2018) AUE3702: Formulating Substantive Procedures: Cycles Khanyisile Mthethwa Introduction The Code of Professional Conduct, By-Laws and rules regarding improper conduct

Endunamoo BCTA Support Course (BCTA2018) AUE3702: Formulating Substantive Procedures: Cycles Khanyisile Mthethwa Introduction The Code of Professional Conduct, By-Laws and rules regarding improper conduct

Oracle Supply Chain Management Cloud Subject Areas for Transactional Business Intelligence in SCM 19A

Oracle Supply Chain Management Cloud for Transactional Business Intelligence in SCM 19A Release 19A Part Number: F11439-01 Copyright 2018, Oracle and/or its affiliates. All rights reserved This software

Oracle Supply Chain Management Cloud for Transactional Business Intelligence in SCM 19A Release 19A Part Number: F11439-01 Copyright 2018, Oracle and/or its affiliates. All rights reserved This software

Al al-bayt UNIVERSITY Faculty of Finance and Business Administration - Accounting Department

1 Al al-bayt UNIVERSITY Faculty of Finance and Business Administration - Accounting Department Advanced Auditing and Financial Control- Course No. (504751) - Credit Hours: 3 (MSc. Level) First semester:

1 Al al-bayt UNIVERSITY Faculty of Finance and Business Administration - Accounting Department Advanced Auditing and Financial Control- Course No. (504751) - Credit Hours: 3 (MSc. Level) First semester:

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

Week 4 Chapter 4 MATERIALS COSTING. FNSACC507A Provide Management Accounting Information

Week 4 Chapter 4 MATERIALS COSTING FNSACC507A Provide Management Accounting Information In this lesson you will learn 1. About the documents used to cost and control factory materials. 2. How to prepare

Week 4 Chapter 4 MATERIALS COSTING FNSACC507A Provide Management Accounting Information In this lesson you will learn 1. About the documents used to cost and control factory materials. 2. How to prepare

When formulating an audit procedure, one should remember that you need to have 3 following elements in the test of control:

Audit Procedure/Test of controls What is an audit procedure? Audit procedures aim to satisfy audit objectives. The audit procedure helps the auditor to determine whether the control is working as intended

Audit Procedure/Test of controls What is an audit procedure? Audit procedures aim to satisfy audit objectives. The audit procedure helps the auditor to determine whether the control is working as intended