Opportunities and Outlook for the Shipping Markets

|

|

|

- Grant Harris

- 5 years ago

- Views:

Transcription

8 th Capital Link Greek Shipping Forum 15 th")

1 Opportunities and Outlook for the Shipping Markets James Frew - Maritime Strategies International (MSI) 8 th Capital Link Greek Shipping Forum 15 th February 2017

2 Agenda Outlook and opportunities 1. Sector Correlations 2. Demand outlook 3. Supply side 4. Price Drivers 5. Recovery? Maritime Strategies International 2

3 Outlook and opportunities Sector correlations Maritime Strategies International

4 Shipping a correlated industry 1) 2) 3) 4) 5) 6) 1) Containerships 2) Bulkers 3) Tankers 4) Chems 5) LPG 6) OSV 7) Drilling Rig >75% Correlated >50% Correlated <50% Correlated Negatively Correlated Commodity shipping sectors well correlated with each other, but not offshore and LPG Maritime Strategies International 4

5 Demand only explains part of the story 1) Crude Oil 2) Product 3) Chemicals 4) LPG 5) LNG 6) Bulker 7) Container 8) PCTC 9) Cruise 10) AHTS >75% Correlated >50% Correlated 1) 2) 3) 4) 5) 6) 7) 8) 9) 10) <50% Correlated Negatively Correlated Most sectors are positively correlated, but not tightly so Maritime Strategies International 5

6 It is supply that is wrecking the markets Supply Supply Supply Supply Maritime Strategies International 6

7 Outlook and opportunities Demand Maritime Strategies International

8 Headline Trade Ratio has Stalled Tradewinds, May 26 th 2016 Maritime Strategies International 8

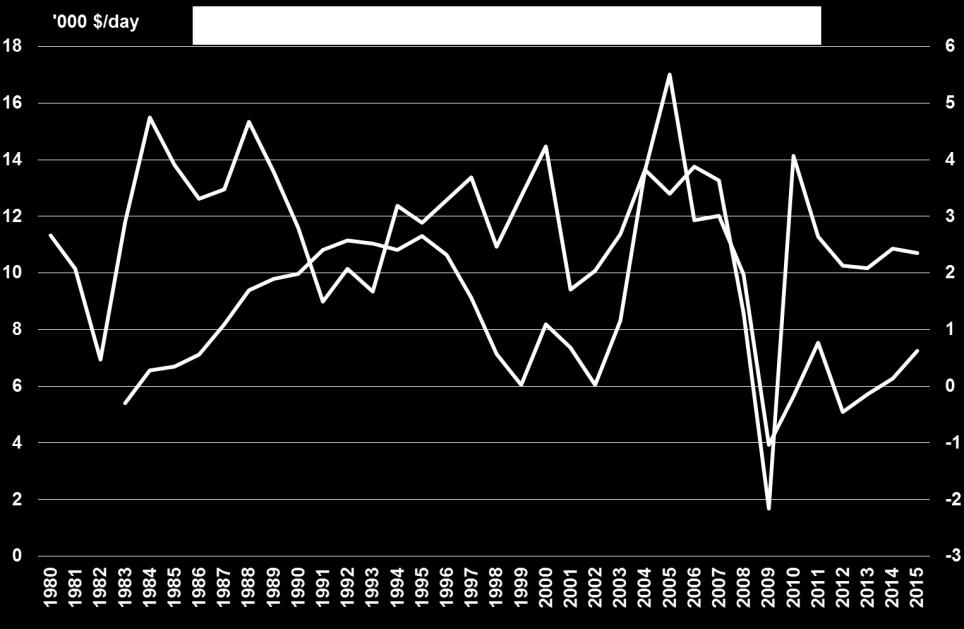

9 And the container trade/gdp multiplier has broken down? 6% YoY Ch Trade/GDP Multiplier 9 5% Global GDP "Multiplier" (RH Axis) 8 4% 7 3% 6 2% 5 1% 4 0% 3-1% 2-2% 1-3% 0 Maritime Strategies International 9

10 Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Year 11 Year 12 Recovery from recessions 120 Trade to GDP ratio, Year 0 = Maritime Strategies International 10

11 The bigger picture 70% Trade as a %age of Global GDP Cyclical? 60% 50% 40% Structural Cyclical 30% 20% 10% 0% Maritime Strategies International 11

12 Outlook and opportunities Supply Maritime Strategies International

13 Bulker 2003 Bulker 2008 Bulker 2016 Tanker 2003 Tanker 2008 Tanker 2016 Orderbook/Fleet ratio looking good?? 80% Orderbook to fleet ratio 70% 60% 50% 40% 30% 20% 10% 0% Maritime Strategies International 13

14 How Many Ships? Routes Distance Speed Waiting/Port Time Operating Days Ballast Ratio Carrying Capacity Size Changes Maritime Strategies International 14

15 Bulker 2003 Bulker 2008 Bulker 2016 Tanker 2003 Tanker 2008 Tanker 2016 The key is the demand side 350 Mn Dwt Orderbook Incremental demand over following three years Maritime Strategies International 15

16 Bulker 2003 Bulker 2008 Bulker 2016 Tanker 2003 Tanker 2008 Tanker 2016 which doesn t look so good 400% 350% Ratio Orderbook to Fleet ratio Orderbook relative to vessel demand 300% 250% 200% 150% 100% 50% 0% Maritime Strategies International 16

17 Shipyard Capacity Is a Worry Mn CGT Other Europe China Korea Japan Maritime Strategies International 17

18 Yards Don t Just Disappear Yards have become ghost towns but haven't disappeared Maritime Strategies International 18

19 Shipyard Capacity Déjà Vu Mn CGT Other Europe China South Korea Japan Maritime Strategies International 19

20 Outlook and opportunities Price drivers Maritime Strategies International

21 What drives asset price formation? Maritime Strategies International 21

22 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Directional Analysis VLCC QoQ % Change NB Price 1 Yr TC Rate 5 Yr Price 40% 30% 20% 10% 0% -10% -20% -30% -40% Maritime Strategies International 22

23 Supramax Quarters where 2 nd hand price moves with NB price only Panamax Capesize MR Aframax VLCC Since 1990 # of Quarters 120 No Yes Maritime Strategies International 23

24 NB Price Outlook FC Pricing Power - YARD FC Pricing Power - OWNERS FC = forward cover Maritime Strategies International 24

25 Outlook and opportunities Recovery? Maritime Strategies International

26 MSI - FMV MSI Forecast Marine evaluator (FMV) is the first web-based tool to provide forecast and historical price data covering virtually all of the deepsea shipping fleet. Data includes forecasts of newbuilding, second-hand prices, 1 year timecharter rates and operating costs for specific vessels. MSI FMV draws on MSI s proven, proprietary models and a consistent cross-sectional view across all principal shipping sectors. It puts asset values in the context of the near term market to enable reliable benchmarking with outputs based on annual averages. Coverage: Crude Oil Tanker Chemical Tanker Multi Purpose Product Oil Tanker LPG Carrier Containership Dry Bulk Carrier LNG Carrier PCC/PCTC AHTS /fmv PSV Maritime Strategies International 26

27 FMV Output Quarterly Fair Market Value & 1 Year Time Charter Rate (1Q history, current Q, 2Q forecast Annual average: Newbuilding contract price Fair Market Value 1 Year Time Charter Rate Operating Cost 5 years history and 15 years forecast Price Development Chart detailing forecast price development in relation to historical metrics /fmv Maritime Strategies International 27

28 MR Tanker Supramax Bulker Handy Containership DFDE LNG Small Anchor Handler Asset play opportunities 20% 18% 16% 14% 12% 10% 8% 6% 4% 2% IRR (invest 2017, divest 2021) Contracting New (Deliv. 2019) Buying Secondhand (5 Yr Old) 0% Maritime Strategies International 28

29 MR Tanker Supramax Bulker Handy Containership DFDE LNG Small Anchor Handler Asset play timespan 30% 25% 20% IRR by year of divestment % 10% 5% 0% Maritime Strategies International 29

30 Thank you for listening Maritime Strategies International 30

31 MSI Background For over 30 years, MSI has developed integrated relationships with a diverse client base of financial institutions, ship owners, shipyards, brokers, investors, insurers and equipment and service providers. MSI s expertise covers a broad range of shipping sectors, providing clients with a combination of sector reports, forecasting models, vessel valuations and bespoke consultancy services. MSI is staffed by economists and scientists offering a structured quantitative perspective to shipping analysis combined with a wide range of industry experience. MSI balances analytical power with service flexibility, offering a comprehensive support structure and a sound foundation on which to build investment strategies and monitor/assess exposure to market risks. Maritime Strategies International 31

32 Disclaimer While this document has been prepared, and is presented, in good faith, Maritime Strategies International assumes no responsibility for errors of fact, opinion or market changes, and cannot be held responsible for any losses incurred or action arising as a result of information contained in this document. The copyright and other intellectual property rights in data, information or advice contained in this document are and will at all times remain the property of Maritime Strategies International. Maritime Strategies International 32

207 940 0070 Fax: +44 (0)207 940 0071 Email:")

33 Maritime Strategies International Ltd 6 Baden Place Crosby Row London SE1 1YW United Kingdom Tel: +44 (0) Fax: +44 (0) info@msiltd.com