Agenda. Sector Trends Company Overview Thesis Risks Valuation Q&A Wendy s/arby s Group (WEN) Rachel Nabatian Will Zhang Mayank Vidyarthi

|

|

|

- Howard Williams

- 5 years ago

- Views:

Transcription

Rachel Nabatian Will Zhang Mayank")

1 Agenda Sector Trends Company Overview Thesis Risks Valuation Q&A Wendy s/arby s Group (WEN) Rachel Nabatian Will Zhang Mayank Vidyarthi

2 Sector Overview Company Overview Thesis Risks DCF Agenda

3 Sector Overview and Trends Customers increasingly price-sensitive Unemployment, underemployment remain high Wealth destruction, increased savings rate Conditions strongly favor lower-cost dining Quick-service restaurants offer best value Magic $5 price point Meals for $5 or less (e.g. Subway $5 Footlongs)

4 Competition

5 Overview: Wendy s Known for square burgers Wendy s 99 Menu Historically low margins (around ~11% vs. Industry avg. of 17%) Margin Improvement Plan Ahead of Schedule Average ticket is $4

6 Overview: Arby s Specializes in premium roast beef sandwiches Unique among QSR s Historically had high average ticket $7.50 vs. under $5 for typical QSR s Historical margins in line with industry average (~17%)

7 Revenue Breakdown by Operating Segment 8% 2% Wendy's Company-Owned 31% 59% Arby's Company- Owned Wendy's Franchises Arby's Franchises

8 Sources of Revenue 1.9% 8.2% 0.18% Delivery of food Bakery items and kid s meal Royalty income from franchisees Rental income 89% Startup franchise fees

9 Thesis Merger = Turnaround Wendy s increasing margins Arby s offering more value Macroeconomic Trends Favor QSR s Over Casual Dining Outlets Short and Long-Term Growth Catalysts DCF

10 Reasons for Merger Wendy s underperformance since 2002 Founder Dave Thomas died in 2002 Wendy s historically low operating margins Poor cost control High breakfast item costs Lack of coherent marketing message Thomas was instrumental in Wendy s advertisements Arby s benefits from Wendy s large size

11 Triarc Acquires Wendy s Initiated by Nelson Peltz Triarc board member Well known in the food industry with turnarounds for Snapple Kraft Cadbury Schweppes Heinz Held 10% of Wendy s shares

12 Merger Details Completed on September 28, 2008 All-stock transaction Wendy s shareholders received 4.25 shares of Wendy s/arby s common stock for each Wendy s share Triarc renamed to Wendy s/arby s Group Triarc CEO Roland Smith becomes CEO of Wendy s/arby s

13 The Turnaround Artist Roland Smith, President and Chief Executive Officer Turnaround Experience Arby s, 1994 to 1999 Tripled op. profit from 1996 to 1998 Industry leader same store sales growth American Golf, 2003 to 2005 Grew revenue and profits 38% IRR to investors AMF, 1999 to 2003 Out of Chapter 11 Reduction of total debt by two-thirds Positive comp sales growth

14 Gets it done The Turnaround Artist Went to West Point U.S. Army for seven years Platoon leader Executive officer Deputy director of Army programs Aide-de-camp Aviation maintenance officer Pilot

15 First there was Wendy s

16 Then there was Arby s

17 And they formed the Wendy s/arby s Group

18 The Turnaround Combining best practices Margin-focused turnaround at Wendy s Goal: Improve operating margins from 11.7% in 2008 to 16.7% by 2011 Value-focused SSS turnaround at Arby s Goal: Increase SSS by providing value-based menu offerings Merger synergies $60 M target G&A Savings

19 Key projects: G&A Savings Integrating Shared Services Center IT systems integration Achieved $25M in cost savings in 2008 On pace to achieve $10M - $25M savings in 2009

20 Wendy s: Impressive Margin Improvements Target: 500 bp operating margin improvement by bp improvement from Q2 '08 to Q2 '09 Commodities were flat over this period from hedging Margins were 15.9% in Q2 '09, back to levels not seen since early 2000 s

21 Already at 15.9%, well above % target

22 Margin Improvement Areas Tighter control of controllable costs Labor hours Wasted food (Actual cost theoretical cost) Utilities Higher same-store sales from new menu items, promotions, marketing campaigns

23 Arby s: Strategic Shift to Value-Based Menu Initiatives aimed at repeat customers Comprise 50% of sales 1 extra visit each year = 3% SSS improvement Offering more value items July: $5 BBQ Bacon Cheddar Roastburger 1.1% SSS increase from June to July

24 Arby s: Premium Products For Great Value Starting in Q4: $5 premium roast beef sandwich combos Full-sized sandwich + Fries + Drink = $5.01 Premium quality: Worth every penny August promotion: 5 for $5 Family & Friends Feast: 5 Roast Beef Sandwiches for $5 ($1 each)

25

26 Arby s: Improving Value Improving Same-Store Sales Coming October 09: Introduction of $5 Combo Meals July 09: BBQ Bacon Cheddar Roastburger Combo Promotion $7.50 $5 Average Arby s Meal Price

27 Wendy s: New Menu Items Boneless chicken wings introduced in June 2.0% increase in same-store sales in July Premium Bacon Deluxe cheeseburger to be introduced in Q4 2009

28 But aren t all these turnaround benefits already priced in?

29 But aren t all these turnaround benefits already priced in? To answer your question, Doug, no! Trading at acquisition values Does include the predicted synergies of $60M Does not include: Organic op. margin improvements which are ahead of schedule Arby s dramatic SSS improvement Cost savings beating everyone s expectations, beyond predicted $60M

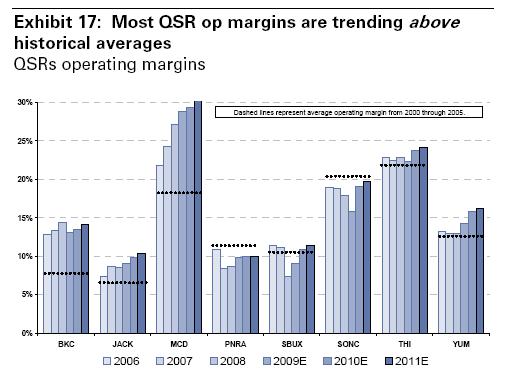

30 Wendy s: Quality Products It's waaay better than fast food... It's Wendy's.

31 Casual Dining vs. QSRs Casual Dining Cheesecake factory Applebee s P.F. Chang s Denny s QSR s Wendy s Arby s McDonald s Burger King Chipotle Panera Taco Bell

32 QSR s Are Undervalued Compared to Casual Dining Casual dining trading above year-ago levels Short interest as % of Share Float: QSR s: 4% Casual Dining:17% High-growth for casual dining = riskier

33 QSR s: Still Undervalued

34

35

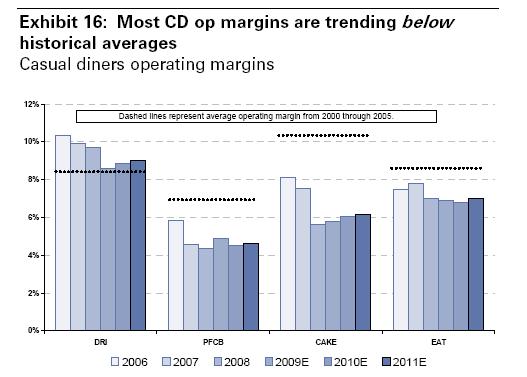

36 Deteriorating SSS for Casual Dining

37 Casual Dining Supply > Demand

38 QSR s Show Strong Margins WEN achieved good margins in Q2 09, despite weak performance of Casual Dining Restaurants

39 Short-Term Catalysts Improving operating margins at Wendy s Value-driven same-store sales growth at Arby s New menu item launches at Wendy s $50M stock buyback plan

40 Breakfast Long-Term Catalysts Testing phase in select stores International stores 135 stores in Middle East and N. Africa franchised by Al Jammaz Group to open over next decade Dual-branded stores 3 test stores to open in Atlanta in early 2010 New brand under consideration $565 million bond offering in June

41 Wendy s/arby s International Presence

42 Comps Current EV/EBITDA: 7x CY10 discount to its group at 8x

43 EBITDA Increase 2Q09: EBITDA of $117.2M Exceeded consensus est. of $110M Result of better than expected Wendy s margin gains Future EBITDA increase resulting from Decreased labor costs from synergies Central purchasing unit

44 Potential Risks RISKS Competition Turnaround fails Commodity volatility impacts input costs Vegetarianism/PETA Increases in minimum wage MITIGANTS Turnaround, dual branding, value rebranding, management team Already ahead of schedule, management team WEN engages in hedging through forward contracts PETA campaign focused mostly on McDonalds Will affect entire industry, so overall market share should not be affected

45 Q