Consumer behavior at the convergence point Irena Yankova, GfK Bulgaria

|

|

|

- Marybeth Wheeler

- 5 years ago

- Views:

Transcription

1 1 Consumer behavior at the convergence point Irena Yankova, GfK Bulgaria

2 Factors influence Consumer s behavior 2 Mobility Purchasing power Arrangement Communication Variaty Special offers

3 Economic market dynamics 3

4 2010: a year of stabilization Real GDP (in %, BGN) GPD +0.2% Inflation Rate 12.5 Inflation +4.5% Source: National Statistical Institute-Bulgaria

9.9 10.3 10.1 10.0 9.5 9.3 9.2 9.1 9.")

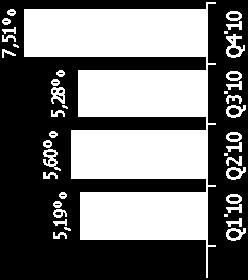

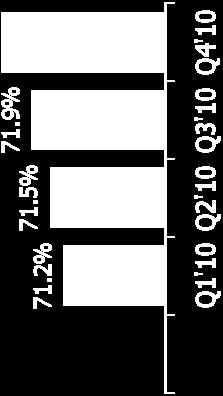

5 2010: Unemployment rate growth has been stoped 2010: Net Wages keep on growing 5 Unemployment Rate % Unemployment Rate (%) I'09 II'09 III'09 IV'09 V'09 VI'09 VII'09 VIII'09 IX'09 X'09 XI'09 XII'09 I'10 II'10 III'10 IV'10 V'10 VI'10 VII'10 VIII'10 IX'10 X'10 XI'10 XII'10 Monthly Net Wages BGN Average net wages, in BGN Quarterly 1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09 3Q'09 4Q'09 1Q'10 2Q'10 3Q'10 4Q' Source: National Statistical Institute-Bulgaria

6 Personal consumption: a year of compromises 2010 vs Food 0,4 Decrease of the overall households 6 Beverages & Tabacco -3,9 consumption in value in 2010 compared to Clothing & footwear Fuel&Power -9,1-2,6 Bulgarian households increased their spending on food, health and personal care, communication. Household equipment&operation Health & personal care Transport Communication -9,2 2,1-1,2 1,9 Contrary to the food basket, a significant decrease was observed within the clothing and footwear, household equipment and operation and education, entertainment, sport and recreation baskets. Education,entertainment,sport,recreation -11,3 Other goods and services 1,7 Source: National Statistical Institute-Bulgaria

7 After reaching its lowest level in February 2010, Consumer confidence index has been increasing during the last months Index % 10 7 Better Consumer Confidence Index 0 Same Worse Source: GfK Bulgaria - Confidence Barometer December 2010 (N= 1000 respondents)

8 Bulgarian Households expectations 8 What are your household s financial expectations for the upcoming 12 months? Better*: 12% About the same: 41% Worse*: 34% Do you intend to buy more, the same or less durables in the next 12 months? More**: 12% The same: 15% Less**: 44% Source: GfK Bulgaria - Confidence Barometer December 2010 (N= 1000 respondents) no opinion does not appear *: will get much better/get somewhat better - *: get somewhat worse/get much worse *8: much more/more - **: somewhat less/much less

9 Financial situation of Bulgarian Households 9 What is your household s present financial situation? 1% We save considerably 15% We save a bit 63% We can barely make ends meet 4% We have to touch regularly our savings 8% We need to borrow in order to cope Source: GfK Bulgaria - Confidence Barometer December 2010 (N= 1000 respondents) no opinion does not appear

10 The Bulgarian households are looking for the best products and the lowest price 10 Factors influencing the choice of a main shopping place Shopping behavior for food and FMCG What is essential What is more and more important Range of products + Price Freshness, Quality Visibility of Level + + of price labels products Presence of branded products What is not so important Possibility to pay without cash Services Source: GfK Bulgaria Shopping Monitor 2011 Shopping Conditions Factors influencing the choice of a main shopping place

11 GfK Bulgaria Consumer behavior at the convergence point, Irena Yankova June 2011 Mobility 11

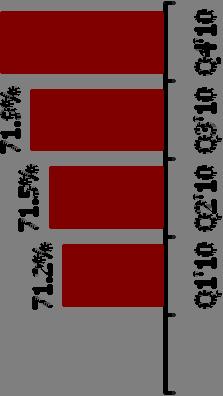

12 An other catalyst of the changes in the shopping habits.. Using a car for food shopping % 14.8% 16.5% Yes, very often 80% 15% 19% Yes, sometimes, for bigger shopping 60% 12.7% 13.5% Exceptionally 40% 18.6% 19.6% No, do not see why 20% 38.0% 31.8% No, we have no car 0% Total 2009 Total 2010 Source: GfK Bulgaria Shopping Monitor 2011 Selected aspects of shopping behaviour

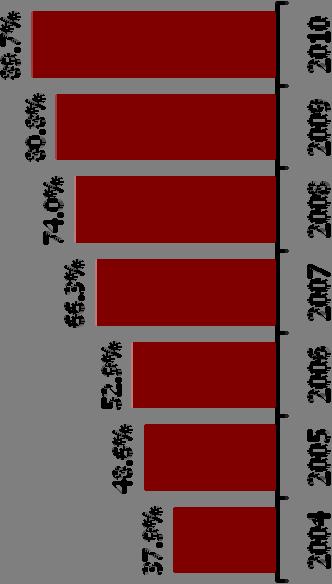

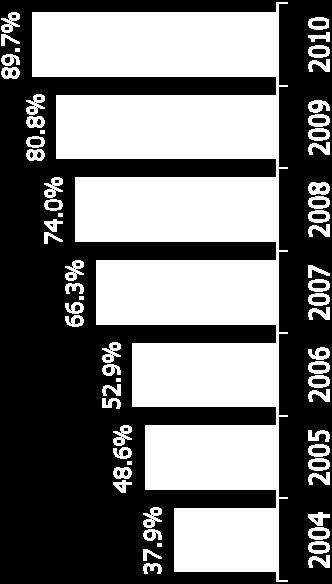

13 Virtual mobility 13 Level of internet penetration 41.7% 45.5% 47.9% 33.4% 28.1% Q2011 Source: GfK Bulgaria Omnibus survey, 15+ aged, n=12000 per year

14 Internet purchases 14 Clothing 40% Books/music/ DVD 38% Home delivery of food from restaurants 28% Flight tickets/holiday travel Entertainment and leisure time (e.g. cinema, tickets for concerts) 25% 25% Furniture, upholstered furniture or accessories for the home Financial services (e.g. insurance) Grocery products (e.g. yoghurt, sugar, chocolate products, drinks, detergents etc.) None of the above categories 4% 9% 13% 18% 22% 16% I can't touch the product, I can't check the quality of goods I don't have trust in this type of shopping, I can't see expiry date and package I don't purchase on-line 20% Source: GfK Bulgaria Online survey, Representative for online population, 15+ aged, n=2800

15 Internet purchases Propensity to do on-line shopping from super/hyper-markets 71% Deterrents 15 I would NOT use this service I would use this service 39% 62% 62% Cosmetics and personal hygiene products 55% Soft drinks and beer 52% Wine and spirit Source: GfK Bulgaria Online survey, Representative for online population, 15+ aged, n=2800

16 Main criteria for choice of main shopping place 1 st : Proximity of home or workplace % 67% 16 2nd: Assortment range, great variety of goods 51% 56% 3rd: Convenient prices / good price in general 44% Discounts, price deductions 41% Source: GfK Bulgaria Shopping Monitor 2011 Preferred types of main shopping places criteria for the choice of main shopping place

17 17 Promotions and Privet Labels

18 Consumers Attitude to Leaflet Campaigns 100% I receive, read it and do shopping accordingly I receive and I read them I receive, but I do not read them I receive no leaflets I don't know 18 80% 51% 48% 63% 62% 59% 60% 11% 40% 12% 8% 9% 10% 29% 20% 23% 19% 26% 29% 0% 13% 8% 5% 6% 5% Source: GfK Bulgaria Shopping Monitor 2011

19 Share of promotions in household basket Promotional purchases share Consumption of categories in promotion % Milk&Yogurt Desserts 24.2% Special Cheese 22.1% Instant Coffee 18.2% % Salad Dressings 16.4% Chocolate&Sweet Bars 14.6% Processed Cheese 14.2% % Detergents 12.7% Hair Shampoos 12.1% Cappuccino&Mixtures 11.6% Juices 11.5% Ice Drinks 11.3% Source: GfK Consumer Tracking; based on Consumer Index category range; volume shares, period: January December 2010

20 Categories in promotional leaflets 20 Non-Food Food 38% 62% Source: GfK Bulgaria Leaflet Monitor, Promoted products in leaflets for period Jan-Dec 2010

21 Most often promoted products in Food categories Number of promoted products 21 Processed meat 7272 Chocolate&Sweet Bars Soft drinks Wine Canned fruit and vegetables Cheeses Stimulants for making drinks Fresh meat Fresh fruit and vegetables Milk and yoghourt Source: GfK Bulgaria Leaflet Monitor, Promoted products in leaflets for period Jan-Dec 2010

22 Most often promoted SUPPLIERS Food Number of promoted products 22 Nestle 1456 Kraft Foods Bella Food industry Danone 614 Sami-M 391 Boni Meggle Coca-Cola Co. 358 Deroni 336 Tandem 327 Source: GfK Bulgaria Leaflet Monitor, Promoted products in leaflets for period Jan-Dec 2010

23 Most often promoted products in Non-Food categories Number of promoted products 23 Body care 7272 Personal hygiene 3620 Detergents 3407 Hair care 3296 Cleaners 3173 Mouth hygiene 3019 Shaving, depilation 2320 Dishes Products for household use Face care Source: GfK Bulgaria Leaflet Monitor, Promoted products in leaflets for period Jan-Dec 2010

24 Most often promoted SUPPLIERS Non-Food Number of promoted products 24 Henkel 2382 P&G 1901 Ficosota Syntez 747 Beiersdorf 596 Unilever Reckitt Benckiser Colgate-Palmolive 315 Medea 302 Aroma 283 Rubella 267 Source: GfK Bulgaria Leaflet Monitor, Promoted products in leaflets for period Jan-Dec 2010

25 Private Labels How big is their piece of the pie? 25 Penetration Value shares (%) Source: GfK Consumer Tracking; based on Consumer Index category range

26 Private Labels top 20 categories with the highest* PL shares 26 *Ranking based on volume shares, Period: January December 2010

27 Private labels piece of the pie varies across the region Private Labels Branded Romania Slovakia 27 Poland Czech Republic Russia Hungary Croatia Bosnia & Herzegovina Serbia Bulgaria Source: GfK Consumer Tracking; Calculation based upon consumer basket including monitored product categories; Measure: value share (%); Period: January December 2010

28 Channels distribution 28

29 Source: GfK Consumer")

29 Share of distribution channels (% in value) 29 Source: GfK Consumer Tracking Measure: Household Consumption, based on measured FMCG basket;

I make only small purchases More than 50% of age group 50 + y.o I make only large purchases 13% of aged 20-29y.")

30 Behaviour at point of sale I make both small and large purchases More than 50% of aged 30-49y.o. 17 times Average monthly frequency of purchases Small purchases (avr. 10BGN) 30 47% 44% 9% 3.5 times Large purchases (avr. 70BGN) I make only small purchases More than 50% of age group 50 + y.o I make only large purchases 13% of aged 20-29y.o Source: GfK Bulgaria Shopping Monitor 2011, n=1000, Way and frequency of purchase

31 Preferred shopping place for selected food categories 31 Hypermarkets +supermarkets Superette+ Small convenient store Consumables, canned food 50% Confectionery Non-alcoholic drinks 48% 52% Sausages and fresh delicacy Detergents and cleaning Body care products 50% 45% 43% Beer Bread and pastry Fresh meat 46% 57% Open market, Specialized store 11% Fresh food and vegetables 22% Source: GfK Bulgaria Shopping Monitor 2011, n=1000, Preferred shopping place for selected categories

32 Behavior at point of sale 2009 vs I always tend to spend more than planned when grocery shopping 42% 48% I always have a look at other people's trolleys to check i have not forgotten anything 18% 27% I shop around to take advantage of special offers I like stores to have clear sign-posting and labelling to help me find my way around I think it is worth paying a bit more to shop at a store that i can get in and out of quickly 35% 45% 90% 91% 39% 45% Source: GfK Consumer Tracking

33 How to influence shopping behavior? 33 Better cooperation between retailers and producers in the point of sale Promotional activates and in store communication Category A Category B Promo 1 Category C Category D Category E Category F Category G Shelf organization and category management Promo 2 Promotion 3 Main Isle

34 34 Thank you for your attention! Growth from Knowledge