investment report Cardinal Health (CAH) business overview From cardinal healthe.com and Reuters.com competition

|

|

|

- Jeffrey Owens

- 5 years ago

- Views:

Transcription

1 investment report Cardinal Health (CAH) business overview From cardinal healthe.com and Reuters.com Cardinal Health, Inc. (Cardinal Health) Cardinal Health, Inc. (Cardinal Health) is a provider of products and services in the healthcare sector. Since its founding in 1971, sales have reached annual sales of $81 billion and its current position on the Fortune 500 is #19. The Company has four segments: Pharmaceutical Distribution and Provider Services; Medical Products and Services; Pharmaceutical Technologies and Services, and Clinical Technologies and Services. Two of the Company's five largest customers are CVS Corporation and Walgreens Co. This aggregate of five largest customers accounted for approximately 46% of Cardinal Health s revenue for the fiscal year of All of the Company's business with its five largest customers is included in its Pharmaceutical Distribution and Provider Services segment. Through this segment, Cardinal Health distributes pharmaceutical and other healthcare products. The Company's Pharmaceutical Distribution business is composed of full-service wholesale distributors of pharmaceutical and related healthcare products to customers in the U.S. including retail clients (these include chain and independent drug stores as well as the pharmacy departments of supermarkets), hospitals and alternate care providers (including mail order customers). Additionally through this segment, the Company provides distribution services to pharmaceutical manufacturers. Through the Medical Products and Services segment CAH distributes a wide variety of medical and laboratory products on behalf of roughly 2,000 suppliers. In addition CAH distributes its own brand of surgical and respiratory therapy products to hospitals and other healthcare providers. Cardinal Health is currently overseen by Robert D. Walter, its Chairman of the Board, and R. Kerry Clark, the President and Chief Executive Officer, who has been with Cardinal Health since April, competition competitor company description implications for CAH McKesson Based in San Francisco, McKesson Corporation (McKesson) provides supply, information and care management products and services. Through its Pharmaceutical Solutions segment, it is a distributor of drugs, and health and beauty care products. It also manufactures and sells automated pharmaceutical dispensing systems for retail pharmacies, and provides medical management, and specialty pharmaceutical solutions. Largest competitor, In May 2006, McKesson acquired HealthCom Partners LLC. In June 2006, the Company acquired RelayHealth Corporation.

2 Amerisource Bergen Owens & Minor Henry Schein Physician s Sales and Service Inc. financials AmerisourceBergen Corporation provides pharmaceutical services to pharmaceutical manufacturers and healthcare providers in the United States and Puerto Rico, and Canada. It distributes brand name and generic pharmaceuticals, over-the-counter healthcare products, and home healthcare supplies and equipment to various healthcare providers, including acute care hospitals and health systems, independent and chain retail pharmacies, mail order facilities, physicians, clinics, alternate site facilities, as well as nursing and assisted living centers. Owens & Minor, Inc. (O&M) is engaged in the distribution of national name-brand medical and surgical supplies, and is a healthcare supply chain management company. Its primary distribution customers are acute care hospitals and integrated healthcare networks (IHNs). IHN s are responsible for more than 90% of O&M's revenue. Henry Schein, Inc. is a distributor of healthcare products and services mainly to office-based healthcare practitioners in the North American and European markets. The Company functions in two business segments. The healthcare distribution segment consists of the Company's dental, medical (including veterinary) and international groups. The technology segment supplies software, technology and other value-added services to healthcare providers, primarily in the United States and Canada. A World Medical Company. The company functions in two segments, Physician Business and Elder Care Business. Competing for same diversified network of clients including physicians and clinics. Competitor more in area of distribution to acute care hospitals and IHNs Distributor focused on private practice physicians. During 2005 Co. acquired the dental products distribution business of Ash Temple Limited, and Demedis Group's business in Austria, which is managed by the Austrodent brand. Country s largest supplier of medical products to physician practices, emerging competitor with increase in Elder Care Business profits. income statement In fiscal 2006, Cardinal had record revenue of $81 billion, a 10 percent increase from fiscal This may be the result of growing demand for Cardinal s diversified products and services. At first glance, it seems as though Cardinal was taking a bath in fiscal The company was willing to have one really bad period and made up for it in fiscal The progress made to strengthen operations led to operating earnings growth of 8 percent to almost $2 billion, and diluted EPS from continuing

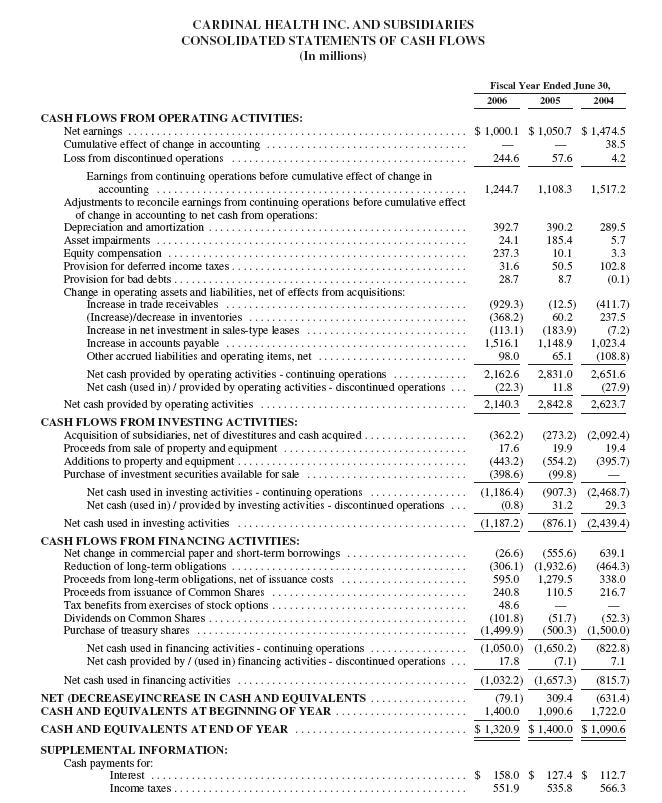

3 operations increased 14 percent to $2.90. That being said, net diluted earnings per common share dropped to $2.33. balance sheet Two things jump out immediately upon looking at the balance sheets. First, there was a jump in shortterm investments available for sale. In fiscal 2006, short-term investments increased almost 500%. Cash used in investing activities during fiscal 2006 primarily represents the Company s purchase of $398.6 million of short-term investments classified as available for sale and capital spending of approximately $443.2 million to develop and enhance the Company s infrastructure. In addition, during fiscal 2006, the Company used cash of approximately $362.2 million to complete acquisitions which expand its role as a provider of services to the healthcare industry. All of the investments have ratings of at least AAA. During fiscal 2006, accounts payable increased approximately $1.5 billion, which was partially offset by increased inventories of $368.2 million and increased accounts receivable of approximately $929.3 million during this period. Second, the accounts payable and related receivable and inventory increases are due to the new sales volume from an existing large retail chain customer and the timing of inventory purchases from vendors in the Pharmaceutical Distribution and Provider Services segment. cash flow Net earnings remained somewhat stagnant. Further research would help clarify the reason. Across all segments, Cardinal made progress to focus and optimize its business portfolio. The company divested several assets that were not strategic to its long-term direction and completed several small acquisitions that broaden its capabilities for a particular market. Thus, Cardinal returned up to 50 percent of its operating cash flow to shareholders by repurchasing $1.5 billion of its shares and increasing its dividend by 50 percent. On November 30 th 2006, Cardinal Health announced plans to divest its Pharmaceutical Technologies and Services (PTS) segment. The company said the decision was made to focus Cardinal Health's capabilities and resources to better serve health-care provider customers, such as hospitals and pharmacies. Like before, the company expects to use the proceeds to repurchase Cardinal Health shares. In anticipation, the board has initially authorized an additional $1 billion, bringing the company's total repurchase authorization to almost $3 billion for fiscal 2007 and To date in fiscal 2007, the company has purchased approximately $500 million in shares and plans to complete a total of $1.5 billion by the end of fiscal At Sept. 30, 2006, Cardinal had approximately $2.0 billion in cash and $1 billion available under its bank revolvers. While this divestiture will make Cardinal's business less diverse, the company will continue to generate strong cash flow. valuation In the past ten years, the CAH stock has reflected market trends. Over the past five years, however, it has had low returns. The stock has had a high P/E ratio of 42.2 and a low of 20.2, during the past ten years. The lower P/E ratios signify an increase in EPS. Currently the ratio is 21.2 compared to the industry s average of 22.8 and the S&P 500 at To get the future P/E ration we can use the EPS of 2007 and 2008 fiscal years, with the current stock price. The resulting ratios are 18.1 and 15.5 respectively. When calculating the EPS growth over a three year period, we can see that CAH has a larger expected growth rate of 17% compared to MCK s 14 % and ABC s 12%, their top competing companies. Looking at the market cap, CAH falls under the large market cap category and makes up a

4 big fraction of the health industry. The stock s current price is 65.54, which is substantially expensive compared to its competing companies Mckesson and ABC, whose prices are and respectively. The high price could be due to the higher growth rate expected in the future, as previously explained. Valuation Ratios Stock Industry S&P 500 Stock's 5Yr Average* Price/Earnings Price/Book Price/Sales Price/Cash Flow Dividend Yield % * Price/Cash Flow uses 3-year average. investment opportunities good relationship with primary suppliers (pharmaceutical drugs) The Company obtains its products from many different suppliers, the largest of which, Pfizer Inc., accounted for approximately 9% (by dollar volume) of the Company s revenue in fiscal The Company s five largest suppliers accounted on a combined basis for approximately 33% (by dollar volume) of the Company s revenue during fiscal Overall, the Company believes that its relationships with its suppliers are good. Pfizer, Inc. spends $7 billion annually on pharmaceutical research and development, and CAH s earnings have also been dampened by this huge sum, but Pfizer has been successful in distributing wildly successful drugs such as the cholesterol medicine, Lipitor (the world s best-selling drug), and the antidepressant Zoloft. While the patents on some of these drugs will expire fairly soon, Pfizer, Inc. is developing new medicines, such as new good cholesterol medicine, which should be popular. Cardinal Health reported strong growth in generics in the past quarter, due to not only the introduction of new drugs, but also to strategic sourcing.. In addition, pharmaceutical price increases for the trailing twelve month period of approximately 5.6% contributed to the revenue growth in this segment. While Cardinal Health depends largely on its suppliers, the relationships appear to be stable (despite Pfizer s looming patent expirations), and Cardinal Health s suppliers are more diverse than its consumers. Note: new products that have been added recently besides pharmaceutical drugs include: respiratory products, new (latex-free!) gloves, converters and oral technologies.

5 Canadian medical distribution One of the pharmaceutical industry's fastest growing segments is so-called reimportation sites, which allow people to buy essential pharmaceuticals at lower prices from foreign countries. Brand-name drugs purchased in Canada can typically cost 30% to 70% less than the same drugs purchased in the U.S. The healthcare industry s major participants include Cardinal Health, some of its competitors, and F. Dohmen Co. and ParMed Pharmaceuticals, two of the company s 2006 acquisitions. The F. Dohmen Co. and ParMed integration is progressing well, according to the company s recent reports, and it is likely that these new branches of the company have increased Canadian distribution growth. The main risk in this area is the political aspect of the Canadian drug trade; while growth is increasing now, new policy may turn this around. In addition, there has been strong growth in lab distribution businesses. management and customer service Cardinal s recent growth can also be attributed to efficient inventory management, improved customer service, and new sales organization. As of the first quarter, the days inventory on hand declined 2 days since last year. Customer service ratings have improved, as has product quality. Finally, the recent personnel changes look promising. On November 10 th, the company announced Mark Parrish the new CEO of the healthcare supply unit. Phillip L. Francis, chairman of PetSmart also recently joined the board, replacing a much older John F. Havens. high barriers to entry In the healthcare sector, barriers to entry tend to be high. There are high start-up costs, and often patent protections must be received before a company can begin work. There is significant product differentiation, so a new company would often have to make many purchases from different suppliers. In addition, there are long drug development cycles. Finally, billions of dollars go into research and development and only a company that is firmly established can afford it. This is a plus for CAH, which is already a leading healthcare provider. investment risks 5 Customers account for half of revenue; low pricing power Cardinal Health s five largest customers account for just under half of its total revenue (46%). The two largest customers are CVS (which accounts for 21% of revenue) and Walgreens (14% of revenue). Because they are depending on very few customers for a large portion of their revenue, this can be dangerous because losing one or both of these customers can strongly affect operations and the company s financial state. Also, because its two largest customers, CVS and Walgreens, are high profile companies, it would be difficult for Cardinal Health to easily raise their prices without risking the fact that CVS and Walgreens could then choose not to use Cardinal Health as a distributor anymore. Evidently, raising prices is a key revenue driver, and therefore Cardinal Health can be said to have a low pricing power (it is difficult for the company to arbitrarily raise its own prices without high risk). Also, Cardinal Health depends on agreements with GPOs (group purchasing organizations) who act as agents

6 and create contracts with Cardinal Health. However, if the members of the GPO do not agree with the contract that the GPO agents have created, then Cardinal Health can lose sales. Although GPOs account for 15% of its revenue, Cardinal Health still considers the loss of sales to a GPO to be considered deleterious to company and financial operations. failure to meet the terms of current and future regulation requirements On August 28, 2006, Cardinal Health had to stop sales of an Alaris SE Infusion Pump because the keyboard touchpad was too sensitive and would register numbers once instead of twice. Therefore patients could potentially receive too high a dose of their medication. This recall was a class 1 recall, which is the most serious type of recall issued by the FDA. Cardinal Health claims that these recalls and problems with medical products are difficult to predict, and they are unable to say that future regulation requirement problems will never happen again. many substitutes for CAH s services Cardinal Health s services are not unique in that there are other large competitive companies that are providing the same services that Cardinal is providing. The company has stiff competition in every one of its sectors, from medical, pharmaceutical, and clinical products and services to pharmaceutical distributions. Cardinal Health is second in the nation to McKesson Corporation, and other companies such as AmerisourceBergen Corporation, Owens and Minor, and Fisher Scientific also strongly compete with Cardinal Health. As a result, the company has recently been consolidating its sectors. On November 30, 2006, Cardinal announced that it would be selling its drug manufacturing business so as to concentrate on its other sectors. limited choice of where to purchase raw materials The raw materials that Cardinal Health uses to manufacture its medical products are only available from a limited number of suppliers. This is because there may be certain customer requirements that constrain Cardinal Health to a particular provider, or product approvals that only make it possible to purchase these specific raw materials from select companies.. Therefore, the company is at the mercy of the prices set by these particular suppliers. legal proceedings and SEC investigations Since July 2004, Cardinal Health has been under legal investigation by the government and has been charged with class-action lawsuits. The government is currently checking to see that Cardinal Health s accounting and financial reporting is accurate. The company admits that it could possibly incur a $35 million dollar penalty. These legal investigations have not been settled as of December Also, class-action lawsuits have been filed since July 2004 by individuals who feel that the company did not accurately present the associated risks with investing in their 401k retirement plan. As of December 2006 this case is yet to be settled, and the company recognizes that an adverse settlement could possibly affect their financial state for the next fiscal year.

7 full financial statements From Google Finance

8

9