Moving Forward with the FG Agenda: Lessons from Indian Financial Inclusion

|

|

|

- Godwin Perkins

- 5 years ago

- Views:

Transcription

1 Moving Forward with the FG Agenda: Lessons from Indian Financial Inclusion Prof Rekha Jain IIMA IDEA Telecom Centre of Excellence, IIM Ahmedabad, India

2 (Source: McKinsey Report- Global Financial Inclusion Fall 2010 )

3 Extent of Financial Exclusion Global 2.5 billion adults, just over half of world s adult population, do not use formal financial services to save or borrow. 2.2 billion of these unserved adults live in Africa, Asia, Latin America, and the Middle East. Of the 1.2 billion adults who use formal financial services in Africa, Asia, and the Middle East, at least two-thirds, a little more than 800 million, live on less than $5 per day (Source: Key findings of research report Half the world is unbanked, March 2009)

4 Extent of Financial Inclusion Share with an account at a formal financial institution All adults Poorest income quintile Key Statistics on Financial Inclusion in India: A Survey Women Adults saving in the past year Using a formal account Using a community -based method Adults originating a new loan in the past year From a formal financial institution From family or friends Adults with a credit card Adults with an outstandi ng mortgage Adults paying personally for health insurance (%) Adults using mobile money in the past year India World Source: Asli Demirguc - Kunt and Klapper, L. (2012): Measuring Financial Inclusion, Policy Research Working Paper, 6025, World Bank, April. The key message from these analyses is that hundreds of millions of adults living on lower segment are already being reached with formal financial services. Serving these segments at scale is not only possible, but to a large extent, is already happening.

5 Road map for Financial Inclusion India For achieving planned, sustained and structured financial inclusion. Approach adopted by RBI- Some Specifics Technology- To be fixed first. All Bank branches must be on Core Banking Solution (CBS). All Regional Rural Banks (RRBs) on CBS by September Multi-channel approach (Handheld devices, mobiles, cards, Micro- ATMs, Branches, Kiosks, etc.) Front-end devices transactions must be seamlessly integrated with the banks CBS.

6 Financial Inclusion Perspective Most important prerequisite of a computer or an electronic device from the customer s perspective and from an inclusion perspective It is the Standardization The best financial innovation of the recent times- the ATMs. Do they result in faster dispensation of cash? A definite "yes". Is it hassle free? To me, "No".

7 Financial Inclusion Perspective The different ATM cards, micro-atm cards, Debit/Credit cards, etc. are confusing to the man on the street. Different operational system of ATMs Insertion: Swallow or Swipe Different point of transactions on Terminal Interaction feature at terminal: GUI keypad or Touch Screen Amount Recognition: in terms of standard multiples, round offs etc. Why do we not think of standardization even in this basic product? K C Chakrabarty, RBI Deputy Governor: ICT based financial inclusion carving a new path through innovation

8 Financial Inclusion Perspective Financial inclusion Low cost for low value transactions Innovative Models prevalent in India - Eko - FINO - ALW Now these model formats are reaching to some convergence via UID enabled Micropayment (Aadhaar) and RuPay (Indian Debit Card Network)

9 AADHAAR The Unique Identification Authority of India (UIDAI) is Government agency for implementing the AADHAAR scheme, a unique identification project and will maintain a database of residents containing biometric and other data. Aadhaar is a 12 digit individual identification number with biometric identification consisting of: Iris Scan 10 Fingerprint Scan Face Camera

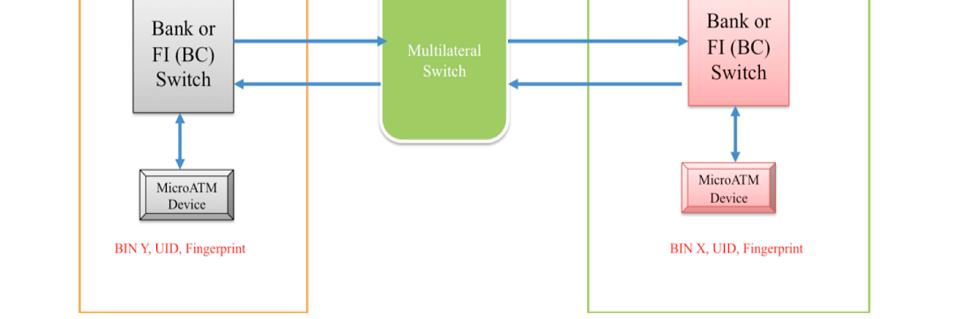

10 Interoperability Architecture for UID enabled Micropayment Key Institutions: Banks Government Department NPCI UIDAI (Source: UIDAI)

11 AADHAAR Enabled Micropayment Architecture (Source:

12 Aadhaar Based Micropayments A UID-enabled Bank Account (UEBA) linked to a UID number A BC (Business Correspondent) operating a handheld micro-atm device. Transactions on the UID-enabled bank account function essentially as a prepaid system, similar to that used by mobile operators. BCs (self-help groups and Grocery shops) to offer basic banking services at low risk to the bank.

13 Micro -ATM Biometric authentication enabled hand-held device BC handles physical currency (cash-in & cashout) not a machine like a regular ATM. All transactions through biometric authentication

at the behest of Indian Banks Association Approved by Reserve Bank of India (RBI).. 237 million transactions for a value of Rs.")

14 270 million debit cards in the country today (RBI data) RuPay is the Indian domestic card payment network. Set up by National Payments Corporation of India (NPCI) at the behest of Indian Banks Association Approved by Reserve Bank of India (RBI) million transactions for a value of Rs. 357 billion at PoS terminals. Maximum usage at ATMs with 4235 million transactions for a value of Rs. 11,144 billion

15 Key Facts about RuPay RuPay will be accepted at all the 91,000 ATMs and over 0.6 million points of sale terminals in the country. Future acceptance on the Internet and also at ATMs/PoS terminals abroad. International remittance arrangement via payment gateway Discover. Adoption of the RuPay Card will help banks save Rs Rs 3000 mn annually as interchange charge is cheaper by up to 40% (Visa and MasterCard).

16 Emergence of Variety of Players -Innovators Sarvatra Technologies provides a world-class EFT switch using international standard ISO 8385 protocol, (validates the customer card, the ATM/POS terminal, and the PIN) and then forwards the transaction to the NFS and back.

17

18 Choices for the FG 1. Choice of Application Area Micropayments?? 2. Which part of payment cycle- Identification Verification/Authentication Aggregation/Switching over different CBS Across Payment different to financial customer products and services 3. Multiplicity of standards- SCOSTA (based on ISO 7816 ), Biometric identification standards (ISO 19794). 4. Multiple technologies and delivery models for financial transactions.