Building the BBVA franchise in the US. Best Practices in Retail Financial Services Symposium American Banker

|

|

|

- Rosalyn Roberts

- 5 years ago

- Views:

Transcription

1 Building the BBVA franchise in the US Best Practices in Retail Financial Services Symposium American Banker Marco Island FL, March 16th 2009

2 Disclaimer This document contains or may contain forward looking statements (in the usual meaning and within the meaning of the US Private Securities Litigation Act of 1995) regarding intentions, expectations or projections of BBVA, BBVA Compass or of its management on the date thereof, including projections about the future earnings of the business. The statements contained herein are based on our current projections, although the said earnings may be substantially modified in the future by certain risks, uncertainty and other relevant factors that may cause the results or final decisions to differ from such intentions, projections or estimates. These factors include, without limitation, (1) the market situation, macroeconomic factors, regulatory, political or government guidelines, (2) domestic and international stock market movements, exchange rates and interest rates, (3) competitive pressures, (4) technological changes, (5) alterations in the financial situation, creditworthiness or solvency of our customers, debtors or counterparts. These factors could result in actual events differing from the information and intentions stated, projected or forecast in this document and other past or future documents. BBVA and BBVA Compass do not undertake to publicly revise the contents of this or any other document, either if the events are not exactly as described herein, or if such events lead to changes in the stated strategies and intentions. Distribution of this document in other jurisdictions may be prohibited, and recipients into whose possession this document comes shall be solely responsible for informing themselves about, and observing any such restrictions. By accepting this document you agree to be bound by the foregoing restrictions.

3 1. BBVA Compass Retail Banking agenda 2. Towards BBVA Retail Business Model 3. Takeaways

4 1. BBVA Compass Retail Banking agenda 2. Towards BBVA Retail Business Model 3. Takeaways

5 Blending the best

6 into one single organization Retail Banking Shelaghmichael Brown

7 BBVA Compass Retail Banking As of December 2008 Million Dollars Percentage of total Loans 13,112 34% Deposits 19,324 51% Revenues 1,299 49% Employees 7,125 59% Branches 577

8 1. BBVA Compass Retail Banking agenda 2. Towards BBVA Retail Business Model 3. Takeaways

9 Transforming our future A Vision: The BBVA franchise in the U.S. Product-centric A new Business Model Customer-centric Outdated and not integrated technology Technology Platform Upgrade Serving a new business model Organizational silos A new Organizational Structure Collaborative and customer oriented Different, better because of you New principles We work for a better future for people Retail Banking transformation process is part of the overall banks transformation

10 Towards a customer-centric model Adapting locally BBVA s best practices

11 1. Customer Intelligence Enhancing our customer knowledge capabilities with Competitive Advantage from BBVA Customer Intelligence Approach Integrated Databases Client Centric View Knowing the client based on past behavior Implementing behavioral tools Campaign Management Online Multichannel Platform Tracking Results Test and learn

12 Accessible & profitable financial product portfolio 2. Innovative solutions Innovative products leveraging BBVA Group s international capabilities and best practices Bi-National mortgages Equity link CD Power CD sm

13 2. Adapting BBVA s positioning to our reality Blending the best of two leading organizations

14 2. and translating it into relevant marketing From the value bank to adaptability Heavy reliance on monthly incentives to drive short-term volume

15 3. Towards an integrated multi-channel strategy Integrate technology for consistency across channels Encourage migration of transactions to most effective channel Enhance self-service capabilities Our goal is to see the same customer across all channels in the same way

16 3. Piloting new concepts of branch Reengineering the branch: As a more efficient sales outlet Focus on sales and advice Cornerstone of our multichannel distribution. Achieving excellence in customer service

17 3. Implementing BBVA s functionalities into our alternative channels New enhanced functionalities Exploring innovative channels Online Banking Mobile Banking ATMs Call Center Further enhancing the customer experience across channels

18 4. Management model Developing a homogeneous Management Methodology Communication Sales Planing Follow - up Goal Setting Customer management Incentive model Turning the retail network into a more powerful sales structure 1. Actively managing budget as a measure of success. 2. Leveraging activity levels, with the commercial plan as the main axis. 3. Combining demanding goals and high levels of support 4. Prioritizing efforts and keeping focus on the customer.

19 4. Management model Developing new Customer Management Plans to upgrade customer relationships Building long term relationships with our customers 1. Increasing and improving the quality of financial dialogue with the customer. 2. Managing customers in different ways depending on the value they bring to the bank. 3. Rediscovering the branch as the center of sales and customer service. 4. Developing distribution synergies with other LOB s.

20 4. Management model Customer Centric Model: Strengthening a different customer approach 1 Customer needs and value All processes initiated and built around the customer 4 Incentive Model 1. Understanding customer s different needs and value they bring to the bank. 3 Roles and functions 2 Sales processes 2. Defining customer sales processes aligned to these different needs and value. 3. Adapting / implementing roles and functions to deploy these processes. 4. Developing incentives plans tailored to each role.

Cash")

Branch Cost Model Branch MIS Follow up")

Branch Staffing Model Sales")

21 4. Management model Applying technology throughout the whole value chain of our customer relationship From customer knowledge to product origination Channels ATM Internet Call Center Others STP Processing No ti cket (no paper) Cash handling Multi customer On line / Off line availability Servicing (Teller) Integrated Teller System Automatic decision maki ng process Customer Identification Improve Customer Experi ence 4 Multi language Workflow Branches Incentive Model Single Customer View Sales tracking Referral Sales Selling support tools & Simulators Cross selling Tools Ops./Commercial Information Cross sell opportunities Sales Origination 1 Customer needs and value Sales Agenda Customer Ownership Model Cross Functions sales support processes (agenda, wallet info) Branch Cost Model Branch MIS Follow up of customer obligations Help Desk 3 Customer Complaints Service Roles and functions Account Posting Resolution Human Resources High Value Capabilities Training 2 Branch Career Plan (specially tellers) Branch Staffing Model Sales processes 15 and monitoring sales staff goals and activities Technology as a key tool to support our dialogue with the customer. 24

22 5. Adapting BBVA s corporate culture and people management tools The BBVA Experience Program Competencies Model Key for the retail unit as they allow for: Empowering our people Management Styles Passion for people Generating enthusiasm and motivation To increase quality of service To deliver a superior customer experience.

23 6. Risk management Implementation of BBVA corporate risk tools according to Basel II standards Global Risk Map: Economic Capital Distribution Gradual integration of economic capital methodology in: Pricing Risk-adjusted return information by product, LOB, customer Value analysis Portfolio management Credit reserves RE CONSTRUCTION 20% CF&A 27% CREDIT & OPERATIONAL RISK ECONOMIC CAPITAL DISTRIBUTION RE RESIDENTIAL 8% Consumer Direct Loans 1% Credit Card 3% Equity Loans 2% CRE 18% Equity LOCs 4% Mortgage 7% Consumer Indirect 10%

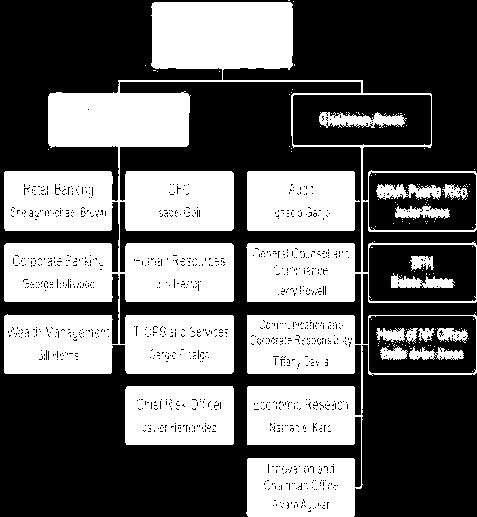

24 7. A customer oriented retail banking organization Financial Planning Pat Riley Retail Banking Shelaghmichael Brown Credit Risk Operations Dianne Bruer Business Development Enrique Gonzalez Liability Products Bill Hippensteel Network Jeff Talpas Consumer Asset Products John Mulkin Marketing Frank Sottosanti Underwriting Ralph Dalton Collections John Frey Management Methods Operational Processes Network Design New Platform Development Strategic Planning Support Internet ATMs Call Centers Payments Incentives DDA & Transaction Accounts Interest Bearing Accounts & Pricing Merchant & Small Business Texas North Branches, Small Business & Mortgage Sales Texas South Branches, Small Business & Mortgage Sales West Branches, Small Business & Mortgage Sales East Branches, Small Business & Mortgage Sales Asset Product Manager Credit Care Mortgage Operations Mortgage Administration Mortgage International Construction Lending Customer Intelligence Advertising & Brand Hispanic Strategy Shared Services

25 1. Who is the BBVA Group agenda 2. BBVA in the US 3. BBVA Retail Business Model 4. Takeaways

26 In summary Our strategy, global customer approach. Our aim, to deliver a superior customer experience. Our retail model, an excellent launching pad for further growth. Our focus, always, execution.

27 Building the BBVA franchise in the US Best Practices in Retail Financial Services Symposium American Banker Marco Island FL, March 16th 2009