PhD Student (presenting): Ian Gregory.

|

|

|

- Stephen Elijah McKenzie

- 5 years ago

- Views:

Transcription

1 Deviance critical values for finite sample size when testing the reduction of (G)ARCH(1,1) to a Gaussian random walk: Results from MATLAB vs. the R-Project PhD Student (presenting): Ian Gregory.

2 Presentation Outline: Overview and Motives (G)ARCH(1,1) model. Available packages to fit (G)ARCH and their pros/cons. Hypothesis statistics for heteroscedasticity. Deviance Statistic. Simulation study. Conclusion and Findings. Finite properties Ranking of packages. 2

3 (G)ARCH(1,1) Non-negative restriction (2.3) important in financial modeling for positive conditional variance. Proof derivation see Nelson and Cao (1992). 3

4 (G)ARCH(1,1) Maximum Likelihood Conditional Gaussian log-likelihood function The solution involves recursive iterations for each data point in the series until terminal conditions are met or an error occurs. NOTE: The rw surface is smooth. GARCH surface is not smooth. Exact estimates are non-trivial. Hamilton (1994) p.123. Maximum likelihood methods are asymptotically consistent; meaning as size increases, estimates should converge to the true values (on average). 4

5 Hypothesis: Each package and test case fits the true values over the interval: Using FOUR test cases of supplying different starting guesses for the (G)ARCH(1,1) parameters. I.) package default settings II.) the null coefficient is supplied III.) 1st solution is resupplied to the routine at least once IV.) uniform random numbers 5

6 Hypothesis test for (G)ARCH(1,1) against random walk One-sided statistics for heteroscedasticity against random walk (listed in increasing power). Engle s ARCH test. Engle (1982). Demos & Sentana (1998), Andrews (2001). Kluppelberg et al. (2002). In the limit, Engle s test is the same as Kluppelberg. Andrews, Demos & Sentana and Kluppelberg are expressions for likelihood ratio tests to be used in a deviance calculation. Finite sample properties may be subject to type I, II errors. (reject/accept null too often). 6

deviance is given in Demos and Sentana (1998) which is a rescaled quasi-likelihood ratio test: 90%,95%,99% critical values for ARCH(1) are 1-2\alpha")

7 Deviance Statistic: Derivation: Vu and Zhou (1997). See Seo (1998) and Andrews (1999) on boundary hypotheses. The asymptotic distribution for ARCH(1) deviance is given in Demos and Sentana (1998) which is a rescaled quasi-likelihood ratio test: 90%,95%,99% critical values for ARCH(1) are 1-2\alpha quintile of a chisquare random variable with 1 df with values: 1.64,2.71,5.51 respectively. 7

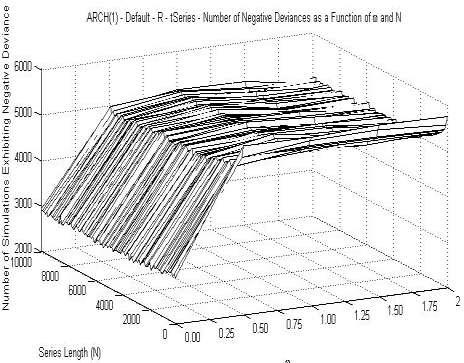

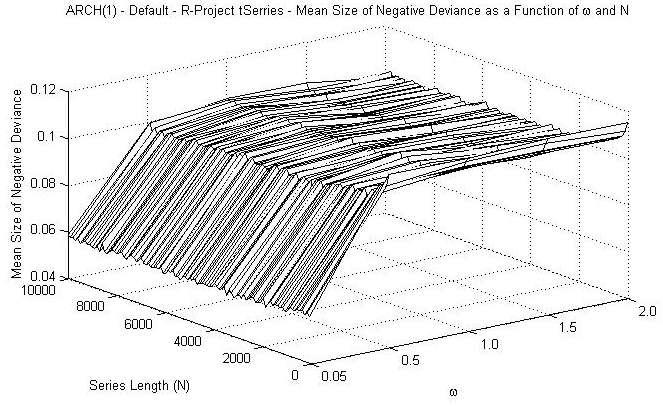

8 Deviance Statistic (cont d): Andrews (2001) derives the rescaled test statistic for GARCH(1,1) as: Andrews rescaled test statistic for GARCH(1,1): Using (3.3) Andrews reports 90%,95%,99% critical values to be 3.06,4.33,7.30 respectively. This corresponds to 1-\alpha (chi-square). 8

9 Which Packages? MATLAB, R/tSeries;fSeries, Eviews, Mathematica/TimeSeries, SAS /ETS, GAUSS/FANPAC, NLOGIT, Ox, S-Plus/FinMetrics, Winrats, Stata. 9

10 Benchmarking Econometric Software: Several authors have investigated benchmarks for (G)ARCH estimation routines. The aim is to improve and maintain a standard for (G)ARCH estimation routines. See: Fiorentini et al (1996) Examines the affect of numerical and analytical derivatives Brooks (1997), Brooks et al (2001), (2003). Examines performance by changing options in the packages. Package comparison and estimation issues. McCullough and Renfro (1996) Software comparison and non-linear methods for GARCH. Several packages unsiuitable for standard model estimation. Bollerslev & Ghysels (1996) Deustche mark/british pound FX data using the approach of Calzolari & Panattoni (1988) has become the generally accepted method for benchmarking GARCH(1,1) software. McCullough and Vonid (2000) Is it safe to assume that software is accurate. He identifies several studies and mentions users should not always plug and play. User friendliness values more than accuracy. McCullough and Vonid (2003) Numerical reliability of econometric software 10

11 Experiment Design: Finite Monte Carlo Using High Throughput Computing (HTC) cluster (approx 600 nodes one of the most powerful networks in the southern hemisphere. For potential throughput.) Demos and Sentana (1998) perform a size and power study on the distribution of LM test, Kuhn-Tucker, Wald tests. The results are presented using Davidson & MacKinnon (1998) plots. Given previous research, the four test cases involves user supplied initial parameter guesses. To improve further on the percentile estimates peak over a high threshold technique was also examined. In finite sample and asymptotic studies, it is customary to tabulate results using percentiles of the distribution. 11

12 Results: $\omega$ vs. Series Length (N) Deviance for different $\omega$ appear to be independent of series length. This agrees with the theoretical derivation. Spikes due to estimation issues. Such as: Negative deviances Failed estimations 12

13 Results (cont d): Deviance vs. Series Length (N) There appears to be a relationship between deviance and series length. 13

14 Results (cont d) - Deviance vs. Series Length (N) ARCH(1) More negative the coefficient a, greater the convergence to the asymptotic. Value C represents the estimation of the asymptotic. MATLAB converges quicker than R-Project tseries for ARCH(1). 14

15 Results (cont d) - Deviance vs. Series Length (N) GARCH(1,1) Default estimation generates reasonable results for MATLAB and R. Supplying null to tseries causes issues. 15

16 Negative Deviances: Negative deviances are theoretically impossible. A negative deviance implies early optimisation termination, misspecification of the model or fit finished before completion. 3 Approaches in the results: Leave them in. Take them out (delete them). Set them to zero. Alternatively to improve on the amount of negative deviances can try settings for starting conditions not included in the default settings. Random numbers Null coefficient Resupply previous solution Resupplying the solution and null coefficients appeared to reduce the number of negative deviances. MATLAB produced less negative deviance values and with a lower mean. R-Project tseries produced negative deviances at a lower omega value. 16

17 Negative Deviances: 17

18 Practical Example: 18

19 Outcomes: Can not plug and play with all commercial econometric packages. Some caution required. False results No results! ie. Program crashes or will not run, even with default settings. Documentation not 100% correct. ie. R-Project, Mathematica. Optimisation in 2008 is not a trivial matter. 2-step optimisation routines more powerful than single step. Supplying analytical derivatives more powerful. Large number of simulations. 1/sqrt(n) required to improve accuracy for empirical studies. Using default estimation settings are not always optimum. Should check for positive deviance. POT analysis improves results slightly. 19

20 Future: Model other distributions. ie. Student-t Examine power+size effects. 20