For personal use only

|

|

|

- Kellie Paul

- 5 years ago

- Views:

Transcription

1 Macquarie WA Investor Conference October 2013

2 Today s agenda 1 A focused strategy 2 The NBN 3 Future drivers of growth

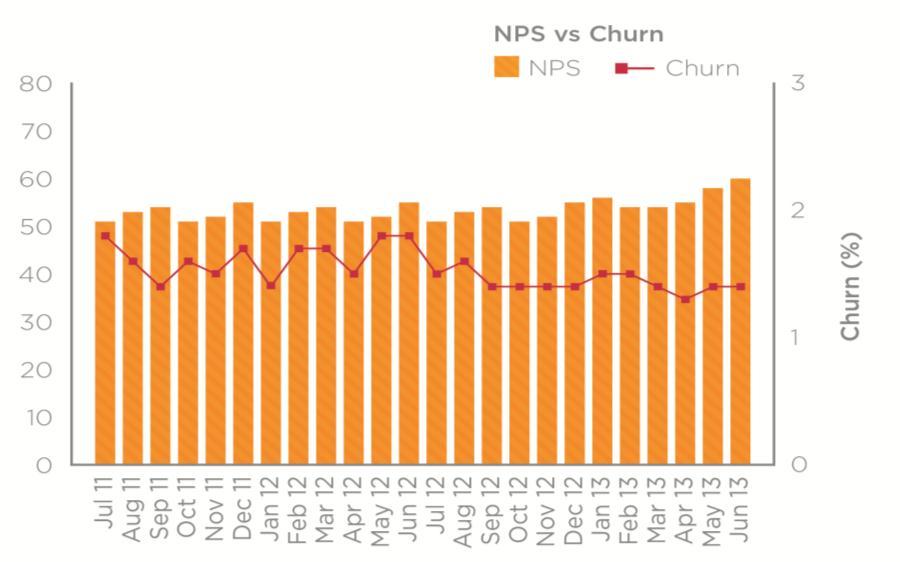

3 iinet today Our historic strategy focused on service, brand, innovation and scale has delivered The clear No.2 in DSL with 910,000 broadband customers The leader in customer satisfaction NPS consistently tracking >55% with market leading low churn A fully integrated service provider leading on innovation - with 20% of revenue coming from Business customers A national network across 450 exchanges with over 320 Gbps of capacity Major fibre and data centre assets in SA, ACT and regional Victoria A $1bn market cap company with over 2,000 employees in 3 countries 3

4 The strategy going forward Sales & service NPS consistently above 55%, reaching 60% in June 2013 More effective sales and targeted marketing - customer segmentation, increased brand awareness, recognition and sales in Eastern states Lead on the NBN opportunity Products per customer Business Integration & Cost outs Products per customer targeting 3, up from 2.23 today Growth in mobile, IPTV and other value added services and products Continue to lead on product innovation to the broadband home Growing revenue at >5% per annum Focussed sales and service across all brands to capture new product growth and product cross sell Integrate best-of-breed capabilities across iinet, Internode and TransACT TransACT and Internode billing migrations ongoing 18 month program to reduce calls into call centre, automation and simplification Adam Internet integration underway 4

5 Today s agenda 1 A focused strategy 2 The NBN 3 Future drivers of growth

6 Why the NBN is so attractive for iinet (current wholesale pricing) A similar access cost equation for on-net (metro) An improving access cost equation for off-net (regional) off-net on-net NBN NBN Access cost per user ($/mth) for like-for-like 12Mbs broadband and phone bundle - excludes backhaul & transmission and customer usage drivers 6

7 Our NBN approach and results Marketing approach Positive performance to date Geographically targeted approach to NBN marketing based on roll out more cost effective Customer communications up to 12 months from network readiness NBN education focus Active customer management through decision and migration cycle Over 20,000 customers >60% of customer sign ups are new to iinet >50% customers bundle voice and data Blended ARPU is ~$70 60% fibre, 35% satellite and 5% wireless 70% of customers buying higher speeds than 12 mbps entry level product 7

Broad policy -")

Out to in approach favoured (regional under served areas first) Attempt to")

Completed more quickly Wireless & Satellite 7% FTTN roll out to continue to 2019; approximately 65% complete")

8 What we know about the Coalition s plans Process and principles New Board appointed awaiting the start of 60 day review including audit, cost benefit analysis of existing FTTP roll out as well as potential approach using new technologies/ approaches (FTTN) Broad policy - quick, effective, cheaper roll out of a high speed broadband network Utilise a mix of technologies to ensure a data rate of between 25 and 100 Mbps by 2016 (extended to between 50 to 100 Mbps) Out to in approach favoured (regional under served areas first) Attempt to enhance infrastructure completion Telstra structural separation still delivered A potential mix of technologies (% of roll out) FTTN FTTP 71% 22% (largely contracted) Completed more quickly Wireless & Satellite 7% FTTN roll out to continue to 2019; approximately 65% complete by

9 What we don t know about the Coalition NBN plans Who will build the network? Will FTTN use the same POIs, or more, or less? Anti cherry-picking will it be repealed? Will we be allowed to extend our fibre networks? Who is responsible for greenfield connections? VDSL2 and vectoring no VDSL2 deployment rules. Will NBNCo be required to meet Customer Service Guarantee for 100% of connections? Will FTTN look like wholesale bitstream ADSL with obligatory PSTN or like NBN UNI-D + UNI-V? Or something else altogether? Will NBNCo revise its FTTP product set and pricing? 9

")

10 Do we need all this? OR One Ethernet port (not 4 x Ethernet + 2 x PSTN + Battery) 10

11 Current CVC pricing mechanism not sustainable We have built new networks with abundant capacity and then, as a result of the NBNCo CVC pricing framework, are at risk of limiting access to them and creating an artificial scarcity There is real customer pull for usable, affordable and reliable broadband The CVC pricing mechanism should be revisited Why have bandwidth based CVC charges, we have built the scale networks so why can t we use them? The $20 per megabit CVC charges represent a significant increase on todays prices and will choke the future growth of broadband services in Australia 11

12 Implications for potential new entrants under current model Establishment of a national network - $30-$35m Operating costs to manage a small national customer base (say 200k) are $30-40m per annum Significant establishment costs to enable a national NBN network presence Significant operating costs to support and service 200k customers Establishment costs include : Presence and transmission from in 121 POI s Points of presence in 7 capital cities Establishment of long term inter-city and international bandwidth agreements Customer authentication and management systems Developing billing and NBN B2B system interfaces Operating costs include : Marketing and brand awareness national brand presence Ordering and provisioning systems and process Customer service and support costs operating a scale call centre Billing systems processing and management Employee support costs across shared services functions Product support costs for complex bundles Analysis excludes direct customer related cost of sales (e.g access fees etc) and operating cost is based on 20-25% of revenue assumption 12

13 Today s agenda 1 A focused strategy 2 The NBN 3 Future drivers of growth

14 Future drivers for growth Broadband growth Headwind PSTN decline Group Scale (FY13) $941m revenue $187m EBITDA 910k customers 1.8m services Mobile, IPTV, Budii Jiva Business market Integration & cost outs 14

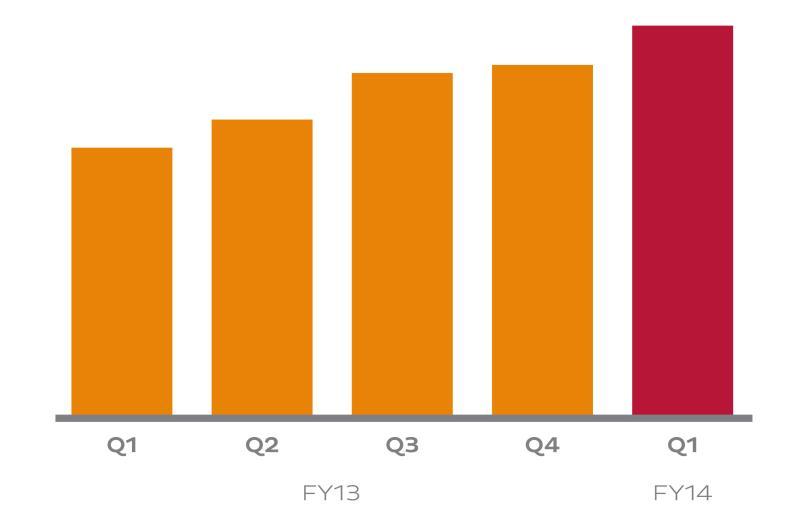

15 Best-in-class service, low churn and growing sales Quarterly broadband sales 15

16 Raising awareness in key growth markets 16

17 Jiva simplicity and quality 17

18 Call packs fat chats, skinny bills 18

19 Mobile 19

20 iinet TV with fetch 20

21 Business market opportunity +53% Business revenue now up to ~20% of group revenue with 5% p.a. organic growth Focus remains on the smaller end of the market SoHo & SMB Bundling additional products into existing base fixed telephony, hosted PBX, hosted cloud services, data centres Integrated suite of products and services across all brands 21

22 A focus on SoHo and SMB Business revenue by customer type Significant opportunity to grow >65% of revenue still in traditional access products Business margins typically >10% higher than residential Opportunity to grow market share and share of wallet through cross sell and new product innovation iinet Business Voice iinet Business Bundles iinet Business Cloud iinet Symmetrical DSL iinet Business Connect iinet Hosted Exchange Growing revenue but still relatively low current market share across all segments - opportunity 22

23 More to come - integration & simplification Area Integration Service IT & Brand systems Process Innovation simplification Marketing Scale costs Actions and outcomes Adam integration planning underway, network synergies to be extracted first Reviewing wider commercial Service opportunities across the Group Billing system integrations across TransACT then Internode and Adam System simplification Brand delivering product integration across brands Simplifying processes that result in customer calls delivering an improved customer experience and fewer issues for staff to resolve Clear focus on improving the effectiveness of our investment cut through, targeting, conversion Results already being Scale delivered Potential for other cost savings to be reinvested in further growth 23

24 In summary Record FY13 results and returns for shareholders Revenue up 13% to $941m EPS up 58% to 38 cps Total dividends up 36% to 19 cps +44% TSR per annum for last 5 years Clear No 2 in DSL executing well across all aspects of the business Strategy for future growth in place and underway Targeting dividend payout ratio of 50% to 60% of normalised NPAT going forward Preserves flexibility and capacity for major capital expenditure or M&A activity 24

25 Q&A

26 Our customers expanding services and products per customer Closing subscriber numbers (000s) Jun-12 Dec-12 June 13 + Adam Total core services up to 1.72m Products per customer strategy driving bundled services to 2.23 per customer and helping to mitigate fixed phone usage decline Further bundling opportunity at Internode and Adam Internet 20,000 NBN customer milestone now passed On-Net Off-Net NBN & Fibre Fixed phone VoIP Mobile Television 910k Broadband customers includes Adam at 70k 26

27 DISCLAIMER Some of the information contained in this presentation contains forward-looking statements which may not directly or exclusively relate to historical facts. These forward-looking statements reflect iinet Limited current intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors, many of which are outside the control of iinet Limited. Important factors that could cause actual results to differ materially from the expectations expressed or implied in the forward-looking statements include known and unknown risks. Because actual results could differ materially from iinet Limited current intentions, plans, expectations, assumptions and beliefs about the future, you are urged to view all forward-looking statements contained herein with caution.