Sabbatical Marine, Inc.: Utilizing Constrained Resources Additional Information Boating Industry Background The boat building industry s North America

|

|

|

- Egbert Smith

- 5 years ago

- Views:

Transcription

1

2

3

4

5

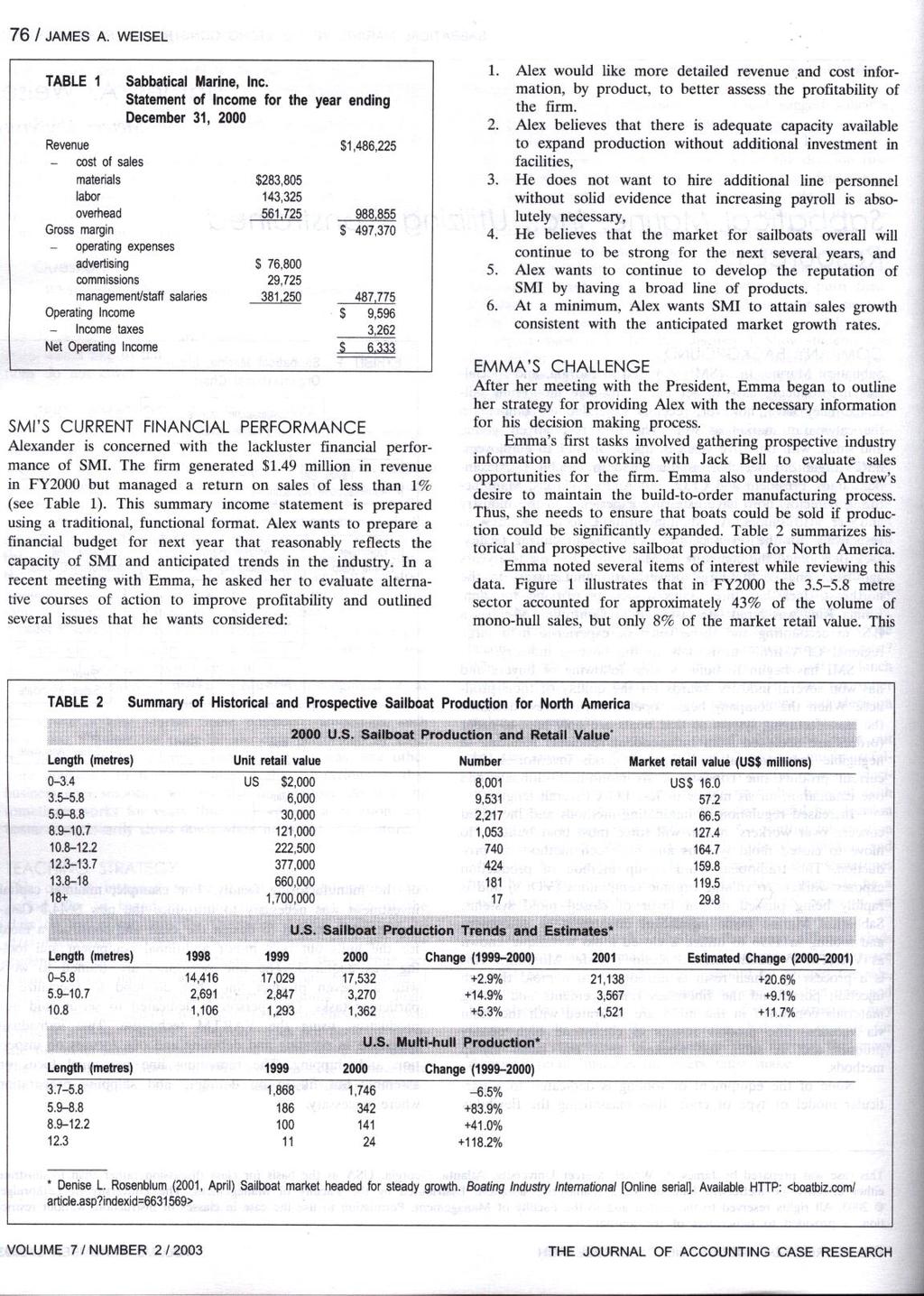

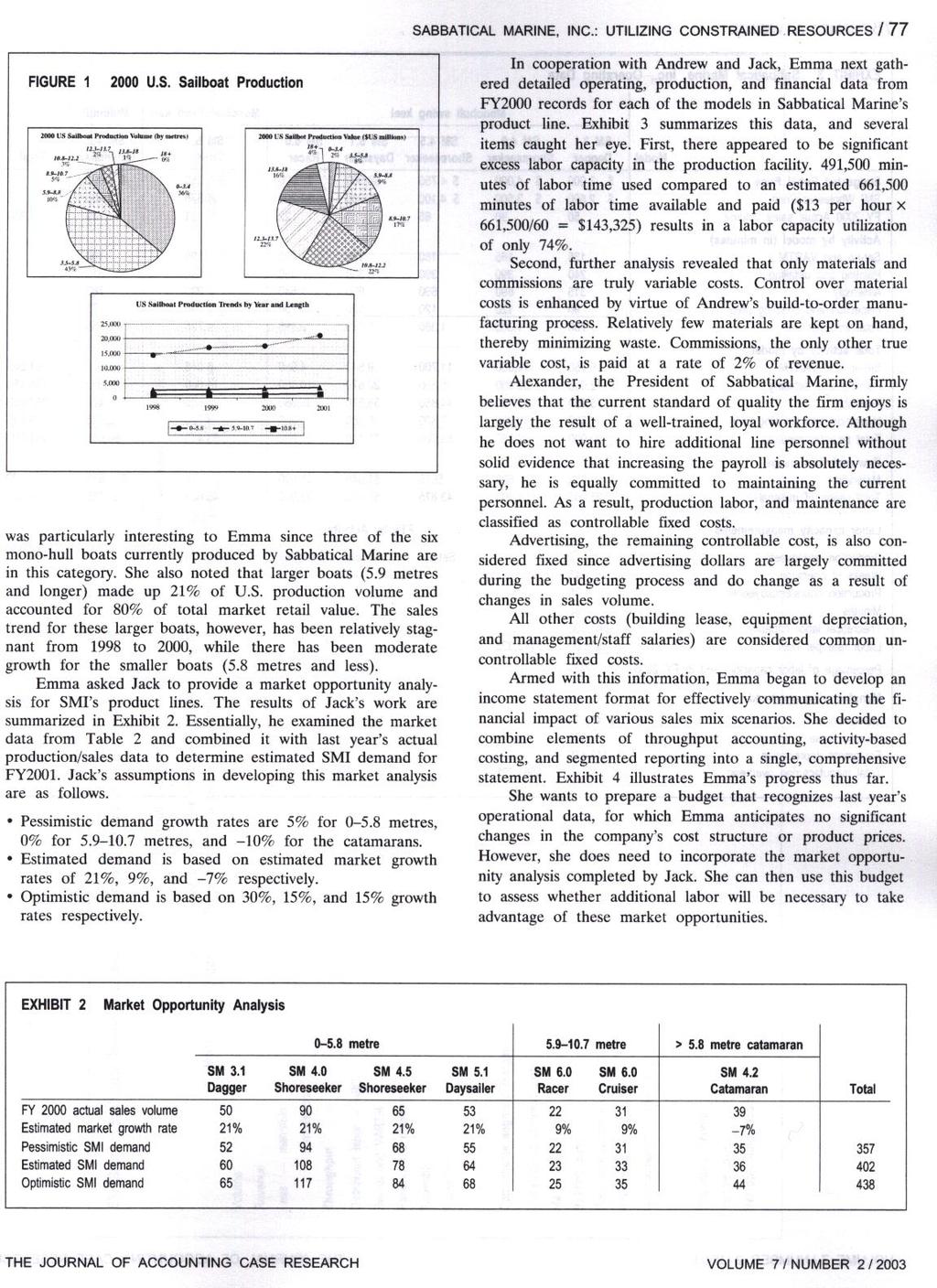

6 Sabbatical Marine, Inc.: Utilizing Constrained Resources Additional Information Boating Industry Background The boat building industry s North American Industry Classification System (NAICS) number is (formerly Standard Industrial Classification [SIC] 3732). According to 2000 statistics from the U.S. Department of Commerce 1, nearly 57,000 people are employed in the boat building industry. The value of shipments in 2000 exceeded $US8.3 billion, an increase of 12% compared to Boat registrations in the U.S. have been growing at a steady 1.6% annual rate for the past ten years, with registrations as of 2000 standing at slightly more than 12.7 million boats 2. The largest sectors of this market are powerboats and jet skis accounting for 27% and 7% market share respectively. Sailboats, while accounting for only 5% of the market, are considered a growth sector. Monohull boats dominate the sector. Although some are constructed of wood or steel, a vast majority of sailboats are of fiberglass construction. Catamarans were of little interest in the market until 1988, when Dennis Conner defended the America s Cup in a catamaran. Today, sales of multihull power and sailing boats are growing rapidly. The fundamentals of sailing are relatively simple - with a few precautions, a new sailor can learn these fundamentals on the first day. However, sailing is also an old and complex art, and a person can spend a lifetime at it and always find something new to learn. People who choose sailboats over powerboats probably do so for two reasons, quiet and challenge. The sound of wind through the sails rather than the roar of the motor is an attractive characteristic. Additionally, setting sails and choosing a tack is a constant challenge. Wind conditions are forever changing, requiring adjustments from the sailor to achieve maximum efficiency and still get to the intended destination. Countless organizations exist to introduce people to the sport of sail boating. Fundamentals of the Theory of Constraints The fundamental concept of Theory of Constraints (TOC), articulated by Eliyahu M. Goldratt and Jeff Cox in their 1984 book The Goal, is actually quite simple. TOC states that every for-profit organization is faced with at least one factor that limits the firm s ability to earn profits. If this were not the case, then a for-profit firm would earn an infinite amount of profits! Given this core concept, the manager who wants more profits must manage the constraint(s) faced by the enterprise. Most businesses can be viewed as a system of linked processes that convert inputs into sellable outputs (products or services). In TOC, an analogy can be drawn between such a system and a chain. What is the most effective means of strengthening a chain? Does one concentrate on the 1 Statistics for Industry Groups and Industries: 2000 Annual Survey of Manufacturers. U.S. Department of Commerce, Economics and Statistics Administration, U.S. Census Bureau. (2002, Washington, DC). < 2 Boating 2001: Facts and Figures at a Glance. National Marine Manufacturers Association, Market Statistics Department (2001, Chicago). <

7 strongest or largest link? Or should the weakest link be improved upon first? TOC clearly indicates that the latter results in a better benefit-cost relationship. The five key steps in implementing the concept of TOC are as follows: 1. Identify the first constraint or bottleneck in the system. Constraints may be internally or externally generated. 2. Determine how to exploit the system s constraints. In other words, maximize the use of the constrained resource. 3. Let the constrained resource set the pace for the remaining elements of the process system. Subordinate other day-to-day operating decisions relative to use of the constrained resource. 4. Improve or expand the constrained resource so that it is no longer the bottleneck in the system. 5. Once the first constraint has been alleviated, return to the first step to identify the next constraint. This is the process of continuous improvement. Although TOC was first developed to improve scheduling in a job-shop environment, the concepts and tools are sufficiently broad to be used in a wide variety of businesses including retail operations and service organizations. TOC can also be used in not-forprofit organizations wanting to maximize the delivery of services while consuming a minimum of resources. TOC cannot be used with traditional cost accounting techniques such as absorption costing and standard cost variance reporting. Absorption costing and variance reporting create incentives to produce excessive inventories. Under absorption costing, building up inventories tends to reduce the apparent average cost of goods sold by spreading fixed overhead over more units of production. When production exceeds sales, the recognition of some of the fixed overhead is delayed by placing it on the balance sheet as a part of inventories rather than on the income statement as a part of cost of goods sold. Under standard cost variance reporting, a work center with fixed labor costs can improve efficiency measures only by increasing output. Since this can happen more easily in a non-constrained process than in a constrained process, the result of building up inventories is inevitable. Instead of using absorption costing, most firms that have successfully implemented TOC use a variation of variable costing where only pure variable costs are subtracted from sales to arrive at profit margin or throughput. All other costs are subtracted from this margin as operating expenses. This form of variable costing is preferred over absorption costing for three primary reasons. It reduces the incentives to build up inventories. The recognition of fixed overhead costs cannot be delayed all of them are deducted as operating expenses to arrive at profit measures. It is considered more useful in decisions. Variable costing is more compatible with cost-volume-profit analysis than is absorption costing. It is closer to a cash flow concept of income measurement. This modification to the management accounting and reporting system implies that there are only three ways to increase profits: increase throughput (sales), decrease operating expenses (any costs not considered part of throughput), or decrease investment, particularly inventories.

8 This modification also suggests an important tool in evaluating the profitability of a firm s output - throughput dollars per unit of constrained resource (sometimes referred to as a critical resource factor). Additional readings that are of value in explaining TOC include: Goldratt, Eliyahu M. and Jeff Cox (1992). The Goal: A Process of Ongoing Improvement, 2nd ed. Great Barrington, MA: North River Press. Noreen, Eric, Debra Smith, and James T. Mackey (1995). The Theory of Constraints and Its Implications for Management Accounting. Great Barrington, MA: North River Press. MacArthur, John B. (1996). From activity-based costing to throughput accounting. Management Accounting, April Institute of Management Accountants. (1999). Theory of Constraints (TOC) Management System Fundamentals, Statement on Management Accounting 4HH. Montvale, NJ: IMA. Corbett, Thomas. (1999). Making better decisions. CMA Management, November Case Requirements Use the following requirements as a guide to help Emma assess the anticipated changes in the market and Sabbatical Marine s ability to capitalize on market opportunities. Prepare a memorandum addressed to Alexander James, President and CEO, with supporting documentation, outlining alternative courses of action for Sabbatical Marine to improve profitability. Case A Using the structure suggested by Emma (Exhibit 4), recast the FY2000 income statement into a throughput format segmented by product line. Determine the cost of underutilized labor resources. Case B Considering production constraints but ignoring the market constraints (i.e. ignore minimum market presence) what is the most profitable product mix for Sabbatical Marine? Considering both sets of constraints (i.e. production and minimum market presence), what is the most profitable product mix for Sabbatical Marine? Is the optimistic SMI demand estimate developed by Jack feasible with the current resources? Case C Prepare a budget for the coming year. Keep in mind the issues that Alexander, the President of Sabbatical Marine, outlined for Emma in their recent planning meeting. Use your judgment in incorporating the elements that you believe are relevant for Sabbatical Marine s management team to consider in preparing this budget for the coming year.