Ricardo Model. Sino-American Trade and Economic Conflict

|

|

|

- Cameron Palmer

- 6 years ago

- Views:

Transcription

1 1 of 18 6/10/2011 4:35 PM Sino-American Trade and Economic Conflict By Ralph E. Gomory and William J. Baumol March 22, 2011 In this note we look carefully at the impact on a developed nation of the economic development of its trading partner; a trading partner that is developing from a rather undeveloped state. If you want to keep the China-U.S. relationship and the impact on the United States of China s development in mind as a possible example, you will not go far wrong. We will discuss what a very standard model, the Ricardo model, shows about this situation. We will see that this very familiar model, properly analyzed, has a number of very unfamiliar consequences. Notably: The economic development of your trading partner can be harmful to you, the home country. Although the effect of that development starts out good, it ends badly. That there is a dominant and dominated relation possible between the two countries that is good for the dominant one and bad for the dominated one. A country can attain a dominant position only by having an undeveloped trading partner. This can occur naturally if the trading partner is simply there in an underdeveloped state, or the underdevelopment can be brought about by mercantilist actions that destroy that partner s industries. There is inherent conflict not only between a nation in a dominant position and its trading partner, but also between that dominant nation and what may loosely be called the interests of the world. In a two-country model of the sort we discuss here this simply is measured as the sum of the benefits obtained by the two countries economies. We assert that from a world point of view, having either nation dominant is bad. While a country cannot gain a dominant position solely by building up its industries, it can avoid a dominated position by developing its own industries and not allowing them to be destroyed. We will explain more clearly what we mean by these assertions as we go along... We will also explain enough about the Ricardo model to make that intelligible to those not already familiar with it. Ricardo Model This model, or at least pieces of it, has been taught to generations of students, and much of what is taught did not originate with Ricardo. It has been, and still is, enormously influential. (A good reference for this is Krugman and Ostfeld, International Economics, Theory and Policy, Chapter 8). Figures 1 and 2 (Appendix D) briefly describe the inputs to the Ricardo model and also what comes out of it. For those more deeply interested, the actual equations of the model and an explanation of them are attached as Appendix A. What the model does for you is this: You enter certain values, like the level of productivity, in various industries and the scale of the demand for the goods, the size of the labor force, etc. into the model (Figure 1). The model then computes the economic outcome, the result of trade between the nations you have described (Figure 3). For example, it computes which country produces how much of what products, what prices are, and also what products and product quantities the nations get to consume. However in this note we want to emphasize not the model itself, but the change in the economic results that come out of this very standard model, as we allow the nations to develop, i.e., increase, their productivities. The Ricardo Model itself is static, one set of inputs, one set of outputs. But we can use it to look at change by giving it a series of different inputs and looking at the different outputs that result.

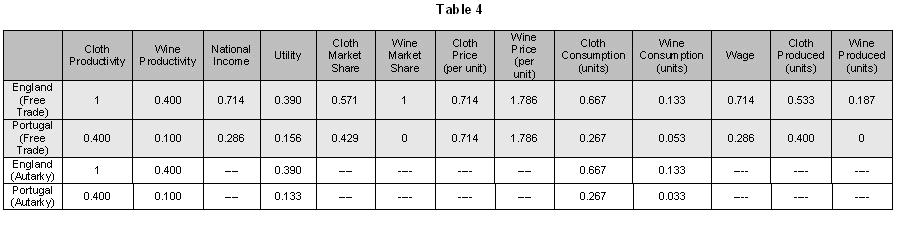

2 2 of 18 6/10/2011 4:35 PM The Simplest Model and Bar Charts We will start our discussion with a two-good model, the famous England-Portugal, wine-cloth model. But we will explore the results of the model not for just one set of inputs, but for several. Initially the inputs will reflect the improvement in the productivities of England s trading partner, Portugal. The model will allow us to explore the impact of Portugal s improvement on both countries. On this subject, the impact of your trading partner s development, there is a widespread belief, especially among those who have been exposed to the theory of comparative advantage, that improved productivity in your trading partner is not only good for your developing trading partner but also for you, the home country, as well. Although this belief is widespread, there is little basis for it in the economic literature. In fact, just to mention two famous names, Professor Hicks in his 1950 inaugural address and Paul Samuelson in a 2006 paper clearly state that the improvement of your trading partner s productivity can be harmful to you the home country. Not to mention the 2001 Gomory-Baumol book Global Trade and Conflicting National Interests in which this effect was the major topic. Nevertheless, the possibility that the model can show harm to the home country from the development of its trading partner, is almost never discussed. And the thought that in the real world the development of China might be bad for the United States is, in our experience, pretty unmentionable. An Example We now get ready to look at one example. In our discussion, we choose the unit of production so that the technological limit is expressed as a productivity of 1. For example, if the best possible output from cloth production is 2 rolls of cloth per worker per day, we choose two rolls as the unit of production, and producing two rolls is said to have a productivity level equal to 1. Producing, half as much, one roll a day, then is taken to give you a productivity of 0.5. At the start (Figure 3), Portugal is good at wine, productivity 1; England is good at cloth, productivity 1. Both are not nearly as productive in the other good. England is poor at wine, productivity 0.4, and Portugal is poor at making cloth, productivity 0.4. In addition to the productivities, the demand structure matters too. In our example both countries want to spend 2/3 of their income on cloth and only 1/3 on wine. Appendix D has a series of bar graphs showing the effect of Portugal improving its cloth productivity. Figure 4 and Figure 5 show the cloth and wine consumption of the two countries at the beginning, then after Portugal s cloth productivity improves from 0.4 to 0.7 and then after it improves further to 1.0. At the beginning we have a situation in which England makes all the cloth and Portugal makes all the wine. This is a good situation for England because England makes so much of what people want. The demand for cloth is assumed here (for illustration) to be twice as great as the demand for wine. Essentially England has the productive industry and Portugal has the unproductive one. The Portuguese are working at a low wage and 2/3 of what they make goes to be consumed in England. This is a good dominant position for England, and a poor position for Portugal. England s consumption of both cloth and wine is twice that of Portugal. a However, the Portuguese understand that too and they start to increase their productivity in textiles and get into making cloth. The second bar graph in Figure 6 shows immediately that the improvement in Portuguese cloth making is good for Portugal; it is good for Portugal even though Portugal s productivity, at 0.7, is still below England s 1.0. The second bar graph in Figure 7 also shows that this change has hurt England. b

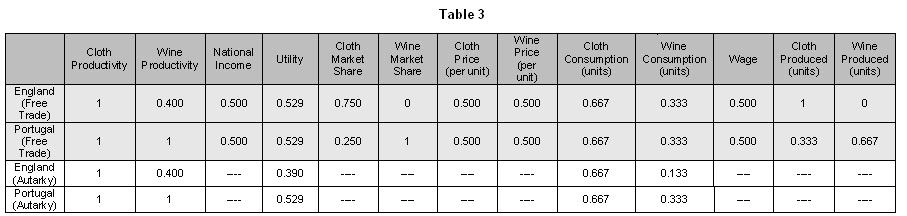

3 3 of 18 6/10/2011 4:35 PM When Portugal improves its cloth productivity to 1.0, matching England, the story is the same, only more so, with even bigger gains for Portugal. c Portugal improves its consumption of cloth at each step and its income and its utility both go up. England still makes only cloth but it now divides the cloth market with Portugal. Its share of world production has gone down, its share of world income has gone down, its exchange rate with Portugal has worsened, and it therefore gets less wine for its money than before. So at each step, England s wine consumption decreases while its cloth consumption holds stable. Meanwhile, it s all good for Portugal. Portugal s consumption improves at every step. What is going on? We will see below that this example is typical; it is common for the improvement in your trading partner to be harmful to the home country. But the idea that your partner s economic progress is always bad for you is not correct either. Let us extend out example. In this next example we start Portugal s development at an even lower state. Instead of Portugal initial productivities being (Cloth, Wine) = (0.4, 1.0) we will start Portugal s wine productivity at 0.1 and let it increase to 0.6 before arriving at the 1.0 which was Portugal s starting productivity in wine in our earlier example. Throughout we keep England s productivities fixed at (Cloth, Wine) = (1.0, 0.4) At our new starting position England s comparative advantage is in wine. It is the sole producer of wine and it divides the cloth market with Portugal. Although it is the sole producer of wine, it is nevertheless not very productive in wine, so its wine consumption is low. Its cloth consumption remains fixed at its autarky value, that is, the state at which it imports no cloth but produces it all at home. d As Portugal increases its wine productivity to 0.6 e and then to 1.0 we see that England s wine consumption goes steadily up while its cloth consumption is stable (Figure 6). Figure 7 shows us that Portugal first improves its consumption of both cloth and wine, and then at the second step it has a further gain in cloth consumption. Portugal s improved productivities have helped both countries. What we will see later in this note is that this example is typical. Generally if your trading partner moves from a very undeveloped to a more developed state, the effect on the home country is good. However after a rather early stage of development the effect changes and becomes bad for the home country. As we said in the introduction, the development of your trading partner starts out good but ends up being bad for you. Where we are going? We will next move beyond a single example. In fact we are we are going to go beyond one or two or three equilibrium examples and look instead at the pattern formed by all possible equilibria. That means that we will consider all productivities equal or less than 1. But to do this we have to shift gears and have a way to look at many outcomes in a way that will permit us to see the outcomes from many examples at the same time. The Utility-Income Diagram In our bar charts so far, we have seen the actual outputs in wine and cloth and also two summary terms, utility and income. Income tells you how what fraction of world value at current prices is created or consumed by a country, and utility is a measure of how satisfying the goods bought with that income were for the country s consumers. Throughout we use the standard Cobb-Douglas utility, which weights the quantities of goods consumed by the demands for them. f

4 4 of 18 6/10/2011 4:35 PM With a two good model just looking at the two goods usually tells you unambiguously which of two equilibrium outcomes is better without needing utility or an equivalent. But once you have more than two goods some measure like utility is definitely needed. When we reach the part of the note where we deal with more than two goods we will discuss this further and indicate why our results are relatively insensitive to the choice of measure. We will use Income and Utility to display the economic outcomes as points in an Income/Utility diagram (Figure 8). Income, or rather share of world income, is horizontal, utility is vertical. Up is goodness in this chart; points that are higher up have more utility and are better. To display the equilibrium result takes a pair of points. The height of the black point measures England s utility and its horizontal distance from the zero on the right its share of income. The gray dot s height shows Portugal s utility, and as the two shares add up to 1, its distance from the 1 on the horizontal scale measures its share of income. Up for a point is always good. Moving left to right increases England s share of world income, moving right to left increases Portugal s. Figure 9 has the five equilibrium points we calculated before. See how (moving from right to left) the points for Portugal go steadily up, meaning more utility and a better outcome for Portugal. But see also how those for England first go up and then go down. g An Important Observation We could also interpret the points in a different way. Let us take them in reverse order. We could start with Portugal having a productivity of 1 in cloth; then, as we move from left to right, Portugal s cloth productivity would go down step by step. Our diagram would clearly tell us that, for a while, Portugal s loss of productivity would help England. It would also tell us that if the Portuguese loss of productivity goes too far, then it starts to hurt England. Once you become aware of the possibility, in this standard model, that a country s loss can be its partner s gain, we also have to consider the possibility that perhaps in the real world, too, a country can gain from another s loss. Perhaps China can gain from losses in U.S. productivity. Moving toward the Basic Pattern Let s add a few more points to the picture. Ricardo s example in fact had Portugal more productive in both cloth and wine than England. But let s be generous; we will try out all sorts of different productivities. h Each gives us two points in the diagram (Figure 12). Higher points are good in this diagram; high points give a country more goods, especially the goods it wants. Points on the right are those in which country 1 (England) has a large share of world income. Those on the left give Portugal (Country 2) a large share. The Basic Two-Good Pattern If you look hard at Figure 10, you can see that the upper edge of the region where the points lie has a vague sort of shape. It is clearer if you look first at the highest black points and where they lie, and then at the highest gray ones. It is possible by mathematical analysis to short-circuit the tedious process of finding one new equilibrium point at a time. i There is an underlying pattern that emerges. Here it is: Figure 11. Note that all the black dots outcomes for country 1, England lie under the blue curve. All gray dots lie under the red curve. What the mathematical analysis shows is that if we were to compute all possible equilibria, all the space under the

5 5 of 18 6/10/2011 4:35 PM blue curve would be solidly filled with black dots and all the space under the red curve would be solidly filled with gray dots. Dots lying on or near these upper boundary curves are the highest and give the best outcomes. For any equilibrium dot below the boundary there is a boundary equilibrium that gives more to both countries. Our five examples from the bar charts are all on the boundary. Examining some Special Points It is clear that the starting point of our first example, located at the peak of the blue curve is the best possible for England (highest point), and that it is very poor for Portugal. At this point England makes all of the most desired good, cloth, at a high wage, and the entire Portuguese nation is devoted to the less desired good, wine, and receives a low wage. This arrangement is good for England and bad for Portugal. Since we are considering all possible productivities, we should also consider the point where Portugal is good at cloth and England good at wine with the productivities interchanged... That is the peak of the red curve. This is a good outcome for Portugal and a poor one for England. This is the point where Portugal would want to be. Remark: Two significant dominant points exist, an England dominant point and a Portugal dominant point. Each point produces 2/3 income for one, and 1/3 for the other. Each country strongly prefers this dominant outcome to someplace in the middle where each produces half the value of the world s goods. In the middle, between these two possibilities, is an equilibrium that is a compromise. In the two- good model we have been discussing, it is the equilibrium where England and Portugal divide the Cloth market, with England having the larger share,, and Portugal makes all the wine. j It is a very important outcome of our analysis that from the middle point a country cannot go to its dominant point without lowering the productivity of the trading partner. If Portugal cannot lower England s productivity in cloth, it cannot get from the middle to its best point. We will say more about the middle point as part of our discussion of the World Boundary Curve and larger models. World Utility, World Boundary Curve, and Three Important Points We can measure world utility, in this two country world in the same way as we measured national utility.- Essentially, you measure the outcome as if the two countries were one country, and give that combined country all the goods produced by the two countries. We measure the world output using the utility function of one or the other country. In this case, as we have the same demand structure, it does not make a difference which we choose. Each equilibrium then gives us a world utility dot in addition to the England and Portugal utility dots we have already. All these world utility dots lie under the World Boundary Curve which we see in Figure 12. In Figure 13, we mark the highest points on the England and Portugal and World Boundary curves. An important conclusion: Each country prefers to be dominant, with a dominated trading partner. The world however prefers something in the middle. There are therefore three special equilibria: the one that is best for England, the one that is best for Portugal, the one that is best for the world. Larger models At this point we should ask, Is this something special about the two-good model, or is this pattern one that persists as we add more and more different goods? The mathematical analysis shows the pattern persists.

6 We show here examples of a six-good model (Figure 14) and an 11 good model (Figure 15). In these models we also allowed the two countries to have different possible largest productivities. The largest possible values of the productivities of the two countries in these examples were not all 1. This enables us to discuss situations in which the countries have inherent productivity limitations; after all if they have no oil under their countries they cannot obtain a productivity of 1 in oil no matter how hard they try. Although less important than in Ricardo s time, countries still have inherent productivity differences. The data for these two models is given in Appendix C. The main difference that comes with size is that the lumpiness disappears, but more importantly the peak of the world curve is much higher relative to the dominant points associated with England or Portugal. Total world output and consumption suffers at these dominant points relative to the world maximum, because of the loss of productivity necessary to get to either one of the two dominant points. We see these effects in larger models, whether they are six-good, or eleven-good, or even larger. Note that in Figure 15 there is a limiting shape that usually starts to become clear with about 8 or more goods. The boundary curves approach the limiting curves as the number of goods increases. k In that shape we can see that as the red boundary curve lifts off from 0 and moves right, the blue curve goes up too. But after passing that dominant point, the blue trends steadily down. We see that there is an early phase where the red curve s rise benefits both countries, but after passing that dominant point the effect of red s further development is uniformly bad for blue. The effect of development starts good, but ends bad. Note that in our large examples, and this is what occurs in almost all examples, the world maximum occurs in the middle, far from either the England Dominant or the Portugal Dominant positions. l The remark we made in the two-good case, that from the middle point a country cannot go to its dominant point without lowering the productivity of the trading partner, generalizes to larger models. The statement for many-good models is this: Find the equilibrium that results when both countries are fully developed. Then: (1) Neither Country can get a better equilibrium without lowering the productivity of its trading partner in one of the industries in which the trading partner has positive market share at the classical equilibrium (2) Neither Country need accept a worse equilibrium unless it loses productivity on one of the industries in which it has a positive market share at the classical equilibrium. Summary In a world in which countries can learn and change their productivities, many things can happen that were really not possible in Ricardo s time. We have used the Ricardo Model to reflect this new world. In a world in which productivities are often not fixed by nature but are often acquired we have shown the following possibilities: That the economic development of a trading partner can be harmful to the home country.although the effect of that development starts good, it ends badly. That there is a dominant and dominated relation possible between two countries, a relation that is good for the dominant one and bad for the dominated one. That a country can attain a dominant position only by having an undeveloped trading partner. This can occur naturally if the trading partner is simply there in an underdeveloped state, or the underdevelopment can be brought about by mercantilist actions that destroy industries. There is inherent conflict not only between a nation in a dominant position but between that dominant partner and the interests of a two-county world. While a country cannot gain a dominant position by building up its industries, it can avoid a dominated position and assure a good outcome by developing a particular subset of its own industries and not allowing them to be destroyed. 6 of 18 6/10/2011 4:35 PM

7 7 of 18 6/10/2011 4:35 PM It is possible that the United States and China were in the dominant and dominated position some time ago. We should recognize that China s evolution away from that state can be harmful to the United States. Furthermore we can observe that China s gain has been accompanied by the disappearance or at least decline of a number of our industries. We need to be cautious because, as these standard models show, there is a distinct possibility that this situation can even lead to significant loss through deindustrialization in an initially prosperous economy. Let us make sure that we do not allow our industries to be destroyed so that we become a dominated nation. This very standard model suggests that such an outcome would be both disastrous for the U.S. and bad for the world. *You can try out various inputs or play with the Ricardo model by using our interactive spreadsheet. Notes a More detail on this outcome is given in Table 1, Appendix B b More detail on this outcome is given in Table 2, Appendix B c More detail on this outcome is given in Table 3, Appendix B d More detail on this outcome is given in Table 4, Appendix B e More detail on this outcome is given in Table 5, Appendix B f If a country consumes a quantity qi of the ith good and its demand for that good is d i then the Cobb-Douglas utility obtained d1 dn by the country is the product q 1 qn g The height of the black dot at each equilibrium is obtained by taking the Cobb- Douglas utility for Country 1 and dividing it by the Cobb-Douglas utility obtained with no trade (autarky) but with Country 1 fully developed, ( all productivities =1). This means that for Country 1 we are taking as the unit of utility the best Country 1 could attain alone, without any imports. That height is marked with a 1 on the U1 vertical scale. We do the same for Country 2, the height of each grey dot is measured against the 1 on the U2 vertical axis which is the best Country 2 can do without trade. h The simple spreadsheet calculation used to compute each equilibrium is attached with an explanation of how to use it. This enables our readers to produce equilibria with productivities and demands of their own choosing. i The methods required for this come from the area of integer programming, a subject one of us (Gomory) pioneered some fifty years ago. j Table 3, Appendix B k The limiting curves are discussed in detail in Reference 4. Furthermore, for each Z 1 value it can be shown that there is a finite list of equilibria that dominate the rest. For every equilibrium not on that finite list there is an equilibrium in the list that produces as much or more of every good. In addition all these strong equilibria lie close to the boundary curves. If we were to choose a different way to measure outcomes, that would produce new boundary curves, but those boundary curves could only pass through members of this list and can therefore not look very different from those we have now. l The world maximum is closely associated with what in our earlier papers we call the classical equilibrium. This is the equilibrium obtained when both countries have obtained their maximal productivities. For example in the example 6 good model, the classical equilibrium assigns three industries in the order of their comparative advantage to England, the remaining three to Portugal. When demands are the same in both countries the World Boundary Maximum is directly above the classical equilibrium.

8 8 of 18 6/10/2011 4:35 PM References 1. "A Ricardo Model with Economies of Scale," Ralph E. G omory, Journal of Economic Theory, April 1994, Volume 62, No. 2, pp "A Linear Ricardo Model With Varying Parameters," Ralph E. Gomory and William J. Baumol, Proceedings of the National Academy of Sciences, U.S.A., 1995, Vol. 92, pp "Analysis of Linear Trade Models and Relation to Scale Economies, " Ralph E. Gomory and William J. Baumol, " Proceedings of the National Academy of Sciences, U.S.A., 1997, Vol. 94, pp National Trade Conflicts Caused by Productivity Changes: The Analysis With Full Proofs," Ralph E. Gomory and William J. Baumol, C. V. Starr Economic Research Report (New York University), November 1998, RR # Global Trade and Conflicting National Interests, Book, Ralph E. Gomory and William J. Baumol MIT Press, Cambridge, MA, Globalization: Country and company interests in conflict. Gomory, R., & Baumol, W J. Journal of Policy Modeling (2009). 7. "Trade, Education, and Innovation: Prospects for the U.S. Economy Ralph E. Gomory and William J. Baumol, Journal of Policy Modeling (to appear). Appendix A: Equilibrium Equations Notation In our standard Ricardian model there are two countries and n industries. The quantity q i, j of good i produced in Country j is determined by linear production function e i, j l i, j with l. i, j denoting the amount of labor employed in Country j in producing good i. The size of labor force for each country is L j. Country j s consumption of good i is denoted by y i, j and its production of good i by q i, j. Country j s productionshare or market share of world output of good i is represented by x i, j = q i, j / (q i, 1 +q i, 2 ), so that the vector x = (x i, j ) describes the pattern of production. Each of the two countries participating in trade has a given utility function of Cobb-Douglas form with demand parameters d i, j. The price of good i, p i, and w j, the wage in Country j, and Y j the national income of Country j. are all expressed in monetary units. The standard equilibrium equations given below are homogenous in these variables. This means that if we choose a different monetary unit thus replacing any set of p i, w j, and Y j values at an equilibrium by kp i, kw j, and ky j, these values too would satisfy the equilibrium conditions while leaving all the non-pecuniary variables such as q i, j andl. i, j unchanged. We eliminate this ambiguity by choosing at each equilibrium the monetary unit, the MU, that that makes the total world income Y 1 +Y 2 = 1 MU. The national incomes with this normalization we will refer to as Z 1 and Z 2. We will then have at each equilibrium uniquely determined pecuniary values and the uniquely determined national income, expressed in MU units, satisfy Z 1 +Z 2 =1. Equilibrium Conditions For any given vector of productivity parameters e= {e i, j } there is a stable equilibrium giving a national income Z j and a utility U j for each country.

9 9 of 18 6/10/2011 4:35 PM The first equilibrium condition stares that national income or consumption Z j in Country j must equal the total value of the goods produced in Country j.. With a Cobb-Douglas utility each country spends d i, j Z j on good i, so total world expenditure on the ith good is (d i,1 Z 1 +d i,2 Z 2 ). Since the fraction produced in each country is x i,j the balance of the value of production and consumption requires for each country: (1.1) Second, we have a zero-profit condition. World expenditure on Country j's output of good i all goes into the wages of the labor l i, j employed in that industry, so: (1.2) Third, is the full-employment requirement for each country: This is expressed as the condition that the wage rate times the country's total labor force equals national income:(the wage rate condition): (1.3) Fourth, we have the requirement that, for each good the value of the output of good i at the equilibrium price p i equals the total amount consumers are willing to spend on it: (1.4) Where the second form of (1.4) follows directly from the first by multiplying through by x i, j = q i,j /(q i,1 +q i,2) and using (1.2). Finally, we have the conditions that require that in each industry production, or equivalently market share, is always assigned to the producer or producers with the lowest unit cost. For example, if in industry i, w 1 /e i,1 < w 2 /e i,2, then x i, 1 =1 and x i, 2 = 0. More generally: (1.5) It is of course the actual producer s unit cost that determines the price p i. The conditions (1.5) include the familiar comparative-advantage criterion. Note that because of (1.1) the equilibrium conditions include balanced trade.

10 10 of 18 6/10/2011 4:35 PM Appendix B

![11 of 18 6/10/2011 4:35 PM Appendix C Data used for the six good model Labor force sizes: L[1]=L[2]=1 Maximum Possible Productivities: e[1]={1,1,1,1,0.7,0.5}, e[2]={0.5,0.7,1,1,1,1}.](/docs-images/71/65844109/images/11-0.jpg "In four of the six industries one country or the other is limited in its productivity. This could represent, for example, the absence of natural gas or oil or some other natural resource.")

11 11 of 18 6/10/2011 4:35 PM Appendix C Data used for the six good model Labor force sizes: L[1]=L[2]=1 Maximum Possible Productivities: e[1]={1,1,1,1,0.7,0.5}, e[2]={0.5,0.7,1,1,1,1}. In four of the six industries one country or the other is limited in its productivity. This could represent, for example, the absence of natural gas or oil or some other natural resource. The third and fourth industries are industries in which a high level of output is attainable for both countries. Demands: d[]1=d[2]= (1/6,1/6,1/6,1/6,1/6,1/6}. There is an equal demand for all six industries. Eleven Good Model In contrast to the six good model, in this eleven good model the numbers both for the maximum possible productivities and for the demands have no particular structure. Country 1 Maximum Productivities: e[1]={0.97, 0.92, 0.72, 0.94, 0.84, 0.52, 0.73, 0.77, 0.53, 0.91, 0.89} Country 2 Maximum Productivities: e[2]={0.52, 0.61, 0.91, 0.92, 0.84, 0.97, 0.83, 0.92, 0.31, 0.83, 0.72} Country 1 demand: d[1] = {0.033, 0.140, 0.073, 0.100, 0.153, 0.046, 0.053, 0.066, 0.133, 0.086, 0.113} Country 2 demand: d[2] = {0.080, 0.806, 0.169, 0.112, 0.177, 0.032, 0.048, 0.104, 0.056, 0.096, 0.040} Additional note: This is also the first example in which the two countries have different demand structures. If you look closely at Figure 15 you will see that the world boundary does not come down exactly to the unit level of the U2 vertical axis. This is because we are using the utility function of Country 1 to measure the value of total world output. When this measure is applied to Country 1 output alone, which is what we see on the extreme right of the diagram, it should come out as 1 which it does. But when applied to the Country 2 output alone, as it is on the extreme left (Country 2 share = 1) there is no reason for it to produce the 1 which is what the Country 2 utility function would produce. Appendix D Figure 1

12 12 of 18 6/10/2011 4:35 PM Figure 2 Figure 3

13 13 of 18 6/10/2011 4:35 PM Figure 4 Figure 5

14 14 of 18 6/10/2011 4:35 PM Figure 6 Figure 7

15 15 of 18 6/10/2011 4:35 PM Figure 8 Figure 9

16 16 of 18 6/10/2011 4:35 PM Figure 10 Figure 11

17 17 of 18 6/10/2011 4:35 PM Figure 12 Figure 13 Figure 14

18 18 of 18 6/10/2011 4:35 PM Figure 15 Issues: Economic Growth The New America Foundation 1899 L Street, N.W., Suite 400, Washington, DC th Street, Suite 901, Sacramento, CA Additional Contact Info New America is a registered trademark of the New America Foundation.

Final Exam - Answers

Page 1 of 8 December 20, 2000 Answer all questions. Write your answers in a blue book. Be sure to look ahead and budget your time. Don t waste time on parts of questions that you can t answer. Leave space

Page 1 of 8 December 20, 2000 Answer all questions. Write your answers in a blue book. Be sure to look ahead and budget your time. Don t waste time on parts of questions that you can t answer. Leave space

Economics 448W, Notes on the Classical Supply Side Professor Steven Fazzari

Economics 448W, Notes on the Classical Supply Side Professor Steven Fazzari These notes cover the basics of the first part of our classical model discussion. Review them in detail prior to the second class

Economics 448W, Notes on the Classical Supply Side Professor Steven Fazzari These notes cover the basics of the first part of our classical model discussion. Review them in detail prior to the second class

Chapter 8: Exchange. 8.1: Introduction. 8.2: Exchange. 8.3: Individual A s Preferences and Endowments

Chapter 8: Exchange 8.1: Introduction In many ways this chapter is the most important in the book. If you have time to study just one, this is the one that you should study (even though it might be a bit

Chapter 8: Exchange 8.1: Introduction In many ways this chapter is the most important in the book. If you have time to study just one, this is the one that you should study (even though it might be a bit

Cambridge University Press Modeling Monetary Economies, Second Edition - Bruce Champ and Scott Freeman Excerpt More information.

Part I Money IN PART I we develop and learn to work with our most basic model of money, applying it to the study of fiat and commodity monies, inflation, and international monetary systems. In studying

Part I Money IN PART I we develop and learn to work with our most basic model of money, applying it to the study of fiat and commodity monies, inflation, and international monetary systems. In studying

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect. The substitution effect of a

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect The substitution effect of a price change is the change that would have happened if income

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect The substitution effect of a price change is the change that would have happened if income

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect. The substitution effect of a

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect The substitution effect of a price change is the change that would have happened if income

It is useful to think of a price change as having two distinct effects, a substitution effect and an income effect The substitution effect of a price change is the change that would have happened if income

Using this information, we then write the output of a firm as

Economists typically assume that firms or a firm s owners try to maximize their profit. et R be revenues of the firm, and C be the cost of production, then a firm s profit can be represented as follows,

Economists typically assume that firms or a firm s owners try to maximize their profit. et R be revenues of the firm, and C be the cost of production, then a firm s profit can be represented as follows,

Practice Midterm Exam Microeconomics: Professor Owen Zidar

Practice Midterm Exam Microeconomics: 33001 Professor Owen Zidar This exam is comprised of 3 questions. The exam is scheduled for 1 hour and 30 minutes. This is a closed-book, closed-note exam. There is

Practice Midterm Exam Microeconomics: 33001 Professor Owen Zidar This exam is comprised of 3 questions. The exam is scheduled for 1 hour and 30 minutes. This is a closed-book, closed-note exam. There is

CHAPTER 4, SECTION 1

DAILY LECTURE CHAPTER 4, SECTION 1 Understanding Demand What Is Demand? Demand is the willingness and ability of buyers to purchase different quantities of a good, at different prices, during a specific

DAILY LECTURE CHAPTER 4, SECTION 1 Understanding Demand What Is Demand? Demand is the willingness and ability of buyers to purchase different quantities of a good, at different prices, during a specific

Intermediate Macroeconomics

Intermediate Macroeconomics ECON 3312 Lecture 2 William J. Crowder Ph.D. Mercantilism Economic Nationalism Beggar-thy-neighbor policies Bullionism Regulate everything! Trade restrictions Monopoly rights

Intermediate Macroeconomics ECON 3312 Lecture 2 William J. Crowder Ph.D. Mercantilism Economic Nationalism Beggar-thy-neighbor policies Bullionism Regulate everything! Trade restrictions Monopoly rights

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 01

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 01

No 10. Chapter 11. Introduction. Real Wage Rigidity: A Question. Keynesianism: Wage and Price Rigidity

No 10. Chapter 11 Keynesianism: Wage and Price Rigidity Introduction We earlier described the Keynesian interpretation of the IS-LM AS-AD Model The Keynesian model assumes that there exists a horizontal

No 10. Chapter 11 Keynesianism: Wage and Price Rigidity Introduction We earlier described the Keynesian interpretation of the IS-LM AS-AD Model The Keynesian model assumes that there exists a horizontal

LECTURE NOTES ON MICROECONOMICS

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part : Consumers and demand Chapter 3: Preferences and utility Section 3.1: Preferences and indifference curves Bundles.

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part : Consumers and demand Chapter 3: Preferences and utility Section 3.1: Preferences and indifference curves Bundles.

Professor David N. Weil Fall, Econ 1560 Second Midterm Exam

Professor David N. Weil Fall, 2012 Econ 1560 Second Midterm Exam Instructions: Please answer all questions in the blue books. You may not use notes, books, or calculators. Please show your work. There

Professor David N. Weil Fall, 2012 Econ 1560 Second Midterm Exam Instructions: Please answer all questions in the blue books. You may not use notes, books, or calculators. Please show your work. There

ECONOMICS 103. Topic 3: Supply, Demand & Equilibrium

ECONOMICS 103 Topic 3: Supply, Demand & Equilibrium Assumptions of the competitive market model: all agents are price takers, homogeneous products. Demand & supply: determinants of demand & supply, demand

ECONOMICS 103 Topic 3: Supply, Demand & Equilibrium Assumptions of the competitive market model: all agents are price takers, homogeneous products. Demand & supply: determinants of demand & supply, demand

Online Student Guide Types of Control Charts

Online Student Guide Types of Control Charts OpusWorks 2016, All Rights Reserved 1 Table of Contents LEARNING OBJECTIVES... 4 INTRODUCTION... 4 DETECTION VS. PREVENTION... 5 CONTROL CHART UTILIZATION...

Online Student Guide Types of Control Charts OpusWorks 2016, All Rights Reserved 1 Table of Contents LEARNING OBJECTIVES... 4 INTRODUCTION... 4 DETECTION VS. PREVENTION... 5 CONTROL CHART UTILIZATION...

Should Consumers Be Priced Out of Pollution-Permit Markets?

Should Consumers Be Priced Out of Pollution-Permit Markets? Stefani C. Smith and Andrew J. Yates Abstract: The authors present a simple diagrammatic exposition of a pollutionpermit market in which both

Should Consumers Be Priced Out of Pollution-Permit Markets? Stefani C. Smith and Andrew J. Yates Abstract: The authors present a simple diagrammatic exposition of a pollutionpermit market in which both

Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007

Answer Key Nov 13, 2007") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and label

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and label

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 1

Economics 2 Spring 2019 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 1 1.a. Opportunity cost is defined as the value of what is forgone to undertake an activity. What you

Economics 2 Spring 2019 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 1 1.a. Opportunity cost is defined as the value of what is forgone to undertake an activity. What you

The Basic Spatial Model with a Single Monopolist

Economics 335 March 3, 999 Notes 8: Models of Spatial Competition I. Product differentiation A. Definition Products are said to be differentiated if consumers consider them to be imperfect substitutes.

Economics 335 March 3, 999 Notes 8: Models of Spatial Competition I. Product differentiation A. Definition Products are said to be differentiated if consumers consider them to be imperfect substitutes.

Fin 345: Lesson 2 (Part 3) Instructor Glenn E. Crellin Slide #1. Slide Title: Fin 345 Lesson 2 (Part 3)

Instructor Glenn E. Crellin Slide #1. Slide Title: Fin 345 Lesson 2 (Part 3)") Fin 345: Lesson 2 (Part 3) Instructor Glenn E. Crellin Slide #1 Slide Title: Fin 345 Lesson 2 (Part 3) -Fin 345 Lesson 2 (Part 3) -Understanding Real Estate Markets -Floyd & Allen -Real Estate Principles,

Fin 345: Lesson 2 (Part 3) Instructor Glenn E. Crellin Slide #1 Slide Title: Fin 345 Lesson 2 (Part 3) -Fin 345 Lesson 2 (Part 3) -Understanding Real Estate Markets -Floyd & Allen -Real Estate Principles,

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management Solutions to Assignment #3 Wednesday, October 14, 1998 Reading Assignment:

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management Solutions to Assignment #3 Wednesday, October 14, 1998 Reading Assignment:

Business Cycle Theory Revised: March 25, 2009

The Global Economy Class Notes Business Cycle Theory Revised: March 25, 2009 We ve seen that economic fluctuations follow regular patterns and that these patterns can be used to forecast the future. For

The Global Economy Class Notes Business Cycle Theory Revised: March 25, 2009 We ve seen that economic fluctuations follow regular patterns and that these patterns can be used to forecast the future. For

2 THINKING LIKE AN ECONOMIST

2 THINKING LIKE AN ECONOMIST LEARNING OBJECTIVES: By the end of this chapter, students should understand: how economists apply the methods of science. how assumptions and models can shed light on the world.

2 THINKING LIKE AN ECONOMIST LEARNING OBJECTIVES: By the end of this chapter, students should understand: how economists apply the methods of science. how assumptions and models can shed light on the world.

ECON 210 MICROECONOMIC THEORY FINAL EXAM, FALL 2005

ECON 210 MICROECONOMIC THEORY FINAL EXAM, FALL 2005 PROFESSOR JOSEPH GUSE Instructions. You have 3 hours to complete the exam. There are a total of 90 points available. It is designed to take about 1 minute

ECON 210 MICROECONOMIC THEORY FINAL EXAM, FALL 2005 PROFESSOR JOSEPH GUSE Instructions. You have 3 hours to complete the exam. There are a total of 90 points available. It is designed to take about 1 minute

Midterm 2 - Solutions

Ecn 100 - Intermediate Microeconomics University of California - Davis November 12, 2010 Instructor: John Parman Midterm 2 - Solutions You have until 11:50am to complete this exam. Be certain to put your

Ecn 100 - Intermediate Microeconomics University of California - Davis November 12, 2010 Instructor: John Parman Midterm 2 - Solutions You have until 11:50am to complete this exam. Be certain to put your

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1 Solutions to Assignment #12 January 22, 1999 Reading Assignment: Please

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1 Solutions to Assignment #12 January 22, 1999 Reading Assignment: Please

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1 Solutions to Assignment #12 January 22, 1999 Reading Assignment: Please

Guided Study Program in System Dynamics System Dynamics in Education Project System Dynamics Group MIT Sloan School of Management 1 Solutions to Assignment #12 January 22, 1999 Reading Assignment: Please

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A.

The answer to this question is A, corresponding to Form A.") This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

Unit QUAN Session 6. Introduction to Acceptance Sampling

Unit QUAN Session 6 Introduction to Acceptance Sampling MSc Strategic Quality Management Quantitative methods - Unit QUAN INTRODUCTION TO ACCEPTANCE SAMPLING Aims of Session To introduce the basic statistical

Unit QUAN Session 6 Introduction to Acceptance Sampling MSc Strategic Quality Management Quantitative methods - Unit QUAN INTRODUCTION TO ACCEPTANCE SAMPLING Aims of Session To introduce the basic statistical

6) Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.

Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.") These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

What is Utility: Total utility & Marginal utility:

Economic Theory of Consumer Behavior * What is utility. * Define total utility and marginal utility.*** * State the law of diminishing marginal utility.**** * Define indifference curve and indifference

Economic Theory of Consumer Behavior * What is utility. * Define total utility and marginal utility.*** * State the law of diminishing marginal utility.**** * Define indifference curve and indifference

Tutorial Formulating Models of Simple Systems Using VENSIM PLE System Dynamics Group MIT Sloan School of Management Cambridge, MA O2142

Tutorial Formulating Models of Simple Systems Using VENSIM PLE System Dynamics Group MIT Sloan School of Management Cambridge, MA O2142 Originally prepared by Nelson Repenning. Vensim PLE 5.2a Last Revision:

Tutorial Formulating Models of Simple Systems Using VENSIM PLE System Dynamics Group MIT Sloan School of Management Cambridge, MA O2142 Originally prepared by Nelson Repenning. Vensim PLE 5.2a Last Revision:

IMF MACRO CONFERENCE RODRIK PRESENTATION

IMF MACRO CONFERENCE Before this panel, we were talking with Mike Spence, and he said he was glad we were having this session on growth. Of course, it s not as if the crisis completely eradicated the field.

IMF MACRO CONFERENCE Before this panel, we were talking with Mike Spence, and he said he was glad we were having this session on growth. Of course, it s not as if the crisis completely eradicated the field.

Beginning of the End? Oil Companies Cut Back on Spending

Our Finite World Exploring how oil limits affect the economy Beginning of the End? Oil Companies Cut Back on Spending Posted on February 25, 2014 Steve Kopits recently gave a presentation explaining our

Our Finite World Exploring how oil limits affect the economy Beginning of the End? Oil Companies Cut Back on Spending Posted on February 25, 2014 Steve Kopits recently gave a presentation explaining our

Optimization Prof. Debjani Chakraborty Department of Mathematics Indian Institute of Technology, Kharagpur

Optimization Prof. Debjani Chakraborty Department of Mathematics Indian Institute of Technology, Kharagpur Lecture - 39 Multi Objective Decision Making Decision making problem is a process of selection

Optimization Prof. Debjani Chakraborty Department of Mathematics Indian Institute of Technology, Kharagpur Lecture - 39 Multi Objective Decision Making Decision making problem is a process of selection

A Classroom Experiment on Import Tariffs and Quotas Under Perfect and Imperfect Competition

MPRA Munich Personal RePEc Archive A Classroom Experiment on Import Tariffs and Quotas Under Perfect and Imperfect Competition Sean Mulholland Stonehill College 4. November 2010 Online at http://mpra.ub.uni-muenchen.de/26442/

MPRA Munich Personal RePEc Archive A Classroom Experiment on Import Tariffs and Quotas Under Perfect and Imperfect Competition Sean Mulholland Stonehill College 4. November 2010 Online at http://mpra.ub.uni-muenchen.de/26442/

2 The Action Axiom, Preference, and Choice in General

Introduction to Austrian Consumer Theory By Lucas Engelhardt 1 Introduction One of the primary goals in any Intermediate Microeconomic Theory course is to explain prices. The primary workhorse for explaining

Introduction to Austrian Consumer Theory By Lucas Engelhardt 1 Introduction One of the primary goals in any Intermediate Microeconomic Theory course is to explain prices. The primary workhorse for explaining

Chapter 2. The Basic Theory Using Demand and Supply. Overview

Chapter 2 The Basic Theory Using Demand and Supply Overview This chapter indicates why we study theories of international trade and presents the basic theory using supply and demand curves. Trade is important

Chapter 2 The Basic Theory Using Demand and Supply Overview This chapter indicates why we study theories of international trade and presents the basic theory using supply and demand curves. Trade is important

1 Competitive Equilibrium

1 Competitive Equilibrium Each household and each firm in the economy act independently from each other, seeking their own interest, and taking as given the fact that other agents will also seek their

1 Competitive Equilibrium Each household and each firm in the economy act independently from each other, seeking their own interest, and taking as given the fact that other agents will also seek their

P rofit t (1 + i) t. V alue = t=0

t. V alue = t=0") These notes correspond to Chapter 2 of the text. 1 Optimization A key concept in economics is that of optimization. It s a tool that can be used for many applications, but for now we will use it for pro

These notes correspond to Chapter 2 of the text. 1 Optimization A key concept in economics is that of optimization. It s a tool that can be used for many applications, but for now we will use it for pro

Networks: Fall 2010 Homework 5 David Easley and Eva Tardos Due November 11, 2011

Networks: Fall 2010 Homework 5 David Easley and Eva Tardos Due November 11, 2011 As noted on the course home page, homework solutions must be submitted by upload to the CMS site, at https://cms.csuglab.cornell.edu/.

Networks: Fall 2010 Homework 5 David Easley and Eva Tardos Due November 11, 2011 As noted on the course home page, homework solutions must be submitted by upload to the CMS site, at https://cms.csuglab.cornell.edu/.

Chapter 5. Market Equilibrium 5.1 EQUILIBRIUM, EXCESS DEMAND, EXCESS SUPPLY

Chapter 5 Price SS p f This chapter will be built on the foundation laid down in Chapters 2 and 4 where we studied the consumer and firm behaviour when they are price takers. In Chapter 2, we have seen

Chapter 5 Price SS p f This chapter will be built on the foundation laid down in Chapters 2 and 4 where we studied the consumer and firm behaviour when they are price takers. In Chapter 2, we have seen

Planning Economics December 6, Practice Problems for the Economic Structure of Cities (These are homework problems from earlier years.

DUSP 11.202 Frank Levy Planning Economics December 6, 2010 Practice Problems for the Economic Structure of Cities (These are homework problems from earlier years.) 1) In the pumpkin model discussed in

DUSP 11.202 Frank Levy Planning Economics December 6, 2010 Practice Problems for the Economic Structure of Cities (These are homework problems from earlier years.) 1) In the pumpkin model discussed in

CHAPTER 2 Production Possibilities Frontier Framework

CHAPTER 2 Production Possibilities Frontier Framework Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

CHAPTER 2 Production Possibilities Frontier Framework Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

Module 18 Aggregate Supply: Introduction and Determinants

Module 18 Supply: Introduction and Determinants What you will learn in this Module: How the aggregate supply curve illustrates the relationship between the aggregate price level and the quantity of aggregate

Module 18 Supply: Introduction and Determinants What you will learn in this Module: How the aggregate supply curve illustrates the relationship between the aggregate price level and the quantity of aggregate

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING In many economic situations, there exists asymmetric information between the di erent agents. Examples are abundant: A seller has better information

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING In many economic situations, there exists asymmetric information between the di erent agents. Examples are abundant: A seller has better information

Economics 352: Intermediate Microeconomics. Notes and Sample Questions Chapter Ten: The Partial Equilibrium Competitive Model

Economics 352: Intermediate Microeconomics Notes and Sample uestions Chapter Ten: The artial Euilibrium Competitive Model This chapter will investigate perfect competition in the short run and in the long

Economics 352: Intermediate Microeconomics Notes and Sample uestions Chapter Ten: The artial Euilibrium Competitive Model This chapter will investigate perfect competition in the short run and in the long

Department of Economics. Harvard University. Spring Honors General Exam. April 6, 2011

Department of Economics. Harvard University. Spring 2011 Honors General Exam April 6, 2011 The exam has three sections: microeconomics (Questions 1 3), macroeconomics (Questions 4 6), and econometrics

Department of Economics. Harvard University. Spring 2011 Honors General Exam April 6, 2011 The exam has three sections: microeconomics (Questions 1 3), macroeconomics (Questions 4 6), and econometrics

Part One. What Is Economics?

Part 1: What Is Economics? 1 Part One What Is Economics? This opening Part of the book provides an introduction to economics. The central themes of Chapter 1 are scarcity, choice, opportunity cost, and

Part 1: What Is Economics? 1 Part One What Is Economics? This opening Part of the book provides an introduction to economics. The central themes of Chapter 1 are scarcity, choice, opportunity cost, and

1 Applying the Competitive Model. 2 Consumer welfare. These notes essentially correspond to chapter 9 of the text.

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

Full file at

Chapter 1 There are no Questions in Chapter 1 1 Chapter 2 In-Chapter Questions 2A. Remember that the slope of the line is the coefficient of x. When that coefficient is positive, there is a direct relationship

Chapter 1 There are no Questions in Chapter 1 1 Chapter 2 In-Chapter Questions 2A. Remember that the slope of the line is the coefficient of x. When that coefficient is positive, there is a direct relationship

Interpreting Price Elasticity of Demand

INTRO Go to page: Go to chapter Bookmarks Printed Page 466 Interpreting Price 9 Behind the 48.2 The Price of Supply 48.3 An Menagerie Producer 49.1 Consumer and the 49.2 Producer and the 50.1 Consumer,

INTRO Go to page: Go to chapter Bookmarks Printed Page 466 Interpreting Price 9 Behind the 48.2 The Price of Supply 48.3 An Menagerie Producer 49.1 Consumer and the 49.2 Producer and the 50.1 Consumer,

A new framework for digital publishing decisions 95. Alastair Dryburgh. Alastair Dryburgh 2003

A new framework for digital publishing decisions 95 Learned Publishing (2003)16, 95 101 Introduction In my previous article 1 I looked in detail at how developments in publishing were creating problems

A new framework for digital publishing decisions 95 Learned Publishing (2003)16, 95 101 Introduction In my previous article 1 I looked in detail at how developments in publishing were creating problems

DOWNLOAD PDF JOB SEARCH IN A DYNAMIC ECONOMY

Chapter 1 : Job Search General Dynamics JOB SEARCH IN A DYNAMIC ECONOMY The random variable N, the number of offers until R is exceeded, has a geometric distribution with parameter p = 1 - F(R) and expected

Chapter 1 : Job Search General Dynamics JOB SEARCH IN A DYNAMIC ECONOMY The random variable N, the number of offers until R is exceeded, has a geometric distribution with parameter p = 1 - F(R) and expected

System Dynamics Group Sloan School of Management Massachusetts Institute of Technology

System Dynamics Group Sloan School of Management Massachusetts Institute of Technology Introduction to System Dynamics, 15.871 System Dynamics for Business Policy, 15.874 Professor John Sterman Professor

System Dynamics Group Sloan School of Management Massachusetts Institute of Technology Introduction to System Dynamics, 15.871 System Dynamics for Business Policy, 15.874 Professor John Sterman Professor

Notes on Chapter 10 OUTPUT AND COSTS

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Evaluation of Police Patrol Patterns

-1- Evaluation of Police Patrol Patterns Stephen R. Sacks University of Connecticut Introduction The Desktop Hypercube is an interactive tool designed to help planners improve police services without additional

-1- Evaluation of Police Patrol Patterns Stephen R. Sacks University of Connecticut Introduction The Desktop Hypercube is an interactive tool designed to help planners improve police services without additional

Final Exam - Solutions

Ecn 00 - Intermediate Microeconomic Theory University of California - Davis September 9, 009 Instructor: John Parman Final Exam - Solutions You have until :50pm to complete this exam. Be certain to put

Ecn 00 - Intermediate Microeconomic Theory University of California - Davis September 9, 009 Instructor: John Parman Final Exam - Solutions You have until :50pm to complete this exam. Be certain to put

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 31 Standard Costing - Material, Labor and Overhead Variances Dear students,

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 31 Standard Costing - Material, Labor and Overhead Variances Dear students,

Consumer and Producer Surplus and Deadweight Loss

Consumer and Producer Surplus and Deadweight Loss The deadweight loss, value of lost time or quantity waste problem requires several steps. A ceiling or floor price must be given. We call that price the

Consumer and Producer Surplus and Deadweight Loss The deadweight loss, value of lost time or quantity waste problem requires several steps. A ceiling or floor price must be given. We call that price the

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

These notes are to be read together with the Chapter in your text. They are complements not substitutes! 2

Tales of the Specific Factor Model 1 (Let me know if you spot errors.) The Specific Factor Model was developed by the distinguished University of Rochester economist, Ronald W. Jones in the mid-1960s.

Tales of the Specific Factor Model 1 (Let me know if you spot errors.) The Specific Factor Model was developed by the distinguished University of Rochester economist, Ronald W. Jones in the mid-1960s.

Andy consumes baseball cards and football cards.

Economics 301 - Homework 3 Fall 006 Stacy Dickert-Conlin Name Due: September 8, at the start of class Three randomly selected questions will be graded for credit. All graded questions are worth 10 points.

Economics 301 - Homework 3 Fall 006 Stacy Dickert-Conlin Name Due: September 8, at the start of class Three randomly selected questions will be graded for credit. All graded questions are worth 10 points.

2. Why is a firm in a purely competitive labor market a wage taker? What would happen if it decided to pay less than the going market wage rate?

Chapter Wage Determination QUESTIONS. Explain why the general level of wages is high in the United States and other industrially advanced countries. What is the single most important factor underlying

Chapter Wage Determination QUESTIONS. Explain why the general level of wages is high in the United States and other industrially advanced countries. What is the single most important factor underlying

Module 55 Firm Costs. What you will learn in this Module:

What you will learn in this Module: The various types of cost a firm faces, including fixed cost, variable cost, and total cost How a firm s costs generate marginal cost curves and average cost curves

What you will learn in this Module: The various types of cost a firm faces, including fixed cost, variable cost, and total cost How a firm s costs generate marginal cost curves and average cost curves

Chapter 12 outline The shift from consumers to producers

Chapter 12 outline The shift from consumers to producers Resource markets are markets in which business firms demand factors of production from household suppliers. (As you can see the tables are now turned

Chapter 12 outline The shift from consumers to producers Resource markets are markets in which business firms demand factors of production from household suppliers. (As you can see the tables are now turned

Chapter 6 TRADE AND LOCAL INCOME DISTRIBUTION: THE SPECIFIC FACTORS MODEL

Chapter 6 TRADE AND LOCAL INCOME DISTRIBUTION: THE SPECIFIC FACTORS MODEL One of the main implications of the Ricardian model is that everyone is better off with free trade. Workers can earn higher wages

Chapter 6 TRADE AND LOCAL INCOME DISTRIBUTION: THE SPECIFIC FACTORS MODEL One of the main implications of the Ricardian model is that everyone is better off with free trade. Workers can earn higher wages

ECONOMICS U$A PROGRAM #2 THE FIRM: HOW CAN IT KEEP COSTS DOWN?

ECONOMICS U$A PROGRAM #2 THE FIRM: HOW CAN IT KEEP COSTS DOWN? AUDIO PROGRAM TRANSCRIPT ECONOMICS U$A PROGRAM #2 THE FIRM (MUSIC PLAYS) Announcer: Funding for this program was provided by Annenberg Learner.

ECONOMICS U$A PROGRAM #2 THE FIRM: HOW CAN IT KEEP COSTS DOWN? AUDIO PROGRAM TRANSCRIPT ECONOMICS U$A PROGRAM #2 THE FIRM (MUSIC PLAYS) Announcer: Funding for this program was provided by Annenberg Learner.

Full file at https://fratstock.eu

CHAPTER 2 THE PRODUCTION POSSIBILITIES FRONTIER FRAMEWORK OF ANALYSIS Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead

CHAPTER 2 THE PRODUCTION POSSIBILITIES FRONTIER FRAMEWORK OF ANALYSIS Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead

knows?) What we do know is that S1, S2, S3, and S4 will produce because they are the only ones

What we do know is that S1, S2, S3, and S4 will produce because they are the only ones") Guide to the Answers to Midterm 1, Fall 2010 (Form A) (This was put together quickly and may have typos. You should really think of it as an unofficial guide that might be of some use.) 1. First, it s

Guide to the Answers to Midterm 1, Fall 2010 (Form A) (This was put together quickly and may have typos. You should really think of it as an unofficial guide that might be of some use.) 1. First, it s

Lesson-8. Equilibrium of Supply and Demand

Introduction to Equilibrium Lesson-8 Equilibrium of Supply and Demand In economic theory, the interaction of supply and demand is understood as equilibrium. We may think of demand as a force tending to

Introduction to Equilibrium Lesson-8 Equilibrium of Supply and Demand In economic theory, the interaction of supply and demand is understood as equilibrium. We may think of demand as a force tending to

Correlation and Simple. Linear Regression. Scenario. Defining Correlation

Linear Regression Scenario Let s imagine that we work in a real estate business and we re attempting to understand whether there s any association between the square footage of a house and it s final selling

Linear Regression Scenario Let s imagine that we work in a real estate business and we re attempting to understand whether there s any association between the square footage of a house and it s final selling

Lecture 7 - Auctions and Mechanism Design

CS 599: Algorithmic Game Theory Oct 6., 2010 Lecture 7 - Auctions and Mechanism Design Prof. Shang-hua Teng Scribes: Tomer Levinboim and Scott Alfeld An Illustrative Example We begin with a specific example

CS 599: Algorithmic Game Theory Oct 6., 2010 Lecture 7 - Auctions and Mechanism Design Prof. Shang-hua Teng Scribes: Tomer Levinboim and Scott Alfeld An Illustrative Example We begin with a specific example

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 1

Economics 2 Spring 2018 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 1 1.a. Opportunity cost is defined as the value of what must be forgone to undertake an activity, where

Economics 2 Spring 2018 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 1 1.a. Opportunity cost is defined as the value of what must be forgone to undertake an activity, where

"Solutions" to Non-constant Sum Games

Unit 3 GAME THEORY Lesson 30 Learning Objective: Analyze two person non-zero sum games. Analyze games involving cooperation. Hello students, The well-defined rational policy in neoclassical economics --

Unit 3 GAME THEORY Lesson 30 Learning Objective: Analyze two person non-zero sum games. Analyze games involving cooperation. Hello students, The well-defined rational policy in neoclassical economics --

1.. There are two firms that produce a homogeneous product. Let p i

University of California, Davis Department of Economics Time: 3 hours Reading time: 20 minutes PRELIMINARY EXAMINATION FOR THE Ph.D. DEGREE Industrial Organization June 30, 2005 Answer four of the six

University of California, Davis Department of Economics Time: 3 hours Reading time: 20 minutes PRELIMINARY EXAMINATION FOR THE Ph.D. DEGREE Industrial Organization June 30, 2005 Answer four of the six

CHAPTER 2 FOUNDATIONS OF MODERN TRADE THEORY

CHAPTER 2 FOUNDATIONS OF MODERN TRADE THEORY MULTIPLE-CHOICE QUESTIONS 1. The mercantilists would have objected to: a. Export promotion policies initiated by the government b. The use of tariffs or quotas

CHAPTER 2 FOUNDATIONS OF MODERN TRADE THEORY MULTIPLE-CHOICE QUESTIONS 1. The mercantilists would have objected to: a. Export promotion policies initiated by the government b. The use of tariffs or quotas

ECON 450 Development Economics

ECON 450 Development Economics Contemporary Models of Development and Underdevelopment University of Illinois at Urbana-Champaign Summer 2017 Introduction In this lecture, we review a sample of some of

ECON 450 Development Economics Contemporary Models of Development and Underdevelopment University of Illinois at Urbana-Champaign Summer 2017 Introduction In this lecture, we review a sample of some of

Chapter 2: The Basic Theory Using Demand and Supply. Multiple Choice Questions

Chapter 2: The Basic Theory Using Demand and Supply Multiple Choice Questions 1. If an individual consumes more of good X when his/her income doubles, we can infer that a. the individual is highly sensitive

Chapter 2: The Basic Theory Using Demand and Supply Multiple Choice Questions 1. If an individual consumes more of good X when his/her income doubles, we can infer that a. the individual is highly sensitive

Introduction to Control Charts

Introduction to Control Charts Highlights Control charts can help you prevent defects before they happen. The control chart tells you how the process is behaving over time. It's the process talking to

Introduction to Control Charts Highlights Control charts can help you prevent defects before they happen. The control chart tells you how the process is behaving over time. It's the process talking to

Reducing Fractions PRE-ACTIVITY PREPARATION

Section. PRE-ACTIVITY PREPARATION Reducing Fractions You must often use numbers to communicate information to others. When the message includes a fraction whose components are large, it may not be easily

Section. PRE-ACTIVITY PREPARATION Reducing Fractions You must often use numbers to communicate information to others. When the message includes a fraction whose components are large, it may not be easily

Case: An Increase in the Demand for the Product

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

3.3 Demand, Supply, and Equilibrium

The text was adapted by The Saylor Foundation under the CC BY-NC-SA without attribution as requested by the works original creator or licensee 3.3 Demand, Supply, and Equilibrium LEARNING OBJECTIVES 1.

The text was adapted by The Saylor Foundation under the CC BY-NC-SA without attribution as requested by the works original creator or licensee 3.3 Demand, Supply, and Equilibrium LEARNING OBJECTIVES 1.

GUIDANCE ON CHOOSING INDICATORS OF OUTCOMES

1 GUIDANCE ON CHOOSING INDICATORS OF OUTCOMES 1. The Basics 1.1 What is the relationship between an outcome and an outcome indicator? 1.2 How are outcome indicators different from other types of indicators?

1 GUIDANCE ON CHOOSING INDICATORS OF OUTCOMES 1. The Basics 1.1 What is the relationship between an outcome and an outcome indicator? 1.2 How are outcome indicators different from other types of indicators?

The 10 Big Mistakes People Make When Running Customer Surveys

The 10 Big Mistakes People Make When Running Customer Surveys If you want to understand what drives customer loyalty for your business and how to align your business to improve customer loyalty, Genroe

The 10 Big Mistakes People Make When Running Customer Surveys If you want to understand what drives customer loyalty for your business and how to align your business to improve customer loyalty, Genroe

Urban Transportation Planning Prof Dr. V. Thamizh Arasan Department of Civil Engineering Indian Institute Of Technology, Madras

Urban Transportation Planning Prof Dr. V. Thamizh Arasan Department of Civil Engineering Indian Institute Of Technology, Madras Lecture No. # 14 Modal Split Analysis Contd. This is lecture 14 on urban

Urban Transportation Planning Prof Dr. V. Thamizh Arasan Department of Civil Engineering Indian Institute Of Technology, Madras Lecture No. # 14 Modal Split Analysis Contd. This is lecture 14 on urban

Unit 2: Theory of Consumer Behaviour

Name: Unit 2: Theory of Consumer Behaviour Date: / / Notations and Assumptions A consumer, in general, consumes many goods; but for simplicity, we shall consider the consumer s choice problem in a situation

Name: Unit 2: Theory of Consumer Behaviour Date: / / Notations and Assumptions A consumer, in general, consumes many goods; but for simplicity, we shall consider the consumer s choice problem in a situation

Appendix A. The horizontal axis measures both GDP and Sales. The vertical axis measures the average price level.

eaching Business Cycle Dynamics: A Comparison of Graphs and Loops 5-17 Appendix A A diagram might help visualize the sticky price theory in action. Here is part of it -- a graph with a horizontal axis

eaching Business Cycle Dynamics: A Comparison of Graphs and Loops 5-17 Appendix A A diagram might help visualize the sticky price theory in action. Here is part of it -- a graph with a horizontal axis

Product Design and Development Dr. Inderdeep Singh Department of Mechanical and Industrial Engineering Indian Institute of Technology, Roorkee

Product Design and Development Dr. Inderdeep Singh Department of Mechanical and Industrial Engineering Indian Institute of Technology, Roorkee Lecture - 06 Value Engineering Concepts [FL] welcome to the

Product Design and Development Dr. Inderdeep Singh Department of Mechanical and Industrial Engineering Indian Institute of Technology, Roorkee Lecture - 06 Value Engineering Concepts [FL] welcome to the

More-Advanced Statistical Sampling Concepts for Tests of Controls and Tests of Balances

APPENDIX 10B More-Advanced Statistical Sampling Concepts for Tests of Controls and Tests of Balances Appendix 10B contains more mathematical and statistical details related to the test of controls sampling

APPENDIX 10B More-Advanced Statistical Sampling Concepts for Tests of Controls and Tests of Balances Appendix 10B contains more mathematical and statistical details related to the test of controls sampling

Module 04 : Targeting. Lecture 11: PROBLEM TABLE ALGORITHM 1 st Part

Module 04 : Targeting Lecture : PROBLEM TABLE ALGORITHM st Part Key words: Problem Table Algorithm, shifted temperature, composite curve, PTA, For a given ΔT min, Composite curves can be used to obtain