Market Design: Theory and Applications

|

|

|

- Bertram Warren

- 6 years ago

- Views:

Transcription

1 Market Design: Theory and Applications ebay and Amazon Instructor: Itay Fainmesser Fall

2 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. 2

3 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. I Equilibrium results in auctions gave us powerful results that might not carry over to environments in which bidders might not all make equilibrium bids. Examples: 2

4 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. I Equilibrium results in auctions gave us powerful results that might not carry over to environments in which bidders might not all make equilibrium bids. Examples: I An experimental literature testing (and often rejecting) the revenue equivalence implications of equilibrium behavior. 2

5 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. I Equilibrium results in auctions gave us powerful results that might not carry over to environments in which bidders might not all make equilibrium bids. Examples: I An experimental literature testing (and often rejecting) the revenue equivalence implications of equilibrium behavior. I Investigation of common value auctions, both in experimental and eld data, which sometimes nds non-equilibrium winner s curse behavior. 2

6 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. I Equilibrium results in auctions gave us powerful results that might not carry over to environments in which bidders might not all make equilibrium bids. Examples: I An experimental literature testing (and often rejecting) the revenue equivalence implications of equilibrium behavior. I Investigation of common value auctions, both in experimental and eld data, which sometimes nds non-equilibrium winner s curse behavior. I Today we revisit the theory that it is a dominant strategy to bid your true value in a sealed bid, second price auction with private values. 2

7 Timing of transactions and their impact on markets I We ve discussed unraveling. And we noticed that transactions take time, which contribute to congestion. Now we re going to look at auctions in which transactions happen late, partly to take advantage of the fact that transactions take time. I Equilibrium results in auctions gave us powerful results that might not carry over to environments in which bidders might not all make equilibrium bids. Examples: I An experimental literature testing (and often rejecting) the revenue equivalence implications of equilibrium behavior. I Investigation of common value auctions, both in experimental and eld data, which sometimes nds non-equilibrium winner s curse behavior. I Today we revisit the theory that it is a dominant strategy to bid your true value in a sealed bid, second price auction with private values. I It turns out that there are auctions that look like this theory should apply, but which are designed so that it doesn t, not just behaviorally, but even when players are ideally rational. 2

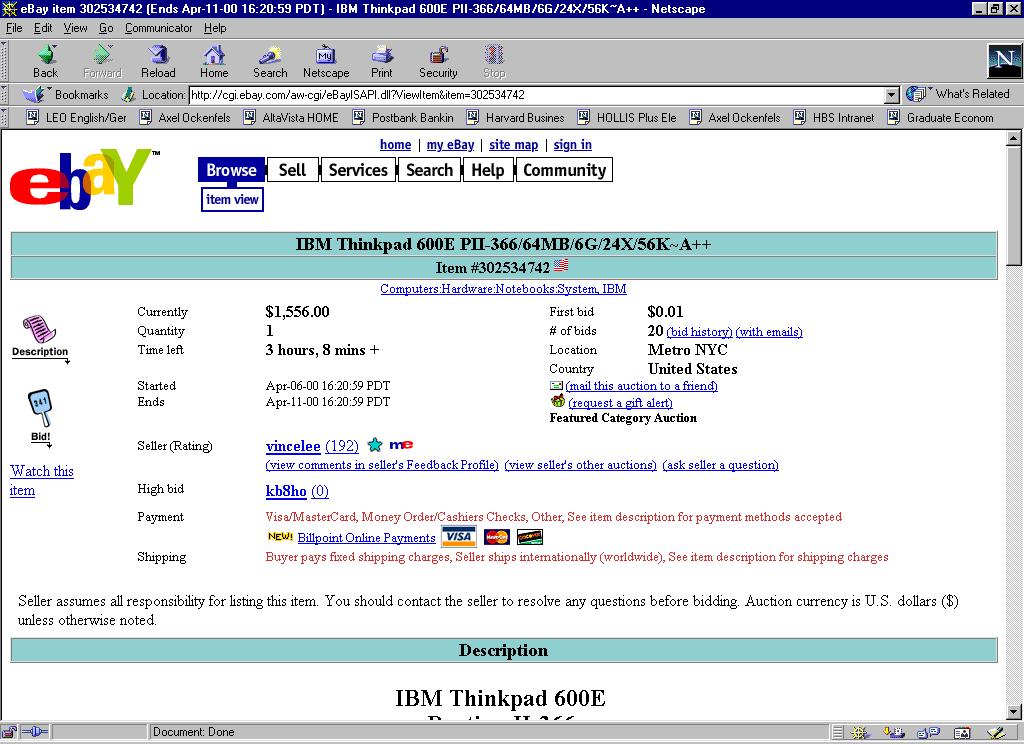

8 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. 3

9 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. I Auctions on ebay have a xed end time. Auctions on Amazon, which operate under similar rules, do not have a xed end time, but continue past the scheduled end time until ten minutes have passed without a bid. 3

10 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. I Auctions on ebay have a xed end time. Auctions on Amazon, which operate under similar rules, do not have a xed end time, but continue past the scheduled end time until ten minutes have passed without a bid. I There is signi cantly more late bidding on ebay than on Amazon. 3

11 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. I Auctions on ebay have a xed end time. Auctions on Amazon, which operate under similar rules, do not have a xed end time, but continue past the scheduled end time until ten minutes have passed without a bid. I There is signi cantly more late bidding on ebay than on Amazon. I More experienced bidders on ebay submit late bids more often than do less experienced bidders, while the e ect of experience on Amazon goes in the opposite direction. 3

12 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. I Auctions on ebay have a xed end time. Auctions on Amazon, which operate under similar rules, do not have a xed end time, but continue past the scheduled end time until ten minutes have passed without a bid. I There is signi cantly more late bidding on ebay than on Amazon. I More experienced bidders on ebay submit late bids more often than do less experienced bidders, while the e ect of experience on Amazon goes in the opposite direction. I On ebay, there is more late bidding for antiques than for computers. 3

13 Overview I An important issue in practical auction design concerns the rules for ending the auction. The internet auctions run by ebay and Amazon presented a natural comparison in the late 1990 s. I Auctions on ebay have a xed end time. Auctions on Amazon, which operate under similar rules, do not have a xed end time, but continue past the scheduled end time until ten minutes have passed without a bid. I There is signi cantly more late bidding on ebay than on Amazon. I More experienced bidders on ebay submit late bids more often than do less experienced bidders, while the e ect of experience on Amazon goes in the opposite direction. I On ebay, there is more late bidding for antiques than for computers. I But there s a limit to what we can conclude from eld data, because of all the uncontrolled di erences between who bids, what is sold, etc. 3

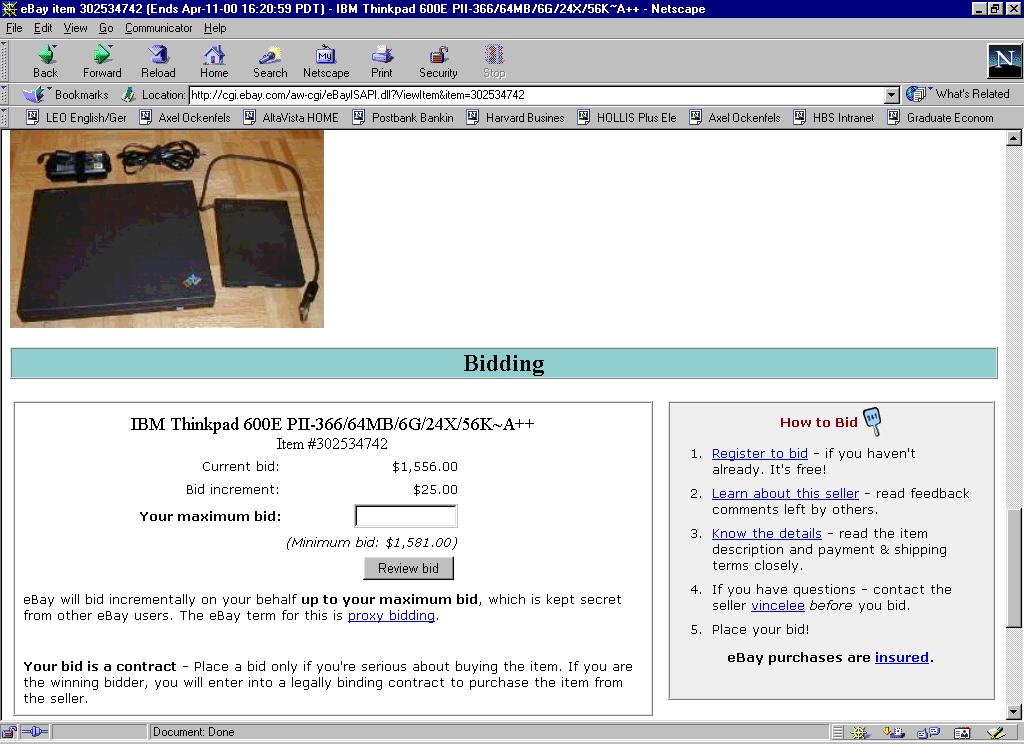

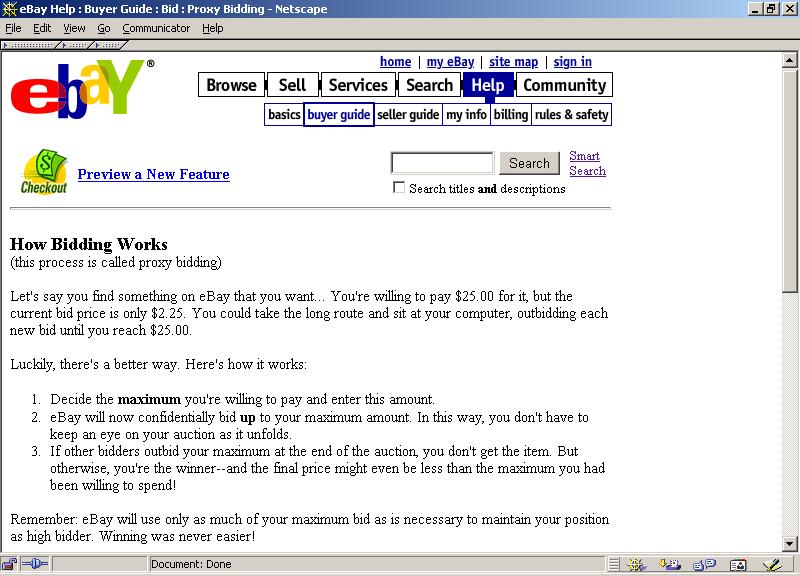

14 Basic rules: Amazon vs. ebay I Second price auctions 4

15 Basic rules: Amazon vs. ebay I Second price auctions I Bidders may submit their reservation price (also called a proxy bid); 4

16 Basic rules: Amazon vs. ebay I Second price auctions I I Bidders may submit their reservation price (also called a proxy bid); The resulting bid registers as the minimum increment above the previous high bid, and rises until it is reached, or until it exceeds the minimum increment over the next highest reservation price. 4

17 Basic rules: Amazon vs. ebay I Second price auctions I I I Bidders may submit their reservation price (also called a proxy bid); The resulting bid registers as the minimum increment above the previous high bid, and rises until it is reached, or until it exceeds the minimum increment over the next highest reservation price. The winning bidder is therefore the one who has submitted the highest reservation price, and the price he pays is the minimum increment over the second highest reservation price. 4

18 Basic rules: Amazon vs. ebay I Second price auctions I I I Bidders may submit their reservation price (also called a proxy bid); The resulting bid registers as the minimum increment above the previous high bid, and rises until it is reached, or until it exceeds the minimum increment over the next highest reservation price. The winning bidder is therefore the one who has submitted the highest reservation price, and the price he pays is the minimum increment over the second highest reservation price. I Auctions typically run for several days. 4

19 Basic rules: Amazon vs. ebay I Second price auctions I I I Bidders may submit their reservation price (also called a proxy bid); The resulting bid registers as the minimum increment above the previous high bid, and rises until it is reached, or until it exceeds the minimum increment over the next highest reservation price. The winning bidder is therefore the one who has submitted the highest reservation price, and the price he pays is the minimum increment over the second highest reservation price. I Auctions typically run for several days. I ebay auctions have a xed deadline. 4

20 Basic rules: Amazon vs. ebay I Second price auctions I I I Bidders may submit their reservation price (also called a proxy bid); The resulting bid registers as the minimum increment above the previous high bid, and rises until it is reached, or until it exceeds the minimum increment over the next highest reservation price. The winning bidder is therefore the one who has submitted the highest reservation price, and the price he pays is the minimum increment over the second highest reservation price. I Auctions typically run for several days. I ebay auctions have a xed deadline. I Amazon auctions are automatically extended for an additional 10 minutes from the time of the latest bid. 4

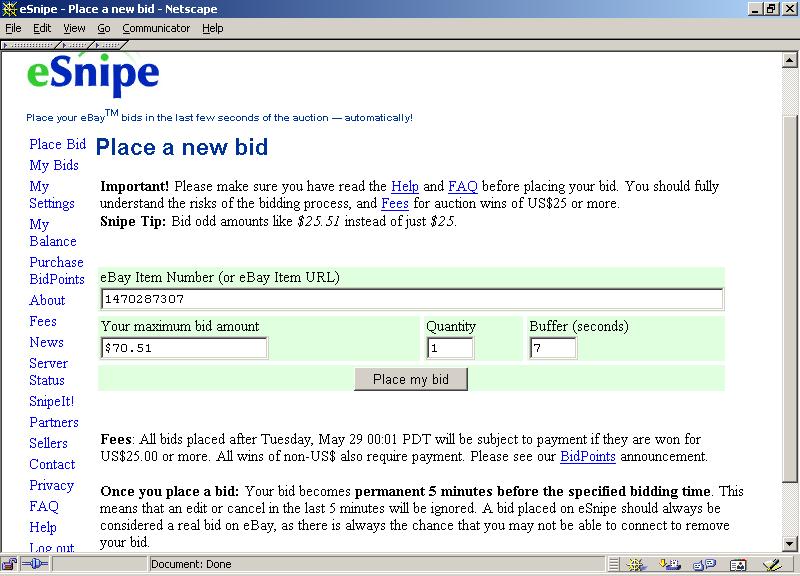

21 Late bidding in ebay auctions I Many bidders submit multiple bids in the course of the auction (i.e. they submit and later raise the reservation price they authorize for proxy bidding on their behalf). I A non-negligible fraction of bids are submitted in the closing seconds of the auction (a practice called sniping ). 5

22 6

23 7

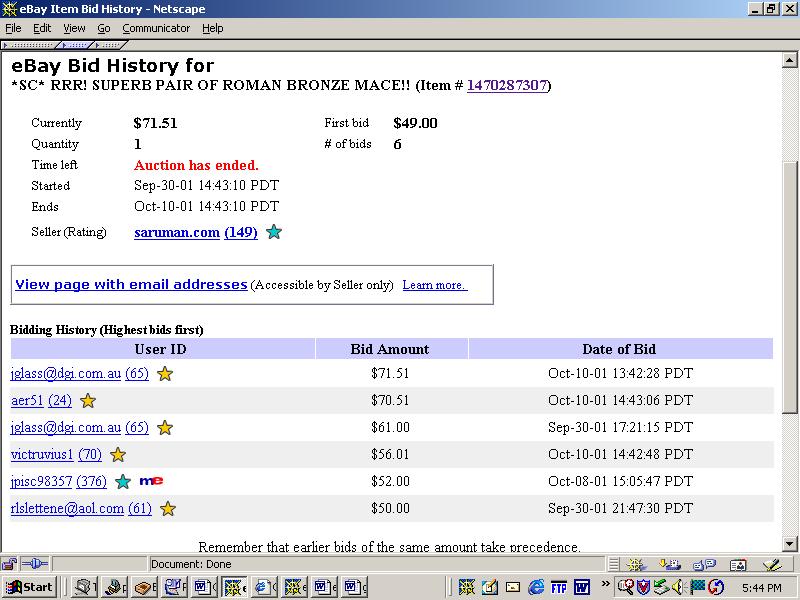

24 8

25 23 bids but only 14 bidders last bid came in at the last second 9

26 10

27 11

28 12

29 13

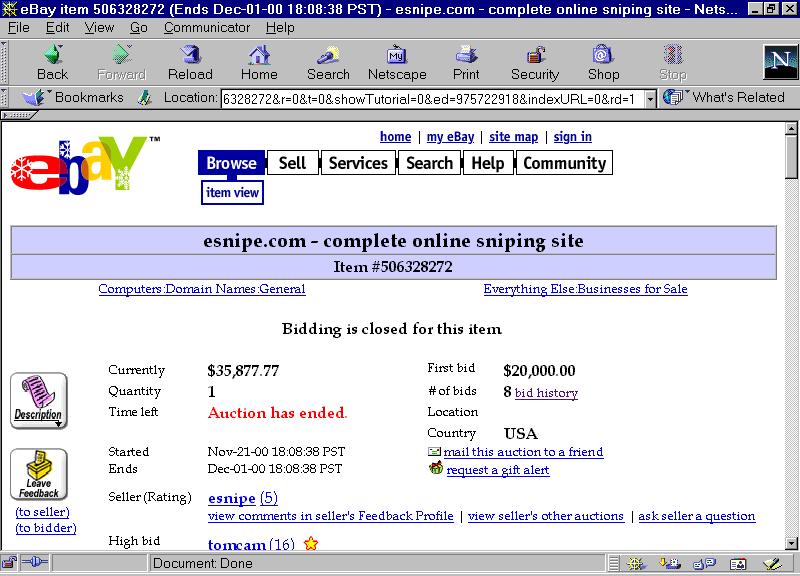

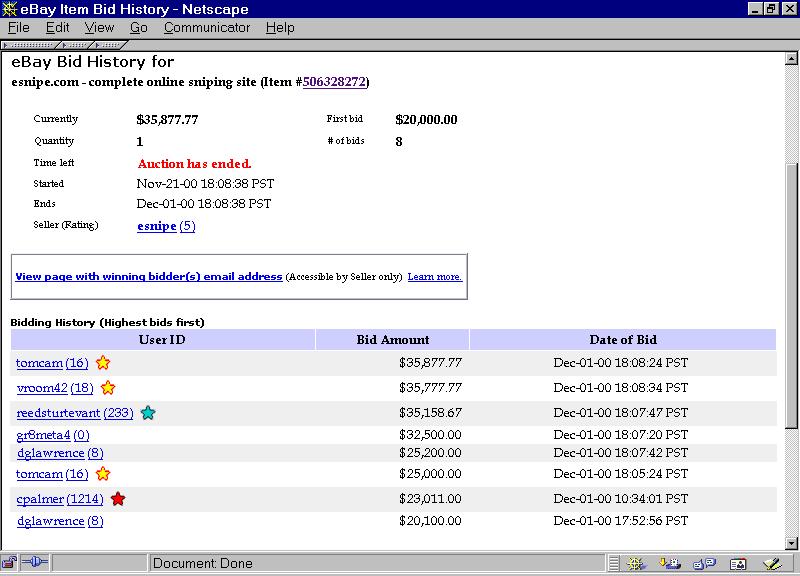

30 14 Selling esnipe.com I 8 bids by 6 bidders. I No bids before the 10th and nal day. I The price rose by more than $10,000 in the last minute, during which time 4 of the 8 bids were placed.

31 15 The dangers of last-minute bidding I ebay.com s view (1999) "ebay always recommends bidding the absolute maximum that one is willing to pay for an item early in the auction...

32 15 The dangers of last-minute bidding I ebay.com s view (1999) "ebay always recommends bidding the absolute maximum that one is willing to pay for an item early in the auction... I A seller s view (Axis Mundi, 1999) "THE DANGERS OF LAST MINUTE BIDDING: Almost without fail after an auction has closed we receive s from bidders who claim they were attempting to place a bid and were unable to get into ebay. There is nothing we can do to help bidders who were "locked out" while trying to place a "last minute" bid. All we can do in this regard is to urge you to place your bids early."

33 The dangers of last-minute bidding I ebay.com s view (1999) "ebay always recommends bidding the absolute maximum that one is willing to pay for an item early in the auction... I A seller s view (Axis Mundi, 1999) "THE DANGERS OF LAST MINUTE BIDDING: Almost without fail after an auction has closed we receive s from bidders who claim they were attempting to place a bid and were unable to get into ebay. There is nothing we can do to help bidders who were "locked out" while trying to place a "last minute" bid. All we can do in this regard is to urge you to place your bids early." I AuctionWatch.com s view (1999) "There are inherent risks in sniping. If you wait too long to bid, the auction could close before your bid is processed. If your maximum doesn t beat the current high bidder, you won t have a second chance to up the ante. And don t overlook the fact that you could be in the company of other snipers who are ready to snipe your snipe. It happens all the time. 15

34 I In an isolated independent private value auction, it would be a dominant strategy for bidders in a second-price sealed-bid auction to submit their maximum willingness-to-pay. 16

35 16 I In an isolated independent private value auction, it would be a dominant strategy for bidders in a second-price sealed-bid auction to submit their maximum willingness-to-pay. I But these aren t sealed bid auctions.

36 16 I In an isolated independent private value auction, it would be a dominant strategy for bidders in a second-price sealed-bid auction to submit their maximum willingness-to-pay. I But these aren t sealed bid auctions. I If all bids on ebay were sniped, ebay would essentially be converted into a sealed bid auction, one with some uncertainty about whether bids would go through.

37 16 I In an isolated independent private value auction, it would be a dominant strategy for bidders in a second-price sealed-bid auction to submit their maximum willingness-to-pay. I But these aren t sealed bid auctions. I If all bids on ebay were sniped, ebay would essentially be converted into a sealed bid auction, one with some uncertainty about whether bids would go through. I ebay could always capture all of esnipe s market by providing that facility on ebay, perhaps without the last minute uncertainty.)

38 It is helpful to model ebay as a continuous time auction followed by a last-minute sealed bid auction. Early bids are transmitted with certainty, but there is time for other bids to respond. Late bids come too late for other bidders to respond, but run the risk that they will not be successfully transmitted themselves. 17

39 18 A strategic model of the ebay environment I n bidders. I Minimum initial bid m and smallest increment s. I The current price (or high bid ) in an auction with at least two bidders is in general equal to the minimum increment over the second highest submitted bidders reservation price. There are two exceptions to this rule. 1. If more than one bidder submitted the highest reservation price, the bidder who submitted her bid rst is the high bidder at a price equal to the reservation price. 2. Second, if the current high bidder submits a new, higher bid, the current price is not raised, although the number of bids increases. I Each submitted reservation price must exceed both the current high bid and the bidder s last submitted reservation price.

40 A strategic model of the ebay environment (cont.) I A player can bid at times t 2 [0, 1) [ f1g. I A player has time to react before the end of the auction to another player s bid at time t 0 < 1, but the reaction cannot be instantaneous, it must be strictly after time t 0, at an earliest time t n, such that t 0 < t n < 1. I At t = 1, everyone knows the bid history prior to t, and has time to make exactly one more bid, without knowing what other last minute bids are being placed simultaneously. I If two bids are submitted simultaneously at the same instant t, then they are randomly ordered, and each has equal probability of being received rst. I At time t = 1, the probability that a bid is successfully transmitted is p < 1 (before that, p = 1). (In an Amazon auction, in contrast, a successful bid at time t = 1 extends the auction, and other bidders can respond.) 19

41 20 Private value ebay auctions In a (pure) private value auction, each bidder j has a true willingness to pay, v j, distributed according to some known, bounded distribution F. A bidder who wins the auction at price h earns v j h, a bidder who does not win earns 0. At t = 0 each player j knows her own v j. Unlike the case of a sealed-bid second-price auction, a bidder in this continuous-time second-price auction does not have any dominant strategy, even in the case of pure private values.

42 21 Theorem A bidder in the continuous-time second-price private value auction does not have any dominant strategies. Proof. WLOG consider the case of two bidders. It is su cient to show that bidder j with value v j > m + s has no strategy that is a best reply to every strategy of the other bidder, i. Suppose i s strategy is to bid the minimum bid m at t = 0 and then not to bid further at any information set at which he remains the high bidder, but to bid B (with B > v j + s) whenever he learns that he is not the high bidder.

43 22 j s best reply is not to bid at any time t < 1 (which would provoke a counterbid of B, and cause j to win at most zero), and to bid v j at time t = 1 (at which time the other bidder does not bid, since he does not learn that he is no longer the high bidder until the game is over). The payo to j from this strategy is p (v j m s) > 0, and it is easy to see that no other bid at time t = 1 could yield j a larger payo. (Other bids at t = 1, while weakly dominated, would yield the same payo against i s strategy, and would also be best replies.) Now suppose instead player i s strategy is not to bid at any time. Then a strategy for player j that calls for bidding only at t = 1 will have expected payo p (v j m) < v j m, i.e. less than the from the strategy of bidding v j at t = 0 (or at any t < 1, at which the bid will be transmitted with certainty instead of with probability p < 1). No best reply to i s second strategy is among player j s best replies to i s rst strategy, so j has no dominant strategy.

44 Possible strategic reasons for bidding late on ebay 1. Best response to naïve, English auction behavior: Another bidding tactic is sentry bidding placing a bid and then keeping close watch on it for the duration of the auction. If others try to outbid you, you can quickly place a counter-bid to regain your high bidder status. [... ] This could lead to an all-out bidding war, so be clear on how much you re willing to spend for an item and how closely you can monitor the auction. And beware of the last-second snipe from your worthy opponent. 1 Bidding very near the end of the auction would give the sentry bidder insu cient time to respond, so a sniper competing with a sentry bidder might win the auction at the sentry bidder s initial, low bid. In contrast, bidding one s true value early in the auction, when a sentry bidder is present, would win the auction only if one s true value were higher than the sentry bidder s, and in that case would have to pay the sentry bidder s true value

45 24 Possible strategic reasons for bidding late on ebay 2. Defense against dishonest sellers ( shill bidding )

46 25 Possible strategic reasons for bidding late on ebay 3. Common value auctions: e.g. concealment of expertise: If an auction is common-value, bidders can get information from others bids that causes them to revise their willingness to pay. In general, late bids motivated by information about common values arise either so that bidders can incorporate into their bids the information they have gathered from the earlier bids of others, or so bidders can avoid giving information to others through their own early bids. In an auction with a xed deadline, a sharp form of this latter cause of late bidding may arise when there is asymmetric information, and some players are better informed than others.

47 26 Possible strategic reasons for bidding late on ebay 3. Common value auctions: e.g. concealment of expertise (cont.): The greatest advantage of sniping is it a ords you anonymity among the other bidders. If you re a long-time bidder, others who bid on the same items as you will recognize your user ID. Some might even "ride your coattails," performing site searches on what you re bidding on, then perhaps bidding against you. If you choose to snipe, the other bidders won t know where you ll strike next, and that can mean more wins and frequently better prices for you. [ 1999]

48 27 Possible strategic reasons for bidding late on ebay 4. Implicit collusion among the bidders (at equilibrium even in a private value auction): There exist a multiplicity of equilibria, including of course equilibria at which each player i bids his true value at t = 0. At the other extreme, there are also equilibria at which no player bids his true value until the last moment.

49 28 Theorem There can exist equilibria in which bidders do not bid their true values until the last moment, t = 1, at which time there is only probability p < 1 that the bid will be transmitted. I The intuition behind last-minute bidding at equilibrium in a private value auction will be that there is an incentive not to bid too high when there is still time for other bidders to react, to avoid a bidding war that will raise the expected nal transaction price. (O the equilibrium path, early bidding causes a price war, at which all bidders bid their true value early enough so that bids go through with certainty.) I Mutual delay until the last minute can raise the expected pro t of all bidders, because of the positive probability that another bidder s last-minute bid will not be successfully transmitted.

50 29 All these strategic reasons to bid late despite the risk that your bid won t go through are eliminated or substantially attenuated in an auction with automatic extension. But, in addition to the possible strategic reasons for bidding late on ebay (but not on Amazon), there are possible non-strategic reasons for bidding late, on both ebay and Amazon. (i.e. reasons not a ected by the strategic e ects of the rule for ending the auction) 1. Procrastination 2. Search engines bring up old auctions rst 3. Desire to retain exibility to bid in other auctions (e.g. o ering the same item) We can try to sort out some of these di erent strategic and non-strategic hypotheses by comparing ebay and Amazon data.

51 Hypotheses about the causes of late bidding 30

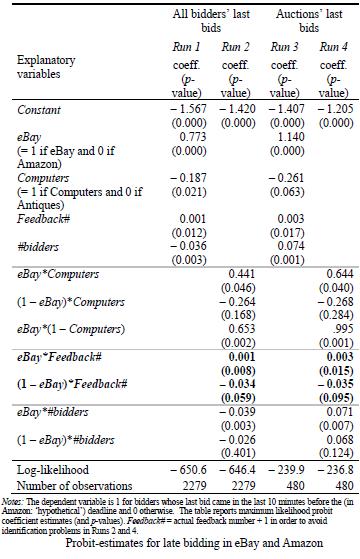

52 31 Description of the data I Amazon and ebay publicly provide data about the bid history. I The research used data in the categories Computers and Antiques. I I Computers ( private value auctions ): information about the retail price of most items is in general easily available. The di erence between the retail price and each bidder s willingness to pay, however, is private information. Antiques ( common value auctions ): retail prices are usually not available and the value of an item is often ambiguous and sometimes require experts to appraise. As a consequence, the number and amounts of bids of others are likely to carry valuable information about the item s value.

53 32 The data set consists of randomly selected auctions that were completed between October 1999 and January 2000 and that met certain criteria. 1. At least two bidders 2. Auctions with a hidden reserve price only if the reserve price was met. 3. No Dutch-, Private-, 10% o 1st bidder -, or Take-it-price -auctions

54 33 In total, 480 randomly selected auctions with 2279 bidders. I 120 ebay-computers with 740 bidders I 120 Amazon-Computers with 595 bidders I 120 ebay-antiques with 604 bidders I 120 Amazon-Antiques with 340 bidders

55 34 Variables: I number of bids I number of bidders I reserve price (y/n) I timing of bidders last bids I bidders feedback numbers

56 35 Timing I For each bidder - downloaded the data about how many seconds before the deadline the last bid was submitted if the bid came in within the last 12 hours of the auction time. I For each last bid in Amazon - computed the number of seconds before a hypothetical deadline. I This hypothetical deadline is de ned as the current actual deadline at the time of bidding under the assumption that the bid in hand and all subsequent bids were not submitted. I Suppose, for example, a bid comes in two minutes before the initial deadline. Then, the auction is extended by 8 minutes. The bid shows up in our data, however, as 120 seconds, respectively.

57 36 Feedback number In ebay, buyers and sellers have the opportunity to give each other a positive feedback (+1), a neutral feedback (0), or a negative feedback ( 1) along with a brief comment. I The cumulative total of positive and negative feedbacks is what we call the feedback number in ebay. In Amazon, buyers and sellers are allowed to post 1-5 star ratings about one another. I We refer to the cumulative number of ratings as the feedback number in Amazon.

58 37 Cumulative distribution of bidders last bids over time 100% % of submitted last bids 95% 90% 85% 80% 75% minutes before auction ends ebay Computers ebay Antiques Amazon Computers Amazon Antiques

59 38 Cumulative distribution of auctions last bids over time 100% % of submitted last bids 90% 80% 70% 60% 50% 40% 30% minutes before auction ends ebay Computers ebay Antiques Amazon Computers Amazon Antiques

60 39 When are the last bids submitted? Furthermore, more experience causes ebay bidders to bid later, but causes Amazon bidders to bid earlier.

61 40

62 41 Survey Hi: We are economists studying bidding on ebay (and sometimes ebay bidder ourselves, as aer51 and aockenfels). We are particularly interested in late bidding, and we are writing to you because we noticed that you have been successful at bidding in the last moment of an auction you participated in... [1] Do you sometimes plan, early in an auction, to submit a bid at the last minute? If so, why? (Or do you bid as the spirit moves you throughout the auction, and only bid at the last minute if you are outbid near the end?)

63 42 [2] Do you bid by hand, or do you use bidding software? If by hand, do you simply use the ebay bidder screens, or do you do something more elaborate, like open multiple windows so that you can follow the bidding while preparing a bid? [3] When bidding late, about what percentage of the time would you say it happened that you started to make a bid, but the auction closed before your bid was received?

64 43 [4] When you have planned to bid late, about what percentage of the time would you say it happened that something came up, so that you were not able to submit a bid as you planned? (We are thinking here of something that prevented you from being available, or from remembering to bid, not the case in which the price had already risen above what you were willing to pay.) [5] On average, would you say you submit only one bid per auction; no more than two bids, or more than two bids?

65 44 [6] Do you have a good idea, early in the auction, of the maximum you would be willing to pay, or do you often adjust what you are willing to pay based on the bids you see by other bidders? In this respect, are some other particular bidders especially in uential, or is it just the general price level and number of bidders that in uences your bid? [7] About what percentage of the time, when you are not the high bidder in an auction, do you regret that you did not bid higher? And in about what percentage of the auctions in which you are the high bidder do you regret having bid as high as you did?

66 [8] Is there anything else about your bidding experience that you think it would be helpful for us to know, as we try to understand what s going on? 45

67 46 Findings I A large majority of responders (91 percent) con rm that late bidding is typically part of their early planned bidding strategy (Question 1, N = 65). I Among the 49 bidders who verbally explain why they are bidding late, almost two thirds (65 percent) unambiguously express that they try to avoid a bidding war or to keep the price down. I Some experienced Antiques-bidders (about 10 percent of all responders, mostly with high feedback numbers) explicitly state that late bidding enables them to avoid sharing valuable information with other bidders. (At the same time, some bidders say that they are sometimes in uenced by the bids and the bidding activity of others, although 88 percent of the late bidders in our survey say that they have a clear idea, early in the auction, about what they are willing to pay (Question 6, N = 65).

68 47 I Some indications of naïve late bidding. A few bidders (less than 10 percent, mostly with zero feedback number) appear to confuse ebay with an English auction. Also, some bidders sometimes felt regret about not being the high bidder or for being the high bidder (Question 7). The median response for those who gave a quantitative estimation for how often this happened is, however, 0 percent in either case (N = 48 and 46, respectively). I Although most bidders never use sniping software (93 percent, Question 2, N = 67), many operate with several open windows and synchronize their computer clock with ebay time in order to improve their late bidding performance.

69 I Nevertheless, when bidding late, 86 percent of all bidders report that it happened at least once to them that they started to make a bid, but the auction was closed before the bid was received (Question 3, N = 65). I 90 percent of all bidders say that sometimes, even though they planned to bid late, something came up that prevented them from being available at the end of the auction so that they could not submit a bid as planned (Question 4, N = 63). (Most bidders gave a quantitative estimation about how often this happened to them. The median response is 10 percent for both, Question 3 (N = 43) and Question 4 (N = 52), respectively.) The survey suggests that late bidding is most often part of a planned strategy, even though bidders know that there is a risk in bidding late. At the same time, the survey reveals some heterogeneity in why later bidders bid late, including bidding war -, and expertise -explanations, and, to a lesser extent, non-strategic explanations. 48

70 49 Conclusions from the eld data Multiple and late bidding can have multiple causes. I The clear di erence in the amount of late bidding on ebay and Amazon is strong evidence that rational strategic considerations play a signi cant role, because ebay s hard close gives more reason to bid late in private value auctions, in common value auctions, and against naïve incremental bidders. This evidence that rational considerations are at work is strengthened by the observation that the di erence is even clearer among more experienced bidders.

71 50 I The di erence between the amount of late bidding for computers and for antiques suggests that the bidders respond to the additional strategic incentives for late bidding in markets in which expertise plays a role in appraising values. I The substantial amount of late bidding observed on Amazon, (even though substantially less than on ebay) suggests that there are also non-strategic causes of late bidding, possibly due to naivete or other non-rational cause, particularly since the evidence suggests that it is reduced with experience.

72 51 The need for experiments Interpretation of the eld data is complicated by the fact that there are di erences between ebay and Amazon other than their ending rules. I ebay has many more items for sale than Amazon, and many more bidders. I buyers and sellers decide in which auctions to participate, so there may be di erences between the seller and buyer characteristics and the objects for sale on ebay and Amazon.

73 52 The feedback ratings are imperfect proxies for experience. I They only re ect the number of completed transactions, but not auctions in which the bidder was not the high bidder. I Also, more experienced buyers on ebay may not only have more experience with the strategic aspects of the auction, they may have other di erences, e.g. they may also have more expertise concerning the goods for sale.

74 Laboratory experiments will allow us to look at the di erence in auction closing rules while controlling away all other di erences. 53

75 Experimental Design 54

76 55 There were two bidders in each auction. Each bidder in each auction was assigned a private value independently drawn from a uniform distribution between $6 and $10. A winner of an auction received his private value minus the nal price, and a loser received nothing for that auction. The minimum bid in all auctions was $1.00, and the smallest bid increment was $0.25.

77 56 ebay.8 Stage 1 is divided into discrete periods. In each period, each trader has an opportunity to make a bid (simultaneously). At the end of each period, the high bidder and current price (minimum increment over second highest bid) are displayed to all. Stage 1 ends (only) after a period at which no player makes a bid. Stage 2 of the ebay.8 auctions consists of a single period. The bidders have the opportunity to submit one (last) bid; it has probability p = 0.8 of being successfully transmitted.

78 57 ebay1 In the ebay1 condition, the probability that a bid made in stage 2 will be transmitted successfully is p = 1, i.e. stage 2 bids are transmitted with certainty. So in this condition, stage 2 is a conventional sealed bid second price auction.

79 58 Amazon In the Amazon condition, stage 1 is followed by stage 2, as in the ebay conditions, but after a successfully submitted stage 2 bid, stage 1 starts again (and is followed by stage 2 again, etc.). The probability that a stage 2 bid will be successfully transmitted is p = 0.8. Thus in the Amazon condition, the risk of bidding late is the same as in the ebay.8 condition, but a successful stage 2 bid causes the auction to be extended.

80 59 Sealed bid In the sealed bid condition, the auction begins with stage 2 (with p = 1), and ends immediately after, so that each bidder has the opportunity to submit only a single bid, and must do so without knowing the bids of the other bidder. (While the sealed bid auction obviously cannot yield any data on the timing of bids, it provides a benchmark against which the revenues in di erent auctions can be measured.)

81 Frequency of Sniping: Stage 2-bids (in Amazon: rst stage 2) per auction % 90% 80% 70% 60% Amazon 50% ebay (p=0.8) 40% ebay (p=1) 30% 20% 10% 0% auction number

82 61 The experimental results reproduce the main internet observations: I There is more late bidding in the xed-deadline (ebay) conditions than in the automatic extension (Amazon) condition. I Furthermore, as bidders gain experience, they are more likely to bid late in the ebay conditions, and less likely to bid late in the Amazon condition.

83 62 Share of bids submitted by current high bidder 50% 40% 30% 20% stage 1 stage 2 10% 0% Amazon ebay (p=0.8) ebay (p=1)

84 We now turn to examine the magnitude of early and late bids: Average increase of proxy bid (conditioned on bidding) over current minimum bid. 63

85 64 Amazon auction number stage 1 bids stage 2 bids

86 65 ebay auction number stage 1 bids stage 2 bids

87 66 ebay auction number stage 1 bids stage 2 bids

88 67 Price Discovery: Final stage 1-price (in Amazon: rst stage 1) as percentage of nal price 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% auction number Amazon ebay (p=0.8) ebay (p=1)

89 68 Median of nal bids (including lost stage 2-bids) as a percentage of value 100% 95% 90% 85% 80% 75% Amazon ebay.8 ebay1 sealed bid 70% 65% trials

90 69 Average revenues relative to second price - all trials 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Amazon ebay (p = 0.8) ebay (p = 1) sealed bid

91 70 Average revenues relative to second price - last 8 trials 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Amazon ebay (p = 0.8) ebay (p = 1) sealed bid

92 71 Average e ciency 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Amazon ebay (p = 0.8) ebay (p = 1) sealed bid

93 72 Median revenues $8.00 $7.80 $7.60 $7.40 $7.20 $7.00 $6.80 $6.60 $6.40 $6.20 $6.00 Amazon ebay.8 ebay1 sealed bid

94 73 Further Design questions raised by the results I Does a xed-deadline auction of a private value good raise less revenue than one with the same number of bidders in which bidding is extended until no one wants to bid anymore? (Because when many bidders plan to bid at the last minute, some don t make it?) I Could the increased entertainment value of a xed deadline attract su ciently many bidders to overcome this? I Does xed-deadline auction of a common-value good attract more sellers of high quality objects than one in which bidding is extended until no one wants to bid anymore? (Because the latter deters experts from bidding?)

95 74 Some nal, methodological thoughts Eclectic Methodology I We use theory, eld data, surveys, laboratory experiments... Timing of Transactions is important I As a profession, economists study the price of transactions much more than we study their time and place, but timing is an important strategic variable. In some markets, the entire organization of the market re ects attempts to control strategic behavior related to timing.

96 75 Design, learning, and prediction - Market design is about understanding markets both when they are new and when they are old, i.e. both when players are inexperienced and when they are experienced. So, the design tools that we are most in need of are theories of learning that can predict behavior in novel environments. Details matter - but there may be general theories about which details matter.

Late Bidding in Internet Auctions:

Late Bidding in Internet Auctions: (Starting with field data, and moving on to experiments, with a little theory on the way) Roth, Alvin E. and Axel Ockenfels Last-Minute Bidding and the Rules for Ending

Late Bidding in Internet Auctions: (Starting with field data, and moving on to experiments, with a little theory on the way) Roth, Alvin E. and Axel Ockenfels Last-Minute Bidding and the Rules for Ending

An experimental analysis of ending rules in internet auctions

An experimental analysis of ending rules in internet auctions Dan Ariely* Axel Ockenfels** Alvin E. Roth*** Abstract A great deal of late bidding has been observed on internet auctions such as ebay, which

An experimental analysis of ending rules in internet auctions Dan Ariely* Axel Ockenfels** Alvin E. Roth*** Abstract A great deal of late bidding has been observed on internet auctions such as ebay, which

Are Incremental Bidders Really Naive? Theory and Evidence from Competing Online Auctions

Are Incremental Bidders Really Naive? Theory and Evidence from Competing Online Auctions Rao Fu Jun 16, 2009 Abstract This paper studies di erent bidding strategies in simultaneous online auctions. I propose

Are Incremental Bidders Really Naive? Theory and Evidence from Competing Online Auctions Rao Fu Jun 16, 2009 Abstract This paper studies di erent bidding strategies in simultaneous online auctions. I propose

Notes on Introduction to Contract Theory

Notes on Introduction to Contract Theory John Morgan Haas School of Business and Department of Economics University of California, Berkeley 1 Overview of the Course This is a readings course. The lectures

Notes on Introduction to Contract Theory John Morgan Haas School of Business and Department of Economics University of California, Berkeley 1 Overview of the Course This is a readings course. The lectures

Game theorists and market designers

AI Magazine Volume 23 Number 3 (2002) ( AAAI) Articles The Timing of Bids in Internet Auctions Market Design, Bidder Behavior, and Artificial Agents Axel Ockenfels and Alvin E. Roth Many bidders in ebay

AI Magazine Volume 23 Number 3 (2002) ( AAAI) Articles The Timing of Bids in Internet Auctions Market Design, Bidder Behavior, and Artificial Agents Axel Ockenfels and Alvin E. Roth Many bidders in ebay

AN EXPERIMENTAL ANALYSIS OF ENDING RULES

AN EXPERIMENTAL ANALYSIS OF ENDING RULES IN INTERNET AUCTIONS DAN ARIELY AXEL OCKENFELS ALVIN E. ROTH CESIFO WORKING PAPER NO. 987 CATEGORY 9: INDUSTRIAL ORGANISATION JULY 2003 An electronic version of

AN EXPERIMENTAL ANALYSIS OF ENDING RULES IN INTERNET AUCTIONS DAN ARIELY AXEL OCKENFELS ALVIN E. ROTH CESIFO WORKING PAPER NO. 987 CATEGORY 9: INDUSTRIAL ORGANISATION JULY 2003 An electronic version of

IO Experiments. Given that the experiment was conducted at a sportscard show, the sequence of events to participate in the experiment are discussed.

IO Experiments 1 Introduction Some of the earliest experiments have focused on how di erent market institutions a ect price and quantity outcomes. For instance, Smith s 1962 paper is a response to Chamberlain

IO Experiments 1 Introduction Some of the earliest experiments have focused on how di erent market institutions a ect price and quantity outcomes. For instance, Smith s 1962 paper is a response to Chamberlain

Chapter Fourteen. Topics. Game Theory. An Overview of Game Theory. Static Games. Dynamic Games. Auctions.

Chapter Fourteen Game Theory Topics An Overview of Game Theory. Static Games. Dynamic Games. Auctions. 2009 Pearson Addison-Wesley. All rights reserved. 14-2 Game Theory Game theory - a set of tools that

Chapter Fourteen Game Theory Topics An Overview of Game Theory. Static Games. Dynamic Games. Auctions. 2009 Pearson Addison-Wesley. All rights reserved. 14-2 Game Theory Game theory - a set of tools that

An experimental analysis of ending rules in Internet auctions

RAND Journal of Economics Vol. 36, No. 4, Winter 2005 pp. 891 908 An experimental analysis of ending rules in Internet auctions Dan Ariely Axel Ockenfels and Alvin E. Roth A great deal of late bidding

RAND Journal of Economics Vol. 36, No. 4, Winter 2005 pp. 891 908 An experimental analysis of ending rules in Internet auctions Dan Ariely Axel Ockenfels and Alvin E. Roth A great deal of late bidding

Speculation and Demand Reduction in English Clock Auctions with Resale

MPRA Munich Personal RePEc Archive Speculation and Demand Reduction in English Clock Auctions with Resale Saral, Krista Jabs Webster University Geneva June 2010 Online at http://mpra.ub.uni-muenchen.de/25139/

MPRA Munich Personal RePEc Archive Speculation and Demand Reduction in English Clock Auctions with Resale Saral, Krista Jabs Webster University Geneva June 2010 Online at http://mpra.ub.uni-muenchen.de/25139/

Measuring the Benefits to Sniping on ebay: Evidence from a Field Experiment

Measuring the Benefits to Sniping on ebay: Evidence from a Field Experiment Sean Gray New York University David Reiley 1 University of Arizona This Version: September 2004 First Version: April 2004 Preliminary

Measuring the Benefits to Sniping on ebay: Evidence from a Field Experiment Sean Gray New York University David Reiley 1 University of Arizona This Version: September 2004 First Version: April 2004 Preliminary

Auction Theory An Intrroduction into Mechanism Design. Dirk Bergemann

Auction Theory An Intrroduction into Mechanism Design Dirk Bergemann Mechanism Design game theory: take the rules as given, analyze outcomes mechanism design: what kind of rules should be employed abstract

Auction Theory An Intrroduction into Mechanism Design Dirk Bergemann Mechanism Design game theory: take the rules as given, analyze outcomes mechanism design: what kind of rules should be employed abstract

EconS Asymmetric Information

cons 425 - Asymmetric Information ric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization ric Dunaway (WSU) cons 425 Industrial Organization 1 / 45 Introduction Today, we are

cons 425 - Asymmetric Information ric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization ric Dunaway (WSU) cons 425 Industrial Organization 1 / 45 Introduction Today, we are

A Note on Revenue Sharing in Sports Leagues

A Note on Revenue Sharing in Sports Leagues Matthias Kräkel, University of Bonn Abstract We discuss the optimal sharing of broadcasting revenues given a central marketing system. The league s sports association

A Note on Revenue Sharing in Sports Leagues Matthias Kräkel, University of Bonn Abstract We discuss the optimal sharing of broadcasting revenues given a central marketing system. The league s sports association

A game is a collection of players, the actions those players can take, and their preferences over the selection of actions taken by all the players

Game theory review A game is a collection of players, the actions those players can take, and their preferences over the selection of actions taken by all the players A strategy s i is dominant for player

Game theory review A game is a collection of players, the actions those players can take, and their preferences over the selection of actions taken by all the players A strategy s i is dominant for player

GAME THEORY: Analysis of Strategic Thinking Exercises on Repeated and Bargaining Games

GAME THEORY: Analysis of Strategic Thinking Exercises on Repeated and Bargaining Games Pierpaolo Battigalli Università Bocconi A.Y. 2006-2007 Exercise 1. Consider the following Prisoner s Dilemma game.

GAME THEORY: Analysis of Strategic Thinking Exercises on Repeated and Bargaining Games Pierpaolo Battigalli Università Bocconi A.Y. 2006-2007 Exercise 1. Consider the following Prisoner s Dilemma game.

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING In many economic situations, there exists asymmetric information between the di erent agents. Examples are abundant: A seller has better information

TOPIC 4. ADVERSE SELECTION, SIGNALING, AND SCREENING In many economic situations, there exists asymmetric information between the di erent agents. Examples are abundant: A seller has better information

Strategic Alliances, Joint Investments, and Market Structure

Strategic Alliances, Joint Investments, and Market Structure Essi Eerola RUESG, University of Helsinki, Helsinki, Finland Niku Määttänen Universitat Pompeu Fabra, Barcelona, Spain and The Research Institute

Strategic Alliances, Joint Investments, and Market Structure Essi Eerola RUESG, University of Helsinki, Helsinki, Finland Niku Määttänen Universitat Pompeu Fabra, Barcelona, Spain and The Research Institute

Two Lectures on Information Design

Two Lectures on nformation Design 10th DSE Winter School Stephen Morris December 2015 nformation Design Usually in information economics, we ask what can happen for a xed information structure... nformation

Two Lectures on nformation Design 10th DSE Winter School Stephen Morris December 2015 nformation Design Usually in information economics, we ask what can happen for a xed information structure... nformation

Online shopping and platform design with ex ante registration requirements. Online Appendix

Online shopping and platform design with ex ante registration requirements Online Appendix June 7, 206 This supplementary appendix to the article Online shopping and platform design with ex ante registration

Online shopping and platform design with ex ante registration requirements Online Appendix June 7, 206 This supplementary appendix to the article Online shopping and platform design with ex ante registration

Experienced Bidders in Online Second-Price Auctions

Experienced Bidders in Online Second-Price Auctions Rod Garratt Mark Walker John Wooders November 2002 Abstract When second-price auctions have been conducted in the laboratory, most of the observed bids

Experienced Bidders in Online Second-Price Auctions Rod Garratt Mark Walker John Wooders November 2002 Abstract When second-price auctions have been conducted in the laboratory, most of the observed bids

Note on webpage about sequential ascending auctions

Econ 805 Advanced Micro Theory I Dan Quint Fall 2007 Lecture 20 Nov 13 2007 Second problem set due next Tuesday SCHEDULING STUDENT PRESENTATIONS Note on webpage about sequential ascending auctions Everything

Econ 805 Advanced Micro Theory I Dan Quint Fall 2007 Lecture 20 Nov 13 2007 Second problem set due next Tuesday SCHEDULING STUDENT PRESENTATIONS Note on webpage about sequential ascending auctions Everything

Council Patches (1488) Jamboree Patches (550) Merit Badges (280) Order of the Arrow Patches (1745) Other Badges, Patches (4085)

Jamboree Patches (550) Merit Badges (280) Order of the Arrow Patches (1745) Other Badges, Patches (4085)") ebay The ISCA Getting Started Collecting Series In the past few years, the internet has become a bigger and bigger part of patch collecting. At one commercial web site in particular, thousands of Scout

ebay The ISCA Getting Started Collecting Series In the past few years, the internet has become a bigger and bigger part of patch collecting. At one commercial web site in particular, thousands of Scout

Bidding Behavior in Internet Auction Markets

Bidding Behavior in Internet Auction Markets Item type Authors Publisher Rights text; Electronic Dissertation Vadovic, Rado The University of Arizona. Copyright is held by the author. Digital access to

Bidding Behavior in Internet Auction Markets Item type Authors Publisher Rights text; Electronic Dissertation Vadovic, Rado The University of Arizona. Copyright is held by the author. Digital access to

Resale and Bundling in Multi-Object Auctions

Resale and Bundling in Multi-Object Auctions Marco Pagnozzi Università di Napoli Federico II and CSEF Allowing resale after an auction helps to achieve an e cient allocation Spectrum trading should be

Resale and Bundling in Multi-Object Auctions Marco Pagnozzi Università di Napoli Federico II and CSEF Allowing resale after an auction helps to achieve an e cient allocation Spectrum trading should be

EconS Bertrand Competition

EconS 425 - Bertrand Competition Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 38 Introduction Today, we

EconS 425 - Bertrand Competition Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 38 Introduction Today, we

EconS Vertical Pricing Restraints 2

EconS 425 - Vertical Pricing Restraints 2 Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 38 Introduction

EconS 425 - Vertical Pricing Restraints 2 Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 38 Introduction

Harvard University Department of Economics

Harvard University Department of Economics General Examination in Microeconomic Theory Spring 00. You have FOUR hours. Part A: 55 minutes Part B: 55 minutes Part C: 60 minutes Part D: 70 minutes. Answer

Harvard University Department of Economics General Examination in Microeconomic Theory Spring 00. You have FOUR hours. Part A: 55 minutes Part B: 55 minutes Part C: 60 minutes Part D: 70 minutes. Answer

Exam #2 (100 Points Total) Answer Key

Answer Key") Exam #2 (100 Points Total) Answer Key 1. A Pareto efficient outcome may not be good, but a Pareto inefficient outcome is in some meaningful sense bad. (a) (5 points) Give an example or otherwise explain,

Exam #2 (100 Points Total) Answer Key 1. A Pareto efficient outcome may not be good, but a Pareto inefficient outcome is in some meaningful sense bad. (a) (5 points) Give an example or otherwise explain,

Intro to Algorithmic Economics, Fall 2013 Lecture 1

Intro to Algorithmic Economics, Fall 2013 Lecture 1 Katrina Ligett Caltech September 30 How should we sell my old cell phone? What goals might we have? Katrina Ligett, Caltech Lecture 1 2 How should we

Intro to Algorithmic Economics, Fall 2013 Lecture 1 Katrina Ligett Caltech September 30 How should we sell my old cell phone? What goals might we have? Katrina Ligett, Caltech Lecture 1 2 How should we

David Easley and Jon Kleinberg November 29, 2010

Networks: Spring 2010 Practice Final Exam David Easley and Jon Kleinberg November 29, 2010 The final exam is Friday, December 10, 2:00-4:30 PM in Barton Hall (Central section). It will be a closed-book,

Networks: Spring 2010 Practice Final Exam David Easley and Jon Kleinberg November 29, 2010 The final exam is Friday, December 10, 2:00-4:30 PM in Barton Hall (Central section). It will be a closed-book,

Lecture 9 Game Plan. Angry Madness Tournament. Examples of auctions Which auction is best? How to bid? Revenue Equivalence Theorem.

Lecture 9 Game Plan Angry Madness Tournament Examples of auctions Which auction is best? Revenue Equivalence Theorem How to bid? Winner s Curse 1 Yield This Round or Wait? U Risk of Waiting Gain of Waiting

Lecture 9 Game Plan Angry Madness Tournament Examples of auctions Which auction is best? Revenue Equivalence Theorem How to bid? Winner s Curse 1 Yield This Round or Wait? U Risk of Waiting Gain of Waiting

Competitive Markets. Jeffrey Ely. January 13, This work is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike 3.0 License.

January 13, 2010 This work is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike 3.0 License. Profit Maximizing Auctions Last time we saw that a profit maximizing seller will choose

January 13, 2010 This work is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike 3.0 License. Profit Maximizing Auctions Last time we saw that a profit maximizing seller will choose

EconS Second-Degree Price Discrimination

EconS 425 - Second-Degree Price Discrimination Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 46 Introduction

EconS 425 - Second-Degree Price Discrimination Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 46 Introduction

Resale and Bundling in Auctions

WORKING PAPER NO. 86 Resale and Bundling in Auctions Marco Pagnozzi November 007 University of Naples Federico II University of Salerno Bocconi University, Milan CSEF - Centre for Studies in Economics

WORKING PAPER NO. 86 Resale and Bundling in Auctions Marco Pagnozzi November 007 University of Naples Federico II University of Salerno Bocconi University, Milan CSEF - Centre for Studies in Economics

P rofit t (1 + i) t. V alue = t=0

t. V alue = t=0") These notes correspond to Chapter 2 of the text. 1 Optimization A key concept in economics is that of optimization. It s a tool that can be used for many applications, but for now we will use it for pro

These notes correspond to Chapter 2 of the text. 1 Optimization A key concept in economics is that of optimization. It s a tool that can be used for many applications, but for now we will use it for pro

Sponsored Search Markets

COMP323 Introduction to Computational Game Theory Sponsored Search Markets Paul G. Spirakis Department of Computer Science University of Liverpool Paul G. Spirakis (U. Liverpool) Sponsored Search Markets

COMP323 Introduction to Computational Game Theory Sponsored Search Markets Paul G. Spirakis Department of Computer Science University of Liverpool Paul G. Spirakis (U. Liverpool) Sponsored Search Markets

Silvia Rossi. Auctions. Lezione n. Corso di Laurea: Informatica. Insegnamento: Sistemi multi-agente. A.A.

Silvia Rossi Auctions Lezione n. 16 Corso di Laurea: Informatica Insegnamento: Sistemi multi-agente Email: silrossi@unina.it A.A. 2014-2015 Reaching Agreements - Auctions (W: 7.2, 9.2.1 MAS: 11.1) 2 Any

Silvia Rossi Auctions Lezione n. 16 Corso di Laurea: Informatica Insegnamento: Sistemi multi-agente Email: silrossi@unina.it A.A. 2014-2015 Reaching Agreements - Auctions (W: 7.2, 9.2.1 MAS: 11.1) 2 Any

Buy-It-Now or Snipe on ebay?

Association for Information Systems AIS Electronic Library (AISeL) ICIS 2003 Proceedings International Conference on Information Systems (ICIS) December 2003 Buy-It-Now or Snipe on ebay? Ilke Onur Kerem

Association for Information Systems AIS Electronic Library (AISeL) ICIS 2003 Proceedings International Conference on Information Systems (ICIS) December 2003 Buy-It-Now or Snipe on ebay? Ilke Onur Kerem

Difinition of E-marketplace. E-Marketplaces. Advantages of E-marketplaces

Difinition of E-marketplace a location on the Internet where companies can obtain or disseminate information, engage in transactions, or work together in some way. E-Marketplaces Assist. Prof. Dr. Özge

Difinition of E-marketplace a location on the Internet where companies can obtain or disseminate information, engage in transactions, or work together in some way. E-Marketplaces Assist. Prof. Dr. Özge

VALUE OF SHARING DATA

VALUE OF SHARING DATA PATRICK HUMMEL* FEBRUARY 12, 2018 Abstract. This paper analyzes whether advertisers would be better off using data that would enable them to target users more accurately if the only

VALUE OF SHARING DATA PATRICK HUMMEL* FEBRUARY 12, 2018 Abstract. This paper analyzes whether advertisers would be better off using data that would enable them to target users more accurately if the only

Cyberspace Auctions and Pricing Issues: A Review of Empirical Findings. Patrick Bajari and Ali Hortacsu Stanford University and University of Chicago

Cyberspace Auctions and Pricing Issues: A Review of Empirical Findings Patrick Bajari and Ali Hortacsu Stanford University and University of Chicago April 8, 2002 Abstract This article surveys empirical

Cyberspace Auctions and Pricing Issues: A Review of Empirical Findings Patrick Bajari and Ali Hortacsu Stanford University and University of Chicago April 8, 2002 Abstract This article surveys empirical

Auctioning Many Similar Items

Auctioning Many Similar Items Lawrence Ausubel and Peter Cramton Department of Economics University of Maryland Examples of auctioning similar items Treasury bills Stock repurchases and IPOs Telecommunications

Auctioning Many Similar Items Lawrence Ausubel and Peter Cramton Department of Economics University of Maryland Examples of auctioning similar items Treasury bills Stock repurchases and IPOs Telecommunications

1 Applying the Competitive Model. 2 Consumer welfare. These notes essentially correspond to chapter 9 of the text.

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

Spring 06 Assignment 4: Game Theory and Auctions

15-381 Spring 06 Assignment 4: Game Theory and Auctions Questions to Vaibhav Mehta(vaibhav@cs.cmu.edu) Out: 3/08/06 Due: 3/30/06 Name: Andrew ID: Please turn in your answers on this assignment (extra copies

15-381 Spring 06 Assignment 4: Game Theory and Auctions Questions to Vaibhav Mehta(vaibhav@cs.cmu.edu) Out: 3/08/06 Due: 3/30/06 Name: Andrew ID: Please turn in your answers on this assignment (extra copies

How much is a dollar worth? Arbitrage on ebay and Yahoo

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown version: March 7, 2005 Abstract This paper uses eld experiments to identify substantial and persistent arbitrage opportunities on

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown version: March 7, 2005 Abstract This paper uses eld experiments to identify substantial and persistent arbitrage opportunities on

AN ASCENDING AUCTION FOR INTERDEPENDENT VALUES: UNIQUENESS AND ROBUSTNESS TO STRATEGIC UNCERTAINTY. Dirk Bergemann and Stephen Morris

AN ASCENDING AUCTION FOR INTERDEPENDENT VALUES: UNIQUENESS AND ROBUSTNESS TO STRATEGIC UNCERTAINTY By Dirk Bergemann and Stephen Morris January 27 Updated March 27 COWLES FOUNDATION DISCUSSION PAPER NO.

AN ASCENDING AUCTION FOR INTERDEPENDENT VALUES: UNIQUENESS AND ROBUSTNESS TO STRATEGIC UNCERTAINTY By Dirk Bergemann and Stephen Morris January 27 Updated March 27 COWLES FOUNDATION DISCUSSION PAPER NO.

Should Speculators Be Welcomed in Auctions?

Should Speculators Be Welcomed in Auctions? Marco Pagnozzi Università di Napoli Federico II and CSEF November 2007 Abstract The possibility of resale after an auction attracts speculators (i.e., bidders

Should Speculators Be Welcomed in Auctions? Marco Pagnozzi Università di Napoli Federico II and CSEF November 2007 Abstract The possibility of resale after an auction attracts speculators (i.e., bidders

The Ascending Bid Auction Experiment:

The Ascending Bid Auction Experiment: This is an experiment in the economics of decision making. The instructions are simple, and if you follow them carefully and make good decisions, you may earn a considerable

The Ascending Bid Auction Experiment: This is an experiment in the economics of decision making. The instructions are simple, and if you follow them carefully and make good decisions, you may earn a considerable

Information and the Coase Theorem. Joseph Farrell. "The Journal of Economic Perspectives," Vol. 1, No. 2 (Autumn, 1987), pp.

, pp.") Joseph Farrell. "The Journal of Economic Perspectives," Vol. 1, No. 2 (Autumn, 1987), pp. 113-129 Introduction On rst acquaintance, the Coase theorem seems much more robust. Like the welfare theorem, it

Joseph Farrell. "The Journal of Economic Perspectives," Vol. 1, No. 2 (Autumn, 1987), pp. 113-129 Introduction On rst acquaintance, the Coase theorem seems much more robust. Like the welfare theorem, it

EconS Monopoly - Part 1

EconS 305 - Monopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 23, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 23 October 23, 2015 1 / 50 Introduction For the rest

EconS 305 - Monopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 23, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 23 October 23, 2015 1 / 50 Introduction For the rest

Information Design: Murat Sertel Lecture

nformation Design: Murat Sertel Lecture stanbul Bilgi University: Conference on Economic Design Stephen Morris July 2015 Mechanism Design and nformation Design Mechanism Design: Fix an economic environment

nformation Design: Murat Sertel Lecture stanbul Bilgi University: Conference on Economic Design Stephen Morris July 2015 Mechanism Design and nformation Design Mechanism Design: Fix an economic environment

How much is a dollar worth? Arbitrage on ebay and Yahoo

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown April 5, 2005 ARE298 Abstract This paper uses eld experiments to identify substantial and persistent arbitrage opportunities on online

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown April 5, 2005 ARE298 Abstract This paper uses eld experiments to identify substantial and persistent arbitrage opportunities on online

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 01

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 01

Chapter 13 Outline. Challenge: Intel and AMD s Advertising Strategies. An Overview of Game Theory. An Overview of Game Theory

Chapter 13 Game Theory A camper awakens to the growl of a hungry bear and sees his friend putting on a pair of running shoes. You can t outrun a bear, scoffs the camper. His friend coolly replies, I don

Chapter 13 Game Theory A camper awakens to the growl of a hungry bear and sees his friend putting on a pair of running shoes. You can t outrun a bear, scoffs the camper. His friend coolly replies, I don

OPTIMISING YOUR FORECOURT. Your guide to maximising stock turn, addressing overage stock and driving maximum profit. Brought to you by Auto Trader.

OPTIMISING YOUR FORECOURT Your guide to maximising stock turn, addressing overage stock and driving maximum profit. Brought to you by Auto Trader. Managing an efficient forecourt For ultimate success

OPTIMISING YOUR FORECOURT Your guide to maximising stock turn, addressing overage stock and driving maximum profit. Brought to you by Auto Trader. Managing an efficient forecourt For ultimate success

Final Exam cheat sheet

Final Exam cheat sheet The space provided below each question should be sufficient for your answer. If you need additional space, use additional paper. You are allowed to use a calculator, but only the

Final Exam cheat sheet The space provided below each question should be sufficient for your answer. If you need additional space, use additional paper. You are allowed to use a calculator, but only the

EconS First-Degree Price Discrimination

EconS 425 - First-Degree Price Discrimination Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 41 Introduction

EconS 425 - First-Degree Price Discrimination Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 41 Introduction

Game Theory: Spring 2017

Game Theory: Spring 2017 Ulle Endriss Institute for Logic, Language and Computation University of Amsterdam Ulle Endriss 1 Plan for Today This and the next lecture are going to be about mechanism design,

Game Theory: Spring 2017 Ulle Endriss Institute for Logic, Language and Computation University of Amsterdam Ulle Endriss 1 Plan for Today This and the next lecture are going to be about mechanism design,

Monitoring individual performance

Monitoring individual performance Does each member of your team perform the tasks allocated to them? Does each member of your team perform to the standard required? What can you do to monitor performance

Monitoring individual performance Does each member of your team perform the tasks allocated to them? Does each member of your team perform to the standard required? What can you do to monitor performance

Counterfeiting as Private Money in Mechanism Design

Counterfeiting as Private Money in Mechanism Design Ricardo Cavalcanti Getulio Vargas Foundation Ed Nosal Cleveland Fed November 006 Preliminary and Incomplete Abstract We describe counterfeiting activity

Counterfeiting as Private Money in Mechanism Design Ricardo Cavalcanti Getulio Vargas Foundation Ed Nosal Cleveland Fed November 006 Preliminary and Incomplete Abstract We describe counterfeiting activity

How much is a dollar worth? Arbitrage on ebay and Yahoo

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown Dept. of Agricultural & Resource Economics University of California - Berkeley John Morgan Haas School of Business University of California

How much is a dollar worth? Arbitrage on ebay and Yahoo Jennifer Brown Dept. of Agricultural & Resource Economics University of California - Berkeley John Morgan Haas School of Business University of California

Grow your business 2016 Issue 10

2016 ISSUE 10 CONTENTS Is it a good idea to buy your boss s business? An essential skill for successful business owners. Have you considered a Pareto analysis? Is it a good idea to buy your boss s business?

2016 ISSUE 10 CONTENTS Is it a good idea to buy your boss s business? An essential skill for successful business owners. Have you considered a Pareto analysis? Is it a good idea to buy your boss s business?

How Much Does Facebook Advertising Cost? The Complete Guide to Facebook Ads Pricing

Bu er Social Advertising How Much Does Facebook Advertising Cost? The Complete Guide to Facebook Ads Pricing Share with Bu er 111 SHARES 2 COMMENTS Written by Alfred Lua Jan 10, 2017 Last updated: Jan

Bu er Social Advertising How Much Does Facebook Advertising Cost? The Complete Guide to Facebook Ads Pricing Share with Bu er 111 SHARES 2 COMMENTS Written by Alfred Lua Jan 10, 2017 Last updated: Jan

Strategic Ignorance in the Second-Price Auction

Strategic Ignorance in the Second-Price Auction David McAdams September 23, 20 Abstract Suppose bidders may publicly choose not to learn their values prior to a second-price auction with costly bidding.

Strategic Ignorance in the Second-Price Auction David McAdams September 23, 20 Abstract Suppose bidders may publicly choose not to learn their values prior to a second-price auction with costly bidding.

Buyer Heterogeneity and Dynamic Sorting in Markets for Durable Lemons

Buyer Heterogeneity and Dynamic Sorting in Markets for Durable Lemons Santanu Roy Southern Methodist University, Dallas, Texas. October 13, 2011 Abstract In a durable good market where sellers have private

Buyer Heterogeneity and Dynamic Sorting in Markets for Durable Lemons Santanu Roy Southern Methodist University, Dallas, Texas. October 13, 2011 Abstract In a durable good market where sellers have private

Econ 3542: Experimental and Behavioral Economics Exam #1 Review Questions

Econ 3542: Experimental and Behavioral Economics Exam #1 Review Questions Chapter 1 (Intro) o Briefly describe the early history of market experiments. Chamberlin s original pit market experiments (1948)

Econ 3542: Experimental and Behavioral Economics Exam #1 Review Questions Chapter 1 (Intro) o Briefly describe the early history of market experiments. Chamberlin s original pit market experiments (1948)

EconS Perfect Competition and Monopoly

EconS 425 - Perfect Competition and Monopoly Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 47 Introduction

EconS 425 - Perfect Competition and Monopoly Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 47 Introduction

The Need for Information

The Need for Information 1 / 49 The Fundamentals Benevolent government trying to implement Pareto efficient policies Population members have private information Personal preferences Effort choices Costs

The Need for Information 1 / 49 The Fundamentals Benevolent government trying to implement Pareto efficient policies Population members have private information Personal preferences Effort choices Costs

The Need for Information

The Need for Information 1 / 49 The Fundamentals Benevolent government trying to implement Pareto efficient policies Population members have private information Personal preferences Effort choices Costs

The Need for Information 1 / 49 The Fundamentals Benevolent government trying to implement Pareto efficient policies Population members have private information Personal preferences Effort choices Costs

EconS Theory of the Firm

EconS 305 - Theory of the Firm Eric Dunaway Washington State University eric.dunaway@wsu.edu October 5, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 16 October 5, 2015 1 / 38 Introduction Theory of the

EconS 305 - Theory of the Firm Eric Dunaway Washington State University eric.dunaway@wsu.edu October 5, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 16 October 5, 2015 1 / 38 Introduction Theory of the

Introduction to Auctions

Common to Optimal in Item Cheriton School of Computer Science University of Waterloo Outline Common Optimal in Item 1 2 Common Optimal 3 in 4 Item 5 Common Optimal in Item Methods for allocating goods,

Common to Optimal in Item Cheriton School of Computer Science University of Waterloo Outline Common Optimal in Item 1 2 Common Optimal 3 in 4 Item 5 Common Optimal in Item Methods for allocating goods,

Behavioral Biases in Auctions: an Experimental Study $

Behavioral Biases in Auctions: an Experimental Study $ Anna Dodonova School of Management, University of Ottawa, 136 Jean-Jacques Lussier, Ottawa, ON, K1N 6N5, Canada. Tel.: 1-613-562-5800 ext.4912. Fax:

Behavioral Biases in Auctions: an Experimental Study $ Anna Dodonova School of Management, University of Ottawa, 136 Jean-Jacques Lussier, Ottawa, ON, K1N 6N5, Canada. Tel.: 1-613-562-5800 ext.4912. Fax:

Introduction to E-Business I (E-Bay)

") Introduction to E-Business I (E-Bay) e-bay is The worlds online market place it is an inexpensive and excellent site that allows almost anyone to begin a small online e-business. Whether you are Buying

Introduction to E-Business I (E-Bay) e-bay is The worlds online market place it is an inexpensive and excellent site that allows almost anyone to begin a small online e-business. Whether you are Buying

AJAE Appendix for Comparing Open-Ended Choice Experiments and Experimental Auctions: An Application to Golden Rice

AJAE Appendix for Comparing Open-Ended Choice Experiments and Experimental Auctions: An Application to Golden Rice Jay R. Corrigan, Dinah Pura T. Depositario, Rodolfo M. Nayga, Jr., Ximing Wu, and Tiffany

AJAE Appendix for Comparing Open-Ended Choice Experiments and Experimental Auctions: An Application to Golden Rice Jay R. Corrigan, Dinah Pura T. Depositario, Rodolfo M. Nayga, Jr., Ximing Wu, and Tiffany

DEMAND CURVE AS A CONSTRAINT FOR BUSINESSES

1Demand and rofit Seeking 8 Demand is important for two reasons. First, demand acts as a constraint on what business firms are able to do. In particular, the demand curve forces firms to accept lower sales

1Demand and rofit Seeking 8 Demand is important for two reasons. First, demand acts as a constraint on what business firms are able to do. In particular, the demand curve forces firms to accept lower sales

INDUSTRY INSIGHTS A REAL ESTATE REPORT FROM

INDUSTRY INSIGHTS A REAL ESTATE REPORT FROM THE REPORT Staying knowledgeable about what s going on in the real estate industry is key to our ability to offer cutting-edge online courses, and our team includes

INDUSTRY INSIGHTS A REAL ESTATE REPORT FROM THE REPORT Staying knowledgeable about what s going on in the real estate industry is key to our ability to offer cutting-edge online courses, and our team includes

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay. Lecture -29 Monopoly (Contd )

") Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

The Auction Arbitrage Secret by Pete Bruckshaw

1 The Auction Arbitrage Secret by Pete Bruckshaw Copyright Pete Bruckshaw All Rights Reserved. There are no resale rights with this product. 2 3 Information Disclaimer All Information provided is for knowledge

1 The Auction Arbitrage Secret by Pete Bruckshaw Copyright Pete Bruckshaw All Rights Reserved. There are no resale rights with this product. 2 3 Information Disclaimer All Information provided is for knowledge

Improving your chances of Successful Sales on ebay. User Guide

Improving your chances of Successful Sales on ebay User Guide Introduction This user guide is an attempt to collate the experiences of various sellers and create a comprehensive guide that you can use

Improving your chances of Successful Sales on ebay User Guide Introduction This user guide is an attempt to collate the experiences of various sellers and create a comprehensive guide that you can use

Perfect surcharging and the tourist test interchange. fee

Perfect surcharging and the tourist test interchange fee Hans Zenger a; a European Commission, DG Competition, Chief Economist Team, 1049 Brussels, Belgium February 14, 2011 Abstract Two widely discussed

Perfect surcharging and the tourist test interchange fee Hans Zenger a; a European Commission, DG Competition, Chief Economist Team, 1049 Brussels, Belgium February 14, 2011 Abstract Two widely discussed

Developing a Model. This chapter illustrates how a simulation model is developed for a business C H A P T E R 5

C H A P T E R 5 Developing a Model This chapter illustrates how a simulation model is developed for a business process. Speci± cally, we develop and investigate a model for a simple productiondistribution

C H A P T E R 5 Developing a Model This chapter illustrates how a simulation model is developed for a business process. Speci± cally, we develop and investigate a model for a simple productiondistribution

CHAPTER 3 Where Prices Come From: The Interaction of Demand and Supply

CHAPTER 3 Where s Come From: The Interaction of Demand and Supply Chapter Outline and Learning Objectives Section 3.1: The Demand Side of the Market Learning Objective: List and describe the variables

CHAPTER 3 Where s Come From: The Interaction of Demand and Supply Chapter Outline and Learning Objectives Section 3.1: The Demand Side of the Market Learning Objective: List and describe the variables

First-Price Auctions with General Information Structures: A Short Introduction

First-Price Auctions with General Information Structures: A Short Introduction DIRK BERGEMANN Yale University and BENJAMIN BROOKS University of Chicago and STEPHEN MORRIS Princeton University We explore

First-Price Auctions with General Information Structures: A Short Introduction DIRK BERGEMANN Yale University and BENJAMIN BROOKS University of Chicago and STEPHEN MORRIS Princeton University We explore

NET Institute*

NET Institute* www.netinst.org Working Paper #06-02 September 2006 Paid Placement: Advertising and Search on the Internet Yongmin Chen and Chuan He University of Colorado at Boulder * The Networks, Electronic

NET Institute* www.netinst.org Working Paper #06-02 September 2006 Paid Placement: Advertising and Search on the Internet Yongmin Chen and Chuan He University of Colorado at Boulder * The Networks, Electronic

Applications of BNE: