Welfare economics part 2 (producer surplus) Application of welfare economics: The Costs of Taxation & International Trade

|

|

|

- Cecily Poole

- 6 years ago

- Views:

Transcription

1 Welfare economics part 2 (producer surplus) Application of welfare economics: The Costs of Taxation & International Trade Dr. Anna Kowalska-Pyzalska Department of Operations Research Presentation is based on:

2 Cost Producer surplus Total surplus Deadweight loss Tax wedge World price Tariff

3

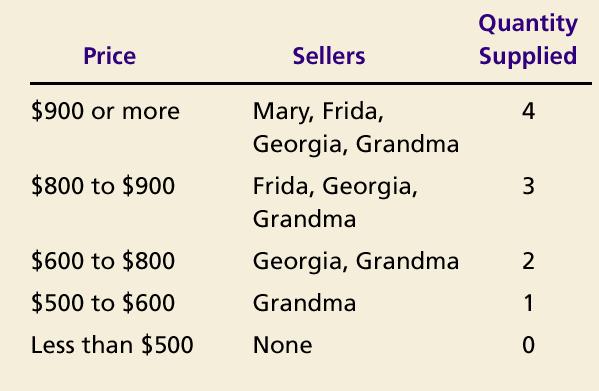

4 It measures the benefit to sellers participating in a market. Producer surplus is the amount a seller is paid for a good minus the seller s cost.

5 Each painter is willing to do the work, if the price is right... The price must exceed the cost of doing the work. Copyright 2004 South-Western

6 Because a painter s cost is the lowest price he would accept for his work, Cost is a measure of his willingness to sell the services. Each painter would be: eager to sell the services at a price greater than the cost. would refuse to sell the services at a price less than the cost. indifferent about selling his services at a price exactly equal to the cost.

7 The job goes to the painter who can do the work at the lowest cost If the painters compete for the job, the price falls If Grandma bids $600, she receives the producer surplus of $100.

8 Producer surplus measures the benefits to sellers of participating in a market. Just as consumer surplus is related to the demand curve, producer surplus is closely related to the supply curve.

9

10 marignal seller a seller who would leave the market if the price were any lower. At any quantity, the price given by the supply curve shows the cost of the marginal seller.

11 The area below the price and above the supply curve measures the producer surplus in a market. The height of the supply curve measures seller s cost, and the difference between the price and the cost is each seller s producer surplus. The total area is the sum of the producer surplus of all sellers.

12 (a) Price = $600 Price of House Painting Supply $ Grandma s producer surplus ($100) Quantity of Houses Painted Copyright 2003 Southwestern/Thomson Learning

13 Price of House Painting $ Total producer surplus ($500) (b) Price = $800 Supply Georgia s producer surplus ($200) Grandma s producer surplus ($300) Quantity of Houses Painted Copyright 2003 Southwestern/Thomson Learning

14 Copyright 2003 Southwestern/Thomson Learning (a) Producer Surplus at Price P Price Supply P 1 B Producer surplus C Sellers always want to get a higher price for the goods they sell. A 0 Q 1 Quantity

15 Copyright 2003 Southwestern/Thomson Learning (b) Producer Surplus at Price P Price Additional producer surplus to initial producers Supply P 2 D E F P 1 B Initial producer surplus C Producer surplus to new producers A 0 Q 1 Q 2 Quantity

16 Consumer surplus and producer surplus may be used to address the following question: Is the allocation of resources determined by free markets in any way desirable?

17 Consumer Surplus = Value to buyers Amount paid by buyers and Producer Surplus = Amount received by sellers Cost to sellers

18 Total surplus = Consumer surplus + Producer surplus or Total surplus = Value to buyers Cost to sellers

19 Efficiency is the property of a resource allocation of maximizing the total surplus received by all members of society. An allocation is inefficient if: a good is not being consumed by the buyers who value it most highly. is not being produced by the sellers who could produce it with the lowest cost.

20 In addition to market efficiency, a social planner might also care about: Equity the fairness of the distribution of well-being among the various buyers and sellers.

21 Copyright 2003 Southwestern/Thomson Learning Price A D Supply Equilibrium price Consumer surplus Producer surplus E Those buyers who value the good more than the price (AE) will buy it. Those sellers whose costs are less than the price will produce and sell the good (CE) B Demand C 0 Equilibrium Quantity quantity

22 Three Insights Concerning Market Outcomes: Free markets allocate the supply of goods to the buyers who value them most highly, as measured by their willingness to pay. Free markets allocate the demand for goods to the sellers who can produce them at least cost. Free markets produce the quantity of goods that maximizes the sum of consumer and producer surplus.

23 Copyright 2003 Southwestern/Thomson Learning Price At quantities below equilibrium value to buyers exceeds the cost to sellers. In this region, increasing quantity raises total surplus, until the quantity reaches Eq. 0 Value to buyers Cost to sellers Equilibrium quantity Cost to sellers Value to buyers Supply Demand Quantity At quantities above the equilibrium the value to buyers is less than the cost to sellers it would lower total surplus Value to buyers is greater than cost to sellers. Value to buyers is less than cost to sellers.

24

25 How do taxes affect the economic well-being of market participants? It does not matter whether a tax on a good is levied on buyers or sellers of the good... the price paid by buyers rises, and the price received by sellers falls. We must compare the reduced welfare of buyers and sellers to the amount of revenue the government gets.

26 Copyright 2004 South-Western Price Supply Price buyers pay Size of tax Price without tax Price sellers receive Demand 0 Quantity with tax Quantity without tax Quantity

27 A tax places a wedge between the price buyers pay and the price sellers receive. Because of this tax wedge, the quantity sold falls below the level that would be sold without a tax. The size of the market for that good shrinks.

28 Tax Revenue T = the size of the tax Q = the quantity of the good sold T Q = = the government s tax revenue

29 Copyright 2004 South-Western Price Tax revenue is spent on public services: e.g. roads, public education, transfer payments, etc. Supply Price buyers pay Price sellers receive Tax revenue (T Q) Size of tax (T) Quantity sold (Q) Demand 0 Quantity with tax Quantity without tax Quantity

30 Copyright 2004 South-Western Price A tax on a good reduces consumer surplus (by the area B+C) and producer surplus (by the area D+E). Price buyers pay Price without tax Price sellers receive = PB = P1 = PS A B D F C E Supply The tax is said to impose a deadweight loss (area C + E). Demand 0 Q2 Because the fall in producer and consumer surplus exceeds tax revenue Quantity Q1 (area B + D), the tax is said to impose a deadweight loss (area C + E).

31 The change in total welfare includes: The change in consumer surplus, The change in producer surplus, and The change in tax revenue. The losses to buyers and sellers exceed the revenue raised by the government. This fall in total surplus is called the deadweight loss.

32 Changes in Welfare A deadweight loss is the fall in total surplus that results from a market distortion, such as a tax. A tax is an incentive to buyers and sellers Taxes distort incentives. They cause markets to allocate resources inefficiently.

33 PETER: OC = $80 PS = $100-$80=$20 Peter cleans Jane s house for $100 Total surplus: $20+$20=$40 JANE: WTP = $120 CS = $120-$100=$20

34 PETER: OC = $80 PS = $100-$80=$20 PETER: OC = $80 PS = $120-$50=$70<$80 Peter cleans Jane s house for $100 Total surplus: $20+$20=$40 If the tax $50 is levied on supplier of the service, then JANE: WTP = $120 CS = $120-$100=$20 JANE: WTP = $120 She cannot pay more than $120. She would need to pay at least $130.

35 Taxes cause deadweight losses because they prevent buyers and sellers from realizing some of the gains from trade.

36 What determines whether the deadweight loss from a tax is large or small? The magnitude of the deadweight loss depends on how much the quantity supplied and quantity demanded respond to changes in the price. That, in turn, depends on the price elasticities of supply and demand.

37 Copyright 2004 South-Western (a) Inelastic Supply Price Supply Size of tax When supply is relatively inelastic, the deadweight loss of a tax is small. Demand 0 Quantity

38 Copyright 2004 South-Western (b) Elastic Supply Price When supply is relatively elastic, the deadweight loss of a tax is large. Size of tax Supply Demand 0 Quantity

39 Copyright 2004 South-Western (c) Inelastic Demand Price Supply Size of tax When demand is relatively inelastic, the deadweight loss of a tax is small. Demand 0 Quantity

40 Copyright 2004 South-Western (d) Elastic Demand Price Supply Size of tax Demand When demand is relatively elastic, the deadweight loss of a tax is large. 0 Quantity

41 The greater the elasticities of demand and supply: the larger will be the decline in equilibrium quantity and, the greater the deadweight loss of a tax.

42 With each increase in the tax rate, the deadweight loss of the tax rises even more rapidly than the size of the tax.

43 Copyright 2004 South-Western Price (a) Small Tax Deadweight loss Supply P B Tax revenue P S Demand 0 Q 2 Q 1 Quantity

44 Copyright 2004 South-Western Price (b) Medium Tax P B Deadweight loss Supply Tax revenue P S Demand 0 Q 2 Q 1 Quantity

45 Tax revenue Copyright 2004 South-Western (c) Large Tax Price P B Deadweight loss Supply Demand P S 0 Q 2 Q 1 Quantity

46 Copyright 2004 South-Western (a) Deadweight Loss Deadweight Loss As the size of a tax increases, its deadweight loss quickly gets larger. 0 Tax Size

47 For the small tax, tax revenue is small. As the size of the tax rises, tax revenue grows. But as the size of the tax continues to rise, tax revenue falls because the higher tax reduces the size of the market.

48 Copyright 2004 South-Western (b) Revenue (the Laffer curve) Tax Revenue Tax revenue first rises with the size of a tax, but then, as the tax gets larger, the market shrinks so much that tax revenue starts to fall. 0 Tax Size

49

50 What determines whether a country imports or exports a good? Who gains and who loses from free trade among countries? What are the arguments that people use to advocate trade restrictions?

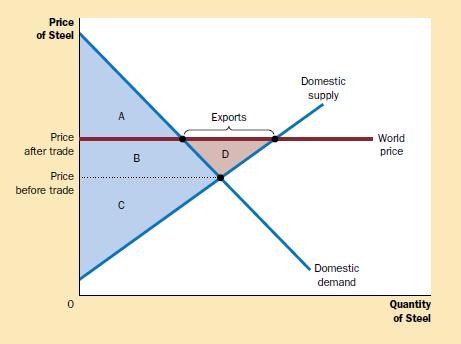

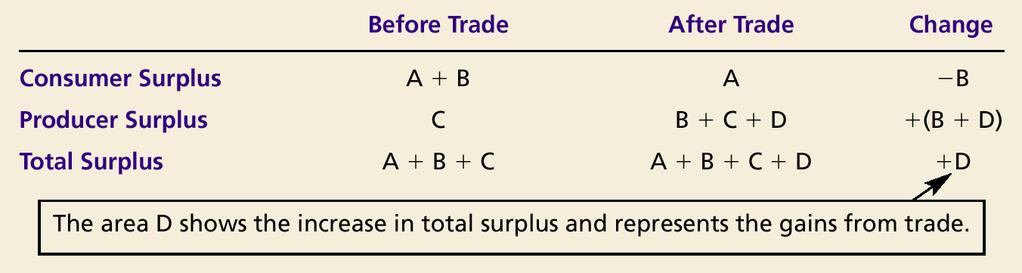

51

52 Equilibrium Without Trade Assume: A country is isolated from rest of the world and produces steel. The market for steel consists of the buyers and sellers in the country. No one in the country is allowed to import or export steel.

53 Copyright 2004 South-Western Price of Steel Domestic supply Equilibrium price Consumer surplus Producer surplus Domestic demand 0 Equilibrium Quantity quantity of Steel

54 Equilibrium Without Trade Results: Domestic price adjusts to balance demand and supply. The sum of consumer and producer surplus measures the total benefits that buyers and sellers receive.

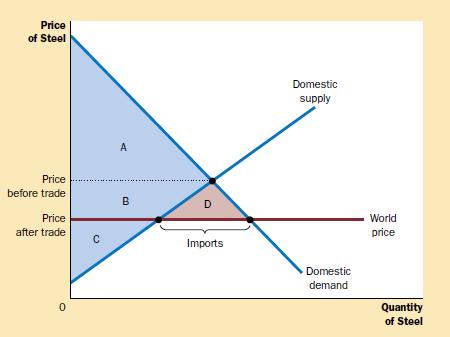

55 If the country decides to engage in international trade, will it be an importer or exporter of steel?

56 The effects of free trade can be shown by comparing the domestic price of a good without trade and the world price of the good. The world price refers to the price that prevails in the world market for that good.

57 If a country has a comparative advantage, then the domestic price will be below the world price, and the country will be an exporter of the good. If the country does not have a comparative advantage, then the domestic price will be higher than the world price, and the country will be an importer of the good.

58 Copyright 2004 South-Western Price of Steel Price after trade Price before trade 0 Domestic quantity demanded Exports Domestic quantity supplied Domestic supply Domestic demand World price Quantity of Steel

59 Copyright 2004 South-Western Price of Steel Price after trade Price before trade A C B Consumer surplus before trade Exports D Domestic supply World price Producer surplus before trade Domestic demand 0 Quantity of Steel

60

61 The analysis of an exporting country yields two conclusions: Domestic producers of the good are better off, and domestic consumers of the good are worse off. Trade raises the economic well-being of the nation as a whole.

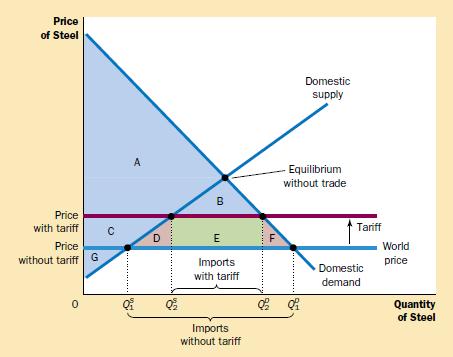

62 International Trade in an importing Country If the world price of steel is lower than the domestic price, the country will be an importer of steel when trade is permitted. Domestic consumers will want to buy steel at the lower world price. Domestic producers of steel will have to lower their output because the domestic price moves to the world price.

63 Price of Steel Price before trade Domestic supply Price after trade Imports Domestic demand World price 0 Domestic Domestic Quantity quantity quantity of Steel supplied demanded Copyright 2004 South-Western

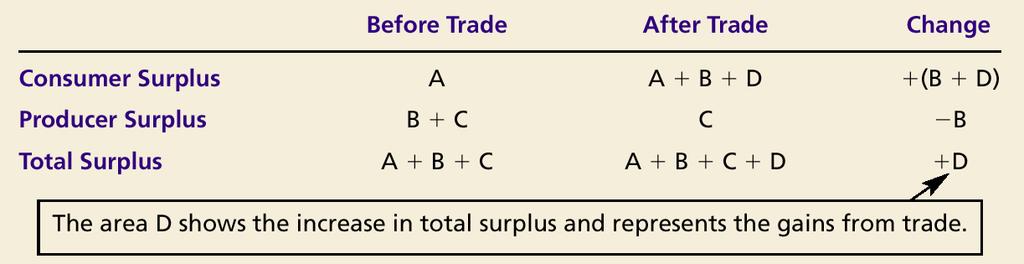

64 Price of Steel Consumer surplus after trade Domestic supply A Price before trade Price after trade C B D Imports World price Producer surplus after trade Domestic demand 0 Quantity of Steel Copyright 2004 South-Western

65

66 The analysis of an importing country yields two conclusions: Domestic producers of the good are worse off, and domestic consumers of the good are better off. Trade raises the economic well-being of the nation as a whole because the gains of consumers exceed the losses of producers.

67 The gains of the winners exceed the losses of the losers. The winners could compensate the losers. The net change in total surplus is positive. But will trade make EVERYONE better off? In practice, compensation for the losers from international trade is rare Without such compensation, opening up to international trade is a policy that expands the size of the economic pie, while perhaps leaving some participants in the economy with a smaller slice...

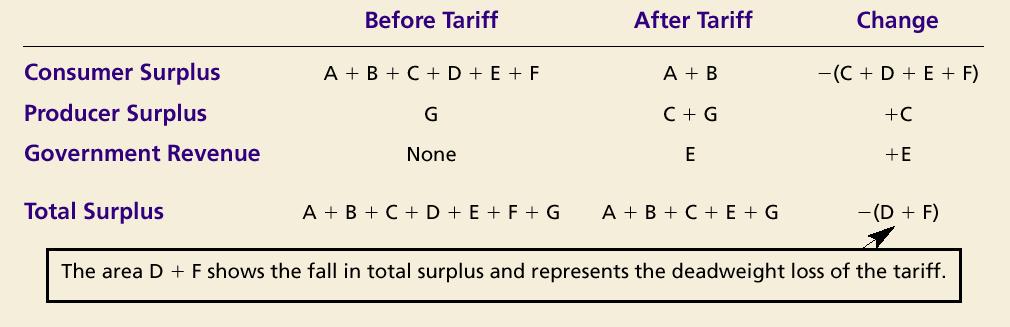

68

69 Tariffs raise the price of imported goods above the world price by the amount of the tariff. A tariff is a tax on goods produced abroad and sold domestically.

70 Price of Steel Domestic supply Equilibrium without trade Price with tariff Price without tariff Imports with tariff Domestic demand Tariff World price 0 Q S Q S Q D Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

71 Price of Steel Consumer surplus before tariff Domestic supply Producer surplus before tariff Equilibrium without trade Price without tariff Domestic demand World price 0 Q S Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

72 Price of Steel Consumer surplus with tariff Domestic supply A Equilibrium without trade Price with tariff B Tariff Price without tariff Imports with tariff Domestic demand World price 0 Q S Q S Q D Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

73 Price of Steel Domestic supply Producer surplus after tariff Equilibrium without trade Price with tariff Price without tariff G C Imports with tariff Domestic demand Tariff World price 0 Q S Q S Q D Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

74 Price of Steel Domestic supply Tariff Revenue Price with tariff Price without tariff E Imports with tariff Domestic demand Tariff World price 0 Q S Q S Q D Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

75 Price of Steel Domestic supply A Deadweight Loss Price with tariff Price without tariff G C D B E Imports with tariff F Domestic demand Tariff World price 0 Q S Q S Q D Q D Quantity of Steel Imports without tariff Copyright 2004 South-Western

76

77 A tariff reduces the quantity of imports and moves the domestic market closer to its equilibrium without trade. With a tariff, total surplus in the market decreases by an amount referred to as a deadweight loss.

78 An allocation of resources that maximizes the sum of consumer and producer surplus is said to be efficient. The equilibrium of demand and supply maximizes the sum of consumer and producer surplus. This is as if the invisible hand of the marketplace leads buyers and sellers to allocate resources efficiently. Markets do not allocate resources efficiently in the presence of market failures.

79 A tax on a good reduces the welfare of buyers and sellers of the good, and the reduction in consumer and producer surplus usually exceeds the revenues raised by the government. The fall in total surplus the sum of consumer surplus, producer surplus, and tax revenue is called the deadweight loss of the tax.

80 The effects of free trade can be determined by comparing the domestic price without trade to the world price. A low domestic price indicates that the country has a comparative advantage in producing the good and that the country will become an exporter. A high domestic price indicates that the rest of the world has a comparative advantage in producing the good and that the country will become an importer.

81 When a country allows trade and becomes an exporter of a good, producers of the good are better off, and consumers of the good are worse off. When a country allows trade and becomes an importer of a good, consumers of the good are better off, and producers are worse off. A tariff a tax on imports moves a market closer to the equilibrium than would exist without trade, and therefore reduces the gains from trade.

Econ 200 Fall Opportunity Cost and the Gains from Trade Supply and Demand Firms and Industries

Econ 200 Fall 2012 Microeconomics Opportunity Cost and the Gains from Trade Supply and Demand Firms and Industries Macroeconomics The Data of Macroeconomics Growth Saving and Investment Money and Exchange

Econ 200 Fall 2012 Microeconomics Opportunity Cost and the Gains from Trade Supply and Demand Firms and Industries Macroeconomics The Data of Macroeconomics Growth Saving and Investment Money and Exchange

Lecture 7. Consumers, producers, and the efficiency of markets

Lecture 7 Consumers, producers, and the efficiency of markets Revisiting the Market Equilibrium Do the equilibrium price and quantity maximize the total welfare of buyers and sellers? Market equilibrium

Lecture 7 Consumers, producers, and the efficiency of markets Revisiting the Market Equilibrium Do the equilibrium price and quantity maximize the total welfare of buyers and sellers? Market equilibrium

Introduction to Economic Institutions

Introduction to Economic Institutions ECON 1500 Week 3 Lecture 2 13 September 1 / 35 Recap 2 / 35 LAW OF SUPPLY AND DEMAND the price of any good adjusts to bring the quantity supplied and quantity demanded

Introduction to Economic Institutions ECON 1500 Week 3 Lecture 2 13 September 1 / 35 Recap 2 / 35 LAW OF SUPPLY AND DEMAND the price of any good adjusts to bring the quantity supplied and quantity demanded

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States.

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

WTP. EFFICIENCY: Demand Supply and SURPLUS

EFFICIENCY: Demand Supply and SURPLUS WTP Willingness to pay is the maximum amount that a buyer will pay for a good. It measures how much the buyer values the good or service. 1 CONSUMER SURPLUS Consumer

EFFICIENCY: Demand Supply and SURPLUS WTP Willingness to pay is the maximum amount that a buyer will pay for a good. It measures how much the buyer values the good or service. 1 CONSUMER SURPLUS Consumer

Revisiting the Market Equilibrium. Consumers, Producers, and the Efficiency of Markets. Consumer Surplus. Welfare Economics

Consumers, Producers, and the Efficiency of Markets Chapter 7 Copyright 21 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions

Consumers, Producers, and the Efficiency of Markets Chapter 7 Copyright 21 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions

Policy Evaluation Tools. Willingness to Pay and Demand. Consumer Surplus (CS) Evaluating Gov t Policy - Econ of NA - RIT - Dr.

Evaluating Gov t Policy - Econ of NA - RIT - Dr.") Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

9.1 Zero Profit for Competitive Firms in the Long Run

9.1 Zero Profit for Competitive Firms in the Long Run Chapter 9 Applications of the Competitive Model With Free Entry into the Market Along with identical costs and constant input prices, implies firms

9.1 Zero Profit for Competitive Firms in the Long Run Chapter 9 Applications of the Competitive Model With Free Entry into the Market Along with identical costs and constant input prices, implies firms

LECTURE NOTES ON MICROECONOMICS

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part 3: Firms and competition Chapter 12: Welfare analysis Problems (12.1) [Pareto improvement, economic efficiency]

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part 3: Firms and competition Chapter 12: Welfare analysis Problems (12.1) [Pareto improvement, economic efficiency]

MICROECONOMICS Midterm Test (sample)

") Student Name:.. MICROECONOMICS Midterm Test (sample) Time: 60 minutes Student Number:. Total Mark:... /50 Class:. Converted Mark:../10 Section A: QUIZ 20 marks Show your answers on the ANSWER SHEET at

Student Name:.. MICROECONOMICS Midterm Test (sample) Time: 60 minutes Student Number:. Total Mark:... /50 Class:. Converted Mark:../10 Section A: QUIZ 20 marks Show your answers on the ANSWER SHEET at

Basic Economics Chapter 7

1 Basic Economics Chapter 7 Consumers, Producers, Efficiency of Markets Welfare economics = how the allocation of resources affects economic well-being Willingness to pay = maximum amount that a buyer

1 Basic Economics Chapter 7 Consumers, Producers, Efficiency of Markets Welfare economics = how the allocation of resources affects economic well-being Willingness to pay = maximum amount that a buyer

Market structures. Why Monopolies Arise. Why Monopolies Arise. Market power. Monopoly. Monopoly resources

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Chapter 9. Applying the Competitive Model

Chapter 9. Applying the Competitive Model We know that a change in supply curve or demand curve will change the price and quantity. But how does this affect consumers and producers? How much do they lose

Chapter 9. Applying the Competitive Model We know that a change in supply curve or demand curve will change the price and quantity. But how does this affect consumers and producers? How much do they lose

Surplus and Welfare: Example 1. The efficiency of competitive markets. Surplus and Welfare: Example 1. Surplus and Welfare: Example

14.3.212 Surplus and Welfare: xample 1 The efficiency of competitive markets onsumer Willingness Firm ost pay X TL 1 Firm TL 2 Y TL 8 Firm TL 4 Z TL 7 Firm TL 6 T TL 5 Firm TL 9 ach consumer will consume

14.3.212 Surplus and Welfare: xample 1 The efficiency of competitive markets onsumer Willingness Firm ost pay X TL 1 Firm TL 2 Y TL 8 Firm TL 4 Z TL 7 Firm TL 6 T TL 5 Firm TL 9 ach consumer will consume

Consumers, Producers, and the Efficiency of Markets

Consumers, Producers, and the Efficiency of Markets PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Welfare economics Consumer Surplus How the allocation of resources affects

Consumers, Producers, and the Efficiency of Markets PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Welfare economics Consumer Surplus How the allocation of resources affects

SOLUTIONS TO TEXT PROBLEMS 7

SOLUTIONS TO TEXT PROBLEMS 7 Quick Quizzes 1. Figure 1 shows the demand curve for turkey. The price of turkey is P 1 and the consumer surplus that results from that price is denoted CS. Consumer surplus

SOLUTIONS TO TEXT PROBLEMS 7 Quick Quizzes 1. Figure 1 shows the demand curve for turkey. The price of turkey is P 1 and the consumer surplus that results from that price is denoted CS. Consumer surplus

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A.

The answer to this question is A, corresponding to Form A.") This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

The Analysis of Competitive Markets

C H A P T E R 9 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 9 OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2

C H A P T E R 9 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 9 OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2

Econ*1050 Introductory Microeconomics Instructor: Vitali Alexeev. Quiz 6 (Chapter 8)

") Econ*1050 Introductory Microeconomics Instructor: Vitali Alexeev Quiz 6 (Chapter 8) 1) A tax on a good a. raises the price buyers pay and lowers the price sellers receive. b. raises both the price buyers

Econ*1050 Introductory Microeconomics Instructor: Vitali Alexeev Quiz 6 (Chapter 8) 1) A tax on a good a. raises the price buyers pay and lowers the price sellers receive. b. raises both the price buyers

Assessment Schedule 2015 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399)

") NCEA Level 3 Economics (91399) 2015 page 1 of 11 Assessment Schedule 2015 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399) Assessment criteria with Merit with Demonstrate

NCEA Level 3 Economics (91399) 2015 page 1 of 11 Assessment Schedule 2015 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399) Assessment criteria with Merit with Demonstrate

1. As a matter of public policy, people are not allowed to sell their organs.

Chapter 7/Consumers, Producers, and the Efficiency of Markets 141 D. Case Study: Should There Be a Market in Organs? 1. As a matter of public policy, people are not allowed to sell their organs. a. In

Chapter 7/Consumers, Producers, and the Efficiency of Markets 141 D. Case Study: Should There Be a Market in Organs? 1. As a matter of public policy, people are not allowed to sell their organs. a. In

SOLUTIONS TO TEXT PROBLEMS 6

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

6) Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.

Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.") These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

Econ Microeconomics Notes

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

LECTURE February Thursday, February 21, 13

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

Microeconomics: Principles, Applications, and Tools NINTH EDITION. Chapter 6

Microeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 6 Market Efficiency and Government Intervention The housing market in New York City is highly regulated. The city issues a relatively

Microeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 6 Market Efficiency and Government Intervention The housing market in New York City is highly regulated. The city issues a relatively

1) Your answer to this question is what form of the exam you had. The answer is A if you have form A. The answer is B if you have form B etc.

Your answer to this question is what form of the exam you had. The answer is A if you have form A. The answer is B if you have form B etc.") This is the guide to Fall 2014, Midterm 1, Form A. If you have another form, the answers will be different, but the solution will be the same. Please consult your TA or instructor if you think there is

This is the guide to Fall 2014, Midterm 1, Form A. If you have another form, the answers will be different, but the solution will be the same. Please consult your TA or instructor if you think there is

FRAMINGHAM STATE COLLEGE PRINCIPLES OF MICROECONOMICS PROBLEM SET NUMBER 6

FRAMINGHAM STATE COLLEGE PRINCIPLES OF MICROECONOMICS PROBLEM SET NUMBER 6 My Name is? Text Chapter 7 Producer Surplus and Market Efficiency 2. Ernie owns a water pump. Because pumping large amounts of

FRAMINGHAM STATE COLLEGE PRINCIPLES OF MICROECONOMICS PROBLEM SET NUMBER 6 My Name is? Text Chapter 7 Producer Surplus and Market Efficiency 2. Ernie owns a water pump. Because pumping large amounts of

Supply, Demand, and Government Policies. Copyright 2004 South-Western

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Econ 101, section 3, F06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Hours needed to produce one unit of manufactured goods agricultural goods Pottawattamie 6 3 Muscatine 3 2

Econ 101, sections 2 and 6, S06 Schroeter Makeup Exam Choose the single best answer for each question. 1. A "zero sum game" is one in which a. every player breaks even in the long run. b. there is only

Econ 101, sections 2 and 6, S06 Schroeter Makeup Exam Choose the single best answer for each question. 1. A "zero sum game" is one in which a. every player breaks even in the long run. b. there is only

Queen s University Department of Economics ECON 111*S

Queen s University Department of Economics ECON 111*S Take-Home Midterm Examination May 24, 25 Instructor: Sharif F. Khan Suggested Solutions PART A TRUE/FALSE/UNCERTAIN QUESTIONS Explain why each of the

Queen s University Department of Economics ECON 111*S Take-Home Midterm Examination May 24, 25 Instructor: Sharif F. Khan Suggested Solutions PART A TRUE/FALSE/UNCERTAIN QUESTIONS Explain why each of the

2. Demand and Supply

2. Demand and Supply The following materials are taken from Chap. 3 to Chap. 7 of Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 1 of 42 2. Demand and Supply, and Market Equilibrium

2. Demand and Supply The following materials are taken from Chap. 3 to Chap. 7 of Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 1 of 42 2. Demand and Supply, and Market Equilibrium

1 Applying the Competitive Model. 2 Consumer welfare. These notes essentially correspond to chapter 9 of the text.

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

These notes essentially correspond to chapter 9 of the text. 1 Applying the Competitive Model The focus of this chapter is welfare economics. Note that "welfare" has a much di erent meaning in economics

DEMAND. Economics Unit 2 Just the Facts Handout

DEMAND Economics Unit 2 Just the Facts Handout What is Demand? A market is a place where people buy and sell things. A market has two sides. There is a buying side and a selling side. The buying side of

DEMAND Economics Unit 2 Just the Facts Handout What is Demand? A market is a place where people buy and sell things. A market has two sides. There is a buying side and a selling side. The buying side of

Econ 200, Summer 2011, Dr. Alan and Prof. Crossley. Problem Set 2. (Reference: Mankiw and Taylor, Chapters 6, 7, 8, 13)

") Multiple Choice Econ 200, Summer 2011, Dr. Alan and Prof. Crossley Problem Set 2 (Reference: Mankiw and Taylor, Chapters 6, 7, 8, 13) 1 Refer to the Figure below. Consider the impact of a tax on sellers,

Multiple Choice Econ 200, Summer 2011, Dr. Alan and Prof. Crossley Problem Set 2 (Reference: Mankiw and Taylor, Chapters 6, 7, 8, 13) 1 Refer to the Figure below. Consider the impact of a tax on sellers,

ECON 2100 (Summer 2015 Sections 07 & 08) Exam #2C

Exam #2C") ECON 21 (Summer 215 Sections 7 & 8) Exam #2C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. A Price Control generally refers to A. who bears the burden of a tax,

ECON 21 (Summer 215 Sections 7 & 8) Exam #2C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. A Price Control generally refers to A. who bears the burden of a tax,

Econ Test 2B Dr. Rupp Tuesday, March 3, 2009 Pledge: I have neither given or received aid on this exam Signature

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

Downloaded for free from 1

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Efficiency of Market Equilibrium 3.1 SAMPLE

Castle Got the answer? Be the first to stand with your group s flag. Market Equilibrium 3.1 Question 1: Define market equilibrium. Got it correct? MAKE or BREAK a castle, yours or any other group s. The

Castle Got the answer? Be the first to stand with your group s flag. Market Equilibrium 3.1 Question 1: Define market equilibrium. Got it correct? MAKE or BREAK a castle, yours or any other group s. The

Lecture 12. Monopoly

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

Lecture 3(iii) Lecture. Announcements. 1. What makes demand more elastic? 2. Income Elasticity

Lecture. Announcements. 1. What makes demand more elastic? 2. Income Elasticity") Lecture 3(iii) Announcements Lecture 1. What makes demand more elastic? 2. Income Elasticity 3. Widget Industry in Econland Consumer Surplus Producer Surplus 4. Pareto Efficiency What Makes Demand More

Lecture 3(iii) Announcements Lecture 1. What makes demand more elastic? 2. Income Elasticity 3. Widget Industry in Econland Consumer Surplus Producer Surplus 4. Pareto Efficiency What Makes Demand More

Competitive markets. Microéconomie, chapter 9. Solvay Business School Université Libre de Bruxelles

Competitive markets Microéconomie, chapter 9 Solvay Business School Université Libre de Bruxelles 1 List of subjects Evaluation of public policies Efficiency of competitive markets Minimum prices Support

Competitive markets Microéconomie, chapter 9 Solvay Business School Université Libre de Bruxelles 1 List of subjects Evaluation of public policies Efficiency of competitive markets Minimum prices Support

Supply and demand: Price-taking and competitive markets

Supply and demand: Price-taking and competitive markets ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 8 CONTEXT Firms with market power can set their own price.

Supply and demand: Price-taking and competitive markets ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 8 CONTEXT Firms with market power can set their own price.

Monopoly. Cost. Average total cost. Quantity of Output

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Outline. Introduction. ciency. Excise Tax. Subsidy 2/29

2/29 Outline Introduction ciency xcise Tax Subsidy 3/29 Where have we come from? Part I I Consumers have a set of preferences over a basket of goods I Consumers choose the basket of goods that is a ordable

2/29 Outline Introduction ciency xcise Tax Subsidy 3/29 Where have we come from? Part I I Consumers have a set of preferences over a basket of goods I Consumers choose the basket of goods that is a ordable

Monopoly. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

ECO 2301 Spring EXAM 2 Form 2 Wednesday, April 1 st Solutions

ECO 2301 Spring 2015 Sec 002 Klaus Becker EXAM 2 Form 2 Wednesday, April 1 st Solutions 1. Mathematically, price elasticity of demand is: A. the percentage change in the quantity of a good that is demanded

ECO 2301 Spring 2015 Sec 002 Klaus Becker EXAM 2 Form 2 Wednesday, April 1 st Solutions 1. Mathematically, price elasticity of demand is: A. the percentage change in the quantity of a good that is demanded

EC101 DD/EE Practice Midterm 2 November 7, 2016 Version Z

EC101 DD/EE Practice Midterm 2 November 7, 2016 Version Z Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE Practice Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION

EC101 DD/EE Practice Midterm 2 November 7, 2016 Version Z Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE Practice Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION

GRAPHS WHAAAA???!!!???

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Chapter 16: Equilibrium

Econ Microeconomic Analysis Chapter : Equilibrium Instructor: Hiroki Watanabe Spring Watanabe Econ Equilibrium / Review Market Clearance Tax Who Pays the Tax? Tax Incidence First Theorem Summary Watanabe

Econ Microeconomic Analysis Chapter : Equilibrium Instructor: Hiroki Watanabe Spring Watanabe Econ Equilibrium / Review Market Clearance Tax Who Pays the Tax? Tax Incidence First Theorem Summary Watanabe

Consumer and Producer Surplus HOW MUCH DO CONSUMERS AND PRODUCERS BENEFIT FROM AN EXCHANGE?

Consumer and Producer Surplus HOW MUCH DO CONSUMERS AND PRODUCERS BENEFIT FROM AN EXCHANGE? How much do consumers and producers benefit from an exchange? Consumer Surplus is the difference between what

Consumer and Producer Surplus HOW MUCH DO CONSUMERS AND PRODUCERS BENEFIT FROM AN EXCHANGE? How much do consumers and producers benefit from an exchange? Consumer Surplus is the difference between what

Externalities. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

10 Externalities PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Externalities Government action can sometimes improve upon market outcomes Why markets sometimes fail to

10 Externalities PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Externalities Government action can sometimes improve upon market outcomes Why markets sometimes fail to

Chapter 9. The Instruments of Trade Policy

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Government Policy, Efficiency, and Welfare

Government Policy, Efficiency, and Welfare Econ 102: Introduction to Microeconomics 1 1.1 Goals of today s class Goals of today s class Learn about consumer surplus and producer surplus, a convenient way

Government Policy, Efficiency, and Welfare Econ 102: Introduction to Microeconomics 1 1.1 Goals of today s class Goals of today s class Learn about consumer surplus and producer surplus, a convenient way

LECTURE February Tuesday, February 19, 13

LECTURE 9 19 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 MIDTERM 1: STUDY TOOLS 2 old midterms are

LECTURE 9 19 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 MIDTERM 1: STUDY TOOLS 2 old midterms are

Monopoly. Basic Economics Chapter 15. Why Monopolies Arise. Monopoly

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

Government Regulation

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

Fundamentals of Markets

Fundamentals of Markets Daniel Kirschen University of Manchester 2006 Daniel Kirschen 1 Let us go to the market... Opportunity for buyers and sellers to: compare prices estimate demand estimate supply

Fundamentals of Markets Daniel Kirschen University of Manchester 2006 Daniel Kirschen 1 Let us go to the market... Opportunity for buyers and sellers to: compare prices estimate demand estimate supply

Basics of Economics. Alvin Lin. Principles of Microeconomics: August December 2016

Basics of Economics Alvin Lin Principles of Microeconomics: August 2016 - December 2016 1 Markets and Efficiency How are goods allocated efficiently? How are goods allocated fairly? A normative statement

Basics of Economics Alvin Lin Principles of Microeconomics: August 2016 - December 2016 1 Markets and Efficiency How are goods allocated efficiently? How are goods allocated fairly? A normative statement

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Fall Semester

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester Duration: 110 minutes ECON101 - Introduction to Economics I Final Exam Type A 11 January

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester Duration: 110 minutes ECON101 - Introduction to Economics I Final Exam Type A 11 January

EC101 DD/EE Midterm 2 November 7, 2017 Version 01

EC101 DD/EE Midterm 2 November 7, 2017 Version 01 Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE F17 Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION BOOKLET:

EC101 DD/EE Midterm 2 November 7, 2017 Version 01 Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE F17 Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION BOOKLET:

EC101 DD/EE Midterm 2 November 7, 2017 Version 04

EC101 DD/EE Midterm 2 November 7, 2017 Version 04 Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE F17 Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION BOOKLET:

EC101 DD/EE Midterm 2 November 7, 2017 Version 04 Name (last, first): Student ID: U Discussion Section: Signature EC101 DD/EE F17 Midterm 2 INSTRUCTIONS (***Read Carefully***): ON YOUR QUESTION BOOKLET:

Problem Set 5. The price will be higher than the equilibrium price. There will be a surplus of cheese.

Problem Set 5 I. 1. The government has decided that the free-market price of cheese is too low. a) Suppose the government imposes a binding price floor in the cheese market. Draw a supply-and-demand diagram

Problem Set 5 I. 1. The government has decided that the free-market price of cheese is too low. a) Suppose the government imposes a binding price floor in the cheese market. Draw a supply-and-demand diagram

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Microeconomics. More Tutorial at

Microeconomics Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A legal maximum price at which a good can be sold is a price a. floor. b.

Microeconomics Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A legal maximum price at which a good can be sold is a price a. floor. b.

MONOPOLY SOLUTIONS TO TEXT PROBLEMS: Quick Quizzes

1 MONOPOLY SOLUTIONS TO TEXT PROBLEMS: Quick Quizzes 1. A market might have a monopoly because: (1) a key resource is owned by a single firm; (2) the government gives a single firm the exclusive right

1 MONOPOLY SOLUTIONS TO TEXT PROBLEMS: Quick Quizzes 1. A market might have a monopoly because: (1) a key resource is owned by a single firm; (2) the government gives a single firm the exclusive right

1. Suppose that policymakers have been convinced that the market price of cheese is too low.

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

SAMPLE FINAL. Part I - Multiple Choice Questions:

Part I - Multiple Choice Questions: SAMPLE FINAL 1. Which of the following is not a characteristic of a perfectly competitive market? a. Firms are price takers. b. Firms have difficulty entering the market.

Part I - Multiple Choice Questions: SAMPLE FINAL 1. Which of the following is not a characteristic of a perfectly competitive market? a. Firms are price takers. b. Firms have difficulty entering the market.

Instructions: DUE: day of your unit exam Block Period 1/31 st or 2/1 st

----------------- AP MICROECONOMICS-2018 MICRO Unit #1 Study Guide Name: Instructions: UE: day of your unit exam Block Period 1/31 st or 2/1 st Section 1: SUPPLY & EMAN (review Section from Semester 1)

----------------- AP MICROECONOMICS-2018 MICRO Unit #1 Study Guide Name: Instructions: UE: day of your unit exam Block Period 1/31 st or 2/1 st Section 1: SUPPLY & EMAN (review Section from Semester 1)

iv. The monopolist will receive economic profits as long as price is greater than the average total cost

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011 There are 30 multiple choice questions in this problem set. Answer these questions by the beginning of the class

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011 There are 30 multiple choice questions in this problem set. Answer these questions by the beginning of the class

ECON 4100: Industrial Organization. Lecture 2- Efficiency

ECON 4100: Industrial Organization Lecture 2- Efficiency 1 Overview Efficiency and markets Pareto Efficiency Consumer Surplus and Producer Surplus revisited A non-surplus approach to efficiency 2 Efficiency

ECON 4100: Industrial Organization Lecture 2- Efficiency 1 Overview Efficiency and markets Pareto Efficiency Consumer Surplus and Producer Surplus revisited A non-surplus approach to efficiency 2 Efficiency

Now suppose a price ceiling of 15 is set by the government.

1. The demand function is Q d = 1 2, and the supply function is = 10 + Q s. a. What is the market equilibrium price and quantity? b. What is the consumer surplus, producer surplus, dead weight loss (WL)

1. The demand function is Q d = 1 2, and the supply function is = 10 + Q s. a. What is the market equilibrium price and quantity? b. What is the consumer surplus, producer surplus, dead weight loss (WL)

Supply, demand and government policies. Dr. Anna Kowalska-Pyzalska

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

PART ONE. Consumers, producers and the efficiency of markets SUPPLY AND DEMAND II: MARKETS AND WELFARE. Learning objectives

PART ONE SUPPLY AND DEMAND II: MARKETS AND WELFARE O1 Consumers, producers and the efficiency of markets O2 Application: The costs of taxation O3 Application: International trade O1 Consumers, producers

PART ONE SUPPLY AND DEMAND II: MARKETS AND WELFARE O1 Consumers, producers and the efficiency of markets O2 Application: The costs of taxation O3 Application: International trade O1 Consumers, producers

Monopoly. While a competitive firm is a price taker, a monopoly firm is a price maker.

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

Chapter 5- Efficiency and Equity Resource Allocation Methods evaluate the ability of markets to allocate resources efficiently and fairly we must

Chapter 5- Efficiency and Equity Resource Allocation Methods evaluate the ability of markets to allocate resources efficiently and fairly we must compare it with its alternative resources are scare, must

Chapter 5- Efficiency and Equity Resource Allocation Methods evaluate the ability of markets to allocate resources efficiently and fairly we must compare it with its alternative resources are scare, must

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus

C H A P T E R 9 The Analysis of Competitive Markets CHAPTER OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2 The Efficiency of Competitive Markets

C H A P T E R 9 The Analysis of Competitive Markets CHAPTER OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2 The Efficiency of Competitive Markets

knows?) What we do know is that S1, S2, S3, and S4 will produce because they are the only ones

What we do know is that S1, S2, S3, and S4 will produce because they are the only ones") Guide to the Answers to Midterm 1, Fall 2010 (Form A) (This was put together quickly and may have typos. You should really think of it as an unofficial guide that might be of some use.) 1. First, it s

Guide to the Answers to Midterm 1, Fall 2010 (Form A) (This was put together quickly and may have typos. You should really think of it as an unofficial guide that might be of some use.) 1. First, it s

1. Perfect Competition and Efficiency 2. Extending the Reach of the Invisible Hand: 3. Extending the Reach of the Invisible Hand:

Chapter 7: and the Invisible Hand Chapter Outline 1. 2. 3. Allocation of Resources across Industries 4. Prices Guide the Invisible Hand 5. Equity and Efficiency Modified by Key Ideas 1. The invisible hand

Chapter 7: and the Invisible Hand Chapter Outline 1. 2. 3. Allocation of Resources across Industries 4. Prices Guide the Invisible Hand 5. Equity and Efficiency Modified by Key Ideas 1. The invisible hand

Externalities. (a short presentation)

") Externalities (a short presentation) WHY EXTERNALITIES ARE IMPORTANT? Adam Smith s invisible hand : self-interested buyers and sellers maximize the total benefit that society can derive from a market.

Externalities (a short presentation) WHY EXTERNALITIES ARE IMPORTANT? Adam Smith s invisible hand : self-interested buyers and sellers maximize the total benefit that society can derive from a market.

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot):

:") 1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Econ 2113 Test #2 Dr. Rupp Fall 2008

D Econ 2113 Test #2 Dr. Rupp Fall 2008 Name Pledge: I have neither given nor received aid on this exam Version A Signature: Directions: Bubble in name: Last, First Bubble in 00 in Special Codes Sign the

D Econ 2113 Test #2 Dr. Rupp Fall 2008 Name Pledge: I have neither given nor received aid on this exam Version A Signature: Directions: Bubble in name: Last, First Bubble in 00 in Special Codes Sign the

Econ 1 Review Session 1. with Maggie aproberts-warren UCSC Fall 2012

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Monopoly. Chapter 15

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

Economics 110 Midterm #2 Practice Multiple Choice Qs Spring 2014

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

within this range? c. Over what range of prices is the demand for motel rooms unit elastic? To

1. Identify the parts of the circular-flow diagram immediately involved in the following transactions. a. Mary buys a car from Jaguar for 40,000. b. Jaguar pays Joe 2,500/month for work on the assembly

1. Identify the parts of the circular-flow diagram immediately involved in the following transactions. a. Mary buys a car from Jaguar for 40,000. b. Jaguar pays Joe 2,500/month for work on the assembly

ECON 101 KONG Midterm 2 CMP Review Session. Presented by Benji Huang

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

Class Agenda. Note: As you hand-in your quiz, pick-up graded HWK #1 and HWK #2 (due next Tuesday).

.") Class 7 Class Agenda 1. Finish discussion on consumer and producer surplus (welfare theory). 2. Elasticity problems (individual/group work to prep for quiz). 3. Quiz #1. Note: As you hand-in your quiz,

Class 7 Class Agenda 1. Finish discussion on consumer and producer surplus (welfare theory). 2. Elasticity problems (individual/group work to prep for quiz). 3. Quiz #1. Note: As you hand-in your quiz,

EXAMINATION 2 VERSION B "Applications of Supply and Demand" October 12, 2016

William M. Boal Signature: Printed name: EXAMINATION 2 VERSION B "Applications of Supply and Demand" October 12, 2016 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted,

William M. Boal Signature: Printed name: EXAMINATION 2 VERSION B "Applications of Supply and Demand" October 12, 2016 INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted,

IB Economics Competitive Markets: Demand and Supply 1.4: Price Signals and Market Efficiency

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

Monopoly and How It Arises

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

Consumers, Producers, and the Efficiency of Markets. Premium PowerPoint Slides by Vance Ginn & Ron Cronovich

C H A T E R Consumers, roducers, and the Efficiency of Markets Economics R I N C I L E S O F N. Gregory Mankiw remium oweroint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage

C H A T E R Consumers, roducers, and the Efficiency of Markets Economics R I N C I L E S O F N. Gregory Mankiw remium oweroint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Fall Semester

Duration: 50 minutes Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester ECON101 - Introduction to Economics I Quiz 2 Answer Key 16 December

Duration: 50 minutes Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester ECON101 - Introduction to Economics I Quiz 2 Answer Key 16 December