The Future of Banking Transformation to a new norm CCG Catalyst Consulting Group

|

|

|

- Diana Fields

- 6 years ago

- Views:

Transcription

1 The Future of Banking Transformation to a new norm

2 CONFIDENTIALITY STATEMENT This document and its contents are confidential and the exclusive property of CCG Catalyst, LLC d.b.a. CCG Catalyst Consulting Group. Any reproduction or dissemination, in any form (written, verbal, electronic or otherwise), without prior written consent of CCG Catalyst is strictly prohibited.

3 In the not so distant future 3

4 4

5 Disruptions like never before

6 Outdated models get replaced Out with the old In with the new

7 Disruptive forces in banking Consolidation Margin Less diverse revenue stream Waning market share in consumer, real estate, commercial + industrial lending markets Legacy systems Competitor rivalry within the bank industry Cost of customer acquisition customer s switching costs Customers demand for more self service they want it now! Crowdsourcing Threat of new entrants like Google, Apple and PayPal, traditional retailers like Wal- Mart, and new firms like Moven and Venmo. Competition outside of traditional banking are new forms of exchange like peer-topeer payments and cryptocurrencies, such as Bitcoin.

8

9 TRANSFORMING

10 THE PAYMENT PROCESSING ECOSYSTEM Acquirers/Processors Issuers Card Networks Gateways ISOs/MSPs

11 CONSUMER TECHNOLOGY Mobile Wallets P2P Payments Phone-Only Carrier Billing Remittances

12 Future View

13

14

15

16 16

17 17

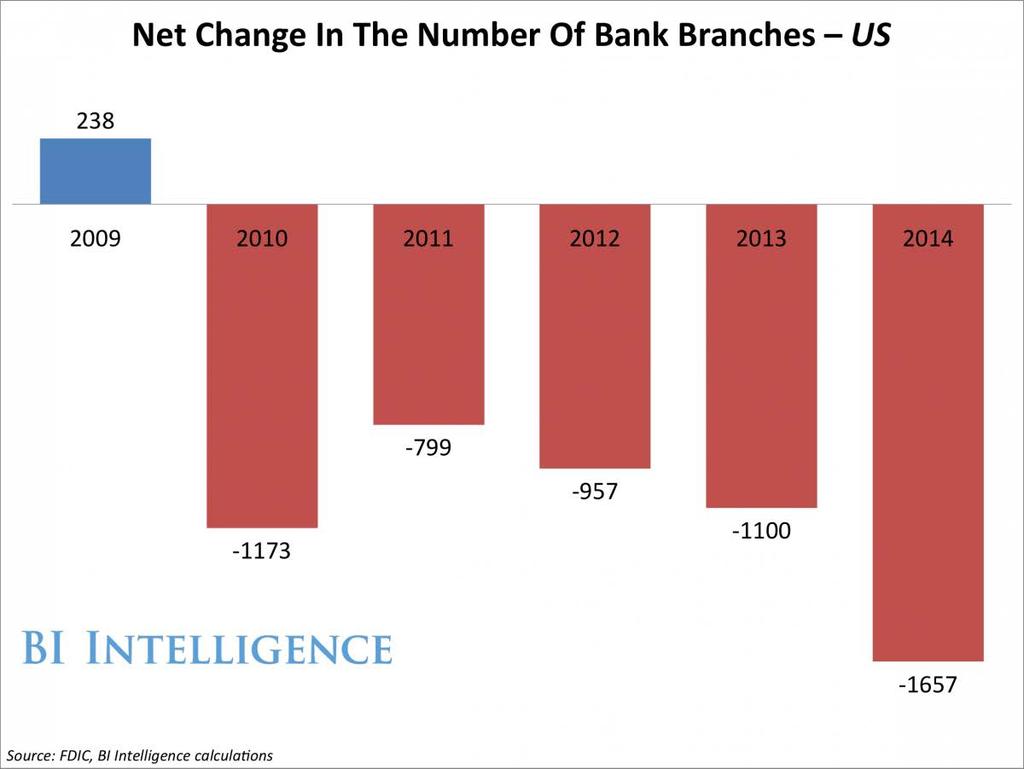

18 Summing it up Branch transaction activity declined 45% since Check use declined 68% since Top 50 U.S. banks have reduced branch networks. but branch density hasn t changed significantly. With a 40% decline in US bank branches since 1991 and projected continuing decline of 25% by Source FDIC

19 Internet of Everything Move to connected the thing learns the needs, negotiates and recalibrates at will. Move to free markets Move to integrated Move to optimize Move to programmable Move to two-way Started out web enablement of household equipment Banking apps moving towards a similar path Source: Nest

20 We are at the beginning of a major transformation to the financial services industry. 20

21 Transitional factors Internal Strategic Development Planning Segmentation Capital Consolidation [M&A] CHANGE External Changing demographics Creation of aggressive 3 rd competition Technology innovation Economic shift 21

22 Moving towards transformation

23 Changing perspectives CONSUMERS WANT Life experience Integration and automation Self-Serve To make better, more informed decisions Transactions to be in real time Scheduling and tasks BUSINESSES Want help to increase revenue See global markets Self-Serve See technology as a way to get closer to more customers and faster service Transactions to be in real time What do they need?

24 Convenience 24

25 Insights 25

26 Estimated Device Shipments Enterprise Government Home By Sector 2014E 2015E 2016E 2017E 2018E 2019E 3,000 2,500 2,000 1,500 1, Millions Of Devices Shipped Source: BI Intelligence, 2014

27 27

28 Banking moving from transactional to experience Deeper Connection Transaction Level: accurate, convenient, flexible, rewarding Historical Integrated Level: Enhances experience by linking together payment and related products and experiences. Coming now and growing Life experience Level: Everything ties together and provides guidance to individual that incorporates everything. A few years out, but coming quickly. 28

29 9 Ways this will impact banking 1. Strategic planning 2. Banks will move to become engaged with what happens before and after a transaction 3. Cooperative Partnerships 4. More modular add-on technology. 5. More bank programming. 6. More customer centric bank organization. 7. More customer centric internal committees. 8. Bank brands will change 9. More of a relationship sales approach 29

30 What s a Bank to do? 30

31 Follow the leader? 31

32 Listen to your vendors? 32

33 Are you uncertain of how to proceed? 33

34 Who are you? 34

35 What is your business? 35

36 Is it current? 36

37 Are you a leader? 37

38 Differentiation, what is it? Image source: Wikimedia Commons, the free media repository Image source: Digital Trends 38

39 Differentiation, what is it? Image source: Wikimedia Commons, the free media repository Image source: Digital Trends 39

40 What is a Customer Centric business model? 40

41 Banks with strategies that are working 3.00 ROA Before and After Three Strategies that worked

42 Bank with strategy that worked Strategy: Specialize in high net worth individuals. Structure: Three separate but integrated Trust, Wealth Mgmt, and a Private Bank. Specialty in Family wealth and education Financial: Fewer but higher paid staff and lower occupancy. Low losses, low margin, only slightly above average non interest income, and high liquidity. Online presence: Website more of a content site. Weekly economic and market forecasts. Weekly family wealth education seminars. No Facebook. Other comments: Philanthropy as a competence to train others with wealth. Bank 1 Size: $509 Million 42

43 Bank with strategy that worked Strategy: Industrial bank, captive home improvement loans under a retail energy company Structure: Only do home improvement loans, funneled through contractors, funded by primarily brokered CD s. Financial: Very high interest income and high credit losses, netting way above average margin 8.19% with 1% of Assets credit loss and no fee income. Risky lack of liquidity. Efficiency in delivery. Online presence: Facebook reads like newsletter to home improvement contractors. Advertising to a large extent happens through indirect. Other Comments: A number of negative comments on Facebook from consumers. Risk in indirect lending. Bank 2 Size: $1.07 Billion 43

44 Bank with strategy that worked Strategy: Dominate a small area with traditional banking. Mortgage Center, Heritage Club Structure: Three branches, one in larger city. Market share leader in two smaller ones, growing in large. Financial: Mostly from margin with above average loan rates and below average deposit rates. Below avg salary, above avg number of people. Online presence: No Facebook. No content. No press releases. No mobile banking. Online banking requires in person or US Mail. Other Comments: The old school, heads down, own the local market still lives. Bank 3 Size: $284 Million 44

45 Bank with strategy that worked Strategy: Commercial Lender, Specialty in Construction expanded C&I and CRE Structure: Five branches, large metropolitan market area. Market leader in their markets, adding a branch, overall growing Financial: Great margin due to the specialization above average loan rates and higher average deposit rates due to growth requirement. Online presence: Focused to their market and niche. Referrals from other banks Other Comments: Progressive bank, long history (over 150 years) well capitalized, cherry picked loan portfolio. Bank 4 Size: $1.7 Billion 45

46 Transformation is happening, let s plan for it. Banks are transforming from financial services firms to a part of a grand effort of the newly enabled customer to find a more optimal relationship with their money that improves their life experience. It s happening already. With changes coming at a breakneck pace. There s no one answer but many things can be done to prepare. First step? Match the new economy and become more customer centric. 46

47 CCG Catalyst is a banking consulting firm and the trusted strategic advisor to banking organizations throughout the Americas. We understand the needs of our clients. We solve problems that are brought about by the disruptions and changes in the financial industry, technology, and the economy. We strategically think about our clients business, partner with them, to make them successful; but more so we form a relationship, go beyond the trends, imagine the future, and stimulate thoughts. CCG Catalyst is headquartered in Phoenix, AZ, with consulting office across the US.

48 Thank you! CCG Catalyst Consulting Group Two Renaissance, 40 North Central Avenue, Suite 1400, Phoenix, AZ Phoenix Atlanta Austin Chicago New York San Francisco Seattle Washington

The Age of Mobile Wallets What Banks Need to Know When Considering the Creation of a Bank Branded Mobile Wallet

RESEARCH HIGHLIGHTS The Age of Mobile Wallets What Banks Need to Know When Considering the Creation of a Bank Branded Mobile Wallet CCG Catalyst investigated and examined customers behaviors and attitudes

RESEARCH HIGHLIGHTS The Age of Mobile Wallets What Banks Need to Know When Considering the Creation of a Bank Branded Mobile Wallet CCG Catalyst investigated and examined customers behaviors and attitudes

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C.

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2 Emerging Trends Industry Consolidation Branch Banking/Digital Services ecommerce Payment Systems Artificial Intelligence Customers Facing

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2 Emerging Trends Industry Consolidation Branch Banking/Digital Services ecommerce Payment Systems Artificial Intelligence Customers Facing

LEADING WITH GRC. Retail evolution and disruption. Gordon Smith CEO, Chase Consumer & Community Banking

LEADING WITH GRC Retail evolution and disruption Gordon Smith CEO, Chase Consumer & Community Banking The game changer $2,495 - $3,495 $600 $499- $599 1989 2004 2007 Smart phones created a massive shift

LEADING WITH GRC Retail evolution and disruption Gordon Smith CEO, Chase Consumer & Community Banking The game changer $2,495 - $3,495 $600 $499- $599 1989 2004 2007 Smart phones created a massive shift

How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

Investing In Next Generation Mobile Platforms To Support Changing Business Models

MOBILE banking crossroads: Investing In Next Generation Mobile Platforms To Support Changing Business Models EXECUTIVE SUMMARY Mobile presents tremendous opportunities customer acquisition and retention,

MOBILE banking crossroads: Investing In Next Generation Mobile Platforms To Support Changing Business Models EXECUTIVE SUMMARY Mobile presents tremendous opportunities customer acquisition and retention,

Inside magazine issue 16 Part 01 - From a digital perspective Re-envisioning the customer banking experience

Re-envisioning the customer banking experience Olivier de Groote Partner Financial Services Industry Leader Deloitte Cedric Deleuze Partner Technology Deloitte Deloitte s digital bank solution is fundamentally

Re-envisioning the customer banking experience Olivier de Groote Partner Financial Services Industry Leader Deloitte Cedric Deleuze Partner Technology Deloitte Deloitte s digital bank solution is fundamentally

How Will Your Bank Thrive?

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

SunTrust Retail Line of Business

SunTrust Retail Line of Business Gene Kirby Corporate Executive Vice President Retail Line of Business Manager Ryan Beck & Co. Financial Institutions Investor Conference November 2005 LEGAL DISCLOSURE

SunTrust Retail Line of Business Gene Kirby Corporate Executive Vice President Retail Line of Business Manager Ryan Beck & Co. Financial Institutions Investor Conference November 2005 LEGAL DISCLOSURE

loyalty points Smartphone PINpad portal of fers secure terminal Android windows receipt business banking customer experience

tance ner ce ation m a voucher transactions Windows d payments eckout customer receipt credit shop M-invoicing Tablet io S mpos inno BlackBer ry seamless NF C ios receipt business banking loyalty points

tance ner ce ation m a voucher transactions Windows d payments eckout customer receipt credit shop M-invoicing Tablet io S mpos inno BlackBer ry seamless NF C ios receipt business banking loyalty points

The Future of Fintech Five technology trends driving the financial services industry.

Five technology trends driving the financial services industry. Originally designating any financial services-specific technology, fintech has emerged as an industry in its own right. Investment in fintech

Five technology trends driving the financial services industry. Originally designating any financial services-specific technology, fintech has emerged as an industry in its own right. Investment in fintech

High Performance Non Interest Income. a High Performance Briefing by Resurgent Performance

High Performance Non Interest Income a High Performance Briefing by High Performance Non Interest Income Non Interest Income (NII) has been an elusive metric for many years. Finding the secret formula

High Performance Non Interest Income a High Performance Briefing by High Performance Non Interest Income Non Interest Income (NII) has been an elusive metric for many years. Finding the secret formula

Financial Services in an era of Exponential change. Oracle Open World October, 2015

Financial Services in an era of Exponential change Oracle Open World October, 2015 D E L O I T T E CDO EN LSO UI TLT TIE NCG OLN LSP U LT I N G L L P Executive Summary EXECUTIVE SUMMARY The Financial Services

Financial Services in an era of Exponential change Oracle Open World October, 2015 D E L O I T T E CDO EN LSO UI TLT TIE NCG OLN LSP U LT I N G L L P Executive Summary EXECUTIVE SUMMARY The Financial Services

It starts today. Chief Executive Officer s Message

It starts today Darryl White Chief Executive Officer BMO is on the move. Adapting. Innovating. Working hard to anticipate customers expectations and deliver value to shareholders. Always. Now it s year

It starts today Darryl White Chief Executive Officer BMO is on the move. Adapting. Innovating. Working hard to anticipate customers expectations and deliver value to shareholders. Always. Now it s year

INCREASING REVENUE GENERATION

INCREASING REVENUE GENERATION Drive maximum returns from your ATM investment. An NCR White Paper It s not a question of if, it s a question of when. As customer needs change and evolve, keeping pace with

INCREASING REVENUE GENERATION Drive maximum returns from your ATM investment. An NCR White Paper It s not a question of if, it s a question of when. As customer needs change and evolve, keeping pace with

The Electronification of Payments Digital disruptors and the future of the DDA. George Warfel Director Payments PwC

The Electronification of Payments Digital disruptors and the future of the DDA George Warfel Director Payments Banks were once effectively the sole providers of all ways to pay C2B B2C B2B P2P PAPER Cash

The Electronification of Payments Digital disruptors and the future of the DDA George Warfel Director Payments Banks were once effectively the sole providers of all ways to pay C2B B2C B2B P2P PAPER Cash

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm Patrick Laurent Partner Technology & Enterprise Application Leader Deloitte Thibault Chollet Director Technology

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm Patrick Laurent Partner Technology & Enterprise Application Leader Deloitte Thibault Chollet Director Technology

The Magnificent 7 Cs of Change in U.S. Financial Services. Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013

The Magnificent 7 Cs of Change in U.S. Financial Services Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013 3 Game Changers The 7Cs: Consolidation Convergence Customer (Member)

The Magnificent 7 Cs of Change in U.S. Financial Services Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013 3 Game Changers The 7Cs: Consolidation Convergence Customer (Member)

ACCELERATING IoT CONNECTIVITY

ACCELERATING IoT CONNECTIVITY 1717 McKinney Avenue Suite 1050 Dallas, Texas 75202 Page 1 Phone: (214) 765-9500 Email: info@avanci.com AVANCI: ACCELERATING IOT CONNECTIVITY AVANCI.COM The Internet of Things

ACCELERATING IoT CONNECTIVITY 1717 McKinney Avenue Suite 1050 Dallas, Texas 75202 Page 1 Phone: (214) 765-9500 Email: info@avanci.com AVANCI: ACCELERATING IOT CONNECTIVITY AVANCI.COM The Internet of Things

Investor Presentation

April 2018 Investor Presentation April, 2018 Cautionary statement regarding forward looking statements «Safe Harbor» Statement under the U.S. Private Securities Litigation Reform Act of 1995: the matters

April 2018 Investor Presentation April, 2018 Cautionary statement regarding forward looking statements «Safe Harbor» Statement under the U.S. Private Securities Litigation Reform Act of 1995: the matters

Here, There, Everywhere: The Rise of Omnichannel Banking. Chris Fleischer Market Research Manager D+H

Here, There, Everywhere: The Rise of Omnichannel Banking Chris Fleischer Market Research Manager D+H chris.fleischer@dh.com @ccfleischer Omnichannel is more than a buzzword Omnichannel is more than a buzzword

Here, There, Everywhere: The Rise of Omnichannel Banking Chris Fleischer Market Research Manager D+H chris.fleischer@dh.com @ccfleischer Omnichannel is more than a buzzword Omnichannel is more than a buzzword

10 Trends For The Future of Banking

10 Trends For The Future of Banking IBA Emerging Leaders September of 2015 Chris Nichols Twitter: @CSB4Banks Industry Homogeneity 2 Non-Bank Competition In 5 Years That is 81% of banks! 3 Preparing for

10 Trends For The Future of Banking IBA Emerging Leaders September of 2015 Chris Nichols Twitter: @CSB4Banks Industry Homogeneity 2 Non-Bank Competition In 5 Years That is 81% of banks! 3 Preparing for

Lecture Materials RETAIL BANKING

Lecture Materials RETAIL BANKING Virginia Heyburn Vice President, Strategic Pursuits Fiserv virginia.heyburn@fiserv.com Miami Beach, Florida 786-239-4898 August 8, 2017 Vision 2020: Growing the Banking

Lecture Materials RETAIL BANKING Virginia Heyburn Vice President, Strategic Pursuits Fiserv virginia.heyburn@fiserv.com Miami Beach, Florida 786-239-4898 August 8, 2017 Vision 2020: Growing the Banking

Case Study. Results. The business. The challenge

Case Study Xavier Latte Head of Performance Management, Clicktale indeed showed us some issues that we were not able to discover with traditional analytics tools. Company www.hellobank.be Industry Finance

Case Study Xavier Latte Head of Performance Management, Clicktale indeed showed us some issues that we were not able to discover with traditional analytics tools. Company www.hellobank.be Industry Finance

RETAIL BANKING: Customer Segment Performance Blueprint A WEB-BASED PERFORMANCE MANAGEMENT APPLICATION

RETAIL BANKING: Customer Segment Performance Blueprint A WEB-BASED PERFORMANCE MANAGEMENT APPLICATION Introduction: driving success one customer at a time Ask most financial services executives about their

RETAIL BANKING: Customer Segment Performance Blueprint A WEB-BASED PERFORMANCE MANAGEMENT APPLICATION Introduction: driving success one customer at a time Ask most financial services executives about their

Creating value from the open API economy A blueprint for banks

WHITE PAPER Creating value from the open API economy A blueprint for banks Change is inevitable as banks explore opportunities for leveraging open APIs to extend and transform their business models. This

WHITE PAPER Creating value from the open API economy A blueprint for banks Change is inevitable as banks explore opportunities for leveraging open APIs to extend and transform their business models. This

Banking on Small-Business Needs Sponsored by:

Banking on Small-Business Needs Sponsored by: 2014 Yodlee. All rights reserved. Reproduction of this white paper by any means is strictly prohibited. EXECUTIVE SUMMARY Banking on Small-Business Needs,

Banking on Small-Business Needs Sponsored by: 2014 Yodlee. All rights reserved. Reproduction of this white paper by any means is strictly prohibited. EXECUTIVE SUMMARY Banking on Small-Business Needs,

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C.

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

Trends Shaping the Bank of the Future

Trends Shaping the Bank of the Future MBA Bank Management and Directors Conference November 30, 2017 Timothy Reimink Managing Director 2017 Crowe Horwath 2017 Crowe Horwath LLP 1LLP This presentation was

Trends Shaping the Bank of the Future MBA Bank Management and Directors Conference November 30, 2017 Timothy Reimink Managing Director 2017 Crowe Horwath 2017 Crowe Horwath LLP 1LLP This presentation was

the 3 pillars of a superior digital customer experience in banking

the 3 pillars of a superior digital customer experience in banking a gap is emerging between the financial firms that are embracing digital business transformation and those that continue doing things

the 3 pillars of a superior digital customer experience in banking a gap is emerging between the financial firms that are embracing digital business transformation and those that continue doing things

API Gateway Digital access to meaningful banking content

API Gateway Digital access to meaningful banking content Unlocking The Core Jason Williams, VP Solution Architecture April 10 2017 APIs In Banking A Shift to Openness Major shift in Banking occurring whereby

API Gateway Digital access to meaningful banking content Unlocking The Core Jason Williams, VP Solution Architecture April 10 2017 APIs In Banking A Shift to Openness Major shift in Banking occurring whereby

Strategies for credit institutions growth. Credit Institution management Lecture 13.

Strategies for credit institutions growth Credit Institution management Lecture 13. 1. Global perspective Where can we earn money in banking business? Source: Roaring to life: Growth and innovation in

Strategies for credit institutions growth Credit Institution management Lecture 13. 1. Global perspective Where can we earn money in banking business? Source: Roaring to life: Growth and innovation in

Innovation and competition in Internet and mobile banking: an industrial organization perspective

Innovation and competition in Internet and mobile banking: an industrial organization perspective Carlotta Mariotto 1 Marianne Verdier 2 1 Mines ParisTech - Centre for Industrial Economics (CERNA), Paris

Innovation and competition in Internet and mobile banking: an industrial organization perspective Carlotta Mariotto 1 Marianne Verdier 2 1 Mines ParisTech - Centre for Industrial Economics (CERNA), Paris

Customer Segmentation and Market Analytics FHLB Regional Member Meetings

Customer Segmentation and Market Analytics 2018 FHLB Regional Member Meetings 158 Route 206 Gladstone, NJ 07934 P: (908) 604-9336 F: (908) 604-5951 finpro@finpro.us www.finpro.us 0 The evolution of customer

Customer Segmentation and Market Analytics 2018 FHLB Regional Member Meetings 158 Route 206 Gladstone, NJ 07934 P: (908) 604-9336 F: (908) 604-5951 finpro@finpro.us www.finpro.us 0 The evolution of customer

WHITE PAPER. REVENUE OPPORTUNITIES CREATED BY OPEN APIs. Venkataraman Durghados IBS Open APIs Solution Architect

REVENUE OPPORTUNITIES CREATED BY OPEN APIs Venkataraman Durghados IBS Open APIs Solution Architect Financial service providers must embrace new technologies and leverage data held in their systems to secure

REVENUE OPPORTUNITIES CREATED BY OPEN APIs Venkataraman Durghados IBS Open APIs Solution Architect Financial service providers must embrace new technologies and leverage data held in their systems to secure

Blockchain Unleashed: Petrochemical Industry Impact

Blockchain Unleashed: Petrochemical Industry Impact 1 Business networks, wealth and markets Business Networks benefit from connectivity Participants are customers, suppliers, partners Cross geography &

Blockchain Unleashed: Petrochemical Industry Impact 1 Business networks, wealth and markets Business Networks benefit from connectivity Participants are customers, suppliers, partners Cross geography &

WHITE PAPER. Revenue Opportunities Created by Open APIs

Revenue Opportunities Created by Open APIs Financial service providers must embrace modern technologies and leverage data held in their systems to secure their long-term futures. Open Banking initiatives,

Revenue Opportunities Created by Open APIs Financial service providers must embrace modern technologies and leverage data held in their systems to secure their long-term futures. Open Banking initiatives,

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

Financial Services: Maximize Revenue with Better Marketing Data. Marketing Data Solutions for the Financial Services Industry

Financial Services: Maximize Revenue with Better Marketing Data Marketing Data Solutions for the Financial Services Industry DataMentors, LLC April 2014 1 Financial Services: Maximize Revenue with Better

Financial Services: Maximize Revenue with Better Marketing Data Marketing Data Solutions for the Financial Services Industry DataMentors, LLC April 2014 1 Financial Services: Maximize Revenue with Better

U.S. COMMUNITY BANK RESULTS. Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1

U.S. COMMUNITY BANK RESULTS Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1 CREATING A NEW LEVEL OF SERVICE FOR U.S. COMMUNITY BANK CUSTOMERS Welcome to the third

U.S. COMMUNITY BANK RESULTS Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1 CREATING A NEW LEVEL OF SERVICE FOR U.S. COMMUNITY BANK CUSTOMERS Welcome to the third

Future of Retail Banking 2016

Future of Retail Banking 2016 Edwin de Ron, Partner Manager & Corporate Entrepreneur Shoot for the moon, even if you miss you will land among stars. Future of Retail Banking 2016 Edwin de Ron, Partner

Future of Retail Banking 2016 Edwin de Ron, Partner Manager & Corporate Entrepreneur Shoot for the moon, even if you miss you will land among stars. Future of Retail Banking 2016 Edwin de Ron, Partner

Retail Banking Insights

Retail Banking Insights Number 6 March 2015 Driving Revenue Growth In Retail Banking Annual revenue growth for U.S. retail banks has hovered near 2 percent since 2010, hindered by historically low interest

Retail Banking Insights Number 6 March 2015 Driving Revenue Growth In Retail Banking Annual revenue growth for U.S. retail banks has hovered near 2 percent since 2010, hindered by historically low interest

Predictive Customer Interaction Management

Predictive Customer Interaction Management An architecture that enables organizations to leverage real-time events to accurately target products and services. Don t call us. We ll call you. That s what

Predictive Customer Interaction Management An architecture that enables organizations to leverage real-time events to accurately target products and services. Don t call us. We ll call you. That s what

Mobile & Online Banking

Mobile & Online Banking Digital banking - no longer a matter of nice to have In today s world, online and mobile banking are no longer nice to have on the consumer s mind. Consumer s daily lives are seamlessly

Mobile & Online Banking Digital banking - no longer a matter of nice to have In today s world, online and mobile banking are no longer nice to have on the consumer s mind. Consumer s daily lives are seamlessly

The Digital Disruption has already happened

12 th February 2018 The Digital Disruption has already happened World s largest taxi company owns no taxis: Uber Largest accommodation provider owns no real estate: Airbnb Largest phone companies own no

12 th February 2018 The Digital Disruption has already happened World s largest taxi company owns no taxis: Uber Largest accommodation provider owns no real estate: Airbnb Largest phone companies own no

Overview of Business Models in Retail Payments

Overview of Business Models in Retail Payments EDC Council Frankfurt November 2012 Edgar, Dunn & Company, 2012 Edgar Dunn Deep Experience with Global Reach Management consultancy focused on payments since

Overview of Business Models in Retail Payments EDC Council Frankfurt November 2012 Edgar, Dunn & Company, 2012 Edgar Dunn Deep Experience with Global Reach Management consultancy focused on payments since

Information Builders. Success in. Banking

Information Builders Success in Banking Information Builders provides trusted data and actionable analytics to banking institutions. 2 Trusted Data at Scotiabank It doesn t really matter what types of

Information Builders Success in Banking Information Builders provides trusted data and actionable analytics to banking institutions. 2 Trusted Data at Scotiabank It doesn t really matter what types of

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING

IN BANKING") OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

Banking Guiding an industry in transition

Banking 2014 Guiding an industry in transition 2 EY s Banking practice Guiding an industry in transition The global financial crisis and the regulatory reform that has taken place over the past several

Banking 2014 Guiding an industry in transition 2 EY s Banking practice Guiding an industry in transition The global financial crisis and the regulatory reform that has taken place over the past several

Benefits of Investing in Digital Onboarding for Small-Business Banking

Benefits of Investing in Digital Onboarding for Small-Business Banking OCTOBER 2017 Prepared for: 2017 Avoka. All rights reserved. Reproduction of this white paper by any means is strictly prohibited.

Benefits of Investing in Digital Onboarding for Small-Business Banking OCTOBER 2017 Prepared for: 2017 Avoka. All rights reserved. Reproduction of this white paper by any means is strictly prohibited.

Business Model Canvas

Business Model Canvas 1-1 Customer Segments Defines the different groups of people or organizations to serve Separate segments if: Needs require and justify distinct offer Reached through different channels

Business Model Canvas 1-1 Customer Segments Defines the different groups of people or organizations to serve Separate segments if: Needs require and justify distinct offer Reached through different channels

Business Model Generation

Business Model Strategy Organisation and Processes Information Systems Infrastructure 2 Digital Products: Change of Business Models Example: Music Industry Vinyl disc Compact Disc Download Streaming Digitization

Business Model Strategy Organisation and Processes Information Systems Infrastructure 2 Digital Products: Change of Business Models Example: Music Industry Vinyl disc Compact Disc Download Streaming Digitization

Expectations & Experiences Channels and New Entrants. September 2017

Expectations & Experiences Channels and New Entrants September 2017 Life made easier People choose financial services options that make their lives easier. From person-to-person payments and voice activation

Expectations & Experiences Channels and New Entrants September 2017 Life made easier People choose financial services options that make their lives easier. From person-to-person payments and voice activation

Bank of the Future. Discussion on the latest banking and digital trends and their implications. April 11-12, 2016

WORKING DRAFT Last Modified 4/1/2016 5:10 PM Central Europe Standard Time Printed Bank of the Future Discussion on the latest banking and digital trends and their implications April 11-12, 2016 Banking

WORKING DRAFT Last Modified 4/1/2016 5:10 PM Central Europe Standard Time Printed Bank of the Future Discussion on the latest banking and digital trends and their implications April 11-12, 2016 Banking

EXCESS CAPACITY EXCHANGE

EXCESS CAPACITY EXCHANGE Automated Sales Platform for selling off all your products in 24 hours. 100% GUARANTEED! Every day, there is $34 trillion of excess production capacity, idle space, unsold products

EXCESS CAPACITY EXCHANGE Automated Sales Platform for selling off all your products in 24 hours. 100% GUARANTEED! Every day, there is $34 trillion of excess production capacity, idle space, unsold products

The credit card industry: navigating an evolving environment. EY Advisory Services

The credit card industry: navigating an evolving environment EY Advisory Services The credit card industry: navigating an evolving environment The path to profitability for card issuers has been increasingly

The credit card industry: navigating an evolving environment EY Advisory Services The credit card industry: navigating an evolving environment The path to profitability for card issuers has been increasingly

Building the BBVA franchise in the US. Best Practices in Retail Financial Services Symposium American Banker

Building the BBVA franchise in the US Best Practices in Retail Financial Services Symposium American Banker Marco Island FL, March 16th 2009 Disclaimer This document contains or may contain forward looking

Building the BBVA franchise in the US Best Practices in Retail Financial Services Symposium American Banker Marco Island FL, March 16th 2009 Disclaimer This document contains or may contain forward looking

OPTIMIZED, PERSONALIZED AND DYNAMIC BANKING HOW ADVANCED ANALYTICS CAN SHAPE NEXT- LEVEL PRICING AND OFFERS

OPTIMIZED, PERSONALIZED AND DYNAMIC BANKING HOW ADVANCED ANALYTICS CAN SHAPE NEXT- LEVEL PRICING AND OFFERS New and disruptive competitors are wooing bank customers with easy, personalized, fits me interactions

OPTIMIZED, PERSONALIZED AND DYNAMIC BANKING HOW ADVANCED ANALYTICS CAN SHAPE NEXT- LEVEL PRICING AND OFFERS New and disruptive competitors are wooing bank customers with easy, personalized, fits me interactions

FOCUSED BUSINESS ANALYTICS. dh.com

FOCUSED BUSINESS ANALYTICS TOTAL ANALYTICS, POWERED BY TOUCHÉ TABLE OF CONTENTS 3 Financial Services Marketing Keys 4 When it Comes to Business Analytics, Where Do You Stand Today? 5 The Total Analytics

FOCUSED BUSINESS ANALYTICS TOTAL ANALYTICS, POWERED BY TOUCHÉ TABLE OF CONTENTS 3 Financial Services Marketing Keys 4 When it Comes to Business Analytics, Where Do You Stand Today? 5 The Total Analytics

Coimatic a global decentralized blockchain deal and discount marketplace White Paper

1 P a g e Coimatic a global decentralized blockchain deal and discount marketplace White Paper 2 P a g e Table of Contents Description Introduction and Vision The Daily Deal Discount Coupon Model The Discount

1 P a g e Coimatic a global decentralized blockchain deal and discount marketplace White Paper 2 P a g e Table of Contents Description Introduction and Vision The Daily Deal Discount Coupon Model The Discount

Nordea Investor Day in London May 11, 2017

Nordea Investor Day in London May 11, 2017 Nordea Personal Banking Business Areas Presentation Day Topi Manner May 11, 2017 Starting from a strong position Largest Nordic customer base Strong local market

Nordea Investor Day in London May 11, 2017 Nordea Personal Banking Business Areas Presentation Day Topi Manner May 11, 2017 Starting from a strong position Largest Nordic customer base Strong local market

Connected Banking Through Enhanced B2B

White Paper Connected Banking Through Enhanced B2B Sponsored by: IBM Jerry Silva October 2017 IN THIS WHITE PAPER Digital transformation is the driving force behind new initiatives in financial services

White Paper Connected Banking Through Enhanced B2B Sponsored by: IBM Jerry Silva October 2017 IN THIS WHITE PAPER Digital transformation is the driving force behind new initiatives in financial services

fmswhitepaper Low transaction-volume branches: An overlooked opportunity By Michael Scott President and CEO, FMSI

fmswhitepaper Low transaction-volume branches: An overlooked opportunity By Michael Scott President and CEO, FMSI Unique Insights Implementation Guidance Strategic and Tactical Direction Immediately Relevant

fmswhitepaper Low transaction-volume branches: An overlooked opportunity By Michael Scott President and CEO, FMSI Unique Insights Implementation Guidance Strategic and Tactical Direction Immediately Relevant

PayPal Holdings Inc. (PYPL US)

") PayPal Holdings Inc. (PYPL US) BUY, TP $46.7 (+25%) Otar Dgebuadze, CFA MBA2017 www.london.edu Market Overview and Presence Strong Position on Huge and Growing Market Current Presence Potential 2.5Tn Online

PayPal Holdings Inc. (PYPL US) BUY, TP $46.7 (+25%) Otar Dgebuadze, CFA MBA2017 www.london.edu Market Overview and Presence Strong Position on Huge and Growing Market Current Presence Potential 2.5Tn Online

Product. LoanServ An Integrated, Real-Time Servicing Platform Designed to Efficiently Manage All of Your Consumer Lending Products

Product LoanServ An Integrated, Real-Time Servicing Platform Designed to Efficiently Manage All of Your Consumer Lending Products Product LoanServ from Fiserv supports all retail loans and lines of credit

Product LoanServ An Integrated, Real-Time Servicing Platform Designed to Efficiently Manage All of Your Consumer Lending Products Product LoanServ from Fiserv supports all retail loans and lines of credit

Bank Technology Trends. Jim Stewart Chief Information Security Officer United Community Bank

Bank Technology Trends Jim Stewart Chief Information Security Officer United Community Bank Welcome to the Georgia Banking School! Give appreciation and feedback to those that allowed you to attend. Encourage

Bank Technology Trends Jim Stewart Chief Information Security Officer United Community Bank Welcome to the Georgia Banking School! Give appreciation and feedback to those that allowed you to attend. Encourage

REINVENTING CHECKING ACCOUNTS. RON SHEVLIN Director of Research Cornerstone Advisors A WHITE PAPER COMMISSIONED BY

REINVENTING CHECKING ACCOUNTS RON SHEVLIN Director of Research Cornerstone Advisors A WHITE PAPER COMMISSIONED BY TABLE OF CONTENTS 1 Executive Summary 2 About the Data 3 The Threats to Checking Accounts

REINVENTING CHECKING ACCOUNTS RON SHEVLIN Director of Research Cornerstone Advisors A WHITE PAPER COMMISSIONED BY TABLE OF CONTENTS 1 Executive Summary 2 About the Data 3 The Threats to Checking Accounts

Today s Financial Consumer: Open for Business

Today s Financial Consumer: Open for Business Bank consumers will ultimately decide the future, so for the past four years CGI has been researching consumer perspectives on digital banking annually. CGI

Today s Financial Consumer: Open for Business Bank consumers will ultimately decide the future, so for the past four years CGI has been researching consumer perspectives on digital banking annually. CGI

Increase Efficiency Boost Growth Stay Ahead of the Curve

Increase Efficiency Boost Growth Stay Ahead of the Curve 3 Payments are going digital, contactless and mobile at a stunning pace. And while bank branches are still very much part of our urban landscape,

Increase Efficiency Boost Growth Stay Ahead of the Curve 3 Payments are going digital, contactless and mobile at a stunning pace. And while bank branches are still very much part of our urban landscape,

Paperless Applications for the Insurance Industry Online Document Solutions

Paperless Applications for the Insurance Industry Online Document Solutions Paperless Applications for the Insurance Industry At a time when environmental concerns are at an all-time high, old-fashioned

Paperless Applications for the Insurance Industry Online Document Solutions Paperless Applications for the Insurance Industry At a time when environmental concerns are at an all-time high, old-fashioned

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

The Road Ahead Brant Standridge President, Retail Banking. Investor Day 2018

The Road Ahead Brant Standridge President, Retail Banking Investor Day 2018 Key Takeaways 1Organizing for exceptionalism Enhancing the 2client experience 3Capitalizing on untapped revenue opportunities

The Road Ahead Brant Standridge President, Retail Banking Investor Day 2018 Key Takeaways 1Organizing for exceptionalism Enhancing the 2client experience 3Capitalizing on untapped revenue opportunities

4 Threats to Small Business Banking and How to Defuse Them

EBOOK 4 Threats to Small Business Banking and How to Defuse Them Gaps in Bank Offerings are Resulting in Small Businesses Going Elsewhere. Find Out How to Turn This Trend Around and Create More Rewarding

EBOOK 4 Threats to Small Business Banking and How to Defuse Them Gaps in Bank Offerings are Resulting in Small Businesses Going Elsewhere. Find Out How to Turn This Trend Around and Create More Rewarding

Global Headquarters: 5 Speen Street Framingham, MA USA P F

Digital Services Play a Key Part in Customer Acquisition a n d Retention W H I T E P A P E R Sponsored by: Adobe Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.620.5533 F.508.988.6761

Digital Services Play a Key Part in Customer Acquisition a n d Retention W H I T E P A P E R Sponsored by: Adobe Global Headquarters: 5 Speen Street Framingham, MA 01701 USA P.508.620.5533 F.508.988.6761

Key Success Factors for Digital Transformation in the Banking Industry

WHITE PAPER Key Success Factors for Digital Transformation in the Banking Industry Sponsored by: TCS Digital Software & Solutions Jerry Silva November 2015 In 2015, IDC conducted in-depth interviews with

WHITE PAPER Key Success Factors for Digital Transformation in the Banking Industry Sponsored by: TCS Digital Software & Solutions Jerry Silva November 2015 In 2015, IDC conducted in-depth interviews with

Bank Platform. Signature A Fully Customizable and Feature-Rich Banking Platform for a Sharper Competitive Edge

Bank Platform Signature A Fully Customizable and Feature-Rich Banking Platform for a Sharper Competitive Edge Fiserv is the U.S. market leader in account processing services. More than one-third of U.S.

Bank Platform Signature A Fully Customizable and Feature-Rich Banking Platform for a Sharper Competitive Edge Fiserv is the U.S. market leader in account processing services. More than one-third of U.S.

Experience. Agility.

Experience Agility ABOUT IDEALINVENT Established in 2005, IDEALINVENT Technologies Pvt. Ltd provides solutions through innovative products focused on the banking and financial industry. Our products and

Experience Agility ABOUT IDEALINVENT Established in 2005, IDEALINVENT Technologies Pvt. Ltd provides solutions through innovative products focused on the banking and financial industry. Our products and

Payments Innovation and National Payment Strategies

Payments Innovation and National Payment Strategies Peter Sidenius, Director Warsaw 9 December 2015 Peter Sidenius peter.sidenius@edgardunn.com Global Financial Services & Payments EDGAR, DUNN & COMPANY

Payments Innovation and National Payment Strategies Peter Sidenius, Director Warsaw 9 December 2015 Peter Sidenius peter.sidenius@edgardunn.com Global Financial Services & Payments EDGAR, DUNN & COMPANY

TITLE Lorem ipsum dolor sit amet

A Guide to Navigating the Mobile Payments Industry TITLE Lorem ipsum dolor sit amet White Paper Table of Contents 1. Introduction 2. Mobile Payment Statistics 3. Technological Advancements in Payments

A Guide to Navigating the Mobile Payments Industry TITLE Lorem ipsum dolor sit amet White Paper Table of Contents 1. Introduction 2. Mobile Payment Statistics 3. Technological Advancements in Payments

Intelligent Payment Management for Today and Tomorrow Technology Advancement to Navigate the Converging Payments Landscape

Intelligent Payment Management for Today and Tomorrow Technology Advancement to Navigate the Converging Payments Landscape Adapting to the Evolution of Payments The payments industry has evolved extensively

Intelligent Payment Management for Today and Tomorrow Technology Advancement to Navigate the Converging Payments Landscape Adapting to the Evolution of Payments The payments industry has evolved extensively

Shareel Whitepaper V.1.2

Shareel Whitepaper V.1.2 Table of content 1. Introduction 2. Why Invest in Shareel? 3. Shareel Investment Opportunities Social Media Syndication Lending To Miners Mining (Proof-of-Stake) 4. Trading 5.

Shareel Whitepaper V.1.2 Table of content 1. Introduction 2. Why Invest in Shareel? 3. Shareel Investment Opportunities Social Media Syndication Lending To Miners Mining (Proof-of-Stake) 4. Trading 5.

ProfytPro ICO CONTENTS

1 ProfytPro ICO CONTENTS ProfytPro ICO CONTENTS... 2 INTRODUCTION... 4 WHAT IS ProfytPro (PFTC) PLATFORM... 5 CORE OBJECTIVES... 6 ADVANTAGES OF BLOCKCHAIN... 7 WHY WE DO TOKEN SALE... 8 TOKEN FUNCTIONS

1 ProfytPro ICO CONTENTS ProfytPro ICO CONTENTS... 2 INTRODUCTION... 4 WHAT IS ProfytPro (PFTC) PLATFORM... 5 CORE OBJECTIVES... 6 ADVANTAGES OF BLOCKCHAIN... 7 WHY WE DO TOKEN SALE... 8 TOKEN FUNCTIONS

Measuring for Success: Redirect Your KPI s

Measuring for Success: Redirect Your KPI s CUNA Technology Council David Potterton, Research Director September, 2014 Changing Banking Models Hitting the Mainstream My own mother even pays bills on her

Measuring for Success: Redirect Your KPI s CUNA Technology Council David Potterton, Research Director September, 2014 Changing Banking Models Hitting the Mainstream My own mother even pays bills on her

Re-imagining Personal Banking Driving Behavioral Change via Mobile. Mohamed Khalil Director of Product, Data & Partnerships

Re-imagining Personal Banking Driving Behavioral Change via Mobile Mohamed Khalil Director of Product, Data & Partnerships mo@moven.com Technology Impacts Behaviors DATA Storage Retrieval Transmission

Re-imagining Personal Banking Driving Behavioral Change via Mobile Mohamed Khalil Director of Product, Data & Partnerships mo@moven.com Technology Impacts Behaviors DATA Storage Retrieval Transmission

New Role as Manager of the Customer Experience. Digital Business Models in the Service Sector

Digital Business Models in the Service Sector New Role as Manager of the Customer Experience Service companies must reposition themselves in the digital world. Their central focus needs to be on customer

Digital Business Models in the Service Sector New Role as Manager of the Customer Experience Service companies must reposition themselves in the digital world. Their central focus needs to be on customer

Moving From Shared Services to GBS What Does World-class Look Like?

Moving From Shared Services to GBS What Does World-class Look Like? Penny Weller, PhD, CMA The Hackett Group Moving From Shared Services to GBS What Does World-class Look Like? Shared Services is a successful,

Moving From Shared Services to GBS What Does World-class Look Like? Penny Weller, PhD, CMA The Hackett Group Moving From Shared Services to GBS What Does World-class Look Like? Shared Services is a successful,

2013 AFP Electronic Payments Survey

lllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllll 2013 AFP Electronic Payments Survey Introduction and Key Findings Underwritten by 2013 AFP

lllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllll 2013 AFP Electronic Payments Survey Introduction and Key Findings Underwritten by 2013 AFP

FinTech: Enabling & Disrupting Finance

FinTech: Enabling & Disrupting Finance This course is presented in London on: 3 April 2019 If you have 4 or more participants, it may be cost effective to have this course presented in-house either on

FinTech: Enabling & Disrupting Finance This course is presented in London on: 3 April 2019 If you have 4 or more participants, it may be cost effective to have this course presented in-house either on

Channel Surfing. How Technology is Changing Member Behavior. Chris Fleischer Harland Financial Solutions

Channel Surfing How Technology is Changing Member Behavior Chris Fleischer Harland Financial Solutions 2 What Has Become of Our Channels? Question? How many here have a branch? How many here have a transactional

Channel Surfing How Technology is Changing Member Behavior Chris Fleischer Harland Financial Solutions 2 What Has Become of Our Channels? Question? How many here have a branch? How many here have a transactional

PEOPLE WATCH MONEY, MONEY, MONEY JUNE 2018 PEOPLE WATCH

MONEY, MONEY, MONEY JUNE 2018 FINANCE TRENDS IN 2018 As technology is incorporated even more so into and finance industries are being impacted, and at a rapid pace. lives, the banking The Internet of Things,

MONEY, MONEY, MONEY JUNE 2018 FINANCE TRENDS IN 2018 As technology is incorporated even more so into and finance industries are being impacted, and at a rapid pace. lives, the banking The Internet of Things,

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments Abstract FSMN is a cryptography-based digital coin and payment gateway introduced to the market in 2018 to

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments Abstract FSMN is a cryptography-based digital coin and payment gateway introduced to the market in 2018 to

WHITE PAPER COMING OF AGE

WHITE PAPER COMING OF AGE Credit Unions Must Position Themselves Now to Compete in Today s Tech Landscape CONTENTS Executive summary 3 01 Navigating the Credit Union Landscape for Change 4 02 Where the

WHITE PAPER COMING OF AGE Credit Unions Must Position Themselves Now to Compete in Today s Tech Landscape CONTENTS Executive summary 3 01 Navigating the Credit Union Landscape for Change 4 02 Where the

Navigating Payments October 2014

Navigating Payments October 2014 Presented by: Debbie Smart, CTP, NCP SVP, Product Management Aptys Solutions Eric Dotson, NCP EVP, Sales Aptys Solutions Agenda Introductions Mobile market trends Customers:

Navigating Payments October 2014 Presented by: Debbie Smart, CTP, NCP SVP, Product Management Aptys Solutions Eric Dotson, NCP EVP, Sales Aptys Solutions Agenda Introductions Mobile market trends Customers:

Continuous customer dialogues

Infor CRM Continuous customer dialogues Strategies for growth and loyalty in multi-channel customer-oriented organizations Table of contents Overview... 3 The continuous customer dialogue vision... 4 Create

Infor CRM Continuous customer dialogues Strategies for growth and loyalty in multi-channel customer-oriented organizations Table of contents Overview... 3 The continuous customer dialogue vision... 4 Create

ATTORNEY AT LAW DIGITAL ASSET PLAN

K KENT W.KEATING ATTORNEY AT LAW DIGITAL ASSET PLAN Recent Survey - 63% of people don t know what will happen to their digital assets when they die. The information, documents and applications have value

K KENT W.KEATING ATTORNEY AT LAW DIGITAL ASSET PLAN Recent Survey - 63% of people don t know what will happen to their digital assets when they die. The information, documents and applications have value

Evolving Our Differentiated Model: Community Banking Commercial David Weaver President, Community Banking. Investor Day 2018

Evolving Our Differentiated Model: Community Banking Commercial David Weaver President, Community Banking Investor Day 2018 Key Takeaways 1Operating a premier model for Commercial Banking with key differentiation

Evolving Our Differentiated Model: Community Banking Commercial David Weaver President, Community Banking Investor Day 2018 Key Takeaways 1Operating a premier model for Commercial Banking with key differentiation

Shifting to Customer-Centric Product Determination and Pricing Optimization

WHITE PAPER Shifting to Customer- Product Determination and Pricing Optimization Is Traditional Segmentation Still a Competitive Advantage? Marvin W. Foest VP Retail and Commercial Banking Solution Architecture

WHITE PAPER Shifting to Customer- Product Determination and Pricing Optimization Is Traditional Segmentation Still a Competitive Advantage? Marvin W. Foest VP Retail and Commercial Banking Solution Architecture

Can Amazon Take Customer Loyalty to the Bank?

Amazon is crushing traditional banks on loyalty scores. The challenge for banks: become more simple and digital. By Gerard du Toit and Aaron Cheris Gerard du Toit is a partner with Bain & Company s Financial

Amazon is crushing traditional banks on loyalty scores. The challenge for banks: become more simple and digital. By Gerard du Toit and Aaron Cheris Gerard du Toit is a partner with Bain & Company s Financial

Prepaid Cards and the Financially Struggling Majority. Member Exclusive Report from CFSI s Consumer Financial Health Study

Prepaid Cards and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate

Prepaid Cards and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate

Veterinarians Rely on Pacific Continental Bank

Veterinarians Rely on Pacific Continental Bank Just as veterinarians are committed to their patients welfare, Pacific Continental is committed to the financial health of veterinary clinics. We understand

Veterinarians Rely on Pacific Continental Bank Just as veterinarians are committed to their patients welfare, Pacific Continental is committed to the financial health of veterinary clinics. We understand

OUR STORY. This one innovation opened the door for the entire prepaid industry.

OUR STORY In 1992, Brooks Smith, founder and CEO, developed point-of-sale activation (POSA) technology, an innovation that allows retailers to activate products like gift cards at the register. This one

OUR STORY In 1992, Brooks Smith, founder and CEO, developed point-of-sale activation (POSA) technology, an innovation that allows retailers to activate products like gift cards at the register. This one