Chapter 11. Monopoly

|

|

|

- Janis Davidson

- 6 years ago

- Views:

Transcription

1 Chapter 11 Monopoly

2 Topics Monopoly Profit Maximization. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions That Create Monopolies. Government Actions That Reduce Market Power. Monopoly Decisions over Time and Behavioral Economics Copyright 2012 Pearson Addison-Wesley. All rights reserved.

3 Monopoly Profit Maximization Monopoly the only supplier of a good for which there is no close substitute. A monopoly can set its price not a price taker. Maximizes profits by setting marginal revenue equal to marginal cost Copyright 2012 Pearson Addison-Wesley. All rights reserved.

4 Marginal Revenue and Price A firm s revenue is: R = pq. A firm s marginal revenue, MR, is: the change in its revenue from selling one more unit. MR = ΔR/Δq. w If the firm sells exactly one more unit, Δq = 1, its marginal revenue is MR = ΔR Copyright 2012 Pearson Addison-Wesley. All rights reserved.

5 Marginal Revenue and Price (cont.) The marginal revenue of a monopoly differs from that of a competitive firm because the monopoly faces a downwardsloping demand curve unlike the competitive firm. Thus, the monopoly s marginal revenue curve lies below the demand curve at every positive quantity Copyright 2012 Pearson Addison-Wesley. All rights reserved.

Competiti v e Fi r m (b) Monopoly P r ic e, p, $ per unit p 1 Demand cu r v e P r ic e, p, $ per unit p 1 C p 2 Demand cu r v")

6 Figure 11.1 Average and Marginal Revenue (a) Competiti v e Fi r m (b) Monopoly P r ic e, p, $ per unit p 1 Demand cu r v e P r ic e, p, $ per unit p 1 C p 2 Demand cu r v e A B A B q q + 1 Quantit y, q, Units per y ear Q Q + 1 Quantit y, Q, Units per y ear 11-6 Copyright 2012 Pearson Addison-Wesley. All rights reserved.

7 Deriving the Marginal Revenue Curve For a monopoly to increase its output by ΔQ, the monopoly lowers its price per unit by Δp/ΔQ, w the slope of the demand curve. By lowering its price, the monopoly loses: (Δp/ΔQ) x Q w on the Q units it originally sold at the higher price, w but it earns an additional p on the extra output it now sells Copyright 2012 Pearson Addison-Wesley. All rights reserved.

8 Deriving the Marginal Revenue Curve (cont.) Thus, the monopoly s marginal revenue is: MR = p + Δp ΔQ Q 11-8 Copyright 2012 Pearson Addison-Wesley. All rights reserved.

9 Solved Problem 11.1 Derive the marginal revenue curve when the monopoly faces the linear inverse demand function, p=24 Q, in Figure How does the slope of the marginal revenue curve compare to the slope of the inverse demand curve? 11-9 Copyright 2012 Pearson Addison-Wesley. All rights reserved.

10 Solved Problem 11.1 p = 24 Q MR = p + Δp ΔQ Q = (24 Q) + ( 1) Q = 24 2Q The slope of this marginal revenue curve is ΔMR/ΔQ = 2, w so the marginal revenue curve is twice as steeply sloped as is the demand curve Copyright 2012 Pearson Addison-Wesley. All rights reserved.

11 Marginal Revenue and Price Elasticity of Demand At a given quantity, 1 MR = p 1 + ε Marginal revenue is closer to price as demand becomes more elastic. Where the demand curve hits the price axis (Q = 0), the demand curve is perfectly elastic, so the marginal revenue equals price: MR = p. Where the demand elasticity is unitary, ε = 1, marginal revenue is zero: MR = p[1 + 1/( 1)] = 0. Marginal revenue is negative where the demand curve is inelastic, 1 < ε Copyright 2012 Pearson Addison-Wesley. All rights reserved.

12 Figure 11.2 Elasticity of Demand and Total, Average, and Marginal Revenue p, $ per unit 24 P er f ectly elastic Elasti c, e < 1 12 DMR = 2 DQ = 1 Dp = 1 DQ = 1 e = 1 Inelasti c, 1 < e < 0 Demand ( p = 24 Q ) P er f ectly inelastic MR = 24 2 Q Q, Units per d a y Copyright 2012 Pearson Addison-Wesley. All rights reserved.

13 Table 11.1 Quantity, Price, Marginal Revenue, and Elasticity for the Linear Inverse Demand Curve p = 24 - Q Copyright 2012 Pearson Addison-Wesley. All rights reserved.

14 Choosing Price or Quantity Any firm maximizes its profit by setting its marginal revenue equal to its marginal cost. Unlike a competitive firm, a monopoly can adjust its price it has a choice of setting its price or its quantity to maximize its profit. The monopoly is constrained by the market demand curve. Because the demand curve slopes downward, the monopoly faces a trade-off between a higher price and a lower quantity or a lower price and a higher quantity Copyright 2012 Pearson Addison-Wesley. All rights reserved.

15 Figure 11.3 Maximizing Profit Copyright 2012 Pearson Addison-Wesley. All rights reserved.

16 Profit-Maximizing Output Because a linear demand curve is more elastic at smaller quantities, w monopoly profit is maximized in the elastic portion of the demand curve. Equivalently, a monopoly never operates in the inelastic portion of its demand curve Copyright 2012 Pearson Addison-Wesley. All rights reserved.

17 Mathematical Approach The monopoly faces a short-run cost function of: C(Q) = Q w where Q 2 is the monopoly s variable cost as a function of output and $12 is its fixed cost. Given this cost function the monopoly s marginal cost function is MC = 2Q Copyright 2012 Pearson Addison-Wesley. All rights reserved.

18 Mathematical Approach (cont.) The average variable cost is: AVC = Q 2 /Q = Q, w so it is a straight line through the origin with a slope of Copyright 2012 Pearson Addison-Wesley. All rights reserved.

19 Mathematical Approach (cont.) We determine the profit-maximizing output by: MR = 24 2Q = 2Q = MC. Solving for Q, we find that Q = 6. Substituting Q = 6 into the inverse demand function: p = 24 Q = 24 6 = $ Copyright 2012 Pearson Addison-Wesley. All rights reserved.

20 Mathematical Approach (cont.) At that quantity, AVC = $6, w which is less than the price, so the firm does not shut down. w The average cost is AC = $(6 + 12/6) = $8, which is less than the price, so the firm makes a profit Copyright 2012 Pearson Addison-Wesley. All rights reserved.

21 Solved Problem 11.2 We now address the first question in the Challenge at the beginning of the chapter: How did Apple set the price of the ipod when the player was first introduced and Apple had a virtual monopoly? Initially, Apple s constant marginal cost of producing its top-of-the-line ipod was $200, its fixed cost was $736 million, and its inverse demand function was p = Q where Q is millions of ipods per year. What was Apple s average cost function? Assuming that Apple was maximizing short-run monopoly profit, what was its marginal revenue function? What were its profit-maximizing price and quantity and what was its profit? Show Apple s profit-maximizing solution in a figure Copyright 2012 Pearson Addison-Wesley. All rights reserved.

22 11-22 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Solved Problem 11.2

23 Effects of a Shift of the Demand Curve Unlike a competitive firm, a monopoly does not have a supply curve. A given quantity can correspond to more than one monopoly-optimal price. w A shift in the demand curve may cause the monopoly optimal price to stay constant and the quantity to change or both price and quantity to change Copyright 2012 Pearson Addison-Wesley. All rights reserved.

24 Figure 11.4 Effects of a Shift of the Demand Curve Copyright 2012 Pearson Addison-Wesley. All rights reserved.

25 Market Power Market power - the ability of a firm to charge a price above marginal cost and earn a positive profit. MR p 1 = 1 + = ε w and rearranging the terms: p MC 1 = 1+ (1/ ε ) MC w so the ratio of the price to marginal cost depends only on the elasticity of demand at the profit-maximizing quantity Copyright 2012 Pearson Addison-Wesley. All rights reserved.

26 Table 11.2 Elasticity of Demand, Price, and Marginal Cost Copyright 2012 Pearson Addison-Wesley. All rights reserved.

27 Lerner Index Lerner Index - the ratio of the difference between price and marginal cost to the price: (p MC)/p. w In terms of the elasticity of demand: p MC p 1 = ε w Because MC 0 and p MC, 0 p MC p, so the Lerner Index ranges from 0 to 1 for a profitmaximizing firm Copyright 2012 Pearson Addison-Wesley. All rights reserved.

28 Application: Apple s Lerner Index Apple s marginal cost for ipod Shuffle was $21.77, $ for a 16GB iphone 4, and $ for a non-3g 16GB ipad. These products retailed for $79, $600, and $499 respectively. Thus, Apple s Lerner indexes are ( )/ , ( )/600.69, and ( )/ Copyright 2012 Pearson Addison-Wesley. All rights reserved.

29 Solved Problem 11.3 If Apple is producing at the short-run profit-maximizing level, what is the elasticity of demand for the ipod, iphone 4, and ipad discussed in the previous application, Apple s Lerner Indexes? Answer w Determine the Lerner Index using Equation Copyright 2012 Pearson Addison-Wesley. All rights reserved.

30 Sources of Market Power All else the same, the demand curve a firm faces becomes more elastic as: 1. better substitutes for the firm s product are introduced, 2. more firms enter the market selling the same product, or 3. firms that provide the same service locate closer to this firm Copyright 2012 Pearson Addison-Wesley. All rights reserved.

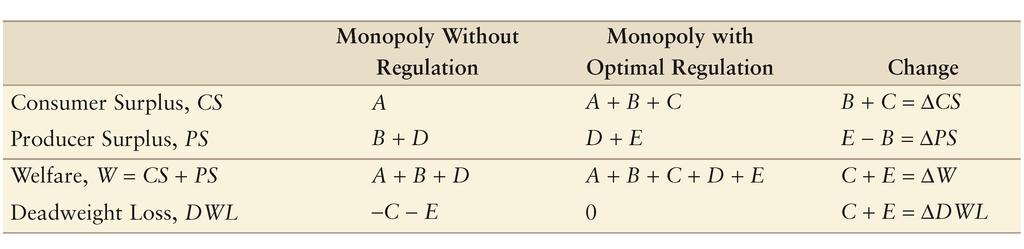

31 Welfare Effects of a Monopoly Welfare, W, is lower under monopoly than under competition. Competition maximizes welfare because price equals marginal cost. By setting its price above its marginal cost, a monopoly causes consumers to buy less than the competitive level of the good, so a deadweight loss to society occurs Copyright 2012 Pearson Addison-Wesley. All rights reserved.

32 Figure 11.5 Deadweight Loss of Monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

33 Solved Problem 11.4 In the linear example in Figure 11.3, how does charging the monopoly a specific tax of τ = $8 per unit affect the monopoly optimum and the welfare of consumers, the monopoly, and society (where society s welfare includes the tax revenue)? What is the incidence of the tax on consumers? Copyright 2012 Pearson Addison-Wesley. All rights reserved.

34 11-34 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Solved Problem 11.4

35 Cost Advantages That Create Monopolies Why are some markets monopolized? w A firm has a cost advantage over other firms or w A government created the monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

36 Sources of Cost Advantages Reasons for cost advantages: w the firm controls an essential facility: a scarce resource that a rival needs to use to survive. w the firm uses a superior technology or has a better way of organizing production Copyright 2012 Pearson Addison-Wesley. All rights reserved.

37 Natural Monopoly Natural monopoly - situation in which one firm can produce the total output of the market at lower cost than several firms could. Believing that they are natural monopolies, governments frequently grant monopoly rights to public utilities to provide essential goods or services such as water, gas, electric power, or mail delivery Copyright 2012 Pearson Addison-Wesley. All rights reserved.

38 Natural Monopoly (cont.) If the cost for any firm to produce q is C(q), the condition for a natural monopoly is where Q=q 1 +q 2 + +q n is the sum of the output of any n 2 firms Copyright 2012 Pearson Addison-Wesley. All rights reserved.

39 Figure 11.6 Natural Monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

40 Solved Problem 11.5 A firm that delivers Q units of water to households has a total cost of C(Q) = mq + F. If any entrant would have the same cost, does this market have a natural monopoly? Answer w Determine whether costs rise if two firms produce a given quantity Copyright 2012 Pearson Addison-Wesley. All rights reserved.

41 Government Actions That Create Monopolies Governments create many monopolies. w Sometimes governments own and manage monopolies. w In the United States, as in most countries, the postal service is a government monopoly. Frequently, however, governments create monopolies by preventing competing firms from entering a market Copyright 2012 Pearson Addison-Wesley. All rights reserved.

42 Barriers to Entry Governments create monopolies in one of three ways: 1. by making it difficult for new firms to obtain a license to operate, 2. by granting a firm the rights to be a monopoly, or 3. by auctioning the rights to be monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

43 Patents Patent - an exclusive right granted to the inventor to sell a new and useful product, process, substance, or design for a fixed period of time. w The length of a patent varies across countries. Question: If a firm with a patent monopoly sets a high price that results in deadweight loss then why do governments grant patent monopolies? Copyright 2012 Pearson Addison-Wesley. All rights reserved.

44 Application: Botox Patent Monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

45 Optimal Price Regulation In some markets, the government can eliminate the deadweight loss of monopoly by requiring that a monopoly charge no more than the competitive price Copyright 2012 Pearson Addison-Wesley. All rights reserved.

46 Figure 11.7 Optimal Price Regulation Copyright 2012 Pearson Addison-Wesley. All rights reserved.

47 Solved Problem 11.6 Suppose that the government sets a price, p 2, that is below the socially optimal level, p 1, but above the monopoly s minimum average cost. How do the price, the quantity sold, the quantity demanded, and welfare under this regulation compare to those under optimal regulation? Copyright 2012 Pearson Addison-Wesley. All rights reserved.

48 11-48 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Solved Problem 11.6

49 Problems in Regulating Problems that governments face in regulating monopolies: w because they do not know the actual demand and marginal cost curves, governments may set the price at the wrong level. w Second, many governments use regulations that are less efficient than price regulation. w Third, regulated firms may bribe or otherwise influence government regulators to help the firms rather than society as a whole Copyright 2012 Pearson Addison-Wesley. All rights reserved.

50 Nonoptimal Price Regulation If the regulated price is not optimal, a deadweight loss results. If the price is set below the firm s minimum average cost, the firm will shut down Copyright 2012 Pearson Addison-Wesley. All rights reserved.

51 Application: Natural Gas Regulation Copyright 2012 Pearson Addison-Wesley. All rights reserved.

52 Increasing Competition Encouraging competition is an alternative to regulation as a means of reducing the harms of monopoly Copyright 2012 Pearson Addison-Wesley. All rights reserved.

53 Monopoly Decisions over Time and Behavioral Economics In some markets decisions today affect demand or cost in a future period. In such markets the monopoly may maximize its long-run profit by making a decision today that does not maximize its short-run profit Copyright 2012 Pearson Addison-Wesley. All rights reserved.

54 Network Externalities Network externality - the situation where one person s demand for a good depends on the consumption of the good by others Copyright 2012 Pearson Addison-Wesley. All rights reserved.

55 Direct Size Effect Many industries exhibit positive network externalities where the customer gets a direct benefit from a larger network. w Example: the larger an ATM network such as the Plus network Copyright 2012 Pearson Addison-Wesley. All rights reserved.

56 Behavioral Economics Bandwagon effect - the situation in which a person places greater value on a good as more and more other people possess it. Snob effect - the situation in which a person places greater value on a good as fewer and fewer other people possess it Copyright 2012 Pearson Addison-Wesley. All rights reserved.

57 Indirect Size Effect In some markets, positive network externalities are indirect. They stem from complementary goods that are offered when a product has a critical mass of users. w The more applications (apps) available for a smart phone, the more people want to buy that smart phone; however, many of these extra apps will be written only if a critical mass of customers buys the smart phone Copyright 2012 Pearson Addison-Wesley. All rights reserved.

58 A Two-Period Monopoly Model A monopoly may be able to solve the chicken-and-egg problem of getting a critical mass for its product by initially selling the product at a low introductory price. By doing so, the firm maximizes its longrun profit but not its short-run profit Copyright 2012 Pearson Addison-Wesley. All rights reserved.

59 A Two Period Monopoly Model (cont.) Suppose that a monopoly sells its good only two periods. If the monopoly sells less than a critical quantity of output, Q, in the first period, its second-period demand curve lies close to the price axis. However, if the good is a success in the first period at least Q units are sold the second-period demand curve shifts substantially to the right Copyright 2012 Pearson Addison-Wesley. All rights reserved.

60 A Two Period Monopoly Model (cont.) Should the monopoly charge a low introductory price in the first period? The firm chooses to charge a low introductory period in the first period if its first period loss (from charging a less than optimal price) is less than its extra profit in the second period Copyright 2012 Pearson Addison-Wesley. All rights reserved.

61 Figure 11.8 Effects of High-Cost Competition Copyright 2012 Pearson Addison-Wesley. All rights reserved.

Chapter Eleven. Monopoly

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Chapter Eleven. Topics. Marginal Revenue and Price. A firm s revenue is:

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

11.1 Monopoly Profit Maximization

11.1 Monopoly Profit Maximization CHAPTER 11 MONOPOLY A monopoly is the only supplier of a good for which there is no close substitute. Monopolies are not price takers like competitive firms Monopoly output

11.1 Monopoly Profit Maximization CHAPTER 11 MONOPOLY A monopoly is the only supplier of a good for which there is no close substitute. Monopolies are not price takers like competitive firms Monopoly output

Chapter 11. Monopoly. I think it s wrong that only one company makes the game Monopoly. Steven Wright

Chapter 11 Monopoly I think it s wrong that only one company makes the game Monopoly. Steven Wright Chapter 11 Outline 11.1 Monopoly Profit Maximization 11.2 Market Power 11.3 Welfare Effects of Monopoly

Chapter 11 Monopoly I think it s wrong that only one company makes the game Monopoly. Steven Wright Chapter 11 Outline 11.1 Monopoly Profit Maximization 11.2 Market Power 11.3 Welfare Effects of Monopoly

Introduction. Managerial Problem. Solution Approach

Monopoly Introduction Managerial Problem Drug firms have patents that expire after 20 years and one expects drug prices to fall once generic drugs enter the market. However, as evidence shows, often prices

Monopoly Introduction Managerial Problem Drug firms have patents that expire after 20 years and one expects drug prices to fall once generic drugs enter the market. However, as evidence shows, often prices

Chapter 8. Competitive Firms and Markets

Chapter 8 Competitive Firms and Markets Topics Perfect Competition. Profit Maximization. Competition in the Short Run. Competition in the Long Run. 8-2 Copyright 2012 Pearson Addison-Wesley. All rights

Chapter 8 Competitive Firms and Markets Topics Perfect Competition. Profit Maximization. Competition in the Short Run. Competition in the Long Run. 8-2 Copyright 2012 Pearson Addison-Wesley. All rights

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

Monopoly and How It Arises

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

Deadweight Loss of Monopoly

Monopoly (part 2) Deadweight Loss of Monopoly Market Failure: non-optimal allocation of goods & services with economic inefficiencies (price is not marginal cost) A monopoly sets p > MC causing consumers

Monopoly (part 2) Deadweight Loss of Monopoly Market Failure: non-optimal allocation of goods & services with economic inefficiencies (price is not marginal cost) A monopoly sets p > MC causing consumers

Unit 6 Perfect Competition and Monopoly - Practice Problems

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Unit 7. Firm behaviour and market structure: monopoly

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Eco 300 Intermediate Micro

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

ECN 3103 INDUSTRIAL ORGANISATION

ECN 3103 INDUSTRIAL ORGANISATION 3. Monopoly Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Monopoly Reference for reviewing these concepts: Carlton, Perloff, Modern

ECN 3103 INDUSTRIAL ORGANISATION 3. Monopoly Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Monopoly Reference for reviewing these concepts: Carlton, Perloff, Modern

Monopolistic Markets. Causes of Monopolies

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

These notes essentially correspond to chapter 11 of the text.

These notes essentially correspond to chapter 11 of the text. 1 Monopoly A monopolist is de ned as a single seller of a well-de ned product for which there are no close substitutes. In reality, there are

These notes essentially correspond to chapter 11 of the text. 1 Monopoly A monopolist is de ned as a single seller of a well-de ned product for which there are no close substitutes. In reality, there are

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Pricing Under Homogeneous Oligopoly We will assume that the

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Pricing Under Homogeneous Oligopoly We will assume that the

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Monopoly. Cost. Average total cost. Quantity of Output

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 11 Perfect Competition

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

ECON 2100 Principles of Microeconomics (Summer 2016) Monopoly

Monopoly") ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

Lecture 12. Monopoly

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly and Market Power. Session V Sep 18, 2010

Monopoly and Market Power. Session V Sep 18, 2010") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly and Market Power Session V Sep 18, 2010 Monopoly In contrast to perfect competition, a monopoly is a market

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly and Market Power Session V Sep 18, 2010 Monopoly In contrast to perfect competition, a monopoly is a market

Monopoly. Chapter 15

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

ECON 2100 (Summer 2012 Sections 07 and 08) Exam #3C Answer Key

Exam #3C Answer Key") ECON 21 (Summer 212 Sections 7 and 8) Exam #3C Answer Key Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller

ECON 21 (Summer 212 Sections 7 and 8) Exam #3C Answer Key Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller

2-1 Copyright 2012 Pearson Education. All rights reserved.

2-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 2 Read this chapter together with unit 1 and 2 in the study guide Supply and Demand Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

2-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 2 Read this chapter together with unit 1 and 2 in the study guide Supply and Demand Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

Monopoly. While a competitive firm is a price taker, a monopoly firm is a price maker.

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

Introduction. Learning Objectives. Learning Objectives. Economics Today Twelfth Edition. Chapter 24 Monopoly

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 24 Monopoly Introduction The cement market in Mexico is dominated by a single company that accounts for more than 70 percent of all sales. Why

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 24 Monopoly Introduction The cement market in Mexico is dominated by a single company that accounts for more than 70 percent of all sales. Why

iv. The monopolist will receive economic profits as long as price is greater than the average total cost

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

CH 14. Name: Class: Date: Multiple Choice Identify the choice that best completes the statement or answers the question.

Class: Date: CH 14 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. We define a monopoly as a market with a. one supplier and no barriers to entry. b. one

Class: Date: CH 14 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. We define a monopoly as a market with a. one supplier and no barriers to entry. b. one

Monopolistic Markets. Regulation

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

Micro Monopoly Essentials 1 WCC

Micro Monopoly Essentials 1 WCC As we've said before, perfect competition is the benchmark against which we will judge all other market structures. It is ideal in the sense that it achieves productive

Micro Monopoly Essentials 1 WCC As we've said before, perfect competition is the benchmark against which we will judge all other market structures. It is ideal in the sense that it achieves productive

The Four Main Market Structures

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Chapter 13 MODELS OF MONOPOLY. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

Quiz #5 Week 04/12/2009 to 04/18/2009

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Ecn Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman Final Exam You have until 5:30pm to complete the exam, be certain to use your time wisely.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis March 19, 2009 Instructor: John Parman Final Exam You have until 5:30pm to complete the exam, be certain to use your time wisely.

Economics 323 Microeconomic Theory Fall 2016

green=b SECOND EXAM Chapter Ten Economics 323 Microeconomic Theory Fall 2016 1. The markets for many come close to satisfying the conditions required for perfect competition. a. agricultural goods b. transportation

green=b SECOND EXAM Chapter Ten Economics 323 Microeconomic Theory Fall 2016 1. The markets for many come close to satisfying the conditions required for perfect competition. a. agricultural goods b. transportation

Oligopoly and Monopolistic Competition

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

All but which of the following are true in the long-run for a competitive firm that maximizes profits?

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Question 11.1: Profit Maximization: Monopoly Which of the following is true in

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Question 11.1: Profit Maximization: Monopoly Which of the following is true in

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman Final Examination You have until 12:30pm to complete the exam, be certain to use your

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman Final Examination You have until 12:30pm to complete the exam, be certain to use your

VIII 1 TOPIC VIII: MONOPOLY AND OTHER INDUSTRY STRUCTURES. I. Monopoly - Single Firm With No Threat of Close Competition. Other Industry Structures

TOPIC VIII: MONOPOLY AND OTHER INDUSTRY STRUCTURES I. Monopoly - Single Firm With No Threat of Close Competition II. Other Industry Structures CONCEPTS AND PRINCIPLES MONOPOLY We now consider the opposite

TOPIC VIII: MONOPOLY AND OTHER INDUSTRY STRUCTURES I. Monopoly - Single Firm With No Threat of Close Competition II. Other Industry Structures CONCEPTS AND PRINCIPLES MONOPOLY We now consider the opposite

Chapter 10 Pure Monopoly

Chapter 10 Pure Monopoly Multiple Choice Questions 1. Pure monopoly means: A. any market in which the demand curve to the firm is downsloping. B. a standardized product being produced by many firms. C.

Chapter 10 Pure Monopoly Multiple Choice Questions 1. Pure monopoly means: A. any market in which the demand curve to the firm is downsloping. B. a standardized product being produced by many firms. C.

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

Chapter 2. Supply and Demand

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

At P = $120, Q = 1,000, and marginal revenue is ,000 = $100

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!

ECON 101: Principles of Microeconomics Discussion Section Week 12 TA: Kanit Kuevibulvanich

Important Concepts: Monopoly ECON 101: Principles of Microeconomics Discussion Section Week 12 Comparison of Perfectly Competitive Market and Monopoly Market Perfect Competition Monopoly Number of Participants

Important Concepts: Monopoly ECON 101: Principles of Microeconomics Discussion Section Week 12 Comparison of Perfectly Competitive Market and Monopoly Market Perfect Competition Monopoly Number of Participants

Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting

Economics 6 th edition 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall

Economics 6 th edition 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall

MICROECONOMIC FOUNDATIONS OF COST-BENEFIT ANALYSIS. Townley, Chapter 4

MICROECONOMIC FOUNDATIONS OF COST-BENEFIT ANALYSIS Townley, Chapter 4 Review of Basic Microeconomics Slides cover the following topics from textbook: Input markets. Decision making on the margin. Pricing

MICROECONOMIC FOUNDATIONS OF COST-BENEFIT ANALYSIS Townley, Chapter 4 Review of Basic Microeconomics Slides cover the following topics from textbook: Input markets. Decision making on the margin. Pricing

Monopoly. Basic Economics Chapter 15. Why Monopolies Arise. Monopoly

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman Final Examination You have until 12:30pm to complete the exam, be certain to use your

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2008 Professor John Parman Final Examination You have until 12:30pm to complete the exam, be certain to use your

Monopoly CHAPTER 15. Henry Demarest Lloyd. Monopoly is business at the end of its journey. Monopoly 15. McGraw-Hill/Irwin

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

Econ Microeconomics Notes

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

CH 15: Monopoly. Lecture

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

ECON 200. Introduction to Microeconomics

ECON 200. Introduction to Microeconomics Homework 5 Part II Name: [Multiple Choice] 1. A firm is a natural monopoly if it exhibits the following as its output increases: (d) a. decreasing marginal revenue

ECON 200. Introduction to Microeconomics Homework 5 Part II Name: [Multiple Choice] 1. A firm is a natural monopoly if it exhibits the following as its output increases: (d) a. decreasing marginal revenue

Chapter 3. Applying the Supply-and- Demand Model

Chapter 3 Applying the Supply-and- Demand Model Reading Assignment for Week: Finish Chapter 3 Chapter 9 (sections 9.2, 9.3, 9.4) Chapter 13 (first few pages through section 13.1) 3-2 Topic How the shapes

Chapter 3 Applying the Supply-and- Demand Model Reading Assignment for Week: Finish Chapter 3 Chapter 9 (sections 9.2, 9.3, 9.4) Chapter 13 (first few pages through section 13.1) 3-2 Topic How the shapes

COMM 295 MIDTERM REVIEW SESSION BY WENDY ZHANG

COMM 295 MIDTERM REVIEW SESSION BY WENDY ZHANG TABLE OF CONTENT I. Introduction, Supply and Demand, Elasticity II. Estimation III. Profit Maximization IV. Competition, Consumer and Producer Surpluses V.

COMM 295 MIDTERM REVIEW SESSION BY WENDY ZHANG TABLE OF CONTENT I. Introduction, Supply and Demand, Elasticity II. Estimation III. Profit Maximization IV. Competition, Consumer and Producer Surpluses V.

Market structures. Why Monopolies Arise. Why Monopolies Arise. Market power. Monopoly. Monopoly resources

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Lesson 3-2 Profit Maximization

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Ch. 9 LECTURE NOTES 9-1

Ch. 9 LECTURE NOTES I. Four market models will be addressed in Chapters 9-11; characteristics of the models are summarized in Table 9.1. A. Pure competition entails a large number of firms, standardized

Ch. 9 LECTURE NOTES I. Four market models will be addressed in Chapters 9-11; characteristics of the models are summarized in Table 9.1. A. Pure competition entails a large number of firms, standardized

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

- pure monopoly: only one seller of a good/service with no close substitutes

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Quiz #4 Week 04/05/2009 to 04/11/2009

Quiz #4 Week 04/05/2009 to 04/11/2009 You have 30 minutes to answer the following 15 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #4 Week 04/05/2009 to 04/11/2009 You have 30 minutes to answer the following 15 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

ECON 102 Brown Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

Coffee is produced at a constant marginal cost of $1.00 a pound. Due to a shortage of cocoa beans, the marginal cost rises to $2.00 a pound.

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 27, 2005 Question 11.1: Monopoly All but which of the following

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 27, 2005 Question 11.1: Monopoly All but which of the following

If the industry s short-run supply curve equals the horizontal sum of individual firms short-run supply curves, which of the following may we infer?

Microeconomics, Module 8: Competition: Long Run (Chapter 7) Illustrative Test Questions (The attached PDF file has better formatting.) Question 8.1: Long Run Equilibrium When is a competitive profit-maximizing

Microeconomics, Module 8: Competition: Long Run (Chapter 7) Illustrative Test Questions (The attached PDF file has better formatting.) Question 8.1: Long Run Equilibrium When is a competitive profit-maximizing

Lecture 2: Market Structure Part I (Perfect Competition and Monopoly)

") Lecture 2: Market Structure Part I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology EC 105. Industrial Organization ( Matt ShumLecture

Lecture 2: Market Structure Part I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology EC 105. Industrial Organization ( Matt ShumLecture

CHAPTER 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

CHAPTER 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets CHAPTER OUTLINE Perfect competition Demand at the market and firm levels Short-run output decisions Long-run decisions

CHAPTER 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets CHAPTER OUTLINE Perfect competition Demand at the market and firm levels Short-run output decisions Long-run decisions

Managerial Economics Prof. Trupti Mishra S. J. M School of Management Indian Institute of Technology, Bombay. Lecture - 27 Monopoly

Managerial Economics Prof. Trupti Mishra S. J. M School of Management Indian Institute of Technology, Bombay Lecture - 27 Monopoly So, we will continue our discussion on theory of perfect competition.

Managerial Economics Prof. Trupti Mishra S. J. M School of Management Indian Institute of Technology, Bombay Lecture - 27 Monopoly So, we will continue our discussion on theory of perfect competition.

Chapter 1- Introduction

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

ECON 2100 (Summer 2012 Sections 07 and 08) Exam #3A

Exam #3A") ECON 21 (Summer 212 Sections 7 and 8) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. Excess Capacity refers to the A. quantity of output at which Average

ECON 21 (Summer 212 Sections 7 and 8) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. Excess Capacity refers to the A. quantity of output at which Average

Study Guide Final Exam, Microeconomics

Study Guide Final Exam, Microeconomics 1. If the price-consumption curve of a commodity slopes downward how can you tell whether the consumer spends more or less on this commodity from her budget (income)?

Study Guide Final Exam, Microeconomics 1. If the price-consumption curve of a commodity slopes downward how can you tell whether the consumer spends more or less on this commodity from her budget (income)?

4. Which of the following statements about marginal revenue for a perfectly competitive firm is incorrect? A) TR

TR") Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Boston College Problem Set 6, Fall 2012 EC Principles of Microeconomics Instructor: Inacio G L Bo

Problem Set 6, Fall 01 EC 131 - Principles of Microeconomics Instructor: Inacio G L Bo Answer the questions in the spaces provided on the question sheets. If you run out of room for an answer, continue

Problem Set 6, Fall 01 EC 131 - Principles of Microeconomics Instructor: Inacio G L Bo Answer the questions in the spaces provided on the question sheets. If you run out of room for an answer, continue

CH 14: Perfect Competition

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

2) A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)

A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)") Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Chapter 8 Profit Maximization and Competitive Supply. Read Pindyck and Rubinfeld (2013), Chapter 8

, Chapter 8") Chapter 8 Profit Maximization and Competitive Supply Read Pindyck and Rubinfeld (2013), Chapter 8 1/29/2017 CHAPTER 8 OUTLINE 8.1 Perfectly Competitive Market 8.2 Profit Maximization 8.3 Marginal Revenue,

Chapter 8 Profit Maximization and Competitive Supply Read Pindyck and Rubinfeld (2013), Chapter 8 1/29/2017 CHAPTER 8 OUTLINE 8.1 Perfectly Competitive Market 8.2 Profit Maximization 8.3 Marginal Revenue,

a. Sells a product differentiated from that of its competitors d. produces at the minimum of average total cost in the long run

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

Ecn Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman Final Exam You have until 8pm to complete the exam, be certain to use your time wisely.

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis June 11, 2009 Instructor: John Parman Final Exam You have until 8pm to complete the exam, be certain to use your time wisely.

Ecn Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman Final Exam You have until 1:50pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis September 9, 2009 Instructor: John Parman Final Exam You have until 1:50pm to complete this exam. Be certain to put your name,

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3C

Exam #3C") ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3D

Exam #3D") ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

Monopoly CHAPTER. Goals. Outcomes

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

Textbook Media Press. CH 12 Taylor: Principles of Economics 3e 1

CH 12 Taylor: Principles of Economics 3e 1 Monopolistic Competition and Differentiated Products Monopolistic competition refers to a market where many firms sell differentiated products. Differentiated

CH 12 Taylor: Principles of Economics 3e 1 Monopolistic Competition and Differentiated Products Monopolistic competition refers to a market where many firms sell differentiated products. Differentiated

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product.

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product. This arises due to consumers indifference between the

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product. This arises due to consumers indifference between the

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

not to be republished NCERT Chapter 6 Non-competitive Markets 6.1 SIMPLE MONOPOLY IN THE COMMODITY MARKET

Chapter 6 We recall that perfect competition was theorised as a market structure where both consumers and firms were price takers. The behaviour of the firm in such circumstances was described in the Chapter

Chapter 6 We recall that perfect competition was theorised as a market structure where both consumers and firms were price takers. The behaviour of the firm in such circumstances was described in the Chapter

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013

Fall 2013") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013 Monopolistic markets and pricing with market power (PR 10.1-10.4 and 11.1-11.4) Module 4 Sep. 20, 2014

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013 Monopolistic markets and pricing with market power (PR 10.1-10.4 and 11.1-11.4) Module 4 Sep. 20, 2014

Class Agenda. Note: As you hand-in your quiz, pick-up graded HWK #1 and HWK #2 (due next Tuesday).

.") Class 7 Class Agenda 1. Finish discussion on consumer and producer surplus (welfare theory). 2. Elasticity problems (individual/group work to prep for quiz). 3. Quiz #1. Note: As you hand-in your quiz,

Class 7 Class Agenda 1. Finish discussion on consumer and producer surplus (welfare theory). 2. Elasticity problems (individual/group work to prep for quiz). 3. Quiz #1. Note: As you hand-in your quiz,

Lecture 2 OLIGOPOLY Copyright 2012 Pearson Education. All rights reserved.

Lecture 2 OLIGOPOLY 13-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 13 Topics Market Structures ( A Recap). Noncooperative Oligopoly. Cournot Model. Stackelberg Model. Bertrand Model.

Lecture 2 OLIGOPOLY 13-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 13 Topics Market Structures ( A Recap). Noncooperative Oligopoly. Cournot Model. Stackelberg Model. Bertrand Model.

Monopoly. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

Lecture 2: Market Structure I (Perfect Competition and Monopoly)

") Lecture 2: Market Structure I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology October 1, 2012 EC 105. Industrial Organization ( Matt

Lecture 2: Market Structure I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology October 1, 2012 EC 105. Industrial Organization ( Matt

Refer to the information provided in Figure 12.1 below to answer the questions that follow. Figure 12.1

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

ECON 2100 (Summer 2014 Sections 08 & 09) Exam #3D

Exam #3D") ECON 21 (Summer 214 Sections 8 & 9) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. If a firm is currently operating at a point where costs of production

ECON 21 (Summer 214 Sections 8 & 9) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. If a firm is currently operating at a point where costs of production