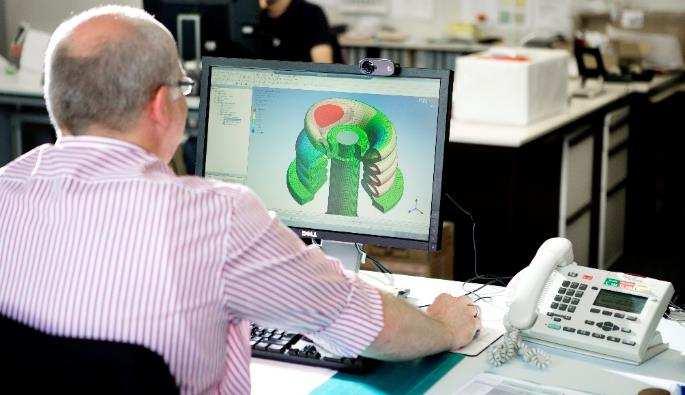

Baader Swiss Equities Conference 12 January 2018, Bad Ragaz. Reto Welte, CFO Dätwyler Group

|

|

|

- Sheryl Flynn

- 6 years ago

- Views:

Transcription

1 Baader Swiss Equities Conference 12 January 2018, Bad Ragaz Reto Welte, CFO Dätwyler Group

2 Datwyler Group Highlights Focused industrial supplier with global presence Leading positions in global and regional market segments Two divisions Sealing Solutions Technical Components Distributor and solution provider to health care, automotive, building and manufacturing industries Revenue of more than CHF 1,200 million More than 7,000 employees Established in 1915 Listed on the SIX Swiss Exchange, Zurich 2

3 Datwyler Group 100 years successful corporate history 3

4 Datwyler Group Continuity thanks to majority shareholder Directors of Dätwyler Holding Inc. representing registered shareholders (bound by a shareholders agreement) 100% Dätwyler Führungs AG The Board of Directors of the listed Dätwyler Holding Inc. holds the majority of the capital and the votes on a fiduciary basis without any beneficial ownership. 100% Free float Pema Holding AG Investments in Datwyler Companies only % of votes 43.97% of capital 78.40% of votes 56.03% of capital Dätwyler Holding Inc. 4

5 Datwyler Group Strategic focus Focus on attractive market niches Improving productivity continuously Building leading market positions Increasing value added Offer system/time critical solutions and services 5

6 Datwyler Group Half of turnover replaced, margins doubled Revenue Revenue Acquisitions Divestments EBIT margin 13.0% 12.0% 11.0% 10.0% 9.0% 8.0% 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% -1.0% -2.0% -3.0% -4.0% -5.0% EBIT margin 6

7 Datwyler Group Key Financials first half 2017 Sales growth of 3.8%, thereof 2.2% organic Adjusted EBIT-margin at 13.5% (PY 13.4%), before one-off costs of CHF 6.6 million Net result slightly lower due to higher tax expenses Net revenue (in CHF million) EBIT (in CHF million) EBIT margin in % Net result (in CHF million) % 11.6% % 12.4% H H H H H H H H H H H H

8 Datwyler Group Liquidity supports planned growth Assets CHF million Liabilities and equity CHF million Cash and cash equivalents Current liabilities Trade and other accounts receivable Inventories Equity Non-current assets 66.2% 66.9% Equity ratio

Reporting to the Carbon")

9 Datwyler Group Sustainable management approach Goal of sustainable profitable growth for the benefit of all stakeholders Balancing economic, social and environmental responsibility Code of Conduct for employees and suppliers Member of the UN Global Compact Sustainability reporting according to the standards of the Global Reporting Initiative (GRI) Reporting to the Carbon Disclosure Project 9

")

10 Datwyler Group Two focused divisions Sealing Solutions Technical Components Products Sealing systems and solutions, elastomer and aluminium/plastic closures, stoppers and plungers; precision moulded elastomer and metal components; special seals, profiles and gaskets Distribution of maintenance, automation electronic and ICT components and accessories (online distribution and branded wholesale) Markets Revenue 2016 GLOBAL Health care, automotive, civil engineering and consumer goods CHF million EUROPE Manufacturing companies, trades, retailers, resellers, universities, private consumers CHF million Employees 6,000 1,200 10

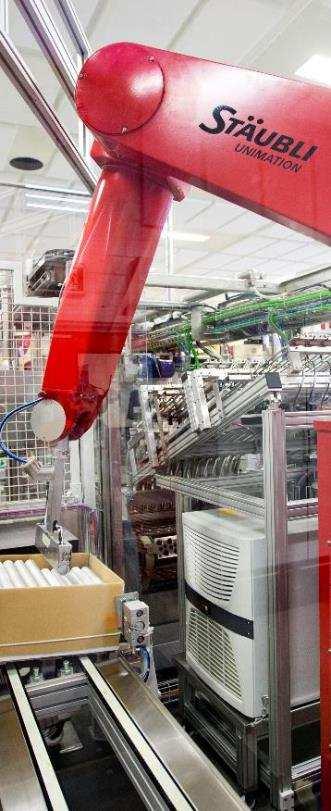

11 Sealing Solutions division 11

12 Sealing Solutions Leading positions in attractive global market segments 2 Consumer Goods CHF 250 m. CHF 1,600 m. Health Care CHF 2,400 m. High market and growth potential CHF 650 m. Automotive Civil Engineering 12

13 Sealing Solutions Health Care: growth drivers and success factors Growth drivers Ageing society in western industrial nations Increasing requirement for medicines in emerging countries Increase in chronic diseases such as diabetes and cardiovascular diseases Trend for injectable medicines and stricter regulations from the authorities Health Care sealing components: Success factors and measures Leading FirstLine production technology Expansion of FirstLine activities New offer strategy from customers' perspective Expansion of key account management Almost 50 years' experience within the industry Market potential CHF 1,600 million Market growth 5% - 7% 13

14 Sealing Solutions Example Health Care: Growth market pre-filled syringes Global market potential for pre-filled syringes in USD billions Average annual market growth of 9.7% over the next 10 years Source: VisionGain 2016 Ideal containers for biotech medicines and vaccines given the risk that properties may change during transfer from bottles to syringes Correct dose every time improves patient safety Technological developments allow higher levels of self-administration Trend for automatic administration systems (including use of WiFi / Bluetooth) Europe leading the way so far, but USA catching up Datwyler elastomer stoppers are systemcritical components Expansion of FirstLine capacities in Belgium and India New FirstLine plant in the USA from mid

15 Sealing Solutions Automotive: growth drivers and success factors Growth drivers Sophisticated, environmentally friendly technologies (e.g. SCR systems) Car ownership increasing fast in emerging countries Trend for customers to outsource engineering aspects Automotive sealing components / O-rings: Success factors and measures Own plants in the three key business regions EU, Asia and NAFTA Experience and customer relationships going back many years New mixing plants in China (since 2015) and the Czech Republic (from 2018) Tapping into new technologies and niche markets through acquisitions (Origom / Ott) Market potential CHF 2,400 million Market growth 4 % - 5% 15

16 Sealing Solutions Example Automotive: Growth market SCR system 14 Number of diesel vehicles with SCR- Systems in millions worldwide Emissions scandal and worldwide tightening of emissions regulations mean diesel emissions require additional treatment 12 Selective Catalytic Reduction (SCR) is the leading technology and the most effective Average annual market growth of 17.0% over the next 6 years Source: PwC AutoFacts 2016, internal estimates Five system-critical sealing components for the conveyor and dispensing module in each SCR system Enormous challenges in terms of geometry, tolerances, cleanliness, adhesion and resistance to high temperatures, pressure and aggressive media The two leading providers are long-standing customers Despite electrification, diesel engines will still have an important role to play in the near future 16

17 Sealing Solutions Core competences CORE COMPETENCES Materials Engineering Processes 17

18 Sealing Solutions Division first half 2017 Acceleration of profitable growth thanks to leading global positions Revenue growth of 9.7%, thereof 6.2% organic, thanks to leading positions and start of series production of new components. Higher EBIT for the fifth consecutive time since the merger of the former two divisions. EBIT-margin at 18.7%. Health Care with above market growth in high quality components for prefilled syringes. Automotive with strong revenue growth, specially in China and in Selective Catalytic Reduction applications % 17.8% % Civil Engineering significantly above prior year. Continuing growth of the Nespresso project Integration of 2016 acquired German company Ott on track. 16.6% 17.6% 18.9% 18.7% Net revenue full year in CHFm Net revenue half year in CHFm EBIT as % of net revenue 18

19 New Health Care plant in the USA on track Serve the growing needs of leading US health care companies for high qualitative components Greenfield manufacturing plant setting new industry standards Ultra-modern clean room technology and fully automated production cells Investment of more than CHF 100 million

20 Technical Components division 20

21 Technical Components Business model high service distribution Manufacturer directly Distribution Volumes EDE Electronic Design Engineers Prototyping High Service Distributor Volume Distributor MRO Maintenance Repair, Operation High Service Distributor R&D Pilot Small OEM Large OEM Service Maintenance Repair Education Prototype Small series Customer Customer needs needs - - in in the the course course of of the the product product life life cycle cycle 21

22 Technical Components Leading position in Europe with three strong brands > Customers CHF 462 m Revenue > 55% Share of ecommerce > Webshop visits per day 18 Languages of webshops and catalogues Omni-Channel Approach Ecommerce, catalogue, call center, field sales, technical support > Suppliers > Products on stock > Employees > Packages per day CHF Average order value 99% On-time delivery 22

23 Technical Components Four important market segments CHF 6 bn Estimated target market size MRO Europe high service distribution CHF 6 bn Estimated target market size Automation Europe high service distribution Maintenance, Repair, Operations Automation Focus on MRO & Automation Wholesale Consumer Electronics CHF 3 bn Estimated target market size Wholesale/ Consumer Electronics Europe CHF 3 bn Estimated target market size EDE&Production Europe high service distribution Electronic Design Engineers 23

Capex limitations ambitions to extend life time of machinery")

24 Technical Components Maintenance, Repair, Operations (MRO) Growth drivers Vendor and inventory reduction Total cost of ownership (TCO) Capex limitations ambitions to extend life time of machinery Industry 4.0 Success factors and measures Brand awareness Regional presence Competent technical support Comprehensive and state of the art product range High quality of own brand Intuitive search in the web-shop 24

25 Technical Components Example MRO: Growth market Industry Market potential of global industrial internet of things in billion US-$. Highly fragmented market Forcasted growth above historic market average, both for new facilities and for retrofit Enough niches for Datwyler distributors to be able to participate in the growth of the European market Anticipation of 5% growth per year of the relevant market Europe (estimate) Quelle: MarketsandMarkets 2016 Average yearly market growth of 8.0% in the next five years 25

26 Technical Components Automation Growth drivers Importance of efficient processes Increased focus on productivity Just in time delivery Industrial robotics Success factors and measures Technology roadmap: fastest integration of innovative components Range focussed application specific product packages Key account management Quality own brand as alternative 26

2016 2017 2018 2019 2020 2021")

27 Technical Components Example Automation: Growth segment industrial robotics Market potential of global industrial robotics in billion US-$ High technology, low volumes Wide range required, computing through to mechanical components Highly innovative products Positive penetration effect into standard business Europe (estimate) Quelle: MarketsandMarkets 2016 Average yearly market growth of 11.9% in the next six years 27

28 Core competences Distribution and logistic Easy to do business with International expansion Ecommerce as main channel Product management

29 Technical Components Division first half 2017 Encouraging B2B demand weak B2C business Organic revenue decline of 4.1% due to weak demand affecting B2C-business and home/consumer electronics wholesaler Nedis. Encouraging demand in the core B2B-business of Distrelec and Reichelt and for the new house brand RND. Lower sales volume lead to an EBIT decline despite strong cost control and improved commercial margins. Adjusted EBIT-margin of 3.6% before one-off costs of CHF 6.6 million. New Distrelec Entreprise Hub in Manchester on track; planned annual cost savings of CHF 3 million % % 2.0% Reichelt with profitable growth and further potential, specially by accelerating the international expansion. 4.6% 2.3% 3.9% 0.7% Nedis with serious drop in revenue in a very challenging and competitive market environment. Strategy is under review and new improvement measures are being implemented. 2014* Net revenue full year in CHFm Net revenue half year in CHFm EBIT as % of net revenue * excluding Maagtechnic 29

30 New Distrelec Enterprise Hub in Manchester Central steering of product, supplier, purchasing, e-commerce and marketing management Significantly increase quality and productivity of proposition delivery Boost the range of products and services on offer to customers Expected one-off costs of CHF 8 million, planned annual cost savings of CHF 3 million

31 Datwyler Group outlook for 2017 Focus on accelerating organic growth Datwyler Group: Revenue between CHF 1'270 and 1'310 million Adjusted EBIT margin in the upper half of target range of 11% - 14%, total one-off costs of approximately CHF 10 million Sealing Solutions division: Above market growth in all four segments thanks to strong positions Accelerate growth by intensifying sales, technical services and marketing activities, by expanding capacities and by upgrading production processes Technical Components division: Enhance segmentation of markets and customers Align value proposition and offering strategy more effectively with current and future customer needs New Distrelec Enterprise Hub, accelerated internationalisation of Reichelt, strategy under review at Nedis 31

32 Questions and Answers 32

33 Disclaimer This presentation contains forward-looking statements that reflect the Group s current expectations regarding market conditions and future events and are therefore subject to a number of risks, uncertainties and assumptions. Unanticipated events could cause actual results to differ from those predicted and from the information contained in this presentation. All forward-looking statements in this presentation are qualified in their entirety by the foregoing. Dätwyler Holding Inc. Gotthardstrasse 31, 6460 Altdorf / Switzerland T , F info@datwyler.com, CS Equity Mid Cap Conference 2017 / Datwyler,

15 November Welcome to the Datwyler Investor Day 2018

15 November 2018 Welcome to the Datwyler Investor Day 2018 PROGRAMME 11.00 12.30 Introductory presentations 12.30 13.15 Buffet lunch 13.15 15.00 Visit of First Line production plant 15.00 15.30 Closing

15 November 2018 Welcome to the Datwyler Investor Day 2018 PROGRAMME 11.00 12.30 Introductory presentations 12.30 13.15 Buffet lunch 13.15 15.00 Visit of First Line production plant 15.00 15.30 Closing

OUR HISTORY RECOGNISING THE SIGNS OF THE TIMES

OUR HISTORY RECOGNISING THE SIGNS OF THE TIMES Demand for cables has grown along with the demand for electricity and the growth of telephone, radio and television. Adolf Dätwyler recognised the signs of

OUR HISTORY RECOGNISING THE SIGNS OF THE TIMES Demand for cables has grown along with the demand for electricity and the growth of telephone, radio and television. Adolf Dätwyler recognised the signs of

Investor Presentation

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

Automotive Aftermarket 2025

Automotive Aftermarket CLEPA Conference March 22nd, 2018 THE GLOBAL AFTERMARKET Global AM parts retail market value by region bn EUR 38 +5.7% 59 135 +3.2% 174 85 +2.3% 102 86 +8.6% 166 Global +4.5% 44

Automotive Aftermarket CLEPA Conference March 22nd, 2018 THE GLOBAL AFTERMARKET Global AM parts retail market value by region bn EUR 38 +5.7% 59 135 +3.2% 174 85 +2.3% 102 86 +8.6% 166 Global +4.5% 44

MADE TO TRADE. Jahresgespräch Kreditversicherer

MADE TO TRADE. Jahresgespräch Kreditversicherer Olaf Koch, CFO 20 July 2011 METRO AG 2011 Disclaimer and Notes To the extent that statements in this presentation do not relate to historical or current

MADE TO TRADE. Jahresgespräch Kreditversicherer Olaf Koch, CFO 20 July 2011 METRO AG 2011 Disclaimer and Notes To the extent that statements in this presentation do not relate to historical or current

SCHULER 175 YEARS OF FUTURE CAPITAL MARKET DAY ANDRITZ MUNICH, OCTOBER 8, 2013

SCHULER 175 YEARS OF FUTURE CAPITAL MARKET DAY ANDRITZ MUNICH, OCTOBER 8, 2013 AGENDA 1 2 3 4 5 6 Schuler at a glance Market footprint of schuler worldwide Technology fields and range of products Our strategy

SCHULER 175 YEARS OF FUTURE CAPITAL MARKET DAY ANDRITZ MUNICH, OCTOBER 8, 2013 AGENDA 1 2 3 4 5 6 Schuler at a glance Market footprint of schuler worldwide Technology fields and range of products Our strategy

Annual Media Conference Welcome

Annual Media Conference 2017 Welcome Agenda 9 March 2017 Financial Review, CFO Business Review, CEO Customer Presentation, UK Customer Presentation, Italy Guidance, CEO Q&A Product Demonstration Annual

Annual Media Conference 2017 Welcome Agenda 9 March 2017 Financial Review, CFO Business Review, CEO Customer Presentation, UK Customer Presentation, Italy Guidance, CEO Q&A Product Demonstration Annual

WESCO International. Dave Schulz, Senior Vice President and Chief Financial Officer Raymond James 39 th Annual Investors Conference, March 7, 2018

WESCO International Dave Schulz, Senior Vice President and Chief Financial Officer 2 Safe Harbor Statement All statements made herein that are not historical facts should be considered as forward-looking

WESCO International Dave Schulz, Senior Vice President and Chief Financial Officer 2 Safe Harbor Statement All statements made herein that are not historical facts should be considered as forward-looking

INVESTOR PRESENTATION

INVESTOR PRESENTATION SWISS EQUITIES CONFERENCE BAADER HELVEA R. ERNI, CFO BAD RAGAZ 12 JANUARY 2018 Panalpina Biz Model / Strategy Achievements and key figures Operating and financial review Appendix

INVESTOR PRESENTATION SWISS EQUITIES CONFERENCE BAADER HELVEA R. ERNI, CFO BAD RAGAZ 12 JANUARY 2018 Panalpina Biz Model / Strategy Achievements and key figures Operating and financial review Appendix

Deutsche Bank German, Swiss & Austrian Conference

Deutsche Bank German, Swiss & Austrian Conference Arnd Zinnhardt CFO May 14, 2013 Safe-Harbor-Statement This presentation contains forward-looking statements based on beliefs of Software AG management.

Deutsche Bank German, Swiss & Austrian Conference Arnd Zinnhardt CFO May 14, 2013 Safe-Harbor-Statement This presentation contains forward-looking statements based on beliefs of Software AG management.

KNOWLEDGE BRIEF. Intershop Communications is Recognized as the 2017 Company of the Year in the Global Digital Commerce Platforms Market

KNOWLEDGE BRIEF Intershop Communications is Recognized as the 2017 Company of the Year in the Global Digital Commerce Platforms Market KNOWLEDGE BRIEF BY Intershop Communications is Recognized as the 2017

KNOWLEDGE BRIEF Intershop Communications is Recognized as the 2017 Company of the Year in the Global Digital Commerce Platforms Market KNOWLEDGE BRIEF BY Intershop Communications is Recognized as the 2017

Software AG Heading for Growth

Software AG Heading for Growth Karl-Heinz Streibich, CEO June 01, 2006 Credit Suisse European Technology Conference, Barcelona, Spain This presentation contains forward-looking statements based on beliefs

Software AG Heading for Growth Karl-Heinz Streibich, CEO June 01, 2006 Credit Suisse European Technology Conference, Barcelona, Spain This presentation contains forward-looking statements based on beliefs

DIRECTION FRANKIE NG, CEO AND CARLA DE GEYSELEER, CFO INVESTOR DAYS, OCTOBER 2015

DIRECTION FRANKIE NG, CEO AND CARLA DE GEYSELEER, CFO INVESTOR DAYS, 29-30 OCTOBER 2015 1 TABLE OF CONTENTS SGS Business Principles Market evolution and opportunities Realign SGS strategic focus Finance

DIRECTION FRANKIE NG, CEO AND CARLA DE GEYSELEER, CFO INVESTOR DAYS, 29-30 OCTOBER 2015 1 TABLE OF CONTENTS SGS Business Principles Market evolution and opportunities Realign SGS strategic focus Finance

Health Care Worldwide. Crédit Suisse Global Credit Products Conference October 1, Barcelona

Health Care Worldwide Crédit Suisse Global Credit Products Conference October 1, 2015 - Barcelona Safe Harbor Statement This presentation contains forward-looking statements that are subject to various

Health Care Worldwide Crédit Suisse Global Credit Products Conference October 1, 2015 - Barcelona Safe Harbor Statement This presentation contains forward-looking statements that are subject to various

Third Party Logistics Market India

Third Party Logistics Market India November 2014 Executive Summary Market Third party logistics is one of the growing sectors in India that has attracted a number of players The market is rapidly evolving

Third Party Logistics Market India November 2014 Executive Summary Market Third party logistics is one of the growing sectors in India that has attracted a number of players The market is rapidly evolving

SIKA CAPITAL MARKETS DAY FROM PATENTS TO WORLD CLASS PRODUCTS PAUL SCHULER, CEO, ZURICH, SEPTEMBER 20, 2017

SIKA CAPITAL MARKETS DAY FROM PATENTS TO WORLD CLASS PRODUCTS PAUL SCHULER, CEO, ZURICH, SEPTEMBER 20, 2017 TABLE OF CONTENTS 1. STRATEGIC TARGETS 2020 2. OUTLOOK 3. SUCCESSFUL STRATEGY EXECUTION LIFE-CYCLE

SIKA CAPITAL MARKETS DAY FROM PATENTS TO WORLD CLASS PRODUCTS PAUL SCHULER, CEO, ZURICH, SEPTEMBER 20, 2017 TABLE OF CONTENTS 1. STRATEGIC TARGETS 2020 2. OUTLOOK 3. SUCCESSFUL STRATEGY EXECUTION LIFE-CYCLE

OTC Virtual Investor Conference

OTC Virtual Investor Conference October 4, 2018 Dr. Chris L. Coccio Chairman and CEO Stephen Harshbarger President 2018 Sono Tek Corporation Safe Harbor Statement This presentation contains forward-looking

OTC Virtual Investor Conference October 4, 2018 Dr. Chris L. Coccio Chairman and CEO Stephen Harshbarger President 2018 Sono Tek Corporation Safe Harbor Statement This presentation contains forward-looking

SWISS EQUITIES CONFERENCE

SWISS EQUITIES CONFERENCE 12 th JANUARY 2018, Bad Ragaz Tobias Knechtle (CFO) Valora: Highlights 2017 - Well on track to achieve mid-term profitability targets - Acquisition and integration of Pretzel

SWISS EQUITIES CONFERENCE 12 th JANUARY 2018, Bad Ragaz Tobias Knechtle (CFO) Valora: Highlights 2017 - Well on track to achieve mid-term profitability targets - Acquisition and integration of Pretzel

SAP Mii Implementation at Dätwyler

SAP Mii Implementation at Dätwyler SAP Digital Manufacturing 30 th of May 2017 Stepan Picka Head of Applications Dätwyler IT Services Polní 224, 504 01 Nový Bydžov, Czech Republic stepan.picka@datwyler.com,

SAP Mii Implementation at Dätwyler SAP Digital Manufacturing 30 th of May 2017 Stepan Picka Head of Applications Dätwyler IT Services Polní 224, 504 01 Nový Bydžov, Czech Republic stepan.picka@datwyler.com,

UBS Global Life Sciences Conference

September 21, 2010 UBS Global Life Sciences Conference Tecan Group AG Thomas Bachmann, CEO September 21, 2010 / p2 / UBS Global Life Sciences Conference Introducing Tecan Provider of instruments and workflow-solutions

September 21, 2010 UBS Global Life Sciences Conference Tecan Group AG Thomas Bachmann, CEO September 21, 2010 / p2 / UBS Global Life Sciences Conference Introducing Tecan Provider of instruments and workflow-solutions

Study Chemical Distribution 2012

Study Chemical Distribution 2012 - Results - Dr. Matthias Hornke, LL.M. (M&A) Münster, February 2012 Matthias.Hornke@gmx.de Agenda Status Quo and Study Overview Results: Overview Results of the Online

Study Chemical Distribution 2012 - Results - Dr. Matthias Hornke, LL.M. (M&A) Münster, February 2012 Matthias.Hornke@gmx.de Agenda Status Quo and Study Overview Results: Overview Results of the Online

Intelligent energy and data solutions for tomorrow's world. Investor Presentation Q1 2018

Intelligent energy and data solutions for tomorrow's world Investor Presentation Q1 2018 A global leader in wiring systems and cable technology LEONI at a glance Industrial Solutions Business mix (in %

Intelligent energy and data solutions for tomorrow's world Investor Presentation Q1 2018 A global leader in wiring systems and cable technology LEONI at a glance Industrial Solutions Business mix (in %

Fit for Leadership Next Stage

Fit for Leadership Next Stage Frank Lindenberg, Member of the Divisional Board Mercedes-Benz Cars Executive Vice President Finance & Controlling Mercedes-Benz Cars Capital Market Day 2015 June 11 th, 2015

Fit for Leadership Next Stage Frank Lindenberg, Member of the Divisional Board Mercedes-Benz Cars Executive Vice President Finance & Controlling Mercedes-Benz Cars Capital Market Day 2015 June 11 th, 2015

FY 2015 Results. Press Conference. March 1, Gisbert Rühl CEO

FY 2015 Results Press Conference March 1, 2016 Gisbert Rühl CEO Disclaimer This presentation contains forward-looking statements which reflect the current views of the management of Klöckner & Co SE with

FY 2015 Results Press Conference March 1, 2016 Gisbert Rühl CEO Disclaimer This presentation contains forward-looking statements which reflect the current views of the management of Klöckner & Co SE with

ULTRA Thermal Precision

Ambient Ambient Temperature Temperature -0.212-0.212-0.203 Ȃ Ȃ &'() 0/27 Ȃ -0.263-0.358-0.014-0.074-0.398-0.053 0.208-0.057-0.322 0.299 0.002-0.016 * -0.020-0.103-2.385 1.093 0.010 1.036 1.816-0.007-2.812-0.128-0.011-0.138

Ambient Ambient Temperature Temperature -0.212-0.212-0.203 Ȃ Ȃ &'() 0/27 Ȃ -0.263-0.358-0.014-0.074-0.398-0.053 0.208-0.057-0.322 0.299 0.002-0.016 * -0.020-0.103-2.385 1.093 0.010 1.036 1.816-0.007-2.812-0.128-0.011-0.138

JPMC European Technology CEO Conference. 18 June 2013

JPMC European Technology CEO Conference 18 June 2013 1 Q1 IMS 2013 Revenue 2% lower year on year Organic growth 6% lower Q1 revenue was lower from softness in B2B markets; and revenue decline from our

JPMC European Technology CEO Conference 18 June 2013 1 Q1 IMS 2013 Revenue 2% lower year on year Organic growth 6% lower Q1 revenue was lower from softness in B2B markets; and revenue decline from our

Investor Presentation. November, 2015

Investor Presentation November, 2015 1 Disclaimer These slides contain (and the accompanying oral discussion will contain) forward looking statements. All statements other than statements of historical

Investor Presentation November, 2015 1 Disclaimer These slides contain (and the accompanying oral discussion will contain) forward looking statements. All statements other than statements of historical

2017 Half Year Results. 28 September 2017

2017 Half Year Results 28 September 2017 Disclaimer Restricted distribution This presentation is not for release, publication or distribution, in whole or in part, directly or indirectly, in, into or from

2017 Half Year Results 28 September 2017 Disclaimer Restricted distribution This presentation is not for release, publication or distribution, in whole or in part, directly or indirectly, in, into or from

Kuoni Group Destinations incl GTA. Analyst & Media Event Zurich, 7 July 2011

Kuoni Group Destinations incl GTA Analyst & Media Event Zurich, 7 July 2011 Disclaimer This communication contains statements that constitute forward-looking statements. In this communication, such forward-looking

Kuoni Group Destinations incl GTA Analyst & Media Event Zurich, 7 July 2011 Disclaimer This communication contains statements that constitute forward-looking statements. In this communication, such forward-looking

CJS Securities Conference New York, NY January 15, 2014

CJS Securities Conference New York, NY January 15, 2014 Forward-Looking Statements This presentation contains certain forward-looking statements concerning the Company's operations, performance, and financial

CJS Securities Conference New York, NY January 15, 2014 Forward-Looking Statements This presentation contains certain forward-looking statements concerning the Company's operations, performance, and financial

SIKA MADE BINDING OFFER TO ACQUIRE PAREX MEDIA AND ANALYST PRESENTATION JANUARY 8, 2019

SIKA MADE BINDING OFFER TO ACQUIRE PAREX MEDIA AND ANALYST PRESENTATION JANUARY 8, 2019 AGENDA TRANSACTION HIGHLIGHTS PAREX A LEADING MORTAR MANUFACTURER TRANSACTION RATIONALE FINANCIAL CONSIDERATIONS

SIKA MADE BINDING OFFER TO ACQUIRE PAREX MEDIA AND ANALYST PRESENTATION JANUARY 8, 2019 AGENDA TRANSACTION HIGHLIGHTS PAREX A LEADING MORTAR MANUFACTURER TRANSACTION RATIONALE FINANCIAL CONSIDERATIONS

Interim results Analysts' meeting. Thursday 23 August Agenda

Interim results 2012 Analysts' meeting Thursday 23 August 2012 Agenda 1. Kendrion at a glance 2. Highlights for the first six months of 2012 3. Key figures and financial objectives 4. Review of the business

Interim results 2012 Analysts' meeting Thursday 23 August 2012 Agenda 1. Kendrion at a glance 2. Highlights for the first six months of 2012 3. Key figures and financial objectives 4. Review of the business

Logistics Market China

Logistics Market China November 2014 Executive Summary Market Logistics market value in China is expected to reach USD 55.1 tn by 2018 from USD 28 tn in 2012, growing at a CAGR of 11.9% Industrial products

Logistics Market China November 2014 Executive Summary Market Logistics market value in China is expected to reach USD 55.1 tn by 2018 from USD 28 tn in 2012, growing at a CAGR of 11.9% Industrial products

Henkel. 17 th German Corporate Conference Frankfurt, January 15, 2018

Henkel 17 th German Corporate Conference Frankfurt, Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate management

Henkel 17 th German Corporate Conference Frankfurt, Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate management

Investor Presentation. November, 2015

Investor Presentation November, 2015 1 Disclaimer These slides contain (and the accompanying oral discussion will contain) forward looking statements. All statements other than statements of historical

Investor Presentation November, 2015 1 Disclaimer These slides contain (and the accompanying oral discussion will contain) forward looking statements. All statements other than statements of historical

A Strategic Approach to Growth in a Global Market

A Strategic Approach to Growth in a Global Market André Lacroix Group CEO Sanford Bernstein Conference 22 September 2010 Global industry leader operating in the premium sector with strong returns. Strengthened

A Strategic Approach to Growth in a Global Market André Lacroix Group CEO Sanford Bernstein Conference 22 September 2010 Global industry leader operating in the premium sector with strong returns. Strengthened

Acquisition of KLX Inc.

Acquisition of KLX Inc. May 1, 2018 Forward-Looking Information Forward-Looking Information Is Subject to Risk and Uncertainty Certain statements in this document may be forward-looking within the meaning

Acquisition of KLX Inc. May 1, 2018 Forward-Looking Information Forward-Looking Information Is Subject to Risk and Uncertainty Certain statements in this document may be forward-looking within the meaning

Shaping the future of TS with Innovation and Quality

Shaping the future of TS with Innovation and Quality Hans M. Schabert, Group President Transportation Systems Financial Day, February 17, 2004 2 Key figures FY01 FY02 FY03 Q1FY04 New orders (in billions

Shaping the future of TS with Innovation and Quality Hans M. Schabert, Group President Transportation Systems Financial Day, February 17, 2004 2 Key figures FY01 FY02 FY03 Q1FY04 New orders (in billions

Presentation for Deutsche Bank Swiss Equities Conference

Zurich Airport, 19 th May 2010 Monika Ribar, CEO Presentation for Deutsche Bank Swiss Equities Conference 19 th May 2010 2 Panalpina at a glance Comprehensive global network Among top 5 globally in air

Zurich Airport, 19 th May 2010 Monika Ribar, CEO Presentation for Deutsche Bank Swiss Equities Conference 19 th May 2010 2 Panalpina at a glance Comprehensive global network Among top 5 globally in air

Half-year figures Amsterdam, August 30th Sharing our DNA

Half-year figures 2018 Amsterdam, August 30th 2018 Sharing our DNA 1 Neways Electronics Safe harbor statement This presentation may include forward-looking statements. Other than reported financial results

Half-year figures 2018 Amsterdam, August 30th 2018 Sharing our DNA 1 Neways Electronics Safe harbor statement This presentation may include forward-looking statements. Other than reported financial results

Telefónica O2 Czech Republic

Telefónica O2 Czech Republic Quarterly Results January September 2008 23 rd October, 2008 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Telefónica O2 Czech Republic Quarterly Results January September 2008 23 rd October, 2008 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Bharat Forge Limited. Analyst/Investor Update

Bharat Forge Limited Analyst/Investor Update July 20, 2002 Financial Highlights Corresponding Quarter Analysis (April - June 2002 v/s April- June 2001) Total sales increased by 27% at Rs.1433.6 million.

Bharat Forge Limited Analyst/Investor Update July 20, 2002 Financial Highlights Corresponding Quarter Analysis (April - June 2002 v/s April- June 2001) Total sales increased by 27% at Rs.1433.6 million.

MADE TO TRADE. Merrill Lynch Retail, Transport & Leisure Conference 2013

MADE TO TRADE. Merrill Lynch Retail, Transport & Leisure Conference 2013 23 May 2013 London METRO AG 2013 0 Disclaimer and Notes To the extent that statements in this presentation do not relate to historical

MADE TO TRADE. Merrill Lynch Retail, Transport & Leisure Conference 2013 23 May 2013 London METRO AG 2013 0 Disclaimer and Notes To the extent that statements in this presentation do not relate to historical

UBS Global Life Sciences Conference

September 20, 2011 UBS Global Life Sciences Conference Tecan Group AG Dr. Rudolf Eugster, CFO September 20, 2011 / p2 / UBS GLSC Contents Introducing Tecan Strategic Growth Drivers Financials H1 2011 &

September 20, 2011 UBS Global Life Sciences Conference Tecan Group AG Dr. Rudolf Eugster, CFO September 20, 2011 / p2 / UBS GLSC Contents Introducing Tecan Strategic Growth Drivers Financials H1 2011 &

EB, Elektrobit Corporation

EB, Elektrobit Corporation Financial Statement 2008 February 13, 2009 Forward-looking Statements Some statements made in this material relating to future circumstances or status, including, without limitation,

EB, Elektrobit Corporation Financial Statement 2008 February 13, 2009 Forward-looking Statements Some statements made in this material relating to future circumstances or status, including, without limitation,

Ascom Investor Presentation. May 2018

Ascom Investor Presentation May 2018 Our Vision Ascom closes digital information gaps allowing for the best possible decisions anytime and anywhere 2 Ascom increases workflow productivity in Healthcare

Ascom Investor Presentation May 2018 Our Vision Ascom closes digital information gaps allowing for the best possible decisions anytime and anywhere 2 Ascom increases workflow productivity in Healthcare

Mike Roman. Chief Operating Officer & Executive Vice President. Bank of America Merrill Lynch Global Industrials Conference.

Mike Roman Chief Operating Officer & Executive Vice President Bank of America Merrill Lynch Global Industrials Conference March 22, 2018 1 Building strength-on-strength and positioned for growth 2017 Executing

Mike Roman Chief Operating Officer & Executive Vice President Bank of America Merrill Lynch Global Industrials Conference March 22, 2018 1 Building strength-on-strength and positioned for growth 2017 Executing

O2 Czech Republic, a. s. 29 th January Quarterly Results January December 2018

O2 Czech Republic, a. s. 29 th January 2019 Quarterly Results January December 2018 Cautionary statement Any forward-looking statements concerning future economic and financial performance of O2 Czech

O2 Czech Republic, a. s. 29 th January 2019 Quarterly Results January December 2018 Cautionary statement Any forward-looking statements concerning future economic and financial performance of O2 Czech

Fresenius Investor News

health care worldwide February 22, 2007 Contact: Birgit Grund Fresenius AG Investor Relations Tel. ++49-6172 - 608 2485 Fax ++49-6172 - 608 2488 e-mail: ir-fre@fresenius.de Internet: www.fresenius-ag.com

health care worldwide February 22, 2007 Contact: Birgit Grund Fresenius AG Investor Relations Tel. ++49-6172 - 608 2485 Fax ++49-6172 - 608 2488 e-mail: ir-fre@fresenius.de Internet: www.fresenius-ag.com

Disclosure Regarding Forward-Looking Statements

Disclosure Regarding Forward-Looking Statements This report contains forward-looking statements within the meaning of the federal securities laws. Other than statements of historical facts, all statements

Disclosure Regarding Forward-Looking Statements This report contains forward-looking statements within the meaning of the federal securities laws. Other than statements of historical facts, all statements

Annual General Meeting of Shareholders

Logistics Healthcare Automotive Industrial Automation Machine & Systems Energy Annual General Meeting of Shareholders Rotterdam, May 22, 2013 Agenda Key results 2012 Operational developments Financial

Logistics Healthcare Automotive Industrial Automation Machine & Systems Energy Annual General Meeting of Shareholders Rotterdam, May 22, 2013 Agenda Key results 2012 Operational developments Financial

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR. January 2019

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR January 2019 Disclaimer The information contained in this presentation is for background purposes only and is subject to amendment, revision and updating.

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR January 2019 Disclaimer The information contained in this presentation is for background purposes only and is subject to amendment, revision and updating.

Sidoti & Company Spring 2018 Conference. Greg Woods, President and CEO David S. Smith, CFO March 29, 2018

Sidoti & Company Spring 2018 Conference Greg Woods, President and CEO David S. Smith, CFO March 29, 2018 Forward-looking Statements Information included in this presentation may contain forward-looking

Sidoti & Company Spring 2018 Conference Greg Woods, President and CEO David S. Smith, CFO March 29, 2018 Forward-looking Statements Information included in this presentation may contain forward-looking

Shoply Gold Coast Investment Showcase

Shoply Gold Coast Investment Showcase June 18, 2015 1 Rapidly growing ecommerce Group 1 Shoply corporate overview 2 Attractive growth in online shopping market 3 Strong customer proposition premium brands

Shoply Gold Coast Investment Showcase June 18, 2015 1 Rapidly growing ecommerce Group 1 Shoply corporate overview 2 Attractive growth in online shopping market 3 Strong customer proposition premium brands

Agricultural Equipment India

Agricultural Equipment India January 2015 Executive Summary Market Overview Global agricultural equipment market is expected to grow at a CAGR of x% through to to reach INR yy bn in Huge demand from Asia

Agricultural Equipment India January 2015 Executive Summary Market Overview Global agricultural equipment market is expected to grow at a CAGR of x% through to to reach INR yy bn in Huge demand from Asia

Corporate Presentation March 2015

Corporate Presentation March 2015 World s trusted tailored-made metal precision manufacturer IPE Group, a leading OEM/ODM manufacturer, is principally engaged in the manufacture of high precision metal

Corporate Presentation March 2015 World s trusted tailored-made metal precision manufacturer IPE Group, a leading OEM/ODM manufacturer, is principally engaged in the manufacture of high precision metal

Solid start into the year

Deutsche Post DHL Group results Q 203 Solid start into the year Larry Rosen, CFO Bonn, 4 May 203 Q 203 Highlights (/2) Delivering solid results in still challenging macro-environment EBIT increase reflects

Deutsche Post DHL Group results Q 203 Solid start into the year Larry Rosen, CFO Bonn, 4 May 203 Q 203 Highlights (/2) Delivering solid results in still challenging macro-environment EBIT increase reflects

Gorenje Gorenje Group Summary of the Strategic plan

Group Summary of the Strategic plan 2010 2013 Summary off tthe Sttrattegiic pllan 2010 -- 2013 Gorrenjje Grroup Velenje, Slovenia, January 2010 1 Group Summary of the Strategic plan 2010 2013 Letter by

Group Summary of the Strategic plan 2010 2013 Summary off tthe Sttrattegiic pllan 2010 -- 2013 Gorrenjje Grroup Velenje, Slovenia, January 2010 1 Group Summary of the Strategic plan 2010 2013 Letter by

The 31st Annual Gabelli Automotive Aftermarket Symposium. Lear s Asian Strategy

The 31st Annual Gabelli Automotive Aftermarket Symposium Lear s Asian Strategy October 31, 2007 Agenda Company Overview Bob Rossiter, Chairman, CEO and President Lear s Asian Strategy Lou Salvatore, Senior

The 31st Annual Gabelli Automotive Aftermarket Symposium Lear s Asian Strategy October 31, 2007 Agenda Company Overview Bob Rossiter, Chairman, CEO and President Lear s Asian Strategy Lou Salvatore, Senior

2015 Financial Statements. Amsterdam, 23 February Sharing our DNA

2015 Financial Statements Amsterdam, 23 February 2016 Sharing our DNA Agenda 2015 Main Points Market and Positioning Financial Operational Outlook and Conclusion 2015 MAIN POINTS 2015 Main Points Our customers

2015 Financial Statements Amsterdam, 23 February 2016 Sharing our DNA Agenda 2015 Main Points Market and Positioning Financial Operational Outlook and Conclusion 2015 MAIN POINTS 2015 Main Points Our customers

TXT e-solutions. Corporate Presentation March 2015

TXT e-solutions Corporate Presentation March 2015 2014: Another year of Growth Revenues: 55.9 m (+6.3%), 57% from Int l Operations EBIT: 5.5 m (+10%) Cash Flow from Op. 9.3% of Revenues NFP: 8.5m (+ Treasury

TXT e-solutions Corporate Presentation March 2015 2014: Another year of Growth Revenues: 55.9 m (+6.3%), 57% from Int l Operations EBIT: 5.5 m (+10%) Cash Flow from Op. 9.3% of Revenues NFP: 8.5m (+ Treasury

Margins of pharmaceutical companies are continuing to decline the future lies in new ecosystems

Karin Mateu Media Relations Tel.: +41 (0) 58 286 44 09 karin.mateu@ch.ey.com Margins of pharmaceutical companies are continuing to decline the future lies in new ecosystems Glaxo is leading the way in

Karin Mateu Media Relations Tel.: +41 (0) 58 286 44 09 karin.mateu@ch.ey.com Margins of pharmaceutical companies are continuing to decline the future lies in new ecosystems Glaxo is leading the way in

21 st Annual Needham Growth Conference. January 15, 2019

21 st Annual Needham Growth Conference January 15, 2019 Forward-Looking Statements Certain statements in this communication may contain forward-looking statements within the meaning of the Private Securities

21 st Annual Needham Growth Conference January 15, 2019 Forward-Looking Statements Certain statements in this communication may contain forward-looking statements within the meaning of the Private Securities

BUSINESS STRATEGY OUTSIDE EUROPE

RPC THE ESSENTIAL INGREDIENT BUSINESS STRATEGY OUTSIDE EUROPE 13 November 2017 2017 RPC Group Plc. All Rights Reserved. Agenda Business strategy outside Europe Eric Chavent Astrapak Robin Moore RPC Group

RPC THE ESSENTIAL INGREDIENT BUSINESS STRATEGY OUTSIDE EUROPE 13 November 2017 2017 RPC Group Plc. All Rights Reserved. Agenda Business strategy outside Europe Eric Chavent Astrapak Robin Moore RPC Group

DISRUPTIVE OPPORTUNITIES

CHALLENGING TIMES, DISRUPTIVE OPPORTUNITIES The Indian logistics industry is rife with fragmentation, inefficiencies and hence, the opportunities for disruption. Inferior management practices, a high level

CHALLENGING TIMES, DISRUPTIVE OPPORTUNITIES The Indian logistics industry is rife with fragmentation, inefficiencies and hence, the opportunities for disruption. Inferior management practices, a high level

Thiel Logistik AG Investor Meetings Frankfurt August 31, 2007

Thiel Logistik AG Investor Meetings Frankfurt August 31, 2007 Agenda Market and Business Profile New Management Structure Financial Review and Outlook Half-Year Results 2007 1 Company Profile Business:

Thiel Logistik AG Investor Meetings Frankfurt August 31, 2007 Agenda Market and Business Profile New Management Structure Financial Review and Outlook Half-Year Results 2007 1 Company Profile Business:

KUKA Aktiengesellschaft

KUKA Aktiengesellschaft Company Presentation 2018 Page: 1 Agenda 1. KUKA Group at a glance 2. Divisions, Strategy and Targets 3. Technology and Innovation 4. Shareholder Structure, Financials and Markets

KUKA Aktiengesellschaft Company Presentation 2018 Page: 1 Agenda 1. KUKA Group at a glance 2. Divisions, Strategy and Targets 3. Technology and Innovation 4. Shareholder Structure, Financials and Markets

Indian Pharmaceutical Industry. January 2018

Indian Pharmaceutical Industry January 2018 Introduction The pharmaceutical Industry around the world is one of the fastest growing industries and a major contributor to the world economy. 2020 55 1400

Indian Pharmaceutical Industry January 2018 Introduction The pharmaceutical Industry around the world is one of the fastest growing industries and a major contributor to the world economy. 2020 55 1400

SKF SHB Nordic Large Cap Seminar Stockholm September 12, 2018 Christian Johansson, Chief Financial Officer and Senior Vice President

SKF 2018 SHB Nordic Large Cap Seminar Stockholm September 12, 2018 Christian Johansson, Chief Financial Officer and Senior Vice President SKF more fit than ever! Agility and customer focus Net debt / equity:

SKF 2018 SHB Nordic Large Cap Seminar Stockholm September 12, 2018 Christian Johansson, Chief Financial Officer and Senior Vice President SKF more fit than ever! Agility and customer focus Net debt / equity:

Telefónica O2 Czech Republic

Telefónica O2 Czech Republic Quarterly Results January December 2009 25 th February, 2010 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Telefónica O2 Czech Republic Quarterly Results January December 2009 25 th February, 2010 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Institutional Presentation. May 2016

Institutional Presentation May 2016 Section 1 Unidas At a Glance Unidas At a Glance 3 rd largest Brazilian car rental company by total fleet, with nationwide operations in fleet management solutions, car

Institutional Presentation May 2016 Section 1 Unidas At a Glance Unidas At a Glance 3 rd largest Brazilian car rental company by total fleet, with nationwide operations in fleet management solutions, car

Business needs and potential solutions

Business needs and potential solutions Survey report Research and Market Intelligence at BDC May 2018 Table of contents 01 Methodology 02 Summary of results 03 Detailed results BDC SME needs and potential

Business needs and potential solutions Survey report Research and Market Intelligence at BDC May 2018 Table of contents 01 Methodology 02 Summary of results 03 Detailed results BDC SME needs and potential

For personal use only. 25 th October Annual General Meeting Presentation

25 th October Annual General Meeting Presentation Organisational Structure For personal use only Performance Update Operational Overview Operational Performance Automotive dealer enquiry growth up 9% on

25 th October Annual General Meeting Presentation Organisational Structure For personal use only Performance Update Operational Overview Operational Performance Automotive dealer enquiry growth up 9% on

ACQUISITION MEGTEC / UNIVERSAL

ACQUISITION MEGTEC / UNIVERSAL Ralf W. Dieter, CEO Dr. Jochen Weyrauch, Member of the Board Bietigheim-Bissingen, June 6, 2018 www.durr.com DISCLAIMER This publication has been prepared independently by

ACQUISITION MEGTEC / UNIVERSAL Ralf W. Dieter, CEO Dr. Jochen Weyrauch, Member of the Board Bietigheim-Bissingen, June 6, 2018 www.durr.com DISCLAIMER This publication has been prepared independently by

Thiel Logistik AG June 19, 2007

Thiel Logistik AG June 19, 2007 Agenda Company Overview New Management Structure Financial Review and Outlook 1 Company Profile Business: As an external partner, Thiel Logistik AG, develops holistic logistics

Thiel Logistik AG June 19, 2007 Agenda Company Overview New Management Structure Financial Review and Outlook 1 Company Profile Business: As an external partner, Thiel Logistik AG, develops holistic logistics

Income before income taxes reached billion yen, up 8.6 billion yen yearon-year.

1 2 [Overview of the consolidated financial results] We posted sales of 4,308.8 billion yen, up 212.8 billion yen from the previous year, equivalent to annual revenue growth of 5.2%. Operating income reached

1 2 [Overview of the consolidated financial results] We posted sales of 4,308.8 billion yen, up 212.8 billion yen from the previous year, equivalent to annual revenue growth of 5.2%. Operating income reached

M16/3/BUSMT/HP1/ENG/TZ0/XX BUSINESS MANAGEMENT STANDARD LEVEL PAPER 1. Practice examination 2016 Todos os Mercados.

M16/3/BUSMT/HP1/ENG/TZ0/XX BUSINESS MANAGEMENT STANDARD LEVEL PAPER 1 Practice examination 2016 Todos os Mercados 1 hour 15 minutes INSTRUCTIONS TO CANDIDATES Do not open this examination paper until instructed

M16/3/BUSMT/HP1/ENG/TZ0/XX BUSINESS MANAGEMENT STANDARD LEVEL PAPER 1 Practice examination 2016 Todos os Mercados 1 hour 15 minutes INSTRUCTIONS TO CANDIDATES Do not open this examination paper until instructed

Fresenius Investor News

health care worldwide August 3, 2006 Contact: Birgit Grund Fresenius AG Investor Relations Tel. ++49-6172 - 608 2485 Fax ++49-6172 - 608 2488 e-mail: ir-fre@fresenius.de Internet: www.fresenius-ag.com

health care worldwide August 3, 2006 Contact: Birgit Grund Fresenius AG Investor Relations Tel. ++49-6172 - 608 2485 Fax ++49-6172 - 608 2488 e-mail: ir-fre@fresenius.de Internet: www.fresenius-ag.com

MR. LI PING MR. ZHENG QIBAO MR. YUAN JIANXING MR. LIU XIAOYI MANAGEMENT EXECUTIVE DIRECTOR & CHAIRMAN EXECUTIVE DIRECTOR & PRESIDENT

MANAGEMENT MR. LI PING EXECUTIVE DIRECTOR & CHAIRMAN MR. ZHENG QIBAO EXECUTIVE DIRECTOR & PRESIDENT MR. YUAN JIANXING EXECUTIVE DIRECTOR, EXECUTIVE VICE PRESIDENT & CFO MR. LIU XIAOYI EXECUTIVE VICE PRESIDENT

MANAGEMENT MR. LI PING EXECUTIVE DIRECTOR & CHAIRMAN MR. ZHENG QIBAO EXECUTIVE DIRECTOR & PRESIDENT MR. YUAN JIANXING EXECUTIVE DIRECTOR, EXECUTIVE VICE PRESIDENT & CFO MR. LIU XIAOYI EXECUTIVE VICE PRESIDENT

ABB LTD, ZURICH, SWITZERLAND, APRIL 19, 2018 Profitable growth. Q results. Ulrich Spiesshofer, CEO; Timo Ihamuotila, CFO

ABB LTD, ZURICH, SWITZERLAND, APRIL 9, 208 Profitable growth Q 208 results Ulrich Spiesshofer, CEO; Timo Ihamuotila, CFO Important notices This presentation includes forward-looking information and statements

ABB LTD, ZURICH, SWITZERLAND, APRIL 9, 208 Profitable growth Q 208 results Ulrich Spiesshofer, CEO; Timo Ihamuotila, CFO Important notices This presentation includes forward-looking information and statements

Year End Results Presentation to 30 June 2013

Year End Results Presentation to 30 June 2013 Organisational Structure Performance Update Operational Overview Operational Performance Automotive dealer enquiry growth up 9% on pcp Enquiry volumes on new

Year End Results Presentation to 30 June 2013 Organisational Structure Performance Update Operational Overview Operational Performance Automotive dealer enquiry growth up 9% on pcp Enquiry volumes on new

Artificial intelligence A CORNERSTONE OF MONTRÉAL S ECONOMIC DEVELOPMENT

Artificial intelligence A CORNERSTONE OF MONTRÉAL S ECONOMIC DEVELOPMENT What is artificial intelligence and what are its applications? Artificial intelligence (AI) is booming in Montréal. In fact, intelligent

Artificial intelligence A CORNERSTONE OF MONTRÉAL S ECONOMIC DEVELOPMENT What is artificial intelligence and what are its applications? Artificial intelligence (AI) is booming in Montréal. In fact, intelligent

Applus Services, S.A. Investor Presentation

Applus Services, S.A. Investor Presentation April 2015 Aston Swift, Investor Relations aston.swift@applus.com A LEADING GLOBAL PROVIDER OF TESTING, INSPECTION AND CERTIFICATION (TIC) SERVICES Revenue 1.62bn,

Applus Services, S.A. Investor Presentation April 2015 Aston Swift, Investor Relations aston.swift@applus.com A LEADING GLOBAL PROVIDER OF TESTING, INSPECTION AND CERTIFICATION (TIC) SERVICES Revenue 1.62bn,

A Leading Provider of Marketing Automation Solutions

A Leading Provider of Marketing Automation Solutions Investor Presentation December 2017 SharpSpring, Inc. investors.sharpspring.com NASDAQ: SHSP Safe Harbor Statement The information provided in this

A Leading Provider of Marketing Automation Solutions Investor Presentation December 2017 SharpSpring, Inc. investors.sharpspring.com NASDAQ: SHSP Safe Harbor Statement The information provided in this

Avery Dennison Investor Presentation August 2014

Avery Dennison Investor Presentation August 2014 Unless otherwise indicated, the discussion of the company s results is focused on its continuing operations, and comparisons are to the same period in the

Avery Dennison Investor Presentation August 2014 Unless otherwise indicated, the discussion of the company s results is focused on its continuing operations, and comparisons are to the same period in the

Kasper Rorsted Carsten Knobel London Nov 16, November 16, 2012 Henkel Strategy

Henkel Strategy Kasper Rorsted Carsten Knobel London Nov 16, 2012 1 November 16, 2012 Henkel Strategy Disclaimer This information contains forward-looking statements which are based on current estimates

Henkel Strategy Kasper Rorsted Carsten Knobel London Nov 16, 2012 1 November 16, 2012 Henkel Strategy Disclaimer This information contains forward-looking statements which are based on current estimates

Product Development Strategy Alan Chow SVP, Product Development & CTO

Product Development Strategy Alan Chow SVP, Product Development & CTO Creating Shareholder Value Innovation Drives Profitable Revenue Growth Innovation Drives Profitable Revenue Growth Innovation Drives

Product Development Strategy Alan Chow SVP, Product Development & CTO Creating Shareholder Value Innovation Drives Profitable Revenue Growth Innovation Drives Profitable Revenue Growth Innovation Drives

WE EMPOWER THE FUTURE

WE EMPOWER THE FUTURE FINANCIAL STATEMENT PRESS CONFERENCE MARCH 20, 2017 AGENDA 1. WELCOME & BUSINESS MODEL, DR. DIRK ROTHWEILER (CEO) 2. RESULTS FOR THE FINANCIAL YEAR 2016, DR. MATHIAS GOLLWITZER (CFO)

WE EMPOWER THE FUTURE FINANCIAL STATEMENT PRESS CONFERENCE MARCH 20, 2017 AGENDA 1. WELCOME & BUSINESS MODEL, DR. DIRK ROTHWEILER (CEO) 2. RESULTS FOR THE FINANCIAL YEAR 2016, DR. MATHIAS GOLLWITZER (CFO)

DEUTSCHE POST DHL GROUP RESULTS Q Analyst Call Bonn, 12 November 2014

DEUTSCHE POST DHL GROUP RESULTS Q3 2014 Analyst Call Bonn, 12 November 2014 AGENDA 1 2 3 4 Q3 Highlights: Key trends (Frank Appel) We have set the course for 2020 (Frank Appel) Financial results Q3 2014

DEUTSCHE POST DHL GROUP RESULTS Q3 2014 Analyst Call Bonn, 12 November 2014 AGENDA 1 2 3 4 Q3 Highlights: Key trends (Frank Appel) We have set the course for 2020 (Frank Appel) Financial results Q3 2014

Commerzbank Sector Conference. Arnd Zinnhardt CFO. August 28, Software AG. All rights reserved.

Commerzbank 2013 Sector Conference Arnd Zinnhardt CFO August 28, 2013 Safe-Harbor-Statement This presentation contains forward-looking statements based on beliefs of Software AG management. Such statements

Commerzbank 2013 Sector Conference Arnd Zinnhardt CFO August 28, 2013 Safe-Harbor-Statement This presentation contains forward-looking statements based on beliefs of Software AG management. Such statements

Supply Chain Networks: Best Practices and Emerging Trends

Global S u p p l y C h a i n s Supply Chain Networks: Best Practices and Emerging Trends N. Viswanadham Deputy Executive Director, The Logistics Institute Asia Pacific National University of Singapore

Global S u p p l y C h a i n s Supply Chain Networks: Best Practices and Emerging Trends N. Viswanadham Deputy Executive Director, The Logistics Institute Asia Pacific National University of Singapore

QAD Inc. Corporate Update March 2015

QAD Inc. Corporate Update March 2015 Disclaimer Safe Harbor This presentation includes forward-looking statements about QAD and its business. These statements are subject to risks and uncertainties that

QAD Inc. Corporate Update March 2015 Disclaimer Safe Harbor This presentation includes forward-looking statements about QAD and its business. These statements are subject to risks and uncertainties that

Full year 2014 results

Listen-only live audio webcast available from www.gemalto.com/investors Full year 2014 results March 5, 2015 Olivier Piou, CEO Jacques Tierny, CFO Disclaimer This communication does not constitute an offer

Listen-only live audio webcast available from www.gemalto.com/investors Full year 2014 results March 5, 2015 Olivier Piou, CEO Jacques Tierny, CFO Disclaimer This communication does not constitute an offer

Continued Growth Ströer Out-of-Home Media AG Investor Presentation Roadshow Stockholm, June

Continued Growth Ströer Out-of-Home Media AG Investor Presentation Roadshow Stockholm, June 7 2011 1 # 1 in underpenetrated and attractive growth markets #1 in GERMANY Europe s largest ad. market #1 in

Continued Growth Ströer Out-of-Home Media AG Investor Presentation Roadshow Stockholm, June 7 2011 1 # 1 in underpenetrated and attractive growth markets #1 in GERMANY Europe s largest ad. market #1 in

Lighting Strategy. Key takeaways. We continue to grow at mid single digit and are taking decisive actions to address margin issues

Lighting Strategy Frans van Houten a.i. CEO Philips Lighting 2 3 Key takeaways 24 1 Key takeaways 25 We have undertaken actions to address issues with our performance Results impacted by Slower market

Lighting Strategy Frans van Houten a.i. CEO Philips Lighting 2 3 Key takeaways 24 1 Key takeaways 25 We have undertaken actions to address issues with our performance Results impacted by Slower market

2011 THIRD-QUARTER EARNINGS

2011 THIRD-QUARTER EARNINGS Paris, November 14th, 2011-8:00 am CET Board of Directors meeting on November 10th, 2011 Revenues: 54.5 million euros, down 20% compared with the third quarter of 2010, linked

2011 THIRD-QUARTER EARNINGS Paris, November 14th, 2011-8:00 am CET Board of Directors meeting on November 10th, 2011 Revenues: 54.5 million euros, down 20% compared with the third quarter of 2010, linked

Telefónica O2 Czech Republic

Telefónica O2 Czech Republic Quarterly Results January December 2008 24 th February, 2009 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Telefónica O2 Czech Republic Quarterly Results January December 2008 24 th February, 2009 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Logistics & Distribution: Revenue driver or necessary evil? Deloitte Introduction. Logistics & Distribution A source of competitive advantage

Logistics & Distribution: Revenue driver or necessary evil? Deloitte Introduction Logistics & Distribution A source of competitive advantage September 2017 Deloitte 2017 1 In a constantly changing environment

Logistics & Distribution: Revenue driver or necessary evil? Deloitte Introduction Logistics & Distribution A source of competitive advantage September 2017 Deloitte 2017 1 In a constantly changing environment

Telefónica Czech Republic

Telefónica Czech Republic Quarterly Results January December 2013 26 th February 2014 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Telefónica Czech Republic Quarterly Results January December 2013 26 th February 2014 CAUTIONARY STATEMENT Any forward-looking statements concerning future economic and financial performance of Telefónica

Business Area Components Technology

Components Technology within ThyssenKrupp Sales share 1 6.2 bn sales 28,941 employees AM IS We stand for o Mission critical components for global MX 14% Components Technology o automotive and industry

Components Technology within ThyssenKrupp Sales share 1 6.2 bn sales 28,941 employees AM IS We stand for o Mission critical components for global MX 14% Components Technology o automotive and industry