Profit Centers. By Kornél Tóth

|

|

|

- Douglas Rice

- 6 years ago

- Views:

Transcription

1 Profit Centers By Kornél Tóth

2 profit center When a responsibility center s financial performance is measured in terms of profit (i.e., by the difference between the revenues and expenses), the center is called a profit center. Profit is a particularly useful performance measure since it allows senior management to use one comprehensive indicator rather than several (some of which may be pointing in different directions)

3 General Considerations A functional organization is one in which each principal manufacturing or marketing function is performed by a separate organization unit. When such an organization is converted to one in which each major unit is responsible for both the manufacture and the marketing, the process is termed divisionalization companies create business units because they have decided to delegate more authority to operating managers

4 Conditions for Delegating Profit Responsibility Many management decisions involve proposals to increase expenses with the expectation of an even greater increase in sales revenue. Such decisions are said to involve expense/revenue trade-offs Additional advertising expense is an example. Before it is safe to delegate such a trade-off decision to a lower level manager, two conditions should exist:

5 two conditions 1. The manager should have access to the relevant information needed for making such a decision. 2. There should be some way to measure the effectiveness of the trade-offs the manager has made

6 conditions A major step in creating profit centers is to determine the lowest point in an organization where these two conditions prevail. All responsibility centers fit into a continuum ranging from those thatvclearly should be profit centers to those that clearly should not. Management must decide whether the advantages of giving profit responsibility offset the disadvantages As with all management control system design choices, there is no clear line of demarcation

7 Prevalence of Profit Centers most companies in the United States remained functionally organized until after the end of World War II. Since that time many major U.S. corporations have divisionalized and have decentralized profit responsibility at the business unit level. Alfréd P. Sloan (General Motors) and Ralph J. Cordiner (General Electric) have documented the philosophy of divisionalization and profit decentralization. In a survey of Fortune 1,000 companies in the United States, of the 638 usable responses, 93 percent were from companies that included two or more profit centers

8 Advantages of Profit Centers The quality of decisions may improve because they are being made by managers closest to the point of decision. The speed of operating decisions may be increased since they do not have to be referred to corporate headquarters. Headquarters management, relieved of day-today decision making, can concentrate on broader issues.

9 Advantages of Profit Centers Managers, subject to fewer corporate restraints, are freer to use their imagination and initiative. Because profit centers are similar to independent companies, they provide an excellent training ground for general management. Their managers gain experience in managing all functional areas, and upper management gains the opportunity to evaluate their potential for higher-level jobs

10 Advantages of Profit Centers Profit consciousness is enhanced since managers who are responsible for profits will constantly seek ways to increase them. (a manager responsible for marketing activities, for example, will tend to authorize promotion expenditures that increase sales, whereas a manager responsible for profits will be motivated to make promotion expenditures that increase profits.) Profit centers provide top management with readymade information on the profitability of the company s individual components. Because their output is so readily measured, profit centers are particularly responsive to pressures to improve their competitive performance

11 Difficulties with Profit Centers Decentralized decision making will force top management to rely more on management control reports than on personal knowledge of an operation, entailing some loss of control. If headquarters management is more capable or better informed than the average profit center manager, the quality of decisions made at the unit level may be reduced.

12 Difficulties with Profit Centers Friction may increase because of arguments over the appropriate transfer price, the assignment of common costs, and the credit for revenues that were formerly generated jointly by two or more business units working together. Organization units that once cooperated as functional units may now be in competition with one another. An increase in profits for one manager may mean a decrease for another. In such situations, a manager may fail to refer sales leads to another business unit better qualified to pursue them; may hoard personnel or equipment that, from the overall company standpoint, would be better off used in another unit; or may make production decisions that have undesirable cost consequences for other units

13 Difficulties with Profit Centers Divisionalization may impose additional costs because of the additional management, staff personnel, and record keeping required, and may lead to task redundancies at each profit center Competent general managers may not exist in a functional organization because there may not have been sufficient opportunities for them to develop general management competence

14 Difficulties with Profit Centers There may be too much emphasis on short-run profitability at the expense of long-run profitability. In the desire to report high current profits, the profit center manager may skimp on R&D, training programs, or maintenance. This tendency is especially prevalent when the turnover of profit center managers is relatively high. In these circumstances, managers may have good reason to believe that their actions may not affect profitability until after they have moved to other jobs. There is no completely satisfactory system for ensuring that optimizing the profits of each individual profit center will optimize the profits of the company as a whole

15 Business Units as Profit Centers

16 Business Units as Profit Centers Most business units are created as profit centers since managers in charge of such units typically control product development, manufacturing, and marketing resources. These managers are in a position to influence revenues and costs and can be held accountable for the bottom line. a business unit manager s authority may be constrained in various ways, which ought to be reflected in a profit center s design and operation.

17 Constraints on Business Unit Authority To realize fully the benefits of the profit center concept, the business unit manager would have to be as autonomous as the president of an independent company. such autonomy is not feasible If a company were divided into completely independent units, the organization would lose the advantages of size and synergy.

18 Constraints on Business Unit Authority in delegating to business unit management all the authority that the board of directors has given to the CEO, senior management would be abdicating its own responsibility. business unit structures represent trade-offs between business unit autonomy and corporate constraints The effectiveness of a business unit organization is largely dependent on how well these trade-offs are made

19 Constraints from Other Business Units One of the main problems occurs when business units must deal with one another. It is useful to think of managing a profit center in terms of control over three types of decisions:

20 Constraints from Other Business Units (1) the product decision (what goods or services to make and sell), (2) the marketing decision (how, where, and for how much are these goods or services to be sold?), and (3) the procurement or sourcing decision (how to obtain or manufacture the goods or services).

21 Constraints from Other Business Units If a business unit manager Controls all three activities, there is usually no difficulty in assigning profit responsibility and measuring performance. the greater the degree of integration within a company, the more difficult it becomes to assign responsibility to a single profit center for all three activities in a given product line;

22 Constraints from Corporate Management The constraints imposed by corporate management can be grouped into three types: (1) those resulting from strategic considerations, (2) those resulting because uniformity is required, and (3) those resulting from the economies of centralization.

23 Constraints from Corporate Management Most companies retain certain decisions, especially financial decisions, at the corporate level, at least for domestic activities. one of the major constraints on business units results from corporate control over new investments. Business units must compete with one another for a share of the available funds

24 Constraints from Corporate Management Thus, a business unit could find its expansion plans thwarted because another unit has convinced senior management that it has a more attractive program. Corporate management also imposes other constraints. Each business unit has a charter that specifies the marketing and/or production activities that it is permitted to undertake, and it must refrain from operating beyond its charter, even though it sees profit opportunities in doing so. Also, the maintenance of the proper corporate image may require constraints on the quality of products or on public relations activities

25 Constraints from Corporate Management Companies impose some constraints on business units because of the necessity for uniformity. One constraint is that business units must conform to corporate accounting and management control systems. This constraint is especially troublesome for units that have been acquired from another company and that have been accustomed to using different systems.

26 uniformity Corporate headquarters may also impose uniform pay and other personnel policies uniform policies on ethics, vendor selection, computers and communication equipment, even the design of the business unit s letterhead

27 corporate constraints corporate constraints do not cause severe problems in a decentralized structure as long as they are dealt with explicitly; business unit management should understand the necessity for most constraints and should accept them with good grace. The major problems seem to revolve around corporate service activities. Often business units believe (sometimes rightly) that they can obtain such services at less expense from an outside source.

28 Other Profit Centers (Examples of profit centers, other than business units)

29 Functional Units Multibusiness companies are typically divided into business units, each of which is treated as an independent profitgenerating unit. the subunits within these business units, however, may be functionally organized It is sometimes desirable to constitute one or more of the functional units e.g., marketing, manufacturing, and service operations as profit centers

30 Functional Units There is no guiding principle declaring that certain types of units are inherently profit centers and others are not Management s decision as to whether a given unit should be a profit center is based on the amount of influence (even if not total control) The unit s manager exercises over the activities that affect the bottom line

31 Marketing A marketing activity can be turned into a profit center by charging it with the cost of the products sold. This transfer price provides the marketing manager with the relevant information to make the optimum revenue/cost trade-offs, and the standard practice of measuring a profit center s manager by the center s profitability provides a check on how well these trade-offs have been made.

32 Marketing The transfer price charged to the profit center should be based on the standard cost, rather than the actual cost, of the products being sold. Using a standard cost base separates the marketing cost performance from that of the manufacturing cost performance, which is affected by changes in the levels of efficiency that are beyond the control of the marketing manager.

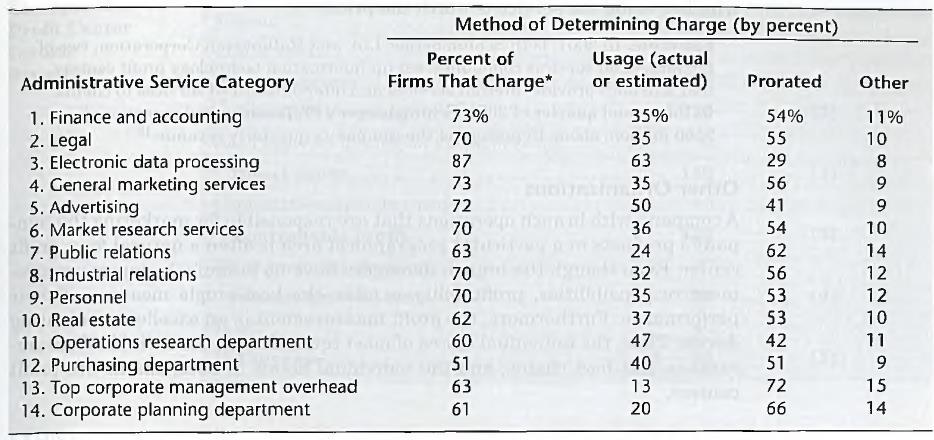

33 Marketing When should a marketing activity be given profit responsibility? When the marketing manager is in the best position to make the principal cost/revenue trade-offs. This often occurs where different conditions exist in different geographical areas for example, a foreign marketing activity.

34 cost/revenue trade-offs In such an activity, it may be difficult to control centrally such decisions as how to market a product; how to set the price; how much to spend on sales promotion, when to spend it, and on which media; how to train salespeople or dealers; where and when to establish new dealers

35 Manufacturing The manufacturing activity is usually an expense center, with the management being judged on performance versus standard costs and overhead budgets This measure can cause problems, since it does not necessarily indicate how well the manager is performing all aspects of his job.

36 Examples A manager may skimp on quality control, shipping products of inferior quality in order to obtain standard cost credit. A manager may be reluctant to interrupt production schedules in order to produce a rush order to accommodate a customer. A manager who is measured against standards may lack the incentive to manufacture products that are difficult to produce or to improve the standards themselves.

37 Manufacturing Therefore, where performance of the manufacturing process is measured against standard costs, it is advisable to make a separate evaluation of such activities as quality control, production scheduling, and make-or-buy decisions

38 Manufacturing as a profit center One way to measure the activity of a manufacturing organization in its entirety is to turn it into a profit center and give it credit for the selling price of the products minus estimated marketing expenses. Such an arrangement is far from perfect, partly because many of the factors that influence the volume and mix of sales are beyond the manufacturing manager s control. However, it seems to work better in some cases than the alternative of holding the manufacturing operation responsible only for costs

39 Manufacturing Some authors maintain that manufacturing units should not be made into profit centers unless they sell a large portion of their output to outside customers; they regard units that sell primarily to other business units as pseudo profit centers on the grounds that the revenues assigned to them for sales to other units within the company are artificial. Some companies, nevertheless, do create profit centers for such units. They believe that, if properly designed, the system can create almost the same incentives as those provided by sales to outside customers.

40 Service and Support Units Units for maintenance, information technology, transportation, engineering, Consulting, customer service, and similar support activities can all be made into profit centers. These may operate out of headquarters and service corporate divisions, or they may fulfill similar functions within business units. They charge customers for services rendered, with the financial objective of generating enough business so that their revenues equal their expenses.

41 examples

42 Service and Support Units When service units are organized as profit centers, their managers are motivated to control costs in order to prevent customers from going elsewhere while managers of the receiving units are motivated to make decisions about whether using the service is worth the price

43 Other Organizations A company with branch operations that are responsible for marketing the company s products in a particular geographical area is often a natural for a profit center. Even though the branch managers have no manufacturing or procurement responsibilities, profitability is often the best single measure of their performance. Furthermore, the profit measurement is an excellent motivating device. Examples: the individual stores of most retail chains, the individual restaurants in fast-food chains, and the individual hotels in hotel chains are profit centers.

44 Measuring Profitability

45 Measuring Profitability There are two types of profitability measurements used in evaluating a profit center, just as there are in evaluating an organization as a whole. First, there is the measure of management performance, which focuses on how well the manager is doing. This measure is used for planning, coordinating, and Controlling the profit center s day-to-day activities and as a device for providing the proper motivation for its manager

46 Measuring Profitability Second, there is the measure of economic performance, which focuses on how well the profit center is doing as an economic entity. The messages conveyed by these two measures may be quite different from each other. For example, the management performance report for a branch store May show that the store s manager is doing an excellent job under the circumstances, while the economic performance report may indicate that because of economic and competitive conditions in its area the store is a losing proposition and should be closed

47 Measuring Profitability The necessary information for both purposes usually cannot be obtained from a single set of data. Because the management report is used frequently, while the economic report is prepared only on those occasions when economic decisions must be made, considerations relating to management performance measurement have first priority in systems design that is, the system should be designed to measure management performance routinely, with economic information being derived from these performance reports as well as from other sources

48 Types of Profitability Measures A profit center s economic performance is always measured by net income (i.e., the income remaining after all costs, including a fair share of the corporate overhead, have been allocated to the profit center).

49 Profitability Measures The performance of the profit center manager may be evaluated by five different measures of profitability: (1) contribution margin, (2) direct profit, (3) controllable profit, (4) income before income taxes, or (5) net income.

50 Profit center income statement

51 Percentages of Companies Using Different Methods of Measuring Profit

52 (1) Contribution Margin Contribution margin reflects the spread between revenue and variable expenses. The principal argument in favour of using it to measure the performance of profit center managers is that since fixed expenses are beyond their control, managers should focus their attention on maximizing contribution

53 (1) Contribution Margin The problem with this argument is that its premises are inaccurate; in fact, almost all fixed expenses are at least partially controllable by the manager, and some are entirely controllable Presumably, senior management wants the profit center to keep these diseretionary expenses in line with amounts agreed on in the budget formulation process. A focus on the contribution margin tends to direct attention away from this responsibility. even if an expense, such as administrative salaries cannot be changed in the short run, the profit center manager is still responsible for controlling employees efficiency and productivity

54 (2) Direct Profit This measure reflects a profit center s contribution to the general overhead and profit of the Corporation. it incorporates all expenses either incurred by or directly traceable to the profit center, regardless of whether or not these items are within the profit center manager s control. Expenses incurred at headquarters, are not included in this calculation. A weakness of the direct profit measure is that it does not recognize the motivational benefit of charging headquarters costs

55 (3) Controllable Profit Headquarters expenses can be divided into two categories: controllable and noncontrollable The former category includes expenses that are controllable, at least to a degree, by the business unit manager information technology services, If these costs are included in the measurement system, profit will be what remains after the deduction of all expenses that may be influenced by the profit center manager. A major disadvantage of this measure is that because it excludes noncontrollable headquarters expenses it cannot be directly compared with either published data or trade association data reporting the profits of other companies in the industry.

56 (4) Income before Taxes In this measure, all corporate overhead is allocated to profit centers based on the relative amount of expense each profit center incurs. There are two arguments against such allocations. First, since the costs incurred by corporate staff departments such as finance, accounting, and human resource management are not controllable by profit center managers, these managers should not be held accountable for them. Second, it may be difficult to allocate corporate staff services in a manner that would properly reflect the amount of costs incurred by each profit center.

57 (4) Income before Taxes There are, however, three arguments in favor of incorporating a portion of corporate overhead into the profit centers performance reports. First, corporate service units have a tendency to increase their power base and to enhance their own excellence without regard to their effect on the company as a whole. Allocating corporate overhead costs to profit centers increases the likelihood that profit center managers will question these costs, thus serving to keep head office spending in check.

58 (4) Income before Taxes Second, the performance of each profit center will become more realistic and more readily comparable to the performance of competitors who pay for similar services. Finally, when managers know that their respective centers will not show a profit unless all costs, including the allocated share of corporate overhead, are recovered, they are motivated to make optimum long-term marketing decisions as to pricing, product mix, and so forth, that will ultimately benefit (and even ensure the viability of) the company as a whole

59 (4) Income before Taxes If profit centers are to be charged for a portion of corporate overhead, this item should be calculated on the basis of budgeted, rather than actual costs, This ensures that profit center managers will not complain about either the arbitrariness of the allocation or their lack of control over these costs, since their performance reports will show no variance in the overhead allocation

60 (5) Net Income Here, companies measure the performance of domestic profit centers according to the bottom line, the amount of net income after income tax. There are two principal arguments against using this measure: (1) aftertax income is often a constant percentage of the pretax income, in which case there would be no advantage in incorporating income taxes, and (2) since many of the decisions that affect income taxes are made at headquarters, it is not appropriate to judge profit center managers on the consequences of these decisions

61 (5) Net Income There are situations, however, in which the effective income tax rate does vary among profit centers. For example, foreign subsidiaries or business units with foreign operations may have different effective income tax rates. In other cases, profit centers may influence Income taxes through their installment credit policies, their decisions on acquiring or disposing of equipment, and their use of other generally accepted accounting procedures to distinguish gross income from taxable income. In these situations, it may be desirable to allocate income tax expenses to profit centers not only to measure their economic profitability but also to motivate managers to minimize tax liability

62 Revenues Choosing the appropriate revenue recognition method is important. Should revenues be recorded when an order is made, when an order is shipped, or when cash is received? In addition to that decision, there are other issues relating to common revenues that may require consideration. In some situations two or more profit centers may participate in a successful sales effort; ideally, each center should be given appropriate credit for its part in the transaction

63 Revenues-example a salesperson from Business Unit A may be the main company contact with a certain customer, but the orders the customer places with that salesperson may be for products carried by Business Unit B. The Unit A salesperson would not be likely to pursue such orders if all resulting revenues were credited to Unit B

64 Revenues-example Many companies do not devote a great deal of attention to solving these common revenue problems. They take the position that the identification of precise responsibility for revenue generation is too complicated to be practical, And that sales personnel must recognize they are working not only for their own profit center but also for the overall good of the company. Other companies attempt to untangle the responsibility for common sales by crediting the business unit that takes an order for a product handled by another unit with the equivalent of a brokerage commission or a finder s fee

P2 Performance Management

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) The standard cost of the actual hours worked was 3,493-85 = 3,408. At 12 per hour the actual hours worked

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) The standard cost of the actual hours worked was 3,493-85 = 3,408. At 12 per hour the actual hours worked

1. Organizational structure refers to the totality of a firm's organization.

Chapter 14 The Organization of International Business True / False Questions 1. Organizational structure refers to the totality of a firm's organization. True False 2. A firm's organizational culture refers

Chapter 14 The Organization of International Business True / False Questions 1. Organizational structure refers to the totality of a firm's organization. True False 2. A firm's organizational culture refers

IFRS Training. IAS 2 Inventories. Professional Advisory Services

IFRS Training IAS 2 Inventories Table of Contents Section 1 Overview 2 Scope 3 Definitions 4 Measurement 5 Perpetual Versus Periodic 6 Cost Formulas 7 Net Realizable Value 8 Recognition 9 Disclosure Section

IFRS Training IAS 2 Inventories Table of Contents Section 1 Overview 2 Scope 3 Definitions 4 Measurement 5 Perpetual Versus Periodic 6 Cost Formulas 7 Net Realizable Value 8 Recognition 9 Disclosure Section

Module Practical Application Checklist:

Module Practical Application Checklist: MODULE 1 The Practical Application Checklists outline specific workplace tasks, by competency area, that CASB students are able to perform upon completion of each

Module Practical Application Checklist: MODULE 1 The Practical Application Checklists outline specific workplace tasks, by competency area, that CASB students are able to perform upon completion of each

INTRODUCTION. Professional Accounting Supplementary School (PASS) Page 1

Page 1") INTRODUCTION Under the new CPA certification program, management accounting has become very important on the CFE and it will therefore be critical for students to have a strong grounding in this area.

INTRODUCTION Under the new CPA certification program, management accounting has become very important on the CFE and it will therefore be critical for students to have a strong grounding in this area.

Designing of Management Control Systems. Lecture 02 Kanchan Damithendra

Designing of Management Control Systems Lecture 02 Kanchan Damithendra Designing of MCS What the organization wants from each employee individually? (CEO to floor level) Key Steps- 1) Setting performance

Designing of Management Control Systems Lecture 02 Kanchan Damithendra Designing of MCS What the organization wants from each employee individually? (CEO to floor level) Key Steps- 1) Setting performance

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

Transfer Pricing Cost Accounting Horngreen, Datar, Foster

Transfer Pricing Why Transfer Prices? Decentralized firms Decision-making power delegated to subunit-managers Intermediate products transferred from one subunit to another need to be priced Transfer prices

Transfer Pricing Why Transfer Prices? Decentralized firms Decision-making power delegated to subunit-managers Intermediate products transferred from one subunit to another need to be priced Transfer prices

Sri Lanka Accounting Standard LKAS 2. Inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

integrate the concept of profit centers and the organization structure of an organization;

UNIT5 PROFIT CENTRES Profit Centres Objectives After you have studied this unit, you should be able to: understand the concept of profit centers; integrate the concept of profit centers and the organization

UNIT5 PROFIT CENTRES Profit Centres Objectives After you have studied this unit, you should be able to: understand the concept of profit centers; integrate the concept of profit centers and the organization

Expanding Formula Retail Controls: Economic Impact Report

Expanding Formula Retail Controls: Economic Impact Report Item #130788 Office of Economic Analysis February 12, 2014 Main Conclusions This economic impact report was prepared in response to a proposed

Expanding Formula Retail Controls: Economic Impact Report Item #130788 Office of Economic Analysis February 12, 2014 Main Conclusions This economic impact report was prepared in response to a proposed

Revenue for chemical manufacturers

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION

EN EN EN CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION 1. INTRODUCTION 1. The Lisbon European Council in March 2000 set a strategic goal for Europe

EN EN EN CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION 1. INTRODUCTION 1. The Lisbon European Council in March 2000 set a strategic goal for Europe

Part 1 Study Unit 6. Cost Allocation Techniques Jim Clemons, CMA

Part 1 Study Unit 6 Cost Allocation Techniques Jim Clemons, CMA Absorption versus Variable Costing You need to be able to answer the following: Under absorption costing, which cost are considered product

Part 1 Study Unit 6 Cost Allocation Techniques Jim Clemons, CMA Absorption versus Variable Costing You need to be able to answer the following: Under absorption costing, which cost are considered product

6 The following terms are used in this Standard with the meanings specified: Inventories are assets:

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

COMMUNICATION FROM THE COMMISSION CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION

EN EN EN COMMUNICATION FROM THE COMMISSION CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION 1. INTRODUCTION 1. The Lisbon European Council in March

EN EN EN COMMUNICATION FROM THE COMMISSION CRITERIA FOR THE COMPATIBILITY ANALYSIS OF TRAINING STATE AID CASES SUBJECT TO INDIVIDUAL NOTIFICATION 1. INTRODUCTION 1. The Lisbon European Council in March

CHAPTER 2 RETAIL STRATEGIC PLANNING AND OPERATIONS MANAGEMENT

CHAPTER 2 RETAIL STRATEGIC PLANNING AND OPERATIONS MANAGEMENT MULTIPLE CHOICE 1. is the anticipation and organization of what needs to be done to reach an objective. a. Analyzing b. Forecasting c. Planning

CHAPTER 2 RETAIL STRATEGIC PLANNING AND OPERATIONS MANAGEMENT MULTIPLE CHOICE 1. is the anticipation and organization of what needs to be done to reach an objective. a. Analyzing b. Forecasting c. Planning

Note on Marketing Arithmetic and Related Marketing Terms

Harvard Business School 574-082 Rev. April 29, 1983 Note on Marketing Arithmetic and Related Marketing Terms This note is about several terms and basic calculations used in the analysis of marketing problems.

Harvard Business School 574-082 Rev. April 29, 1983 Note on Marketing Arithmetic and Related Marketing Terms This note is about several terms and basic calculations used in the analysis of marketing problems.

P2 Performance Management September 2013 examination

Management Level Paper P2 Performance Management September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Management Level Paper P2 Performance Management September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

1. Market Definition, Measurement And Concentration

1. Market Definition, Measurement And Concentration 1.0 Overview A merger is unlikely to create or enhance market power or to facilitate its exercise unless it significantly increases concentration and

1. Market Definition, Measurement And Concentration 1.0 Overview A merger is unlikely to create or enhance market power or to facilitate its exercise unless it significantly increases concentration and

NEED TO KNOW. IFRS 15 Revenue from Contracts with Customers

NEED TO KNOW IFRS 15 Revenue from Contracts with Customers 2 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS 3 TABLE OF CONTENTS Table of contents 3 1. Introduction

NEED TO KNOW IFRS 15 Revenue from Contracts with Customers 2 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS 3 TABLE OF CONTENTS Table of contents 3 1. Introduction

Questions You Need To Answer Before Starting a Business. Presented by Burt Wallerstein

Questions You Need To Answer Before Starting a Business Presented by Burt Wallerstein Defining Your Business Model 1. What product or service are you selling? 2. Who s your target customer? 3. What customer

Questions You Need To Answer Before Starting a Business Presented by Burt Wallerstein Defining Your Business Model 1. What product or service are you selling? 2. Who s your target customer? 3. What customer

Mona Loa Malaysian Manufacturing cost per bag... $6.00 $5.00 Add markup at 30% Selling price per bag... $7.80 $6.50

Case 8-24 1. a. The predetermined overhead rate would be computed as follows: Expected manufacturing overhead cost $3,000,000 = Estimated direct labour-hours 50,000 DLHs =$60 per DLH b. The unit product

Case 8-24 1. a. The predetermined overhead rate would be computed as follows: Expected manufacturing overhead cost $3,000,000 = Estimated direct labour-hours 50,000 DLHs =$60 per DLH b. The unit product

Transfer Pricing. 2. Advantages and Disadvantages of Decentralization

Smeal College of Business Managerial Accounting: ACCTG 404 Pennsylvania State University Professor Huddart 1. Overview An essential feature of decentralized firms is responsibility centers (e.g., cost-,

Smeal College of Business Managerial Accounting: ACCTG 404 Pennsylvania State University Professor Huddart 1. Overview An essential feature of decentralized firms is responsibility centers (e.g., cost-,

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

EUROPEAN UNION ACCOUNTING RULE 9 INVENTORIES Page 2 of 9 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of inventories... 4 5. Measurement... 5 5.1 Cost of inventories... 5

Sri Lanka Accounting Standard-LKAS 2. Inventories

Sri Lanka Accounting Standard-LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard-LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Inventories IAS 2 IAS 2. IFRS Foundation

IAS 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

IAS 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

CMA Part 2 Financial Decision Making. Study Unit 9 - Decision Analysis and Risk Management Ronald Schmidt, CMA, CFM

CMA Part 2 Financial Decision Making Study Unit 9 - Decision Analysis and Risk Management Ronald Schmidt, CMA, CFM Objectives of the Class Use Marginal Analysis for Decision Making Calculate effect on

CMA Part 2 Financial Decision Making Study Unit 9 - Decision Analysis and Risk Management Ronald Schmidt, CMA, CFM Objectives of the Class Use Marginal Analysis for Decision Making Calculate effect on

Inventories. IAS Standard 2 IAS 2. IFRS Foundation

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

NOGDAWINDAMIN FAMILY AND COMMUNITY SERVICES

This dictionary describes the following six functional competencies and four enabling competencies that support the differentiated territory for professional accountants in strategic management accounting:

This dictionary describes the following six functional competencies and four enabling competencies that support the differentiated territory for professional accountants in strategic management accounting:

Revenue for retailers

Revenue for retailers The new standard s effective date is coming. US GAAP September 2017 kpmg.com/us/frv b Revenue for retailers Revenue viewed through a new lens Again and again, we are asked what s

Revenue for retailers The new standard s effective date is coming. US GAAP September 2017 kpmg.com/us/frv b Revenue for retailers Revenue viewed through a new lens Again and again, we are asked what s

IND AS 2 IND AS 2: INVENTORIES. Applies To All inventories excepta) Financial Instruments (Ind AS 32/ Ind AS 109)

Financial Instruments (Ind AS 32/ Ind AS 109)") IND AS 2: INVENTORIES 1. OBJECTIVE: The main objective of this standard is to prescribe accounting treatment of inventories and to determine cost of the inventories and its subsequent recognition as an

IND AS 2: INVENTORIES 1. OBJECTIVE: The main objective of this standard is to prescribe accounting treatment of inventories and to determine cost of the inventories and its subsequent recognition as an

Topic 2: Accounting Information for Decision Making and Control

Learning Objectives BUS 211 Fall 2014 Topic 1: Introduction Not applicable Topic 2: Accounting Information for Decision Making and Control State and describe each of the 4 items in the planning and control

Learning Objectives BUS 211 Fall 2014 Topic 1: Introduction Not applicable Topic 2: Accounting Information for Decision Making and Control State and describe each of the 4 items in the planning and control

Chapter 2 Functions and Types of Transfer Prices

Chapter 2 Functions and Types of Transfer Prices Abstract Transfer prices as the internal price of products created within the company have two main functions: profit allocation (in order to assess divisional

Chapter 2 Functions and Types of Transfer Prices Abstract Transfer prices as the internal price of products created within the company have two main functions: profit allocation (in order to assess divisional

Chapter 2 Lecture Notes Strategic Marketing Planning. Chapter 2: Strategic Marketing Planning

Chapter 2: I. Introduction A. Beyond the Pages 2.1 discusses several aspects of Ford s strategy to restructure its operating philosophy. B. Although the process of strategic marketing planning can be complex

Chapter 2: I. Introduction A. Beyond the Pages 2.1 discusses several aspects of Ford s strategy to restructure its operating philosophy. B. Although the process of strategic marketing planning can be complex

UNIT 4 RESPONSIBILITY CENTRES

UNIT 4 RESPONSIBILITY CENTRES Objectives After you have studied this unit, you should be able to: Responsibility Centres understand and explain the concept of responsibility centres in the context of an

UNIT 4 RESPONSIBILITY CENTRES Objectives After you have studied this unit, you should be able to: Responsibility Centres understand and explain the concept of responsibility centres in the context of an

STRAGETIC RISK MANUAL

Strategic Risk Manual 1 Unofficial Translation prepared by The Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language. Please refer to the Thai text

Strategic Risk Manual 1 Unofficial Translation prepared by The Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language. Please refer to the Thai text

MANAGERIAL MODELS OF THE FIRM

MANAGERIAL MODELS OF THE FIRM THE NEOCLASSICAL MODEL 1. Many Models of the firm based on different assumptions that could be described as economic models. 2. One particular version forms mainstream orthodox

MANAGERIAL MODELS OF THE FIRM THE NEOCLASSICAL MODEL 1. Many Models of the firm based on different assumptions that could be described as economic models. 2. One particular version forms mainstream orthodox

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC FORM 8-K/A MICROCHIP TECHNOLOGY INCORPORATED

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 June 8, 2016 (April 4, 2016) Date

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 June 8, 2016 (April 4, 2016) Date

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Allocation of Joint Costs

40 Part III Cost Management Systems For example, suppose that Jennifer determines that $400,000 of the fixed costs in Information Services is avoidable. When she evaluates bids from outside vendors, she

40 Part III Cost Management Systems For example, suppose that Jennifer determines that $400,000 of the fixed costs in Information Services is avoidable. When she evaluates bids from outside vendors, she

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

P2 Performance Management

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) (i) The optimum selling price occurs where marginal cost = marginal revenue. Marginal cost is assumed

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) (i) The optimum selling price occurs where marginal cost = marginal revenue. Marginal cost is assumed

Project Selection. Request for information systems are typically motivated by one of the following three general objectives :

Project Selection Reasons for project proposals Request for information systems are typically motivated by one of the following three general objectives : Solve a problem An activity, process or function

Project Selection Reasons for project proposals Request for information systems are typically motivated by one of the following three general objectives : Solve a problem An activity, process or function

GLOSSARY OF TERMS ENTREPRENEURSHIP AND BUSINESS INNOVATION

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP

DVM, MBA, CFP") VHMA 2013 Annual Meeting and Conference September 26-29, 2013 The Westin, Charlotte, NC Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP Inventory

VHMA 2013 Annual Meeting and Conference September 26-29, 2013 The Westin, Charlotte, NC Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP Inventory

University of Waterloo. Vershire Company. AFM 482: Performance Measurement and Organizational Control

University of Waterloo Vershire Company AFM 482: Performance Measurement and Organizational Control Team 8: Akua Acheampong, Lori Chin Suey, Kieng Iv, Tara Mathanda, Hubert Sy October 4, 2010 Table of

University of Waterloo Vershire Company AFM 482: Performance Measurement and Organizational Control Team 8: Akua Acheampong, Lori Chin Suey, Kieng Iv, Tara Mathanda, Hubert Sy October 4, 2010 Table of

Judge Assessment. Oregon Region: OR Fri Jul :26 PM

Accounting Applications Series Composite Score 75.00 out of 100 International 67.63 out of 100 Role Play 1 88.33 out of 100 International 74.30 out of 100 Explain the nature of accounts receivable. 14.67

Accounting Applications Series Composite Score 75.00 out of 100 International 67.63 out of 100 Role Play 1 88.33 out of 100 International 74.30 out of 100 Explain the nature of accounts receivable. 14.67

BUSINESS PLAN MANAGEMENT

BUSINESS PLAN MANAGEMENT Managing the Implementation of a Business Plan Learning Outcome 2 Propose the necessary procedures to effectively manage the implementation of a business plan. Assessment Criteria

BUSINESS PLAN MANAGEMENT Managing the Implementation of a Business Plan Learning Outcome 2 Propose the necessary procedures to effectively manage the implementation of a business plan. Assessment Criteria

NRV vs. FV NRV is entity-specific value; FV is not. NRV for inventories may not equal FV-CTS.

IAS 2 DEFINITIONS NRV FV are assets: (a) held for sale in the ordinary course of business (finished goods); (b) in the process of production for such sale (WIP); or (c) in the form of materials or supplies

IAS 2 DEFINITIONS NRV FV are assets: (a) held for sale in the ordinary course of business (finished goods); (b) in the process of production for such sale (WIP); or (c) in the form of materials or supplies

CORPORATE GOVERNANCE GUIDELINES

CORPORATE GOVERNANCE GUIDELINES [Translation] Chapter 1 General Provisions Article 1 Purpose These Guidelines set forth the Company s basic views and systems regarding corporate governance in order to

CORPORATE GOVERNANCE GUIDELINES [Translation] Chapter 1 General Provisions Article 1 Purpose These Guidelines set forth the Company s basic views and systems regarding corporate governance in order to

Corporate Governance. Corporate Philosophy: Mizuho's fundamental approach to business activities, based on the raison d etre of Mizuho

Corporate Governance Mizuho's Corporate Identity, which is composed of Corporate Philosophy, Vision and the Mizuho Values, serves as the concept that forms the basis of all activities conducted by MHFG.

Corporate Governance Mizuho's Corporate Identity, which is composed of Corporate Philosophy, Vision and the Mizuho Values, serves as the concept that forms the basis of all activities conducted by MHFG.

Full file at Job Order Costing and Analysis QUESTIONS

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

WELLS FARGO & COMPANY CORPORATE GOVERNANCE GUIDELINES

WELLS FARGO & COMPANY CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Wells Fargo & Company (the Company ), based on the recommendation of its Governance and Nominating Committee,

WELLS FARGO & COMPANY CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of Wells Fargo & Company (the Company ), based on the recommendation of its Governance and Nominating Committee,

Current Developments in Loyalty Accounting 2015 IAAIA Conference October 2015

Current Developments in Loyalty Accounting 2015 IAAIA Conference October 2015 Topics Loyalty overview and current developments Common issues Separation transactions Deferral models and accounting for breakage

Current Developments in Loyalty Accounting 2015 IAAIA Conference October 2015 Topics Loyalty overview and current developments Common issues Separation transactions Deferral models and accounting for breakage

CANADIAN NATURAL RESOURCES LIMITED (the Corporation ) BOARD OF DIRECTORS CORPORATE GOVERNANCE GUIDELINES

BOARD OF DIRECTORS CORPORATE GOVERNANCE GUIDELINES") CANADIAN NATURAL RESOURCES LIMITED (the Corporation ) BOARD OF DIRECTORS CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of the Corporation has adopted the following Corporate Governance

CANADIAN NATURAL RESOURCES LIMITED (the Corporation ) BOARD OF DIRECTORS CORPORATE GOVERNANCE GUIDELINES The Board of Directors (the Board ) of the Corporation has adopted the following Corporate Governance

THE FIRST OF LONG ISLAND CORPORATION CORPORATE GOVERNANCE GUIDELINES

PURPOSE AND BOARD RESPONSIBILITIES The purpose of these Corporate Governance Guidelines is to continue a long-standing commitment to good corporate governance practices by The First of Long Island Corporation

PURPOSE AND BOARD RESPONSIBILITIES The purpose of these Corporate Governance Guidelines is to continue a long-standing commitment to good corporate governance practices by The First of Long Island Corporation

The papers submitted by many candidates were good but some well documented weaknesses once again appeared.

Paper P Performance Management May 011 Exam General Comments The overall performance was a little disappointing, especially as the paper contained topics that had been tested in several recent papers such

Paper P Performance Management May 011 Exam General Comments The overall performance was a little disappointing, especially as the paper contained topics that had been tested in several recent papers such

Chapter 1: MANAGERS, PROFITS, AND MARKETS

Chapter 1: MANAGERS, PROFITS, AND MARKETS Essential Concepts 1. Managerial economics applies microeconomic theory the study of the behavior of individual economic agents to business problems in order to

Chapter 1: MANAGERS, PROFITS, AND MARKETS Essential Concepts 1. Managerial economics applies microeconomic theory the study of the behavior of individual economic agents to business problems in order to

TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS

SEPTEMBER 2014 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS u INTRODUCTION On May 28, 2014, the FASB issued its long-awaited standard,

SEPTEMBER 2014 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS u INTRODUCTION On May 28, 2014, the FASB issued its long-awaited standard,

CAS - 15 COST ACCOUNTING STANDARD ON SELLING AND DISTRIBUTION OVERHEADS

CAS - 15 COST ACCOUNTING STANDARD ON SELLING AND DISTRIBUTION OVERHEADS The following is the COST ACCOUNTING STANDARD -15 (CAS-15) issued by the Council of The Institute of Cost Accountants of India on

CAS - 15 COST ACCOUNTING STANDARD ON SELLING AND DISTRIBUTION OVERHEADS The following is the COST ACCOUNTING STANDARD -15 (CAS-15) issued by the Council of The Institute of Cost Accountants of India on

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Existence and Valuation of Inventories in the Context of the Historical Cost System

AUDIT GUIDANCE STATEMENT AGS 4 Existence and Valuation of Inventories in the Context of the Historical Cost System This Statement of Auditing Practice was approved by the Council of the Institute of Singapore

AUDIT GUIDANCE STATEMENT AGS 4 Existence and Valuation of Inventories in the Context of the Historical Cost System This Statement of Auditing Practice was approved by the Council of the Institute of Singapore

P2 Performance Management

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) (i) One of the reasons why the chart does not provide a useful summary of the budget data is inherent

Performance Pillar P2 Performance Management Examiner s Answers SECTION A Answer to Question One (a) (i) One of the reasons why the chart does not provide a useful summary of the budget data is inherent

Case 5:14-cv cr Document 33-7 Filed 09/11/14 Page 1 of 10

Case 5:14-cv-00117-cr Document 33-7 Filed 09/11/14 Page 1 of 10 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF VERMONT GROCERY MANUFACTURERS ASSOCIATION, et at, v. Plaintiffs. WILLIAM H. SORRELL,

Case 5:14-cv-00117-cr Document 33-7 Filed 09/11/14 Page 1 of 10 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF VERMONT GROCERY MANUFACTURERS ASSOCIATION, et at, v. Plaintiffs. WILLIAM H. SORRELL,

Paper P2 Performance Management (Russian Diploma) Post Exam Guide Nov 2012 Exam. General Comments

Post Exam Guide Nov 2012 Exam. General Comments") General Comments Generally, this examination was well attempted by most candidates and this is reflected in the high pass rate for this paper. Some candidates performed poorly in the longer questions (6

General Comments Generally, this examination was well attempted by most candidates and this is reflected in the high pass rate for this paper. Some candidates performed poorly in the longer questions (6

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Cambridge Assessment International Education Cambridge International Advanced Subsidiary and Advanced Level. Published

Cambridge Assessment International Education Cambridge International Advanced Subsidiary and Advanced Level BUSINESS 9609/1 Paper 1 Short Answer and Essay MARK SCHEME Maximum Mark: 40 Published This mark

Cambridge Assessment International Education Cambridge International Advanced Subsidiary and Advanced Level BUSINESS 9609/1 Paper 1 Short Answer and Essay MARK SCHEME Maximum Mark: 40 Published This mark

BREAK EVEN ANALYSIS EXERCISES

BREAK EVEN ANALYSIS EXERCISES Q.1. (a) is defined as the excess of price over available cost. It contributes towards the covering of the fixed costs and then towards the profit targets. It can be calculated

BREAK EVEN ANALYSIS EXERCISES Q.1. (a) is defined as the excess of price over available cost. It contributes towards the covering of the fixed costs and then towards the profit targets. It can be calculated

Corporate Governance Guidelines

Corporate Governance Guidelines The following Corporate Governance Guidelines have been adopted by the Board of Directors of Conduent Incorporated to assist the Board in the exercise of its responsibilities.

Corporate Governance Guidelines The following Corporate Governance Guidelines have been adopted by the Board of Directors of Conduent Incorporated to assist the Board in the exercise of its responsibilities.

The software revenue recognition picture begins to crystallize

Software Industry Revenue Recognition and the Revised Revenue Recognition Exposure Draft The software revenue recognition picture begins to crystallize As proposed in the November 2011 revised joint revenue

Software Industry Revenue Recognition and the Revised Revenue Recognition Exposure Draft The software revenue recognition picture begins to crystallize As proposed in the November 2011 revised joint revenue

Institute of Certified Management Accountants of Sri Lanka. Strategic Level May 2013 Examination. Risk & Control Strategy and Policy (RSP / SL 4 404)

") Copyright Reserved Serial No Strategic Level May 2013 Examination Examination Date : 5 th May 2013 Number of Pages : 07 Examination Time: 1.30 p:m. 4.30 p:m. Number of Questions: 05 Instructions to Candidates

Copyright Reserved Serial No Strategic Level May 2013 Examination Examination Date : 5 th May 2013 Number of Pages : 07 Examination Time: 1.30 p:m. 4.30 p:m. Number of Questions: 05 Instructions to Candidates

Final May Corporate Governance Guideline

Final May 2006 Corporate Governance Guideline Table of Contents 1. INTRODUCTION 1 2. PURPOSES OF GUIDELINE 1 3. APPLICATION AND SCOPE 2 4. DEFINITIONS OF KEY TERMS 2 5. FRAMEWORK USED BY CENTRAL BANK TO

Final May 2006 Corporate Governance Guideline Table of Contents 1. INTRODUCTION 1 2. PURPOSES OF GUIDELINE 1 3. APPLICATION AND SCOPE 2 4. DEFINITIONS OF KEY TERMS 2 5. FRAMEWORK USED BY CENTRAL BANK TO

Accounting for Overheads - Marginal Costing

Accounting for Overheads - Marginal Costing Marginal cost is the variable cost of one unit of product or service. Marginal costing is an alternative method of costing to absorption costing. In marginal

Accounting for Overheads - Marginal Costing Marginal cost is the variable cost of one unit of product or service. Marginal costing is an alternative method of costing to absorption costing. In marginal

TRUST & RELATIONAL CONTRACTING

TRUST & RELATIONAL CONTRACTING EXTRACT FROM MDL PAPER ON RELATIONAL CONTRACTING 1.0 THE RELEVANCE OF TRUST IN CONTRACTING 1.1 The role of trust in building relationships is fast gaining ground in the theory

TRUST & RELATIONAL CONTRACTING EXTRACT FROM MDL PAPER ON RELATIONAL CONTRACTING 1.0 THE RELEVANCE OF TRUST IN CONTRACTING 1.1 The role of trust in building relationships is fast gaining ground in the theory

Organizational capacity Assessment tool 1

Organizational capacity Assessment tool 1 Purpose This assessment tool is intended to guide HI staff and members of local structures to assess organisational capacity. The questions highlight three key

Organizational capacity Assessment tool 1 Purpose This assessment tool is intended to guide HI staff and members of local structures to assess organisational capacity. The questions highlight three key

Relevant Costs and Revenues

Harvard Business School 9-892-010 Rev. 08/05/94 Relevant Costs and Revenues Companies often use the information in their accounting and control systems for multiple purposes. These purposes can range from

Harvard Business School 9-892-010 Rev. 08/05/94 Relevant Costs and Revenues Companies often use the information in their accounting and control systems for multiple purposes. These purposes can range from

Anti-Corruption Compliance in Emerging Markets: A Resource Guide

Anti-Corruption Compliance in Emerging Markets: A Resource Guide Keith M. Korenchuk, Samuel M. Witten, Arthur Luk, Cristian R.C. Kelly arnoldporter.com Compliance Challenges in Emerging Markets Multinational

Anti-Corruption Compliance in Emerging Markets: A Resource Guide Keith M. Korenchuk, Samuel M. Witten, Arthur Luk, Cristian R.C. Kelly arnoldporter.com Compliance Challenges in Emerging Markets Multinational

Future revenues A$ A$6 500 Deduct future costs Operating income A$8 500 A$6 500

Chapter 8 DECISION MAKING AND RELEVANT INFORMATION 8-16 (20 min.) Disposal of assets 1. This is an unfortunate situation, yet the A$78 000 costs are irrelevant regarding the decision to re-machine or sold

Chapter 8 DECISION MAKING AND RELEVANT INFORMATION 8-16 (20 min.) Disposal of assets 1. This is an unfortunate situation, yet the A$78 000 costs are irrelevant regarding the decision to re-machine or sold

Purchasing and Supply Chain Management. Supplier Evaluation and Selection

Purchasing and Supply Chain Management Supplier Evaluation and Selection Class Objectives Present supplier evaluation and selection as a key part of the strategic sourcing process Understand how supply

Purchasing and Supply Chain Management Supplier Evaluation and Selection Class Objectives Present supplier evaluation and selection as a key part of the strategic sourcing process Understand how supply

Chapter 1. The Demand for Audit and Other Assurance Services

Solutions Manual Auditing and Assurance Services an Integrated Approach 15th Edition Alvin A. Arens Instant download and all chapters Auditing and Assurance Services an Integrated Approach 15th Edition

Solutions Manual Auditing and Assurance Services an Integrated Approach 15th Edition Alvin A. Arens Instant download and all chapters Auditing and Assurance Services an Integrated Approach 15th Edition

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

Technical Line FASB final guidance

No. 2017-11 9 May 2017 Technical Line FASB final guidance How the new revenue standard affects retail and consumer products entities In this issue: Overview... 1 Customer options for additional goods and

No. 2017-11 9 May 2017 Technical Line FASB final guidance How the new revenue standard affects retail and consumer products entities In this issue: Overview... 1 Customer options for additional goods and

COST COST OBJECT. Cost centre. Profit centre. Investment centre

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

Cost Accounting The Foundation of Management Control

Cost Accounting The Foundation of Management Control Management Activities One can view the management activities of all healthcare organizations, from the largest tertiary hospital system to the smallest

Cost Accounting The Foundation of Management Control Management Activities One can view the management activities of all healthcare organizations, from the largest tertiary hospital system to the smallest

For personal use only

ASX ANNOUNCEMENT 1 November 2016 Corporate Governance Statement 30 June 2016 The Board of Directors is committed to improving and achieving good standards of corporate governance and has established corporate

ASX ANNOUNCEMENT 1 November 2016 Corporate Governance Statement 30 June 2016 The Board of Directors is committed to improving and achieving good standards of corporate governance and has established corporate

Solution Manual for Auditing and Assurance Services 14th Edition by Arens

Chapter 1 Solution Manual for Auditing and Assurance Services 14th Edition by Arens Link download full: https://testbankservice.com/download/solutionmanual-for-auditing-and-assurance-services-14th-edition-by-arens/

Chapter 1 Solution Manual for Auditing and Assurance Services 14th Edition by Arens Link download full: https://testbankservice.com/download/solutionmanual-for-auditing-and-assurance-services-14th-edition-by-arens/

COST CONCEPTS IN DECISION MAKING

CHAPTER 2 COST CONCEPTS IN DECISION MAKING BASIC CONCEPTS & FORMULAE Basic Concepts 1. Relevant cost in decision making process: Costs which are relevant for a particular business option, which are not

CHAPTER 2 COST CONCEPTS IN DECISION MAKING BASIC CONCEPTS & FORMULAE Basic Concepts 1. Relevant cost in decision making process: Costs which are relevant for a particular business option, which are not

Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39

39") Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39 IRG PUBLIC CONSULTATION DOCUMENT Principles of Implementation and Best Practice

Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39 IRG PUBLIC CONSULTATION DOCUMENT Principles of Implementation and Best Practice

OECD MODEL TAX CONVENTION: COMMENTS ON REVISED DISCUSSION DRAFT INTERPRETATION AND APPLICATION OF ARTICLE 5 (PERMANENT ESTABLISHMENT)

") OECD MODEL TAX CONVENTION: COMMENTS ON REVISED DISCUSSION DRAFT INTERPRETATION AND APPLICATION OF ARTICLE 5 (PERMANENT ESTABLISHMENT) Section 2: Meaning of at the disposal of (paragraph 4.2 of the Commentary)

OECD MODEL TAX CONVENTION: COMMENTS ON REVISED DISCUSSION DRAFT INTERPRETATION AND APPLICATION OF ARTICLE 5 (PERMANENT ESTABLISHMENT) Section 2: Meaning of at the disposal of (paragraph 4.2 of the Commentary)

10th Meeting of the Advisory Expert Group on National Accounts, April 2016, Paris, France

SNA/M1.16/4 10th Meeting of the Advisory Expert Group on National Accounts, 13-15 April 2016, Paris, France Agenda item: 4 The Internet economy Introduction This paper presents the challenges which the

SNA/M1.16/4 10th Meeting of the Advisory Expert Group on National Accounts, 13-15 April 2016, Paris, France Agenda item: 4 The Internet economy Introduction This paper presents the challenges which the

Principles of Business Marketing and Finance (Grades: 9-12) 1st Six Weeks

1st Six Weeks") Principles of Business Marketing and Finance (Grades: 9-12) Semster Class Only International and Domestic Business: 1st Six Weeks (1)The student describes the characteristics of business. (A) Explain the

Principles of Business Marketing and Finance (Grades: 9-12) Semster Class Only International and Domestic Business: 1st Six Weeks (1)The student describes the characteristics of business. (A) Explain the

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE AGRIUM INC. CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE TABLE OF CONTENTS Page 1. Introduction... 1 2. Overview of Responsibilities: The Board and the Chief Executive

CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE AGRIUM INC. CHIEF EXECUTIVE OFFICER TERMS OF REFERENCE TABLE OF CONTENTS Page 1. Introduction... 1 2. Overview of Responsibilities: The Board and the Chief Executive

The importance of a transfer pricing system. Understanding that optimum TP we will lead to goal congruency

Transfer Pricing This Master Class will cover; A consideration of the theory The importance of a transfer pricing system Understanding the optimum transfer price Understanding that optimum TP we will lead

Transfer Pricing This Master Class will cover; A consideration of the theory The importance of a transfer pricing system Understanding the optimum transfer price Understanding that optimum TP we will lead

The Management of Marketing Profit: An Investment Perspective

The Management of Marketing Profit: An Investment Perspective Draft of Chapter 1: A Philosophy of Competition and An Investment in Customer Value Ted Mitchell, May 1 2015 Learning Objectives for Chapter

The Management of Marketing Profit: An Investment Perspective Draft of Chapter 1: A Philosophy of Competition and An Investment in Customer Value Ted Mitchell, May 1 2015 Learning Objectives for Chapter

Full file at

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice made to acquire it. True False 2. An expense is an expired cost matched with revenues in a specific

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice made to acquire it. True False 2. An expense is an expired cost matched with revenues in a specific

COMPETITION AUTHORITY OF KENYA GUIDELINES ON RELEVANT MARKET DEFINITION I. INTRODUCTION

COMPETITION AUTHORITY OF KENYA GUIDELINES ON RELEVANT MARKET DEFINITION I. INTRODUCTION 1. The purpose of these guidelines is to provide guidance as to how the Authority applies the concept of relevant

COMPETITION AUTHORITY OF KENYA GUIDELINES ON RELEVANT MARKET DEFINITION I. INTRODUCTION 1. The purpose of these guidelines is to provide guidance as to how the Authority applies the concept of relevant