6) The mailing must be postmarked by June 15. 7) If you have any questions please me at

|

|

|

- Abraham Robbins

- 6 years ago

- Views:

Transcription

1 Examination Instructions: 1) Answer the examination only after you have read the honesty pledge below. 2) The multiple choice section will be taken in WebCT and a tutorial for using WebCT is to be found at: 3) The multiple choice section of the examination will be available for you to take from midnight, June 7 through midnight, June 16. 4) Answer the essay questions on the exam itself. Do not use an electronic format there are too many graphs required. 5) Sign the Honesty Pledge below. Mail the essay section of the examination and the signed Honesty Pledge back to me at: Bradley K. Hobbs, Ph.D. Florida Gulf Coast University College of Business FGCU Boulevard South Fort Myers, FL ) The mailing must be postmarked by June 15. 7) If you have any questions please me at bhobbs@fgcu.edu Page 1

2 Honesty Pledge: Distance Learning Examination for ECO 5005 Summer 2002 CRN I have neither given nor received aid from any person on this examination. The work here is entirely my own. I understand that I can use the Thinkwell materials in an open book format. print name sign name Page 2

3 Name: A 1. The main criticism of the kinked - demand curve model is that it does not explain how firms reach the original price / output at the kink C 2. Demand is price inelastic if: A) The price of the good responds slightly to a quantity change. B) The demand curve shifts very little when a demand shifter changes. C) The percentage change in quantity demanded is relatively small in response to a relatively large percentage change in price. D) All of the above are true. C 3. Consumer preferences, prices of other goods, income, and demographic characteristics are often termed: A) Market technologies. B) Demand prices. C) Demand shifters. D) Supply determinants. A 4. A demand curve that is perfectly inelastic: A) Will be vertical. B) Will be horizontal. C) Will be upward sloping. D) Has an elasticity equal to 1 everywhere on the curve. B 5. The market for breakfast cereal contains hundreds of similar products, such as Fruit Loops, Corn Flakes, and Rice Krispies, that are considered to be different products by different buyers. This situation violates the perfect competition assumption of: A) Many buyers and sellers. B) Identical goods. C) Complete information. D) Ease of entry and exit. B 6. If steak and potatoes are complements, when the price of steak goes up, the demand curve for potatoes: A) Shifts to the right. B) Shifts to the left. C) Stays the same. D) Shifts to the right and then moves back. C 7. A perfectly competitive firm's total revenue: A) Curve is a straight, downward sloping line B) Curve has a slope equal to marginal cost. C) Is found by multiplying price by quantity sold by the firm. D) Is always above its total cost. Page 3

4 C 8. A perfectly competitive firm is a ; a monopoly is a. A) Price setter; price setter B) Price taker; price taker C) Price taker; price setter D) Price setter; price taker A 9. Perfect competition is a model of the market that assumes a large number of buyers and sellers engaged in the purchase and sale of identical goods. B 10. The statement that the minimum wage needs to be increased is a: A) Positive statement. B) Normative statement. C) Condition contained in the fallacy of false cause. D) Scientific conclusion based on marginal analysis. B 11. An increase in supply, with no change in demand, will lead to in equilibrium quantity and in equilibrium price. A) An increase; an increase B) An increase; a decrease C) A decrease; an increase D) A decrease; a decrease B 12. If a perfectly competitive firm sells 300 units of output at a market price of $1 per unit, its marginal revenue is: A) Less than $1. B) $1. C) More than $1 but less than $300. D) $300. C 13. Which of the following is true? A) Since there are few firms that match the conditions assumed in perfect competition, the model is not very useful. B) The model of perfect competition is a good example of the old adage, "That's O.K. in theory, but not in practice." C) Although few world markets meet the assumptions of perfect competition, the model is useful in analyzing real world forces that affect prices and outputs. D) The model of perfect competition comes very close to describing the real world. A 14. The shutdown point is where MC = minimum AVC. D 15. In a competitive market, a change in price of a product A) Will shift long run average cost B) Will shift short run marginal cost C) Will shift short run average total cost D) Will cause movement along short run marginal cost curve Page 4

5 B 16. The supply curve for the firm in perfect competition: A) Is the MC curve above the minimum of ATC? B) Tells the quantity produced at each price. C) Must result in a price greater than MR. D) Shows the outputs at which the firm makes an economic profit. A 17. Given that pizza is a normal good, if students' income at your college increases substantially, there would be: A) An increase in the demand for pizza. B) An increase in the quantity of pizza demanded. C) A decreases in the demand for pizza. D) No change in the demand for pizza. C 18. In the long run, all costs are: A) Fixed. B) Constant. C) Variable. D) Marginal. C 19. Which of the following is true regarding monopoly? A) Monopolies produce too much and charge too much from the standpoint of efficiency. B) Monopolies usually are economically efficient because they have economic profits with which to work. C) Monopolies produce too little and charge too much from the standpoint of efficiency. D) Monopolies create an efficiency problem but are not associated with an equity problem. B 20. Positive statements: A) Imply value judgments must be made. B) Are factual and can be tested. C) Deal with what ought to be. D) Are dealt with primarily in microeconomics. B 21. When the percentage change in quantity demanded is less than the percentage change in price: A) Demand is price elastic. B) Demand is price inelastic. C) An increase in price will result in lower total revenue. D) Total revenue will be zero at the midpoint of a linear demand curve. A 22. If marginal product is greater than average product, then average product must be rising. B 23. The property tax is a regressive tax. Page 5

6 C 24. Perfect competition is characterized by: A) Rivalry in advertising. B) Fierce quality competition. C) The inability of any one firm to influence price. D) Widely recognized brands. C 25. Perfect competition assumes that information about a product and its price is: A) Widely shared among buyers. B) Widely shared among sellers. C) Widely shared among both buyers and sellers. D) Costless. A 26. Product differentiation is a type of A) Non-price competition B) Price competition C) Collusion D) Price taking C 27. The concept of elasticity is most closely related to: A) The equilibrium price. B) The equilibrium quantity. C) A movement along the demand curve. D) A shift in the demand curve. B 28. A monopolist is not as good for society as a perfectly competitive firm because A) The monopolist does not sell the profit maximizing quantity B) Output is lower and price is higher than under competition C) Monopolist is inefficient D) The monopolist s costs are higher than in perfect competition A 29. If a firm in perfect competition sells 500 units of a product at $10 per unit, its marginal revenue per unit is $10. C 30. In making decisions about factor mix, a firm is seeking to: A) Maximize output. B) Maximize profits. C) Maximize profits within its budget constraint, much like a consumer maximizes utility within a budget constraint. D) Do all of the above. Page 6

7 Production Possibilities Schedule 1 Alternatives A B C D E F Consumer goods per period Capital goods per period B 31. (Exhibit: Production Possibilities Schedule 1) If the economy produces 10 units of capital goods per period, it also can produce at most unit(s) of consumer goods per period. A) 5 B) 4 C) 3 D) 2 A 32. In perfect competition P = MC and in monopoly P > MC. B 33. "Diminishing marginal returns, means that: A) Each additional unit of an input used will decrease output. B) Each additional unit of an input used will increase output, but by smaller and smaller amounts. C) Each additional unit of an input used will increase output by larger and larger amounts. D) The firm is maximizing profit. C 34. Economists know that a particular good can be classified as an inferior good if a (n) in buyers' income causes a (n). A) Increase; increase in demand B) Increase; increase in quantity demanded C) Increase; decrease in demand D) Decrease; decrease in demand B 35. The total product curve indicates the quantity of inputs needed to produce a given level of output. A 36. Firms seek to use factors in the most efficient way in order to maximize profits. A 37. Game theory is an analysis that provides insight into the behavior of firms in oligopoly. Page 7

8 A 38. The sum of fixed and variable costs is: A) Total cost. B) Marginal cost. C) Variable cost. D) Average cost. B 39. Profit maximization for a monopoly firm is where P = MC. B 40. The primary difference between a change in demand and a change in the quantity demanded is: A) A change in demand is a movement along the demand curve and a change in quantity demanded is a shift in the demand curve. B) A change in quantity demanded is a movement along the demand curve and a change in demand is a shift in the demand curve. C) Both a change in quantity demanded and a change in demand are shifts in the demand curve, only in different directions. D) Both a change in quantity demanded and a change in demand are movements along the demand curve, only in different directions. B 41. In a kinked demand curve model, the demand curve at prices greater than the kink is ; but the curve below the kink is A) Inelastic; elastic B) Elastic; inelastic C) Elastic; elastic D) Elastic; perfectly inelastic D 42. A firm becomes more capital-intensive when it: A) Reduces the ratio of output to capital. B) Increases the ratio of output to labor. C) Reduces the ratio of capital to labor. D) Increases the ratio of capital to labor. B 43. An increase in demand and a decrease in supply, will lead to a (n) in equilibrium quantity and a (n) in equilibrium price. A) Decrease; decrease B) Indeterminate change; increase C) Indeterminate change; decrease D) Increase; indeterminate change B 44. A monopoly firm enjoys a because it is protected by from. A) Weak position; barriers to entry; competition B) Privileged position; barriers to entry; competition C) Position that always achieves economic profit; competition; new entrants into the industry. D) All of the above are true. Page 8

9 D 45. When an action by one agent harms another outside of any market exchange, there is a (n): A) Public choice. B) Tax incidence. C) Transfer payment. D) External cost. A 46. The demand curve facing a monopolist is always: A) The same as the industry's demand curve. B) Perfectly elastic. C) Unit elastic. D) Perfectly inelastic. C 47. If: P 0 = $5, Q 0 = 120, P 1 = $6 and Q 1 = 84 the arc elasticity of demand will be approximately: A) 3.10 B) 1.33 C) 1.94 D) 2.25 B 48. If a university decreases the price of tickets to football games in order to collect more revenue, it is assuming that the demand for tickets is: A) Unstable. B) Price inelastic. C) Price elastic. D) Unit price elastic. A 49. The fundamental economic questions that every economic system must answer are: A) What, how, and for whom. B) What, why, and for whom. C) When, why, and for whom. D) How, when, and how much. D 50. Market power exists when a firm is A) A price setter B) Able to determine output level for the entire market C) Able to influence market price of its good D) All of the above A 51. Short Run cost curves are U-shaped due to: A) the law of diminishing marginal returns. B) the pricing of labor inputs. C) the initial over-utilization of fixed capital. D) the initial over-utilization of fixed labor. Page 9

10 B 52. If a monopolist sells 100 units for $10 each unit and has an average cost of $8 per unit, what is the firms total cost. A) 1000 B) 800 C) 200 D) None of the above D 53. Because of monopoly, consumers typically have: A) Fewer choices. B) Higher costs. C) Lower quality. D) All of the above. A 54. A price taker is a market participant who is able to accept or reject the market price but cannot alter it. A 55. The principle stating that, for virtually all goods and services, there is a negative relationship between price and quantity demanded, all other things unchanged, is the law of: A) Demand. B) Supply. C) Scarcity. D) Increasing costs. A 56. The assumptions of perfect competition imply that: A) Individuals in the market accept the market price as given. B) Individuals can influence the market price. C) The price will be a fair price. D) The price will be low. B 57. A monopolist is a: A) Price taker. B) Price setter. C) cost maximizer. D) quantity taker. A 58. An oligopoly is an industry dominated by a few firms. D 59. The marginal product of labor is: A) The change in output resulting from a 1 unit change in labor. B) The slope of the total product curve. C) Positive at some levels of input and negative at others. D) Described by all of the above. B 60. A monopolist will always be able to operate at a profit Page 10

11 A 61. A monopoly is a market characterized by: A) A product with no close substitutes. B) A single buyer and several sellers. C) A large number of small firms. D) A small number of large firms. D 62. The problem of scarcity is confronted by: A) Industrialized societies. B) Pre-industrialized societies. C) Societies governed by communist philosophies. D) All societies. B 63. A progressive tax takes a lower percentage of income as income rises. C 64. The production possibilities curve represents the fact that: A) The economy will automatically end up at full employment. B) An economy's productive capacity increases proportionally with its population. C) If all resources of an economy are being used efficiently, more of one good can be produced only if less of another good is produced. D) Economic production possibilities have no limit. A 65. An example of a positive statement is: A) The rate of unemployment is 4 percent. B) A high rate of economic growth is good for the country. C) Everyone in the country needs to be covered by national health insurance. D) Baseball players should not be paid higher salaries than the president of the United States. D 66. (Exhibit: Guns and Butter) The maximum amounts of guns and butter this economy can produce is: A) 18 units of guns and 0 units of butter per period. B) 0 units of guns and 20 units of butter per period. C) 16 units of guns and 12 units of butter per period. D) All of the above combinations are maximum possible combinations. Page 11

12 B 67. The Short Run market supply curve is constructed by the horizontal summation of of the individual firms, the shut down point A) Marginal cost curves, below B) Marginal cost curves, above C) Average variable cost curves, below D) Average variable cost curves, above A 68. Long run cost curves are always lower than short run cost curves because the firm has flexibility to change both capital and labor in the long run C 69. The demand curve in monopolistic competition is: A) downward sloping and relatively inelastic B) horizontal C) downward sloping and relatively elastic D) the same as the demand curve facing the firm under pure competition C 70. Suppose the MP of the last unit of capital hired equals 12 and the MP of the last unit of labor hired is equal to 16. If the price of capital is $8 per unit and the price of labor is $8 per unit, then the firm A) Is maximizing costs with this combination of factors B) Is maximizing profits with this combination of factors C) Should hire more labor and less capital to minimize its costs D) Should hire more capital and less labor to minimize its costs A 71. If a firm in monopolistic competition is producing at a level of output where MC > MR and they are profit maximizing they should: A) increase production levels B) decrease production levels C) increase prices D) decrease prices D 72. A key aspect of monopolistic competition is: A) horizontal demand curves facing each individual firm B) low barriers to entry C) product differentiation D) both B and C. C 73. Over the long run the level of economic profits in a monopolistically competitive industry A) is low, but sustainable B) zero, due to regulatory pressures C) zero, due to entry D) is above normal economic profits Page 12

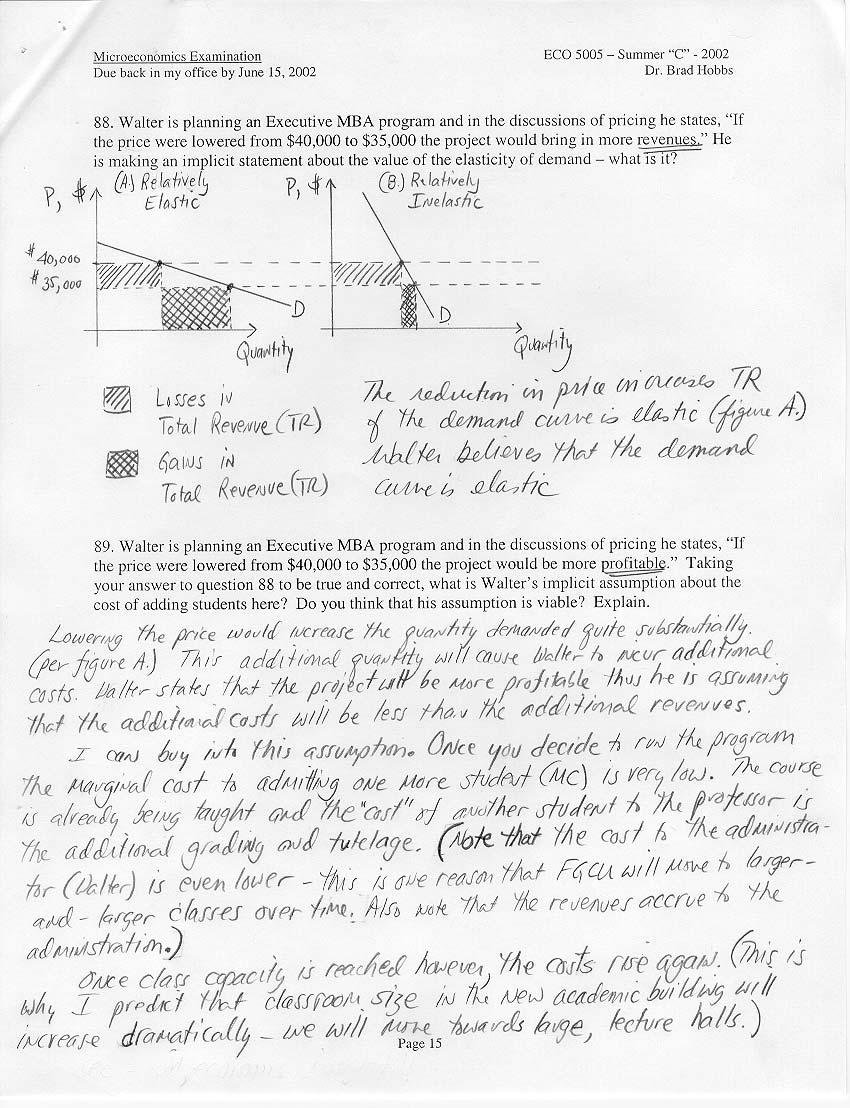

13 C 74. A Moral hazard may exist in a transaction when one party A) Has market power B) Is a monopolist C) Can take an unobservable post-transaction action that is potentially injurious to the other party D) Creates pollution with no cost to itself. B 75. When a public project is considered by a simple majority vote A) the project will never be undertaken B) the project will be undertaken even if total costs exceed total benefit C) the project will be undertaken only if total benefits exceed total cost D) The intensity of voter turn out is always taken into account A 76. For a market system to smoothly function property rights must be well defined and transferable. A 77. A risk adverse person would probably purchase life insurance C 78. The expected value of a gamble is A) The maximum potential payoff B) Equal to the amount wagered C) The average expected payoff if you repeatedly made the same gamble. D) Always less than the amount wagered D 79. The true social cost of an action is A) Private costs plus public costs B) Private benefits minus private costs C) External benefits minus external costs D) Private costs plus external costs. A 80. Sunk Costs A) Are expenditures made in the past that cannot be regained no matter what is done now or in the future. B) Are a component of variable costs, but not fixed costs. C) Represent best available foregone opportunities and therefore the firm's managers should consider these costs when they are making current decisions. D) Can be avoided only if the firm goes out of business Essay Section on the Next Page Page 13

14

15

16

17

18

19

Exam 3 Practice Questions

Exam 3 Practice Questions 1. The price elasticity of demand is a measure of: a) how quickly a particular market reaches equilibrium. b) the change in supply associated with lower prices. c) the percent

Exam 3 Practice Questions 1. The price elasticity of demand is a measure of: a) how quickly a particular market reaches equilibrium. b) the change in supply associated with lower prices. c) the percent

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

2007 Thomson South-Western

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

Market Structure & Imperfect Competition

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

Chapter 6. Competition

Chapter 6 Competition Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 Chapter 6 The goal of this

Chapter 6 Competition Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 Chapter 6 The goal of this

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following statements is correct? A) Consumers have the ability to buy everything

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following statements is correct? A) Consumers have the ability to buy everything

Slides and Images, Worth Publishers Inc. 8-1

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela

Practice Exam #4 Spring 2007 Dan Mallela") ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

Perfect Competition CHAPTER 14. Alfred P. Sloan. There s no resting place for an enterprise in a competitive economy. Perfect Competition 14

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

Monopolistic Competition

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

UNIT 4 PRACTICE EXAM

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

Refer to the information provided in Figure 12.1 below to answer the questions that follow. Figure 12.1

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

a. Sells a product differentiated from that of its competitors d. produces at the minimum of average total cost in the long run

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

Microeconomics. More Tutorial at

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Principles of Microeconomics Module 5.1. Understanding Profit

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

CLEP Microeconomics Practice Test

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

CHAPTER 8 Competitive Firms and Markets

CHAPTER 8 Competitive Firms and Markets CHAPTER OUTLINE 8.1 Competition Price Taking Why the Firm s Demand Curve Is Horizontal Why We Study Competition 8.2 Profit Maximization Profit Two Steps to Maximizing

CHAPTER 8 Competitive Firms and Markets CHAPTER OUTLINE 8.1 Competition Price Taking Why the Firm s Demand Curve Is Horizontal Why We Study Competition 8.2 Profit Maximization Profit Two Steps to Maximizing

Multiple Choice Part II, A Part II, B Part III Total

SIMON FRASER UNIVERSITY ECON 103 (2007-2) MIDTERM EXAM NAME Student # Tutorial # Multiple Choice Part II, A Part II, B Part III Total PART I. MULTIPLE CHOICE (56%, 1.75 points each). Answer on the bubble

SIMON FRASER UNIVERSITY ECON 103 (2007-2) MIDTERM EXAM NAME Student # Tutorial # Multiple Choice Part II, A Part II, B Part III Total PART I. MULTIPLE CHOICE (56%, 1.75 points each). Answer on the bubble

AGENDA Mon 10/12. Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp Q #7

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

Figure: Profit Maximizing

Name: Student ID: 1. A manufacturing company that benefits from lower costs per unit as it grows is an example of a firm experiencing: A) scale reduction. B) increasing returns to scale. C) increasing

Name: Student ID: 1. A manufacturing company that benefits from lower costs per unit as it grows is an example of a firm experiencing: A) scale reduction. B) increasing returns to scale. C) increasing

JANUARY EXAMINATIONS 2008

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

Chapter 10 Pure Monopoly

Chapter 10 Pure Monopoly Multiple Choice Questions 1. Pure monopoly means: A. any market in which the demand curve to the firm is downsloping. B. a standardized product being produced by many firms. C.

Chapter 10 Pure Monopoly Multiple Choice Questions 1. Pure monopoly means: A. any market in which the demand curve to the firm is downsloping. B. a standardized product being produced by many firms. C.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. FIGURE 1-2

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICRO EXAM REVIEW SHEET

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

Chapter 13. What will you learn in this chapter? A competitive market. Perfect Competition

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Graded exercise questions. Level (I, ii, iii)

") Graded exercise questions Level (I, ii, iii) 248 MICRO ECONOMICS LEVEL 1 GRADED EXERCISE QUESTIONS (LEVEL I, II, III) INTRODUCTION 1. Why does an economic problem arise? 2. What is economics about? 3.

Graded exercise questions Level (I, ii, iii) 248 MICRO ECONOMICS LEVEL 1 GRADED EXERCISE QUESTIONS (LEVEL I, II, III) INTRODUCTION 1. Why does an economic problem arise? 2. What is economics about? 3.

I enjoy teaching this class. Good luck and have a nice Holiday!!

ECON 202-501 Fall 2008 Xiaoyong Cao Final Exam Form A Instructions: The exam consists of 2 parts. Part I has 35 multiple choice problems. You need to fill the answers in the table given in Part II of the

ECON 202-501 Fall 2008 Xiaoyong Cao Final Exam Form A Instructions: The exam consists of 2 parts. Part I has 35 multiple choice problems. You need to fill the answers in the table given in Part II of the

Multiple choice questions 1-60 ( 1.5 points each)

") NAME: STUDENT ID: Final Exam ECON 101, Section 2 summer 2004 Ying Gao Instructions Please read carefully! 1. Print your name and student ID number at the top of this cover sheet. 2. Check that your exam

NAME: STUDENT ID: Final Exam ECON 101, Section 2 summer 2004 Ying Gao Instructions Please read carefully! 1. Print your name and student ID number at the top of this cover sheet. 2. Check that your exam

Principles of Economics Final Exam. Name: Student ID:

Principles of Economics Final Exam Name: Student ID: 1. In the absence of externalities, the "invisible hand" leads a competitive market to maximize (a) producer profit from that market. (b) total benefit

Principles of Economics Final Exam Name: Student ID: 1. In the absence of externalities, the "invisible hand" leads a competitive market to maximize (a) producer profit from that market. (b) total benefit

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

MONOPOLY. Characteristics

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

AP Microeconomics Review Session #3 Key Terms & Concepts

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

Instructions: must Repeat this answer on lines 37, 38 and 39. Questions:

Final Exam Student Name: Microeconomics, several versions Early May, 2011 Instructions: I) On your Scantron card you must print three things: 1) Full name clearly; 2) Day and time of your section (for

Final Exam Student Name: Microeconomics, several versions Early May, 2011 Instructions: I) On your Scantron card you must print three things: 1) Full name clearly; 2) Day and time of your section (for

Practice Exam 3 Questions

1. What is the main goal of a firm? A) To be as big as possible. B) To hire as many people as possible. C) To make as much profit as possible. D) All of the above answers are correct. Practice Exam 3 Questions

1. What is the main goal of a firm? A) To be as big as possible. B) To hire as many people as possible. C) To make as much profit as possible. D) All of the above answers are correct. Practice Exam 3 Questions

Use the following to answer question 4:

Homework Chapter 11: Name: Due Date: Wednesday, December 4 at the beginning of class. Please mark your answers on a Scantron. It is late if your Scantron is not complete when I ask for it at 9:35. Get

Homework Chapter 11: Name: Due Date: Wednesday, December 4 at the beginning of class. Please mark your answers on a Scantron. It is late if your Scantron is not complete when I ask for it at 9:35. Get

Economics : Principles of Microeconomics Spring 2014 Instructor: Robert Munk April 24, Final Exam

Economics 001.01: Principles of Microeconomics Spring 01 Instructor: Robert Munk April, 01 Final Exam Exam Guidelines: The exam consists of 5 multiple choice questions. The exam is closed book and closed

Economics 001.01: Principles of Microeconomics Spring 01 Instructor: Robert Munk April, 01 Final Exam Exam Guidelines: The exam consists of 5 multiple choice questions. The exam is closed book and closed

Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet. Class Day/Time

Answer Sheet. Class Day/Time") 1 Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet Name Class Day/Time Questions of this homework are in the next few pages. Please find the answer of the questions and fill in the blanks

1 Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet Name Class Day/Time Questions of this homework are in the next few pages. Please find the answer of the questions and fill in the blanks

Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011

Answer Key March 23, 2011") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Jacob: W hat if Framer Jacob has 10% percent of the U.S. wheat production? Is he still a competitive producer?

Microeconomics, Module 7: Competition in the Short Run (Chapter 7) Additional Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 9, 2005 Question 7.1: Pricing in a

Microeconomics, Module 7: Competition in the Short Run (Chapter 7) Additional Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 9, 2005 Question 7.1: Pricing in a

COST OF PRODUCTION & THEORY OF THE FIRM

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

1 of 14 5/1/2014 4:56 PM

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

Practice Test for Midterm 2 Econ Fall 2009 Instructor: Soojae Moon

Practice Test for Midterm 2 Econ 2010-200 Fall 2009 Instructor: Soojae Moon Please read carefully and choose the choice that best completes the statement or answers the question. Table 7-2 This table refers

Practice Test for Midterm 2 Econ 2010-200 Fall 2009 Instructor: Soojae Moon Please read carefully and choose the choice that best completes the statement or answers the question. Table 7-2 This table refers

Total revenue Quantity. Price Quantity Quantity

s in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. The goods offered by the various

s in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. The goods offered by the various

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION. 4. Is free medicine given to patients in Govt. Hospital a scarce commodity?

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

Chapter 14. Chapter Outline

Chapter 14 Labor Chapter Outline A Perfectly Competitive Firm s Demand for Labor Market Demand Curve for Labor An Imperfect Competitor s Demand for Labor Labor Supply Market Supply Curve Monopsony Minimum

Chapter 14 Labor Chapter Outline A Perfectly Competitive Firm s Demand for Labor Market Demand Curve for Labor An Imperfect Competitor s Demand for Labor Labor Supply Market Supply Curve Monopsony Minimum

Chapter Outline McGraw Hill Education. All Rights Reserved.

Chapter 14 Labor Chapter Outline A Perfectly Competitive Firm s Demand for Labor Market Demand Curve for Labor An Imperfect Competitor s Demand for Labor Labor Supply Market Supply Curve Monopsony Minimum

Chapter 14 Labor Chapter Outline A Perfectly Competitive Firm s Demand for Labor Market Demand Curve for Labor An Imperfect Competitor s Demand for Labor Labor Supply Market Supply Curve Monopsony Minimum

Chapter 28 The Labor Market: Demand, Supply, and Outsourcing

Chapter 28 The Labor Market: Demand, Supply, and Outsourcing Learning Objectives After you have studied this chapter, you should be able to 1. define marginal factor cost, marginal physical product of

Chapter 28 The Labor Market: Demand, Supply, and Outsourcing Learning Objectives After you have studied this chapter, you should be able to 1. define marginal factor cost, marginal physical product of

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

Bremen School District 228 Social Studies Common Assessment 2: Midterm

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

2) All combinations of capital and labor along a given isoquant cost the same amount.

All combinations of capital and labor along a given isoquant cost the same amount.") Micro Problem Set III WCC Fall 2014 A=True / B=False 15 Points 1) If MC is greater than AVC, AVC must be rising. 2) All combinations of capital and labor along a given isoquant cost the same amount. 3)

Micro Problem Set III WCC Fall 2014 A=True / B=False 15 Points 1) If MC is greater than AVC, AVC must be rising. 2) All combinations of capital and labor along a given isoquant cost the same amount. 3)

6. The law of diminishing marginal returns begins to take effect at labor input level: a. 0 b. X c. Y d. Z

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

ECON 251 Exam 2 Pink. Fall 2012

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008

Answer Key March 31, 2008") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Unit 4: Imperfect Competition

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics

External University of Karachi Micro-Economics") Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics Annual Examination 1997 Time allowed: 3 hours Marks: 100 Maximum 1) Attempt any five questions. 2) All questions

Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics Annual Examination 1997 Time allowed: 3 hours Marks: 100 Maximum 1) Attempt any five questions. 2) All questions

ECON December 4, 2008 Exam 3

Name Portion of ID# Multiple Choice: Identify the letter of the choice that best completes the statement or answers the question. 1. A fundamental source of monopoly market power arises from a. perfectly

Name Portion of ID# Multiple Choice: Identify the letter of the choice that best completes the statement or answers the question. 1. A fundamental source of monopoly market power arises from a. perfectly

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION. Professor Charles Fusi

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

Section I. Number of Workers. Total Gyros per Hour

MICROECONOMICS Section I Time 70 Minutes 60 Questions Directions: Each of the question or incomplete statements below is followed by five suggested answers or completions. Select the one that is best in

MICROECONOMICS Section I Time 70 Minutes 60 Questions Directions: Each of the question or incomplete statements below is followed by five suggested answers or completions. Select the one that is best in

MEPS Preparatory and Orientation Weeks. Lectures by Kristin Bernhardt. Master of Science in Economic Policy. March 2012

MEPS Preparatory and Orientation Weeks Master of Science in Economic Policy March 2012 Lectures by Kristin Bernhardt Fundamentals of Microeconomics 1. Introduction 2. Markets 3. Consumers and Households

MEPS Preparatory and Orientation Weeks Master of Science in Economic Policy March 2012 Lectures by Kristin Bernhardt Fundamentals of Microeconomics 1. Introduction 2. Markets 3. Consumers and Households

Sample. Final Exam Sample Instructor: Jin Luo

Final Exam Instructor: Jin Luo Multiple Choice (2 *30 = 60) Identify the letter of the choice that best completes the statement or answers the question. 1. Price takers refer to buyers and sellers in a.

Final Exam Instructor: Jin Luo Multiple Choice (2 *30 = 60) Identify the letter of the choice that best completes the statement or answers the question. 1. Price takers refer to buyers and sellers in a.

Do not open this exam until told to do so. Solution

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Fall 003 Final (Version): Intermediate Microeconomics (ECON30) Solution Final (Version

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Fall 003 Final (Version): Intermediate Microeconomics (ECON30) Solution Final (Version

GACE Economics Assessment Test at a Glance

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

Monopoly CHAPTER. Goals. Outcomes

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

A monopoly market structure is one characterized by a single seller of a unique product with no close substitutes.

These notes provided by Laura Lamb are intended to complement class lectures. The notes are based on chapter 12 of Microeconomics and Behaviour 2 nd Canadian Edition by Frank and Parker (2004). Chapter

These notes provided by Laura Lamb are intended to complement class lectures. The notes are based on chapter 12 of Microeconomics and Behaviour 2 nd Canadian Edition by Frank and Parker (2004). Chapter

Unit 4: Imperfect Competition

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation National Round I: Microeconomics David Ricardo Division 1. If your income tax liability is $15,000 and your income is $60,000, your A. average

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation National Round I: Microeconomics David Ricardo Division 1. If your income tax liability is $15,000 and your income is $60,000, your A. average

Introduction. Learning Objectives. Chapter 24. Perfect Competition

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Monopoly. Cost. Average total cost. Quantity of Output

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

ECON 101 Introduction to Economics1

ECON 101 Introduction to Economics1 Session 11 Market Structures(Perfect Competition) Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of

ECON 101 Introduction to Economics1 Session 11 Market Structures(Perfect Competition) Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of

Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007

Answer Key Nov 13, 2007") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and label

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key Nov 13, 2007 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and label

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot):

:") 1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

SIMON FRASER UNIVERSITY Department of Economics Sample Final Examination. PART I. Multiple Choice. Choose the best answer. (60% - 1 point each!

Econ 103 SIMON FRASER UNIVERSITY Department of Economics Sample Final Examination PART I. Multiple Choice. Choose the best answer. (60% - 1 point each!) PART 1: MULTIPLE CHOICE (answers are at the end

Econ 103 SIMON FRASER UNIVERSITY Department of Economics Sample Final Examination PART I. Multiple Choice. Choose the best answer. (60% - 1 point each!) PART 1: MULTIPLE CHOICE (answers are at the end

Monopolistic Competition

CHAPTER 16 Monopolistic Competition Goals in this chapter you will Examine market structures that lie between monopoly and competition Analyze competition among firms that sell differentiated products

CHAPTER 16 Monopolistic Competition Goals in this chapter you will Examine market structures that lie between monopoly and competition Analyze competition among firms that sell differentiated products

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

ECON 311 MICROECONOMICS THEORY I

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

Commerce 295 Midterm Answers

Commerce 295 Midterm Answers October 27, 2010 PART I MULTIPLE CHOICE QUESTIONS Each question has one correct response. Please circle the letter in front of the correct response for each question. There

Commerce 295 Midterm Answers October 27, 2010 PART I MULTIPLE CHOICE QUESTIONS Each question has one correct response. Please circle the letter in front of the correct response for each question. There

Economics 110 Final exam Practice Multiple Choice Qs Fall 2013

Final Exam Practice Multiple Choice Questions - ANSWER KEY Which of the following statements is not correct? a. Monopolistic competition is similar to monopoly because in each market structure the firm

Final Exam Practice Multiple Choice Questions - ANSWER KEY Which of the following statements is not correct? a. Monopolistic competition is similar to monopoly because in each market structure the firm

Pure Monopoly. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

10 Pure Monopoly McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Four Market Models Characteristics of the Four Basic Market Models Characteristic Number of firms

10 Pure Monopoly McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Four Market Models Characteristics of the Four Basic Market Models Characteristic Number of firms

The "competition" in monopolistically competitive markets is most likely a result of having many sellers in the market.

Chapter 16 Monopolistic Competition TRUE/FALSE 1. The "competition" in monopolistically competitive markets is most likely a result of having many sellers in the market. ANS: T 2. The "monopoly" in monopolistically

Chapter 16 Monopolistic Competition TRUE/FALSE 1. The "competition" in monopolistically competitive markets is most likely a result of having many sellers in the market. ANS: T 2. The "monopoly" in monopolistically

Monopolistic Competition. Chapter 17

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

The above Figure 1 shows the demand and cost curves facing a monopolist.

Practice 13&14 1) The key characteristics of a monopolistically competitive market structure include A) few sellers. B) sellers selling similar but differentiated products. C) high barriers to entry. D)

Practice 13&14 1) The key characteristics of a monopolistically competitive market structure include A) few sellers. B) sellers selling similar but differentiated products. C) high barriers to entry. D)

Question Paper Business Economics I (MB1B3): January 2009

: January 2009") Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

Competitive Markets. Chapter 5 CHAPTER SUMMARY

Chapter 5 Competitive Markets CHAPTER SUMMARY This chapter discusses the conditions for perfect competition. It also investigates the significance of competitive equilibrium in a perfectly competitive

Chapter 5 Competitive Markets CHAPTER SUMMARY This chapter discusses the conditions for perfect competition. It also investigates the significance of competitive equilibrium in a perfectly competitive

ECON 2100 (Summer 2009 Section 06) Final Exam. Multiple Choice Questions: (2 points each)

Final Exam. Multiple Choice Questions: (2 points each)") ECON 2100 (Summer 2009 Section 06) Final Exam Multiple Choice Questions: (2 points each) 1. Price Elasticity of Demand is defined as A. the unique price at which Total Consumer Expenditures on a good are

ECON 2100 (Summer 2009 Section 06) Final Exam Multiple Choice Questions: (2 points each) 1. Price Elasticity of Demand is defined as A. the unique price at which Total Consumer Expenditures on a good are