1 Although the relative export price on a contract currency basis should normally be used, the dollar-based

|

|

|

- Coleen Hines

- 6 years ago

- Views:

Transcription

1 Part II Strengthening Japan s competitiveness by taking advantage of its robustness Chapter 1 Analysis: Japan s competitive advantage in cross-border activities Section 1 Competitiveness in exports 1. Decomposition of the changes in Japan s goods exports In Part I, Chapter I, it was mentioned that Japan has continued to record a trade deficit since 2011 and that in 2014, the expansion of the trade deficit is starting to be arrested as the volume of exports resumed growing. Below, in light of this trend in Japan s trade in recent years, the causes of changes in the export volume of goods from Japan will be identified. (1) Price competitiveness and export volume Figure II shows a comparison between changes in Japan s relative export price (relative to export prices in the world and developed countries, dollar-based, year-on-year changes) and the real effective exchange rate (year-on-year changes). The relative export price refers to the ratio of Japan s export price (dollar-based) to the world export price (dollar-based), with a rise in the relative export price indicating a decline in the price competitiveness of Japanese export goods and a drop in the price indicating an improvement of the price competitiveness 1. The yen s real effective exchange rate is an indicator of the potential price competitiveness of Japan s export goods. When measuring Japan s international competitiveness, it is desirable to use the yen s real exchange rate, which takes account of changes in product prices in trading partner countries, rather than merely looking at nominal exchange rate movements. Also, in order to examine Japan s competitive relationship in the entire global market, it is necessary to use the yen s effective exchange rate, which takes account of its exchange rate movements relative to a basket of currencies, rather than against a single foreign currency. As the real effective exchange rate takes account of these two points, it is a better indicator of Japan s international competitiveness than the nominal exchange rate relative to a single foreign currency 2. When the yen s exchange rate rises relative to the basket of currencies, the real effective exchange rate rises accordingly if there is not any difference between the inflation rates in Japan and the trading partner countries. In this case, it can be said that the potential price competitiveness of Japan s export goods declines. Conversely, when the yen s exchanges rate drops, the real effective exchange rate falls accordingly. In this case, it can be said that the potential price competitiveness of Japan s export goods increases. Potential refers to a such situation that the actual price competitiveness does not change unless companies revise their sales prices. A closer look at the relationship between corporate price-setting 1 Although the relative export price on a contract currency basis should normally be used, the dollar-based relative export price is used here due to data constraints. In Japan s case, around 40 of export transactions are settled in yen in terms of value, so it should be kept in mind that the calculation of dollar-based export prices is directly affected by changes in the dollar-yen exchange rate. 2 From Ito et al. (2011). 91

2 behavior and exchange rate movements will be shown below. Figure II Changes in real effective exchange rate and relative export price (Year-on-year change, ) Relative export prices (in the world) Relative export prices (in developed countries) Real effective exchange rate Decline in price competitiveness Improvement of price competitiveness Notes: Relative export price = Japan s export price (dollar-based) / world (developed countries) export price (dollar-based) Source: BIS, IFS (IMF). (Year) Generally speaking, when the yen s real effective exchange rate is rising, Japanese companies suffer a drop in profits unless they raise their sales prices abroad. That is because when the yen strengthens relative to other currencies, the yen-based value of overseas sales prices declines. To mitigate the effects of the reduced margin, it is necessary to raise overseas sales prices 3. Consequently, when the yen s real effective exchange rate is rising, an increasing number of Japanese companies are expected to raise their overseas sales prices (which means a decline in their price competitiveness in the relevant countries). Conversely, when the real effective exchange rate is declining, there is room for lowering overseas sales prices while keeping the profit margin unchanged. Consequently, when the real effective exchange rate is declining, an increasing number of Japanese companies are expected to lower their overseas sales prices (which means an improvement in their price competitiveness in the relevant countries). Although there are analytical limits, such as the susceptibility of export prices in the world and in developed countries to the effects of international prices of crude oil and other commodities, Figure shows that Japan s real effective exchange rate has mostly been moving in parallel with the relative export price. 3 Cabinet Office (2004), Chapter 3, Section 2. 92

3 Other factors being equal, it is not until Japanese companies slash their overseas sales prices against the backdrop of an improvement in their potential price competitiveness (a decline in their real effective exchange rates) when their overseas sales volume increases, and consequently their export volume increases. However, the figure also shows that during periods of significant exchange rate movements, such as the yen s strengthening in 2009 and its weakening in 2013, there was temporarily a large disparity between the real effective exchange rate and the relative export price. Presumed factors behind the disparity include the presence of speculative trading in the exchange market and the diversification of corporate price-setting behavior in recent years. For example, when many exporting companies refrain from lowering overseas sales prices in order to secure profits, rather than sales volume, during a period of the yen s weakening, the change in the export price is small relative to the change in the real effective exchange rate. The same is also true when many countries refrain from raising overseas sales prices during a period of the yen s strengthening with priority placed on maintaining sales volume, rather than profits. Indeed, Figure II shows that when the yen s real effective exchange rate was declining from 2005 to 2007 and from late 2012 to 2013, the export price index on a contract currency basis dropped only slightly. Meanwhile, when the yen was appreciating from the middle of 2008 onwards, export prices did not rise much. 93

4 Figure II Real effective exchange rate and export price index Total products Contract currency basis Real effective exchange rate Source: Corporate Goods Price Index (Bank of Japan), BIS. (Month, year) Furthermore, corporate price-setting behavior varies depending on the type of goods that they export. Figure II is a comparison between the movements of the real effective exchange rate and the export price index (on a contract currency basis). This shows that against the backdrop of intensifying international price competition, the export prices of electric and electronic machinery on a contract currency basis have continued to decline with no regard to the movements of the real effective exchange rate. In contrast, the export price of textiles on a contract currency basis has been rising against the backdrop of a trend shift in export products to higher price ranges. The figure indicates that the export price of chemicals tends to move in line with the price of crude oil, which is a raw material of chemicals. Although the export price of transportation equipment, including motor vehicles, generally moved in line with the real effective exchange rate until around 2010, the link seems to have been weakening somewhat since Another factor that is weakening the link between the export price and the real effective exchange rate is growth in exports by companies in Japan to their overseas affiliates following an increase in the number of Japanese companies moving their business operations to other countries. Price-setting behavior concerning such intra-company transactions may be substantially different from that concerning export transactions in general. 94

5 Figure II Electric and electronic machinery Real effective exchange rate Real effective exchange rate and export price index Transportation Textiles equipment Real effective exchange rate Real effective exchange rate Contract currency basis (right scale) Contract currency basis (right scale) Contract currency basis (right scale) (Month, year) (Month, year) (Month, year) Source: Corporate Goods Price Source: Corporate Goods Price Source: Corporate Goods Price Index (Bank of Japan), BIS. Index (Bank of Japan), BIS. Index (Bank of Japan), BIS. Chemicals Chemicals Real effective exchange rate Crude oil prices Contract currency basis (right scale) Contract currency basis (right scale) (Month, year) Source: Corporate Goods Price Index (Bank of Japan), BIS. (Month, year) Source: Corporate Goods Price Index (Bank of Japan), BIS. To consider this matter, let us look at Figure II , which is a comparison between the movements of Japan s export volume (2010=100) and the yen s real effective exchange rate (2010=100). This figure shows that from around 2000 to 2007, the export volume continued to grow while the real effective exchange rate continued to decline. However, around the middle of 2007, when the subprime mortgage loan problem surfaced in the United States, the real effective exchange rate turned up sharply and subsequently stayed at a high level until late In the meantime, Japan s export volume has remained stagnant, failing to regain the level before the collapse of Lehman Brothers. Although the real effective exchange rate has 95

6 declined significantly since late 2012, Japan s export volume has stayed almost flat, rather than starting to grow again. In general, it takes a certain amount of time before companies revise their export prices following a change in the exchange rate 4. In addition, it presumably takes time before an export price revision is reflected in overseas sales prices and causes a sales volume change. Therefore, it may take a substantial period of time before the effects of a decline in the real effective exchange rate can be observed in the export volume change by way of a price revision 5. As more than two years have elapsed since the yen s real effective exchange rate started to decline significantly, attention is focusing on the future trend in Japan s export volume. Figure II Changes in real effective exchange rate and Japan's export volume Export volume index Real effective exchange rate Appreciation of yen Depreciation of yen Notes: Export volume index is seasonally adjusted. Source: Trade Statistics of Japan (MOF), BIS. (Year) Why has the export volume remained stagnant despite the improvement in Japan s price competitiveness? Factors other than corporate price-setting behavior that may affect the export volume will be shown below. (2) External demand and export volume Among other factors that may affect the export volume, the external demand trend must be mentioned first. Usually, the aggregate value of real GDP (dollar-based) of countries around the world 4 For example, Ito et al. (2010) conducted a questionnaire survey on 215 Japanese exporting companies, and regarding the frequency of reflecting exchange rate movements in sales prices, the survey found that around 80 of the 137 respondent companies made price revision within one year. 5 In cases where the yen is weakening, this is called the J-curve effect. 96

7 is adopted as an indicator of external demand. However, in order to identify external demand as seen from the standpoint of Japanese export industries, it is necessary to take into consideration the breakdown of goods export by export destination country. Figure II shows changes in the shares of exports to the United States, Europe (EU28) and China in Japan s overall exports. As an export destination for Japan, the United States has the largest share, around 20, followed by China with around 19 and Europe with around 12. The three main export destinations together account for half of overall Japanese exports. The figure indicates that while Europe-bound exports share has been on a long-term downtrend since the Collapse of Lehman Brothers, U.S.-bound exports share has been growing since 2012, whereas China-bound exports share has remained flat since Figure II Changes in Japan's export by destination country and region United States China Europe (EU28) Notes: Shares of the value of customs-cleared exports to destination countries and regions in Japan s overall exports (Yen basis) Source: Trade Statistics of Japan (MOF). (Year) Figure II shows the weighted average of changes in real GDPs of 26 trading partners of Japan 6 using each value of customs-cleared exports to them as the weight. According to this figure, Japan s export volume, which had previously increased almost in line with the real GDP growth of major export destination countries, has been growing at a much slower pace than the real GDP growth of those countries since This finding suggests that Japan s stagnant export volume in recent years is not attributable to the external demand trend. 6 The 26 countries and regions are: the United States, the United Kingdom, Belgium, Denmark, France, Germany, Italy, the Netherlands, Norway, Sweden, Canada, Finland, Portugal, Spain, Australia, New Zealand, Mexico, the Republic of Korea, Taiwan, India, Indonesia, Singapore, Malaysia, the Philippines, Thailand and China (including Hong Kong). The 26 countries and regions account for approximately 87 (the average between 1985 and 2014) of Japan s overall export value. 97

8 Figure II Changes in foreign real GDP and Japan's exports volume Export volume index Foreign real GDP (Year) Notes: 1. Foreign real GDPs is a weighted average of GDPs using each value of customs-cleared exports to trading partners of Japan as the weight (from the 1st quarter of 1985 to the 4th quarter of 2014). 2. Export volume index is seasonally adjusted. Source: Trade Statistics of Japan (MOF), Economic Outlook Database (OECD), Oxford Economics. (3) Value addition and export volume Value addition of export goods is another factor that may significantly affect the export volume. Here, the definition of value addition of export goods will be first clarified in relation to the export price index 7. In general, the export price index is computed by fixing products investigated, removing effects of both qualitative changes and changes in the product mix. Therefore, even if value addition to export goods which may imply either an increase in value-added of individual exported products or an increase in the share of higher value-added products in export, has occurred after the base year of the index, such changes do not affect the export price index. Value addition to individual export products may imply a shift in price range of passenger cars, for example, cars toward a higher range of cars with larger engine displacement. The export price index for ordinary passenger cars is produced by fixing a basket of cars of a specific category (in terms of engine displacement) as the survey subjects tracing their price changes. Therefore, even if the average export price of passenger cars may increase due to a shift in their price range toward a higher range of cars with larger engine displacement, such increase does not affect the export price index for ordinary passenger cars. An increase in the share of higher value-added products may imply, for example, such a case 7 The export price index is produced by the Bank of Japan using the methodology based on a fixed-weight Laspeyres formula. 98

9 that the share of large passenger cars increases where the price index for passenger cars is comprised of two sub-categories (ordinary passenger cars and large passenger cars). In this case, as the export price index makes the shares of sub-categories fixed in the reference period, the index for passenger cars does not change even if the average export price for passenger cars increases. Therefore, value addition to export goods may be regarded as a price increase that cannot be captured by the export price index. As for the relationship with export volume, the more value is added to an exported item, the less likely it is to increase its export volume even if the export price remains constant. Indeed, as value addition to Japanese export goods steadily proceeds, Japan s goods trade has become structurally biased against an export increase. (Figure II ). Figure II Value addition to Japanese export goods Value-added index Notes: value-added index = real exports / export volume; The index is seasonally adjusted. Source: Trade Statistics of Japan (MOF), Corporate Goods Price Index (BOJ). (Year) Figure II decomposes changes (year-on-year) in value addition to Japanese export goods into value addition to individual export products (product quality factor) and increases in high-value-added products shares among exports (product mix factor). The result shows that the product quality factor constantly contributes positively to value addition while the product mix factor tends to contribute negatively to value addition through an increase in low-value-added products shares. As demand for products with reduced prices usually grows, it is not easy to promote value addition by enhancing product mix. Indeed, Figure II indicates that between late 2004 and 2009, Japanese export industries, while promoting value addition to individual export items, expanded 99

10 production of low-value-added products at the same time, as they failed to increase high-value-added products shares. However, since 2010, whereas value addition to individual export products has continued, the rise in low-value-added products shares in the product mix, which had intermittently been observed until then, has all but disappeared. This suggests that the move to expand production of low-value-added products has been rolled back substantially. Furthermore, since 2013, the value addition to individual export products has slowed down significantly, indicating that the trend of value addition to Japanese export goods has remained stagnant. Figure II Decomposition of changes in value-added index (Year-on-year change, ) Product quality factor Product mix factor Value-added index Notes: For details of the decomposition, see Supplementary Note 1. Source: Trade Statistics of Japan (MOF), Corporate Goods Price Index (BOJ). (Year) (4) Export goods production capacity and export volume Export goods production capacity is also an important factor that may affect export volume. As is widely known, amid the rapid overseas expansion of the Japanese manufacturing industry, there are concerns over a possible hollowing out of the industry due to transfer of production facilities to foreign countries. If domestic production infrastructure continues to shrink, it would become difficult to increase exports from Japan by taking advantage of growing external demand in the future because of constraints imposed by the production capacity reduction. Therefore, it may be said that domestic production capacity is the most important element of Japan s competitiveness in export. In general, other conditions being equal, a country s export volume is proportionate to the scale of 100

11 its domestic export goods production capacity 8. Therefore, below, the relationship between the export goods production capacity and export volume will be shown. First, changes in the Japanese manufacturing industry s total domestic production capacity will be shown, including for domestic sales and exports (Figure II ). The figure shows that the production capacity of the entire manufacturing industry continued to grow until around 1997, when it started to decline. The production capacity continued to decline until around 2004 and resumed growing in 2005, with the uptrend continuing until In 2009, the year after the Collapse of Lehman Brothers, the production capacity started to decline again, and the downtrend continued until Next, production capacity by individual industry will be shown. The production capacity of the electric machinery industry (old classification) 9 (machinery manufacturing industry + information equipment and communication electronics industry + electronics parts and devices industry) remained on the path of recovery from the collapse of the IT bubble in 2001 until 2011, when it started to decline again following the Great East Japan Earthquake in March of the year. In particular, in the field of household electric appliances, where Japanese companies face severe competition from their counterparts in emerging countries, production capacity has been declining steeply over a long period of time since the latter half of the 1990s. In materials industries, including iron and steel, metal products, ceramics, stone and clay products and chemicals, production capacity has been on a long-lasting downtrend. In the transport equipment industry, which is the core of Japan s export industries, production capacity shrank significantly between 2000 and Although production capacity remained flat thereafter, it has been declining again since The production capacity of electronics parts and devices, which consistently continued to grow in the past, has been shrinking after peaking around As shown above, domestic production capacity has been declining in almost all industries in recent years. 8 Refer to Goldstein, M and Mohsin S. Khan (1978), pp276, for example. 9 The electric machinery industry as referred to here, which is an old classification of the Indices of Industrial Production, comprises the electric machinery manufacturing industry, the information equipment and communication electronics manufacturing industry and the electronics parts and devices manufacturing industry under the current 2010 classification. 101

12 Figure II Domestic production capacity index by industry (exports + domestic consumption) Manufacturing industry Electric machinery industry (old classification) Household electric appliances industry Iron and steel industry Metal products industry Ceramics, stone and clay products industry Chemical industry Information and communication electronics equipment industry Transportation equipment industry Electronic parts and devices industry Source: Indices of Production Capacity of Japan s Manufacturing Industry (METI) 102

13 Next, changes in the ratio of exports to overall shipments (export ratio) by industry will be shown. Figure II shows changes in the export ratio concerning materials industries and processing/assembly industries. According to this figure, the export ratio has been rising in recent years in many industries. The uptrend in the export ratio started in materials industries, including textile manufacturing, in the 1990s or so, and in processing/assembly industries such as transport equipment and general-purpose machinery manufacturing a little later, in the 2000s. However, since around 2008, the export ratio growth has remained stagnant in both materials and processing/assembly industries. In the information and communication electronics equipment industry, which is among the processing/assembly industries, the export ratio started to rise again in 2011 after a long period of decline. On the other hand, the export ratio has continued to decline steeply in the electronic parts and devices industry since Meanwhile, in the electrical machinery industry, the export ratio has remained almost flat. The figure shows that in 2014, the export ratio rose in most industries, including materials industries but excluding the electronic parts and devices and some other industries. In particular, the export ratio rose steeply in the information and communication electronics equipment industry. Figure II Changes in export share by industry I. Materials industries Iron and steel industry Chemical industry Textile industry Plastic products industry (Year) Notes: Export share = (index of shipments for export x export weight) / (index of shipments for exports x export weight + index of shipments for domestic sales x domestic shipment weight) x 100 Source: Breakdown List of Industrial Shipment (METI). 103

14 II. Processing/assembly industries. Electronic parts and devices industry Electric machinery industry Transportation equipment industry Information and communication electronics equipment industry General machinery industry (Year) Notes: Export share = (index of shipments for export x export weight) / (index of shipments for exports x export weight + index of shipments for domestic sales x domestic shipment weight) x 100 Source: Breakdown List of Industrial Shipment (METI). In general, there is presumably a positive correlation between the movements of the export goods production capacity and shipments for exports, so it may be assumed that when the export ratio (shipments for export / (shipments for exports + shipments for domestic sales)) is rising while domestic production capacity as a whole is declining, the export goods production capacity is growing. Below is predicted changes in the production capacity of exports goods in Japan using data concerning domestic production capacity and the export ratio. As there are no statistics directly concerning the export goods production capacity, a figure obtained by multiplying the domestic production capacity component of the Indices of Production Capacity prepared by METI by the export ratio calculated based on the breakdown list of industrial shipments (shipments for exports/(shipments for domestic sales + shipments for exports), also prepared by METI 10 is used as a proxy for the Japanese exporting industries export goods production 10 However, the operating rate of production facilities is not taken into consideration here. The production capacity obtained through shipment data reflects the effects of short-term fluctuations of the operating rate that accompany the economic cycle. In other words, in this case, a drop in shipments for export caused by a decline in the operating rate of export goods production facilities, rather than a decline in the export goods production capacity, is also treated as the effect of a decline in the export goods production capacity. Therefore, it should be kept in mind that the export goods production capacities calculated below reflect the effects of fluctuations of the operating rate. In recent years, the so-called mixed line production system, which refers to the production of products for export and those for domestic sales on a single production line, has become widespread, mainly in the motor vehicle and general machinery industries. A production system innovation like this makes it possible for companies to flexibly use existing production capacities for export and domestic sales in accordance with the demand trend. Consequently, when evaluating the trend in production capacity for export and domestic sales based on 104

15 capacity. Figure II shows the estimation results. Looking at the figure, the domestic consumption goods production capacity continued to decline for a long period of time from the late 1990s onwards, the export goods production capacity continued to grow until around early 2011 except for the temporary decline in the aftermath of the Collapse of Lehman Brothers. During this period, Japan s export goods production capacity stayed flat until around the middle of the 1990s before starting to grow rapidly around the middle of 1996 against the backdrop of the strong performance of the U.S. economy and the yen s weakening. Given that the yen started to weaken around the middle of 1995, it took around one year before the effects of the yen s weakening appeared in the form of growth in the export goods production capacity. Subsequently, the export goods production capacity generally remained flat until 2002, when it resumed growing after the collapse of the IT bubble. At that time, the yen started to weaken around the beginning of 2001, indicating that it took around one year before the effects of the yen s weakening appeared in the form of growth in the export goods production capacity. The yen remained weak until around the middle of 2007, and the export goods production capacity continued to grow over this period. The export goods production capacity has fallen steeply twice since The first plunge in the production capacity started in the fourth quarter of 2011, around three years after the Collapse of Lehman Brothers, and continued for five quarters, until the fourth quarter of The second plunge continued from the first quarter of 2014 to the third quarter of the same year (however, given that the production capacity declined only 0.4 year on year in the third quarter of 2014, the effective duration of the plunge was two quarters). As the yen s strengthening that started around the middle of 2007 continued until around the end of 2012, the first plunge took place amid the prolonged strong-yen trend. Given that the capacity continued to decline year on year for more than one year and that it has not yet recovered to the pre-plunge period 11, it can be presumed that Japanese companies made earnest efforts to curtail their export goods production capacity. On the other hand, the second plunge in the export goods production capacity is unlikely to be the result of earnest efforts to cut back on the capacity, given that it took place after the yen started to weaken around the end of 2012 and that the plunge continued just two quarters, with the capacity rebounding far above the pre-plunge level in the fourth quarter of 2014, just three quarters from the start of the plunge. Rather, these data strongly suggest that some special factor or other caused the export goods production capacity to drop temporarily. shipment data, it is necessary to closely watch other relevant economic statistics and the various underlying economic phenomena as well. 11 The export goods production capacity index immediately before the plunge was (in the third quarter of 2011). As of the fourth quarter of 2014, the index was lower than this level. 105

16 Figure II Changes in production capacity of export goods (Year-on-year change, ) Index of production capacity of export goods (right scale) Index of production capacity of export goods Index of production capacity of domestic consumption goods (Year) Notes: Production capacity of export goods = production capacity index x export share Export share = (index of shipments for export x export weight) / (index of shipments for exports x export weight + index of shipments for domestic sales x domestic shipment weight) x 100 Production capacity of domestic consumption goods = production capacity index x (1 - export share) Source: Indices of Production Capacity of Japan's Manufacturing Industry, Breakdown List of Industrial Shipment (METI). What special factor was there at that time? In April 2014, the consumption tax rate was raised, and in the first quarter of the year, there was a last-minute surge in demand before the tax hike. Indeed, the actual operating rate 12 of Japan s manufacturing industry started to rise in 2013, the year before the consumption tax hike, after continuing to decline from the second quarter of In the first quarter of 2014, the actual operating rate, which stood at 74.6 in the fourth quarter of 2012, climbed to 84.9, the highest level since the third quarter of 2008, the year of the Collapse of Lehman Brothers. Subsequently, the operating rate fell back to 78.6 in the third quarter of 2014, immediately after the consumption tax hike (Figure II ). In the meantime, the growth in shipments for export slowed down considerably, to 2.6 in the first quarter of 2014, followed by a decline of 1.2 in the second quarter of the same year. However, shipments for export started to grow again in the third quarter of the same year and posted a significant increase, 4.3, in the fourth quarter of the year. On the other hand, shipments for domestic sales grew significantly in the fourth quarter of 2013 and the first quarter of 2014, before starting to decline again in the third quarter of These data 12 Estimated by multiplying the published actual operating rate level in the base year (2010) by the operating rate index. 106

17 provide a strong indication that Japanese companies shifted some of their production capacity for export to production for domestic sales in order to meet the last-minute surge in demand before the consumption tax hike 13. As shown above, it is highly likely that the two phases of plunge in the export goods production capacity since 2011 are quite different in nature from each other. Figure II Changes in actual operating rate, shipments for exports, and shipments for domestic sales before and after the consumption tax hike (Year-on-year change, ) Shipments for exports Shipments for domestic sales Actual operating rate (exports + domestic consumption; right scale) (Year) Source: Indices of Production Capacity of Japan's Manufacturing Industry, Breakdown List of Industrial Shipment (METI). Finally, looking at recent developments, since the latter half of 2014, the export goods production capacity has been growing again. In the fourth quarter of the same year, it recovered to the level before the collapse of Lehman Brothers. The continuing decline in the domestic consumption goods production capacity is a cause for concern. However, regarding the export goods production capacity, there are indications that Japanese exporting industries started again to devote efforts to building up their production capacity in Japan against the backdrop of a recent improvement in the export environment, backed by a recovery in external demand and stable exchange rate movements. A comparison of the movements of the export goods production capacity thus identified and the 13 Regarding motor vehicle-related real exports, the Bank of Japan (2014) reported that supply constraints associated with a steep rise in domestic sales temporarily had an export volume-reducing effect. It was reported at a meeting in August 2014 of the Industrial Structure Council s Manufacturing Industry Committee (second meeting) that companies response to the last-minute surge in demand (production increase) continued after the consumption tax hike implemented in April 2014, mainly in the motor vehicle industry, as production did not catch up with demand. 107

18 movements of export volume shows a strong positive correlation between the two. However, it also shows that there was a large disparity between them during periods of short-term volatility of export volume, such as around the time of the Collapse of Lehman Brothers (Figure II ). Overseas inventory investment, which is explained below, is an important factor that may trigger short-term volatility of export volume. Figure II Changes in production capacity of export goods and export volume Export volume index Index of production capacity of exports goods (Year) Notes: 1. Index of production capacity of exports goods = production capacity index x export share; Export share = (index of shipments for export x export weight) / (index of shipments for export x export weight + index of shipments for domestic sales x domestic shipment weight) x Export volume index is seasonally adjusted. Source: Indices of Production Capacity of Japan's Manufacturing Industry, Breakdown List of Industrial Shipment (METI). (5) Overseas inventory investment and export volume In general, in the expansionary phase of the business cycle, companies increase their production and exports to accumulate their inventories, while in the recessionary phase, they reduce or suspend their production and export in order to cut back on excessive inventories. Consequently, corporate inventory investment activities, including inventory accumulation and adjustment, work to magnify the changes in production and export in the course of business cycle, rather than offset the changes 14. At this time, as a proxy variable for overseas inventory investment by Japanese export industries, the change in inventories is used, which consists one of demand components of GDP, as a share of 14 For example, the Economic Planning Agency (1992) stated as follows in Chapter 2, Section 5 concerning the characteristics of inventory investment: In reality, as inventory investment increases in the expansionary phase and declines in the recessionary phase, it magnifies, rather than offsets, the changes of production during the business cycle. This indicates that when inventory plays a buffer role, there is an appropriate amount of inventory which is broadly proportionate to the level of demand and that the inventory changes in parallel to the changes in demand. 108

19 the aggregate nominal GDPs of major trade partners of Japan (Figure II ). This makes it possible to explain a large part of the short-term volatility of Japan s export volume induced by overseas inventory investment. Indeed, Figure II shows that Japanese companies made rapid inventory adjustment and accumulation in such a short period of one year, from 2001 to 2002 immediately after the bursting of the IT bubble and from 2008 to 2009 immediately after the Collapse of Lehman Brothers. The more inventory investment volatile, the more export volume swings during a short period of time. Figure II Changes in overseas inventory investment Changes in overseas inventory as a share of the nominal GDP (Year) Notes: Figure shows the weighted average of SNA base changes in inventories as shares of the nominal GDPs of 24 major trading partners of Japan (US, UK, Belgium, Denmark, France, Germany, Italy, Netherlands, Norway, Sweden, Canada, Finland, Portugal, Spain, Australia, Mexico, ROK, Taiwan, India, Indonesia, Malaysia, Philippines, Thailand, and China excluding Hong Kong) using the customs-cleared values of export to those trade partners as the weight. The figure is seasonally adjusted. Source: Oxford Economics. A look at overseas inventory investment since 2012 indicates that the investment amount has been on a downtrend even though there has not been a significant change in overseas demand. In the fourth quarter of 2014, overseas inventory investment declined 0.2, marking the first drop since around the time of the Collapse of Lehman Brothers. A decomposition of overseas inventory investment by export partners shows that while inventory accumulation has continued in the United States, China and Indonesia because of favorable economic conditions there, inventory adjustment has intensified since around 2012 in some Asian countries, including the Republic of Korea, Thailand and the Philippines, and EU member countries (Figure II ). In particular, inventory investment in the Republic of Korea fell steeply in the fourth quarter of

United States China ROK Thailand Taiwan (Year) Notes: Figure shows the weighted average of SNA base changes in inventories as shares of the nominal GDPs of 24 major")

20 Figure II Overseas inventory investment by export trading partners Canada Australia India Mexico EU Taiwan Malaysia Philippines Thailand Indonesia ROK United States China Overseas inventory investment (shares of nominal GDP) United States China ROK Thailand Taiwan (Year) Notes: Figure shows the weighted average of SNA base changes in inventories as shares of the nominal GDPs of 24 major trading partners of Japan (US, UK, Belgium, Denmark, France, Germany, Italy, Netherlands, Norway, Sweden, Canada, Finland, Portugal, Spain, Australia, Mexico, ROK, Taiwan, India, Indonesia, Malaysia, Philippines, Thailand, and China excluding Hong Kong) using each value of customs-cleared exports to them as the weight. The figure is seasonally adjusted. Source: Oxford Economics. (6) Estimation of the export volume function and decomposition of changes Above, five factors presumed to be closely linked with the movements of Japan s export volume price competitiveness, external demand, value addition to export goods, domestic production capacity for export goods and overseas inventory investment are examined in detail for their characteristics and their relationship with the export volume. Below, Japan s export function will be estimated using all these five factors. In addition, using the estimation results, decomposition of the changes in export volume will be exhibited to show to what extent each factor affects Japan s export volume 15. Figure II is a comparison between the estimated export volumes based on the export volume function and the actual export volumes. This figure indicates that the estimated figures accurately track the volatile changes in the export volume around the time of the bursting of the IT bubble in 2001 and the Collapse of Lehman Brothers in As for the details of methods for estimation and descriptions as well as their results, refer to Supplementary Note However, the estimated figures are slightly higher than the actual figures for 2011 and later. This suggests that some structural factor other than these five factors used in the export volume function at this time has been newly emerging since Replacement of domestic production with the expansion of overseas production, for example, may be the candidate. However, analysis in this respect was refrained 110

21 Figure II shows a decomposition of changes (year-on-year) in export volume into five factors price competitiveness, external demand, value addition to export goods and export goods production capacity using the estimated figures obtained through estimation based on the export function. First, an overview of the relationship between each factor and export volume will be shown. As was expected, the overseas inventory investment factor explains a large part of the high volatility of the export volume when foreign demand has showed high volatility in the aftermaths of the Asian currency crisis in , the bursting of the IT bubble in 2001 and the Collapse of Lehman Brothers in However, since 2012, overseas inventory investment made negative contributions to the export volume during most of the period despite a lack of significant changes in external demand. This was because inventory investment has been curbed or reduced since 2012 in some Asian countries, including the Republic of Korea, which is a major export destination for Japan, and some EU countries, as shown in 1. (5). Next will be the real effective exchange rate, which is an indicator of the price competitiveness factor. The real effective exchange rate affects export volume with a time lag of around four quarters (one year). The figure shows that the real effective exchange rate turned to a positive contributor to the export volume since the fourth quarter of 1996 that corresponds to the year elapsed around one year since the middle of 1995 when the yen started to weaken. Likewise, the real effective exchange turned to a positive contributor to the export volume since the first quarter of 2002 corresponding year that have elapsed around one year since the beginning of 2001 when the yen started to weaken. In addition, when the yen started to weaken at the end of 2012, the export volume-increasing effect started to appear around one year later, at the end of Conversely, at the time of the yen s strengthening, including 1993, , and 2008 and subsequent years, the real effective exchange rate began to appear as a negative contributor to the export volume around one year after the strong-yen trend started. When looking at the movements of overseas real GDP, an indicator of the external demand factor, it had been a steadily positive contributor to export volume throughout the estimation period except for the subsequent year to the Collapse of Lehman Brothers in the fourth quarter of Meanwhile, the value addition factor had been a negative contributor to export volume throughout most of the period, reflecting the trend of value addition to Japan s export goods. However, since 2013, the negative contributions made by the factor have become somewhat smaller. This reflects the trend of value addition to Japanese export goods has remained stagnant since 2013, as was described in 1. (3). The export goods production capacity factor had been a temporarily negative contributor when external demand slumped seriously in the aftermaths of the bursting of the IT bubble and the Collapse of Lehman Brothers. But at other times, this factor constantly had been a positive contributor through the expansion of production of low-value-added products. because the necessary numbers of data cannot be obtained due to the brevity of the period. 111

22 Following the Collapse of Lehman Brothers, the exports goods production capacity factor ceased to make positive contributions to export volume despite a lack of a significant decline in external demand, as the expansion of production of low-value-added products was rolled back. Between the end of 2011 and the fourth quarter of 2012, the factor had an export volume-reducing effect 17. The above findings indicate that Japan s export volume expanded steadily between 2002 and 2008, before the Collapse of Lehman Brothers, because the positive contribution from an increase in the export goods production capacity backed by external demand growth and the expansion of production of export goods, mainly low-value-added products, constantly outweighed the negative contribution from the value addition trend, except when export volume was affected by the short-term impact of the overseas inventory investment factor 18. Meanwhile, Japan s export volume has remained stagnant since 2011 because the positive contribution from an improvement in price competitiveness due to robust external demand and the yen s weakening failed to surpass the negative contribution from such factors as the trend of value addition to export goods, the reduction of the export goods production capacity that continued from the end of 2011 to 2012, a temporary decline in the export goods production capacity caused by the response to the consumption tax hike and the progress in inventory adjustment abroad. (7) Summary Japan s export volume resumed growing year on year in the fourth quarter of 2014 thanks to such factors as continued robust external demand, mainly in the United States, the ongoing recovery in the export goods production capacity after a temporary slump caused by the response to the consumption tax hike, and the improving price competitiveness due to the yen s weakening. However, as was already mentioned, Japan s goods trade has become structurally biased against an export increase because of the ongoing value addition trend. Besides, since the Collapse of Lehman Brothers, the expansion of production of low-value-added products, which presumably had led the growth in the export goods production capacity until then, has been rolled back significantly. As a result, if Japan is to maintain a certain degree of export volume growth in the future amid the rapidly evolving economic globalization, it is essential for the country to continue to promote the trend of value addition to export goods and maintain and expand the export goods production capacity. The key to maintaining and expanding the export goods production capacity will be whether Japanese export industries can grow their shares in the market for high-value-added products. 17 The export goods production capacity had a negative contribution in 2014 as well. However, this was probably because of a last-minute surge in demand before the consumption tax hike, rather than earnest efforts to reduce production capacity, as mentioned in 1. (4). 18 However, in 2005, export volume declined year on year because the negative contribution from the value addition factor temporarily surpassed the positive contribution from export the overseas demand and export goods production capacity factors. 112

23 Figure II Estimated export volume (not seasonally adjusted) and actual export volume Actual Estimated Notes: For details of the estimation method, see Supplementary Note 2(1). (Year) Source: Trade Statistics of Japan (MOF), Indices of Production Capacity of Japan's Manufacturing Industry, Breakdown List of Industrial Shipment (METI), Input-Output Tables for Japan (MIC), Corporate Goods Price Index (BOJ), Economic Outlook Database (OECD), IFS (IMF), BIS, Oxford Economics. 113

Factors of production capacity of exports goods (indices of production capacity of exports goods) Higher value added content")

24 Figure II Decomposition of changes in export volume (not seasonally adjusted) (Year-on-year change, ) Asian Collapse of currency Bursting of Lehman crisis IT bubble Brothers Residuals Overseas inventory investment factors (changes in overseas inventories) Factors of production capacity of exports goods (indices of production capacity of exports goods) Higher value added content factors (value added index) Great East Price competitiveness factors (real effective exchange rates) Overseas demand factors (overseas real GDP) Japan Trend component Export volume (actual volume) Earthquake Consumption tax hike (Note 2) (Year) Source: Trade Statistics of Japan (MOF), Indices of Production Capacity of Japan's Manufacturing Industry, Breakdown List of Industrial Shipment (METI), Corporate Goods Price Index (BOJ), IFS (IMF), BIS, Oxford Economics, Economic Outlook Database (OECD). Notes: 1. For details of decomposition, see Supplementary Note 2(2). 2 The negative contribution by the production capacity of exports goods from the 1st quarter to the 2nd quarter of 2014 is considered to be caused mainly by the temporary shift of part of domestic production capacity from export sales to domestic sales in response to last-minute demand before the consumption tax hike, rather than by an intentional shift toward reduction of production capacity of export goods. For details, see Section 1 (4). 114

25 2. Overview of international comparison of competitiveness in export In this section, we will examine the force of Japan s competitiveness in export. Recently, signs of a recovery in Japan s export volume have started to appear at long last. However, while the export volume indexes for emerging countries and the United States have surpassed and remained above the level before the collapse of Lehman Brothers, the index for Japan has remained stagnant below the level before the collapse of Lehman Brothers (Figure II ). Here, we will look at the characteristics of Japanese exports through international comparison of traded goods classified by production process. Then, we will evaluate Japan s competitiveness in export by examining the export growth rates of major Japanese industries in terms of value and Japanese traded goods shares of imports by country/region (import value shares) based on Trade Statistics (Ministry of Finance). Figure II Changes in export volume indices of world and Japan Europe United States Emerging countries United States Japan Europe Emerging countries Japan World Europe Notes: Figures show annual equivalent of monthly data. Source: World Trade Monitor (Netherlands Bureau for Economic Policy Analysis (CPB)). (Year) (1) World trade and international comparison of traded goods classified by production process We will look at changes in the value of world trade and Japan s export trend and take an overview of the characteristics of Japan s exports through international comparison of traded goods classified by production process. (A) Changes in the value of world trade (export value) World trade has recorded high growth in terms of export value since 2000 (Figure II ). In the 2000s (2001 to 2010), world trade registered an average annual growth rate of 9.0, up sharply from 6.3 in the 1990s (1991 to 2000). So far in the 2010s (2011 to 2013), the average annual growth 115

26 rate slowed down to 6.9, which is still higher than the growth rate in the 1990s. In the 2000s, the world trade growth was led more by growth in emerging countries than by growth in developed countries (Table II ). (Trillion dollars) Figure II Changes in world trade (export value) World Developed countries Emerging countries Source: IFS (IMF). (Year) Table II Growth rates of world trade (export value) World Developed countries Source: IFS (IMF). Emerging countries (B) Exports by major exporting countries/regions in terms of value and their shares of world export value Exports by major exporting countries/regions 19 have generally been on an uptrend in terms of value since the latter half of the 2000s, with exports by China in particular growing considerably. Although the value of exports by Japan was higher than the values of exports by other Asian countries in the 1990s, its growth has been stagnant since the 2000s (Figure II ). 19 Here, major exporting countries/regions refers to the four largest exporting countries in 2014 (China, the United States, Germany and Japan) plus the Republic of Korea and ASEAN

27 As for major countries/regions shares of the world export value, whereas many countries/regions have been losing shares, China s share has been growing (Figure II ). Figure II Changes in export value of major export partners and regions (Billion dollars) Japan China United States ROK Germany ASEAN5 (Year) Notes: 1. Figures show data in and after 1991 for the U.S. and Germany and those in and after 1992 for China. 2. ASEAN5 consists of Indonesia, Malaysia, the Philippines, Singapore and Thailand. Figures from 1990 to 1994 exclude those for the Philippines and show those for the other four countries. Source: UN Comtrade. 117

28 Figure II Changes in shares of export value of major export partners and regions in world export value Japan China United States ROK Germany ASEAN5 (Year) Notes: 1. Figures show data in and after 1991 for the U.S. and Germany and those in and after 1992 for China. 2. ASEAN5 consists of Indonesia, Malaysia, the Philippines, Singapore and Thailand. Figures from 1990 to 1994 exclude those for the Philippines and show those the other four countries. Source: UN Comtrade. (C) Trend in exports of traded goods classified by production process Next, we will conduct international comparison of traded goods classified by production process (Figure II ) and look at changes 20. World trade (export value) in all types of traded goods classified by production process has been growing since the 2000s. Although it declined temporarily in 2009 due to the impact of the Collapse of Lehman Brothers, it has recovered moderately since then. World trade in raw materials increased by a factor of 6.8 (from billion dollars to 2,798.0 billion dollars) between 1990 and 2013 as it has gradually grown since the latter half of the 2000s. World trade in intermediate goods expanded by a factor of 5.3 (from 1,490.8 billion dollars to 7,950.6 billion dollars) between 1990 and 2013, while world trade in final goods grew by a factor of 4.5 (from 1,327.5 billion dollars to 6,011.1 billion dollars) (Figure II ). As for the shares of traded goods by production process in world trade (export value), intermediate goods share has stayed at around 50, but final goods share has been declining since peaking in 1999, falling to between 30 and 40 by now (Figure II ). 20 In this analysis, traded goods are classified by production process (raw materials, intermediate goods and final goods) with division of production in mind. As the basic data for the analysis, RIETI-TID2013, prepared by the Research Institute of Economy, Trade and Industry under the Ministry of Economy, Trade and Industry, is used. 118

29 Figure II Classification of trade goods by production process Raw materials Intermediate goods Final goods Raw materials Processed products. Iron and steel. Refined oil. Chemical products etc. Consumer goods Goods related to personal consumption:. Pharmaceuticals. Home appliances. Passenger cars etc.. Iron ore. Crude oil. Stone and clay etc. Parts. Machinery parts etc. Capital goods Goods as production capital:. Machine tools. Construction machinery. Trucks. Personal computers etc. Primary products Industrial products in particular Source: METI. 119

Figure II-1-1-2-8 Changes in shares of trade goods by production process in world trade (export value) Intermediate goods Final goods Source: RIETI-TID 2013 database.")

30 Figure II (Billion dollars) Changes in trade goods by production process in world trade (export value) Raw materials Intermediate goods Final goods Source: RIETI-TID 2013 database. (Year) Figure II Changes in shares of trade goods by production process in world trade (export value) Intermediate goods Final goods Source: RIETI-TID 2013 database. (Year) 120

31 (a) International comparison concerning final goods Regarding the value of final goods exports (consumer goods and capital goods) by major countries/regions 21, the export value in 2013 came to 1,211.3 billion dollars for China, billion dollars for Germany and billion dollars for the United States. In particular, the value of exports by China has increased steeply, expanding by a factor of 22.1 between 1990 and Although the value of exports by Japan continued to grow until 2008, it dropped sharply in 2009 due to the impact of the Collapse of Lehman Brothers. The value of exports by Japan later recovered temporarily, but has been declining again since 2011, falling to billion dollars in 2013 (Figure II ). Figure II Changes in values of final goods export by major export partner and region (Billion dollars) Japan United States ASEAN Germany China ROK Source: RIETI-TID 2013 database. (Year) (b) International comparison concerning intermediate goods As for the value of intermediate goods exports (processed goods and parts) by major countries/regions, the export value in 2013 stood at billion dollars for China, billion dollars for the United States and billion dollars for Germany. In particular, the value of exports by China increased by a factor of 36.2 between 1990 and The trend in intermediate goods exports by Japan was similar to the trend in final goods exports by the country: while the value of intermediate exports continued to grow moderately until 2008, it fell in 2009 because of the impact of 21 Here, major exporting countries/regions refers to Japan, the United States, ASEAN, Germany, China and the Republic of Korea in accordance with the regional classification of RIETI-TID. ASEAN here refers to eight countries Brunei, Cambodia, Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam. However, relevant statistics are unavailable concerning some countries and some years due to data constraints. The same applies to figures based on RIETI-TID data unless otherwise specified. 121

32 the Collapse of Lehman Brothers. Although it temporarily recovered, it has been declining after peaking in 2011, falling to billion dollars in 2013 (Figure II ). Figure II Changes in values of intermediate goods export by major export partner and region (Billion dollars) Japan United States ASEAN Germany China ROK Source: RIETI-TID 2013 database. (Year) (c) Changes in the value of Japanese exports of traded goods by production process and in the value of Japanese exports of traded goods classified by production process and by export destination Regarding the value of Japanese exports of traded goods by production process, processing goods and parts, both of which are categorized as intermediate goods, account for the largest portions of the value, making it clear that intermediate goods are the country s mainstay export goods. As for final goods, although the value of capital goods exports recovered after falling steeply in 2009 due to the impact of the Collapse of Lehman Brothers, it has been declining significantly again since peaking in Likewise, the value of consumer goods exports recovered slightly in 2010 after falling steeply in 2009 but has remained flat since then (Figure II ). 122

33 Figure II Changes in values of Japanese trade goods export by production process (Billion dollars) Raw materials Processed products (intermediate goods) Parts (intermediate goods) Capital goods (final goods) Consumer goods (final goods) Source: RIETI-TID 2013 database. (Year) Next, we will look at changes in the value of Japanese exports of traded goods classified by production process and by export destination. The value of exports of processed goods (intermediate goods) to China increased by a factor of 15.0 (from 3.63 billion dollars to billion dollars) and the value of exports of parts (intermediate goods) to China expanded by a factor of 30.3 (from 1.63 billion dollars to billion dollars) over the same period. As for capital goods (final goods) and consumer goods (final goods), the value of exports to the United States, Japan s biggest export market, is the largest. Since 2000, the values of exports of capital goods and consumer goods to China have been growing. Between 1990 and 2013, the value of exports of capital goods (final goods) to China increased by a factor of 13.3 (from 2.81 billion dollars to 37.4 billion dollars), while the value of exports of consumer goods (final goods) to the country grew by a factor of 18.1 (from 0.6 billion dollars to billion dollars). The higher values of exports of intermediate goods to China and ASEAN than the values of exports of consumer goods thereto indicate that Asia is at the center of Japanese supply chains (Figure II ). 123

34 Figure II Changes in values of Japanese trade goods export by production process and by export destinations [Raw materials (Japan)] (100 million dollars) China ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Processed products (Japan)] China ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) 124

35 (100 million dollars) [Parts (Japan)] China ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Capital goods (Japan)] China ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) 125

36 (100 million dollars) [Consumer goods (Japan)] China ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) The value of Japanese exports of capital goods has been on a downtrend since peaking 2011, with exports to China, EU28 and the Republic of Korea declining. In particular, exports to EU28 slumped sharply in 2009 because of the impact of the Collapse of Lehman Brothers and have remained sluggish since then without recovering to the level before the collapse of Lehman Brothers. A comparison of exports of final goods (capital goods and consumer goods) by Japan and the United States to EU28 shows that whereas the value of exports by the United States has been increasing, the value of exports by Japan has remained almost flat since the 1990s (Figure II ). Regarding final goods as classified into capital goods and consumer goods, the value of capital goods exports by Japan has remained flat, while the value of consumer goods exports has been declining. In contrast, the values of both capital goods and consumer goods exports by the United States have been increasing. 126

[Changes in values of final goods exports by Japan to EU28] (100 million dollars) Consumer goods Capital goods Final goods Source: RIETI-TID 2013 database. (Year) 127")

37 Figure II Changes in values of final goods exports by Japan and the United States to (100 million dollars) EU28 Japan United States Source: RIETI-TID 2013 database. (Year) [Changes in values of final goods exports by Japan to EU28] (100 million dollars) Consumer goods Capital goods Final goods Source: RIETI-TID 2013 database. (Year) 127

![[Changes in values of final goods exports by the United States to EU28] (100 million dollars) Consumer goods Capital goods Final goods Source: RIETI-TID 2013 database.](/docs-images/78/77489604/images/38-0.jpg "(Year) Next, we will take a look at major exporting countries exports of traded goods classified by product process.")

38 [Changes in values of final goods exports by the United States to EU28] (100 million dollars) Consumer goods Capital goods Final goods Source: RIETI-TID 2013 database. (Year) Next, we will take a look at major exporting countries exports of traded goods classified by product process. In the case of the United States, the value of exports of intermediate goods (processed goods and parts) is higher than the value of final goods (capital goods and consumer goods) exports. In particular, the value of processed goods (intermediate goods) exports has been on an uptrend since the 2000s. Although the export value temporarily declined in 2009 due to the impact of the Collapse of Lehman Brothers, it resumed growing in The value of parts (intermediate goods) exports accounts for the second largest portion of overall U.S. exports, after the value of processed goods exports. The value of materials exports has also been on an uptrend, as the United States has an edge in exports of such materials as crude oil and natural gas (Figure II ). By export destination, the values of U.S. exports of intermediate goods (processed goods and parts) and final goods (capital goods and consumer goods) to China, ASEAN and EU28 have been increasing. In particular, parts (intermediate foods) exports to China expanded by a factor of 36.7 (from 0.81 billion dollars to billion dollars) between 1990 and 2013 and consumer goods (final goods) exports to the country increased by a factor of 39.1 (from 0.42 billion dollars to billion dollars) (Figure II ). 128

39 Figure II Changes in values of trade goods exports by production process in the United States (100 million dollars) Raw materials Processed products (intermediate goods) Parts (intermediate goods) Capital goods (final goods) Consumer goods (final goods) US main export destination countries (export values in 2014) 1. Canada (31,212.5 billion dollars) 2. Mexico (24,032.6 billion dollars) 3. China (12,402.4 billion dollars) 4. Japan (6,696.4 billion dollars) 5. U.K. (5,386.5 billion dollars) Source: RIETI-TID 2013 database, Global Trade Atlas. (Year) Figure II Changes in values of US trade goods exports by production process and by export destination (100 million dollars) [Raw materials (US)] Japan China ROK ASEAN EU28 Source: RIETI-TID 2013 database. (Year) 129

40 (100 million dollars) [Processed products (US)] Japan China ROK ASEAN EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Parts (US)] Japan China ROK ASEAN EU28 Source: RIETI-TID 2013 database. (Year) 130

41 (100 million dollars) [Capital goods (US)] Japan China ROK ASEAN EU28 Source: RIETI-TID 2013 database. (Year) [Consumer goods (US)] (100 million dollars) Japan China ROK ASEAN EU28 Source: RIETI-TID 2013 database. (Year) In the case of Germany, the values of exports of most types of traded goods have surpassed and stayed above the level before the collapse of Lehman Brothers. Whereas the value of German exports of raw materials is small as in the case of Japan, the values of German exports of processed goods 131

42 (intermediate goods) and consumer goods (final goods) are large (Figure II ). By export destination, the values of German exports to the United States, the rest of the EU and China have been growing. Parts (intermediate goods) exports to China increased by a factor of 55.2 (from 0.5 billion dollars to billion dollars) between 1990 and 2013, while the value of consumer goods (final goods) exports to the country expanded by a factor of 60.7 (from 0.3 billion dollars to billion dollars) (Figure II ). Figure II Changes in values of Germany's trade goods exports by production process (100 million dollars) Germany s main export Raw materials destination countries (export values in 2014) 1. France (13,449.0 billion dollars) Processed products 2. U.S. (12,743.6 billion dollars) (intermediate goods) 3. U.K. (10,577.5 billion dollars) Parts (intermediate 4. China (9,891.2 billion dollars) goods) 5. Netherlands (9,355.3 billion Capital goods (final dollars) goods) Consumer goods (final goods) Source: RIETI-TID 2013 database, Global Trade Atlas. (Year) 132

43 Figure II Changes in values of Germany's trade goods exports by production process and by export destination [Raw materials (Germany)] (100 million dollars) (100 million dollars) Japan China ROK ASEAN United States EU28 (right scale) Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Processed products (Germany)] (100 million dollars) Japan China ROK ASEAN United States EU28 (right scale) Source: RIETI-TID 2013 database. (Year) 133

44 (100 million dollars) [Parts (Germany)] (100 million dollars) Japan China ROK ASEAN United States EU28 (right scale) Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Capital goods (Germany)] (100 million dollars) Japan China ROK ASEAN United States EU28 (right scale) Source: RIETI-TID 2013 database. (Year) 134

45 (100 million dollars) [Consumer goods (Germany)] (100 million dollars) Japan China ROK ASEAN United States EU28 (right scale) Source: RIETI-TID 2013 database. (Year) As for China, the value of final goods (capital goods and consumer goods) exports has been growing rapidly. Even though the value of exports declined in 2009 due to the impact of the Collapse of Lehman Brothers, it later grew rapidly (Figure II ). By export destination, the value of Chinese exports to ASEAN grew by a factor of (from 0.17 billion dollars to billion dollars) between 1990 and 2013 and the value of exports to Japan expanded by a factor of (from 0.12 billion dollars to billion dollars) over the same period. Chinese exports of capital goods (final goods) to Japan increased by a factor of (from 0.27 billion dollars to billion dollars) between 1990 and 2013, while exports to ASEAN grew by a factor of (from 0.41 billion dollars to billion dollars) over the same period (Figure II ). 135

46 Figure II (100 million dollars) Raw materials Processed products (intermediate goods) Parts (intermediate goods) Capital goods (final goods) Consumer goods (final goods) Changes in values of China's trade goods exports by production process China s main export destination countries (export values in 2014) 1. U.S. (39,606.3 billion dollars) 2. Hong Kong (36,322.3 billion dollars) 3. Japan (14,945.2 billion dollars) 4. ROK (10,040.2 billion dollars) 5. Germany (7,273.1 billion dollars) Source: RIETI-TID 2013 database, Global Trade Atlas. (Year) Figure II Changes in values of China's trade goods exports by production process and by export destination [Raw materials (China)] (100 million dollars) Japan ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) 136

47 (100 million dollars) [Processed products (China)] Japan ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Parts (China)] Japan ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) 137

48 (100 million dollars) [Capital goods (China)] Japan ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Consumer goods (China)] Japan ROK ASEAN United States EU28 Source: RIETI-TID 2013 database. (Year) In the case of ASEAN, the values of exports of processed goods (intermediate goods) and parts (intermediate goods) in particular have increased (Figure II ). 138

49 By export destination, ASEAN s exports of processed goods (intermediate goods) and parts (intermediate goods) have been growing. Exports of processed goods to China increased by a factor of 32.8 (from 1.76 billion dollars to billion dollars) between 1990 and 2013, while exports of parts expanded by a factor of (from 0.22 billion dollars to billion dollars) over the same period. Exports of raw materials to Japan have also been increasing, with the annual value of exports staying above 10 billion dollars since the latter half of the 2000s (Figure II ). Figure II Changes in values of ASEAN trade goods exports by production process (100 million dollars) Raw materials Processed products (intermediate goods) Parts (intermediate goods) Capital goods (final goods) Consumer goods (final goods) Source: RIETI-TID 2013 database. (Year) 139

50 Figure II (100 million dollars) Changes in values of ASEAN trade goods exports by production process and by export destination [Raw materials (ASEAN)] Japan China ROK United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Processed products (ASEAN)] Japan China ROK United States EU28 Source: RIETI-TID 2013 database. (Year) 140

51 (100 million dollars) [Parts (ASEAN)] Japan China ROK United States EU28 Source: RIETI-TID 2013 database. (Year) (100 million dollars) [Capital goods (ASEAN)] Japan China ROK United States EU28 Source: RIETI-TID 2013 database. (Year) 141

52 (100 million dollars) [Consumer goods (ASEAN)] Japan China ROK United States EU28 Source: RIETI-TID 2013 database. (Year) (d) Summary of the trend in world trade and exports by type of goods Amid the stagnant growth in exports by developed countries, emerging countries have led the growth in world trade (export value). In particular, the value of exports by China has grown remarkably. The value of exports by Japan, which is low compared with other countries export values, has been declining after peaking in When we look at world trade (export value) by production process and by type of traded goods, we see that the values of exports of all of final goods, intermediate goods and raw materials have been growing. Whereas the share of intermediate goods in world trade has remained flat since the 1990s, the share of final goods has been on a downtrend since the 2000s. As for changes in major exporting countries exports of traded goods classified by production process, the values of exports of final goods and intermediate foods by China, the United States and Germany have been growing. In the case of Japan, the value of intermediate goods exports is higher than the value of consumer goods exports, indicating that the country mainly supplies intermediate goods with relatively high added value to China and other assembly locations. A breakdown of Japanese exports of traded goods classified by production process indicates that Japan s weakness in exports of final goods compared with other countries is a factor behind the stagnant growth in the value of Japanese exports. While Japan mainly exports intermediate goods, rather than final goods, the United States and Germany have been increasing exports of both intermediate goods and final goods. In the case of Japan in particular, exports of final goods to EU28 have been on a downtrend, an indication that Japanese exports of consumer goods (final goods) have not grown compared with U.S. exports. 142

53 Below, we will evaluate Japan s competitiveness in export by comparing the export growth rates for major Japanese industries and examining individual Japanese product items import value shares in countries and regions in order to make clear in which products Japan has an export advantage. (2) Evaluation of Japan s competitiveness in export (A) Japan s main export destinations Japan s main export destinations are the United States and China. Although the United States was previously the largest export destination for Japan, the values of Japanese exports to the United States and China have been almost the same since As the value of Japanese exports to ASEAN10 has been increasing slightly, ASEAN 10 is also an important trading partner as the third major export destination after the United States and China. Japanese exports to EU28 declined after the Collapse of Lehman Brothers, and the value of exports to the region has remained flat without recovering to the level before the collapse of Lehman Brothers (Figure II ). Figure II Japan's main export destination countries (top 6 countries) (Trillion yen) ASEAN10 EU28 United States China ROK Taiwan Source: Global Trade Atlas. (Year) (B) Changes in the values of exports by major Japanese industries Next, we will look at changes in the values of Japanese exports by major industries as classified under Trade Statistics (HS Code). Exports by the motor vehicle, machinery and electrical machinery industries, which are the main drivers of Japanese exports, have been growing steadily. In addition, exports by the chemicals and plastic materials industry have also been increasing gradually, 143

Vehicles (87) Transportation equipment (86, 88, 89) Electrical machinery (85) General machinery (84) Non-ferrous metal (74-81) Base metal products (82) Articles of iron or")

5.8 Vehicles (87) 20.6 Electrical machinery (85) 15.1 Other 12.5 Chemicals and plastics (28-40) 13.3 General machinery (84) 19.2 Textiles and clothing (53-63) 1.")

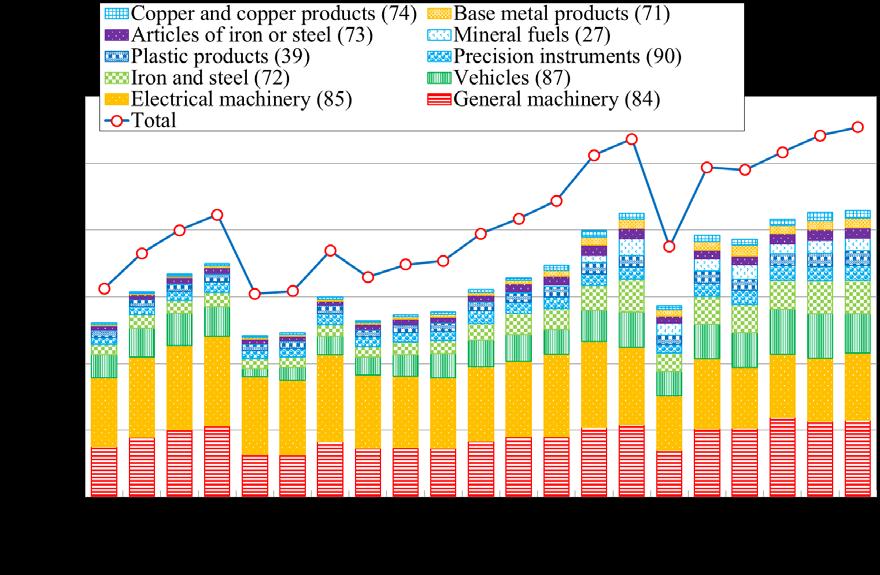

54 accounting for 15 of the overall export value recently (Figure II Figure II (Trillion yen) Changes in Japan's export values by major industry and shares of major industries in 2014 Precision instruments (90) Vehicles (87) Transportation equipment (86, 88, 89) Electrical machinery (85) General machinery (84) Non-ferrous metal (74-81) Base metal products (82) Articles of iron or steel (73) Iron and steel (72) Glass (70) Textiles and clothing (53-63) Chemicals and plastics (28-40) Source: Global Trade Atlas. Transportation equipment (86, 88, 89) 2.8 Precision instruments (90) 5.8 Vehicles (87) 20.6 Electrical machinery (85) 15.1 Other 12.5 Chemicals and plastics (28-40) 13.3 General machinery (84) 19.2 Textiles and clothing (53-63) 1.1 Glass (70) 0.5 (Year) Iron and steel (72) 4.8 Articles of iron or steel (73) 1.9 Non-ferrous metal (74-81) 1.9 Base metal products (82) 0.6 Source: Global Trade Atlas. 22 The figures in parentheses after category names refer to their HS codes. Unless otherwise specified, the figures after category and product names refer to their HS codes hereinafter in this paragraph. 144

55 (C) Japan s major export items in the main export destinations According to the list of Japan s major export items in the main export destinations (the top 10 export items in each of the export destinations) (Figure II ), machinery, electrical machinery, motor vehicles and iron and steel products are among the top export items in Asia, including China, Taiwan, the Republic of Korea and ASEAN. In the United States, which is Japan s largest export market, machinery, electrical machinery, precision instruments as well as transport machinery such as motor vehicles and aircraft are among the top export items. In EU28, similar items, including machinery, electrical machinery, motor vehicles and precision instruments are among the top export items. 145

56 Figure II Japan s major export items in main export destination countries and regions [China] [Taiwan] 146

![[ROK]](/docs-images/78/77489604/images/57-0.jpg "[ASEAN]")

57 [ROK] [ASEAN] 147

![[EU28]](/docs-images/78/77489604/images/58-1.jpg "148")

58 [United States] [EU28] 148